Russia Automotive Actuators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

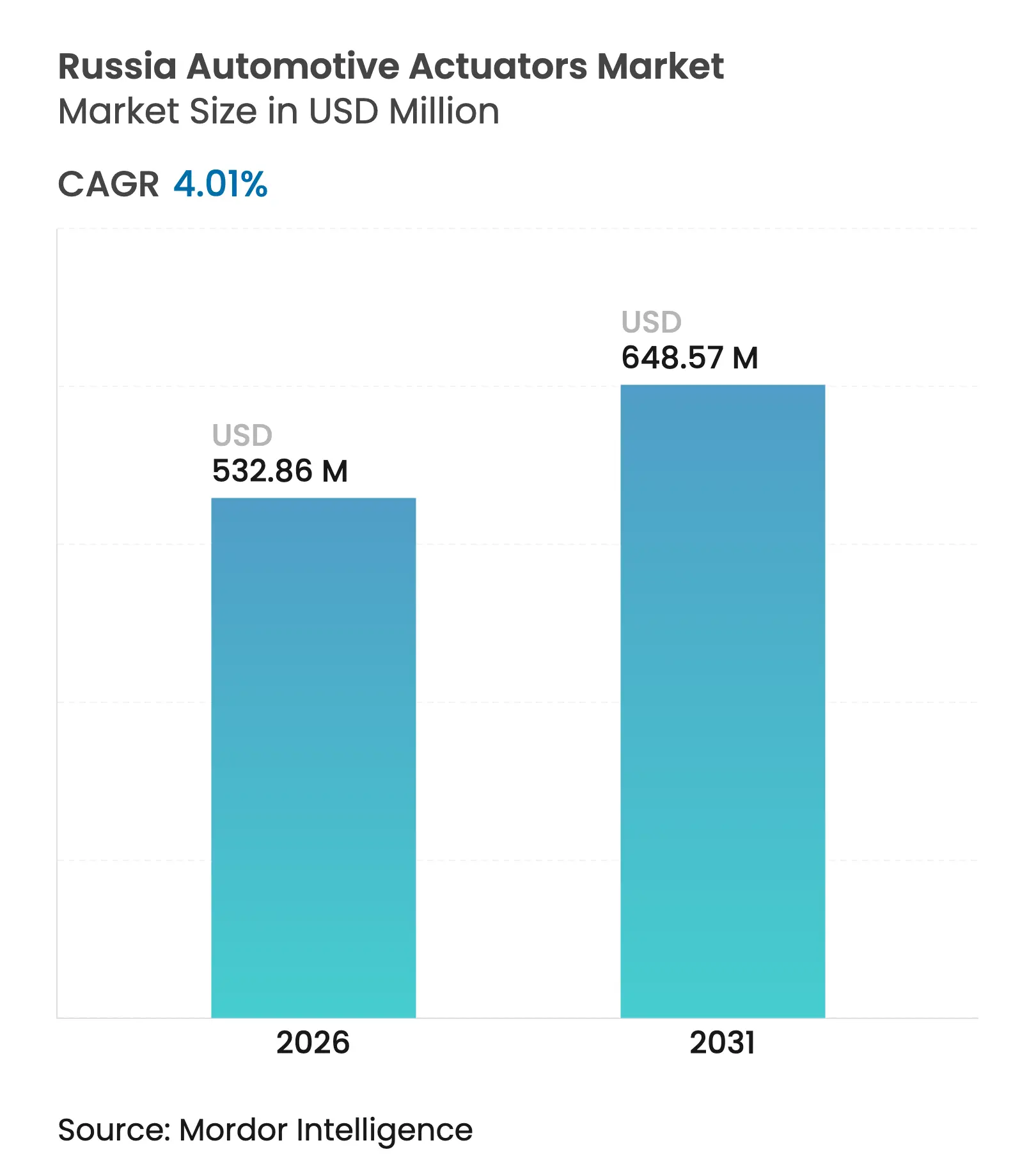

| Market Size (2026) | USD 532.86 Million |

| Market Size (2031) | USD 648.57 Million |

| Growth Rate (2026 - 2031) | 4.01 % CAGR |

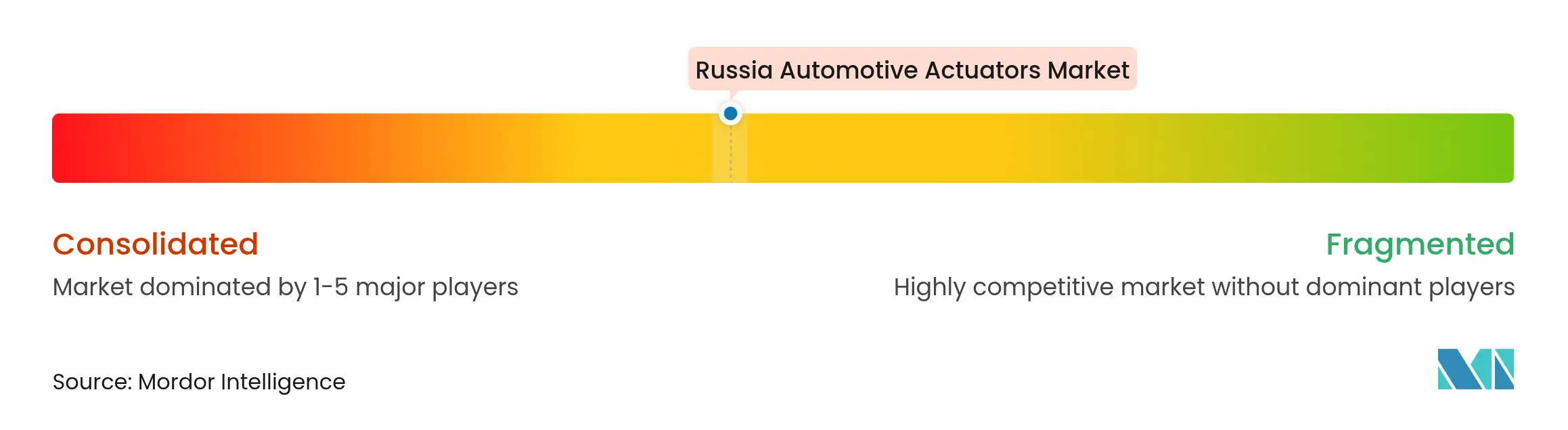

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Russia Automotive Actuators Market Analysis by Mordor Intelligence

The Russian automotive actuators market size was valued at USD 512.32 million in 2025 and estimated to grow from USD 532.86 million in 2026 to reach USD 648.57 million by 2031, at a CAGR of 4.01% during the forecast period (2026-2031). Steady demand for electrical and linear motion systems, combined with localization imperatives, supports this expansion even as sanctions reshape supply chains. Passenger-car production recovery, aging-fleet maintenance spending, and Chinese joint-venture assembly lines anchor near-term volumes. Over the medium term, electrification and ADAS penetration lift electronic content per vehicle, shifting value toward smart, low-voltage actuators. Competitive dynamics favor suppliers that localize precision machining and electronic sub-assemblies, while rouble volatility and semiconductor shortages keep cost management in focus.

Key Report Takeaways

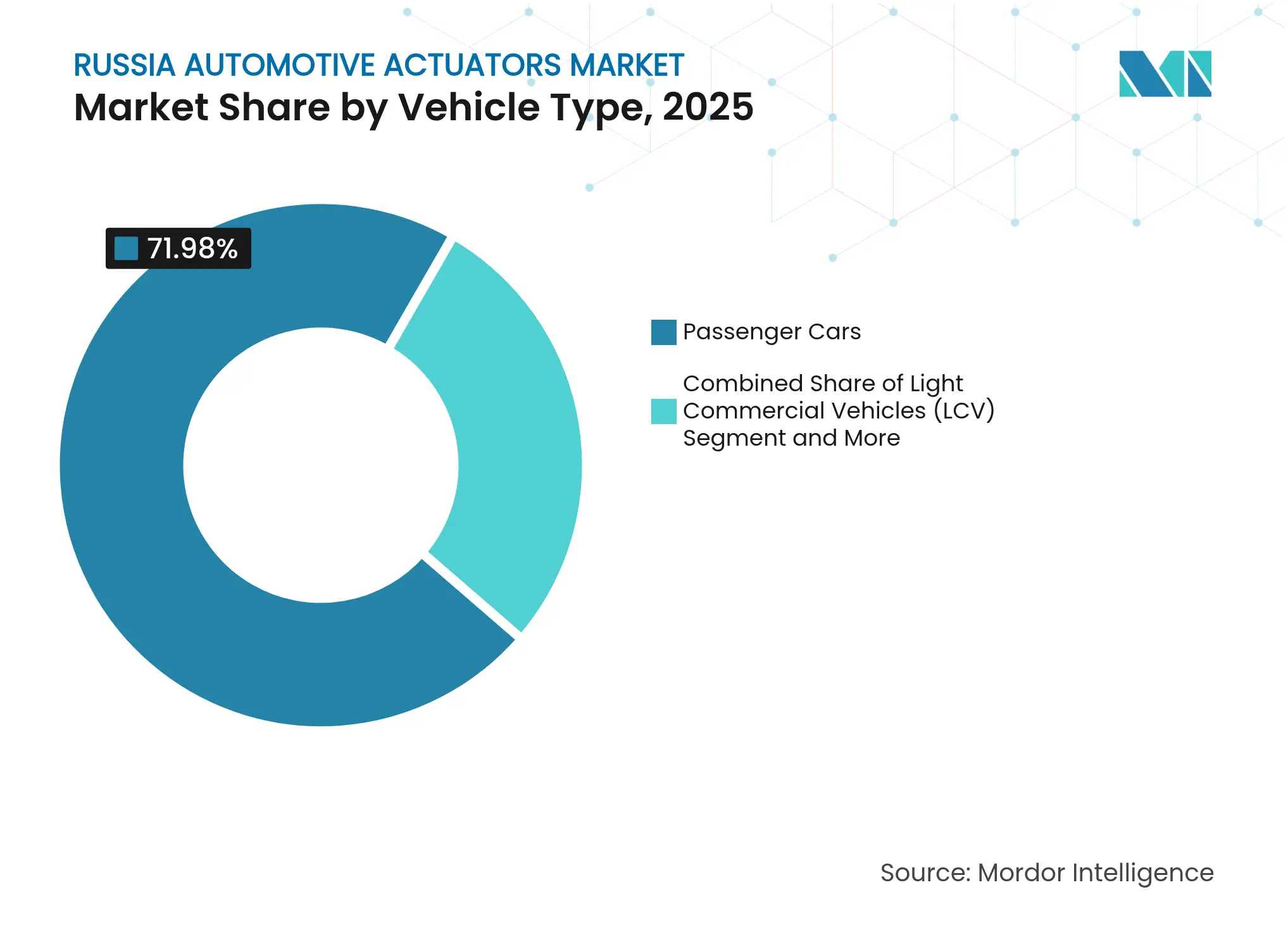

- By vehicle type, passenger cars held 71.98% of the Russian automotive actuators market share in 2025 and are forecast to expand at a 4.43% CAGR through 2031.

- By actuator type, electrical systems commanded a 62.58% share of the Russian automotive actuators market size in 2025 and are projected to grow at an 8.15% CAGR.

- By motion type, linear solutions accounted for 56.42% of the Russian automotive actuators market size in 2025, while rotary motion is set to advance at a 6.01% CAGR.

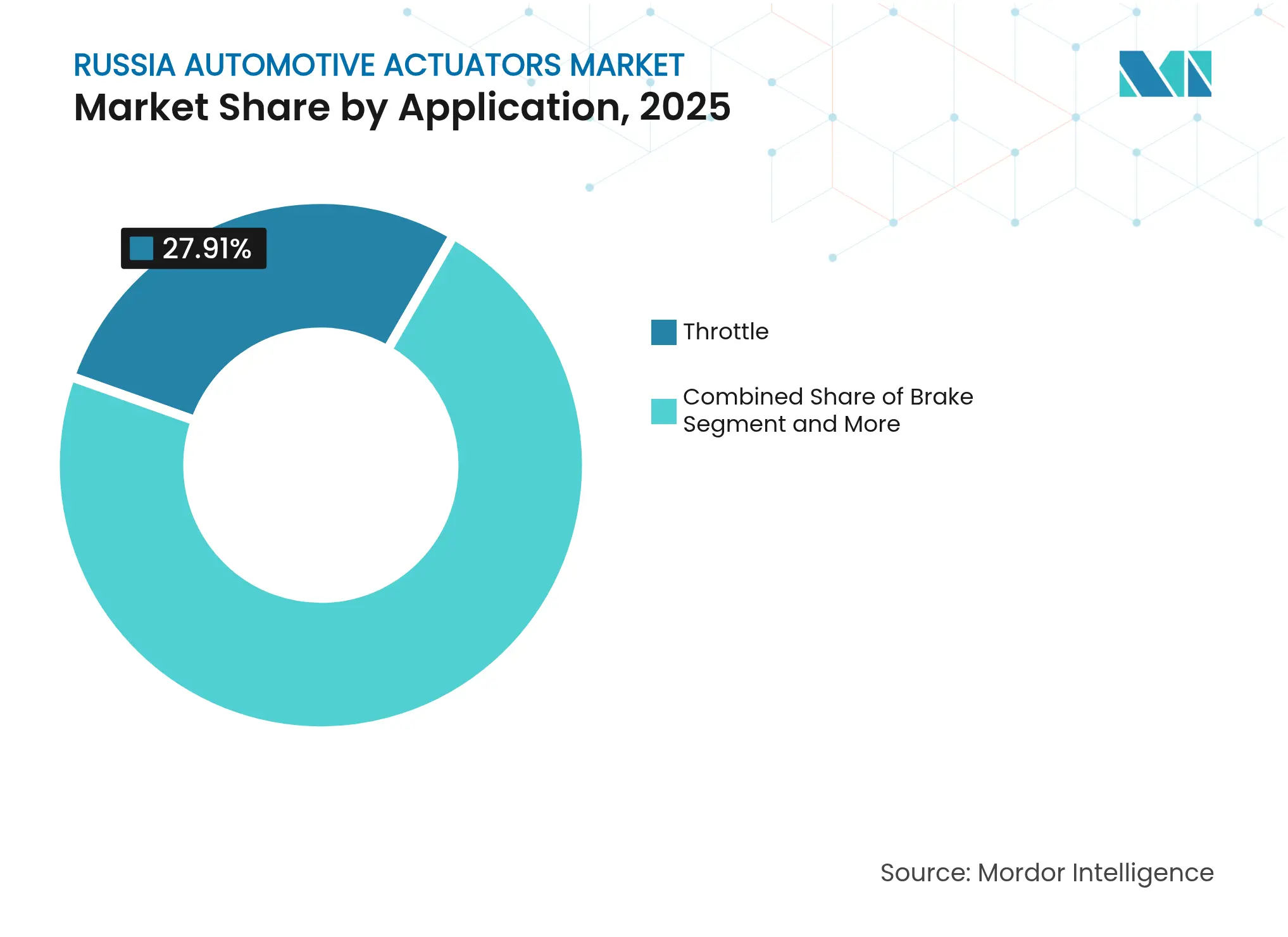

- By application, brake actuators recorded the fastest 7.02% CAGR, whereas throttle devices retained the largest 27.91% share of the Russian automotive actuators market size in 2025.

- By sales channel, OEM fitment delivered 80.87% of 2025 revenue; the aftermarket segment is poised for a 7.31% CAGR as vehicle age rises.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Automotive Actuators Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

EV Adoption Accelerating Low-Voltage E-Actuators' Demand EV Adoption Accelerating Low-Voltage E-Actuators' Demand | +1.8% | Moscow, St. Petersburg, Tatarstan | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Moscow, St. Petersburg, Tatarstan | Impact Timeline:Medium term (2-4 years) |

ADAS Penetration Raising the Actuator-Per-Vehicle Count ADAS Penetration Raising the Actuator-Per-Vehicle Count | +1.2% | Moscow, St. Petersburg, Leningrad Oblast | Long term (≥ 4 years) | |||

Recovery of Passenger-Car Production Recovery of Passenger-Car Production | +0.9% | Samara Oblast, Nizhny Novgorod Oblast | Short term (≤ 2 years) | |||

Quotas and Tax Credits for Tier-1 Suppliers Quotas and Tax Credits for Tier-1 Suppliers | +0.7% | Tula Oblast, Kaliningrad Oblast, Moscow Oblast | Medium term (2-4 years) | |||

Chinese JV Inflow Replacing Sanctioned Supply Lines Chinese JV Inflow Replacing Sanctioned Supply Lines | +0.6% | Tula Oblast, Kaliningrad Oblast, Moscow | Short term (≤ 2 years) | |||

After-Sales Boom from Ageing Fleet (13 Years and Above) After-Sales Boom from Ageing Fleet (13 Years and Above) | +0.5% | All federal districts | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

EV Adoption Targets Accelerating Demand for Low-Voltage E-Actuators

State incentives that cut charging fees and exempt electric cars from road taxes in major cities push manufacturers toward 12 V and 48 V architectures. Further, these programs reward suppliers able to integrate compact motor-driven throttle, HVAC, and battery-cooling actuators that maximise range. Moscow and St. Petersburg show the highest charger density, concentrating early demand. Chinese partners supply most controller chips, anchoring a new tier-two ecosystem.

ADAS and Autonomy Penetration Raising the Actuator-Per-Vehicle Count

Russian OEMs equip mid-range models with lane-keeping and automatic emergency braking to narrow the technology gap with imports. Pilot autonomous trials on Moscow expressways stimulate orders for precision rotary steering units and electro-mechanical brake boosters. Domestic electronics firms collaborate on real-time driver-monitoring platforms that call for responsive linear actuators. Growth clusters around R&D hubs in Moscow and St. Petersburg, where test fleets validate components under local climatic conditions. These programs gradually lift the actuator bill of materials and favour smart diagnostic features.

Recovery of Passenger-Car Production After 2024 Trough

National passenger car production rebounded to 753,754 units in 2024 as supply bottlenecks eased and consumer confidence returned. AvtoVAZ boosted deliveries 34.4% by accelerating Lada assembly in Togliatti and Izhevsk. This upswing transferred directly to actuator call-offs for powertrain, body, and comfort functions. Component suppliers clustered in Samara, Nizhny Novgorod, and Kaluga ramped up machining shifts but remained exposed to credit-cost spikes. Analysts expect production volumes to plateau after 2026 as sanctions pressure weighs on disposable incomes.

Government Localization Quotas and Tax Credits for Tier-1 Suppliers

The Ministry of Industry and Trade awards procurement points when sub-assemblies are machined, soldered, and tested domestically. Tier-1 suppliers reaching 65% localisation, such as joint-venture plants in Tula, qualify for reduced payroll tax and subsidised tooling finance[1]"Балльная система оценки локализации промышленной продукции", rctest.ru. Actuator makers that relocate gear-train milling, PCB population, and end-of-line calibration gain a bidding edge. The policy also encourages import substitution consortia that share laboratories and certification labs in Kaluga and Kaliningrad.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Semiconductor Shortages and Sanctions-Driven Import Curbs Semiconductor Shortages and Sanctions-Driven Import Curbs | -1.4% | All federal districts, most severe in Moscow, St. Petersburg | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:All federal districts, most severe in Moscow, St. Petersburg | Impact Timeline:Short term (≤ 2 years) |

Exit/Downsizing of Western OEMs Exit/Downsizing of Western OEMs | -0.8% | Kaluga Oblast, St. Petersburg, Moscow Oblast | Medium term (2-4 years) | |||

Rouble Volatility and Metal Price Swings Rouble Volatility and Metal Price Swings | -0.6% | All federal districts, manufacturing centers most affected | Short term (≤ 2 years) | |||

Domestic Precision-Machining Gap Domestic Precision-Machining Gap | -0.4% | Samara Oblast, Nizhny Novgorod Oblast, Tula Oblast | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Global Semiconductor Shortages and Sanctions-Driven Import Curbs

Neon supply disruptions, export controls on advanced lithography, and payment-system hurdles cut deliveries of MCU-based controller boards. AvtoVAZ halted 550 part numbers during 2024 stoppages, exposing electronic brake and steering lines to costly redesigns. Parallel imports via Turkic and Caucasus hubs partially fill gaps but inflate lead times. Short-term mitigation includes derating ADAS features and reverting to simpler relay-driven circuits, although that risks losing market appeal.

Exit/Downsizing of Western OEMs Dampens Near-Term Volumes

Plant mothballing by European and Japanese brands removed premium SUV and luxury sedan lines that carried high actuator content. Assembly closures in Kaluga and St. Petersburg displaced established supply chains, trimming overall demand despite rising Chinese share. Remaining OEMs renegotiate pricing, pressing suppliers already hit by currency depreciation. Some displaced vendors pivot to aftermarket kits, but scale losses hamper R&D budgets for next-generation smart systems.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Market Resilience

Passenger-car output accounted for 71.98% of the Russian automotive actuators market in 2025 and is expected to deliver a 4.43% CAGR. Robust localisation incentives, coupled with value-focused consumer preferences, sustain weekly build schedules even when credit conditions tighten. Light commercial vans absorb e-commerce parcel growth, while medium and heavy trucks rely on state infrastructure spending. Chinese brands leverage knock-down kits to tap the segment swiftly, raising local sourcing requests for throttle and HVAC modules.

The segment’s future remains entwined with localisation scores that unlock tax benefits. AvtoVAZ, Great Wall Motor, and newcomers such as Changan collectively raise the Russian automotive actuators market baseline volume through progressively higher trim levels. Ageing fleet averages at 13.6 years secure ongoing replacement orders, cushioning suppliers during cyclical dips. The convergence on Euro-6 equivalents and passive safety mandates further elevates actuator density per passenger car, pulling electronic and rotary variants into mainstream fitment.

Note: Segment shares of all individual segments available upon report purchase

By Actuator Type: Electrical Systems Lead Technological Transition

Electrical units delivered a 62.58% share in 2025 and will grow at an 8.15% CAGR as EV and 48 V mild-hybrid programs proliferate. Decarbonisation targets favour compact BLDC motor drives over vacuum or hydraulic devices, notably in turbo-wastegate and brake applications. Hybrid electro-hydraulic modules retain niches in heavy vehicles where force density remains critical.

Technology transfer from Sino-Russian ventures introduces modular printed-circuit assemblies and over-the-air firmware, accelerating the pivot toward smart diagnostics. Suppliers that mount PCB population lines locally qualify for localisation credits, strengthening the Russian automotive actuators market position. Dependence on imported ASICs remains a cost headwind, although state-funded micro-foundry projects aim to bridge the gap by 2028.

By Motion Type: Linear Applications Maintain Industrial Relevance

Linear products held a 56.42% share in 2025 thanks to their ubiquity in seat tracks, window lifts, and throttle bodies. Cost-effective rod-style designs meet domestic content rules with lower precision tooling compared with geared rotary alternatives. Rotary actuators, however, will post a 6.01% CAGR as steering-by-wire and mirror-adjust functions spread from premium to mass segments.

Shape-memory alloy technology enhances travel accuracy and frost resistance in both motion classes, aligning with Russia’s climatic demands. Domestic research institutes partner with metallurgy firms to scale SMA wire drawing, improving localisation metrics and strengthening the Russian automotive actuators market outlook for advanced motion solutions.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Application: Throttle Dominance Faces Brake System Growth

Throttle bodies contributed 27.91% of revenue in 2025, underpinning baseline volumes across gasoline, diesel, and hybrid engines. Regulatory pressure for electronic stability control and collision avoidance stimulates brake actuator demand, giving that niche a 7.02% CAGR through 2031. Seat comfort, HVAC blend, and mirror adjustment round out balanced portfolios that shield suppliers from single-application risk.

Brake growth is reinforced by forthcoming mandatory ABS rules on all new passenger cars, scheduled for 2026. Continental and Bosch already localise electronic brake booster machining, helping safeguard their Russia automotive actuators market share against low-cost competitors. Throttle relevance will taper in full battery-electric models, yet continues in hybrids and range extenders expected to dominate rural sales.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: OEM Fitment Leads While Aftermarket Accelerates

OEM contracts generated 80.87% of 2025 sales, reflecting long-term platform awards and localisation requirements. Volume security attracts multinational Tier-1 suppliers that invest in end-of-line calibration rigs and failure-analysis labs near assembly plants. The Russian automotive actuators market size attached to the aftermarket segment, however, will expand at a 7.31% CAGR as motorists retain vehicles longer amid economic uncertainty.

Price spikes for imported parts open space for domestic distributors carrying locally made or Chinese-sourced SKUs. E-commerce portals that promise 48-hour delivery to regional service garages widen reach, although counterfeit risk demands stricter traceability codes. Suppliers that blend OEM pedigree with retail logistics capture both channels and diversify exposure to cyclical assembly fluctuations.

Geography Analysis

The Central Federal District anchors more than one-third of Russia's automotive actuators market demand. Moscow’s proximity to regulatory bodies, fintech hubs, and premium dealerships creates a dense cluster where both OEM and aftermarket volumes converge. The Moscow Oblast hosts multiple Tier-1 machining parks that feed EV programs, while a high charger count sustains low-voltage actuator uptake. St. Petersburg and the Leningrad Oblast follow as legacy export gateways, retaining supplier campuses even after Western OEM retrenchment. Companies pivot these facilities toward Chinese model lines, safeguarding utilisation rates and sustaining orders for steering and braking assemblies.

Volga Federal District, led by Samara and Nizhny Novgorod Oblasts, remains the historic heartland of Russian vehicle manufacturing. AvtoVAZ’s Togliatti complex alone consumes tens of thousands of throttle and HVAC actuators monthly. Government co-investment in tooling and robotics helps regional plants reach localisation thresholds that underpin stable Russian automotive actuators market flows. Kaluga’s supplier belt, once dedicated to European brands, retools lines for Sino-centric platforms through technology-transfer accords that include actuator gear-train milling and PCB wash stations.

The Northwest, Siberian, and Far Eastern districts together provide a growing hinterland where commercial vehicle projects and resource extraction fleets spur hydraulic and pneumatic actuator demand. Kaliningrad’s special-economic-zone framework supports CKD assembly that relies on imported sub-assemblies, although its geographic separation raises shipping premiums. The Far East counts on cross-border trade with China to backfill semiconductor gaps, making Vladivostok a pivotal forwarding base for replacement parts. In rural Siberia, average vehicle age exceeds 15 years, sustaining robust aftermarket sales channels that distribute linear actuators for basic throttle and door-lock repairs. Overall, regional variations in powertrain mix, climate, and regulatory oversight drive a diverse tapestry of sourcing patterns across the Russia automotive actuators market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Global suppliers still command double-digit shares yet face a reshaped arena influenced by sanctions, currency swings, and rapid localisation. Rouble depreciation and import licensing delays, however, trimmed margins and prolonged inventory cycles. Western incumbents now lean on joint stocking centres and ruble-indexed contracts to cushion volatility.

Chinese entrants accelerate capacity roll-outs, most visibly at Great Wall Motors’ USD 500 million Tula factory that sources up to 65% of actuator content locally. Smaller private brands subcontract electronics to Shenzhen design houses and rely on Russian specialised forges for casings, which boosts local employment and satisfies government localisation audits. Domestic mid-tier suppliers capture white-space niches in gear-train hobbing and rotary-shaft sealing, benefiting from state subsidies that underwrite CNC acquisition. These trends collectively broaden the Russia automotive actuators market supplier base and heighten price rivalry.

Strategic repositioning also features consolidation among legacy European groups. The 2024 Schaeffler-Vitesco merger produced a EUR 25 billion powerhouse that combines e-mobility inverter know-how with mechanical actuation expertise, streamlining procurement for OEM chassis teams. Suppliers that deliver system-level solutions, combining motor, sensor, and controller software, are best placed to defend share as ADAS and autonomy lift content per vehicle across the Russia automotive actuators market.

Russia Automotive Actuators Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nexteer Automotive showcased steer-by-wire and rear-wheel steering systems, including handwheel and road-wheel actuators, positioning its portfolio for Russia’s next-generation safety programs.

- February 2025: AvtoVAZ cut output targets due to rouble devaluation and cost spikes on imported components such as actuator electronic boards.

Table of Contents for Russia Automotive Actuators Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1EV adoption targets accelerating demand for low-voltage e-actuators

- 4.2.2ADAS and autonomy penetration raising the actuator-per-vehicle count

- 4.2.3Recovery of passenger-car production after 2024 trough

- 4.2.4Government localisation quotas and tax credits for Tier-1 suppliers

- 4.2.5Chinese JV inflow replacing sanctioned supply lines

- 4.2.6After-sales boom from ageing fleet (13 years and above) fuels replacement demand

- 4.3Market Restraints

- 4.3.1Global semiconductor shortages and sanctions-driven import curbs

- 4.3.2Exit/downsizing of Western OEMs dampens near-term volumes

- 4.3.3Rouble volatility and metal price swings squeeze margins

- 4.3.4Domestic precision-machining gap slows localisation

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook (Smart, shape-memory and mini-actuators)

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value (USD))

- 5.1By Vehicle Type

- 5.1.1Passenger Cars

- 5.1.2Light Commercial Vehicles (LCV)

- 5.1.3Medium and Heavy Commercial Vehicles (MHCV)

- 5.2By Actuator Type

- 5.2.1Electrical

- 5.2.2Hydraulic

- 5.2.3Pneumatic

- 5.2.4Electro-hydraulic (Hybrid)

- 5.3By Motion Type

- 5.3.1Linear Actuators

- 5.3.2Rotary Actuators

- 5.4By Application

- 5.4.1Throttle

- 5.4.2Brake

- 5.4.3Seat Adjustment

- 5.4.4Mirror/Window and Closure

- 5.4.5HVAC and Air-mix

- 5.4.6Drivetrain (VVT, Turbo, E-waste-gate)

- 5.5By Sales Channel

- 5.5.1OEM Fitment

- 5.5.2Aftermarket Replacement

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves (JVs, localisation, MandA)

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Robert Bosch GmbH

- 6.4.2Continental AG

- 6.4.3Denso Corporation

- 6.4.4Mitsubishi Electric Corp.

- 6.4.5Nidec Corporation

- 6.4.6Hitachi Astemo

- 6.4.7BorgWarner Inc.

- 6.4.8Aptiv PLC

- 6.4.9Valeo SA

- 6.4.10ZF Friedrichshafen AG

- 6.4.11Johnson Electric Holdings

- 6.4.12Aisin Corp.

- 6.4.13Hyundai Mobis

- 6.4.14Magna International

- 6.4.15Mando Corp.

- 6.4.16Schaeffler AG

7. Market Opportunities and Future Outlook

- 7.1White-space & Unmet-Need Assessment

Russia Automotive Actuators Market Report Scope

The Russia Automotive Actuators Market report covers the current and upcoming trends with recent technological development. The report will provide a detailed analysis of various areas of the market by vehicle, product and drive type. The market share of significant actuator companies and country level analysis will be provided in the report.