Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

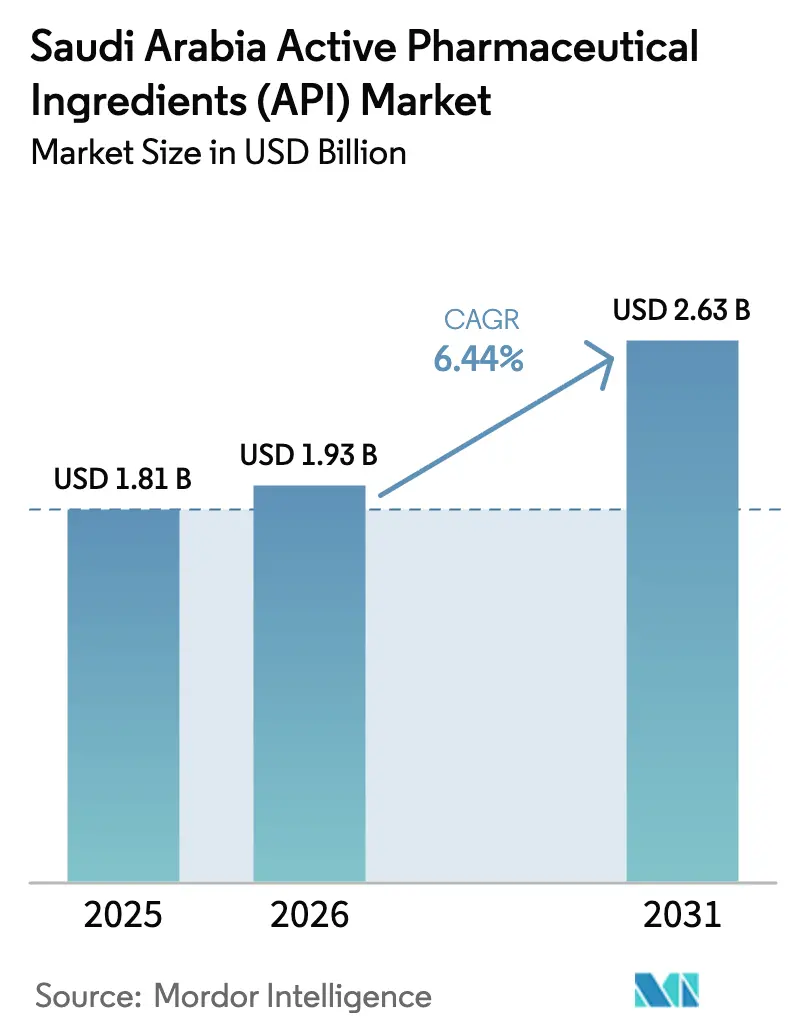

| Base Year Market Size (2025) | USD 1.81 Billion |

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Active Pharmaceutical Ingredients (API) Market Analysis by Mordor Intelligence

The Saudi Arabia Active Pharmaceutical Ingredients market size is expected to grow from USD 1.81 billion in 2025 to USD 1.93 billion in 2026 and is forecast to reach USD 2.63 billion by 2031 at 6.44% CAGR over 2026-2031. Vision 2030 incentives, the National Biotechnology Strategy, and a combined SAR 260 billion healthcare and social development budget allocation are steering the sector toward self-sufficiency while attracting multinational contract developers. Demand also benefits from a 16.4% diabetes prevalence and a 14.9% rise in cardiovascular disease diagnoses, which together elevate chronic-care prescriptions. Supply-side momentum stems from government-backed biologics clusters in King Abdullah Economic City (KAEC) and Jeddah, 50-year tax holidays in the Special Integrated Logistics Zone, and streamlined approvals under the Breakthrough Medicine Program. Near-source strategies gained urgency after Red Sea shipping disruptions, prompting firms to anchor production inside the Saudi Arabia Active Pharmaceutical Ingredients market for regional resilience.

Key Report Takeaways

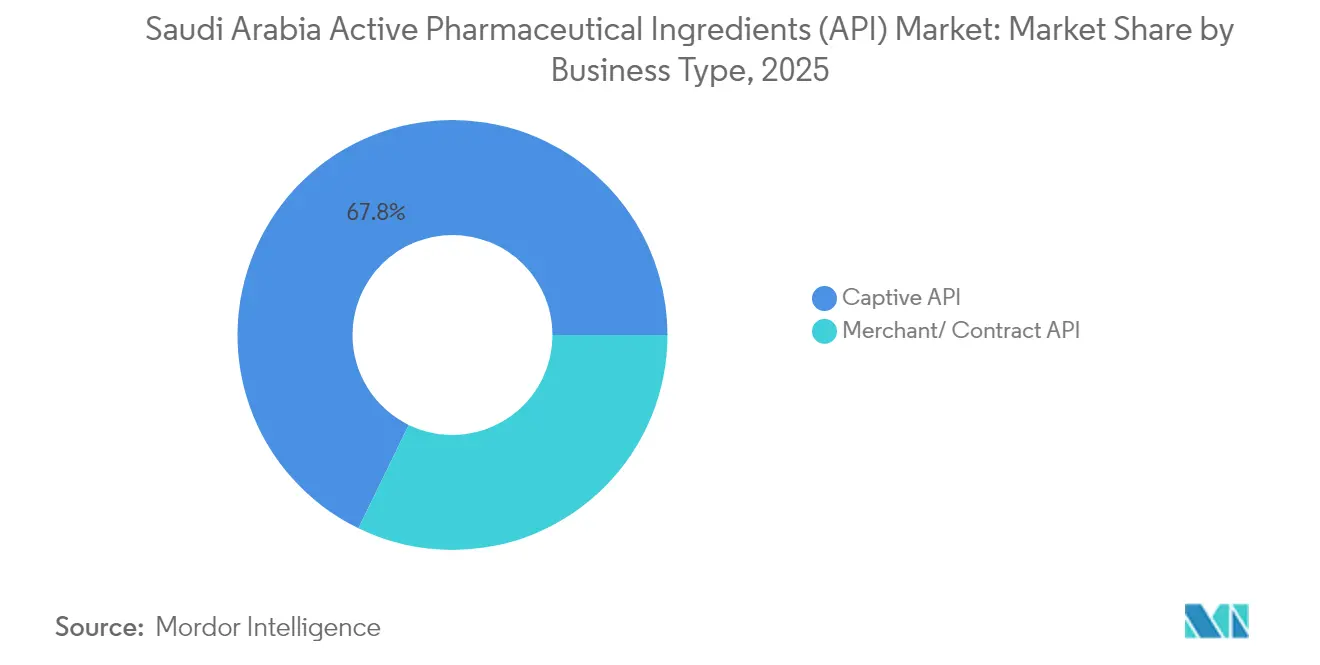

- Captive API production led with 67.79% of the Saudi Arabia Active Pharmaceutical Ingredients market share in 2025, while merchant manufacturing posted the fastest 6.86% CAGR through 2031.

- Synthetic APIs captured 76.05% revenue in 2025; biotech APIs are advancing at a 6.9% CAGR to 2031.

- Small-molecule compounds held 69.15% of 2025 value, whereas large-molecule biologics are projected to grow at a 6.95% CAGR.

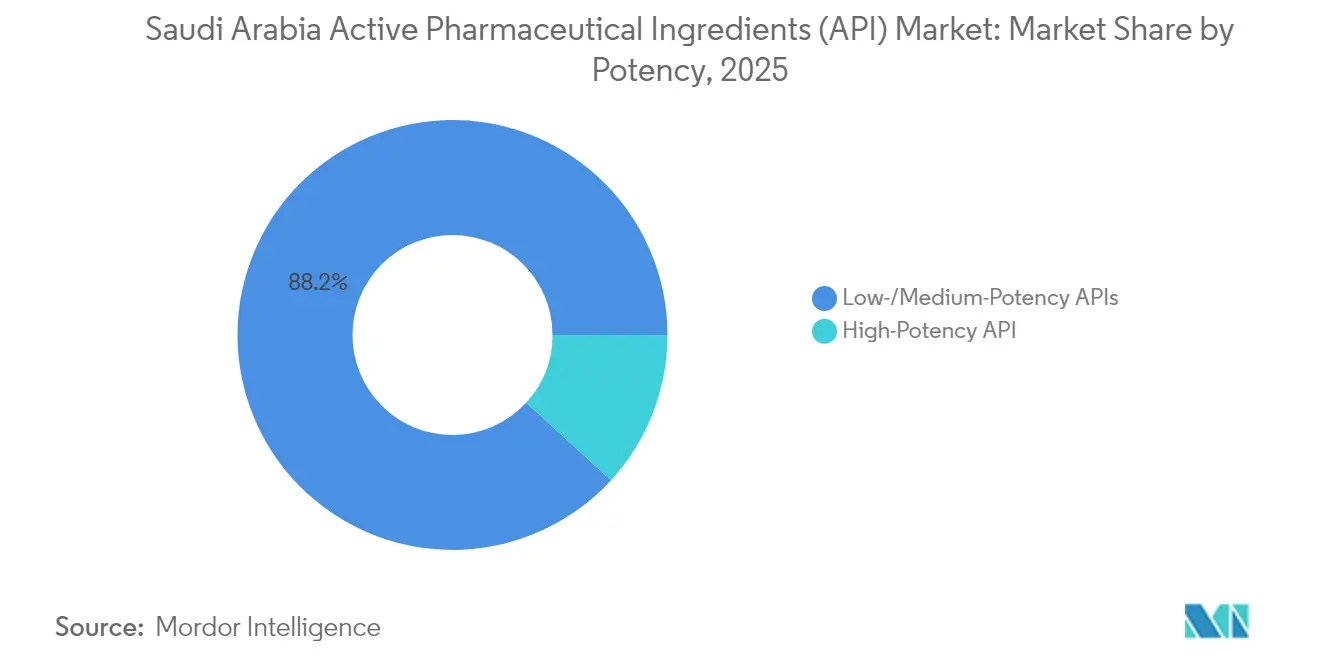

- Low/medium-potency substances represented 88.20% of 2025 sales; high-potency APIs are rising at a 6.99% CAGR.

- Cardiovascular therapies commanded 28.55% share in 2025, yet oncology is set to expand at a 7.04% CAGR to 2031.

- Pharmaceutical companies retained 68.55% share in 2025, with CDMOs pacing at 6.83% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Active Pharmaceutical Ingredients (API) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 localization incentives & NIDLP subsidies | +1.2% | National, concentrated in KAEC & Jeddah | Medium term (2-4 years) |

| Mandatory local-content quotas in MoH tenders | +0.8% | National, with priority in government procurement | Short term (≤ 2 years) |

| Rising chronic-disease burden expanding domestic drug demand | +1.0% | National, highest in urban centers | Long term (≥ 4 years) |

| Biologics cluster investments at KAEC & Jeddah for mAbs/viral-vector APIs | +0.7% | Regional, KAEC & Jeddah industrial zones | Medium term (2-4 years) |

| CDMO tax-free industrial-zone appeal to global partners | +0.6% | National, focused on Special Economic Zones | Medium term (2-4 years) |

| Import-route disruptions accelerating near-source API production | +0.5% | National, with spillover to GCC region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Localization Incentives & NIDLP Subsidies

Government cash grants, 30-year tax relief, and fast-track approvals make local production financially compelling. More than 350 multinationals secured Regional Headquarters licenses by March 2024, many converting distribution outposts into full-scale plants. Novo Nordisk and Sanofi signed 2024 insulin tie-ups with NUPCO, signaling momentum for domestically sourced inputs. Reduced import reliance could trim external API spend by 25% over the forecast horizon.

Mandatory Local-Content Quotas in MoH Tenders

Pharmaceutical bids covering about 60% of national drug purchases now score highest when ingredients are Saudi-made. NUPCO bundles multi-year purchase guarantees, ensuring plant utilization and de-risking capital expenditure. Global players have partnered with local firms solely to preserve access to this protected channel. Early adopters gain predictable demand, which supports financing for capacity expansions inside the Saudi Arabia Active Pharmaceutical Ingredients market.

Rising Chronic-Disease Burden Expanding Domestic Drug Demand

Diabetes alone costs SAR 17 billion annually and continues to rise alongside hypertension and obesity. Universal insurance slated for 2026 will widen treatment access, locking in repetitive demand for cardiovascular, metabolic, and oncology APIs. Urban lifestyles intensify prevalence, assuring sustained volume growth. Chronic-care regimens require uninterrupted supply, prompting manufacturers to localize primary intermediate lines to avoid freight and tariff volatility.

Biologics Cluster Investments at KAEC & Jeddah

KFSHRC-Germfree’s modular ATMP campus and deep-water export lanes give Saudi plants an edge in cold-chain biologics. Government grants targeting 11,000 biotech jobs nurture monoclonal antibody and viral-vector lines, anchoring the Saudi Arabia Active Pharmaceutical Ingredients market as a regional supply base for high-margin biologics. Co-location with logistics corridors shortens time to clinical sites, a critical factor for temperature-sensitive therapies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of GMP-experienced chemical-engineering talent | -0.9% | National, acute in specialized manufacturing zones | Long term (≥ 4 years) |

| Continued reliance on imported key starting materials | -0.6% | National, with supply chain vulnerabilities | Medium term (2-4 years) |

| High energy & water footprint vs national sustainability targets | -0.4% | National, concentrated in industrial zones | Long term (≥ 4 years) |

| Lengthy SFDA plant-approval cycle slowing time-to-market | -0.3% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of GMP-Experienced Chemical-Engineering Talent

Industrial expansion needs engineers with sterile-processing expertise, yet Saudization policies cap expatriate hiring. An estimated 175,000 extra health-sector professionals are required by 2030, leaving the Saudi Arabia Active Pharmaceutical Ingredients market short of critical skill sets. Companies now fund accelerated curricula and overseas fellowships to bridge gaps. Although training pipelines have begun to scale, staffing constraints still slow facility ramp-up and inflate wage costs.

Continued Reliance on Imported Key Starting Materials

Roughly 80% of raw intermediates still arrive from Asia, exposing manufacturers to freight shocks and regulatory differences. SABIC’s upstream projects focus on bulk chemicals rather than specialized precursors, delaying full value-chain localization. Firms hedge by diversifying suppliers, yet any extended shipping disruption could squeeze inventories and raise working-capital requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Captive Operations Hold Scale While Contract Manufacturing Gains Pace

Captive plants accounted for 67.79% of 2025 revenue, as integrated drug makers prefer in-house control over quality and intellectual property. SPIMACO’s vertically aligned campus in Jeddah achieved 97% utilization, reinforcing its 6% overall share in the Saudi Arabia Active Pharmaceutical Ingredients market. The model locks down supply security for chronic-care molecules, supports predictable lines, and limits audit complexity.

Merchant production, though smaller in absolute terms, is advancing at a 6.86% CAGR. Zero-tax zones and long-term land leases entice global CDMOs to locate batch lines locally for Middle East and Africa fulfillment. Sudair Pharmaceutical City’s plug-and-play modules allow rapid scale-up, while plans by WuXi AppTec to explore a Gulf hub underline growing confidence among multinational contractors.

By Synthesis Type: Synthetic Dominance Continues as Biotech Gathers Momentum

Synthetic compounds captured 76.05% of 2025 turnover because petrochemical feedstocks remain inexpensive and plentiful. Cardiovascular and diabetes therapies, still dominated by small-molecule drugs, sustain base-load demand, keeping utilization high across older multipurpose reactors. The Saudi Arabia Active Pharmaceutical Ingredients market size for established synthetic lines therefore benefits from economies of scale and minimal technology risk.

Biotech-derived APIs are expanding at a 6.9% CAGR, propelled by the National Biotechnology Strategy and KAEC’s large fermentation vessels. NEOM’s precision-fermentation equity investment in Liberation Labs widens applications into enzymes and nutritional proteins, foreshadowing more diverse revenue streams inside the sector.

By Molecule Size: Small-Molecule Foundations Complement Large-Molecule Upswing

Small molecules retained 69.15% of 2025 activity due to entrenched mass-market therapies and favorable cost-of-goods. Jamjoom’s dermatology and ophthalmology portfolio demonstrates ongoing room for process innovation within traditional chemistry pipelines. These efficiencies allow producers to serve dense chronic-disease demand while generating reliable cash flows.

Large molecules are growing fastest at 6.95% CAGR as hospitals embrace monoclonal antibodies and cell-based regimens. Modular cleanrooms at KAEC enable rapid switching between biologic campaigns, which reduces downtime and boosts the Saudi Arabia Active Pharmaceutical Ingredients market size attributable to biologics. As clinical guidelines shift toward targeted therapies, large-molecule plants capture an increasing share of new product launches.

By Potency: High-Potency Increment Fueled by Oncology Needs

Low and medium-potency ingredients generated 88.20% of 2025 sales, reflecting continuing volume in hypertension, diabetes, and respiratory drugs. Such plants require standard containment, supporting economies of scale and predictable scheduling.

High-potency APIs are advancing 6.99% annually as oncology protocols proliferate. SPIMACO’s SAR 272 million cytotoxic line, co-financed by AstraZeneca, adds isolator suites and sub-micro-gram air handling to manufacture antibody–drug conjugate payloads, setting higher barriers to entry. Tighter regulatory oversight also supports premium pricing and specialization.

By Therapeutic Area: Cardiovascular Anchors Volume; Oncology Leads Growth

Cardiovascular APIs held 28.55% market share in 2025 because hypertension affects 11.1% of Riyadh adults. Consistent dosing keeps batch campaigns long and repetitive, anchoring baseline revenue.

Oncology substances are advancing at 7.04% CAGR, buoyed by earlier diagnostics and government cancer-center buildouts. KFSHRC protocols increasingly require monoclonal antibody intermediates, strengthening localization imperatives and lifting high-potency demand.

By End User: Integrated Pharma Dominates as CDMOs Accelerate

Domestic and multinational drug makers controlled 68.55% share in 2025, leveraging owned facilities for supply security. Regional-headquarters incentives lure global brand owners to embed R&D alongside manufacturing, reinforcing vertical integration.

CDMOs are scaling at 6.83% CAGR as sponsors outsource to contain fixed costs. Duty-free equipment imports inside the Special Integrated Logistics Zone translate into thin-margin agility attractive to Western biotech start-ups running Gulf-based clinical trials.

Geography Analysis

Saudi Arabia commands roughly 60% of GCC healthcare outlays, positioning the Saudi Arabia Active Pharmaceutical Ingredients market as the region’s anchor tenant. KAEC’s deep-water port shortens freight routes to African and European buyers, while 100% foreign ownership aligns with multinational governance requirements. Import-substitution quotas push firms to install lysine fermenters and spray-dryers near Jeddah, thereby increasing local content in chronic-care supply chains.

GCC harmonization under the Gulf Health Council simplifies registration requirements for exports. Jamjoom enjoyed 19.2% expansion in fellow GCC states, illustrating export scalability nurtured by Saudi batch capacity. North Africa’s USD 17 billion pharmaceutical spend represents additional pull: Avalon Pharma lifted exports 85% by leveraging Saudi certificates of analysis accredited by WHO prequalification.

Logistics diversification remains a strong selling point. Multiple Red Sea and Gulf ports plus a planned east-to-west land bridge reduce reliance on Suez-linked passages that recently faced insurance premiums and security delays. These corridors reinforce the Saudi Arabia Active Pharmaceutical Ingredients market in safeguarding just-in-time supply chains for MENA formulators

Competitive Landscape

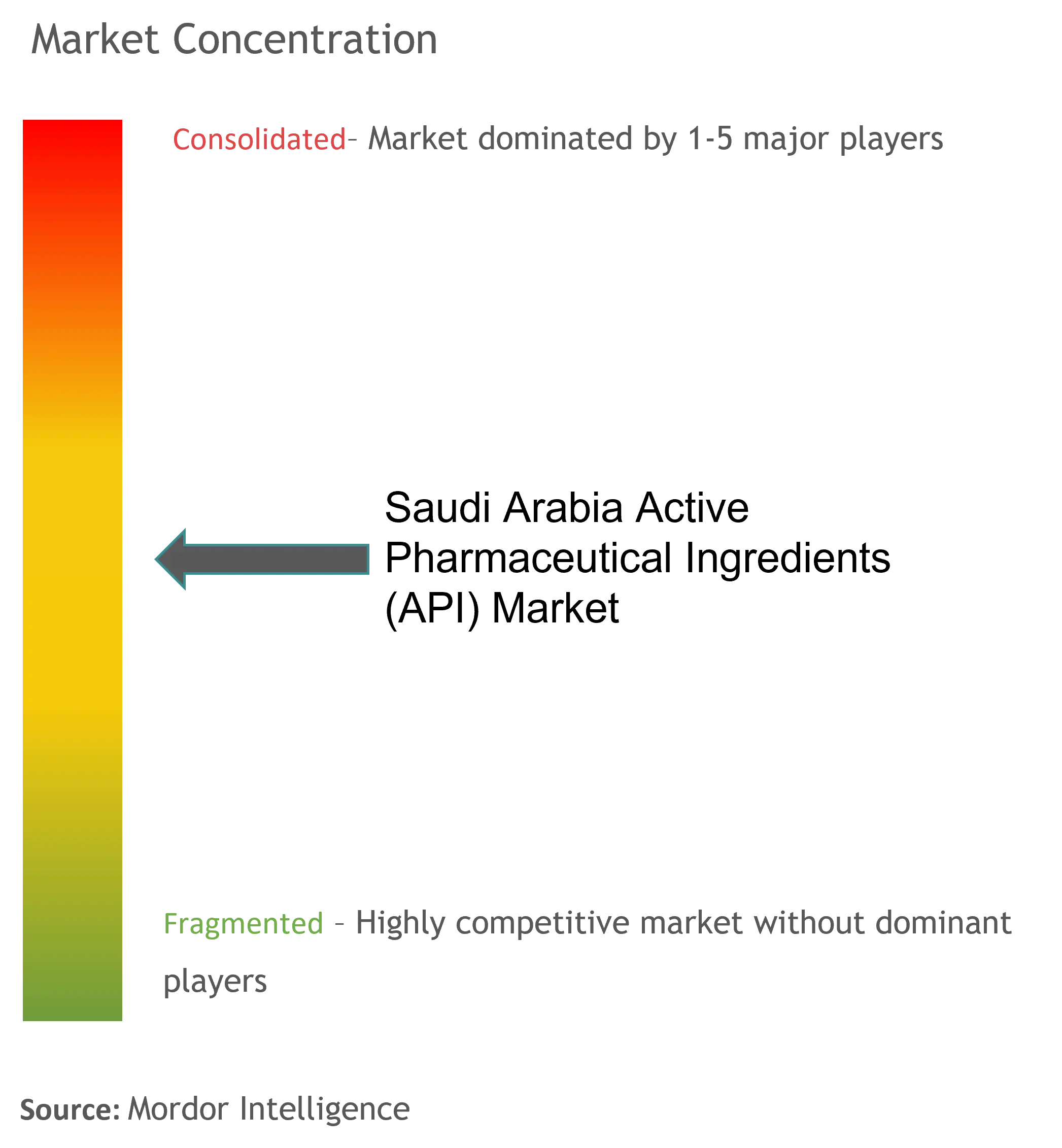

The field remains moderately fragmented; the five largest domestic and foreign players capture significant portion of total sales, leaving ample opportunity for niche specialists. SPIMACO’s reflects advantages from end-to-end oncology lines and high visibility in public procurement. International entrants such as Hikma leverage regional acquisitions to deepen therapeutic catalogs and secure multi-year tenders.

Merger-control filings rose 16% in Q1 2025, with 80% involving overseas investors, signaling intensifying consolidation and technology-transfer deals. Biotech-specific investments create white-space differentiation; KFSHRC’s ATMP site enables viral-vector APIs rarely manufactured locally, giving early movers premium pricing room.

Regulatory agility further shapes competitive posture. The Breakthrough Medicine Program trims dossier review cycles, allowing innovators to commercialize faster while adhering to ICH-aligned quality. Firms with robust regulatory affairs teams gain a head start over generic-heavy rivals, underscoring why local liaison offices become strategic assets in the Saudi Arabia Active Pharmaceutical Ingredients market.

Saudi Arabia Active Pharmaceutical Ingredients (API) Industry Leaders

Pfizer, Inc.

Aurobindo Pharma

Novartis AG

BASF SE

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- undefined

- Dec 2024: Bio-Thera Solutions and Tabuk Pharma partnered for Stelara biosimilar development and local production.

- December 2024: Hikma Pharmaceuticals acquired Takeda’s MENA portfolio, broadening its regional therapeutic breadth

Saudi Arabia Active Pharmaceutical Ingredients (API) Market Report Scope

An active pharmaceutical ingredient (API) is a part of any drug that produces its effects. Some drugs, such as combination therapies, have multiple active ingredients to treat different symptoms or act in different ways. They are produced using highly technological industrial processes, both during the R&D and the commercial production phase.

The Saudi Arabia Active Pharmaceutical Ingredients (API) Market is Segmented by Drug Type (Branded and Generic) and Application (Cardiology, Oncology, Neurology, Orthopedic, Ophthalmology, and Other Applications). The report offers the value (in USD billion) for the above segments.

By Business Mode

| Captive API |

| Merchant / Contract API |

By Synthesis Type

| Synthetic APIs |

| Biotech APIs |

By Molecule Size

| Small-Molecule |

| Large-Molecule / Biologics |

By Potency

| High-Potency APIs (HPAPI) |

| Low/Medium-Potency APIs |

By Therapeutic Area

| Oncology |

| Cardiovascular |

| Metabolic Disorders (Diabetes) |

| Infectious Diseases |

| CNS & Neurology |

| Respiratory |

| Other Therapeutic Areas |

By End-User

| Domestic Pharma Manufacturers |

| Multinational Pharma Subsidiaries (KSA) |

| CDMOs / CMOs |

| Hospitals & Research Institutes |

| By Business Mode | Captive API |

| Merchant / Contract API | |

| By Synthesis Type | Synthetic APIs |

| Biotech APIs | |

| By Molecule Size | Small-Molecule |

| Large-Molecule / Biologics | |

| By Potency | High-Potency APIs (HPAPI) |

| Low/Medium-Potency APIs | |

| By Therapeutic Area | Oncology |

| Cardiovascular | |

| Metabolic Disorders (Diabetes) | |

| Infectious Diseases | |

| CNS & Neurology | |

| Respiratory | |

| Other Therapeutic Areas | |

| By End-User | Domestic Pharma Manufacturers |

| Multinational Pharma Subsidiaries (KSA) | |

| CDMOs / CMOs | |

| Hospitals & Research Institutes |

Key Questions Answered in the Report

How large is the Saudi Arabia Active Pharmaceutical Ingredients market today?

The Saudi Arabia Active Pharmaceutical Ingredients market size stood at USD 1.93 billion in 2026 and is expected to reach USD 2.63 billion by 2031.

What growth rate is expected through 2031?

The sector is forecast to expand at a 6.44% CAGR between 2026 and 2031, propelled by Vision 2030 incentives and rising chronic-disease prevalence.

Which segment is expanding fastest?

Oncology APIs lead growth with a projected 7.04% CAGR through 2031, supported by new cancer-drug manufacturing partnerships.

How are biologics influencing production patterns?

Government-backed clusters in KAEC and Jeddah are accelerating biotech API capacity, pushing biologics output toward a 6.9% CAGR.

What policy tools support localization?

Vision 2030 subsidies, mandatory local-content quotas, 50-year tax holidays in logistics zones, and the Breakthrough Medicine Program all fast-track domestic API manufacture.

What challenges could slow expansion?

Skill shortages in GMP-trained engineers and dependence on imported starting materials remain key bottlenecks to rapid scale-up.

Page last updated on: