Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.12 Billion |

| Market Size (2026) | USD 5.24 Billion |

| Market Size (2031) | USD 5.86 Billion |

| Growth Rate (2026 - 2031) | 2.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Home Appliances Market Analysis by Mordor Intelligence

The Russia home appliance market size is expected to grow from USD 5.12 billion in 2025 to USD 5.24 billion in 2026 and is forecast to reach USD 5.86 billion by 2031 at 2.30% CAGR over 2026-2031. Steady income growth, a historic 7.20% poverty low, and continued ruble appreciation underpin unit demand even as consumers gravitate toward better-featured products. Parallel-import competition has trimmed average retail prices 10–20% without eroding manufacturer margins since brands quickly recalibrated sourcing and hedging strategies to protect profitability [1]Izvestia Staff, “Prices for household appliances in the Russian Federation decreased by 10–20%,” Izvestia, iz.ru. . Central Federal District continues to command roughly one-third of nationwide sales thanks to dense affluence and mature brick-and-mortar footprints, while Far-Eastern Federal District leads growth at a 7.18% CAGR on the back of large-scale infrastructure upgrades and resource-sector wage gains. Washing machines remain the volume mainstay with 28.22% share, but dishwashers post the fastest 8.77% CAGR as time-pressured urban households invest in convenience appliances. E-commerce penetration has accelerated to 53.10% of all units sold, helped by Ozon and Wildberries, whose 85% pickup-point dominance provides a decisive last-mile advantage across Russia’s vast sub-Arctic expanse. Technology adoption shows conventional formats holding 52.33% share in 2024; however, smart/connected appliances race ahead at a 20.29% CAGR, enabled by 90.40% household internet connectivity and increasingly attractive tariff savings under Russia’s new three-tier electricity pricing regime.

Key Report Takeaways

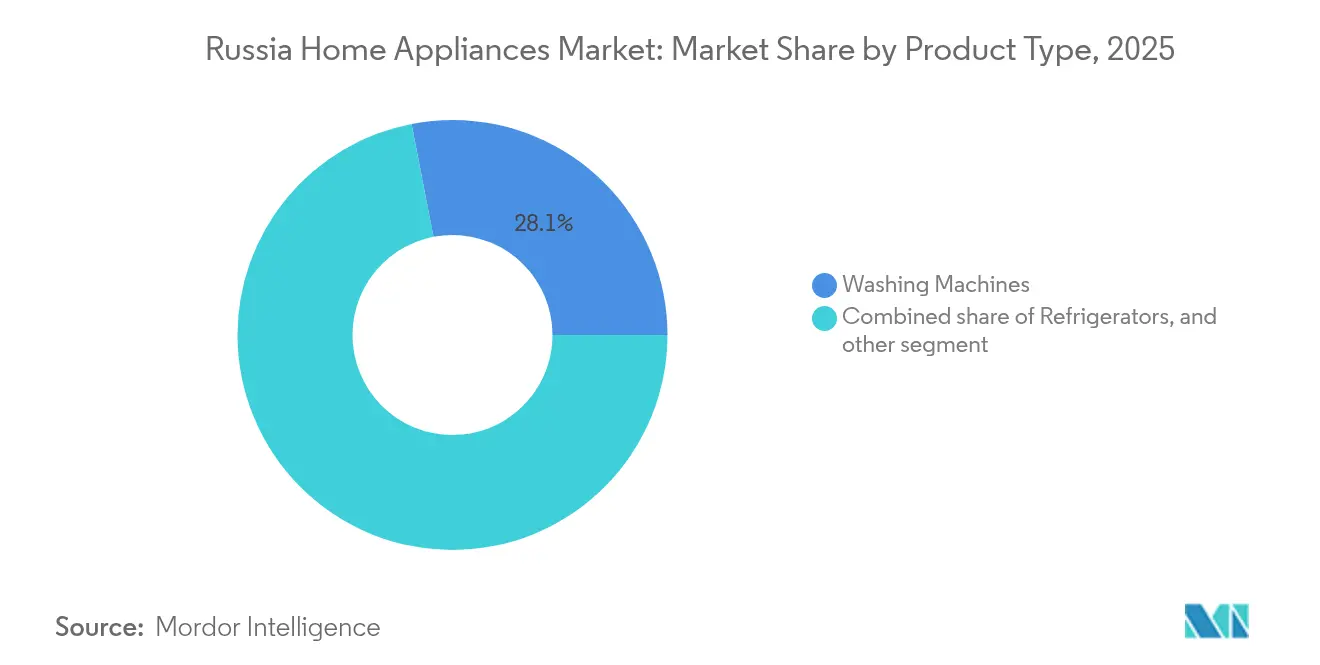

- By product type, washing machines led with 28.05% of the Russia home appliance market share in 2025; dishwashers are advancing at an 8.42% CAGR through 2031.

- By distribution channel, multi-branded stores retained 46.95% of the Russia home appliance market share in 2025, while e-commerce is growing at a 15.70% CAGR to 2031.

- By technology, conventional appliances captured 52.10% of the Russia home appliance market size in 2025; smart/connected models are projected to expand at a 19.35% CAGR between 2026-2031.

- By geography, the Central Federal District commanded a 32.10% share of the Russia home appliance market size in 2025, whereas the Far-Eastern Federal District is forecast to post the highest 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of Russian middle-class demand | +0.8% | Central FD, Northwestern FD, major metropolitan areas | Medium term (2-4 years) |

| Retailer-led financing schemes | +0.5% | National, with concentration in Central and Volga FDs | Short term (≤ 2 years) |

| Energy-tariff pressure boosting inverter uptake | +0.6% | National, particularly regions with higher electricity costs | Medium term (2-4 years) |

| E-commerce logistics maturation beyond Tier-1 cities | +0.7% | Siberian FD, Far-Eastern FD, Ural FD | Long term (≥ 4 years) |

| Government substitution programmes for imported white-goods | +0.4% | National, with manufacturing hubs in Central and Volga FDs | Long term (≥ 4 years) |

| Data-driven after-sales monetisation | +0.3% | Central FD, Northwestern FD, tech-enabled urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumisation of Russian middle-class demand

Elevated discretionary incomes and declining poverty spur households to trade up from entry-level to mid- and premium-grade appliances that promise durability and aesthetics [2]Consumer Analytics Team, “Consumer Trends in Russia 2025: How Russians Shop and Payment Habits,” Sberbank, sberbank.ru. . Coffee-machine unit sales rose 17% to 2.4 million during 2024 as urban consumers embraced café-style living at home, underscoring a willingness to pay more for experiential features. Moscow and St. Petersburg shoppers treat white goods as lifestyle markers, stimulating average ticket values even when ruble fluctuations inject price volatility. Premiumisation also benefits domestic makers able to reposition formerly mass products as locally engineered “smart” alternatives to departed Western brands. Consumers appear comfortable paying an 8% price uplift recorded during 2024, suggesting elasticity remains in positive territory for aspirational lines. Market entrants that pair streamlined online journeys with extended warranties have quickly built brand equity among status-conscious millennials. Altogether, premiumisation adds roughly 0.8% to forecast CAGR, mostly in metro districts where incomes exceed the national median.

Retailer-led financing schemes

Interest-free installment plans popularized by major chains and marketplaces unlock demand for big-ticket refrigerators and washer-dryer bundles that would otherwise strain household budgets. With 93 million active credit cards and average limits near 98,000 rubles, Russians increasingly view monthly repayments as a manageable alternative to full cash outlays. Yandex Market, Ozon, and regional chains now push one-click credit approvals that compress checkout friction to seconds, lifting conversion rates. Sales promotions repeatedly headline social media feeds, sustaining visibility while rewarding loyal viewers with instant coupon codes that reduce effective prices. Although consumer debt delinquencies have nudged higher, government policy still encourages household consumption by keeping benchmark rates below late-2010 peaks. Financing boosts replacement cycles, allowing retailers to seed future upgrades at end-of-term intervals. Short-term tailwind effect is calculated at +0.5% CAGR, though tightening credit standards could trim momentum after 2026.

Energy-tariff pressure boosting inverter uptake

From January 2025 Russia adopted tiered residential electricity bands starting at 1.106 rubles per kWh before climbing to 3.43 rubles for heavy users, sharply widening cost spreads for high-consumption households. Consumers respond by favoring inverter compressors and 5-star energy labels that promise 10–15% savings relative to fixed-speed motors [3]BIO Conference Committee, “Energy Efficiency Assessment in Smart Homes,” BIO-Web of Conferences, bio-conferences.org. . Demand spikes most in Far-Eastern districts where electric stoves dominate cooking duties because pipeline gas is scarce. Appliance makers now spotlight kilowatt efficiency in marketing materials and offer real-time consumption dashboards via smartphone apps. Retailers further nudge shoppers by bundling discounted smart plugs that track usage in rubles, translating abstract kilowatts into monthly bill impacts. Regulation cements the trend; GOST standards place stricter limits on allowable standby losses, forcing hold-out manufacturers to re-engineer legacy models. Resulting uptake adds roughly 0.6% to sector CAGR through mid-term horizons.

E-commerce logistics maturation beyond Tier-1 cities

Expansion of pickup lockers and partner-run issue points from Kaliningrad to Kamchatka compresses last-mile expenses once viewed as prohibitive. Ozon and Wildberries collectively operate 95,000 locations and now deliver bulky appliances within three days to most Siberian postcodes, a timeline unimaginable two years ago. Their partner income jumped 97% and 70% respectively in 2024, proving the viability of asset-light franchise models. Improved roads, rail-hub automation, and dedicated cold-weather SOPs ensure refrigerators remain within safe tilt angles and temperature windows en route to Arctic towns. Consumers welcome the choice: online revenue share for appliances climbed to 16.50% in 2024 and continues to outpace offline channels. Logistics density also reduces return times, building trust that faulty units receive swift swaps rather than lengthy repairs. Long-run impact is estimated at +0.7% CAGR as digital participation spreads across lower-tier urban clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ruble volatility on imported components | −0.9% | Assembly hubs in Central & Volga | Short term (≤ 2 years) |

| Skilled-labor shortage in local assembly | −0.6% | Factory clusters countrywide | Medium term (2 – 4 years) |

| Sanctions limiting access to Western technologies and components | -0.7% | National, with higher impact on premium and smart appliance segments | Medium term (2-4 years) |

| Declining consumer purchasing power impacting mid-to-premium segments | -0.5% | Urban and semi-urban areas | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Ruble volatility on imported components

Although the stronger ruble briefly lowered shelf prices early 2025, currency swings keep component procurement a guessing game for plants still reliant on compressors, sensors, and chips sourced from Asia and Europe. Import licenses introduced in late-2024 for refrigerant-containing goods complicate planning by layering legal reviews onto already jittery FX exposures. Manufacturers with hedging desks can offset spot moves, but smaller brands are forced into just-in-time buying at whatever rate prevails that week. Frequent MSRP adjustments confuse shoppers and dampen promotion effectiveness, causing demand spikes to dissipate faster than historical patterns. Parallel-import corridors offer temporary relief yet remain at risk of new Eurasian Economic Union crackdowns that raise fines for improper customs codes. Thus, ruble volatility slices an estimated 0.9% from forecast CAGR during the near term. If domestic substitution of imported parts accelerates, drag could ease post-2027.

Skilled-labor shortage in local assembly

National unemployment fell to a record-low 3.30% in 2024, intensifying competition for technicians versed in mechatronics, robotics maintenance, and precision soldering. Defense contractors lure staff with wages triple regional factory averages, leaving appliance lines scrambling to backfill shifts. Government targets doubling the industrial automation market to 207 billion rubles by 2030, yet capital scarcity and skills gaps slow the adoption of fully unmanned assembly cells. Leading brands now co-fund vocational programs, but curriculum lag means graduates fit entry-level roles rather than complex quality-control posts. Productivity bottlenecks already delay peak-season shipments, prompting distributors to stockpile inventories months ahead at extra warehouse cost. Medium-term CAGR impact is assessed at –0.6% until training pipelines stabilize and automation capex spreads beyond pilot cells in Moscow Oblast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functionality Drives Core Segments while Lifestyle Appliances Accelerate

In 2025 washing machines held 28.05% of overall sales, underscoring their status as indispensable fixtures in Russian homes. Domestic production gives the segment a pricing buffer because localized labor and shorter supply lines mute the pass-through of ruble fluctuations to retail tags. Refrigerators captured a 19.35% slice as state import-substitution schemes incentivized manufacturers to source compressors locally and thereby bolster the Russia home appliance market size for cold-chain categories. Dishwashers, at 8.42% CAGR, demonstrate how urban lifestyle shifts favor products that reclaim time in smaller kitchens-a trend magnified in Moscow’s new-build apartments that average just 38 square meters. Microwave ovens scored unit growth of 7.7%, lifted by ready-meal adoption among single-person households that now comprise one-quarter of big-city dwellers . Air-conditioners are exhibiting stable double-digit revenue expansion in southern regions where summer heatwaves linger longer each year. Coffee-machine demand echoes the premiumisation motive, with espresso systems marketed as aspirational upgrades to everyday routines.

Lifecycle economics reveal that washer ownership approaches market saturation, yet replacement cycles shorten to roughly 6.5 years as financing and higher incomes encourage earlier swaps for quieter or larger-capacity models. The Russia home appliance market share associated with dishwashers still trails mature European peers, signaling white-space potential once kitchen designers standardize 600-millimeter niches during apartment retrofits. Upright freezer and wine-cooler micro-segments post niche yet accelerating numbers, supported by gourmet food habits and a nascent domestic wine movement in Krasnodar Krai. Cross-selling opportunities emerge because 42% of households that upgrade a refrigerator within 12 months also purchase either a blender or juicer, illustrating bundled shopping behavior. Manufacturers that integrate antimicrobial linings and rapid-cool drawers win loyalty among nutrition-focused consumers. Extended warranties bundled with premium lines anchor brand reputation while generating data for predictive maintenance upsells. Overall, product-innovation cadence is fast enough that SKU obsolescence drives natural demand rotation even in flat population scenarios.

By Distribution Channel: Digital Channels Reshape Shopper Decision Journeys

Multi-branded stores ended 2025 with 46.95% sales, evidence that Russian shoppers still value tactile product trials before committing to high-ASP appliances. Nevertheless, e-commerce leapt to over half of all unit volume after booking a 15.70% CAGR, an inflection that permanently alters the Russia home appliance market structure. Ozon and Wildberries influence extends beyond Moscow; their combined pickup network covers 85% of issue points nationwide and gives rural customers reliable access to large white goods. Specialty chains preserved a 17.85% stake by emphasizing curated premium assortments, certified installers, and in-house technicians able to tackle warranty calls within two hours in top ten cities. Smaller direct-to-consumer labels lean on social-commerce livestreams where influencers demo smart-kettle voice control and generate impulse buys via limited coupons. Installment financing embedded during online checkout boosts average basket values by 32%, supporting the Russia home appliance market size expansion despite unit price deflation. Return logistics technology, including AI triage that labels cosmetic damage, reduces reverse-flow costs and further improves digital economics.

Store footprints are also evolving as chains convert prime mall locations into “experience centers” showcasing smart-home ecosystems that cross-link refrigerators, lighting, and voice assistants. Conventional outlets invest in narrow-aisle robotics to cut restock time and free associates for consultative selling. Meanwhile, marketplaces build regional sorting hubs fitted with low-temperature staging rooms enabling safe transfer of refrigerants under new licensing rules. Omnichannel strategies converge as offline giants integrate same-day click-and-collect while e-commerce leaders test showroom kiosks inside public-transit hubs. Customer acquisition costs remain lower online, yet last-mile subsidies erode net margins unless offset by advertising revenue from banner placements on listing pages. Brands must therefore balance channel mix carefully to safeguard profitability while maximizing reach. Over 46% of Russian consumers declare willingness to switch appliance brands if loyalty perks or faster shipping options appear, illustrating fluid buyer allegiances in this rapidly digitizing arena.

By Technology: Connectivity, Efficiency, and Familiarity Coexist

Conventional designs generated 52.10% of 2025 revenue, confirming enduring trust in tried-and-tested form factors across large swathes of the population. Energy-efficient variants already account for 29.60%, buoyed by stepped electricity tariffs that sharpen payback calculations on inverter adopters. Smart/connected models expand at a 19.35% CAGR, though their Russia home appliance market size remains lower in absolute terms owing to price premiums and patchy broadband outside city centers. Manufacturers address coverage gaps by integrating dual Wi-Fi and LoRa modules that maintain connectivity even at fringe signal strength. Basic app functionality such as delayed-start washers adds convenience without overwhelming first-time users. Energy-monitor dashboards resonate with environmentally minded millennials, boosting perceived value and nudging households toward higher-margin SKUs. Regulatory frameworks, such as GOST 2025 revisions, now require standby power below 0.3 watts, accelerating the turnover of aging models.

Despite favorable growth, just 30% of organizations offer advanced IoT capabilities, underscoring an innovation gap that domestic brands can exploit by partnering with Russian cloud providers to ensure data-sovereignty compliance. Integration of Yandex’s Alice voice assistant into air-purifier controls exemplifies local ecosystem advantages, fostering network effects that non-resident brands struggle to replicate. Battery-backup modules in smart ranges guarantee safe shutdown during Siberian winter outages, solving pain points unique to Russia’s grid. Retrofittable sensor kits offer a budget pathway into connected living, appealing to cost-conscious households wary of full appliance replacement. AI-driven predictive diagnostics help service centers pre-order parts, shortening repair windows and elevating customer satisfaction. The technology stack hence evolves along dual tracks: cost-down efficiency for mainstream buyers and cloud-enhanced experiences for early adopters. Over the forecast horizon these lanes will converge, gradually eroding the conventional category’s share as connectivity becomes table stakes rather than a premium upsell.

Geography Analysis

Central Federal District controlled 32.10% of 2025 turnover, anchored by Moscow’s outsized GDP per capita and dense retail ecosystems. Proximity to production lines reduces freight costs and enables two-hour repair commitments that appeal to premium buyers. Northwestern Federal District contributed 14.75%, leveraging St. Petersburg’s historical manufacturing base-despite BSH Hausgeräte halting operations, legacy capacity still supports contract runs for domestic badges Volga Federal District’s 12.55% share reflects its role as a logistics cross-road and home to Haier’s Naberezhnye Chelny complex, a plant increasingly vital for international export ambitions. Siberian and Ural districts illustrate the transformative power of e-commerce; shipment tracking data show average delivery times falling 40% in two years thanks to cross-dock hubs near Novosibirsk. Southern and North Caucasus territories combine for 9.15% but outpace national averages in refrigerator uptake due to hotter summers and agrarian cold-chain needs.

Far-Eastern Federal District, though currently below 5.85% share, will outstrip all peers at a projected 6.90% CAGR as government infrastructure grants and Pacific trade ties funnel disposable income into household upgrades. Port-linked free-trade zones lower import duty on components shipped from China, enabling competitive assembly lines in Khabarovsk Territory. Consumer behavior surveys reveal island settlements prioritize durability over brand cachet, propelling domestic labels that offer ruggedized circuit boards. Renewable-energy micro-grids emerging across Sakhalin encourage off-grid appliance designs with wider voltage tolerances. Inter-district variations in electricity tariffs further shape product mixes; households in grid-constrained zones adopt solar-ready induction cooktops, while gas-rich Volga opts for high-capacity electric ovens where gas infrastructure overlaps cannot meet peak demand. Collectively, Russia’s seven federal districts reinforce how geographic breadth, resource endowments, and policy incentives weave a nuanced mosaic across the Russia home appliance market.

Regulatory Landscape

Home appliances placed on the Russian market are governed primarily by Eurasian Economic Union (EAEU) technical regulations and related conformity assessment, notably TR CU 004/2011 (low-voltage equipment safety), TR CU 020/2011 (electromagnetic compatibility), TR EAEU 037/2016 (restriction of hazardous substances), and energy-efficiency requirements under the EAEU framework. Market access typically requires an EAC certificate or declaration of conformity issued via accredited bodies, with Rosstandart overseeing Russia's national standardization system (including GOST/IEC alignment) that underpins testing methods and labeling expectations for categories such as major white goods and small appliances.

In 2026, compliance and import administration remained a moving piece for vendors relying on cross-border flows. A Government of the Russian Federation decree dated April 23, 2026 (Decree No. 455) updated the list of products subject to mandatory certification, with an effective date of September 1, 2026, reinforcing the need for SKU-level document control when assortments change. In parallel, Minpromtorg confirmed on May 28, 2026 that the updated parallel-import list that entered into force on May 27, 2026 would be kept stable in the near term while it processes business applications, which affects the availability of foreign-branded appliances supplied through authorized parallel channels.

Value Chain Analysis

The Russia home appliances value chain spans upstream components (compressors, motors, plastics, electronics and sensors), assembly and OEM/ODM manufacturing, certification and compliance (EAC/TR EAEU documentation), and then distribution through multi-branded retail, specialty chains, and marketplaces. Sanctions and payment frictions have reshaped sourcing toward Asian corridors and domestic substitution efforts, while parallel imports have become a structural supply mechanism for maintaining foreign-brand availability. In-country manufacturing and assembly remain strategically important in major appliances, reflected in localized production activity such as LG resuming operations at its Ruza facility for washing machines and refrigerators using available inventories and materials.

Midstream constraints have concentrated around component availability, notably electronics, along with longer transit times and higher logistics and financing costs. These pressures are especially punitive for domestic brands that depend on contract manufacturing in China and therefore must carry greater buffer inventory to protect service levels. Downstream, the chain has tilted toward digitally driven sell-through and fulfillment, with marketplaces using dense pickup-point networks to reduce last-mile costs and extend bulky-appliance delivery coverage beyond Tier-1 cities. Overall, compliance documentation, import routing, and last-mile capability increasingly shape assortment breadth and speed-to-shelf alongside traditional factors such as brand and pricing.

Competitive Landscape

The Russia home appliance market is moderately concentrated, with the top players accounting for a significant portion of 2024 sales. LG Electronics holds the leading position, having navigated sanctions by partially restarting production of washers and refrigerators at its Moscow facility after obtaining updated product certifications. Samsung’s market presence remains uncertain; while marketing activities have resumed, full-scale production is on hold pending clearer guidance on sanctions. BSH Hausgeräte continues to maintain a strong foothold despite halting operations in St. Petersburg, supported by a steady flow of imported inventory through authorized distributors. Haier benefits from local manufacturing in Naberezhnye Chelny, which helps protect margins from currency volatility. Meanwhile, domestic brands like Polaris, Vitek, and Kitfort have collectively strengthened local market share, capitalizing on patriotic consumer sentiment and flexible supply chains to fill the void left by departing Western brands.

Strategic playbooks pivot around localization depth, component self-reliance, and digital consumer touchpoints. Haier has earmarked incremental capex to double compressor output, counteracting vulnerability to Eurasian license regimes on refrigerants. LG embeds AI-based predictive maintenance apps to lock users into brand ecosystems long after warranty expiry, generating recurring filter and detergent revenues. Samsung considers contract manufacturing through third-party Russian partners, allowing brand presence without direct capex exposure. Parallel-import rules remain in flux; firms with robust compliance software mitigate seizure risks, protecting channel throughput when enforcement tightens. Industrial automation innovations—including collaborative robots and machine-vision QA benches—drive OEE gains, an imperative as wage inflation from labor scarcity escalates operating costs. Sustainability credentials matter, too; brands that switch to R600a refrigerants and 100% recyclable packaging resonate with eco-aware millennials increasingly vocal on Russian social media. Long-run competitiveness is therefore tied to a multifaceted matrix of cost, compliance, technology, and brand narrative.

M&A chatter centers on domestic conglomerates eyeing foreign divestitures of Russian assets, a dynamic that could redistribute market power if completed. Start-ups in the smart-appliance niche receive seed funding from sovereign technology funds, hinting at future category fragmentation. Yet barriers to scale—GOST conformity testing and TR EAEU approvals—temper overnight disruptions, favoring incumbents that possess accredited labs and regulatory muscle. After-sales monetization emerges as a white space; only 18% of installed smart appliances currently connect to OEM service clouds, indicating latent subscription revenue untapped. E-commerce platforms also morph into quasi-media entities, selling sponsored keyword placements that smaller brands use to level visibility against giants. Industry consensus predicts that by 2030 domestic players’ combined share could top 45% if localization incentives persist, potentially altering supply-chain bargaining power in favor of Russian component suppliers. In that scenario, technology partnerships with local semiconductor fabs would become the next strategic frontier.

Russia Home Appliances Industry Leaders

LG Electronics

Samsung Electronics

BSH Hausgeräte (Bosch–Siemens)

Haier Group

Whirlpool (Indesit)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localization of major-appliance manufacturing and critical subcomponents is a concrete whitespace as brands seek to reduce exposure to import routing, payment friction, and certification lead times. Evidence of this push includes production ramp activity at the former Bosch facility in Strelna under Gazprom Household Systems, which reported output of more than 30,000 refrigerators from May 2025 to March 2026, alongside stated plans to lift volumes further. Onshore capacity like this also supports adjacent opportunities in compressor and motor supply, local tooling, and certified test-lab services aligned to EAEU requirements, particularly for cold-chain appliances where cost structure and serviceability influence purchase decisions.

Retail-led supply-chain diversification and cross-border procurement platforms also create near-term operating opportunities in assortment continuity, refurbishment, and warranty-backed after-sales. M.Video's April 2026 launch of a cross-border trade division sourcing from markets such as China, Hong Kong, and the UAE illustrates how large retailers are formalizing procurement to stabilize availability under parallel-import conditions. Announced full-cycle manufacturing investment plans, such as Regiontransneft's July 2026 plan for a Moscow-region plant for home appliances and computer equipment, further point to demand for localized supplier ecosystems, certified installers, spare-parts hubs, and data-driven service models for connected and energy-efficient appliances.

Recent Industry Developments

- July 2026: Regiontransneft announced plans to build a full-cycle home appliance and computer equipment plant in the Moscow region with a stated initial investment of about USD 400 million. The announcement reflected active interest in deeper localization, which can shift competitive dynamics by expanding domestic manufacturing capacity and pulling in local component and service ecosystems.

- May 2026: LG Electronics filed multiple trademark applications with Rospatent in Russia covering key product and technology marks, including OLED, QNED, and AI-related lines. Protecting IP and brand identifiers supports continued commercialization via partners and parallel-import channels and reduces counterfeiting risk in a market with fluid brand availability.

- October 2024: Russia's Ministry of Natural Resources introduced licensing requirements for importing refrigerators and air conditioners containing refrigerants. The measure added administrative steps to cross-border supply for major white goods categories, increasing the importance of compliant documentation, importer capability, and retailer logistics planning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Russia home appliances market is defined as the value (USD) of household appliance sales within Russia across major appliances and small appliances, tracked through common retail and online channels.

Scope exclusions: We do not count after-sales services, installation labor, extended warranties, spare parts, or resale of used appliances as part of the market value.

Segmentation Overview

- By Product Type

- Major Home Appliances

- Refrigerators

- Freezers

- Dishwashing Machines

- Washing Machines

- Ovens

- Air Conditioners

- Other Major Products (Electric Hobs, Ranges, etc.)

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Toasters

- Vacuum Cleaners

- Juicers & Blenders

- Other Small Appliances (Waffle Makers, Egg Cookers, Air Fryers, Kettles, etc.)

- Major Home Appliances

- By Distribution Channel

- Multi-Branded Stores

- Specialty Stores

- E-Commerce

- Other Distribution Channels

- By Technology

- Smart / Connected Appliances

- Energy-Efficient (? 5-Star, Inverter) Appliances

- Conventional Appliances

- By Geography

- Central Federal District

- Volga Federal District

- Siberian Federal District

- Northwestern Federal District

- Southern & North Caucasus Districts

- Ural Federal District

- Far-Eastern Federal District

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the historical context, and put realistic ranges around unit shipments, pricing, and consumer demand shifts inside Russia. We mainly reviewed public statistics and policy materials to understand household formation, disposable income trends, inflation, and trade flows, which then helped structure assumptions on appliance replacement cycles and mix changes.

Sources used include official trade and customs statistics, central bank and national statistics releases, energy efficiency and labeling rules from regulators, and import duty and standards documentation. We also reviewed company annual reports and investor presentations, major retailer disclosures, trade association updates, and trusted press coverage for channel and product trend signals. In addition, paid database subscriptions were used selectively for company financials and intelligence, news and financials, and shipment-level import and export checks where public series were not granular enough. These sources are illustrative only, and many other references were used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with appliance brands, distributors, retail channel leaders, and industry experts who track demand in core Russian federal districts. These conversations were used to confirm product mix shifts (major versus small appliances), realistic pricing moves under ruble volatility, and channel splits between offline retail and e-commerce, and then to stress-test assumptions coming from desk research.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 44% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 37% |

| Smaller Players: 17% | Managers: 46% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where trade flows, local production signals, and channel demand indicators were used to reconstruct the annual sales pool for home appliances in Russia, and then split into major and small appliances in value terms. The totals were then checked with selective bottom-up approximations, such as sampled average selling price ranges by product group multiplied by estimated unit volumes from channel checks, which helped correct any overstatement coming from single-source assumptions.

Inputs that mattered in this market included import and export direction for appliance categories, ruble movement and consumer price inflation, household replacement timing for core appliance types, share shift toward e-commerce, and changes in availability that influence mix and pricing. When gaps appeared in unit signals for a specific product group, we used conservative ranges validated in interviews and kept the adjustment logic consistent across years.

For forecasting, scenario analysis was used so that demand recovery, price progression, and trade normalization could be flexed without breaking the underlying model. Assumption paths were aligned to what experts expect for retail demand, availability, and pricing behavior, and then the final growth curve was smoothed so year-to-year moves stayed explainable on a client call.

Data Validation & Update Cycle

Validation was handled through triangulation across independent signals, and then through variance checks at each major model step, including channel splits, pricing, and year-over-year growth. If an output moved outside the expected band, we revisited the assumption, checked it against desk indicators, and re-contacted interviewees when the reason was not clear.

Before sign-off, the model and write-up go through multi-step analyst reviews so calculation logic, units, and currency handling are consistent. Reports are refreshed annually, and interim updates are made when material events affect demand, trade, or pricing. Right before delivery, a final pass is completed so clients receive the latest updated view rather than an older draft.

Mordor Intelligence's Russia Home Appliances Market Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for Russia home appliances because each publisher draws the boundary differently and then applies its own price and currency assumptions. Differences also come from whether the estimate is built from trade and supply signals versus consumer spending totals, and from how quickly major market events are reflected in the latest year.

By tracking import and production direction, refreshing ruble-to-USD conversion timing, and separating appliance revenue from adjacent consumer electronics, Mordor Intelligence keeps the estimate tied to an appliances-only demand pool rather than a broader retail basket.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.24 B (2026) | |

| Industry Publisher A | USD 15.20 B (2025) | This estimate appears to use a wider revenue scope that can behave like consumer spending totals and may include a broader set of categories, which lifts the total versus an appliances-only model. Timing choices for currency conversion and price escalation can also expand the reported USD value in high-inflation years. |

| Industry Publisher B | USD 15.72 B (2024) | The number is materially higher, which is consistent with a household appliances definition that may bundle smart home or adjacent device categories and apply aggressive growth and pricing assumptions. Limited visibility into trade and availability checks can also cause the value pool to be overstated when supply constraints are present. |

Looking at the spread, the main drivers are category boundary, currency timing, and how pricing is stepped forward during volatile periods. Our approach stays easier to audit because it is built from a clear appliances scope and repeatable checks that link value back to observable demand and supply signals.

Key Questions Answered in the Report

What is the current value of the Russia home appliance market in 2026?

The market is valued at USD 5.24 billion in 2026 and is forecast to reach USD 5.86 billion by 2031.

Which product category holds the largest share within Russian households?

Washing machines lead with a 28.05% share, driven by domestic assembly and habitual replacement cycles.

How fast is the smart-appliance segment expanding?

Smart and connected models are growing at a robust 19.35% CAGR as internet penetration tops 90% of households.

Which region is projected to grow fastest through 2031?

The Far-Eastern Federal District is expected to post a 6.90% CAGR, benefiting from infrastructure spending and resource-sector incomes.

How are new electricity tariffs influencing appliance choices?

Tiered pricing introduced in 2025 incentivizes households to adopt inverter and 5-star rated devices that cut energy bills by up to 15%.

Page last updated on: