Russia Automotive Pneumatic Actuators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

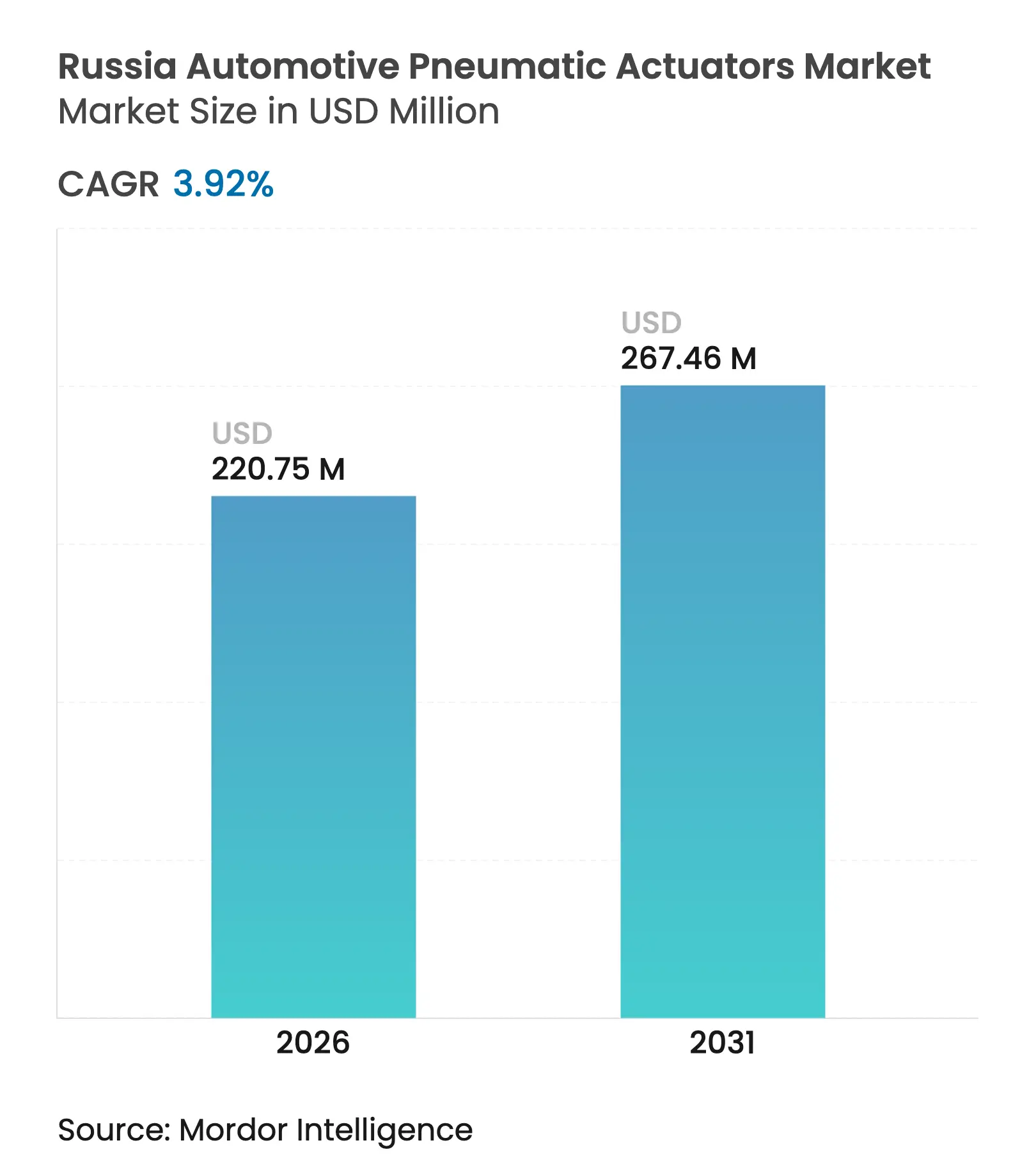

| Market Size (2026) | USD 220.75 Million |

| Market Size (2031) | USD 267.46 Million |

| Growth Rate (2026 - 2031) | 3.92 % CAGR |

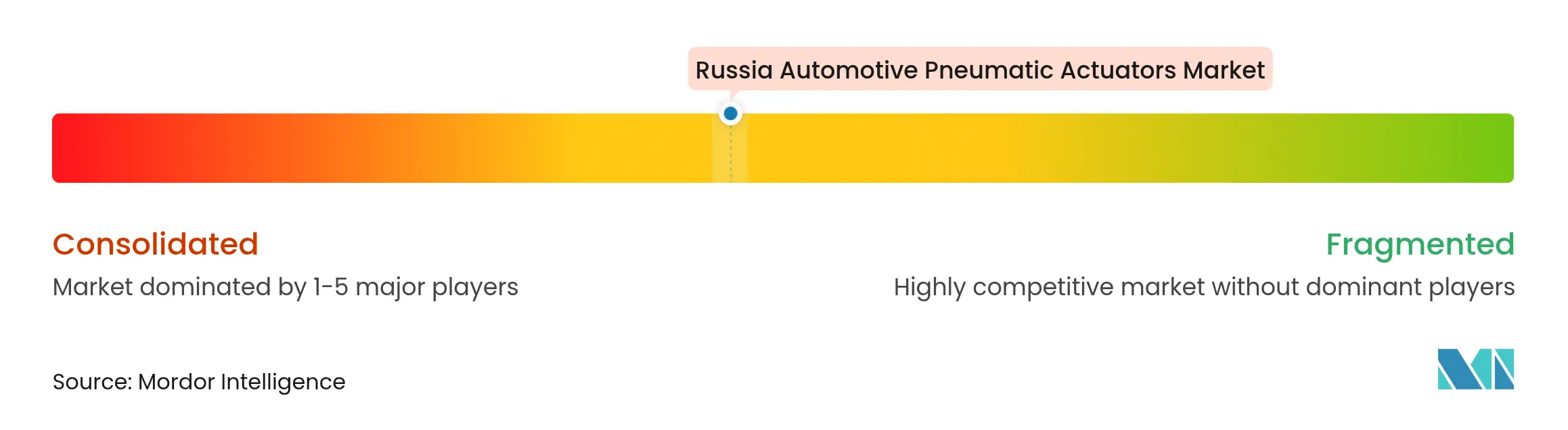

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Russia Automotive Pneumatic Actuators Market Analysis by Mordor Intelligence

The Russia automotive pneumatic actuators market size is expected to grow from USD 212.42 million in 2025 to USD 220.75 million in 2026 and is forecast to reach USD 267.46 million by 2031 at 3.92% CAGR over 2026-2031. Momentum comes from government localization programs, a rebound in domestic vehicle output, and expanding defense procurement that together keep actuation demand resilient despite sanctions and currency volatility[1]“Public procurement regulations,” Ministry of Finance of the Russian Federation, minfin.gov.ru . The Russia automotive pneumatic actuators market also benefits from ongoing fleet modernization, tighter safety regulations that favor brake systems, and accelerating investments in intelligent transport infrastructure that call for electro-pneumatic precision. At the same time, elevated recycling fees on imported sub-assemblies and a volatile ruble are prompting manufacturers to localize supply chains, a shift already visible in Special Investment Contract (SPIC) awards that reward domestic content targets. Technology transition is gradual; conventional vacuum-pneumatic designs still dominate, yet IoT-ready electro-pneumatic units are gaining traction as predictive-maintenance features move from pilots to scaled deployment in large fleets.

Key Report Takeaways

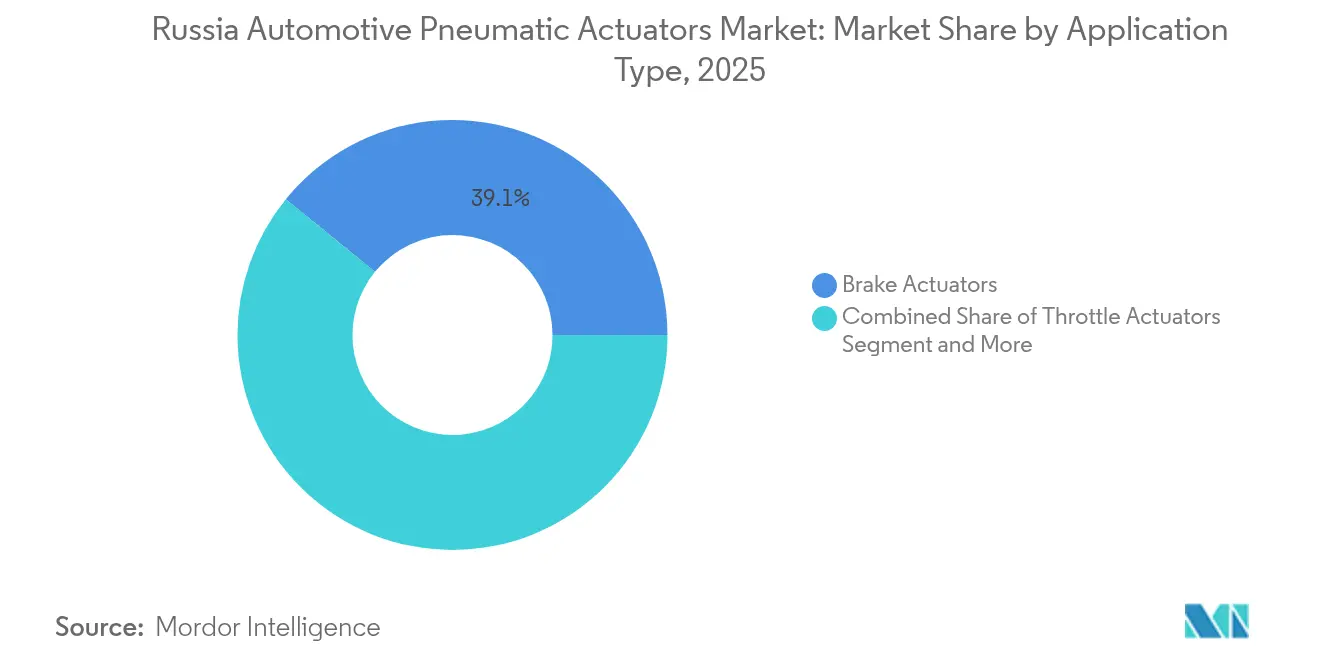

- By application, Brake Actuators led with 39.12% of Russia automotive pneumatic actuators market share in 2025, while Turbo Wastegate Actuators are forecast to expand at a 4.77% CAGR through 2031.

- By vehicle type, Passenger Cars held 64.58% share of the Russia automotive pneumatic actuators market size in 2025; Commercial Vehicles represent the fastest-growing category at a 5.18% CAGR to 2031.

- By sales channel, the Aftermarket commanded 63.10% share in 2025, whereas the OEM channel is set to post a 6.01% CAGR between 2026 and 2031.

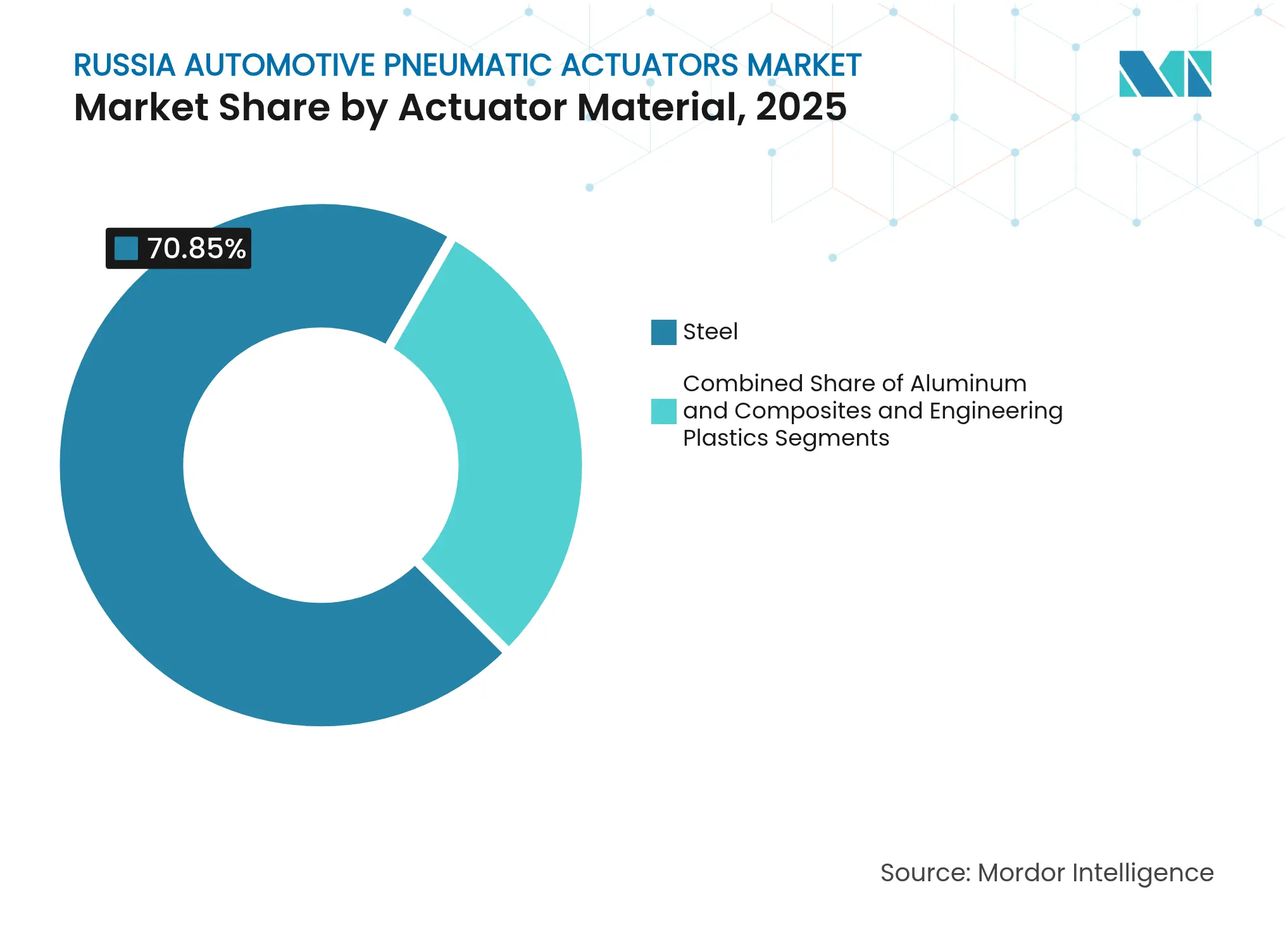

- By actuator material, Steel dominated with 70.85% revenue share in 2025, and Composites & Engineering Plastics are on track for 5.63% CAGR growth through 2031.

- By technology, Conventional Vacuum-Pneumatic systems accounted for 84.60% of 2025 revenue, yet Electro-Pneumatic systems are projected to rise at a 5.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Automotive Pneumatic Actuators Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government Localization Contracts (SPIC) Government Localization Contracts (SPIC) | +1.2% | Major auto hubs in Moscow, St. Petersburg, Kaluga | Medium term (2-4 years) |

( ~ ) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Major auto hubs in Moscow, St. Petersburg, Kaluga

|

Impact Timeline

:

Medium term (2-4 years)

|

State-Subsidized Sales Programs State-Subsidized Sales Programs | +0.8% | All federal districts | Short term (≤ 2 years) | |||

Growing Commercial-Vehicle Output Growing Commercial-Vehicle Output | +0.9% | Tatarstan, Ural regions, defense clusters | Medium term (2-4 years) | |||

Surge in Defense and Special-Purpose Vehicle Demand Surge in Defense and Special-Purpose Vehicle Demand | +0.7% | Uralvagonzavod corridor, KAMAZ belt | Long term (≥ 4 years) | |||

IoT-Enabled Predictive-Maintenance Adoption IoT-Enabled Predictive-Maintenance Adoption | +0.4% | Large urban agglomerations | Medium term (2-4 years) | |||

Low-Pressure Pneumatics for Hydrogen-Blend Engines Low-Pressure Pneumatics for Hydrogen-Blend Engines | +0.3% | Moscow, Tatarstan R&D centers | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Government localization contracts (SPIC)

SPIC agreements mandate high local content and offer tax incentives that favor Russian-made actuators across brake, throttle, and turbo wastegate systems. The federal RR90 billion automobile-platform program targets 80% localization and is expected to secure long-term demand from both civilian and defense OEM lines. AvtoVAZ’s USD 3 billion plan to reach 75% local content on the Lada Vesta underscores how SPICs pull actuator sourcing in-country, a dynamic that helped lift national auto sales 47% in 2024.

State-subsidized sales programs

Preferential loans and rebates kept new-car registrations resilient at 1.8 million units in 2024, translating into steady build schedules for actuator suppliers. Commercial vehicle turnover hit RR1.56 trillion, with trucks alone consuming three-quarters of that spend. Subsidies reward domestic brands, giving AvtoVAZ roughly one-third of unit sales in 2024, though pricing pressures limit its value share.

Growing commercial-vehicle output

KAMAZ sustained an 18.3% home-market truck share in 2024 and is scaling lines to fill military and export orders. Russia’s truck volume reached 126,200 units, and upcoming tank and armored-vehicle programs translate into larger-bore brake, exhaust and turbo actuation needs. The company’s new Senegal assembly plant shows how export diversification will keep Russia automotive pneumatic actuators market demand broad-based.

Surge in defense and special-purpose vehicle demand

The Ministry of Defense plans to field 1,500 tanks and 3,000 armored vehicles in 2025, embedding specialized pneumatic devices engineered for rugged duty cycles. New platforms such as the BTR-22 incorporate advanced actuation in mobility and survivability subsystems, reinforcing steady pull for domestic actuator specialists.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Sanctions-Driven Parts Shortages

Sanctions-Driven Parts Shortages

| -0.9% | Import-dependent regions | Short term (≤ 2 years) |

( ~ ) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Import-dependent regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

Rapid Substitution by Electric Actuators

Rapid Substitution by Electric Actuators

| -0.6% | Large cities, premium segments | Medium term (2-4 years) | |||

Volatile Ruble Inflates Imported Raw-material Costs

Volatile Ruble Inflates Imported Raw-material Costs

| -0.5% | All manufacturing centers | Short term (≤ 2 years) | |||

Rising Recycling Fee on Imported Sub-assemblies

Rising Recycling Fee on Imported Sub-assemblies

| -0.4% | Border areas, ports | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Sanctions-driven parts shortages

Payment bottlenecks to Chinese suppliers affect up to 90% of transactions, stretching lead times and forcing higher-cost secondary routes. The EU’s 17th sanctions package limits dual-use goods, adding compliance risks for actuator SKUs that also serve military programs.

Rapid substitution by electric actuators

Software-defined vehicle projects such as Continental’s Aumovio prioritize electro-mechanical devices. Premium EV and autonomous platforms coming to Russia’s urban showrooms require fewer pneumatic components, eroding future demand in those niches [2]“Aumovio launch press release,” Continental AG, continental.com.

Segment Analysis

By Application: Safety-Critical Brake Systems Dominate

Brake actuators generated the largest revenue slice in the Russia automotive pneumatic actuators market, holding 39.12% share in 2025, a figure that underscores mandatory safety compliance across all vehicle classes. Fleet upgrades in trucking and armored fleets demand robust, serviceable brake hardware, and this necessity anchors a stable baseline for suppliers. Turbo Wastegate Actuators, while a smaller niche, are slated for a 4.77% CAGR as OEMs downsize engines yet maintain torque via turbocharging. Throttle actuators retain a steady pull because electronic throttle control is now standard. Exhaust Gas Recirculation (EGR) actuators gain relevance as diesel and future hydrogen-blend engines chase NOx limits. Fuel-injection activators and other specialty mechanisms round out demand in performance-oriented sub-systems.

Turbo technology relies increasingly on electro-pneumatic precision to meet tight boost-pressure windows, a trend that helps modernize product mixes without displacing low-cost vacuum drives overnight. Military procurement of next-generation APCs and MBTs requires high-flow, temperature-resistant actuation for mobility and environmental systems, reinforcing a premium sub-segment within conventional categories. Across applications, the Russia automotive pneumatic actuators market continues to balance commoditized, price-sensitive spares with opportunities for digitally enabled designs adapted to predictive maintenance.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: Passenger Scale Meets Commercial Upside

Passenger Cars maintained a commanding 64.58% revenue share in 2025 as Chinese OEMs expanded retail presence and contributed large-volume orders for standard vacuum actuators. Conversely, Commercial Vehicles, spanning heavy trucks to buses, are poised for stronger momentum at a 5.18% CAGR through 2031. Defense truck and tank programs accelerate demand for hardy, wide-bore actuators able to operate in extreme climates.

Light commercial vans benefit from standardized platforms that ease sourcing and contain cost. Within passenger models, SUVs increasingly integrate turbo and EGR systems that up-spec actuator counts per vehicle. Sedans and hatchbacks, although cost-conscious, still rely on brake and throttle actuators that must comply with stricter crash-avoidance and emissions norms. As a result, the Russia automotive pneumatic actuators market retains its broad base while deepening in high-duty niches.

By Sales Channel: Aftermarket Resilience Outpaces OEM Growth

The aftermarket captured 63.10% of 2025 revenue as owners keep vehicles longer amid an outlook for 15-20% price hikes on new units. Elevated repair costs—up 31% last year—drive steady turnover of brake and turbo-related actuators. Distributors and independent workshops value drop-in interchangeability, favoring conventional vacuum products with wide cross-carline compatibility. Meanwhile, OEM demand should grow faster at 6.01% CAGR, reflecting localization mandates that require fresh sourcing for newly assembled vehicles.

SPIC-backed models such as the revamped Lada Vesta integrate higher domestic content, opening lanes for Russian actuator plants to graduate from aftermarket reliance to direct assembly contracts. Over the forecast, OEM pull will redistribute volume but not fully eclipse aftermarket heft, keeping the Russia automotive pneumatic actuators market balanced between new-build and service sectors.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Actuator Material: Steel Endures, Composites Advance

Steel retained a 70.85% share in 2025, benefiting from robust local metallurgy and proven fatigue resistance in severe duty. Domestic mills like MMK supply KAMAZ and others under long-term contracts, shielding the value chain from currency shocks tied to imported alloys. Aluminum offers mass-reduction advantages, especially in passenger turbo and EGR housings, yet its share grows slowly due to cost premiums.

Composites and engineering plastics, projected at 5.63% CAGR, advance in secondary housings, firmware-bearing covers, and low-pressure hydrogen blend fuel metering. Smart-material research, shape-memory alloys, and electroactive polymers indicate long-range potential for hybrid constructions. That said, serviceability expectations and rugged climate demands mean buyers still prize steel’s predictability, so the Russia automotive pneumatic actuators market will shift material mix only gradually.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Conventional Dominance Faces Electro-Pneumatic Uptick

Conventional vacuum-pneumatic devices controlled 84.60% of 2025 sales. Their simple architecture, ready spares availability, and low unit cost match tight fleet-maintenance budgets. Electro-pneumatic formats, rising to 5.98% CAGR, respond to IoT gatekeepers seeking real-time diagnostics. Intelligent transport tenders stipulate data-ready components, nudging fleets toward new-technology adoption.

Still, electro-pneumatic systems carry higher BOM costs, limiting penetration to premium passenger trims, defense platforms, and forward-leaning logistics operators. As municipal ITS rollouts and predictive-maintenance pilots scale, suppliers able to deliver CAN-bus or Ethernet-enabled actuators will capture growing demand pockets within the Russia automotive pneumatic actuators market.

Geography Analysis

The Central Federal District, anchored by Moscow’s manufacturing corridor, accounts significant market chunk as state procurement programs clustered near administrative centers. SPIC incentives have enticed brake and turbo actuator lines to set up in Kaluga and St. Petersburg, shortening lead-times and qualifying models for preferential content scoring. The Volga Federal District follows, powered by KAMAZ operations in Naberezhnye Chelny and AvtoVAZ plants along the Samara–Ulyanovsk arc. Despite posting a RUB 3.83 billion net loss for the first nine months of 2024, KAMAZ continues to draw actuator capacity upgrades to support truck and armored-vehicle builds.

The Urals Federal District is the growth standout thanks to Uralvagonzavod’s ramp-up of T-72B3 and T-90M output. High-torque brake and suspension actuators tailored for tracked vehicles convert into predictable annual orders insulated from consumer cyclicality. The Northwestern Federal District, with Aurus taking over Toyota’s former Saint Petersburg plant, shows potential in luxury segments that prefer electro-pneumatic systems. Funding of over RUB 20 billion for smart traffic systems across 62 urban agglomerations will magnify demand for actuators capable of data exchange, especially around St. Petersburg’s freight nodes.

Far Eastern regions gain relevance as China-bound trade lanes diversify through the Northern Sea Route, enabling more consistent inbound flow of actuator sub-components despite sanctions. Yet settlement failure rates on cross-border payments highlight ongoing risk to supply continuity. The Southern Federal District, gateway for land-border imports, now faces higher recycling fees that alter the landed cost calculus for imported pneumatic kits. Together these patterns underscore why the Russia automotive pneumatic actuators market remains regionalized, with policy, defense activity, and logistics shaping demand clusters.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

International tier-one suppliers coexist with emerging Russian players in a moderately concentrated field. Continental AG reorganized its automotive portfolio under the Aumovio banner to capture software-defined vehicle opportunities, implicitly favoring electronic over pneumatic actuation and prompting local affiliates to recalibrate product roadmaps. Parker-Hannifin posted a record USD 19.9 billion in fiscal 2024 sales, attributing a sizable slice to transportation, yet its Russia exposure sits under review amid tightening dual-use export rules[3]“FY2024 Annual Report,” Parker-Hannifin Corporation, parker.com .

Chinese brands own significant presence in the domestic truck market, spurring KAMAZ to intensify localization and defense-order focus rather than price wars. Domestic mid-tiers leverage SPIC incentives and preferential procurement clauses to push vacuum and hybrid actuator lines into OEM programs, lessening dependence on volatile import pathways. The technology front sees first movers pairing electro-pneumatic hardware with embedded diagnostics to align with ITS mandates; smaller firms that master this transition will enjoy higher margins than commodity brake-actuator providers. Consequently, the Russia automotive pneumatic actuators market rewards scale in steel-based volumes yet still offers white-space upside in smart, lightweight designs.

Strategic moves in 2024-2025 center on dual-localization and portfolio pivot. Western firms hold on via licensing, technical support, or minority stakes, while Russian consortia secure funding under defense and infrastructure budgets. Currency hedging, alternate logistics corridors, and Ruble-denominated contracts are now standard practice to shield against exchange spikes. As market players adapt, competitive intensity tightens, but visibility into future demand improves thanks to multiyear governmental procurement timetables.

Russia Automotive Pneumatic Actuators Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Standard Motor Products expanded its Electronic Parking Brake Actuator line covering 2023-2024 Ford models; the plug-and-play units target the growing service-market niche.

- December 2024: Cummins introduced Exhaust Throttle Valves with electric or pneumatic drive options for diesel and hydrogen engines to meet Euro 6 and BS6 standards.

Table of Contents for Russia Automotive Pneumatic Actuators Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Government localization contracts (SPIC)

- 4.2.2State-subsidized sales programs

- 4.2.3Growing commercial-vehicle output

- 4.2.4Surge in defense and special-purpose vehicle demand

- 4.2.5IoT-enabled predictive-maintenance adoption

- 4.2.6Low-pressure pneumatics for hydrogen-blend engines

- 4.3Market Restraints

- 4.3.1Sanctions-driven parts shortages

- 4.3.2Rapid substitution by electric actuators

- 4.3.3Volatile ruble inflates imported raw-material costs

- 4.3.4Rising recycling fee on imported sub-assemblies

- 4.4Value/Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value (USD))

- 5.1By Application Type

- 5.1.1Throttle Actuators

- 5.1.2Fuel Injection Actuators

- 5.1.3Brake Actuators

- 5.1.4Exhaust Gas Recirculation Actuators

- 5.1.5Turbo Wastegate Actuators

- 5.1.6Others

- 5.2By Vehicle Type

- 5.2.1Passenger Cars

- 5.2.1.1Hatchback

- 5.2.1.2Sedan

- 5.2.1.3SUV/MUV

- 5.2.2Commercial Vehicles

- 5.2.2.1Light Commercial Vehicles

- 5.2.2.2Heavy Trucks

- 5.2.2.3Buses and Coaches

- 5.3By Sales Channel

- 5.3.1OEM

- 5.3.2Aftermarket

- 5.4By Actuator Material

- 5.4.1Steel

- 5.4.2Aluminum

- 5.4.3Composites and Engineering Plastics

- 5.5By Technology

- 5.5.1Conventional Vacuum-Pneumatic

- 5.5.2Electro-Pneumatic

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Continental AG

- 6.4.2Robert Bosch GmbH

- 6.4.3Denso Corporation

- 6.4.4ASCO Valve (Emerson)

- 6.4.5Hitachi Astemo Ltd

- 6.4.6Aisin Seiki Co.

- 6.4.7Duncan Engineering Limited

- 6.4.8CTS Corporation

- 6.4.9Parker Hannifin Corp.

- 6.4.10SMC Corporation

- 6.4.11IMI Norgren

- 6.4.12Festo SE

- 6.4.13Nidec Corporation

- 6.4.14Mitsubishi Electric Corporation

- 6.4.15Aptiv PLC

- 6.4.16MPA Rus LLC

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Russia Automotive Pneumatic Actuators Market Report Scope

The Russian Automotive Pneumatic Actuator Market report contains the latest trends and technological developments in the market and demand by Application Type and By Vehicle Type.