3D Printed Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 17.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printed Medical Devices Market Analysis by Mordor Intelligence

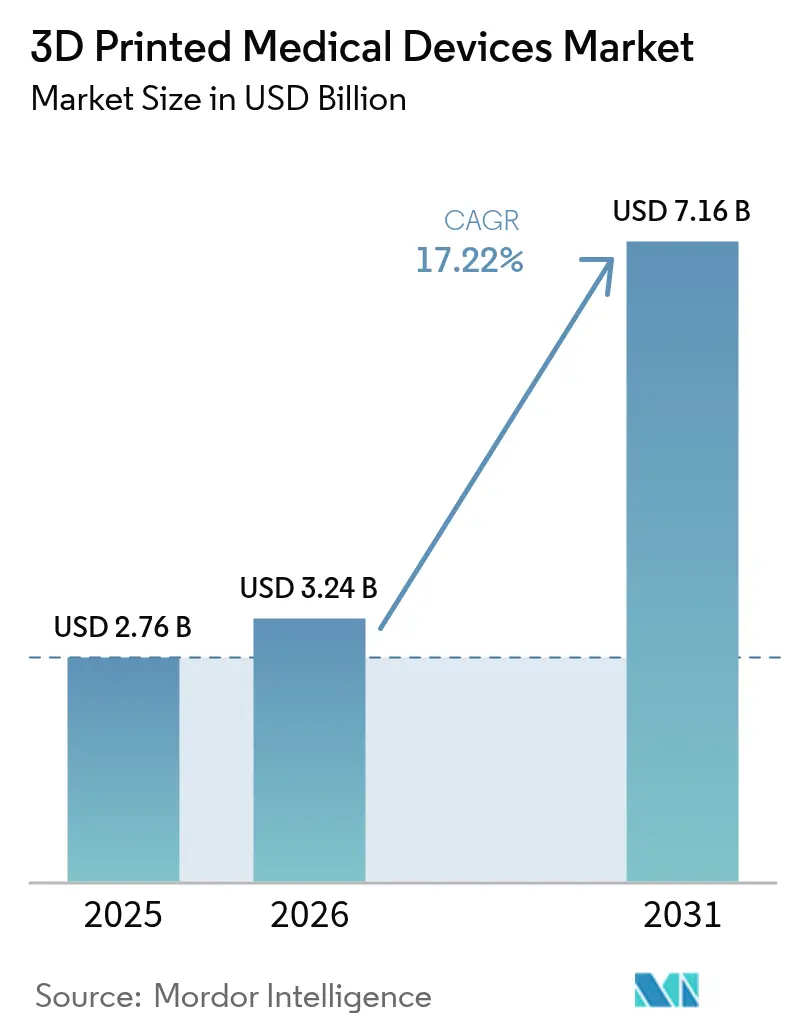

The 3D Printed Medical Devices Market size is expected to grow from USD 2.76 billion in 2025 to USD 3.24 billion in 2026 and is forecast to reach USD 7.16 billion by 2031 at 17.22% CAGR over 2026-2031. Adoption accelerates as point-of-care manufacturing shortens lead times, material science improves the performance of polymers and metals, and regulators issue clearer pathways for patient-specific devices. Hospital-owned print laboratories already cut surgical planning time by 62 minutes per case, saving USD 3,720 per procedure while keeping quality under surgeons’ direct control. Laser beam melting continues to anchor high-value orthopedic and cranio-maxillofacial implants, yet binder jetting gains momentum for faster batch production of metal components. Competitive intensity rises as hardware revenues soften; incumbents now pivot toward software, bioprinting partnerships, and workflow automation to defend margins and capture recurring revenue from consumables.

Key Report Takeaways

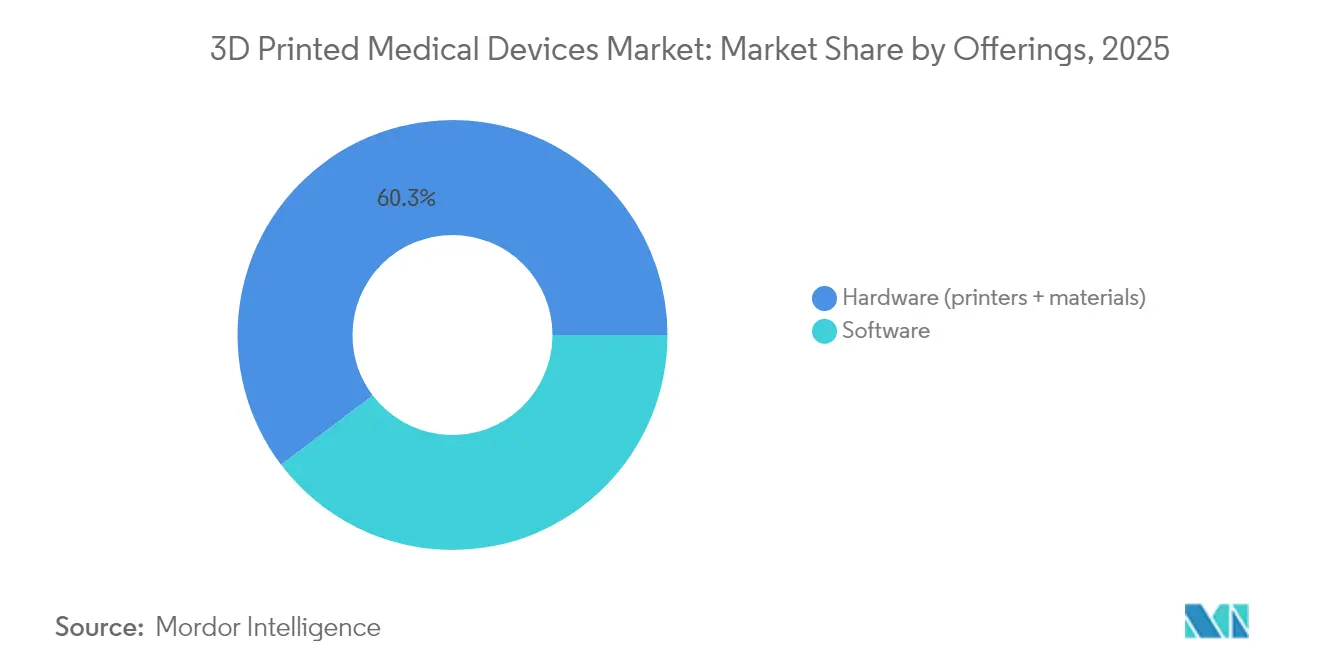

- By offerings, hardware led with 60.32% revenue share in 2025; software is projected to expand at a CAGR higher than the 17.22% market average through 2031.

- By type, prosthetics and implants captured 38.55% of the 3D printed medical devices market share in 2025, while tissue engineering products are projected to grow at an 18.45% CAGR between 2026 and 2031.

- By material, plastics, including surgical-grade photopolymers, held a 49.22% share; biocompatible polymers are projected to grow at an 18.02% CAGR between 2026 and 2031.

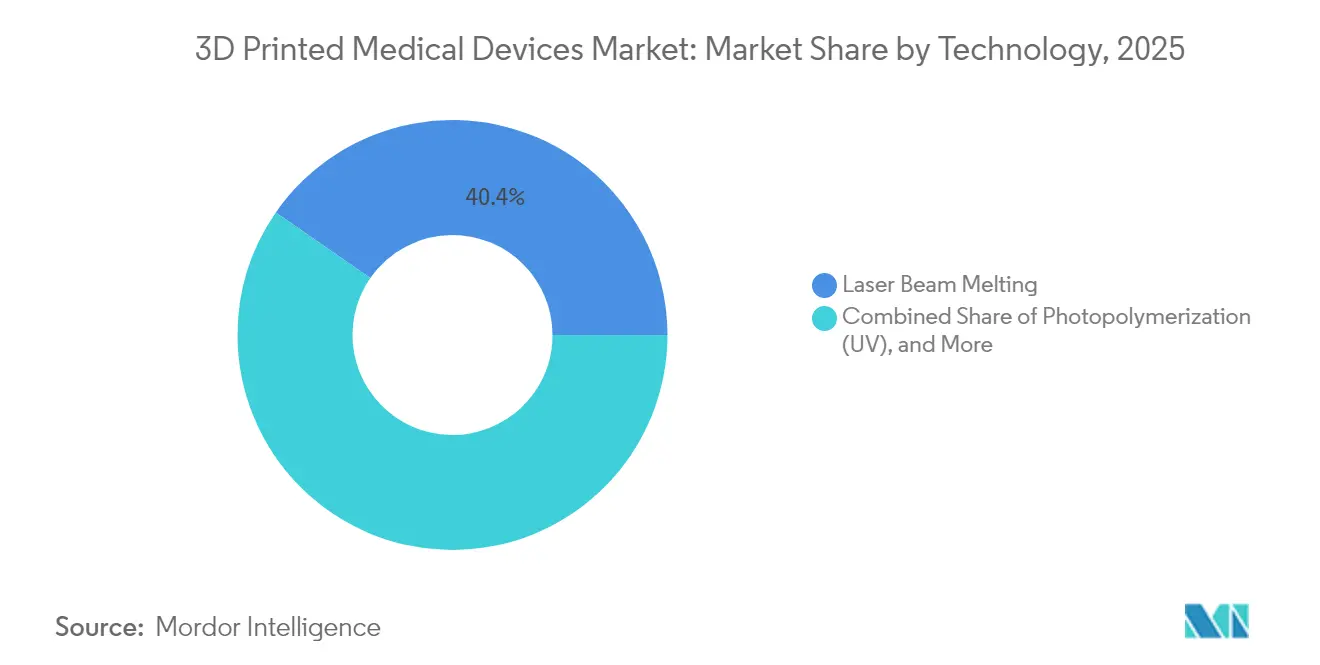

- By technology, laser beam melting held 40.35% of the 3D printed medical devices market share in 2025; binder jetting is projected to expand at an 17.86% CAGR from 2026 to 2031.

- By end user, hospitals and surgical centers accounted for a 47.28% share of the 3D printed medical devices market size in 2025, while specialty clinics are forecast to grow at a 18.01% CAGR from 2026 to 2031.

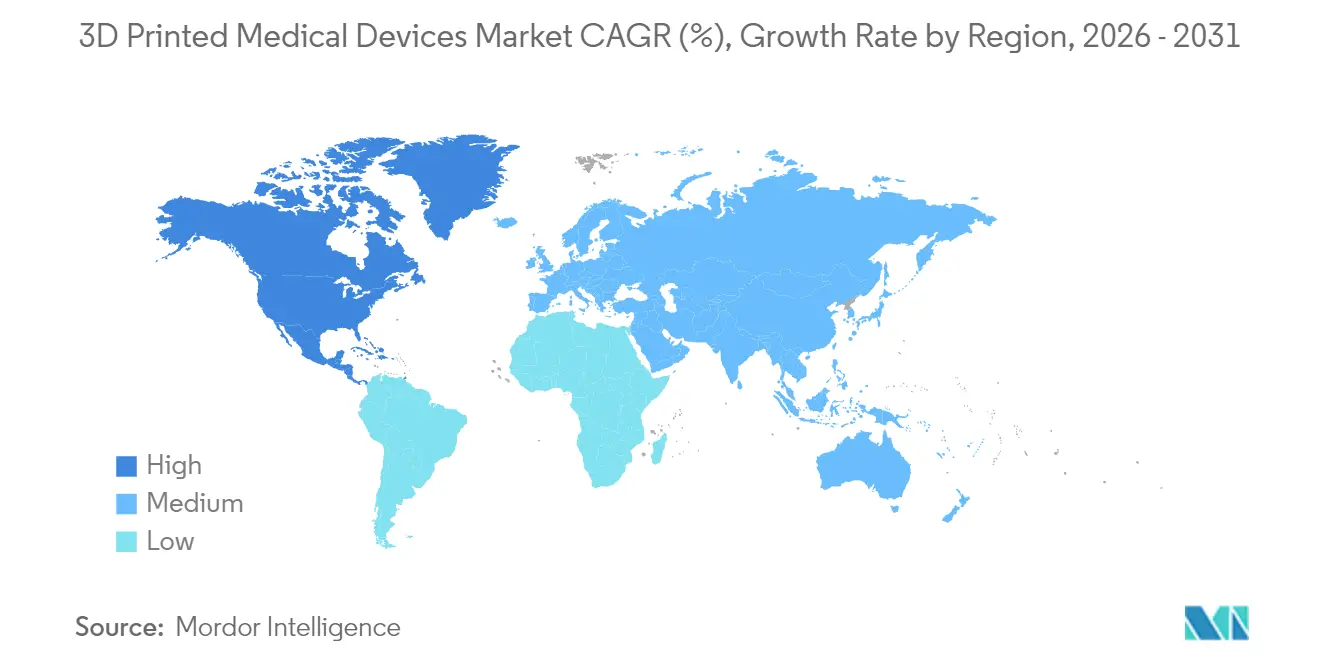

- By geography, North America led with a 45.42% revenue share in 2025; the Asia-Pacific region is expected to grow at a 18.05% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Printed Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Easy mass-customization capability | +4.20% | Global; early uptake in North America and Europe | Medium term (2-4 years) |

| Rising transplant waiting lists | +3.80% | Global; acute in North America and Europe | Long term (≥ 4 years) |

| Cost and lead-time reduction vs. subtractive manufacturing | +3.10% | Global; strongest in developed markets | Short term (≤ 2 years) |

| Surge in hospital-owned point-of-care print labs | +2.90% | North America and Europe; expanding to Asia Pacific | Medium term (2-4 years) |

| ISO/ASTM 52931 biocompatibility standard unlocking new polymers | +2.70% | Global; strongest pull-through in EU/US regulatory environments | Medium term (1–3 years) |

| Defense-funded battlefield bioprinting programs | +2.30% | US (DoD), NATO procurement ecosystems; selective Asia Pacific (Japan, S. Korea) | Long term (3–5+ years) |

| Source: Mordor Intelligence | |||

Easy Mass-Customization Capability

Patient-specific printing removes the constraint of one-size-fits-all devices. Since August 2024, 3D Systems’ EXT 220 MED platform has supported over 60 cranioplasties, each precisely matched to the patient’s anatomy.[1] 3D Systems, “EXT 220 MED delivers 60 successful cranioplasties,” 3dsystems.com Basel surgeons implanted the first MDR-compliant 3D-printed PEEK facial implant in March 2025, bypassing prolonged external supply chains. Operating rooms now generate surgical guides with 100% dimensional accuracy, eliminating the need for iterative template revisions. Complex trabecular structures printed in titanium or PEEK foster osseointegration and mitigate stress shielding, directly improving orthopedic outcomes. The shift from mass production to mass customization underpins higher clinical value and supports premium reimbursement models.

Rising Transplant Waiting Lists

More than 100,000 Americans remain on transplant lists, spurring investment in tissue and organ bioprinting. Bioprinting firms secured a record amount of funding in 2024, and the related market is projected to grow at a 11.8% CAGR through 2034. Galway researchers in 2025 printed contractile heart tissue that morphs under cell-generated forces, bringing functional organs closer to clinical reality.[2]Science Daily, “Shape-changing heart tissues printed at Galway,” sciencedaily.com As vascularization techniques mature, bioprinted constructs are transitioning from research to regulated therapy, positioning the segment as a long-term solution to organ shortages.

Cost and Lead-Time Reduction vs. Subtractive Manufacturing

Additive workflows eliminate the 60-90% material waste typically associated with machining. Hip arthroplasty studies show patient-specific guides shorten procedures from 45.7 minutes to 31.9 minutes and drop blood loss by 88 milliliters. Local printing sidesteps freight delays and reduces inventory write-offs, significant at a time when supply chain expenses equal 20% of medical device revenue. Spare-part production on demand particularly benefits low-volume, high-complexity devices.

Surge in Hospital-Owned Point-of-Care Print Labs

One hundred thirteen US hospitals ran internal 3D labs by late 2024, and Ricoh opened a turnkey point-of-care service in June 2024 that embeds design, printing, and sterilization next to the OR. Yale’s 3D Collaborative for Medical Innovation prototypes surgical instruments in hours, rather than weeks. AI-driven nesting and extended-reality visualization further streamline workflows, cutting design-to-print durations from 100 hours to 18 hours. Embedding quality control inside hospital quality-management systems protects compliance while scaling the model across multi-site systems.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA class-III device clearance pathway | -2.80% | North America; global harmonization | Medium term (2-4 years) |

| High material qualification costs | -2.10% | Global | Short term (≤ 2 years) |

| Shortage of GMP-grade bio-inks | -1.90% | Global; most acute in US/EU (21 CFR / EMA grade requirements) | Medium term (2–4 years) |

| Cyber-sabotage risks in distributed print files | -1.40% | Global; defense + critical care systems highest exposure | Long term (3–5+ years) |

| Source: Mordor Intelligence | |||

Stringent FDA Class-III Device Clearance Pathway

Implantable devices often default to class-III, demanding exhaustive biocompatibility and clinical evidence. ISO 10993-1 guidance can stretch review cycles 12-18 months longer than for traditional forgings. Still, the agency’s 510(k) database logged notable 2024 wins: Curiteva’s PEEK lumbar fusion and Restor3D’s cementless knee replacement gained clearance, illustrating that equivalence arguments are possible even for additively manufactured implants. Achieving predicate alignment remains complex when lattice structures or gradient compositions have no historical analogs.

High Material Qualification Costs

Each new medical-grade polymer or alloy requires toxicity, sterility, and mechanical validation that can cost USD 500,000-1 million. Price pressure worsened in 2024 when PEEK climbed 15-20% and titanium powders rose 25-30% amid geopolitical supply constraints.[3]Evonik, “VESTAKEEP Fusion PEEK pricing update,” evonik.com Smaller firms struggle to amortize these expenses across limited production volumes, risking slower material innovation. Additional hurdles emerge for bio-inks, where batch sterility and cell-culture compatibility compound testing time and documentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offerings: Hardware Dominance Drives Infrastructure Investment

Hardware generated 60.32% of the 3D printed medical devices market size in 2025, as hospitals and service bureaus initially invest in printers and clean-room modifications. Industrial bioprinters cost USD 200,000 to USD 500,000, reinforcing the up-front capital intensity. Printer utilization subsequently generates recurring revenue through polymers, metal powders, and cell-laden hydrogels, a pattern evident as Stratasys posted record consumables revenue despite total sales slipping in 2024.

Printers alone are no longer the sole differentiator of suppliers; workflow software now shortens design iterations, automates support generation, and links directly to sterilization logs. However, Software grows at a rapid rate of 17.64% CAGR during the forecast period (2026-2031). AI-driven platforms cut complex anatomical model preparation from 100 hours to 18 hours, lifting throughput for overstretched clinical engineers. Service offerings remain fragmented, yet health-system buyers increasingly demand integrated ecosystems that combine hardware, validated materials, cloud rendering, and on-site support contracts.

By Type: Prosthetics Lead While Tissue Engineering Accelerates

Prosthetics and implants accounted for 38.55% of the 3D printed medical devices market share in 2025, driven primarily by demand in cranio-maxillofacial and orthopedic applications. Surgeons value latticed titanium hip cups or PEEK skull plates that reduce stress shielding and enable imaging clarity. Regenerative medicine pushes tissue engineering forward at an 18.45% CAGR, outpacing traditional implant growth as scaffold vascularization and immune modulation mature.

Printed surgical guides and instruments further expand the application mix, reducing intraoperative time and enhancing resection accuracy. University Hospital Basel proved regulatory viability when its team implanted the first MDR-compliant facial PEEK device on-site in March 2025. Tissue engineering is expected to register the fastest growth of 18.45% from 2026 to 2031. Tissue engineering will expand into organ-on-chip platforms that support drug discovery, reinforcing the convergence between device and pharmaceutical workflows.

By Materials: Plastics Dominate as Biocompatible Polymers Advance

Plastics, including photopolymer resins, accounted for 49.22% of revenue in 2025, due to their affordability and versatility for models and non-load-bearing devices. Metal powders remain indispensable for load-bearing implants; however, biocompatible polymers are expected to grow at a rate of 18.02% during the forecast period, driven by PEEK variants that bond with calcium phosphate for superior osseointegration.

Titanium and cobalt-chromium powders still define orthopedic load paths, though new tantalum interspinal cages approved by China’s NMPA in 2025 highlight expanding material portfolios. Ceramic resins hold niche dental positions, balancing aesthetics with bio-inert performance.

By Technology: Laser Beam Melting Leads Metal Processing

Laser beam melting accounted for 40.35% of the 3D printed medical devices market share in 2025, as it repeatedly delivers pore-controlled titanium components crucial for hip and spinal implants. Binder jetting is projected to grow at a 17.86% CAGR through 2031, as high-speed heads produce dense metal parts that require minimal post-processing.

Photopolymerization advances through faster light engines and biocompatible resins, making surgical guides more economical for same-day surgery. Extrusion-based techniques dominate cell-laden bioprinting due to their gentle pressure regimes, which preserve cell viability. Electron beam melting remains specialized for aerospace-grade alloys intended for complex anatomical implants, where lower residual stresses help prevent cracking.

By End User: Hospitals Drive Point-of-Care Adoption

Hospitals and surgical centers accounted for 47.28% of the 3D printed medical devices market size in 2025, validating in-house labs as strategic assets that reduce sterile field preparation time and enhance patient engagement through tactile models. Specialty clinics, such as orthopedic and dental practices, are growing at the fastest rate of 18.01% from 2026 to 2031, adopting desktop polymer printers for niche implants and aligners. This growth is faster than institutional averages, achieved by leveraging agile decision-making.

Academic institutes continue to generate translational breakthroughs while serving as low-risk environments for testing new bio-inks and regenerative constructs. Research consortia linking universities with hospitals expedite first-in-human trials by co-locating cell culture labs, printers, and GMP suites.

Geography Analysis

North America contributed 45.42% of global revenue in 2025, reflecting early FDA guidance, mature reimbursement codes, and heavy hospital infrastructure investment. The region’s ecosystem deepens as DARPA channels grants into battlefield bioprinting and smart bandages that merge additive electronics with antimicrobial delivery. Consolidation continues; Enovis paid EUR 800 million for LimaCorporate, expanding its 3D-printed titanium hip portfolio.

Asia-Pacific outpaced the global CAGR with 18.05% during the forecast period. China’s NMPA approved 61 innovative devices in 2024, representing an 11% year-over-year increase that shortens the time-to-market for domestic startups. Japan’s medical device sector is growing at a significant rate annually, driven by aging demographics that demand minimally invasive implants. India harmonizes its regulatory code with IMDRF principles, attracting foreign direct investment for local printer assembly and powder atomization.

Europe balances strict MDR requirements with robust R&D incentives. Germany invests in additive qualifications that transfer know-how from automotive firms to orthopedic suppliers, while UK universities spin out software startups specializing in generative implant design. Sustainability policies that emphasize circular manufacturing favor additive techniques, which reuse powders and eliminate machining waste.

Competitive Landscape

The market remains moderately fragmented. 3D Systems' healthcare revenue declined 21% to USD 40.4 million in 2024, following an accounting shift in its regenerative medicine program; however, it retained clinical momentum through its PEEK cranial series. Stratasys revenue dipped to USD 572.5 million, but a USD 120 million infusion from Fortissimo Capital finances platform consolidation and AI workflows.

Materialise secured FEops to merge cardiovascular simulation with personalized stent planning, while Johnson & Johnson’s USD 16.6 billion Abiomed deal adds heart-recovery technology that may benefit from patient-specific components. Emerging players focus on niche biomaterials, filing patents on stromal cell-laden inks and antimicrobial lattice topologies that integrate directly with hospital sterilizers. Software innovators compete on cloud-based compliance engines that automatically generate production DMRs for MDR and FDA audits, thereby lowering regulatory overhead.

3D-printed medical devices are increasingly being categorized among vertically integrated OEMs, materials science firms, and digital manufacturing platforms. Established leaders in medtech are expanding hybrid additive/subtractive workflows to safeguard their procedural franchises. At the same time, specialists in polymers are hurrying to secure qualified bio-inks and chemistries suitable for implants. On another front, software-centric distributed manufacturing networks, including hospital POC print labs and contract additive service bureaus, are challenging the traditional dominance of centralized manufacturing. The competitive edge is now leaning more towards engines that accelerate regulatory processes, validated libraries of digital parts, and intellectual property in materials, rather than just the hardware of printers.

3D Printed Medical Devices Industry Leaders

3D Systems

Stratasys

Materialise

SLM Solutions

GE Additive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DARPA launched the BEST program to create bioelectronic smart bandages for infection control.

- April 2025: 3D Systems enabled the first MDR-compliant PEEK facial implant at University Hospital Base.

- March 2025: Johnson & Johnson MedTech unveiled digital orthopedics innovations, including FDA-cleared robotic knee systems.

- February 2025: Teleflex bought BIOTRONIK’s vascular intervention unit for EUR 760 million, adding drug-coated balloons to its portfolio.

Global 3D Printed Medical Devices Market Report Scope

3D printing is a method that creates a three-dimensional object by building consecutive layers of raw material. Through this, the manufacturers can create patient-specific devices or devices with very complicated internal structures. Some of the medical devices produced by 3D printing include dental restorations such as crowns, and external prosthetics, surgical instruments and orthopedic and cranial implants. Also, 3D printing enables doctors to work faster, shorten patient theatre time, and improve operation results.

| Hardware | 3D Printers | FDM Printers |

| SLS Printers | ||

| SLA/DLP Printers | ||

| Bioprinters | ||

| Materials | ||

| Software |

| Surgical Guides | |

| Surgical Instruments | |

| Prosthetics and Implants | Orthopedic |

| Dental | |

| Cranio-maxillofacial | |

| Tissue Engineering Products |

| Plastics |

| Metal and Metal Alloy Powders |

| Biocompatible Polymers |

| Ceramics |

| Laser Beam Melting |

| Photopolymerization (UV) |

| Electron Beam Melting |

| Extrusion-based |

| Binder Jetting |

| Hospitals and Surgical Centers |

| Specialty Clinics |

| Academic and Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Gulf Cooperation Council (GCC) |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Offerings | Hardware | 3D Printers | FDM Printers |

| SLS Printers | |||

| SLA/DLP Printers | |||

| Bioprinters | |||

| Materials | |||

| Software | |||

| By Type | Surgical Guides | ||

| Surgical Instruments | |||

| Prosthetics and Implants | Orthopedic | ||

| Dental | |||

| Cranio-maxillofacial | |||

| Tissue Engineering Products | |||

| By Materials | Plastics | ||

| Metal and Metal Alloy Powders | |||

| Biocompatible Polymers | |||

| Ceramics | |||

| By Technology | Laser Beam Melting | ||

| Photopolymerization (UV) | |||

| Electron Beam Melting | |||

| Extrusion-based | |||

| Binder Jetting | |||

| By End User | Hospitals and Surgical Centers | ||

| Specialty Clinics | |||

| Academic and Research Institutes | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East | Gulf Cooperation Council (GCC) | ||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the 3D printed medical devices market expected to grow through 2031?

The market is forecast to expand from USD 3.24 billion in 2026 to USD 7.16 billion by 2031, translating to a 17.22% CAGR.

Which segment currently generates the most revenue?

Hardware, including industrial printers and consumables, accounted for 60.32% of market revenue in 2025.

What application area shows the quickest future growth?

Tissue engineering products, supported by bioprinting advances, are projected to grow at an 18.45% CAGR, outpacing traditional implants.

Why are hospitals investing in in-house 3D printing labs?

Point-of-care facilities shorten surgical planning by 62 minutes and cut USD 3,720 in costs per case, while giving surgeons full control over patient-specific devices.

Which technology is gaining share the fastest?

Binder jetting is projected to exceed the overall 17.22% market CAGR as high-speed print heads accelerate metal part production for surgical instruments.

How stringent are FDA requirements for 3D-printed implants?

Implantable devices often fall under class-III, requiring extensive biocompatibility and clinical evidence, which can extend approval by 12-18 months versus conventional devices.

Page last updated on: