Competent Cells Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 3.91 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Competent Cells Market Analysis by Mordor Intelligence

The competent cells market size is expected to grow from USD 2.45 billion in 2025 to USD 2.65 billion in 2026 and is forecast to reach USD 3.91 billion by 2031 at 8.12% CAGR over 2026-2031. Increasing reliance on synthetic biology, gene-editing platforms, and automated bioprocessing pipelines positions competent cells as a foundational reagent class. Growth is reinforced by the 28.3% CAGR expansion of the global synthetic biology sector, which directly amplifies demand for ultra-high-efficiency transformation systems that can handle large plasmid constructs. Parallel investments in CRISPR-Cas9 therapeutics, government-funded biofoundries, and continuous advances in cell-free protein synthesis broaden the scope of applications that require tailored competent cell formats. As laboratories transition from manual bench procedures to fully automated high-throughput environments, suppliers with automation-friendly packaging and validated strain performance gain a strategic edge in the competent cells market.

Key Report Takeaways

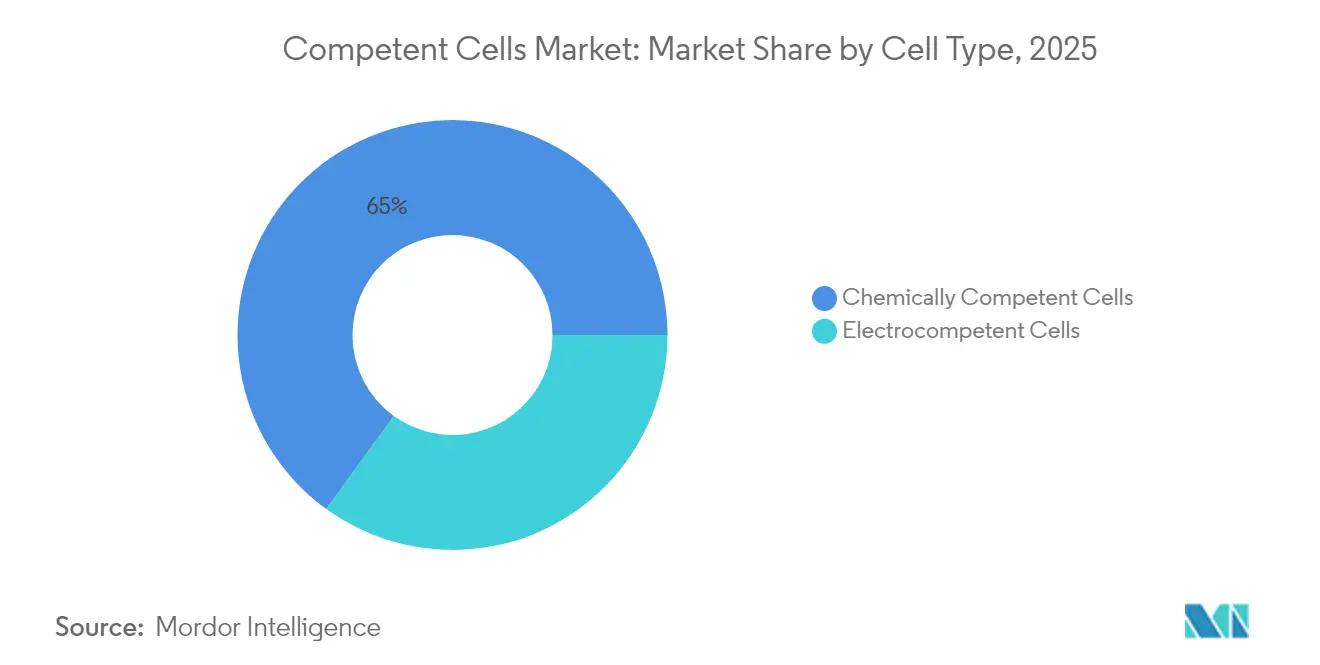

- By cell type, chemically competent cells led with 65.02% of competent cells market share in 2025, while electrocompetent cells are projected to expand at a 8.87% CAGR through 2031.

- By application, protein expression accounted for 49.35% of the competent cells market share in 2025; cloning and sub-cloning is set to grow fastest at a 8.76% CAGR to 2031.

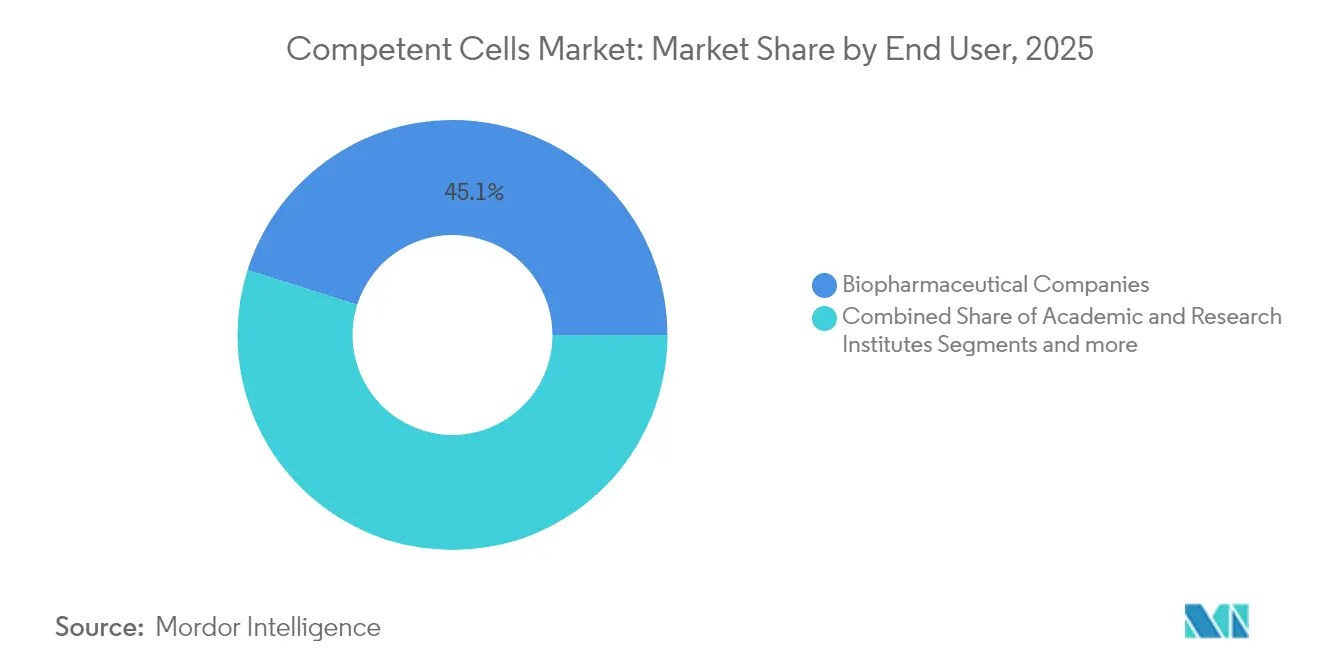

- By end user, biopharmaceutical companies held 45.12% revenue in 2025, whereas academic and research institutes are forecast to register the highest 9.02% CAGR.

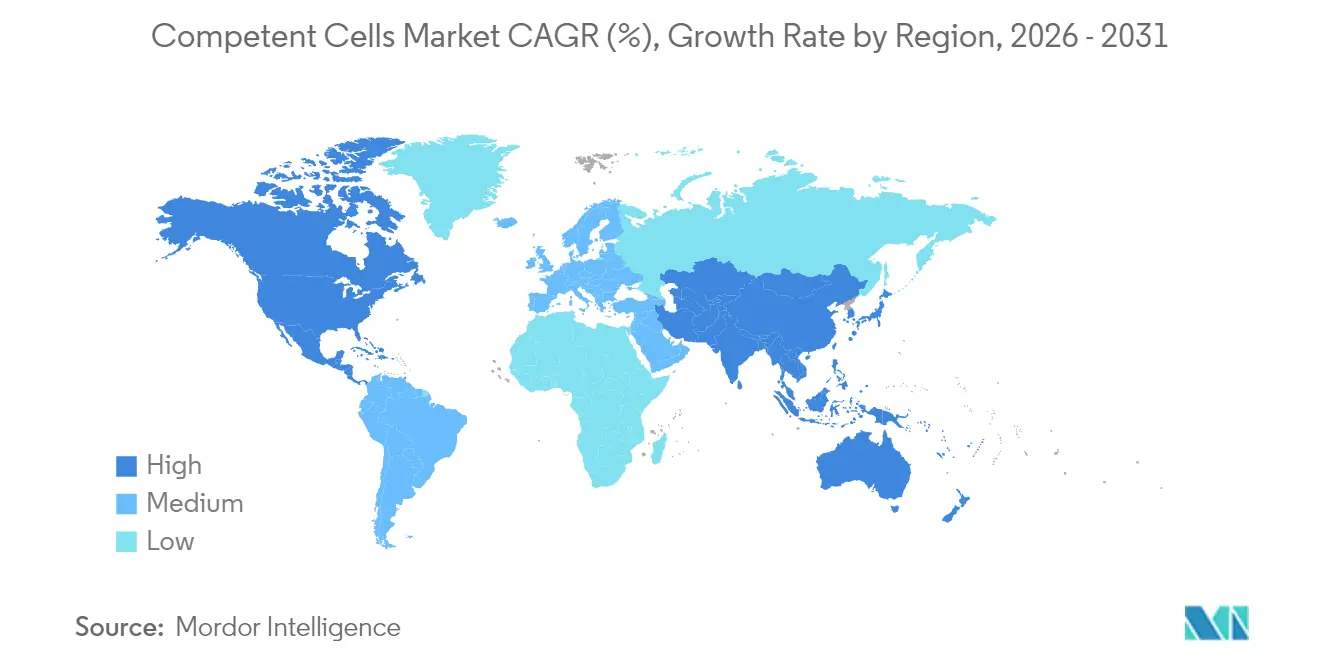

- By geography, North America dominated with 41.74% share in 2025, but Asia-Pacific is positioned for the quickest 9.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Competent Cells Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial Demand & Continuous Academic/Government Support | +2.1% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Expanding Biologics & Recombinant Protein Pipelines | +1.8% | Global, strongest in APAC & North America | Medium term (2-4 years) |

| Adoption Of High-Throughput Automation-Friendly Formats | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising CRISPR Gene-Editing Workflows Needing Ultra-High Efficiency Cells | +1.4% | Global, led by North America research hubs | Short term (≤ 2 years) |

| Growth Of Synthetic Biology & Cell-Free Systems | +1.2% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Regional Capacity-Building Funds for Life-Science Manufacturing | +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commercial demand and academic or government support

Government-backed infrastructure programs have locked in multiyear reagent spending, giving the competent cells market predictable baseline volumes. The National Science Foundation’s USD 75 million allocation to five biofoundries equips institutions with permanent, high-capacity facilities that must stock standardized competent cell lots for automated workflows [1]National Science Foundation, “NSF Invests USD 75 Million in Biofoundries,” nsf.gov . The National Institutes of Health adds a focused USD 2 million annual stream for genome-editing therapeutics, stimulating uptake of ultra-high-efficiency strains suitable for CRISPR pipelines [2]National Institutes of Health, “Genome Editing Therapeutics Funding Opportunity,” nih.gov . Policy testimony before the U.S.-China Economic and Security Review Commission projects that the bio-economy could underpin 60% of global economic inputs by mid-century, underscoring continued public financing that favors long-term reagent demand.

Expanding biologics and recombinant protein pipelines

Contract development and manufacturing organizations (CDMOs) are scaling to meet a biologics pipeline that rose from USD 19.89 billion in 2023 toward USD 31.92 billion by 2032. As upstream cell line development often dictates downstream yields, manufacturers specify high-titer competent cells capable of supporting complex plasmid expression constructs. Asimov’s CHO Edge platform guarantees ≥ 5 g/L monoclonal antibody titers, signaling an industry shift toward predictable strain performance that relies on consistent transformation efficiency for template plasmids. Cell-free expression systems taken to 4,500 L scale by Sutro Biopharma further widen the addressable market for specialized competent cells tuned for in vitro protein synthesis.

Adoption of high-throughput automation-friendly formats

Robotic liquid handlers are now routine in cell line screening, forcing a rethink of packaging. Beckman Coulter’s Cydem VT platform processes 96 clones simultaneously, compelling suppliers to deliver competent cells in plate or strip-tube formats with verified lot-to-lot homogeneity [3]Beckman Coulter Life Sciences, “Cydem VT Automated Clone Screening System,” beckman.com . Predictive cold-chain algorithms built on SARIMA and Prophet models allow distributors to streamline −80 °C inventory positions, reducing loss incidents for temperature-sensitive competent cell vials. The wider adoption of virtual control-tower logistics is pivotal for stabilizing supply in regions with patchy cold-chain infrastructure.

Rising CRISPR gene-editing workflows

Therapeutic-grade CRISPR methods pack guide RNAs, repair templates, and Cas proteins into large plasmids that demand ≥ 1 × 10¹⁰ cfu/µg transformation performance. Recent work in HEK293T cells showed a 40% boost in membrane protein yield after ATF6B editing, illustrating direct links between efficient editing and downstream protein output. Industrial Komagataella phaffii CRISPR toolkits have brought markerless integration efficiencies high enough for commercial enzyme production, expanding the customer base that requires specialized ultra-competent strains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D And Production Costs | -1.2% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Market Consolidation & Difficult Entry for Start-Ups | -0.8% | North America & EU, spreading to APAC | Medium term (2-4 years) |

| Cold-Chain Fragility in Emerging Nations | -0.6% | APAC emerging markets, MEA, Latin America | Long term (≥ 4 years) |

| Shift Toward Synthetic Gene Circuits That Bypass Transformation | -0.4% | North America & EU research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High R&D and production costs

A single biopharmaceutical approval carries a median USD 2.3 billion development price tag, which forces sponsors to eliminate inefficiencies across every reagent class. For monoclonal antibodies, capture chromatography alone can swallow 25% of total cost of goods; upstream strain choice therefore receives intense scrutiny. Stable producer cell lines that cut GMP-grade plasmid demand from four to one provide clear evidence of the economic leverage tied to competent cell design. These economics place margin pressure on smaller vendors that cannot amortize development costs across global volumes.

Cold-chain fragility in emerging nations

More than 85% of biologics require strict cold storage, and −80 °C logistics remain scarce outside tier-one metropolitan centers. Field trials of freeze-preventive cold boxes in rural Nepal confirmed technical feasibility but introduced bulk and weight issues that restrict use on mountainous routes. China's outreach to Southeast Asia exposes similar gaps, as local distributors lack capital for IoT-enabled tracking that guarantees temperature compliance for high-value competent cells. Without large-scale investment, fragmented supply networks can undermine transformation performance, raising barriers for academic labs in developing economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cell Type: Chemical dominance faces automation challenge

Chemically prepared strains contributed 65.02% revenue in 2025, supported by cost-efficient manufacturing and straightforward calcium chloride protocols that suit teaching laboratories with limited capital equipment. Standard products deliver 1 × 10⁶ cfu/µg efficiency sufficient for routine molecular cloning, preserving the strong volume base of the competent cells market. Electrocompetent formats, however, post the quickest 8.87% CAGR, driven by automated electroporation platforms that need consistent sub-microliter aliquots. For ultra-demanding CRISPR pipelines, leading electrocompetent offerings certify efficiencies above 5 × 10⁹ cfu/µg, which outpaces the ceiling of most chemical counterparts. The competent cells market size for electrocompetent products is forecast to add USD 680 million through 2031 as labs automate transformation steps to match robotic liquid handling throughput.

Innovation within chemical methods continues. Escherichia coli BW25113, a recA⁺ strain, achieves 100-fold improvements in transformation over XL1-Blue MRF′ using an optimized chemical protocol, and records 440- to 1,267-fold boosts in cloning success for large plasmids. Such performance erodes the traditional efficiency gap with electroporation and appeals to institutes lacking electroporators. The competent cells market therefore balances the entrenched cost advantage of chemical formats with the rising performance and automation appeal of electrocompetent lines.

By Application: Protein expression leads despite cloning acceleration

Protein expression retained 49.35% revenue share in 2025 because therapeutic protein projects demand well-characterized strains that avoid proteolytic degradation. The T7 expression system dominates due to IPTG-inducible polymerase control, and BL21 derivatives with lon and ompT knockouts restrict unwanted protease activity. For disulfide-rich proteins, the SHuffle T7 line’s oxidizing cytoplasm and 1 × 10⁶ cfu/µg efficiency answer a persistent manufacturing need. Together these features keep the protein expression sub-segment a heavy consumer of high-purity reagent lots.

Cloning and sub-cloning applications will climb fastest at 8.76% CAGR through 2031. The competent cells market size for cloning workflows is expected to register USD 1.18 billion by the decade’s close as CRISPR, Golden Gate assembly, and kilobase-scale synthetic gene circuits flood research pipelines. High-throughput 96-well transformations support combinatorial library assembly, and suppliers register growing demand for strains that tolerate toxic inserts or tandem repeats. Mutagenesis, driven by error-prone PCR and saturation point mutagenesis, still occupies a smaller slice but benefits from library sizes that scale directly with transformation efficiency.

By End User: Academic institutions accelerate past biopharma

Biopharmaceutical firms commanded 45.12% of 2025 revenue, leveraging validated competent cells to cut process-development timelines. CDMOs serving these firms depend on lot-to-lot reproducibility that meets cGMP documentation, driving premium sales tiers. The competent cells market share for academic and research institutes sits lower today but will climb swiftly on a 9.02% CAGR aided by biofoundry rollouts that reduce barriers to advanced synthetic biology experiments.

Academic momentum is tied to funding streams aimed squarely at gene-editing therapeutics. The NIH earmarks USD 2 million annually for CRISPR-based translational projects, ensuring predictable purchases of ultra-high-efficiency strains. University-industry partnerships embed industrial-grade workflows in academic labs, shrinking the performance gap with commercial operations. CROs and CDMOs that expand service menus capitalize on these trained graduates, reinforcing demand continuity across the competent cells industry value chain.

Geography Analysis

North America anchors 41.74% of 2025 revenue owing to deep life-science capital pools, robust regulatory clarity, and a dense network of GMP facilities. Thermo Fisher Scientific’s pledge to invest USD 2 billion across 64 manufacturing sites in 37 states secures local bioprocessing capacity that guarantees large call-offs for premium competent cell lots. FDA guidance on cell-substrate characterization further standardizes quality benchmarks, reducing lot rejection risk and favoring domestic suppliers with traceable supply chains. The competent cells market size in North America is projected to surpass USD 1.63 billion by 2031 as CRISPR therapeutics enter late-phase trials.

Asia-Pacific is the growth engine, advancing at 9.08% CAGR through 2031. Japan aims to triple its biotechnology output to 15 trillion yen by 2030, supporting local venture rounds that finance platform strains customized for mammalian and bacterial workflows. China’s pivot toward Southeast Asian manufacturing corridors hedges against geopolitical headwinds, linking 600 million potential patients to lower-cost biologics factories. India’s biologics roadmap targets USD 12 billion value by 2025, and policy incentives for biosimilars energize local CDMOs that procure automation-ready competent cells at scale.

Europe sustains steady uptake through entrenched pharmaceutical hubs in Germany, Ireland, and Switzerland. The Hovione-iBET venture ViSync Technologies demonstrates how contract formulators team with academic institutes to solve stability and delivery hurdles for complex biologics. EMA guidelines on advanced therapy medicinal products align with FDA standards, facilitating trans-Atlantic supplier qualification. EU-funded Horizon projects encourage university participation in industrial biomanufacturing, lifting baseline demand for research-grade competent cells. Collectively, regional cooperation keeps the competent cells market in Europe on a balanced trajectory despite slower underlying population growth.

Regulatory Landscape

Regulatory requirements affecting competent cells are driven mainly by end-use, particularly when cells, plasmids, or microbial starting materials support regulated biomanufacturing and advanced therapy medicinal products (ATMPs). In the European Union, manufacture for ATMP clinical supply ties to EU GMP expectations (EudraLex Volume 4, Part IV) and the EMA quality, non-clinical, and clinical guidance for investigational ATMPs, which raises the bar for traceability, contamination control, and starting-material characterization across the supply chain.

In the United States, FDA cellular and gene therapy guidances and related potency-testing expectations shape how upstream inputs and process controls are justified in filings, increasing pressure for consistent, well-characterized transformation systems in qualified workflows. Cross-border movements also matter: biological materials imported into the United States must meet documentation, packaging, labeling, and declaration requirements under 42 CFR 71.54. Export-control changes can affect enabling lab technologies, including the US Department of Commerce action effective January 16, 2025 that adds controls on certain laboratory equipment and related technology tied to dual-use concerns. Standards used to formalize operational controls also influence procurement and audit readiness, including ISO 24088-1:2022 for biobanking of bacteria and archaea and ISO/TS 5441:2024 on competence requirements for biorisk management advisors in laboratories handling hazardous biological materials.

Competitive Landscape

The competent cells market reveals moderate consolidation. Thermo Fisher Scientific, Merck KGaA, and New England Biolabs leverage global logistics and broad reagent portfolios to protect incumbency. Thermo Fisher’s USD 4.1 billion buyout of Solventum’s purification and filtration business enlarges an integrated upstream-to-downstream channel that captures value beyond cell transformation reagents. Merck expands its Sigma-Aldrich legacy strains with CRISPR-optimized offerings calibrated to high-molecular-weight plasmids, and New England Biolabs pushes strain diversification for niche mutagenesis and difficult-to-clone sequences.

Competition pivots on transformation efficiency and automation compatibility rather than price. Vendors validate 96-well plate presentations that integrate with Beckman, Hamilton, and Tecan robots, reducing manual thaw and aliquoting steps in high-throughput screens. Product data sheets highlight cfu/µg consistency across wells, a metric that now influences purchasing decisions as strongly as raw efficiency numbers. Suppliers without automated format options risk losing bids to centralized purchasing units at university core facilities.

Disruptors enter via synthetic biology pathways. Asimov’s AI-guided CHO Edge algorithms remove iterative wet-lab optimization, lowering barriers to cell line development and potentially skirting traditional competent cell use for certain applications. Sutro Biopharma’s large-volume cell-free platform challenges the concept that living cells are required for protein expression, introducing a parallel consumables demand that could siphon budget from classic transformation reagents. Long-run success will depend on whether these alternatives match the versatility and cost-profile of traditional bacteria-based competence.

Competent Cells Industry Leaders

Thermo Fisher

Merck KGaA

New England Biolabs

Takara Bio

Agilent Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product whitespace is widening beyond traditional E. coli catalog offerings as synthetic biology programs push non-model chassis and accelerate build cycles. Academic work in 2026 points to the direction of travel, with enhanced natural competence in Bacillus subtilis using inducible promoters reporting a 45-fold increase in transformant yield versus conventional methods. In parallel, a 2026 engineered strain (NBx CyClone) derived from Vibrio natriegens was presented as a faster-growing alternative for cloning workflows. Together, these signals support an opportunity for suppliers to commercialize ready-to-use competent cells and validated protocols for non-traditional hosts, including plate and strip-tube presentations that fit automated liquid handling.

A second opportunity sits at the overlap of regulated bioprocessing and supply assurance. As CRISPR and ATMP development increases scrutiny of starting materials, buyers increasingly distinguish between research-grade reagents and documented, qualified cell banks and competent cell lots that can fit controlled environments. This aligns with the market shift already visible in high-throughput labs adopting automation-friendly formats, and with government-backed infrastructure such as the National Science Foundation USD 75 million allocation to five biofoundries, which institutionalizes standardized, repeatable transformation workflows and sustains reagent purchasing at scale.

Recent Industry Developments

- February 2026: Researchers reported the engineered strain NBx CyClone derived from Vibrio natriegens as a faster-growing alternative chassis for cloning workflows. The work highlights a shift toward non-model hosts, creating whitespace for vendors to offer competent-cell products and validated transformation protocols beyond standard E. coli strains.

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum's purification and filtration unit for USD 4.1 billion to strengthen end-to-end bioproduction workflows. The acquisition expands bundled upstream-to-downstream offerings, tightening competitive pressure on standalone reagent suppliers that depend primarily on transformation consumables.

- May 2024: Hovione and iBET formed ViSync Technologies to develop delivery systems for complex biologics, including gene and cell therapies. Increased activity in advanced modalities supports demand for higher-quality molecular biology workflows upstream, reinforcing the value of traceable inputs used in plasmid construction and related transformation steps.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the competent cells market covers ready-to-use microbial cells that are manufactured and sold specifically for DNA uptake in lab workflows, and the revenue counted is the product value realized by suppliers across regions.

Scope exclusions: Services, lab instruments, plasmid DNA, and general cell culture reagents that are not sold as competent cells are excluded from the market value.

Segmentation Overview

- By Cell Type

- Chemically Competent Cells

- Electrocompetent Cells

- By Application

- Protein Expression

- Cloning & Sub-cloning

- Mutagenesis

- Others

- By End User

- Biopharmaceutical Companies

- Contract Research/Manufacturing Organizations (CROs/CDMOs)

- Academic and Research Institutes

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the starting view of demand and supply, and to set realistic assumptions on how cloning and protein expression work is trending in universities, biotech labs, and CRO settings. We reviewed public sources such as NIH and NSF funding statistics, OECD and World Bank R&D indicators, and trade and customs statistics where lab reagent flows can be directionally checked. Regulatory and standards-facing references, such as FDA and EMA guidance pages and ISO documentation around lab quality systems, were also used to understand where adoption tends to be higher.

On the supply side, we leaned on annual reports, investor presentations, product catalogs, and press releases to map what is being sold and how product formats are positioned. Peer-reviewed papers indexed in sources such as PubMed helped track common host strains and transformation methods, which later supported our stress-test of mix and efficiency assumptions. When public financial disclosure was limited, we used paid subscriptions for company financials and intelligence, patent databases, and an import or export shipment-level database selectively to validate exposure and directionality. The sources listed above are illustrative, and we checked many other public and paid references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on practitioners and decision-makers who touch competent cells purchasing and usage, including suppliers, distributors, lab procurement teams, and bench-level users in academic and biopharma labs. We used these conversations to validate practical split assumptions, such as how often electrocompetent cells are chosen for high-efficiency needs, and what pricing movement looks like across different pack sizes and efficiencies. Since this is a global market, we ensured coverage across key usage hubs in APAC, EMEA, and the Americas so regional differences in research intensity and lab budgets could be reflected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 52% |

| Mid tier: 46% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 15% | Managers: 54% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the demand pool is reconstructed using life-science R&D intensity and active molecular biology workload indicators, and then it is narrowed to the share of workflows that typically consume competent cells. Those totals are then split by major geographies and adjusted using practical adoption checks gathered from interviews, including where labs show a preference for chemical versus electroporation based on lab type. To keep the totals realistic, we run selective bottom-up approximations in parallel, using sampled price points by cell efficiency and pack format, along with supplier and channel feedback on volumes, and then we tune the model when the two views do not align.

Inputs used in the model include public R&D spending direction, funding signals tied to genetic engineering and synthetic biology activity, the mix of cloning versus protein expression use, average units consumed per project cycle, and observed pricing differences by transformation efficiency. When gaps appear in bottom-up inputs, which is common for smaller suppliers and private labels, we use range-based assumptions anchored to comparable catalog pricing and distributor feedback, then limit the impact using conservative share caps. Forecasting is carried forward using scenario analysis supported by expert views on how research funding, lab throughput, and replacement cycles are likely to move, followed by an annualized price progression that is tested against interview-based expectations.

Data Validation & Update Cycle

Outputs are checked through multiple passes, where totals are compared with independent signals such as research funding direction, publication intensity in relevant methods, and supplier commentary on demand. If a region or segment shows an unusual jump, the drivers are re-checked, assumptions are revisited, and targeted re-contacts are triggered to confirm whether the shift is real or model-driven. Before sign-off, another analyst reviews key inputs, conversion steps, and calculations to catch avoidable errors and double counting.

The study is refreshed annually, and interim updates are made when material events can change demand, pricing, or supply availability. Right before delivery, the content and numbers are re-validated with a fresh scan of public updates so clients receive the latest view available at that time.

Mordor Intelligence's Competent Cells Market Size Compared Against Other Published Estimates

Published market values for competent cells can look far apart, even when the topic sounds the same, because each publisher picks its own year anchors, product boundaries, and pricing logic. Differences also show up when models assume a faster ramp for advanced cloning needs versus a steadier lab budget environment, which then flows into the forecast curve.

The main gap comes from whether revenues outside ready-to-use competent cell products are folded in. In Mordor Intelligence calculations, the total is limited to competent cells sold as products for transformation workflows, with pricing normalized to typical catalog and channel ranges for the stated year rather than blended lab-reagent baskets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.65 B (2026) | |

| Global Research Publisher A | USD 2.25 B (2024) | Uses an earlier base year and may mix adjacent molecular biology consumables into the revenue pool, which can pull the 2024 value away from a product-only competent cells count. |

| Industry Research Group B | USD 2.24 B (2024) | Anchors sizing to 2024 and can apply a higher growth curve from broad biotechnology activity, without always showing how transformation-only usage rates and price tiers were validated by region. |

The comparison shows that most of the spread is explained by year selection and what gets counted as part of the revenue pool, followed by how quickly prices and usage are assumed to move. By keeping the model tied to observable workflow adoption and practical price tiers, we end up with a market size that is easier to trace back to clear inputs and re-check over time.

Key Questions Answered in the Report

What is the current value of the competent cells market?

The market stands at USD 2.65 billion in 2026 and is projected to reach USD 3.91 billion by 2031.

Which regional segment leads the competent cells market?

North America holds the largest 41.74% share due to mature biomanufacturing infrastructure and sustained public funding.

Which application will grow fastest through 2031?

Cloning and sub-cloning is expected to post the highest 8.76% CAGR as CRISPR and synthetic biology libraries expand.

Why are electrocompetent cells gaining traction?

They offer transformation efficiencies above 5 × 10⁹ cfu/µg and come in automation-friendly plate formats that suit high-throughput labs.

How do high R&D costs influence competent cell demand?

Sponsors seek strains that maximize yield to control production costs, raising the bar on transformation efficiency and lot consistency.

What major corporate move reshaped the competitive landscape in 2025?

Thermo Fisher Scientific’s USD 4.1 billion acquisition of Solventum’s purification business integrated upstream and downstream capabilities, signaling further consolidation.

Page last updated on: