Silicon Carbide Fiber Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

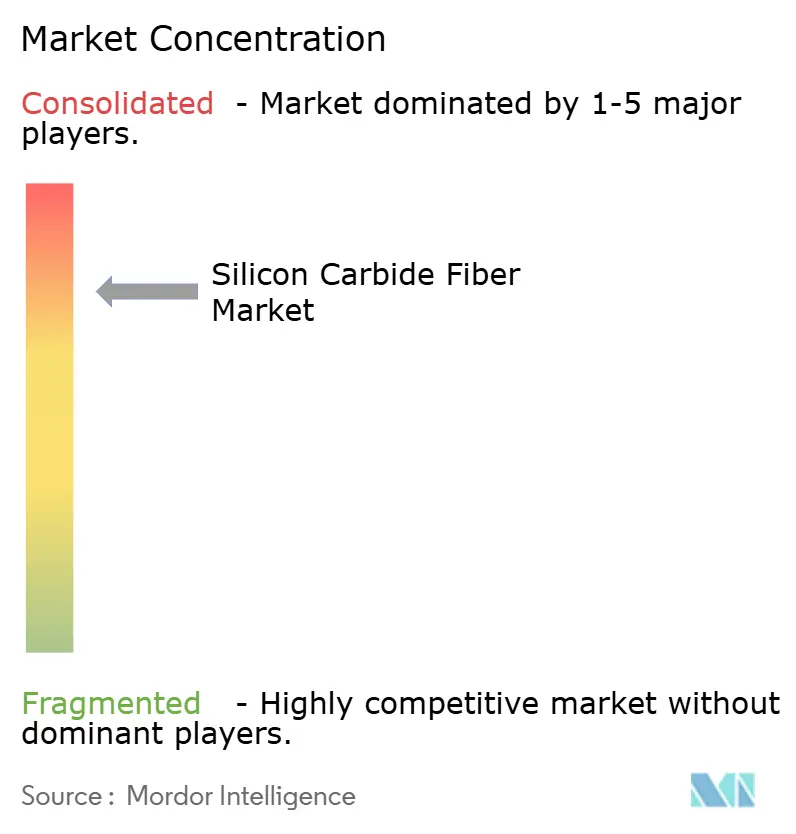

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicon Carbide Fiber Market Analysis by Mordor Intelligence

The Silicon Carbide Fiber Market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.12 billion in 2026 to reach USD 1.66 billion by 2031, at a CAGR of 8.09% during the forecast period (2026-2031). Surging adoption of ceramic-matrix composites (CMCs) in next-generation gas-turbine engines, rising demand for high-temperature accident-tolerant nuclear fuel cladding, and rapid progress in electric-mobility thermal-protection systems collectively underpin growth. Continuous fibers dominate structural applications because they preserve tensile strength above 2.8 GPa at 1,600 °C, enabling aerospace engine components to run 250 °C hotter than legacy super-alloys without weight penalties. Woven cloth preforms further accelerate uptake by simplifying lay-up of 3-D reinforcement architectures. Regionally, North America benefits from the first commercial-scale fiber plants in Huntsville, while Asia-Pacific captures the fastest growth as Japanese, South Korean, and Chinese programs scale Polycarbosilane-derived technologies. Competitive intensity centers on proprietary processing know-how rather than volume capacity, causing price points to remain above cost-sensitive thresholds despite incremental cost-down initiatives.

Key Report Takeaways

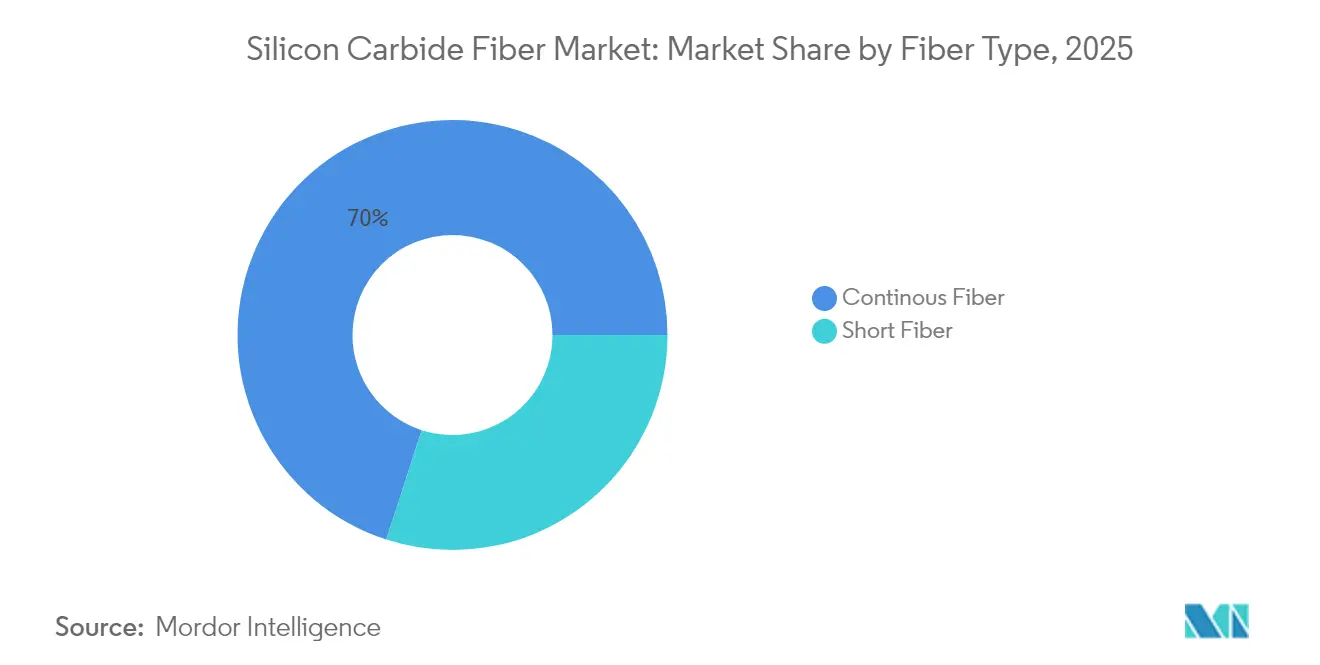

- By fiber type, continuous fiber held 70.02% of the silicon carbide fiber market share in 2025 and is projected to post an 8.63% CAGR through 2031.

- By form, woven cloth preforms accounted for 56.10% of the silicon carbide fiber market size in 2025, while the segment is forecast to expand at an 8.44% CAGR to 2031.

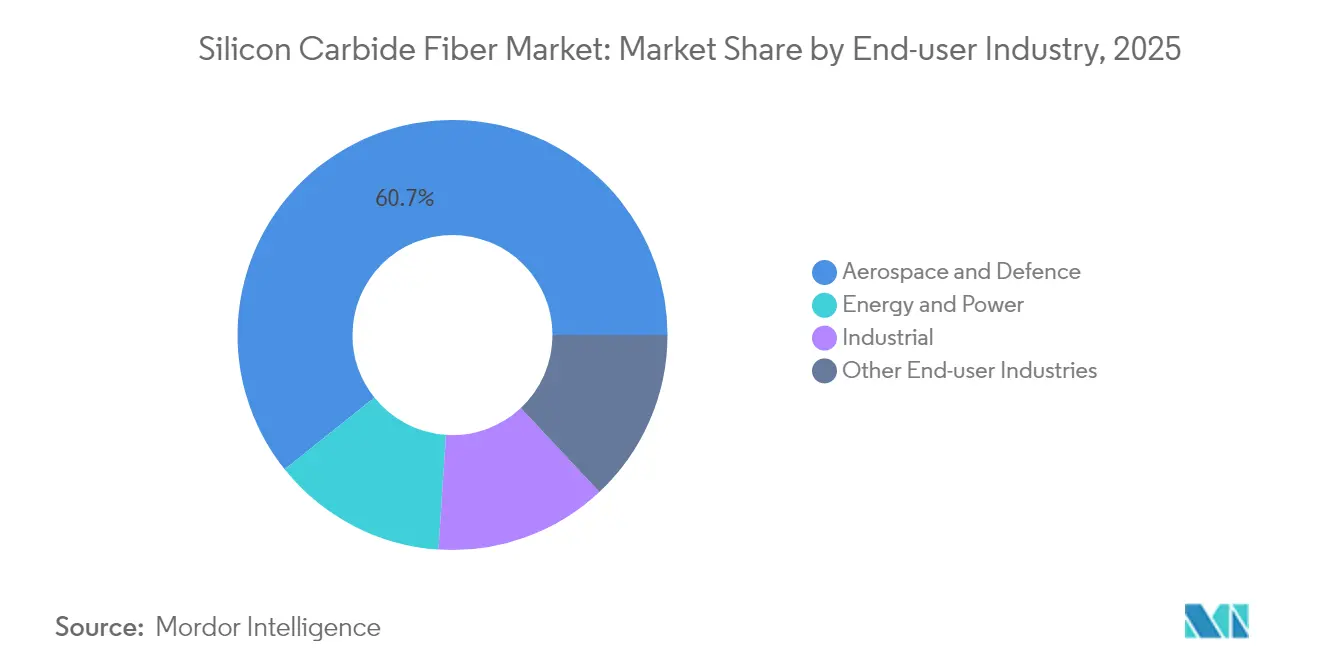

- By end-user industry, aerospace and defense represented 60.74% of the silicon carbide fiber market size in 2025 and is advancing at an 8.78% CAGR through 2031.

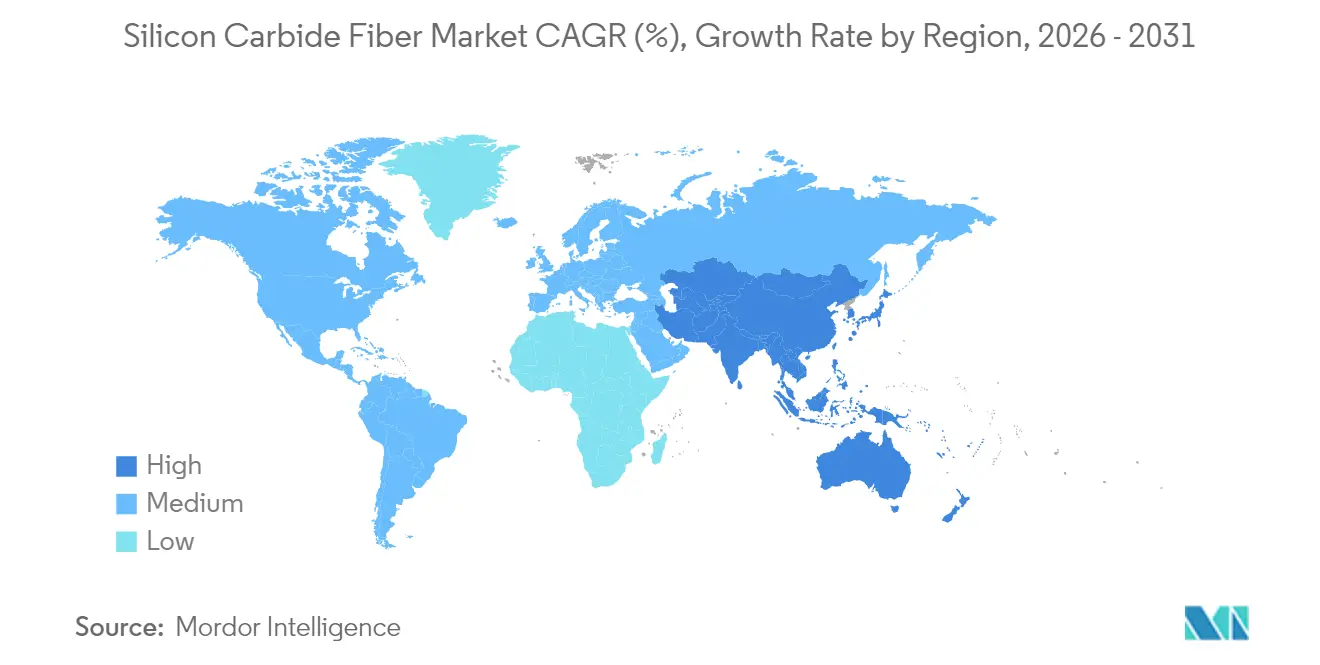

- By geography, North America represented 37.21% of the silicon carbide fiber market size in 2025, while Asia-Pacific is advancing at an 8.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicon Carbide Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Rise in Commercial and Military Aerospace Engine Production | +2.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Surging Demand for SiC-Reinforced Ceramic Matrix Composites in Next-Gen Gas Turbines | +1.8% | Global, with APAC manufacturing growth | Long term (≥ 4 years) |

| Nuclear Small Modular Reactor Vendors Adopting SiC Fibers for Accident-Tolerant Fuel Cladding | +1.3% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Lightweighting Push in E-Mobility Thermal-Protection Systems | +0.9% | Global, led by China and Europe | Medium term (2-4 years) |

| Hypersonic-Flight Thermal-Shield Programs Adopting SiC Fibers | +0.7% | North America and China defense programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Commercial and Military Aerospace Engine Production

LEAP-series CMC shrouds have surpassed 10 million flight hours, validating silicon carbide fiber composites in commercial service. Parallel military adoption is notable; the T901 engine for the UH-60M Black Hawk delivers 1,000 extra shaft horsepower while retaining form factor because SiC CMCs reduce component mass by 50%. Pratt & Whitney has opened a 60,000 ft² CMC center in Carlsbad to accelerate qualification of SiC-reinforced vanes and combustors. Engine OEMs expect more than 1,200 annual LEAP shop visits by 2028, prompting Safran to commit over EUR 1 billion to global maintenance networks. As fleets mature, aftermarket demand secures long-term fiber volumes and justifies continued capacity expansion.

Surging Demand for SiC-Reinforced Ceramic Matrix Composites in Next-Gen Gas Turbines

Gas-turbine makers target firing temperatures above 1,300 °C to raise combined-cycle efficiency, and SiC fibers are pivotal because they retain tensile strength where nickel alloys creep[1]MDPI Editors, “Silicon Carbide Fiber Composites for High-Temp Gas Turbines,” mdpi.com. Steam oxidation once limited CMC lifetimes, but environmental-barrier coatings designed for SiC fibers now extend service beyond 25,000 hours. Hydrogen-fired turbines add further impetus because SiC exhibits superior resistance in high-temperature hydrogen compared with steel. Marine propulsion is another vector: 5 MW compact turbines equipped with SiC liners allow ferry operators to meet IMO Tier III emissions without costly SCR systems. Collectively, power and marine users diversify demand beyond aerospace, smoothing the silicon carbide fiber market growth curve.

Nuclear Small Modular Reactor Vendors Adopting SiC Fibers for Accident-Tolerant Fuel Cladding

General Atomics’ SiGA cladding endured 1,900 °C during 120-day irradiation at Idaho National Laboratory, a milestone for Gen-IV and SMR safety cases. The U.S. Nuclear Regulatory Commission is concurrently reviewing SiC cladding from Framatome and Westinghouse, signaling regulatory momentum toward mid-2030s deployment. Digital-twin modeling cuts qualification cost and time, giving utilities clearer economics for fuel reloads. Japan and South Korea have begun feasibility studies for SiC-based ATF in advanced boiling-water reactors, broadening potential offtake. As SMR vendors finalize designs, firm fiber contracts are expected to lock in base-load volumes, insulating the silicon carbide fiber market from cyclical aerospace swings.

Lightweighting Push in E-Mobility Thermal-Protection Systems

Battery packs exceeding 800 V raise thermal-runaway risk, and automakers now specify SiC fiber cloth barriers capable of 1,300 °C ablation resistance. Early field data show 40% weight reduction versus traditional mica shields without sacrificing flame arrest capability. Carbon-based heat-spreaders doped with SiC fibers improve through-thickness conductivity, lowering peak cell temperatures by 15 °C during fast charging. China’s GB 38031-2020 regulations and Euro NCAP’s 2026 battery-fire protocols intensify focus on robust thermal barriers, driving OEM requests for automotive-grade SiC fabrics. While volumes per vehicle are modest, unit value remains high, adding another profitable niche for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-High Production Cost and Capital Intensity | -1.9% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Scale-Up Bottlenecks in Polycarbosilane Precursor Supply | -1.4% | Global, concentrated in Asia-Pacific production | Medium term (2-4 years) |

| Substitution Threat from Cost-Competitive Carbon and Alumina Fibers | -0.8% | Price-sensitive applications globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-High Production Cost and Capital Intensity

Four-component polycarbosilane synthesis and 1,800 °C sintering create production costs well above carbon fiber benchmarks. GE Aerospace’s twin Huntsville plants together cost USD 200 million, underscoring steep entry barriers. Energy spending alone can exceed 20% of finished-fiber price because furnaces must maintain oxygen-controlled atmospheres. Research into photosensitive polycarbosilanes shows promise for ambient-pressure curing but remains at pilot scale. Until breakthrough processing or broader volumes dilute fixed costs, the silicon carbide fiber market will stay concentrated among capital-rich incumbents, limiting price elasticity in cost-sensitive sectors.

Scale-Up Bottlenecks in Polycarbosilane Precursor Supply

Less than a dozen facilities worldwide synthesize precursor at required purity, with Japanese suppliers dominating technology. Chemical-vapor curing routes could double throughput yet still face solvent-recovery and exhaust-scrubbing challenges at scale. Research on polyaluminocarbosilane opens diversification, but formulation stability issues have delayed commercialization. Alternating air-vacuum oxidation cycles lower energy intensity by 15% but require specialized furnaces that few producers possess. These constraints expose the silicon carbide fiber market to regional supply shocks and slow the pace at which new entrants can qualify material.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Continuous Dominance Drives Performance

Continuous fibers captured 70.02% of the silicon carbide fiber market share in 2025 and are forecast to grow at an 8.63% CAGR through 2031. Third-generation grades such as Hi-Nicalon S deliver 2.8 GPa tensile strength at 1,600 °C, satisfying aerospace load paths where creep resistance is critical. Manufacturing refinements that suppress abnormal grain growth have raised room-temperature strength toward 4 GPa, widening the design envelope. Continuous filaments also enable winding of nuclear fuel cladding tubes, where hoop stress alignment enhances burst tolerance during loss-of-coolant scenarios. Short fibers remain relevant for polymer infiltration and pyrolysis (PIP) routes that mold complex geometries, especially industrial burner nozzles, but their mechanical ceiling restrains broader structural uptake.

Advances in defect-controlled spinning coupled with surface-oxygen management produce smoother filaments that bond uniformly within SiC matrices. This microstructural harmony boosts interfacial shear by 25%, improving cyclic fatigue life in engine hot-sections. Automated winder upgrades now maintain ±1% roving tension, ensuring repeatable composite thickness in aero-engine flanges. As learning curves flatten, production scrap rates have dropped below 5%, reducing effective cost per kilogram. Continuous fibers consequently underpin most high-value aerospace orders, securing the silicon carbide fiber market a stable revenue core while allowing producers to experiment with lower-grade products for emerging sectors.

By Form: Woven Architectures Enable Complex Applications

Woven cloth preforms represented 56.10% of the silicon carbide fiber market size in 2025 and are tracking an 8.44% CAGR through 2031. Plane, satin, and twill weaves permit 3-D lay-ups that conform to turbine shroud curvature, thereby limiting machining waste. Near-net-shape weaving reduces buy-to-fly ratios to 1.2:1 in some nozzle guide vane programs, translating directly into cost savings at USD 1,000 per kg material rates. Aerospace primes prefer woven cloth because fiber crimp is predictable, yielding uniform porosity for slurry infiltration. Continuous unidirectional tapes still excel where loads are quasi-axial, such as pressure vessels and hypersonic leading edges, yet adoption is curbed by line investment exceeding USD 15 million per head.

Three-dimensional braids now achieve 660 MPa flexural strength after repeated infiltration cycles, enabling stiffened panels that replace metallic honeycomb. Robotic looms support variable-angle fibers, giving designers freedom to tailor stiffness gradients across complex ducting. Hybrid preforms mixing SiC with carbon rovings tackle cost-sensitive exhaust-duct projects by concentrating SiC only in hot spots. Collectively, woven formats sustain the silicon carbide fiber market growth momentum because they slash assembly steps, shorten autoclave cycles, and simplify certification documentation by achieving more homogeneous microstructures.

By End-user Industry: Aerospace Leadership Drives Innovation

Aerospace and defense commanded 60.74% of the silicon carbide fiber market share in 2025 and is projected to expand at an 8.78% CAGR through 2031. The segment pays price premiums for SiC CMCs that cut engine weight by 45 kg per LEAP-1A set, improving thrust-to-weight and fuel burn. Military programs amplify demand because thermal margins directly translate into range extension for stealth platforms whose inlets restrict cooling airflow. Energy and power emerges as the fastest-growing secondary sector because industrial gas-turbine OEMs require higher firing temperatures to achieve 65% combined-cycle efficiency targets. Marine applications follow suit as navies retrofit ships with CMC-lined turbines to comply with sulphur emissions limits.

Industrial heaters, chemical reaction tubes, and molten-salt pumps adopt SiC fibers for corrosion-resistant liners that withstand 1,400 °C while resisting fluorine attack. The silicon carbide fiber industry also penetrates automotive battery-pack enclosures and filtration candles for hot gas streams above 900 °C. Nonetheless, aerospace remains the anchor customer segment for the silicon carbide fiber market, underwriting capital investments in spinning lines and precursor facilities that spin off cost reductions benefiting secondary segments.

Geography Analysis

North America retained 37.21% of 2025 revenue due to its entrenched aerospace supply chain and government funding for high-temperature materials. The U.S. Department of Energy earmarked USD 150 million for harsh-environment SiC fiber programs, accelerating qualification for power and SMR reactors. Huntsville hosts the first western commercial fiber line, positioning the region as a self-sufficient hub, while Canada’s MDA and Mexico’s Queretaro aero-clusters integrate composites into nacelle structures. The geographic concentration supports early adopter pricing and tight customer feedback loops that advance material iterations.

Asia-Pacific, growing at 8.70% CAGR, benefits from Japanese leadership in polycarbosilane chemistry and expanding Korean aero-engine overhaul networks. UBE Corporation plans to multiply precursor output tenfold this decade to meet domestic and export demand. China scales its aero-engine institute’s SiC CMC test bed for hypersonic glide vehicles, signaling future high-volume consumption once technology transfer hurdles ease. Semiconductor fabrication in South Korea spurs SiC heat-spreader development, anchoring non-aero demand. India and ASEAN nations are yet nascent but show potential as local composites clusters mature.

Europe leverages a robust gas-turbine and automotive footprint to sustain steady demand. STMicroelectronics’ silicon-carbide power-device roadmap necessitates advanced heat spreaders, indirectly boosting fiber uptake. Germany’s engine programs seek 40% efficient microturbines for district heat, requiring SiC liners. The UK funds CMC demonstrators under its Aerospace Technology Institute, widening qualification data sets. Nordic utilities exploring hydrogen co-firing in combined-cycle plants also specify SiC liners. Although current macroeconomic headwinds affect capital spending, Europe’s regulatory focus on emission reduction preserves long-term fiber demand.

Competitive Landscape

The silicon carbide fiber market remains technologically consolidated; knowledge of precursor synthesis and controlled atmospheres outweighs simple scale in conferring advantage. Japanese firms NGS Advanced Fibers and UBE Corporation dominate polycarbosilane IP while maintaining reputations for sub-1% defect rates, securing long-term supply contracts with aero primes. GE Aerospace’s USD 200 million vertically integrated campus links fiber spinning with prepreg lay-up, enabling closed-loop quality control that accelerates engine certification. General Atomics focuses on nuclear applications; its SiGA cladding captures premium pricing on the basis of 1,900 °C survivability.

Process innovation shapes rivalry. MATECH’s field-assisted sintering densifies CMC panels in minutes, delivering 20× ablation resistance relative to silica-phenolic baselines. Safran integrates braiding robotics to cut lay-up labor by 30%, while Specialty Materials introduces oxygen-gradient fibers that dampen matrix micro-cracks. White-space opportunities center on hypersonic vehicle nose tips and e-mobility fire-barrier panels, niches that reward agile R&D pipelines. Patent filings reveal that top five producers control more than 70% of high-temperature coated-fiber claims, deterring commoditization.

Collaborative programs bridge regional gaps. U.S.–Japan research under the Monosozukuri partnership explores faster precursor curing, and EU’s Clean Aviation initiative funds endurance testing of SiC vane inserts. Yet entrants still face steep capital outlays and decade-long qualification timelines, preserving high entry barriers. Consequently, suppliers with vertically integrated capabilities and end-market diversification hold pricing power even as volumes climb, cementing their positions through 2030.

Silicon Carbide Fiber Industry Leaders

GE Aerospace

NGS Advanced Fibers Co., Ltd

Specialty Materials Inc.

COI Ceramics

Safran Ceramics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: General Atomics Electromagnetic Systems received a Department of Energy (DOE) contract to develop silicon carbide materials for fusion power plants. This development is expected to drive innovation and future demand for silicon carbide fibers, as they are essential for high-temperature, structural applications in energy and defense sectors.

- March 2023: SGL Carbon will provide essential graphite components to Wolfspeed's silicon carbide production facilities. This collaboration aims to enhance the manufacturing efficiency and increase the production capacity of silicon carbide materials, including fibers for industrial applications.

Global Silicon Carbide Fiber Market Report Scope

The silicon carbide fiber market report includes:

| Continous Fiber |

| Short Fiber |

| Continuous |

| Woven |

| Aerospace and Defence |

| Energy and Power |

| Industrial |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fiber Type | Continous Fiber | |

| Short Fiber | ||

| By Form | Continuous | |

| Woven | ||

| By End-user Industry | Aerospace and Defence | |

| Energy and Power | ||

| Industrial | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the silicon carbide fiber market?

The silicon carbide fiber market size reached USD 1.12 billion in 2026.

Which segment holds the largest share of the silicon carbide fiber market?

Continuous fiber leads with 70.02% share in 2025.

What CAGR is forecast for the silicon carbide fiber market from 2026 to 2031?

The market is projected to expand at an 8.09% CAGR over the period.

Why are silicon carbide fibers important for aerospace engines?

They allow gas-turbine components to run 250 °C hotter while cutting weight by up to 50%, improving fuel efficiency and thrust margins.

Which region is growing fastest in the silicon carbide fiber market?

Asia-Pacific is advancing at an 8.70% CAGR, driven by Japanese precursor capacity expansions and rising aerospace manufacturing in South Korea and China.

Page last updated on: