Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

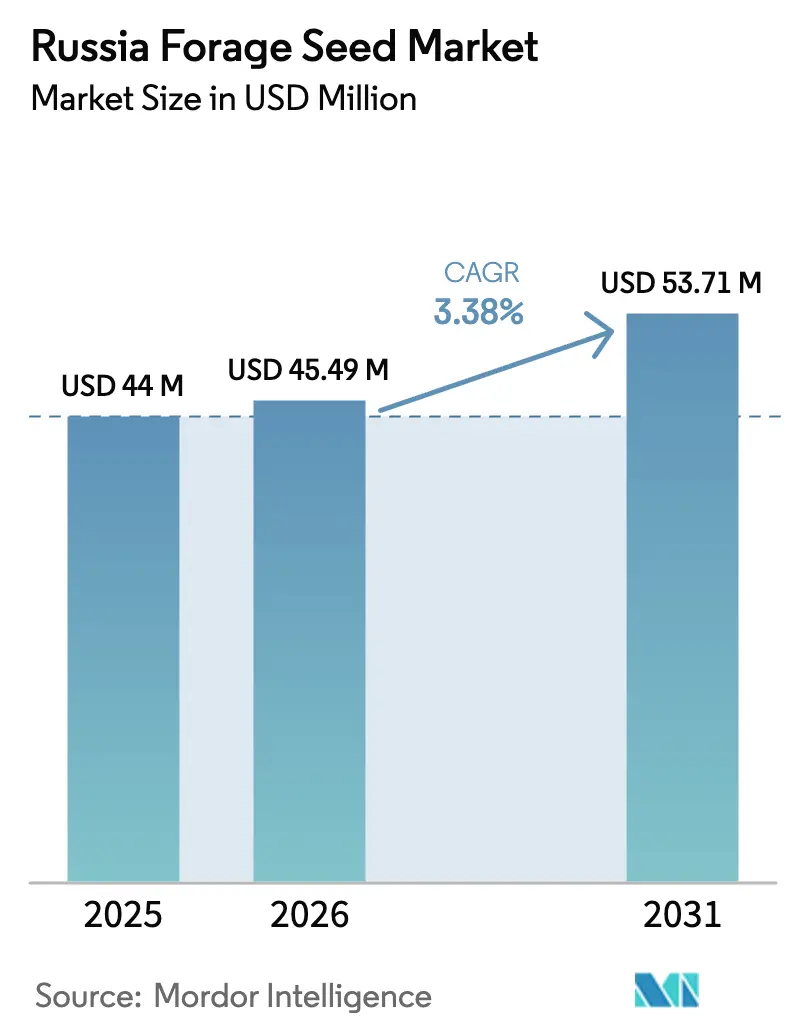

| Base Year Market Size (2025) | USD 44 Million |

| Market Size (2026) | USD 45.49 Million |

| Market Size (2031) | USD 53.71 Million |

| Growth Rate (2026 - 2031) | 3.38% CAGR |

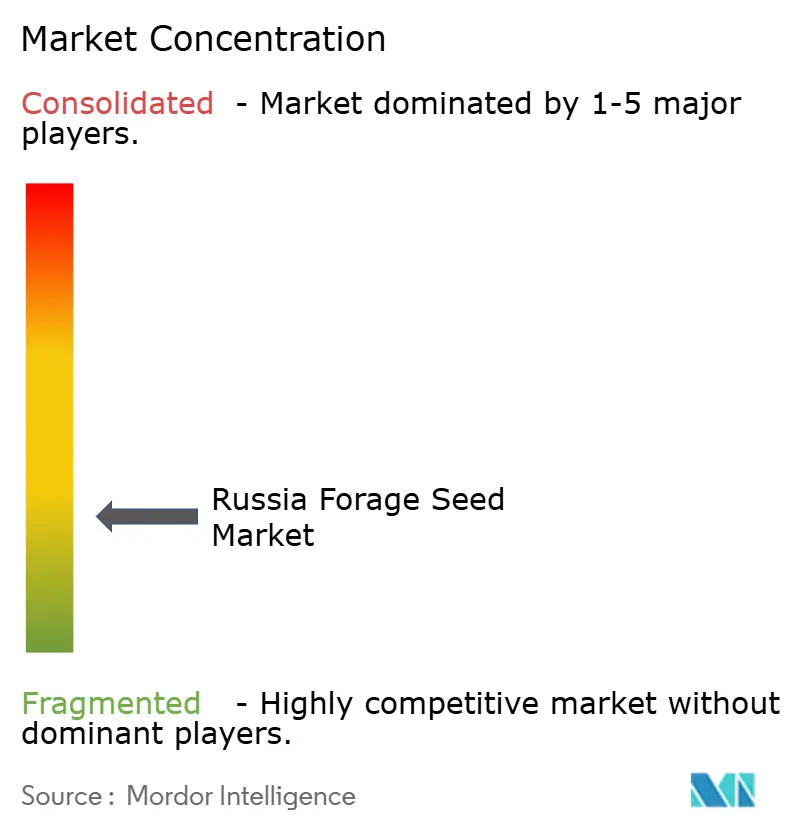

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Forage Seed Market Analysis by Mordor Intelligence

The Russia forage seed market size is expected to grow from USD 44 million in 2025 to USD 45.49 million in 2026 and is forecast to reach USD 53.71 million by 2031 at 3.38% CAGR over 2026-2031. The measured expansion of the Russia forage seed market arises from the government’s import-substitution policy, rising livestock numbers, and continuous territorial cultivation. Persistent policy support has already lifted domestic seed self-sufficiency in 2024, with a formal target set for 2030. Precision agriculture tools, drought-tolerant hybrids, and new seed-processing plants underpin productivity gains, while emerging arable acreage in newly incorporated territories widens the geographic footprint of the Russia forage seed market. Climate volatility, higher input costs, and residual reliance on imported elite germplasm temper the pace of progress.

Key Report Takeaways

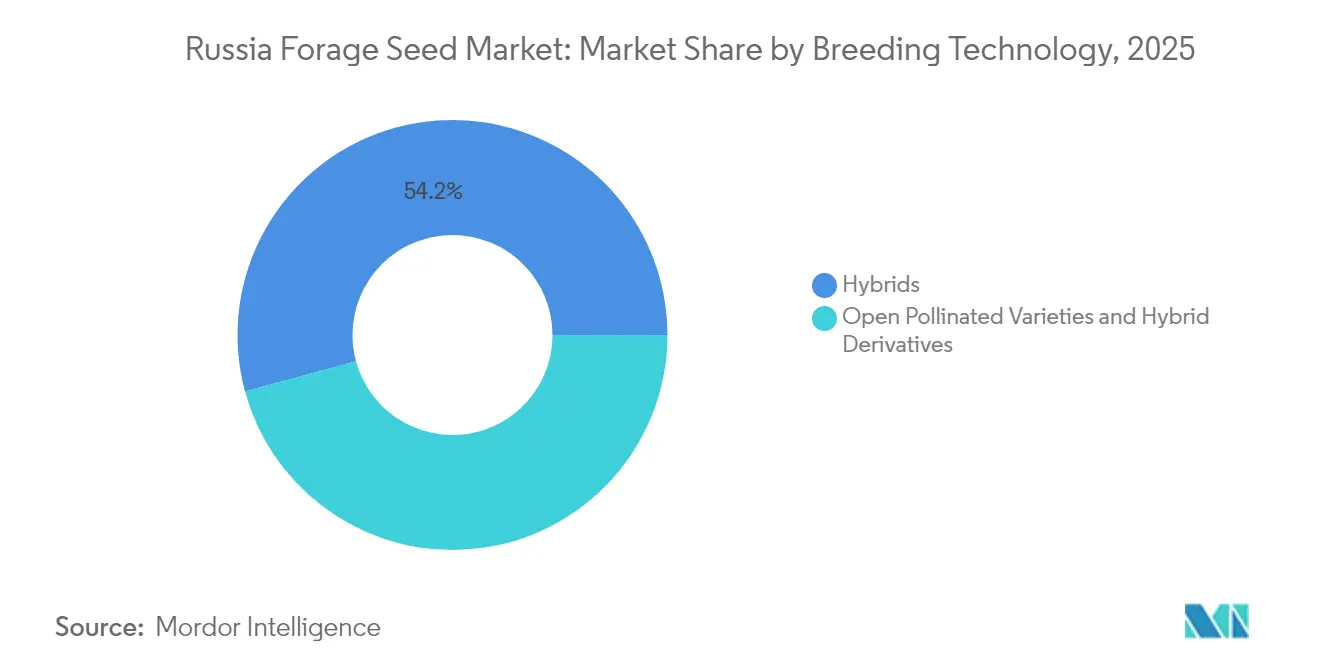

- By breeding technology, hybrids led with 54.23% of the Russia forage seed market share in 2025; open-pollinated varieties expanded at a 3.74% CAGR through 2031.

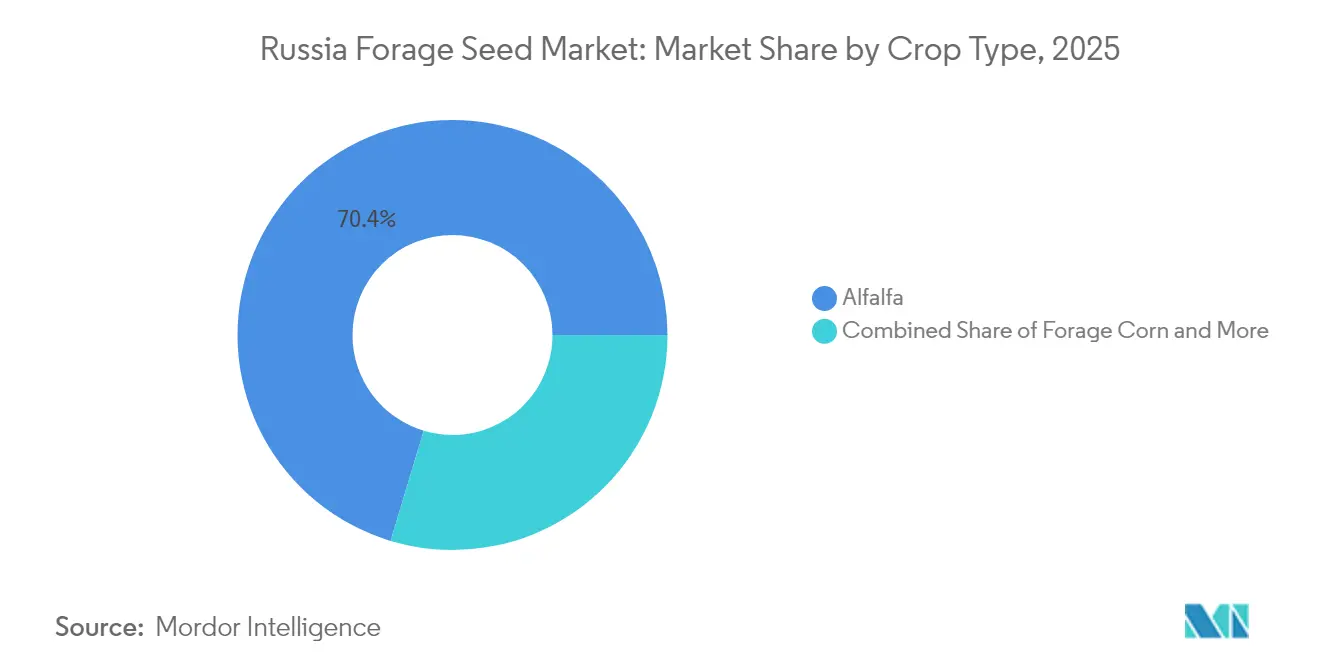

- By crop type, alfalfa accounted for 70.35% of the Russia forage seed market size in 2025, while forage sorghum posted the fastest 8.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Forage Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in domestic livestock and dairy production | +0.8% | National, concentrated in the Central and Volga federal districts | Medium term (2-4 years) |

| Government seed-self-sufficiency programs and subsidies | +0.9% | National, with priority regions receiving enhanced support | Long term (≥ 4 years) |

| Adoption of drought-tolerant hybrid cultivars | +0.6% | Southern regions, the Volga basin, and newly incorporated territories | Short term (≤ 2 years) |

| Precision-agriculture driven variable-rate seeding | +0.4% | Central, North Caucasus federal districts | Medium term (2-4 years) |

| Expansion of arable land in newly incorporated territories | +0.5% | Newly incorporated territories, adjacent border regions | Long term (≥ 4 years) |

| Rapid build-out of private domestic seed-processing plants | +0.7% | National, concentrated in major agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in domestic livestock and dairy production

Sustained herd expansion fuels core demand for quality forage across dairy and beef operations. Federal forecasts point to livestock output growth through 2027, while raw milk volumes climb, sharply lifting per-animal forage requirements. Intensification toward confinement systems increases reliance on protein-rich alfalfa and high-energy forage corn, concentrating seed purchases in the Central and Volga belts, where 73% of agricultural output originates. Capital inflows from a USD 51 billion state program improve housing, feed storage, and irrigation, reinforcing a virtuous feedback loop between animal productivity and seed demand. Regional clustering around processing hubs further smooths distribution costs, making premium hybrids more attainable for mid-size farms.

Government seed-self-sufficiency programs and subsidies

A binding national target to lift seed self-reliance by 2030 energizes local research, multiplication, and certification initiatives. The Federal State Information System “Semenovodstvo” obliges every producer to file yearly localization plans, and Order No. 1983 deploys quantitative quotas on imports from “unfriendly” nations starting January 2025[1]Source: CIS Legislation, “Temporary quantitative restriction on import of seeds,” CIS-LEGISLATION.COM. Coupled with preferential credit lines and a USD 1.9 million grant package for plant-breeding labs, the framework tilts market leverage toward domestic players. Blockchain-based anti-counterfeit seals, rolled out in 2024, aim to eliminate a grey-market share estimated at 40%, raising overall quality benchmarks and discouraging price-led competition.

Adoption of drought-tolerant hybrid cultivars

Severe 2024 droughts in Kalmykia and Voronezh underscored the economic toll of weather-related stand failures, pushing farmers to embrace hybrids engineered for moisture stress[2]Source: Springer, “Russian Agricultural Sciences Vol 50-1,” LINK.SPRINGER.COM. Forage sorghum exemplifies this shift, recording the fastest growth among forage seed crop types. Research teams showcased variegated alfalfa crosses capable of sustaining fodder yields under 30-40% rainfall deficits, validating the commercial upside of non-transgenic hybridization. Uptake is briskest in Southern zones where precipitation volatility is acute, broadening the addressable base for seed developers that bundle agronomic advice with climate-ready genetics.

Precision-agriculture driven variable-rate seeding

GPS-guided drills, UAV imagery, and soil sensors enable per-zone seed-rate modulation that lifts germination success by 15-20%. The Ministry of Agriculture earmarked RUB 750 million (USD 7.9 million) in 2024 for digital hardware and decision-support software rollouts. Because hybrids respond more uniformly to optimal spacing, precision adopters tend to up-trade from open-pollinated lots, adding value even if surface area sown remains flat. Planned linkage between field maps and the “Semenovodstvo” database by 2026 will streamline variety recommendations, reinforcing data-driven seed selection habits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate volatility requires costly re-seeding | -0.7% | National, acute in the southern and southeastern regions | Short term (≤ 2 years) |

| Escalating fertilizer and fuel costs | -0.5% | National, disproportionate impact on remote regions | Medium term (2-4 years) |

| Ongoing reliance on imported elite germplasm | -0.4% | National, concentrated in specialty crop segments | Long term (≥ 4 years) |

| Low adoption of on-farm seed-treatment technology | -0.3% | National, pronounced in smaller farming operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate volatility requiring costly re-seeding

Droughts, hail, and winter thaw events force unplanned stand renewal at USD 150-200 per hectare, siphoning working capital from growth investments. Weather models warn of continued moisture anomalies into mid-2025 for northern and southeastern belts, fueling short-cycle seed orders yet crimping profitability. Transport bottlenecks aggravate price spikes in distant regions, with West Siberian farmers paying a premium over Central peers due to freight surcharges. Subsidized crop-insurance uptake remains below 25%, exposing smaller operators to liquidity strains that deter hybrid purchases despite their resilience benefits.

Escalating fertilizer and fuel costs

Fertilizer spot prices stay inflated amid geopolitical supply dislocations, while diesel, 15-20% of mechanized forage budgets, tracks elevated crude benchmarks. Equipment finance rates of 25-27% discourage upgrades to fuel-efficient tractors and applicators, locking farmers into higher variable costs. Regional disparities in input availability create geographic cost variations, with remote agricultural areas facing premium pricing due to transportation expenses and limited supplier competition. These cost pressures force farmers to prioritize lower-cost seed varieties over premium hybrids, potentially constraining market value growth despite volume expansion driven by increased forage demand from livestock sector development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Leadership Broadens the Value Pool

Hybrids dominated with 54.23% Russia forage seed market share in 2025 and are set to post a 3.61% CAGR through 2031. Performance edge stems from consistent yields, drought tolerance, and tighter nutritive quality bands that align with intensive dairy rations. As credit access improves, mid-scale operations increasingly justify the higher ticket, nudging open-pollinated varieties toward budget-constrained niches. The hybrid segment's market size is projected to increase through 2031. Non-transgenic pathways attract R&D dollars given the country’s strict GMO curbs, while derivative lines combining hybrid vigor with lower royalty fees cater to cost-sensitive provinces.

Parallel investments in regional test plots and digital decision tools shorten the learning curve, reinforcing loyalty to branded hybrids. Certification audits under “Semenovodstvo” expose sub-par seed lots, indirectly steering demand toward suppliers with proven field data. Open-pollinated varieties still anchor emergency re-seeding due to affordability and immediate availability, yet their Russia forage seed market share drifts lower as farm-gate milk prices climb and management intensifies. Hybrid derivatives optimized for forage-specific traits, rapid regrowth, or enhanced lignin digestibility promise fresh revenue streams, especially once seed-processing upgrades allow on-site inoculation with rhizobia or bio-stimulants.

By Crop Type: Alfalfa Supremacy Faces Drought-Driven Sorghum Upswing

Alfalfa held 70.35% of the Russia forage seed market size in 2025. The segment benefits from irrigation build-outs and expanding silage bunk capacity, ensuring robust baseline demand. Forage sorghum’s 8.29% CAGR underscores a rising appetite for water-efficient alternatives that survive erratic rainfall. Hybrids boasting high sugar content and brown-midrib traits deliver respectable feed energy with 25-30% less water than corn, resonating in the Volga and Southern districts.

Forage corn remains a stalwart in mixed rations, yet its sensitivity to mid-season drought nudges some acreage to sorghum or sorghum-sudan crosses. Secondary crops like annual ryegrass and clovers address niche rotations but struggle for share as large dairies pivot to simplified feed systems. Russia forage seed market size allocated to alfalfa still expands in absolute terms, while sorghum’s fast clip gradually chips away at dominance in arid locales. Breeders leveraging dual-purpose cultivars, grain and forage position sorghum as a hedge crop, enhancing its agronomic appeal.

Geography Analysis

Russia forage seed market gravitates toward the Central, North Caucasus, Urals, and Volga federal districts, which jointly supply nearly three-quarters of national agricultural output. Central clusters funnel seed throughput into vertically integrated dairy chains that value high-digestibility alfalfa and precision-planted corn silage. North Caucasus farmers prioritize drought-tolerant sorghum variants, reflecting lower rainfall and shallow topsoil horizons. Urals and Siberia face shorter growing seasons, favoring early-maturing alfalfa and cold-tolerant grasses, albeit at lower per-hectare revenue compared with their southern peers.

Newly incorporated territories add roughly 1.6 million hectares of winter crops, offering upside once roads, storage, and credit unions materialize. Government inventory of idle land aims to reactivate another 31 million hectares nationwide by end-2025, potentially enlarging the Russia forage seed market by double digits mid-decade. Yet transport costs remain punitive in remote zones; hauling a truckload of seed from Krasnodar to Omsk adds over ex-works price, creating a moat for localized multipliers.

Regulatory uniformity advances via nationwide roll-out of the “Semenovodstvo” registry, ensuring traceability across oblast lines. Still, subsidy distribution diverges: Volga dairy centers receive preferential rate loans for hybrid alfalfa, while Far East districts focus on grain legumes for mixed-feed mills. Such heterogeneity compels seed firms to maintain region-specific portfolios and decentralized warehousing to capture dispersed demand pockets.

Competitive Landscape

Russia forage seed market exhibits fragmentation, with domestic firms scaling capacity under protectionist incentives and multinationals forming a good share of Russian-owned joint ventures to stay compliant. Bayer AG and Corteva Inc. leverage local field stations to adapt germplasm, whereas Kubanhleb Agroholding and Ruseed LLC expand processing lines to seize quota-displaced volumes. Strategic plays center on drought-hardy hybrids, with Ruseed releasing a sorghum hybrid delivering 18% higher dry-matter yield in low-rain trials.

International entrants often cede volume but retain premium niches by bundling agronomic analytics and performance guarantees. Asset seizures such as AgroTerra’s 2024 case remind foreign investors of regulatory risk, prompting some to license genetics to local partners instead of retaining capital-intensive footprints. Domestic sunflower seed share under special technologies rose 14 percentage points to 26%, showcasing breeder capability gains[3]Source: ROSNG.RU, “Share of domestic sunflower seeds under special technologies rose,” ROSNG.RU .

Digital differentiation accelerates: Kubanhleb’s mobile app links field imagery with seed recommendations, locking in repeat orders. Price competition eases as quotas thin grey-market imports, allowing branded hybrids to command 10% spreads over non-certified seed. Looking forward, competitive intensity will hinge on who best aligns with state self-sufficiency milestones, given that subsidy access increasingly rewards documented localization ratios.

Russia Forage Seed Industry Leaders

Euralis Semences

Groupe Limagrain

KWS SAAT SE & Co. KGaA

Royal Barenbrug Group

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Russian Government implemented comprehensive quantitative import restrictions on forage seed varieties from "unfriendly" countries through Order No. 1983, fundamentally restructuring supply chains for alfalfa, forage corn, and specialty legume seeds while creating protected market opportunities for domestic producers.

- December 2024: Russia achieved 60% reduction in overall seed imports, with forage seed categories experiencing particularly sharp declines as domestic production capacity expanded and government localization incentives accelerated adoption of Russian-bred varieties across livestock farming operations.

- February 2024: Russian Agricultural Sciences published research on variegated alfalfa selection programs targeting intensive varieties with enhanced fodder productivity, indicating sustained academic investment in forage breeding that supports domestic variety development and reduces reliance on imported genetics.

Russia Forage Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Alfalfa, Forage Corn, Forage Sorghum are covered as segments by Crop.Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives |

Crop Type

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives | ||

| Crop Type | Alfalfa | |

| Forage Corn | ||

| Forage Sorghum | ||

| Other Forage Crops |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms