Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

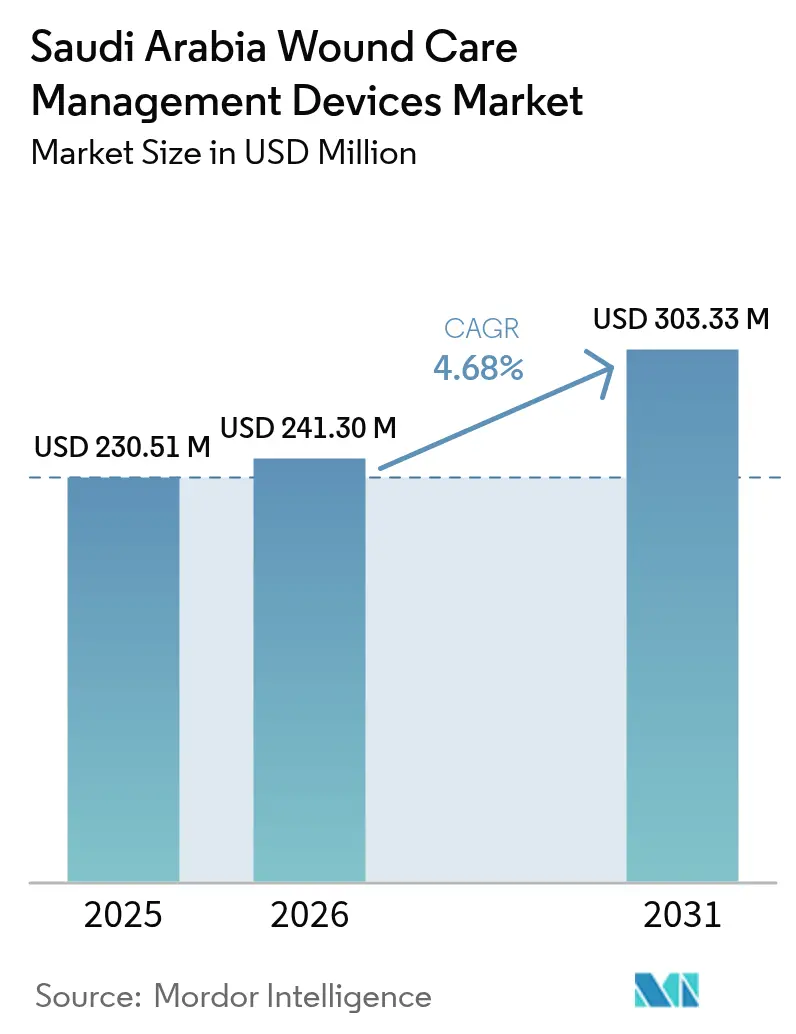

| Base Year Market Size (2025) | USD 230.51 Million |

| Market Size (2026) | USD 241.3 Million |

| Market Size (2031) | USD 303.33 Million |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Wound Care Management Devices Market Analysis by Mordor Intelligence

The Saudi Arabia wound care management devices market size was valued at USD 230.51 million in 2025 and estimated to grow from USD 241.3 million in 2026 to reach USD 303.33 million by 2031, at a CAGR of 4.68% during the forecast period (2026-2031). Sustained funding under Vision 2030, demographic aging, and high diabetes prevalence are moving the market from basic dressings to sophisticated negative-pressure and smart monitoring systems [1]Vision 2030 Authority, “Healthcare Transformation Program,” vision2030.gov.sa . Hospitals remain the principal buyers, yet home-health and retail channels are enlarging as insurance coverage broadens and telehealth platforms mature. Domestic manufacturing incentives under the “Made in Saudi” program are shortening supply chains and tempering import costs. Competitive intensity is rising because multinational device makers are pairing with Saudi distributors to meet localization quotas while defending technology leadership.

Key Report Takeaways

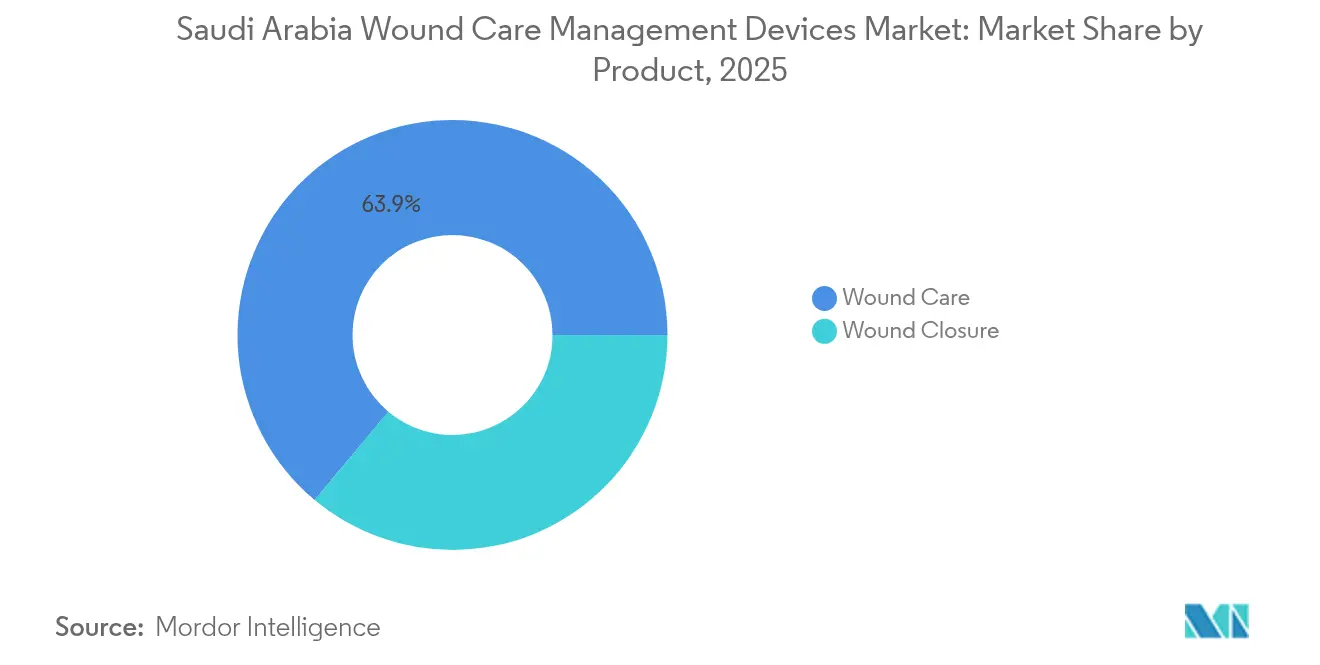

- By product category, Wound Care products led with 63.92% of the Saudi Arabia wound care management devices market share in 2025, whereas the Wound Closure segment is set to grow fastest at 5.41% CAGR to 2031.

- By wound type, Chronic Wounds accounted for 60.55% share of the Saudi Arabia wound care management devices market size in 2025, while Acute Wounds are advancing at a 5.54% CAGR through 2031.

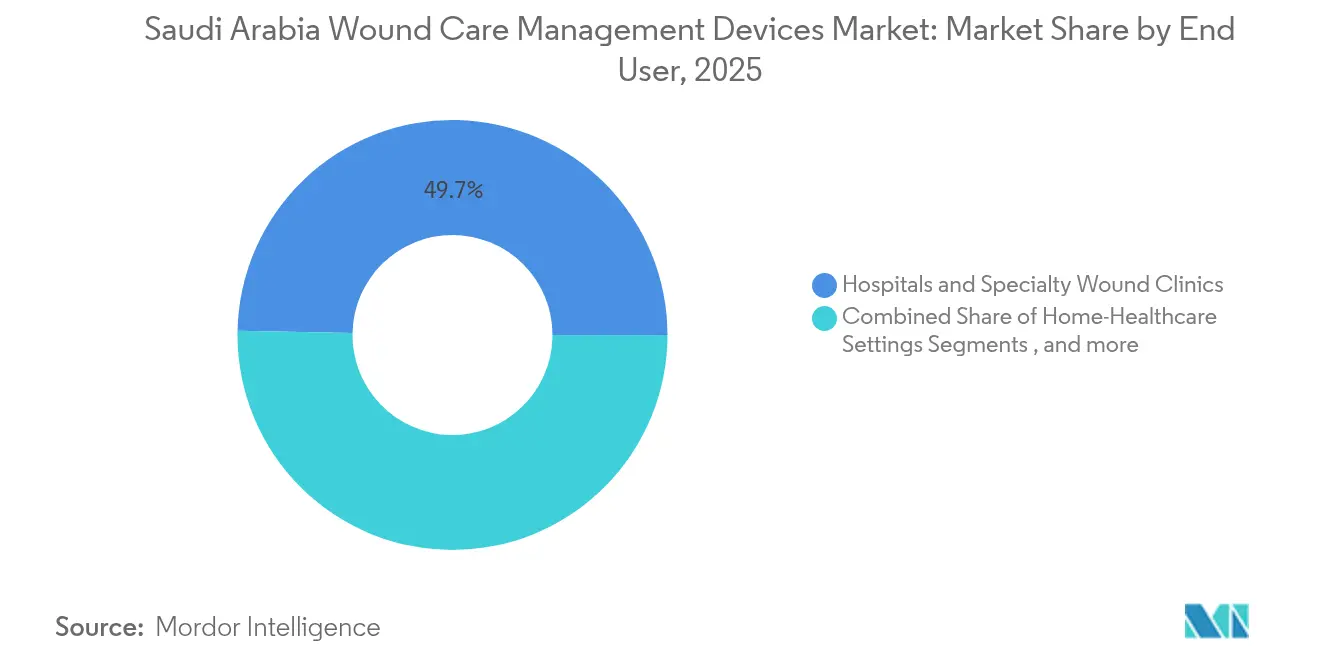

- By end user, Hospitals and Specialty Wound Clinics held 49.68% of the Saudi Arabia wound care management devices market size in 2025; Home-Healthcare Settings record the highest projected CAGR at 5.58% to 2031.

- By mode of purchase, Institutional Procurement captured 63.88% share of the Saudi Arabia wound care management devices market size in 2025, while the Retail/OTC channel is forecast to expand at 5.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes & diabetic-foot ulcers | +1.2% | National, urban centers | Long term (≥ 4 years) |

| Surge in surgical procedures under Vision 2030 hospitals program | +0.9% | National, Riyadh / Jeddah / Dammam | Medium term (2-4 years) |

| Growing geriatric population with chronic wounds | +0.8% | National, Northern and Eastern regions | Long term (≥ 4 years) |

| Government capex on local medical-device manufacturing | +0.6% | National, industrial cities | Medium term (2-4 years) |

| Mandatory NPWT adoption in new MOH protocols | +0.5% | National, hospital-centric | Short term (≤ 2 years) |

| Expansion of home-health and tele-wound monitoring | +0.4% | National, rural emphasis | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Diabetic-Foot Ulcers

Diabetes affects 17.7% of Saudi adults and drives a steady inflow of chronic wound cases that require advanced care. Diabetic foot ulcers alone cost SAR 6,684.9 (USD 1,782.6) per patient each year at tertiary hospitals, a figure that motivates payers to adopt preventive dressings and NPWT. Only 35% of patients possess adequate foot-care knowledge, so education campaigns are expanding device uptake [2]Mona Eihab Aljaouni, "Knowledge and Practice of Foot Care among Patients with Diabetes Attending Diabetes Center, Saudi Arabia," MDPI, mdpi.com. Urban demand clusters in Riyadh and Jeddah steer distributors toward city-center wound clinics, while new smart dressings achieving 99.75% closure by day 14 signal rapid technology migration into standard protocols [3]Ahmad F. Turki, "A Bioelectrically Enabled Smart Bandage for Accelerated Wound Healing and Predictive Monitoring," MDPI, mdpi.com.

Surge in Surgical Procedures Under Vision 2030 Hospitals Program

Government plans call for 26,000–43,000 new beds by 2030, and rising operating-room volumes are elevating demand for closure products that shorten healing times. Annual health spending reached SAR 214 billion (USD 57.04 billion) in 2023, and procurement teams now rate infection-control metrics when awarding contracts. Negative-pressure therapy cuts surgical site infections by 77% compared with standard dressings, so adoption accelerates in flagship hospitals. AI-assisted planning at King Faisal Specialist Hospital reinforces the shift toward sensor-enabled dressings that integrate with digital records.

Growing Geriatric Population with Chronic Wounds

Adults ≥ 65 years will form 18.4% of citizens by 2050, and 52% already live with multimorbidity that complicates healing. Polypharmacy rates of 55% extend wound-healing timelines and justify premium antimicrobial dressings. Home-health visits rose to 6,548 between 2017 and 2020, proving capacity for community-based care. Closed-incision NPWT shows superior results among elderly reconstructive patients, prompting nursing homes to standardize the modality. Emerging demand in Northern and Eastern provinces is reshaping distributor footprints.

Government Capex on Local Medical-Device Manufacturing

The “Made in Saudi” program links tax breaks to local production targets, so partnerships such as Nahdi Medical with the Saudi Exports Development Authority are accelerating domestic output. NUPCO tenders increasingly favor Saudi plants that hold SFDA licenses, and fresh capacity for gauze, hydrocolloids, and NPWT consumables is reducing lead times. Local fabrication attracts technology transfer from global OEMs, shrinking import dependence and moderating currency risk in hospital budgets. Industrial city clusters also align with Vision 2030 jobs targets, bolstering political support for continued capex.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced dressings & devices | -0.7% | National, rural burden | Medium term (2-4 years) |

| Reimbursement gaps for outpatient NPWT | -0.5% | National, private sector | Short term (≤ 2 years) |

| Cold-chain limits for bioactive dressings | -0.3% | Rural Northern / Southern provinces | Medium term (2-4 years) |

| Low adoption of bio-resorbable closures | -0.2% | National, conservative centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Dressings & Devices

Premium systems carry steep upfront prices, and rural hospitals restrict purchases to essential stock. Vision 2030 insurance reforms promise wider coverage, yet immediate budgets remain tight. Clinical studies prove NPWT lowers total costs by EUR 4,155.98 per closed wound, but procurement still focuses on sticker price. Engineers have produced low-cost NPWT using wall suction at USD 4 per change, signaling a value tier for budget-constrained sites.

Reimbursement Gaps for Outpatient NPWT and Dressings

Home-based negative-pressure kits require new billing codes that private insurers have yet to standardize. Primary-care spending remains a small share of health budgets, so out-of-hospital therapies struggle for payment. Single-use NPWT devices show outcome parity at lower total cost, bolstering the case for inclusion in basic benefit packages. Unified electronic records now rolling out will later enable automated claims, but interim uncertainty slows device turnover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Drives Innovation

Wound Care products held 63.92% of the Saudi Arabia wound care management devices market in 2025, underscoring their position as the default solution set for both chronic and acute wounds. Volume growth is tied to the high diabetes load and nationwide directives that prioritize pressure-ulcer prevention in long-stay wards. Advanced hydrofiber, silver-impregnated, and bioelectric dressings are expanding fastest because clinical teams link them to shorter bed stays and infection avoidance. Mandatory NPWT adoption in MOH hospitals further amplifies consumable demand, while real-time telemetry modules that upload exudate data are being trialed in tertiary centers.

The Wound Closure category, though smaller, is tracking a 5.41% CAGR as surgical throughput rises under Vision 2030. Surgeons favor traditional sutures for cost reasons, yet tissue adhesives and bio-resorbable staples are gaining credibility in teaching hospitals that publish outcome data. Suppliers co-locate field trainers to improve technique adoption and to counter conservative practice norms. Topical antimicrobials reinforce both categories because infection control remains a central KPI in public procurement scoring.

By Wound Type: Chronic Conditions Shape Market Dynamics

Chronic Wounds commanded 60.55% share of the Saudi Arabia wound care management devices market size in 2025, reflecting diabetic foot ulcers, venous ulcers, and pressure injuries concentrated in urban settings. Extended healing cycles prompt payers to reimburse advanced dressings that reduce readmissions, and specialty foot clinics in Riyadh now serve as referral hubs for complex cases. Machine-learning triage tools classify ulcer severity and recommend product bundles, which streamlines inventory planning.

Acute Wounds are expanding at a 5.54% CAGR through 2031, propelled by trauma center upgrades and elective surgery growth. The Saudi Arabia wound care management devices market size for surgical wounds is rising in line with bed additions, and burn units in Jeddah have adopted enzymatic debridement kits that shorten OR time. Military hospitals also act as early adopters of bio-resorbable closure technology for combat injuries, providing proof points that diffuse to civilian facilities.

By End User: Hospital Transformation Enables Home Care Growth

Hospitals and Specialty Wound Clinics controlled 49.68% of the Saudi Arabia wound care management devices market in 2025, thanks to centralized budgets and availability of skilled staff. AI scheduling cut wait times at King Faisal Specialist Hospital to 6 hours, which increases procedure throughput and device consumption. Clinics attached to tertiary hospitals act as pilot sites for smart bandages that integrate with electronic records.

Home-Healthcare Settings, advancing at a 5.58% CAGR, benefit from telemedicine and patient preferences for in-home recovery. Portable NPWT pumps with eight-day battery life allow remote treatment, and insurers now cover wound-photo uploads for diabetic members. Caregiver training modules in Arabic show strong engagement, raising compliance with dressing changes. Long-term care homes continue to adjust protocols to accommodate sensor-enabled pressure dressings that alert staff before tissue breakdown.

By Mode of Purchase: Institutional Dominance Faces Retail Disruption

Institutional Procurement retained 63.88% share of the Saudi Arabia wound care management devices market share in 2025, as NUPCO bulk bids anchor public demand. Framework contracts include volume tiers that trigger price rebates, encouraging hospitals to standardize brands. Localization clauses require a rising proportion of Saudi-made components, steering global suppliers toward joint-ventures.

The Retail/OTC channel, growing 5.72% annually, rides consumer interest in preventive care and e-commerce convenience. Pharmacies highlight diabetic foot kits alongside glucometers, and QR codes on packages link buyers to instructional videos. Domestic producers leverage lower shipping costs to offer competitive pricing on gauze and hydrocolloid ranges. Advanced devices remain mostly institutional because professional oversight and reimbursement codes have not yet migrated fully to retail.

Geography Analysis

The Central Region, led by Riyadh, houses the most tertiary hospitals and consumes the largest share of Saudi Arabia wound care management devices market products. Government agencies headquartered in the capital also oversee centralized purchasing, which channels early technology rollouts into nearby facilities. AI-enabled wound triage pilots show the highest penetration here and influence nationwide protocol updates.

The Western Region, with Jeddah and Makkah, benefits from influxes of medical tourists during Hajj seasons who often present with chronic conditions aggravated by travel. Hospitals have specialized multilingual wound teams that drive higher NPWT usage. Religious-tourism revenue underwrites ongoing capital upgrades that favor advanced dressings with rapid-healing evidence.

The Eastern Region’s industrial workforce raises workplace injury incidence, so trauma and burn care centers purchase large volumes of closure devices. Petroleum installations partner with local clinics to stock emergency wound kits, creating steady off-take for suppliers. The region also hosts several new device plants that shorten delivery times to all Gulf markets.

Northern and Southern provinces remain smaller in value yet record above-average growth because Vision 2030 telehealth investments allow clinicians to manage complex wounds remotely. Cold-chain limitations in these areas hinder bioactive dressing adoption, but domestic production of shelf-stable hydrofiber packs has begun to fill gaps. Mobile clinics equipped with tablet-sync NPWT pumps now tour remote villages, broadening market coverage.

Digital health investment of USD 1.5 billion in IT infrastructure underpins a national wound registry that standardizes treatment benchmarks across all regions and guides equitable product allocation. As demographic aging accelerates nationwide, each cluster aligns procurement with chronic-wound caseload projections, supporting sustained market expansion.

Regulatory Landscape

Wound care management devices and non-medicated dressings are regulated as medical devices in Saudi Arabia under the Saudi Food and Drug Authority (SFDA) medical devices framework, which governs the full product lifecycle from manufacturing and importation through distribution, storage, and post-market oversight. Products must be appropriately classified (per SFDA Products Classification Guidance, Version 7, February 2024) and obtain SFDA Medical Devices Marketing Authorization (MDMA) before being placed on the market. Where manufacturers do not have a local legal presence, they commonly operate through an SFDA-licensed Authorized Representative.

Market access also depends on establishment licensing and import or shipment clearance controls. Importers, distributors, marketers, and storage providers must hold SFDA establishment licenses (including branch licensing requirements, reinforced in SFDA licensing requirements updates such as MDS-REQ 9, Version 2, March 2025), and imported shipments are cleared through SFDA-linked processes using the SFDA Faseh Services System and the FASAH (Tabadul) platform at ports of entry. These requirements tend to shape go-to-market timelines and increase the documentation and quality management system readiness needed for advanced wound-care products, which raises the operational value of in-country distribution and localization setups aligned to Saudi medical devices law updates (MISA, Law of Medical Devices and Supplies, July 2025).

Competitive Landscape

The Saudi Arabia wound care management devices market contains a mix of global majors and increasingly capable local firms. Smith+Nephew, Mölnlycke, and ConvaTec maintain brand leadership through continuous R&D and SFDA compliance expertise. Their strategies revolve around local assembly agreements that satisfy localization quotas while ensuring quality consistency. Mölnlycke widened its Saudi joint-venture stake to 60% in March 2025, signaling long-term commitment to in-country production.

Domestic players such as Arabian International Healthcare Holding (TIBBIYAH) and Saudi Mais win sizable NUPCO tenders by coupling competitive pricing with fast delivery. These firms leverage proximity to industrial cities to minimize logistics costs and to respond quickly to emergency orders. Start-ups focusing on bioelectric smart bandages and low-cost NPWT variants fill technology gaps that multinationals overlook, and several hold patents filed with the Saudi Authority for Intellectual Property.

Acquisition activity centers on biologics and digital monitoring. Smith+Nephew’s USD 180 million CartiHeal purchase adds cartilage regeneration expertise that can migrate into chronic-wound scaffolds. ConvaTec’s Triad Life Sciences deal strengthens its advanced biomaterial lineup. Suppliers now bundle analytics dashboards that feed wound-image data into AI engines, providing clinical decision support and locking customers into ecosystem subscriptions.

Saudi Arabia Wound Care Management Devices Industry Leaders

-

Smith and Nephew

-

ConvaTec Inc.

-

Medtronic Plc

-

Coloplast

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localization and procurement modernization are creating clear whitespace beyond commodity dressings, particularly where suppliers can pair SFDA-compliant documentation with in-country manufacturing or assembly. The government focus on localizing medical devices manufacturing under Vision 2030, alongside the Health Sector Transformation Program push toward privatization, health clusters, and expanded e-health and telemedicine, supports opportunities for wound-care portfolios that show measurable outcomes and cost-of-care impact across hospital and home pathways. In February 2026, the Ministry of Industry and Mineral Resources highlighted advancing plans to localize production of higher-technology medical equipment, which signals room for wound-care device makers and component suppliers to extend local capability beyond basic consumables.

A second opportunity is in market-access acceleration and regional scaling for companies that fit SFDA lifecycle oversight and can leverage existing global technical files. SFDA requires marketing authorization for circulating devices and maintains structured establishment licensing and import clearance pathways, which can favor manufacturers that streamline authorized representative models, labeling/UDI readiness, and post-market processes from the start. With institutional procurement still anchored by centralized buying and localization clauses in tenders, suppliers that combine Saudi-based supply reliability with evidence packages for advanced wound therapies (including NPWT and advanced dressings used in protocol-driven hospital settings) have a practical route to broader adoption. Telehealth-enabled home wound management also expands the addressable base for portable systems and consumables as reimbursement and service models are built out.

Recent Industry Developments

- July 2026: Professional Medical Expertise Company (ProMedEx) signed a joint venture agreement with Beijing Synapsor Artificial Intelligence Company Limited to establish BMX Sci Arabia and back a SAR 35 million medical manufacturing plant for single-use medical products. The agreement supports Saudi supply localization and adds domestic capacity relevant to disposable consumables used across hospital care pathways, including wound management.

- March 2025: Molnlycke Health Care expanded its stake from 33.3% to 60% to become majority shareholder in Tamer Molnlycke Care. Increasing control over a local manufacturing and distribution platform strengthens in-country availability of wound care products and improves responsiveness to institutional procurement requirements.

- November 2024: Bonvadis topical cream received Medical Device Marketing Authorization approval for all wound indications across Saudi Arabia. The authorization broadened commercial access under SFDA oversight and highlights the central role of MDMA approvals in scaling wound care offerings nationally.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from devices used to prevent, treat, and manage wounds in Saudi Arabia, across inpatient and outpatient care. It includes items such as wound dressings, negative pressure therapy systems, and wound-closure tools used for acute and chronic wounds.

Scope exclusions: We exclude products that are purely pharmaceuticals for healing support, cosmetic scar-reduction kits, and diagnostic-only imaging tools.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map what is actually purchased as a wound care device in Saudi Arabia, before any numbers were built. Public sources were reviewed to capture demand-side signals and context for utilization, such as Saudi Ministry of Health publications, Saudi Food and Drug Authority guidance and device registration cues, General Authority for Statistics demographic tables, World Health Organization country health profiles, and peer-reviewed clinical literature on wound prevalence and diabetic foot ulcers.

Next, we used secondary material to anchor assumptions that are hard to see in a single place, such as hospital capacity expansion, procedure volumes, and shifts toward home care. This included company annual reports and investor decks, reputable press coverage, association websites, and selective use of paid subscriptions for company financials and intelligence, news and financials, patent lookups, and import and export shipment-level checks to sense supply flow direction. The desk sources named above are illustrative and not exhaustive, and other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work then focused on validating what gets counted as device revenue, and how purchasing behavior differs between large hospitals, specialty wound clinics, and home-health oriented channels. We spoke with a mix of clinical stakeholders, procurement and supply-chain teams, distributors, and local market advisors, which helped close information gaps and test the assumptions carried over from desk findings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 53% | Functional/Unit leaders: 39% | |

| Smaller Players: 19% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the treated wound pool in Saudi Arabia is reconstructed by care setting, and then converted into device demand using penetration and replacement logic. For this market, we linked chronic wound drivers (including diabetes-related ulcers), surgical volumes, trauma incidence, and hospital bed capacity to expected use rates for dressings, therapy devices, and closure products, which are then translated into value using typical pricing bands and realistic mix shifts.

After the first total was formed, we used selective bottom-up approximations to keep it practical, such as sampled roll-ups from supplier and distributor revenue shares, channel checks on tender-driven hospital procurement, and a volume times average selling price cross-check for higher-value therapy systems. When a bottom-up view was incomplete, gaps were handled by expanding from observed facility patterns to the national level using hospital counts and care pathway weighting, followed by another round of interview validation.

For forecasting, scenario analysis was applied around a core trend line, because usage is sensitive to policy and care delivery changes. Inputs such as reimbursement expansion, localization initiatives, adoption of negative pressure therapy, movement toward advanced dressings, and home-care growth were stress-tested with expert views, and the final trajectory was kept smooth unless a clear market trigger supported a step change.

Data Validation & Update Cycle

Validation was done through triangulation of the model against independent signals, followed by anomaly checks before sign-off. We compared implied per-patient and per-procedure consumption against clinical practice expectations, reviewed price and mix movements for internal consistency, and flagged any abrupt changes that did not align with procurement cycles or known policy shifts.

Before release, estimates go through multi-analyst review, and respondents are re-contacted when a key assumption moves or when a variance is too large to explain with evidence. Reports are refreshed annually, with interim updates when material events occur, and a final freshness pass is completed right before delivery so clients receive the most current view.

Mordor Intelligence's Saudi Arabia Wound Care Management Devices Market Estimate Compared With Other Published Estimates

Published market values for wound care devices can differ across sources because the product basket is not always the same and the usage assumptions vary by care setting. Gaps also show up when some estimates push a more conservative or aggressive scenario, and when currency timing and local price progression are applied differently.

The main gap comes from whether dressings and wound-closure tools are counted together with therapy devices, where Mordor Intelligence includes the full wound care management device basket (not only wound therapy systems) and then cross-checks demand using treated-wound volumes by setting instead of relying on a narrow supplier-category total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 230.51 M (2025) | |

| Industry Publisher A | USD 225.40 M (2025) | Likely applies a different split across hospitals, long-term care, and home care, which can shift the 2025 product mix and the implied average pricing even when the country and year match. |

| Research Firm B | USD 92.40 M (2025) | Appears to focus on wound management therapy device categories (such as NPWT and compression) and does not capture the larger dressing and closure revenue pool, which pulls the total down. |

Looking across the table, most variance is explained by scope selection first and then by how usage is translated into value through mix and pricing. When the included devices are clearly defined and checked against care-setting level demand signals, the market total stays easier to reproduce and update over time.

Key Questions Answered in the Report

What is the current size of the Saudi Arabia wound care management devices market?

The market stands at USD 241.3 million in 2026 and is forecast to reach USD 303.33 million by 2031.

Which product category leads the market?

Wound Care products lead with 63.92% market share, driven by advanced dressings and mandatory NPWT adoption.

Why are home-health settings growing so quickly?

Telemedicine expansion and insurance coverage for portable devices push the home-health segment to a 5.58% CAGR.

How does Vision 2030 influence market growth?

Vision 2030 funds hospital expansion, mandates advanced therapies, and supports local manufacturing, all of which elevate device demand.

What restraint most affects advanced device uptake?

High upfront costs and reimbursement gaps for outpatient NPWT hinder swift adoption, especially in rural facilities.

Which regions show the fastest growth potential?

Northern and Southern provinces record above-average growth due to telehealth rollout and mobile clinic penetration, despite smaller current volumes.

Page last updated on: