Safflower Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

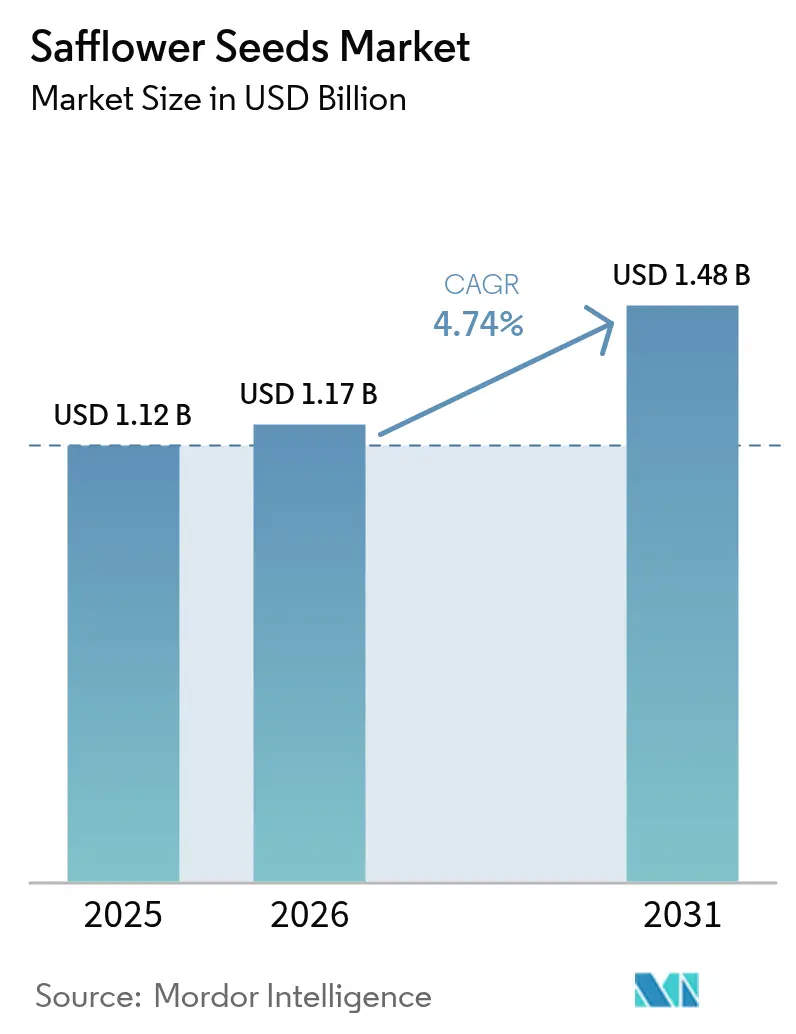

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Safflower Seeds Market Analysis by Mordor Intelligence

Safflower seeds market size in 2026 is estimated at USD 1.17 billion, growing from 2025 value of USD 1.12 billion with 2031 projections showing USD 1.48 billion, growing at 4.74% CAGR over 2026-2031. Growth reflects the crop’s high-oleic profile, suitability for climate-resilient rotations, and expanding use in cosmetics, functional foods, bird feed, and industrial biolubricants. The Asia-Pacific anchors demand through India’s oilseed self-sufficiency drive and China’s specialty oil imports, while processors in Europe and North America channel high-oleic output toward renewable diesel mandates. Africa enters the supply mix as an emerging origin, though logistics gaps temper near-term upside. Global crushers treat safflower as a rotational filler, leaving room for regional specialists to capture premiums through identity-preserved, non-GMO, and organic channels.

Key Report Takeaways

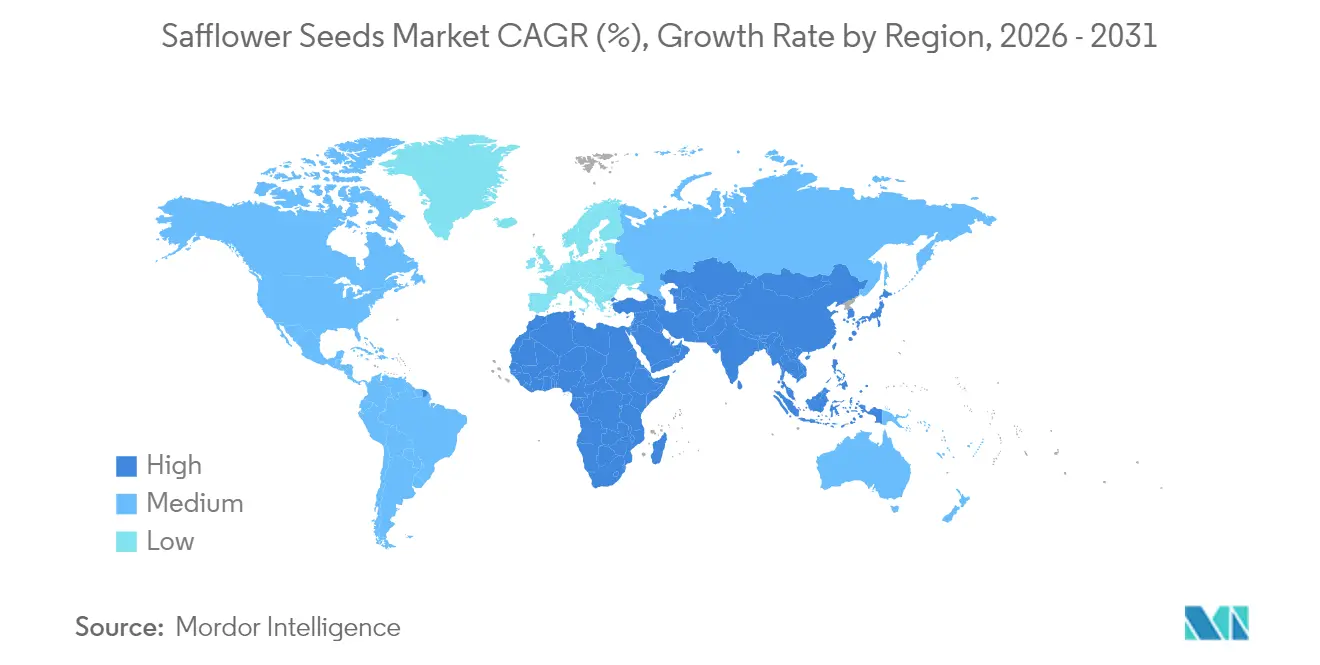

- By geography, Asia-Pacific led with 33.90% of the safflower seeds market share in 2025, while Africa is forecast to expand at a 7.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Safflower Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Plant-Based Oils | +1.2% | Global, with concentration in North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Expansion in Cosmetic Formulations | +0.9% | North America, Europe, and the Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth of Functional Foods Sector | +0.7% | Asia-Pacific, North America | Long term (≥4 years) |

| Increasing Bird-feed Consumption | +0.5% | North America, Europe | Short term (≤2 years) |

| Adoption in Biolubricants | +0.8% | Europe, North America, with spillover to Asia-Pacific industrial zones | Long term (≥4 years) |

| Carbon-Sequestration Crop Programs | +0.6% | Europe and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Plant-Based Oils

Food makers replacing trans-fats are favoring high-oleic safflower oil, which delivers 79% oleic acid and 338 mg/kg tocopherols, matching olive oil stability at a lower cost. OECD-FAO outlook puts vegetable-oil demand growth at 1.8% annually through 2033, with 52% for food and 18% for biodiesel [1]Source: Food and Agriculture Organization of the United Nations, “OECD-FAO Agricultural Outlook,” FAO.ORG. India’s per-capita oil use rises from 11 kg in 2024 to 13 kg by 2034, prompting rabi-season safflower expansion in Maharashtra and Karnataka. Processors, must segregate high-oleic and linoleic lots, adding logistics costs absent in sunflower or canola flows. As health-centric labeling grows, the safflower seeds market secures a durable demand channel even when edible oil prices soften.

Expansion in Cosmetic Formulations

Safflower oil’s non-comedogenic profile elevates it from commodity to prestige skincare ingredient. Sharon Personal Care’s Hydresia SF2 lowers transepidermal water loss by 18% and allows brands to claim biomimetic hydration without synthetic emulsifiers. Clean-beauty labels, such as Typology, pay USD 8–50/kg for organic, cold-pressed oil, rewarding identity-preserved supply chains. Regulatory alignment with European Cosmetic Regulation 1223/2009 and eases cross-border trade. Yet cosmetics absorb only 2-3% of the global output, so the segment cannot fully buffer crush margins during weak edible oil cycles. Still, the safflower seeds market gains brand visibility that cascades into functional-food and nutraceutical innovation.

Growth of Functional Foods Sector

Extracts rich in hydroxysafflor yellow A target cardiovascular and metabolic benefits, shifting value from commodity oil to high-margin nutraceuticals. Research into omega-3 enrichment positions safflower as a terrestrial alternative to marine DHA for the USD 4.1 billion supplement market. Brands fold neutral-tasting oil into fortified drinks and bars, but commercial claims hinge on costly randomized clinical trials. Iranian dual-purpose trials yielded 11,266 kg/ha forage plus 520 kg/ha seed, showing livestock feed that could widen farmer adoption. The safflower seeds market thus taps health-oriented consumers while supporting agronomic diversification.

Increasing Bird-Feed Consumption

North American and European backyard-bird enthusiasts favor safflower seed for its hard shell that deters squirrels. Retail sells 5 bags at USD 10 and 50-lb sacks at USD 65, a 30–40% premium over sunflower blends. Bird feed accounts for 8–10% of regional safflower production, offering a reliable outlet for off-grade products. Seasonal winter surges pose warehousing challenges, which vertically integrated suppliers mitigate with climate-controlled storage. Although its geographic reach is limited, this niche sets a demand floor that stabilizes prices in the safflower seeds market during edible oil gluts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Sunflower and Canola Seeds | -0.9% | Global, particularly Europe, North America, and the Asia-Pacific | Short term (≤2 years) |

| High Processing Costs | -0.6% | Global, with an acute impact in North America and Europe | Medium term (2-4 years) |

| Volatile Specialty-Crop Acreage Incentives | -0.5% | North America, with spillover to Argentina and Australia | Short term (≤2 years) |

| Limited Cold-Chain Infrastructure in Africa | -0.4% | Africa, particularly Tanzania and Ethiopia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Competition from Sunflower and Canola Seeds

Sunflower and canola output of 60 million metric tons and 85 million metric tons dwarfs safflower’s 723,873 metric tons, yielding lower per-unit crush costs and stronger processor commitment. Projections indicate that safflower prices will decline to USD 0.185 by 2028, as the stocks-to-use ratio reaches 9.6% [2]Source: U.S. Department of Agriculture, “USDA Farm Programs Baseline—06-2024,” CBO.GOV. While Black Sea disruptions in 2022-2023 briefly boosted substitution, the normalization of sunflower exports restores their cost advantage in price-sensitive markets. The safflower seeds market, therefore, competes on niche credentials rather than volume economics.

High Processing Costs

Identity-preserved supply, lower oil yields, and molecular distillation increase processing expenses by USD 0.10–0.15/lb, while forward contracts must offer USD 1.00–1.75/bu farmer premiums for biotech seed and USD 1.50–2.50/bu for non-GMO lots. Line changes in multi-oil plants can reduce throughput by up to 20%. Smaller crushers lack scale to amortize these costs, leaving the safflower seeds market vulnerable to margin compression when edible-oil spreads narrow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific holds 33.90% of the 2025 value, reflecting India’s subsidy-led rabi-season acreage, China’s specialty-oil import pull, and Australia’s rotation strategy. India’s National Mission on Edible Oils-Oilseeds allocates Rs 10,103 crore (USD 1.2 billion) for 2024-2031 to boost oilseed output, positioning safflower as a water-smart alternative in Maharashtra and Karnataka. China continues to import high-oleic grades, allowing processors like Xinjiang Tianding to capture organic premiums. Australia’s plantings remain modest, but Bunge’s 2024 multi-oil plant announcement signals future capacity that could integrate safflower on flexible lines.

Africa is projected to post the fastest growth at a 7.68% CAGR through 2031, driven by Tanzania and Ethiopia’s export-oriented agricultural expansion, despite logistics gaps. Ethiopian trials have shown seed yields of up to 2,343 kg/ha under irrigation, with oil content increasing to 29.5% under rainfed conditions. Tanzania paradoxically imports sunflower-safflower blends while exporting raw seed, underscoring cold-chain deficits that erode farmgate returns . Unlocking the potential of the safflower seeds market in Africa hinges on the availability of refrigerated storage and financing for rural electrification.

Europe, North America, and the Middle East account for the remainder. Europe’s Renewable Energy Directive pulls safflower into renewable-diesel supply chains through the 2025 Bunge-Repsol pact. Russia and Kazakhstan supply over 52% of global production, yet Turkey captures downstream value with USD 120.8 million seed imports in 2023. North America’s area declines while prices soften, signaling processors’ reluctance to invest in the absence of policy tailwinds. Mexico’s 65,760 metric ton harvest satisfies domestic bird feed and crush demand, leaving a limited export surplus. Field trials in Turkey and Iran inform European breeding programs that are exploring high-oleic genetics for the safflower seeds market.

Competitive Landscape

Global crushers, including Archer Daniels Midland, Olam International Limited, Richardson International Limited, Cargill Incorporated, and Colorado Mills LLC, process safflower on shared lines alongside soy and sunflower, treating it as a rotational filler rather than a core business. This leaves premiums for regional specialists such as Gansu Yasheng Industrial Group, Shandong Bohi Industry, and Soni Safflower Agritech, which secure USD 8–50/kg prices by selling organic, high-oleic oil to cosmetics and nutraceutical buyers. The April 2025 Bunge-Repsol partnership embeds safflower in European renewable-diesel value chains, signaling incumbent interest when policy incentives align.

Kazakhstan and Russia lead production but lack branded downstream channels, exporting raw seed that Turkey refines into specialty oils. The technology focus shifts to blockchain traceability and precision agriculture, which document non-GMO status and carbon footprint, essential for premium buyers. Gene-edited high-oleic varieties promise to reduce farmer premiums, potentially increasing participation in the safflower seeds market.

Africa presents white-space potential: first movers willing to invest in cold-chain and testing labs can capture currently missing seed-to-oil spreads. Bunge’s forthcoming Destrehan, Louisiana multi-oil plant shows how flexible infrastructure could accommodate safflower if carbon-intensity metrics justify its inclusion.

Safflower Seeds Industry Leaders

Archer Daniels Midland Company

Cargill Incorporated

Olam International Limited

Richardson International Limited

Colorado Mills LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bunge Limited and Repsol announced a strategic partnership to deploy camelina and safflower as intermediate crops for renewable fuel production across European agricultural zones, leveraging the low-input agronomics of both oilseeds to meet the sustainability criteria of the Renewable Energy Directive without displacing primary food crops.

- October 2024: The Indian Union Cabinet approved the National Mission on Edible Oils - Oilseeds (NMEO-Oilseeds) to increase domestic oilseed production and reduce import dependency. The mission, with a budget allocation will operate from 2024-25 to 2030-31. NMEO-Oilseeds aims to enhance the production of primary oilseed crops including safflower, rapeseed-mustard, groundnut, soybean, sunflower, and sesamum. The mission also focuses on improving the collection and extraction efficiency from secondary sources such as cottonseed, rice bran, and tree-borne oils.

- June 2024: The Canadian government invested in Seed, including safflower seeds facilities, to support economic growth. The governments of Canada and Ontario are investing through the Sustainable Canadian Agricultural Partnership (Sustainable CAP) to enhance the Superior Plant Upgrading and Distribution (SPUD) Unit in New Liskeard. The SPUD Unit supports farmers and the wider agriculture and food industry by offering testing for plant diseases and providing a stock of healthy plants to commercial growers across the province.

Global Safflower Seeds Market Report Scope

Safflower is an annual plant belonging to the Asteraceae family, characterized by its herbaceous nature and thistle-like branched structure. As one of humanity's oldest cultivated crops, it is primarily grown commercially for its seed-derived vegetable oil. The global safflower market is segmented by geography. The report includes production, consumption, and trade analysis of the top safflower markets across the world. The report offers market size and forecast in terms of Value in (USD) and Volume in (metric tons) for all the segments mentioned above.

| North America | United States | Production Analysis |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Mexico | Production Analysis | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| South America | Argentina | Production Analysis |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Europe | Russia | Production Analysis |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Spain | Production Analysis | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Asia-Pacific | China | Production Analysis |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| India | Production Analysis | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Australia | Production Analysis | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Middle East | Turkey | Production Analysis |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Iran | Production Analysis | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Africa | Tanzania | Production Analysis |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Ethiopia | Production Analysis | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| By Geography | North America | United States | Production Analysis |

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Mexico | Production Analysis | ||

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| South America | Argentina | Production Analysis | |

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Europe | Russia | Production Analysis | |

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Spain | Production Analysis | ||

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Asia-Pacific | China | Production Analysis | |

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| India | Production Analysis | ||

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Australia | Production Analysis | ||

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Middle East | Turkey | Production Analysis | |

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Iran | Production Analysis | ||

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Africa | Tanzania | Production Analysis | |

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

| Ethiopia | Production Analysis | ||

| Consumption Analysis (Value and Volume) | |||

| Import Analysis (Value and Volume) | |||

| Export Analysis (Value and Volume) | |||

| Price Trend Analysis | |||

Key Questions Answered in the Report

What is the current value of the safflower seeds market?

The safflower seeds market size stands at USD 1.17 billion in 2026.

How fast is global demand growing?

Market value is forecast to rise at a 4.74% CAGR, reaching USD 1.48 billion by 2031.

Which region leads consumption?

Asia-Pacific holds 33.90% of 2025 value, driven by India and China.

Where is production expanding fastest?

Africa shows the highest growth pace at a 7.68% CAGR through 2031.

Why do processors pay premiums for high-oleic safflower?

High-oleic oil offers oxidative stability for cosmetics, biolubricants, and functional foods, justifying the pricing.

What limits further capacity investment?

High processing costs, acreage volatility, and competition from sunflower and canola restrain new crush projects.

Page last updated on: