Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

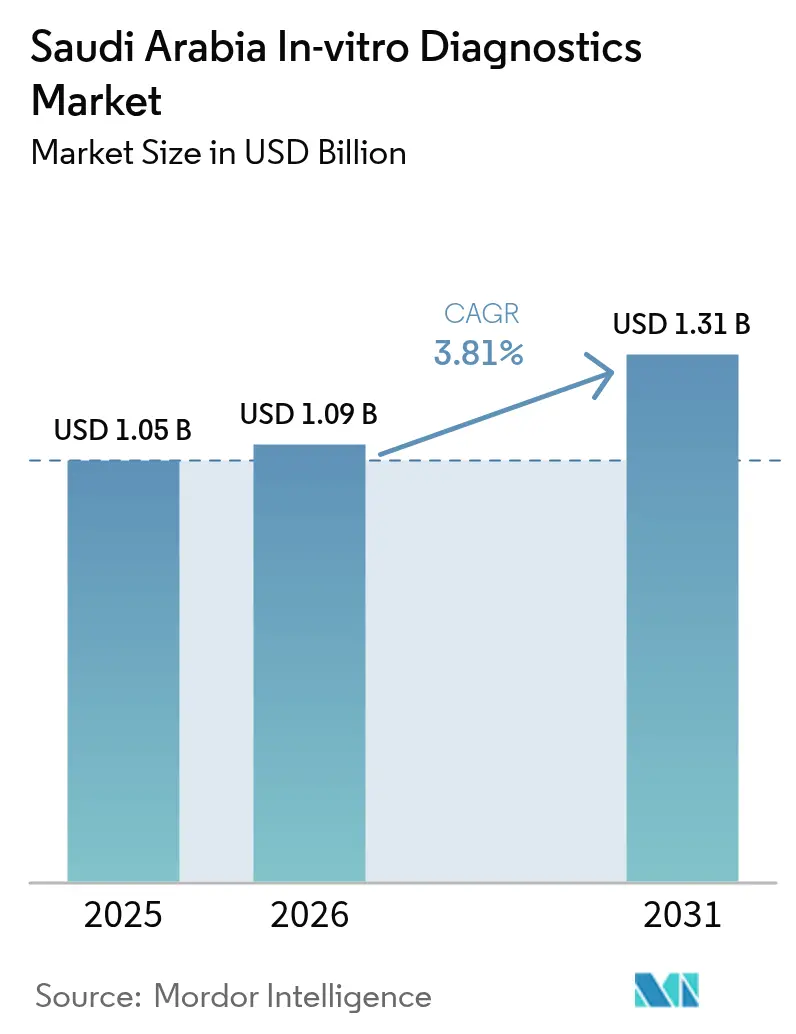

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia In-vitro Diagnostics Market Analysis by Mordor Intelligence

The Saudi Arabia In-vitro Diagnostics Market size is expected to grow from USD 1.05 billion in 2025 to USD 1.09 billion in 2026 and is forecast to reach USD 1.31 billion by 2031 at 3.81% CAGR over 2026-2031.

Clinical chemistry remains the volume backbone, yet molecular diagnostics is rising fastest, fed by Vision 2030 oncology initiatives and the Saudi Genome Program. Budget allocations of SAR 214 billion (USD 57.1 billion) in 2024 and a projected SAR 260 billion (USD 69.3 billion) in 2026 are underwriting lab-automation upgrades, enabling the private sector to capture emerging precision-medicine demand. Reagents and kits still command two-thirds of consumables revenue, but instruments tied to digital pathology and total lab automation are entering a capital-investment cycle. Meanwhile, mandatory newborn, premarital, and cancer screening mandates are driving test volume growth beyond historical infectious-disease baselines. Competitive dynamics increasingly hinge on localized genomic data centers and end-to-end multiomic testing as Lifera Omics, QIAGEN, and BD relocate regional command centers to Riyadh, shrinking decision-to-deployment timelines and embedding Saudi Arabia in global diagnostics value chains.

Key Report Takeaways

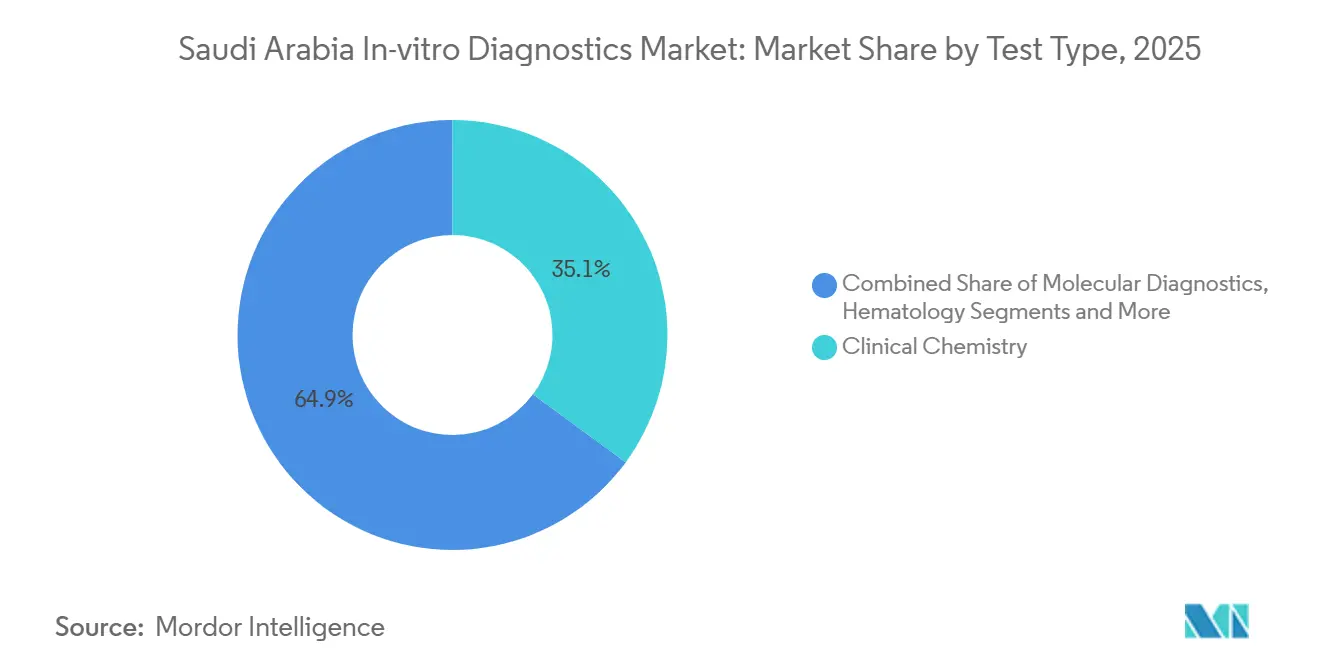

- By test type, clinical chemistry led with 35.1% of the Saudi Arabia in-vitro diagnostics market share in 2025, while molecular diagnostics recorded the highest projected 5.33% CAGR through 2031.

- By product, reagents and kits accounted for 68.12% of the Saudi Arabia in-vitro diagnostics market size in 2025; instruments are poised to expand at a 5.66% CAGR between 2026-2031.

- By usability, disposable IVD devices accounted for 71.32% of the Saudi Arabia in-vitro diagnostics market size in 2025; Re-usable IVD devices are poised to expand at a 5.87% CAGR between 2026-2031.

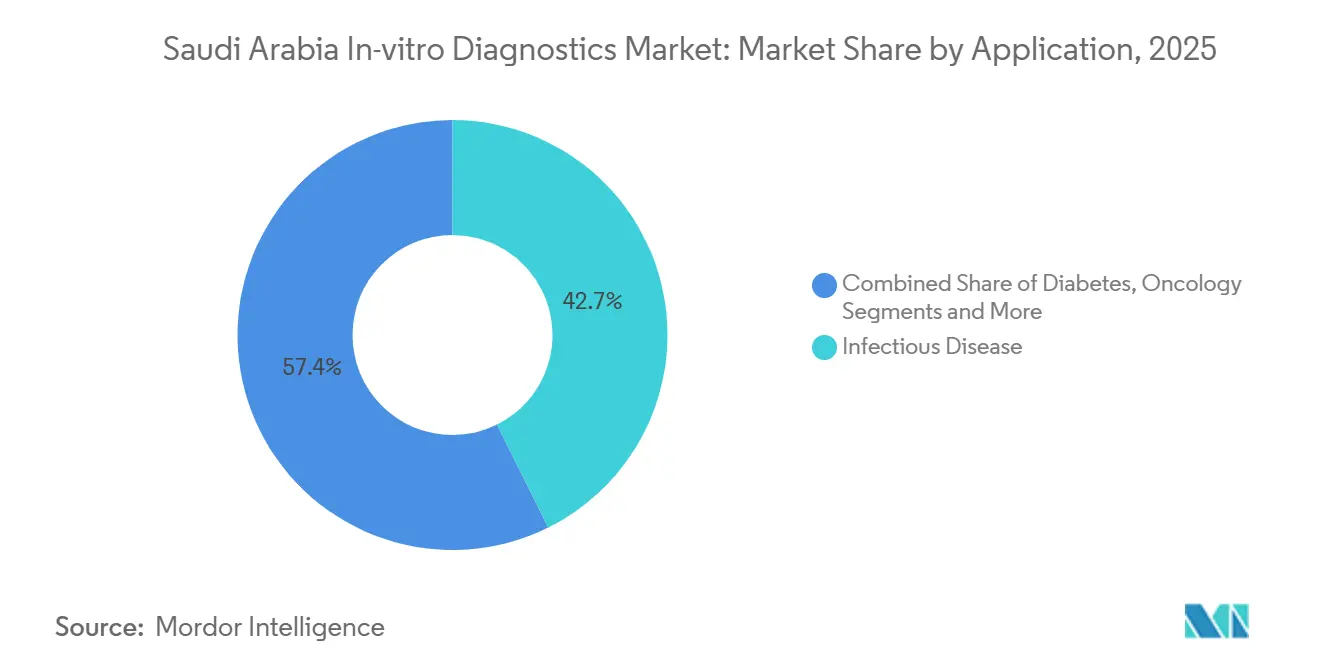

- By application, infectious disease retained a 42.65% revenue share in 2025, yet oncology testing is advancing at a 6.12% CAGR to 2031.

- By end user, diagnostic laboratories captured 47.87% revenue in 2025, whereas home-care and point-of-care settings are set to grow at a 6.54% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia In-vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Chronic Disease Prevalence | +1.2% | National, concentrated in urban centers (Riyadh, Jeddah, Dammam) | Medium term (2-4 years) |

| Growing Government Healthcare Expenditure and Vision 2030 Investments | +1.5% | National, with flagship projects in NEOM, Riyadh health clusters | Long term (≥ 4 years) |

| Rapid Expansion of Private Healthcare Infrastructure | +0.9% | National, led by Riyadh, Jeddah, and Eastern Province | Short term (≤ 2 years) |

| Rising Demand for Personalized and Genomic Diagnostics | +0.7% | National, anchored in tertiary hospitals and research centers | Medium term (2-4 years) |

| Proliferation of Digital Health and IoMT Platforms | +0.6% | National, accelerated by NPHIES integration | Short term (≤ 2 years) |

| Increasing Awareness Through Mandatory Screening Programs | +0.5% | National, emphasis on premarital, newborn, and cancer screening | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Chronic Disease Prevalence

Saudi Arabia’s diabetic population is projected to grow from 2.69 million in 2020 to 4.21 million by 2030, boosting demand for HbA1c, lipid, and tumor marker panels. King Faisal Specialist Hospital’s AI-driven hematology lab launched in 2024 processes 9,000 flow tests annually, illustrating nationwide upgrades that support precision hematology[1]King Faisal Specialist Hospital & Research Centre, “Advanced Hematology Diagnostics Lab Launch,” kfshrc.edu.sa. The Ayenati network now links 1,194 reference labs and has logged 5.3 million samples, creating a national data backbone for population screening. ISO 15189 accreditation is becoming a gatekeeper for public tenders, concentrating volumes within labs that maintain rigorous quality systems.

Growing Government Healthcare Expenditure and Vision 2030 Investments

Health-sector budgets rose to SAR 214 billion (USD 57.1 billion) in 2024 and are slated for SAR 260 billion (USD 69.3 billion) by 2026, funneling funds into lab modernization, digital pathology, and telemedicine nodes. Privatization plans covering 290 public hospitals will fragment procurement and widen access for specialty-test vendors. Lifera Omics, a November 2023 joint venture with CENTOGENE, positions the Kingdom to localize multiomic testing, reducing outbound sample flows. NPHIES now covers 31 million insured residents, mandating real-time claims adjudication that rewards digitized labs.

Rapid Expansion of Private Healthcare Infrastructure

Al Borg Diagnostics serves 15,000 daily customers and opened two of the region’s largest reference labs in 2023, driving economies of scale in molecular testing. BD and QIAGEN secured regional headquarters licenses in Riyadh during 2023-2024, enabling co-developed clinical guidelines and shortening technology rollouts. Private operators’ flexible capital structures accelerate adoption of total lab automation, positioning them to meet precision-medicine demand ahead of public counterparts.

Rising Demand for Personalized and Genomic Diagnostics

The Saudi Genome Program has sequenced more than 10,000 genomes, shifting focus from research to routine clinical decision-making. Lifera Omics’ Riyadh facility integrates phenomics, genomics, and proteomics, slashing oncology-panel turnaround from weeks to days. QIAGEN’s localized data center provides on-shore bioinformatics, addressing data-sovereignty concerns and ensuring faster variant interpretation. AI-enabled multiparametric flow cytometry at King Faisal Specialist Hospital underscores the market’s pivot toward precision hematology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Reimbursement for Advanced Molecular Assays | -0.8% | National, more acute in public sector and smaller private insurers | Medium term (2-4 years) |

| Stringent Regulatory Approval Processes | -0.6% | National, affecting all device and reagent imports | Short term (≤ 2 years) |

| Shortage of Skilled Laboratory Professionals | -0.5% | National, concentrated in secondary cities and rural areas | Long term (≥ 4 years) |

| Supply Chain Vulnerabilities and Cold-Chain Constraints | -0.4% | National, most severe outside Riyadh and Jeddah | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Advanced Molecular Assays

The Council of Cooperative Health Insurance reimburses insulin pumps under strict criteria but has not published guidelines for next-generation sequencing or liquid-biopsy assays, leaving most advanced molecular tests self-pay[2]Saudi National Diabetes Center, “Reimbursement Guidelines and Device Safety Alerts,” sndc.sa. Fragmented private-payer policies force suppliers into piecemeal negotiations, inflating administrative costs and slowing adoption. Penetration of insulin pumps among type 1 diabetics remains below 3%, underscoring how eligibility rules can suppress device uptake even when clinical value is clear. Absent a national medical-device formulary, coverage decisions vary widely, perpetuating regional inequities in access to precision diagnostics.

Stringent Regulatory Approval Processes

The Saudi Food and Drug Authority’s four-tier IVD risk classification demands pre-market scientific evaluation and post-market surveillance, driving approval timelines for Class C and D devices past 12 months[3]Saudi Food and Drug Authority, “IVD Device Classification Framework,” sfda.gov.sa. Local bridging studies add complexity for rare-disease panels with limited Saudi cohorts. NUPCO tenders layer additional technical and delivery requirements, favoring incumbents with proven local supply chains. While vigilance safeguards patient safety—the National Center for Medical Device Reporting issued 253 safety alerts between 2021-2024—lengthy approvals can let competitors leapfrog first movers with newer technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Gains on Clinical Chemistry’s Volume Base

Clinical chemistry commanded 35.1% revenue in 2025 on the strength of high-volume liver-function and lipid panels. Despite this, the Saudi Arabia in-vitro diagnostics market size for molecular assays is projected to expand at a 5.33% CAGR through 2031, the fastest among test types. Uptake is fueled by syndromic infectious-disease panels and oncology profilers required for targeted therapies. King Faisal’s automated flow cytometry track exemplifies a nationwide pivot toward AI-assisted hematology that reduces manual microscopy and enriches immunophenotyping depth. Immuno-diagnostics remains essential but faces margin compression under NUPCO’s bulk-purchase pricing caps. Hematology platforms now bundle digital image analysis, optimizing throughput amid staffing shortages.

Workflow efficiency differentiates suppliers. Beckman Coulter’s DxC 700 AU analyzer cut processing steps by 30%, aligning with labs’ need to handle rising sample loads without headcount growth. National interoperability mandates through the Ayenati network further accelerate retirement of legacy instruments lacking digital connectivity. Overall, molecular diagnostics’ high growth rate will rebalance the Saudi Arabia in-vitro diagnostics market toward precision tests while preserving clinical chemistry’s foundational role.

By Product: Reagents & Kits Dominate, Instruments Enter an Upgrade Cycle

Reagents and kits held 68.12% revenue in 2025, reflecting consumable annuity economics that lock customers into proprietary chemistries over instrument lifespans. Yet instruments are expected to record a 5.66% CAGR by 2031 as labs modernize under Vision 2030. Al Borg’s twin reference labs required next-generation sequencers, high-throughput chemistry tracks, and digital pathology scanners, all of which create durable reagent pull-through. The Saudi Arabia in-vitro diagnostics market share for high-value specialty reagents—flow cytometry cocktails, liquid-biopsy kits—will outpace commoditized routine chemistries, buffering suppliers against pricing pressure.

Suppliers now bundle predictive maintenance and remote diagnostics; Beckman Coulter’s “3 & 60” concept allows part changes in three steps within 60 seconds, minimizing downtime where field engineers are scarce. Privatization of 290 hospitals will transfer procurement authority from centralized NUPCO tenders to emerging group-purchasing organizations, favoring vendors offering flexible financing and localized service.

By Usability: Disposable Devices Prevail, Re-Usables Ride Automation

Disposable devices captured 71.32% of 2025 revenue as infection-control protocols and single-use cartridges became entrenched during COVID-19. Conversely, reusable analyzers, tracks, and sequencing platforms are projected to grow at 5.87% through 2031 as hospitals chase economies of scale. King Faisal’s automated hematology track shows how high-throughput reusable systems can absorb rising volumes without proportional staffing. Home-care adoption of connected CGMs and insulin pumps like Omnipod 5 underscores a parallel surge in disposables that feed longitudinal data into care pathways while shifting HbA1c testing out of labs.

Compliance oversight is intense: the Saudi Food and Drug Authority had cleared 12 CGMs by September 2024 and investigated 427 home-use device incidents since 2021, issuing 253 safety alerts. Reusable platforms increasingly integrate data analytics; BD’s safety memorandum with 500 hospitals embeds software that feeds specimen-tracking metrics into hospital systems. This dual-track evolution will persist, with disposables dominating primary care and reusables anchoring high-volume centers.

By Application: Infectious Disease Still Leads, Oncology Rises Fastest

Infectious disease testing held a 42.65% revenue share in 2025, underpinned by residual COVID-19 capacity and endemic TB, hepatitis, and meningitis. QIAGEN’s QIAstat-Dx platform for national meningitis elimination and QuantiFERON-TB Gold Plus for latent TB screening embeds molecular tests into public-health protocols. The Saudi Arabia in-vitro diagnostics market size for oncology panels, however, is forecast to grow at 6.12% CAGR, the fastest among applications, propelled by rising cancer incidence and localized multiomic testing at Lifera Omics. Diabetes testing retains high volumes although CGMs dampen lab HbA1c demand.

Cardiology assays for troponins and BNP are migrating to emergency-department point-of-care instruments, shortening decision cycles for acute-coronary-syndrome management. King Faisal’s AI-enabled hematology services illustrate growing demand for minimal residual disease monitoring in hematologic malignancies. Government HPV molecular screening agreements further entrench oncology testing in national preventive frameworks.

By End User: Labs Dominate, Home & POC Settings Surge

Diagnostic laboratories captured 47.87% of 2025 revenue, benefiting from centralized procurement and reference-lab consolidation. However, home-care and point-of-care environments will expand at a 6.54% CAGR, outpacing all other segments. The Omnipod 5 automated insulin-delivery system, launched in 2026, exemplifies decentralized devices generating clinically actionable data outside traditional labs. Hospitals now embed point-of-care platforms for troponins and blood gases, diverting urgent tests away from central labs.

Ayenati’s network connectivity lets smaller facilities outsource esoteric assays while retaining patient relationships, raising the Saudi Arabia in-vitro diagnostics market’s digital maturity. NPHIES real-time adjudication incentivizes electronic ordering and result reporting, favoring organizations with robust IT interfaces. BD’s partnership with the Saudi Patient Safety Center extends specimen-management best practices across 500 hospitals, demonstrating how enterprise-wide initiatives can transform end-user requirements.

Competitive Landscape

Global majors—Roche, Abbott, Siemens Healthineers, and Danaher—anchor hospital tenders via NUPCO, together accounting for 58% of 2025 centralized-procurement revenue. Their installed instrument bases lock in reagent pull-through and create high switching costs. Regional champion Al Borg Diagnostics leverages 15,000 daily customer contacts to negotiate favorable reagent contracts and pursue franchise-style expansion across secondary cities.

Lifera Omics, backed by the Public Investment Fund, represents a sovereign play to capture high-margin precision-diagnostics revenue and localize data processing, challenging international reference labs’ traditional dominance. Technology integration is the key battleground: King Faisal’s AI-driven hematology lab showcases prospects for suppliers that can deliver middleware, remote diagnostics, and predictive analytics. BD’s and QIAGEN’s Riyadh headquarters exemplify the pivot toward local co-development of clinical pathways and data solutions, shortening regulatory cycles and aligning with data-sovereignty laws.

Upcoming hospital privatizations will dilute NUPCO’s centralized power, allowing niche vendors to penetrate through group-purchasing alliances and cloud-based instrument-as-a-service contracts. Suppliers capable of offering financing, local warehousing, and on-shore analytics will win share as procurement authority fragments.

Saudi Arabia In-vitro Diagnostics Industry Leaders

Abbott Laboratories

Siemens Healthineers

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific

Danaher (Cepheid & Beckman Coulter)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Insulet launched Omnipod 5 automated insulin delivery and Omnipod Discover data-management platform across Saudi Arabia and neighbors, integrating with Abbott Libre 2 Plus and Dexcom G7 CGMs.

- December 2024: King Faisal Specialist Hospital inaugurated the region’s largest automated hematology laboratory with AI image analysis and multiparametric flow cytometry.

Saudi Arabia In-vitro Diagnostics Market Report Scope

As per the scope of this report, in-vitro diagnostics refers to medical tests and procedures that analyze samples of tissues, blood, urine, and other bodily fluids to diagnose diseases, infections, or other medical conditions. These tests are performed outside the body in a laboratory setting, with the sample taken from the patient being analyzed in a controlled environment.

The Saudi Arabia In-vitro Diagnostics Market is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Immuno Diagnostics, Haematology, and Other Types), Product (Instrument, Reagent, Other Product), Usability ( Disposable IVD Device and Reusable IVD Device), Application (Infectious Disease, Diabetes, Cancer/Oncology, Cardiology, and Other Applications), and End-User (Diagnostic Laboratories, Hospitals and Clinics, and Other End-users). The report offers the value (in USD) for the above segments.

By Test Type

| Clinical Chemistry |

| Molecular Diagnostics |

| Immuno-Diagnostics |

| Hematology |

| Other Test Types |

By Product

| Instruments |

| Reagents & Kits |

By Usability

| Disposable IVD Devices |

| Re-Usable IVD Devices |

By Application

| Infectious Disease |

| Diabetes |

| Oncology |

| Cardiology |

| Other Applications |

By End-User

| Diagnostic Laboratories |

| Hospitals & Clinics |

| Home-Care & POC Settings |

| Other End-Users |

| By Test Type | Clinical Chemistry |

| Molecular Diagnostics | |

| Immuno-Diagnostics | |

| Hematology | |

| Other Test Types | |

| By Product | Instruments |

| Reagents & Kits | |

| By Usability | Disposable IVD Devices |

| Re-Usable IVD Devices | |

| By Application | Infectious Disease |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Other Applications | |

| By End-User | Diagnostic Laboratories |

| Hospitals & Clinics | |

| Home-Care & POC Settings | |

| Other End-Users |

Key Questions Answered in the Report

How fast is the Saudi Arabia in-vitro diagnostics market expected to grow through 2031?

It is projected to reach USD 1.31 billion by 2031, registering a 3.81% CAGR from 2026-2031.

Which test type is expanding most rapidly across Saudi laboratories?

Molecular diagnostics leads with a forecast 5.33% CAGR, fueled by oncology panels and syndromic infectious-disease assays.

What share of 2025 revenue did reagents and kits represent?

Reagents and kits accounted for 68.12% of industry revenue, reflecting strong consumables pull-through.

Which application segment shows the highest future growth?

Oncology testing is advancing at a 6.12% CAGR as precision oncology programs scale nationally.

How are home-care settings influencing demand?

Home-care and point-of-care environments are the fastest-growing end-user category at 6.54% CAGR, driven by connected CGMs and automated insulin delivery systems like Omnipod 5.

What keeps adoption of advanced molecular assays below potential?

A lack of unified reimbursement guidelines leaves many genomic and liquid-biopsy tests under self-pay models, restraining broader uptake.

Page last updated on: