Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

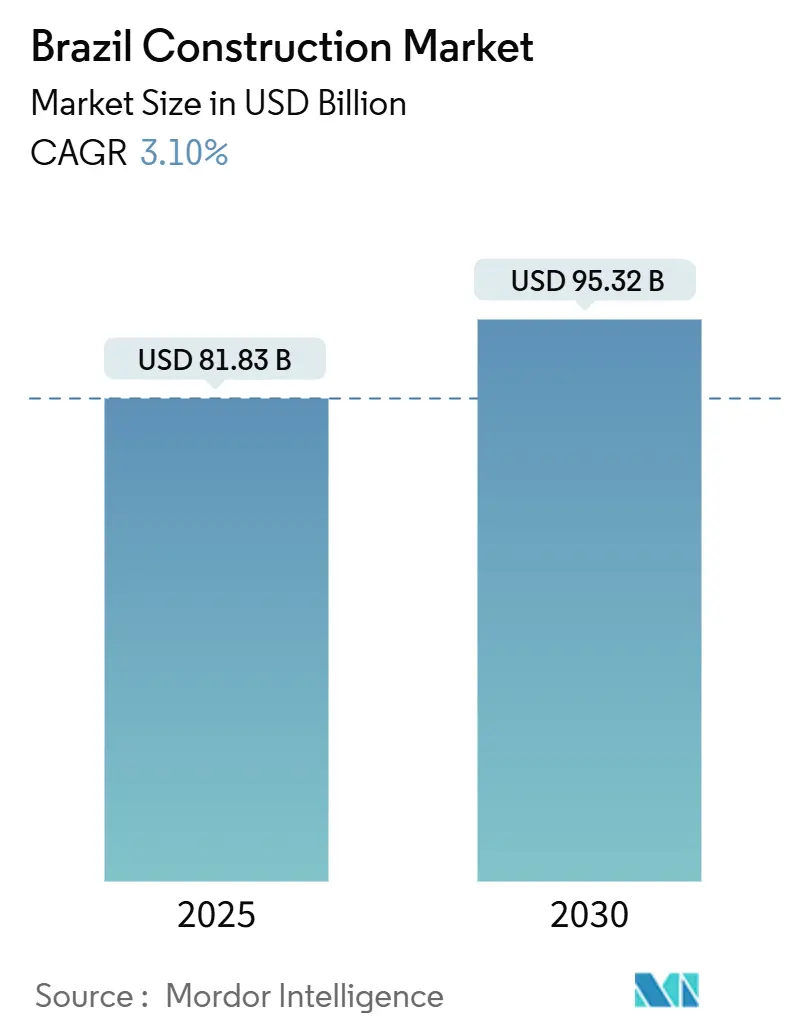

| Market Size (2025) | USD 81.83 Billion |

| Market Size (2030) | USD 95.32 Billion |

| Growth Rate (2025 - 2030) | 3.10% CAGR |

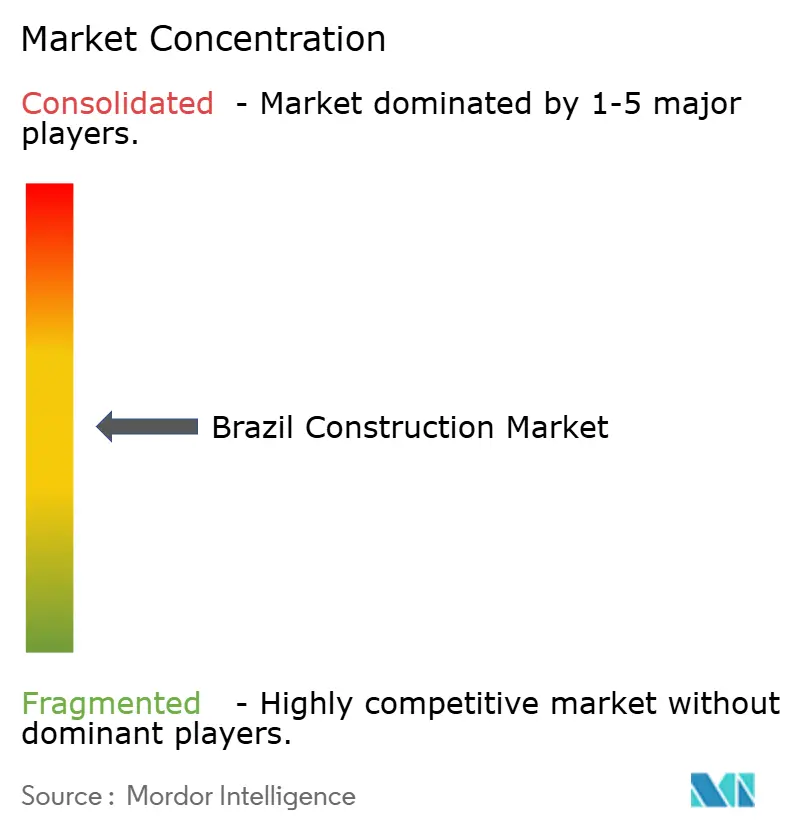

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Construction Market Analysis by Mordor Intelligence

The Brazil Construction Market size reached USD 81.83 billion in 2025 and is forecast to expand at a 3.1% CAGR to USD 95.32 billion by 2030. Public-sector infrastructure outlays under the third Growth Acceleration Program (PAC-3), deeper private participation in concessions, and the scaled-up Minha Casa Minha Vida (MCMV 3.0) housing scheme are keeping order books full despite high financing costs. Contractors posted a 48% jump in net profit in Q4 2024, mainly on brisk low-income housing demand. Modern methods such as modular construction are gaining traction as developers push for faster cycle times and lower waste, while a steady renewable-energy build-out is anchoring greenfield transmission and port works. Nevertheless, the elevated Selic policy rate complicates working-capital access, and supply-chain kinks in cement and rebar still impose scheduling risk. Medium-sized players are responding through joint procurement platforms and regional consolidation to regain pricing power in materials.

Key Report Takeaways

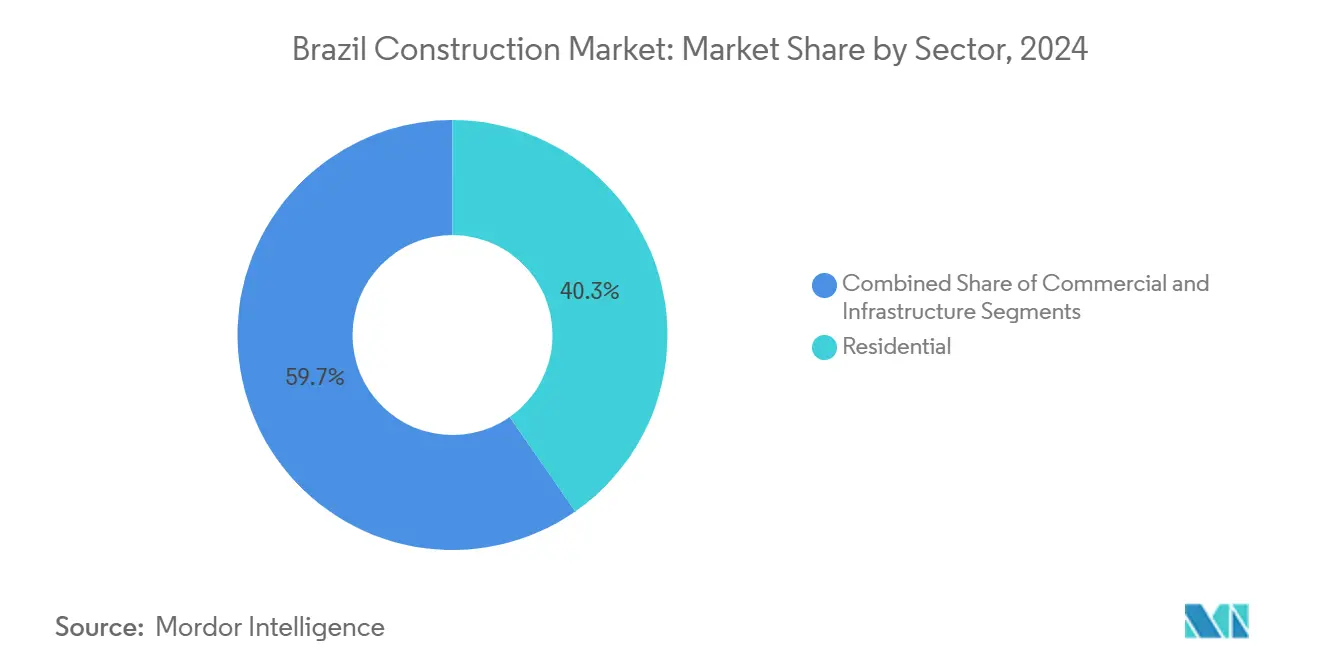

- By sector, residential construction commanded 40.32% of Brazil's construction market share in 2024; infrastructure is advancing at a 5.45% CAGR to 2030.

- By construction type, new builds accounted for 73.45% of the Brazil construction market size in 2024, while renovation is projected to accelerate at a 4.32% CAGR through 2030.

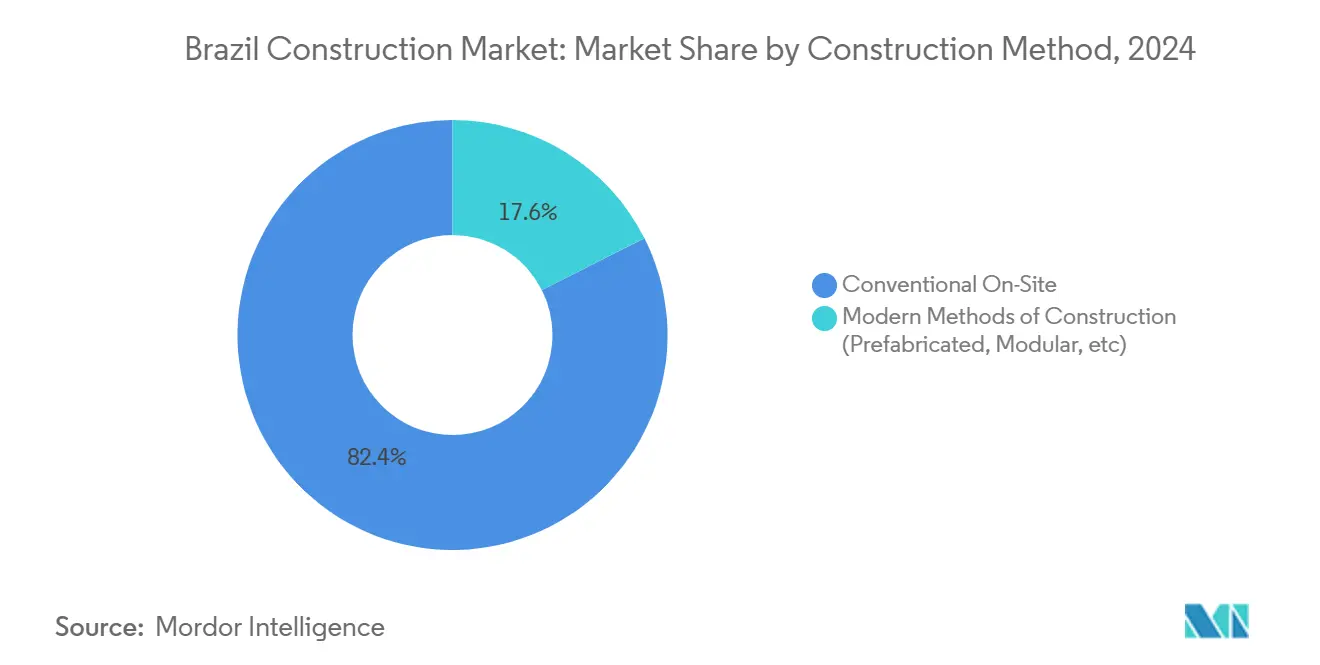

- By construction method, conventional on-site techniques held 82.43 of % Brazil construction market share in 2024; prefabricated and modular solutions are expanding at a 10.40% CAGR between 2025-2030.

- By investment source, public funds represented 62.34% of the Brazil construction market size in 2024, whereas private capital inflows are set to grow at a 5.65% CAGR over the forecast horizon.

- By geography, the Southeast led with a 55.43% share 2024; the Northeast registered the fastest growth at 4.90% CAGR through 2030.

Brazil Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PAC-3 infrastructure stimulus & PPP pipeline | 1.2% | Global, with concentration in Southeast and Northeast | Medium term (2-4 years) |

| Housing-deficit programs (Minha Casa Minha Vida 3.0) | 0.8% | National, strongest in Southeast and Northeast | Short term (≤ 2 years) |

| Utility-scale renewables build-out | 0.6% | Northeast and South regions primarily | Long term (≥ 4 years) |

| Industrialised & modular building adoption | 0.4% | Southeast concentration, expanding to Central-West | Medium term (2-4 years) |

| Re-industrialisation & EV-supply-chain facilities | 0.3% | National, early adoption in South and Southeast | Long term (≥ 4 years) |

| Digital-twin O&M mandates | 0.2% | Major metropolitan areas initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PAC-3 infrastructure stimulus and PPP pipeline

Brazil has earmarked USD 333.3 billion for the latest Growth Acceleration Program, with USD 120.0 billion reserved for private-sector participation across 92 concessions. Project scopes span highways, ports, and defense facilities, pushing tender backlogs beyond pre-pandemic levels. The Brazilian Development Bank approved USD 5.1 billion in infrastructure credit during H1 2024, more than doubling the prior-year period. Railway priorities include the 537 km FIOL1 corridor, expected to move 60 million t of freight annually by end-2026. Tax-incentivized infrastructure debentures are widening the investor base and partially insulating projects from bank-lending volatility. As large EPC contractors ramp up mobilization, multiplier effects are seen in cement, steel, and heavy-equipment orders.

Expanded Minha Casa Minha Vida program

The MCMV 3.0 scheme closed 2024 with 1.26 million units contracted toward its 2 million-unit 2026 target, backed by a USD 27.5 billion 2025 budget. Higher income ceilings now let households earning up to USD 1,568 per month access subsidized mortgages, broadening the demand pool. MRV Engenharia, the country’s largest homebuilder, plans a 17% rise in launches for 2025, citing the new brackets that lift achievable selling prices by USD 5,100–7,300 per unit. Integrated urban-mobility criteria require schools, clinics, and transit links within projects, boosting spill-over work for commercial, water, and road contractors. Since its inception in 2009, the program has delivered 8.4 million homes, and the latest version directly tackles the 5.9 million-unit housing gap[1]Ministério das Cidades, “Minha Casa Minha Vida alcança 1,26 mi de unidades,” gov.br.

Utility-scale Renewable Build-out

Wind and solar farms are reshaping regional order books. The 553 MW Babilônia Centro complex secured USD 620 million in BNDES financing covering 80% of capex, underscoring lender appetite for green assets. Vestas landed a 1.3 GW turbine supply with Casa dos Ventos, the largest onshore order in Latin America. Developers must also fund grid extensions; Brookfield sold 2,416 km of transmission lines for USD 843 million, recycling capital into new concessions. Petrobras added offshore wind, solar, and green-hydrogen projects to its 2024-2028 plan, signaling heavy civil-works demand at ports. These initiatives stretch the supply chain for high-voltage hardware and specialized concrete towers, sustaining a diversified construction workload.

Industrialized & Modular Building Uptake

The opening of a fully automated plant in Cascavel, Paraná, capable of turning out 2,400 housing units in six months on pre-molded lines, illustrates the shift toward factory-built solutions. Prefabricated assemblies reduce on-site labor needs by 30% and cut waste disposal volumes. Building Information Modeling (BIM) mandates in federal procurement are accelerating digital workflows, with contractors now submitting ISO 19650-aligned execution plans. Early adopters cite faster permitting and fewer re-work claims, improving margin resilience amid tight credit. Equipment amortization, however, remains a barrier for smaller firms, prompting consortium models where plants lease production slots to multiple developers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High real-interest-rate cycle tightening credit | 1.1% | National, particularly affecting Southeast markets | Short term (≤ 2 years) |

| Fiscal/political budget volatility | 0.7% | National, with federal project dependencies | Medium term (2-4 years) |

| Skilled-labour migration to agribusiness | 0.4% | Central-West and Northeast regions | Medium term (2-4 years) |

| Cement & rebar supply bottlenecks | 0.3% | National, acute in high-growth regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High real-interest-rate cycle, tightening credit

The Selic benchmark reached 14.25% in 2025, with analysts bracing for a possible 15% peak. Mortgage spreads widened and working-capital lines for contractors became costlier, eroding project IRRs. Cement deliveries slipped 1.7% in 2024 to 62 million t as households postponed upgrades. Developers trimmed pre-sales to preserve cash, and real-estate launches fell 16% before the full rollout of MCMV 3.0. Nonetheless, government concessional lenders and infrastructure debentures have softened the blow, preventing a deeper contraction in the project pipeline.

Fiscal and political budget volatility

Congressional negotiations over spending caps can delay disbursements for PAC-3 earmarks, creating stop-start execution cycles. The Court of Accounts flagged 17% of federally funded job sites as “slow-moving” due to payment backlogs. Municipalities reliant on value-added-tax transfers struggle to meet counterpart funding, affecting sanitation and urban-mobility schemes. Election-year shifts in gubernatorial priorities may re-rank project lists, causing procurement resets. Contractors hedge by prioritizing PPP or concession models where user-fee revenues cushion against budget deferrals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Holds Sway While Infrastructure Surges Ahead

The residential segment captured 40.32% of Brazil's construction market share in 2024, underpinned by the robust pipeline of MCMV 3.0 contracts and strong rental-housing appetite in São Paulo. Developers such as MRV and Brookfield channeled capital into multifamily towers that maintain occupancy even as mortgage demand softens. Commercial starts were more selective; premium offices like the 219-meter Alto das Nações move forward, yet mid-range launches receded. Infrastructure is the main growth engine, forecast to post a 5.45% CAGR through 2030 as highway, rail, and energy concessions crowd the tender calendar. Contractors are scaling precast yards and tunneling teams to handle simultaneous megaprojects, while margin discipline is tightening through lump-sum EPC contracts.

Demand patterns varied inside residential construction. Rental-only funds raised USD 49 million in 2024, targeting middle-income tenants seeking flexible leases, and new-build condos priced under USD 100,000 sold quickly in satellite cities. On the infrastructure front, the USD 150 million Salvador-Itaparica bridge loan and a USD 38.8 billion PPP roster affirm government intent to close logistics gaps. Electric-vehicle value-chain facilities are clustering in Minas Gerais and São Paulo, spurring feeder-road improvements. Healthcare has also accelerated; Rede D’Or set aside USD 1.47 billion to add 5,400 beds by 2028, lifting demand for specialized MEP contractors.

By Construction Type: New Builds Dominate but Renovation Accelerates

New construction accounted for 73.45% of the Brazil construction market size in 2024 as greenfield housing and infrastructure kept crews busy. The renovation niche, however, is gaining speed with a 4.32% CAGR projection on the back of aging bridges, schools, and commercial blocks. BNDES cleared USD 1.43 billion for upgrades on BR-116, BR-465, and BR-493, creating 24,000 jobs and stimulating concrete and asphalt orders. Contractors specializing in structural strengthening and energy retrofits are booking longer-cycle frameworks, reflecting regulatory pushes for efficiency labels under PROCEL Edifica.

Retrofit favorability extends beyond transport networks. São Paulo is analyzing a USD 1.12 billion expansion of the Anchieta-Imigrantes system, adding twin tunnels and viaducts to ease port-bound freight. Industrial plants face mandatory emissions monitoring once Brazil’s Carbon Trading System is active, prompting early abatement retrofits in cement and steel mills. Commercial landlords are investing in HVAC and façade upgrades to command green-lease premiums. The combined renovation pipeline, therefore, offers counter-cyclical stability during soft patches in new-home sales[2]Governo do Estado da Bahia, “Contrato de financiamento da Ponte Salvador-Itaparica,” ba.gov.br.

By Construction Method: Conventional Still Rules, Modular Rises Rapidly

Traditional on-site techniques retained an 82.43% share in 2024, but prefab and modular builds are sprinting at a 10.40% CAGR as developers chase shorter payback periods. The automated Cascavel factory, a USD 39.2 million investment, showcases robotized casting that embeds electrical and plumbing lines, trimming on-site trades. Large social-housing lots are ideal candidates for repeatable modules, and state governments are drafting standards to harmonize joints, finishes, and logistics. Equipment vendors report order backlogs for concrete 3D printers, while universities partner on design catalogs compatible with BIM workflows.

Digital adoption is the bridge between methods. Ministries now require BIM Execution Plans in nationally funded jobs, compelling even small consortium partners to upgrade software. Real-time progress dashboards and drone-based as-built scans cut scheduling disputes. Yet up-front capex and talent shortages hinder diffusion. Trade associations are lobbying for accelerated depreciation on smart-factory assets to level the field. Coupled with modular financing models, these policy nudges could lift industrialized techniques beyond the current niche.

By Investment Source: Public Outlays Remain Predominant, Private Capital Gains Pace

Government budgets delivered 62.34% of 2024 spending, reflecting PAC-3 and the scaled-up housing mandate. User-fee concessions and debenture placements, though, will push private allocations to a 5.65% CAGR through 2030. Brazil plans USD 73.0 billion in private infrastructure commitments for 2025-2029, buoyed by water-utility and toll-road auctions. The partial privatization of Sabesp alone added USD 12.9 billion to the five-year tally. Banks have pivoted from direct lending to project structuring, with BNDES acting as a transaction adviser rather than sole financier.

M&A activity indicates appetite for operating portfolios: cement maker CSN is eyeing InterCement assets amid a USD 2.8 billion restructuring, while global funds target transmission-line sales to lock in regulated yields. Higher interest rates discourage IPO exits, so sellers lean on strategic buyers. PPP frameworks, once plagued by red tape, now feature template contracts vetted by the Federal Court of Accounts, reducing legal uncertainty. All told, a more balanced capital stack is emerging, mitigating fiscal-budget shocks.

Geography Analysis

Brazil’s Southeast cluster retained its 55.43% share in 2024, led by São Paulo’s dense pipeline of high-rise condominiums, premium offices, and the USD 1.12 billion Anchieta-Imigrantes upgrade. Abundant engineering capacity, deeper capital markets, and a strong municipal bond program enable continuous contracting, even when federal disbursements lag. Developers bundle air-rights and mixed-use zoning to optimize plot yields, while city authorities fast-track housing permits that align with transit corridors.

The Northeast region, though smaller, charts a 4.90% CAGR to 2030 as federal planners channel PAC-3 funds toward economic-corridor projects. The USD 24.5 million Salvador cable-car scheme and the 537 km FIOL1 rail revival extend construction footprints beyond coastal capitals. Wind-farm clusters across Bahia and Rio Grande do Norte drive auxiliary substation and service-road contracts. Higher public-sector multipliers underpin a rapid skills migration, narrowing the historical labor gap vis-à-vis São Paulo.

Southern states display a blend of industrialized buildings and upscale tourism assets. The Cascavel smart-factory’s 2,400-unit annual run provides a testbed for modular codes, and port authorities in Paranaguá upgrade berths to handle offshore-wind components. Luxury hospitality builds in Santa Catarina, bolstering specialized façade and fit-out trades. Meanwhile, Central-West corridors such as the USD 0.48 billion Integration Highway unlock grain-belt logistics, triggering warehouse and cold-chain investments. Together, these regional narratives create a balanced demand mosaic that fortifies national resilience.

Competitive Landscape

Brazil’s contractor universe is moderately concentrated, with the top five players holding a moderate percentage of the ongoing works. Market leaders such as Andrade Gutierrez are restructuring capital stacks. Its USD 476 million foreign-note renegotiation frees headroom for new PAC-3 bids. Cement majors Votorantim Cimentos and CSN capitalize on InterCement’s USD 2.8 billion workout to purchase surplus plants and shore up distribution footprints. Foreign entrants like Vinci Construction clinched a USD 163 million civil package, signaling renewed international appetite for Brazilian margins[3]Governo do Paraná, “Fábrica automatizada de casas em Cascavel,” pr.gov.br.

Digitization is a primary battleground. Firms embedding BIM and drone mapping shave scheduling overruns and strengthen ESG credentials demanded by multilaterals. Intertek’s takeover of TESIS testing labs extends quality-control coverage across façades, concrete, and thermal systems, giving it a service-layer advantage. Automated precast factories act as disruptive capacity hubs, letting alliances of regional builders compete head-to-head with longstanding giants in social-housing tenders.

Regulatory shifts in carbon accountability add another competitive filter. Companies with verified lifecycle-emissions inventories are better placed to win BNDES-financed jobs that apply green-credit criteria. Contractors diversify revenue via operations-and-maintenance concessions, expanding annuity streams from highways and wastewater plants. Heightened due diligence by equity sponsors raises the threshold for governance compliance, nudging smaller, under-capitalized firms toward mergers to meet bonding and disclosure norms.

Brazil Construction Industry Leaders

MRV Engenharia

Cyrela Brazil Realty

Direcional Engenharia

Tenda

Gafisa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: São Paulo raised planned investment on the 285 km Paranapanema highway lot to USD 1.12 billion; auction slated for Q3 2025.

- January 2025: Bradesco BBI sought to seize Mover Group’s 14.86% stake in CCR as collateral on USD 2.8 billion debt following a December 2024 restructuring filing.

- January 2025: Sweden’s VBG Group acquired Italytec Imex for USD 50.9 million to widen HVAC offerings in Brazilian off-road vehicles.

- December 2024: Bahia state secured up to USD 150 million from CAF for the Salvador-Itaparica bridge, including BA-001 upgrades.

Brazil Construction Market Report Scope

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Region

| Southeast(São Paulo, Rio de Janeiro, Belo Horizonte) |

| South(Curitiba, Porto Alegre, Florianópolis) |

| Northeast(Salvador, Recife, Fortaleza) |

| Central-West(Brasília, Goiânia) |

| North(Manaus, Belém) |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Region | Southeast(São Paulo, Rio de Janeiro, Belo Horizonte) | |

| South(Curitiba, Porto Alegre, Florianópolis) | ||

| Northeast(Salvador, Recife, Fortaleza) | ||

| Central-West(Brasília, Goiânia) | ||

| North(Manaus, Belém) | ||

Key Questions Answered in the Report

How large is the Brazil construction market in 2025?

The market stands at USD 81.83 billion in 2025 and is projected to reach USD 95.32 billion by 2030.

Which segment is growing fastest in Brazilian construction?

Infrastructure construction shows the quickest expansion, advancing at a 5.45% CAGR through 2030 on the back of PAC-3 projects and renewable-energy grids.

How do high interest rates affect building activity?

A Selic rate exceeding 14% raises borrowing costs, discourages mortgage uptake, and squeezes contractor working capital, trimming short-term volumes despite public spending buffers.

What role do modular methods play in Brazil?

Prefabricated and modular techniques are scaling at a 10.40% CAGR as developers pursue quicker delivery and lower waste; the new Cascavel factory exemplifies this shift.

Which region offers the best growth prospects?

The Northeast leads with a 4.90% forecast CAGR through 2030, fueled by mega-bridge projects, railway corridors, and sizable wind-farm clusters.

Is private investment increasing in Brazilian construction?

Yes, private commitments are set to rise to USD 73 billion between 2025-2029, supported by concessions in sanitation, highways, and power transmission.

Page last updated on: