Safety Syringes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

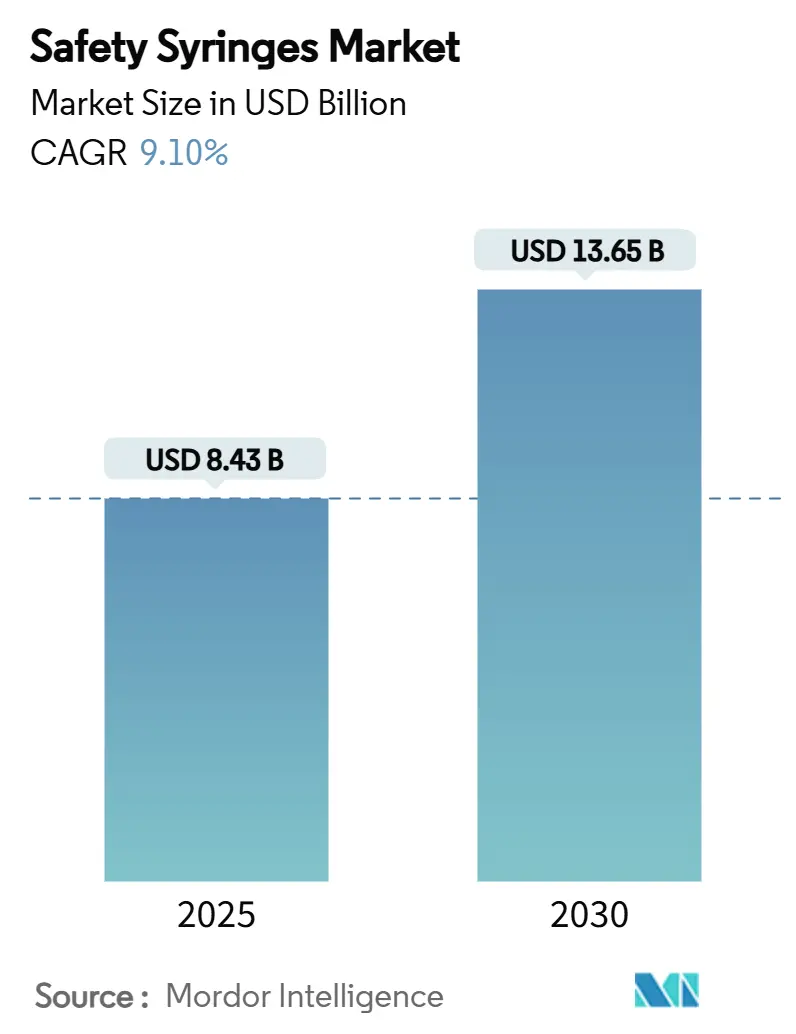

| Market Size (2025) | USD 8.43 Billion |

| Market Size (2030) | USD 13.65 Billion |

| Growth Rate (2025 - 2030) | 9.10% CAGR |

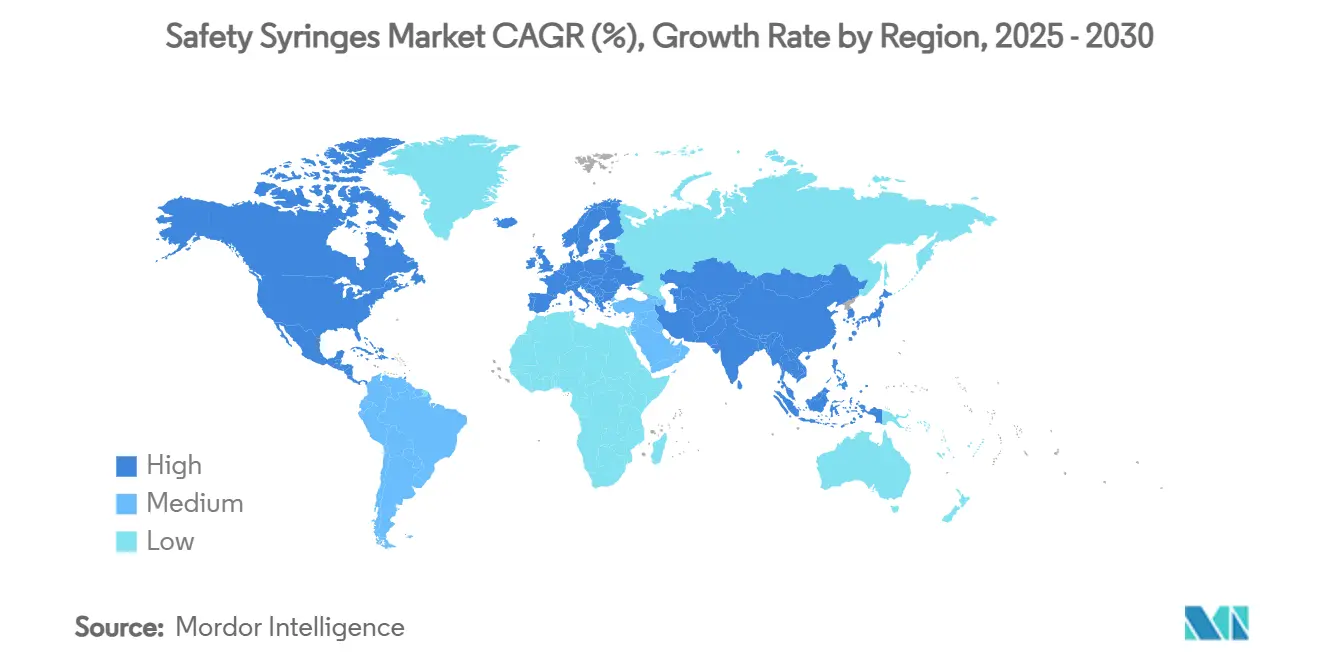

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Safety Syringes Market Analysis by Mordor Intelligence

The global safety syringes market size is USD 8.43 billion in 2025 and is forecast to climb to USD 13.65 billion by 2030, advancing at a 9.1% CAGR over the period. Firm demand is rooted in needle-stick-injury mandates, post-pandemic immunization capacity, and rapid biologics growth, each of which elevates purchasing volumes and reshapes device specifications across public and private healthcare channels. North America retains scale leadership through long-standing OSHA-aligned statutes, deep group-purchasing networks, and broad electronic traceability adoption, while Asia Pacific logs the fastest uptake as China, India, and ASEAN members harmonize procurement rules with ISO 23908 and WHO PQS st-001 guidelines. Hospitals order in bulk, yet rising home-based chronic-care pushes manufacturers toward small-case pack designs and intuitive locking triggers for self-injectors. Manual retractable formats continue to outsell all rivals, but automatic retraction captures share wherever nursing shortages, emergency departments, and biologic viscosity challenges raise the cost of activation failure. Supply-chain shocks in medical-grade polyolefins and FDA import alerts on Chinese barrels raise near-term cost volatility, but the medium-term outlook remains constructive as tier-one firms relocate production and qualify multiple resin suppliers.

Key Report Takeaways

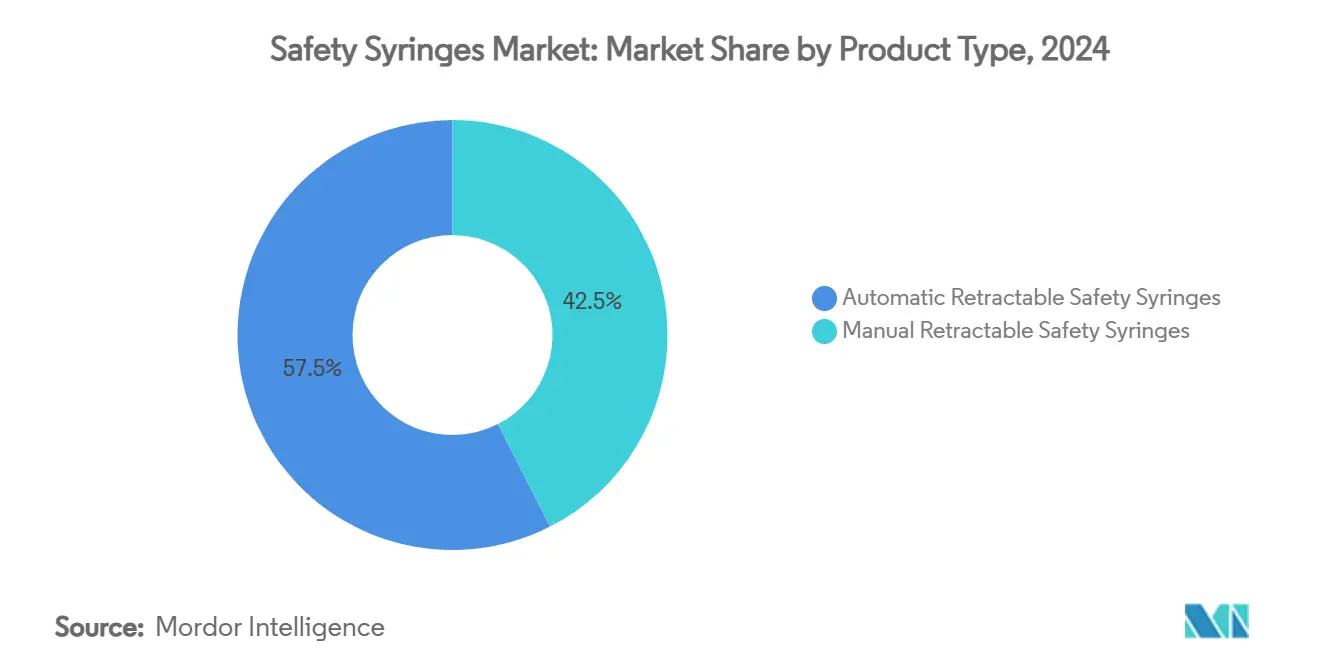

- By product type, manual retractable syringes accounted for 42.5% revenue share in 2024, while automatic retractable units are projected to expand at a 12.4% CAGR through 2030.

- By end-user, hospitals commanded 68.3% of the safety syringes market share in 2024; home-care and self-injection channels are forecast to grow at an 11.8% CAGR to 2030.

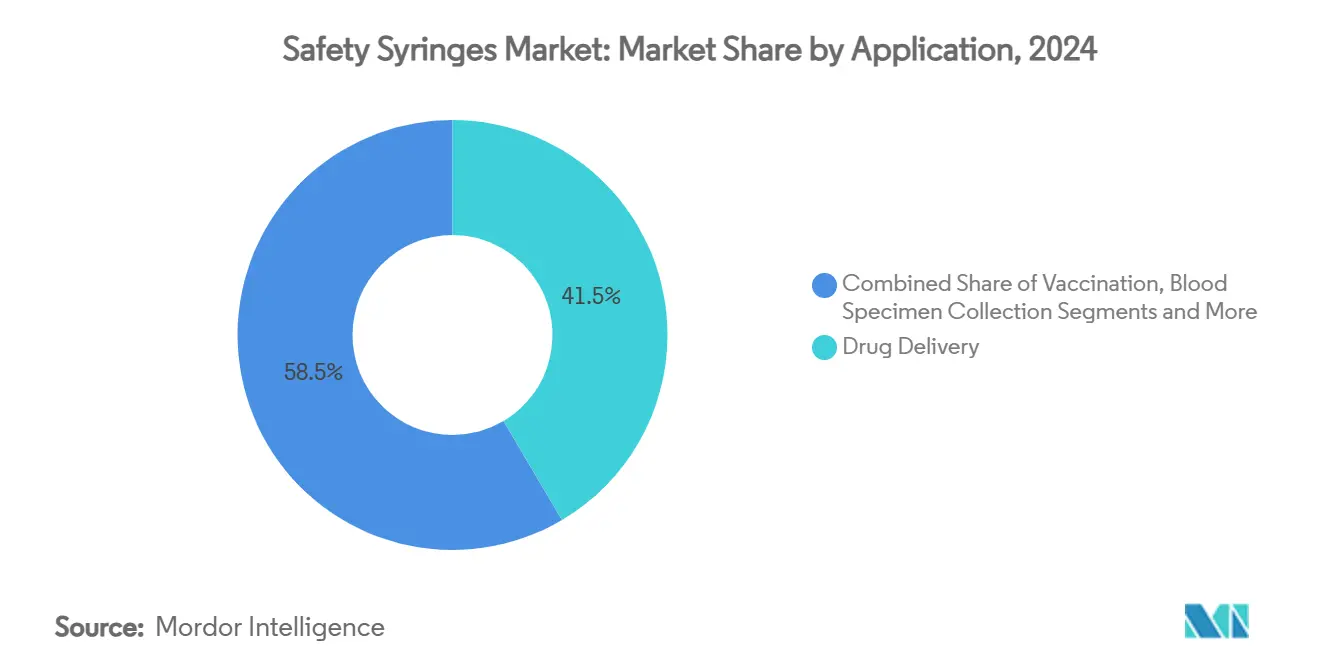

- By application, drug delivery led with 41.5% share of the safety syringes market size in 2024, and vaccination devices are advancing at a 13.5% CAGR through 2030.

- By geography, North America controlled 38.6% of revenue in 2024, while Asia Pacific logs the highest anticipated CAGR at 11.2% over 2025-2030.

Global Safety Syringes Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Needle-stick-injury legislation acceleration | +2.10% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Covid-era vaccine infrastructure repurposed for routine immunization | +1.80% | Global, particularly APAC & MEA | Short term (≤ 2 years) |

| Rapid expansion of biologics & GLP-1 injectables | +2.30% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Shift to home-based chronic-care (diabetes, RA) | +1.40% | Global, led by developed markets | Medium term (2-4 years) |

| Hospital ESG targets favour single-use safety devices | +0.90% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| AI-enabled smart syringes for auto-calibration & adherence | +0.70% | North America & EU early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Needle-Stick-Injury Legislation Acceleration

Regulators continue to tighten rules on sharps protection, with Massachusetts obliging hospitals to keep detailed injury logs and deploy engineered safeguards, while the UK Health and Safety Executive strengthens risk-assessment duties.[1]Massachusetts Department of Public Health, “Needlesticks and Other Sharps Injuries among Healthcare Workers,” mass.gov Hospital associations increasingly view liability exposure as a cost multiplier, spurring bulk conversion plans that cover everything from oncology suites to blood-gas labs. Emerging economies still experience high injury incidence, such as Ethiopia’s 40.5% rate among clinical staff, yet the gap itself catalyzes donor-funded tenders for safety syringes market expansion. Device makers answer with colour-coded activation cues, audible clicks, and passive shields to ensure compliance even under heavy workload. As post-incident legal settlements rise, procurement leaders prioritize automatic mechanisms despite higher list prices.

COVID-Era Vaccine Infrastructure Repurposed for Routine Immunization

The storage, cold-chain, and data-reporting networks built for SARS-CoV-2 inoculation are now embedded in seasonal flu, HPV, and pediatric schedules, creating predictable bulk orders for the safety syringes market.[2]Ankunda Collins et al., “Integrating COVID-19 vaccination into routine healthcare,” BMC Public Health, biomedcentral.com Countries that ran robust influenza programs showed higher COVID-19 throughput, proving infrastructure portability and influencing UNICEF tender specifications. Hospitals in Uganda demonstrated that standing vaccination pods could pivot to routine care while maintaining staff ratios, placing strain on manual retraction stock buffers but aligning well with automatic variants that cut training time. WHO’s Immunization Agenda 2030 encourages needle-free prototypes, yet until those gain scale, retractable safety syringes remain the default. Volume certainty from these programs lets manufacturers lower unit costs by lengthening production runs.

Rapid Expansion of Biologics & GLP-1 Injectables

GLP-1 agonists for metabolic disease and a growing slate of monoclonal antibodies drive a surge in prefillable glass syringes engineered for viscosities above 15 cP, spurring premium demand inside the safety syringes market. BD’s Neopak XtraFlow seven-fold capacity increase reflects clients’ push for ≥1 mL fill volumes and silicone-oil-reduced barrels that mitigate protein aggregation. Analysts calculate the United States could need 1 billion injections annually for obesity drugs by 2030, implying parallel growth in autoinjector fill-finish lines. Device teams also integrate RFID chips for cold-chain trace, satisfying both pharmacovigilance and anti-counterfeit goals. As biologic pipelines diversify, procurement teams stipulate pre-qualified safety features to streamline regulatory filings.

Shift To Home-Based Chronic-Care (Diabetes, RA)

Roughly 2 billion self-injections occur yearly in the United States for diabetes, allergies, and hormone therapies, turning the living room into the new med-surg unit. Patient ethnographies reveal that emotional stress and dexterity limits rank alongside needle phobia as barriers, so suppliers offer ergonomic grips, large rotation wings, and auto-disable locks. Training is often delivered by video, making visible activation indicators essential. Errors in insulin syringe use seen among Brazilian diabetics reinforce the need for clearer dose windows and audible plunger stops to reduce mis-dial incidence.[3]Santos Thaís et al., “Insulin Self-Administration Technique,” scielo.br Healthcare insurers reimburse devices bundled with cloud-linked adherence apps, opening a lane for AI-enabled smart syringes. Combined, these factors pull demand away from institutional purchase channels and broaden the safety syringes market footprint.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply bottlenecks in specialty medical-grade plastics | -1.60% | Global, acute in APAC hubs | Short term (≤ 2 years) |

| Unit-cost premium vs. conventional syringes in LICs | -1.20% | Sub-Saharan Africa most affected | Medium term (2-4 years) |

| Patent thickets around spring-retract designs | -0.80% | North America & EU | Long term (≥ 4 years) |

| Growing popularity of needle-free injectors | -0.90% | Developed markets first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Bottlenecks in Specialty Medical-Grade Plastics

Medical-grade polypropylene and cyclic olefin polymers remain tight after pandemic-era plant outages, forcing device firms to dual-source and pre-buy resin, which adds 15-25% to barrel costs. FDA import alerts on several Chinese syringe producers exposed brittle supply chains, prompting BD to invest USD 40 million in US barrel molding and tip grinding capacity. Engineering teams experiment with 3D-printed polyolefin filaments for validation runs, yet throughput limits keep them from mass production, especially for the safety syringes market, where annual volumes exceed 20 billion units. Until resin logistics normalize, manufacturers hold higher safety stock, tying up working capital.

Unit-Cost Premium Vs. Conventional Syringes In LICs

A standard safety model can cost twice a disposable conventional syringe, presenting tough trade-offs in low-income country budgets where vaccination per-dose economics dominate. Although needlestick injuries impose downstream treatment costs, those are borne by occupational health budgets rather than immunization line items, blurring accountability. Multilateral agencies mitigate the gap through pooled procurement but coverage remains uneven. Pilot studies in Malawi pegged overall Covid-19 delivery at USD 16.15 per dose when logistics and labour were counted, magnifying the visibility of device costs. Consequently, adoption moves in waves tied to donor grants rather than stable domestic finance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Manual Retractable Dominance Faces Automation Pressure

Manual retractable devices captured 42.5% of 2024 revenue, giving them the largest slice of the safety syringes market size—their cost advantage and minimal mechanism complexity suit high-volume vaccine drives and general ward medication rounds. Automatic retractable units post a 12.4% forecast CAGR, propelled by emergency departments and self-injection kits where consistent trigger activation is critical. Sliding-sleeve and sheathing-tube models serve specialties such as interventional cardiology, where clinicians require a clear line-of-sight to the bevel. Spring-powered patents create royalty obligations that consolidate production among license holders, yet emerging low-cost actuators promise to narrow the price delta and gradually shift volume toward automation. Clinical procurement panels increasingly weigh disposal ease, with auto-disable features preventing barrel reuse in low-resource settings, strengthening the segment’s appeal across global tenders. Combined, these trends ensure the product mix evolves but leave the overall safety syringes market resilient to competitive shifts.

Second-generation automation designs further cement demand by integrating RFID tags that record batch numbers directly into EHR systems. Pilot rollouts in US oncology centers shaved 12 seconds off average administration time, translating to staffing efficiencies that offset higher device costs. Should reimbursement formulas start valuing staff savings, automatic variants could accelerate their share gains beyond the current projection.

By End-User: Hospital Procurement Shifts Toward Decentralized Care

Hospital systems still represent 68.3% of unit volumes and maintain pricing leverage through long-term GPO contracts. That dominance placed hospitals at the center of recent antitrust scrutiny, with lawsuits alleging exclusive clauses inhibit smaller vendors’ access, a situation that ripples through the safety syringes market. Even so, home-care channels exhibit an 11.8% CAGR as insurers encourage self-administration for chronic therapies. Device packaging morphs accordingly: tamper-evident pouches ship in ten-count sleeves for retail pharmacies, and instruction leaflets carry QR codes linking to tutorial videos for patients. Ambulatory surgery centers present an intermediate niche, favoring compact trays that streamline turnover between cases. Diabetic clinics, where coaching on needle angle and depth is crucial, adopt colour-coded barrel gauges to curb dosing errors.

Furthermore, telehealth-enabled monitoring apps pair with connected plungers to push data to clinicians, thereby closing the loop on adherence without a clinic visit. This hybrid model dilutes the hospital share but expands the safety syringes market overall, because total injections rise when barriers to access fall.

By Application: Drug Delivery Leadership Challenged by Vaccination Surge

Drug delivery accounted for 41.5% of 2024 revenue and remains the anchor of the safety syringes market. High-viscosity biologics, hormone therapies, and long-acting antipsychotics all demand reliable passive safety at varying fill volumes. Prefillable glass barrels with fluoropolymer stoppers dominate this sub-segment, and leading suppliers invest heavily in oleophobic coatings that preserve protein integrity. Vaccination devices, however, post a 13.5% CAGR—more than double the overall market—thanks to Covid-19 infrastructure repurposing and expanded pediatric schedules. Mass campaigns value device interchangeability, pushing manufacturers to harmonize hub geometry and color codes across dose sizes, which in turn simplifies cross-training and inventory management.

Blood specimen collection syringes hold steady volume but shift toward safety-engineered transfer devices that cap needle exposure during tube exchange. Insulin administration maintains a large installed base, yet mounting competition from insulin pens and patch pumps keeps that slice of the safety syringes market share relatively flat. Looking forward, vaccine growth could overtake drug delivery in annual incremental volume by 2028 if current public-health funding levels persist.

Geography Analysis

North America generated 38.6% of 2024 revenue on the strength of OSHA compliance enforcement, a mature payer mix, and the world’s densest GPO networks. Safety-engineered standards have reached near-universal penetration, yet replacement cycles keep annual unit demand high as hospitals refresh stock to newer ISO 80369 Luer standards. FDA 510(k) pathways streamline line extensions; consequently, suppliers channel R&D into incremental trigger refinements and smart-label integration, rather than radical new forms. Canada tracks similar trends but lags the United States in smart-syringe pilots due to provincial procurement fragmentation.

Europe exhibits plateauing growth yet steady replacement demand as EU-wide device directives mandate unique device identifiers and life-cycle carbon reporting. Several university hospitals in Germany and the Nordics run pilot schemes with recyclable barrels, and national tenders increasingly allot scoring weight to environmental declarations. As a result, automatic retractable designs utilizing mono-material polypropylene barrels gain favor because they simplify recycling streams, which supports the broader safety syringes market transition.

Asia Pacific shows the fastest expansion with an 11.2% CAGR through 2030. China’s National Medical Products Administration codified safety-engineered requirements for tertiary hospitals, while India enforces injectable safety through Bureau of Indian Standards performance tests, both actions widening domestic demand. Urbanization and chronic disease burdens in Southeast Asia accelerate retail pharmacy uptake of self-injection kits. Japan’s aging population fuels high-viscosity biologic volumes, and local CDMOs collaborate with global syringe majors to ensure supply security. Despite currency swings, most countries earmark incremental health budgets for sharps-injury reduction, keeping regional growth on track. Latin America and the Middle East & Africa trail but show steady procurement gains as donor programs bundle safe-injection objectives with basic immunization funding.

Competitive Landscape

The safety syringes market displays high concentration, with BD holding a dominant share through expansive IP and long-term GPO contracts. The company’s recent USD 2.5 billion plan to renovate US assembly lines underscores its strategy to leverage domestic capacity as a differentiator amid FDA scrutiny of offshore barrels. Terumo, Nipro, and Retractable Technologies contest niches via patent carving and specialty coatings that minimize silicone oil migration. Antitrust cases accuse BD of bundling discounts that restrict hospital choice, and any court-mandated changes could open capacity windows for challengers.

Technological differentiation centers on retraction reliability, user ergonomics, and smart connectivity. Start-ups focus on AI-enabled dose capture, though they face scale barriers in glass barrel supply. Global manufacturers simultaneously pursue low-cost polypropylene conversions and premium RFID-tagged glass formats to cover the spectrum. Patent landscapes remain dense; however, some critical spring-retract protections expire after 2027, potentially lowering entry hurdles.

Strategic moves include Ypsomed’s partnership with BD to blend the Neopak XtraFlow syringe with the YpsoMate 2.25 autoinjector for biologics above 15 cP, expanding joint access to the obesity-drug device segment. Terumo widened contract-development offerings to biotech clients needing low-dead-space barrels, and Nipro secured a multiyear supply pact with a leading US pharmacy chain for home-use insulin kits. Capital allocations tilt toward domestic resin molding to reduce import-alert exposure. Overall, scale, patent leverage, and integrated service models remain decisive factors.

Safety Syringes Industry Leaders

Becton, Dickinson & Company

Terumo Corporation

Smiths Medical

B. Braun Melsungen AG

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BD invested USD 10 million to expand US capacity for safety-engineered syringes at Connecticut and Nebraska plants, boosting domestic safety syringe output by more than 40%.

- January 2025: BD highlighted the BD iDFill prefillable syringe with RFID and the Neopak XtraFlow platform at Pharmapack 2025.

- October 2024: BD and Ypsomed launched cooperation on high-viscosity autoinjectors to serve expanding GLP-1 pipelines.

- September 2024: BD commercially released the Neopak XtraFlow Glass Prefillable Syringe and expanded French capacity sevenfold to meet biologics demand.

Global Safety Syringes Market Report Scope

| Retractable | Manual Retractable Safety Syringes |

| Automatic Retractable Safety Syringes | |

| Non-retractable | Sliding Needle Cover Syringes |

| Sheathing Tube Syringes | |

| Hinged Needle Cover Syringes |

| Hospitals |

| Ambulatory Surgery Centres |

| Home-care / Self-Injection |

| Diabetic Clinics |

| Other Healthcare Settings |

| Drug Delivery |

| Vaccination |

| Blood Specimen Collection |

| Insulin Administration |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Retractable | Manual Retractable Safety Syringes |

| Automatic Retractable Safety Syringes | ||

| Non-retractable | Sliding Needle Cover Syringes | |

| Sheathing Tube Syringes | ||

| Hinged Needle Cover Syringes | ||

| By End-user | Hospitals | |

| Ambulatory Surgery Centres | ||

| Home-care / Self-Injection | ||

| Diabetic Clinics | ||

| Other Healthcare Settings | ||

| By Application | Drug Delivery | |

| Vaccination | ||

| Blood Specimen Collection | ||

| Insulin Administration | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global safety syringes market?

The market is worth USD 8.43 billion in 2025 and is set to reach USD 13.65 billion by 2030.

Which region leads in safety syringe revenue?

North America holds 38.6% of 2024 revenue, driven by stringent regulations and mature purchasing networks.

Which product type dominates the market?

Manual retractable syringes lead with 42.5% share in 2024, although automatic versions are growing fast.

How fast is the vaccination application segment growing?

Vaccination devices are projected to rise at a 13.5% CAGR through 2030 on the back of expanded immunization programs.

What factor most restricts adoption in low-income countries?

The unit-cost premium of safety models over conventional syringes remains a key barrier despite donor support.

Who is the largest player in the competitive landscape?

BD commands the largest share through extensive IP and multiyear group-purchasing agreements.

Page last updated on: