France Aesthetic Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

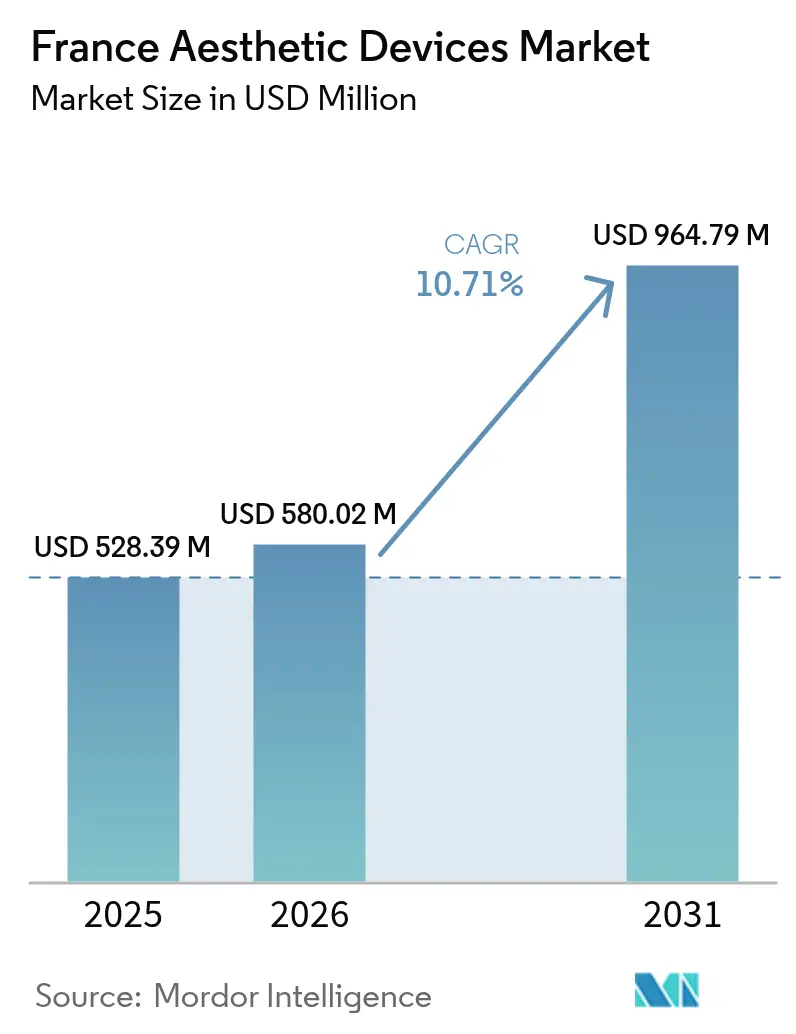

| Base Year Market Size (2025) | USD 528.39 Million |

| Market Size (2026) | USD 580.02 Million |

| Market Size (2031) | USD 964.79 Million |

| Growth Rate (2026 - 2031) | 10.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Aesthetic Devices Market Analysis by Mordor Intelligence

The France Aesthetic Devices Market size is expected to increase from USD 528.39 million in 2025 to USD 580.02 million in 2026 and reach USD 964.79 million by 2031, growing at a CAGR of 10.71% over 2026-2031.

Growing preference for minimally invasive procedures, an aging population with higher disposable income, and a clear tilt toward energy-based technologies are sustaining this expansion. Clinic operators are replacing single-purpose lasers with multifunction consoles that combine laser, radiofrequency, and ultrasound, thereby improving treatment versatility while trimming capital outlays per procedure.[1]ClinicalTrials.gov Registry Editors, “Combination Laser-RF Clinical Study,” ClinicalTrials.gov, clinicaltrials.gov Social-media visibility of successful outcomes is widening the patient funnel, especially among men and younger adults who previously remained outside the aesthetic mainstream. At the same time, France’s role as an intra-EU medical-tourism hub channels demand from Belgium, the United Kingdom, and Germany, giving local clinics incremental volume and pricing power.[2]European Commission Directorate-General for Health and Food Safety, “Cross-Border Healthcare Directive,” European Commission, ec.europa.eu

Key Report Takeaways

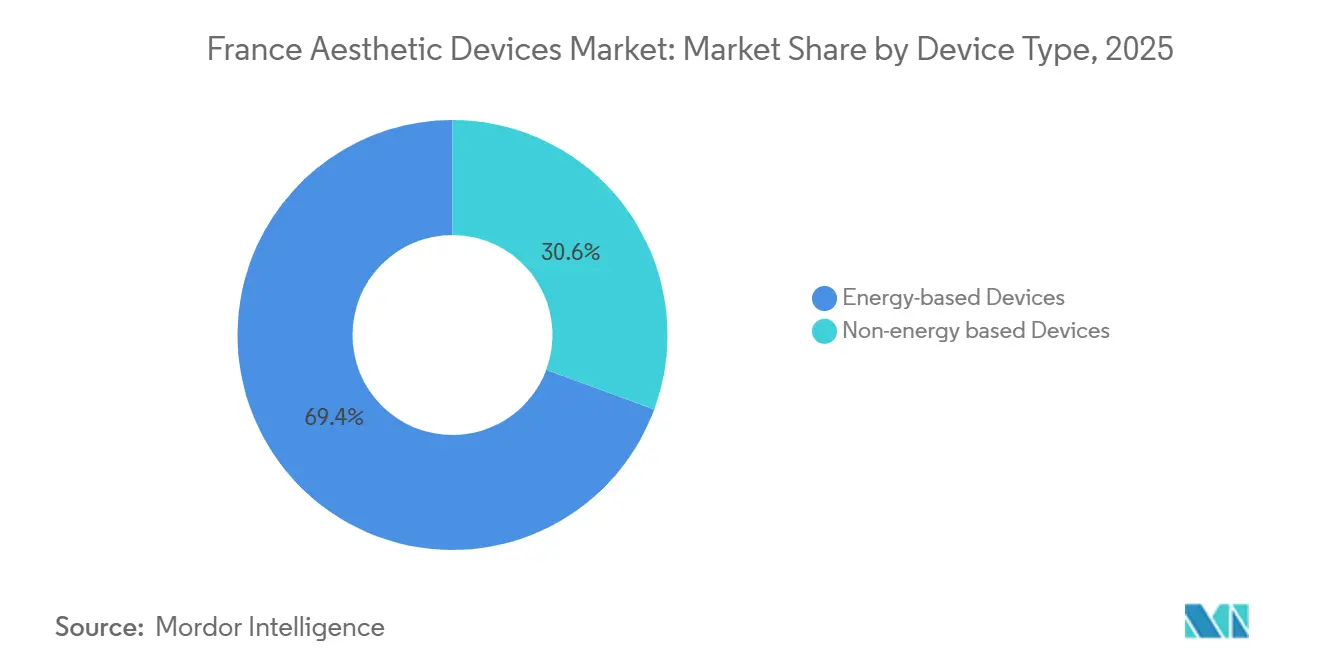

- By device type, energy-based platforms led with 69.36% of the France aesthetic devices market share in 2025. Non-energy devices are projected to expand at a 13.64% CAGR through 2031.

- Hair removal accounted for 31.66% revenue share of the France aesthetic devices market size in 2025. Skin rejuvenation and tightening applications are advancing at a 14.53% CAGR over 2026-2031.

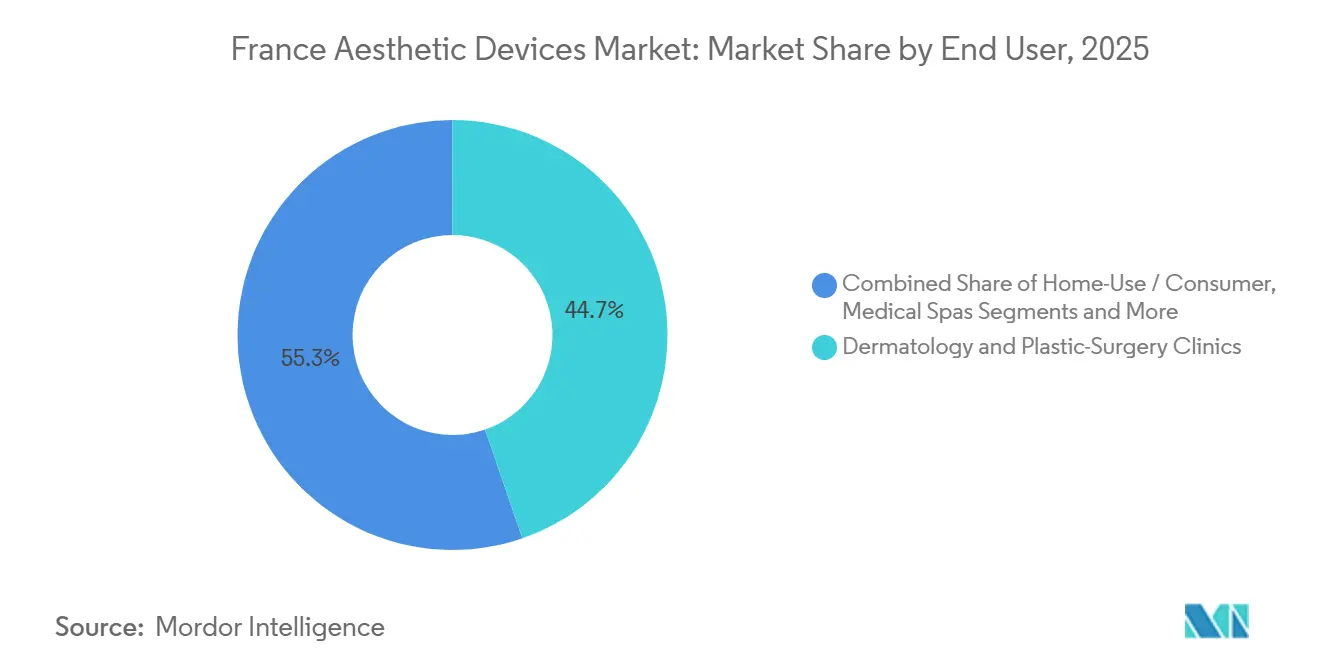

- Dermatology and plastic-surgery clinics held 44.72% of end-user revenue in 2025. Medical spas record the fastest growth at a projected 12.33% CAGR to 2031.

- Female patients represented 71.42% of procedures in 2025. Male demand is climbing at a 12.42% CAGR, the highest gender-specific pace to 2031.

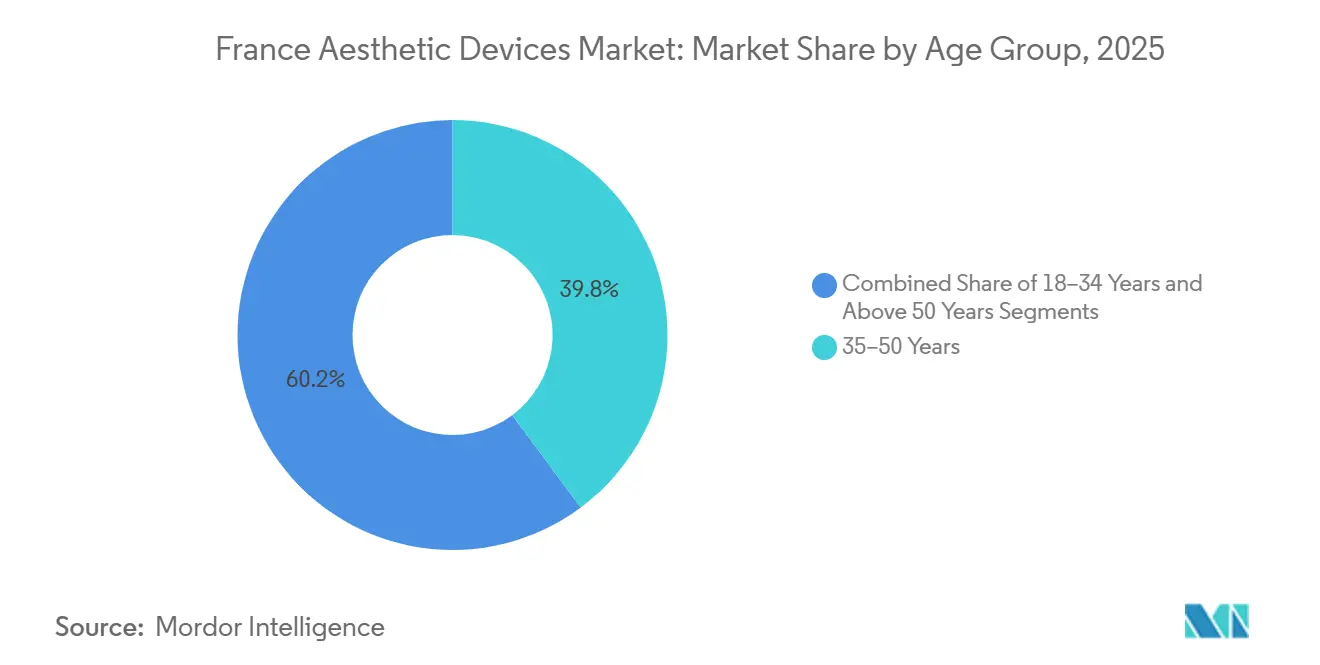

- The 35-50 age group commanded 39.83% procedure volume in 2025. The 18-34 cohort is expanding at a 12.63% CAGR, the quickest among all age brackets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Demand for Minimally Invasive Aesthetic Procedures | +2.1% | Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d’Azur | Short term (≤ 2 years) |

| Rapid Adoption of Energy-Based Combination Platforms | +1.8% | Metropolitan dermatology clinics | Medium term (2-4 years) |

| Aging French Population with Rising Disposable Income | +1.5% | National urban centers | Long term (≥ 4 years) |

| Social-Media-Fueled Beauty Consciousness and Intra-EU Medical Tourism | +1.3% | France, Belgium, United Kingdom, Germany | Medium term (2-4 years) |

| Emergence of AI-Guided Personalized Treatment Planning | +1.0% | Academic dermatology centers | Medium term (2-4 years) |

| Rise of Subscription-Based At-Home Device Ecosystem | +0.9% | Urban millennials and Gen-Z | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Minimally Invasive Aesthetic Procedures

French patients now favor treatments that promise quick recovery and lower surgical risk, moving wallet share away from facelifts and toward laser resurfacing, RF skin tightening, and neuromodulator injections.[3]Marie-Thérèse Legrand, “Patient Preference for Non-Surgical Aesthetic Procedures in France,” Journal of Cosmetic Dermatology, onlinelibrary.wiley.com Heightened vigilance from ANSM after adverse-event reports has pushed manufacturers to package training and certification with every device sale. Disposable income climbed 2.1% in real terms during 2024, underpinning discretionary spending on appearance-enhancement services. Preventive consultations are increasingly integrated into routine dermatology visits, normalizing early intervention even for patients in their twenties. The France aesthetic devices market benefits directly from this attitudinal shift because procedure volumes rise without a parallel jump in complexity.

Rapid Adoption of Energy-Based Combination Platforms

Multifunction systems such as BTL Exilis Ultra 360 and Cutera Secret PRO deliver laser, RF, and ultrasound in a single console, trimming clinic footprint and boosting protocol flexibility. A Paris study found 34% higher collagen density with combination therapy compared with laser alone, with no extra adverse events. Capital efficiency resonates with medical spas whose revenue depends on maximizing room utilization. Nonetheless, operators must invest in extensive laser-safety training to reduce thermal-injury risk, an expenditure some small practices hesitate to absorb. The France aesthetic devices market looks set to deepen vendor relationships around these hybrid platforms as patient outcomes continue to outperform single-modality benchmarks.

Aging French Population with Rising Disposable Income

Adults older than 65 already represent 21.3% of France’s population, and INSEE projects this share to reach 23.4% by 2030. Older consumers spend more per visit on skin tightening and pigmentation correction as they aim to align appearance with extended professional engagement. Real household purchasing power advanced 2.1% in 2024, accelerating elective procedure uptake across income tiers. Uptake is strongest in urban regions such as Île-de-France, where clinic density is highest and wait times are shortest. Survey data from the European Society of Aesthetic Medicine indicate that 42% of French residents aged 50-65 had at least one non-surgical aesthetic treatment last year, compared with 28% five years earlier. This rising tide strongly supports long-term revenue in the France aesthetic devices market.

Social-Media-Fueled Beauty Consciousness and Intra-EU Medical Tourism

Influencers now outpace physicians as the first touchpoint for information on aesthetic procedures, cited by 56% of French patients seeking laser hair removal or skin rejuvenation in 2024. At the same time, France enjoys inbound patient flows from neighboring EU countries because procedure pricing undercuts Switzerland and Germany, and reimbursement pathways are simplified by the Cross-Border Healthcare Directive. ANSM regulations introduced in 2025 force clinics to display credentials online, helping patients verify quality before booking. Clinics that invest in multilingual digital marketing and transparent pricing convert the highest share of foreign inquiries. This confluence of online engagement and medical tourism adds incremental volume to the France aesthetic devices market during the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Devices Limiting Small Clinics | −1.2% | Independent clinics outside metros | Short term (≤ 2 years) |

| Stringent EU-MDR Regulations Lengthening Approval Timelines | −0.9% | France and wider EU | Long term (≥ 4 years) |

| Proliferation of Counterfeit and Grey-Market Devices Eroding Trust | −0.7% | Nationwide, spillover from EU trade | Medium term (2-4 years) |

| Practitioner Skill Gap for Operating Multi-Modality Platforms | −0.6% | Smaller clinics and spas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Devices Limiting Small Clinics

A multifunction laser-RF console ranges from USD 75,000 to USD 180,000 and annual maintenance absorbs 5-7% of that sticker price. Even with leasing, monthly payments can overrun cash flow for sites performing fewer than 100 sessions a month. Almost 38% of dermatologists surveyed by EADV identified equipment expense as the single biggest adoption hurdle, often sending patients elsewhere and surrendering revenue. France’s move toward value-based reimbursement intensifies the pressure because clinics must show both outcomes and cost-effectiveness. The France aesthetic devices market consequently tilts toward hospital groups and national spa chains that can amortize costs across many rooms.

Stringent EU-MDR Regulations Lengthening Approval Timelines

EU-MDR demands thicker clinical files and closer post-market surveillance than its predecessor, extending notified-body reviews to 18-24 months for Class IIb and III platforms. Compliance costs, estimated at EUR 50,000-150,000 per device, disproportionately burden startups and slow innovation cycles. With notified-body numbers down 34% since 2021, application backlogs are common. Incumbents leverage prior certifications to refresh products faster, widening their moat. These delays temper growth potential for the France aesthetic devices market, especially in high-tech niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Energy Platforms Dominate, Non-Energy Gains Momentum

Energy-based systems held 69.36% of the France aesthetic devices market share in 2025, anchored by lasers, RF, intense pulsed light, ultrasound, and emerging plasma solutions. Radiofrequency and picosecond lasers enjoy specific momentum for body contouring and pigment removal respectively. Meanwhile, the non-energy cohort is forecast to outpace at a 13.64% CAGR through 2031 as microdermabrasion kits, dermal rollers, and implants attract price-sensitive clinics and at-home users. Cutera enlighten SR and Candela PicoWay typify the latest picosecond generation, offering shorter pulse widths that shrink thermal diffusion and shave treatment sessions.

Laser systems still own the largest slice of the France aesthetic devices market size because they solve multiple indications from hair removal to vascular lesions. Yet diode technology is steadily cannibalizing IPL for epilation thanks to melanin selectivity and faster session times. Non-invasive ultrasound platforms such as Ultherapy lure patients wary of surgical lifts, while plasma pens build a niche in scar revision thanks to shallow ablation depth. Consumer microdermabrasion gadgets priced below EUR 500 pair with smartphone coaching, drawing younger audiences into entry-level resurfacing. These shifts illustrate how non-energy devices broaden reach while energy platforms retain revenue dominance within the France aesthetic devices market.

By Application: Hair Removal Leads, Skin Rejuvenation Accelerates

Hair removal supplied 31.66% of 2025 revenue, leveraging diode and alexandrite lasers that produce long-lasting follicle disablement with minimal downtime. However, skin rejuvenation and tightening already post the fastest upswing at a 14.53% CAGR because combination laser-RF regimens yield deeper collagen remodeling than monotherapy. Body contouring gains lift from platforms like BTL EMSCULPT Neo, cleared in 2024 for simultaneous muscle building and fat reduction.

Scar management, acne therapy, and pigmentation correction rely increasingly on picosecond lasers that minimize post-inflammatory hyperpigmentation in Fitzpatrick III-V skins. Tattoo-removal volumes stay niche yet lucrative given the premium per session. Emerging indications such as non-surgical vaginal rejuvenation and stretch-mark reduction extend platform utilization further, making the application mix more balanced and lengthening upgrade cycles in the France aesthetic devices market.

By End User: Medical Spas Outpace Traditional Clinics

Dermatology and plastic-surgery clinics generated 44.72% of 2025 revenue because they command hospital-grade gear and established trust. Even so, medical spas post a 12.33% CAGR, the quickest among settings, as they capture demand for quick, discretionary treatments in upscale environments. Hospitals retain their place for anesthesia-requiring procedures but surrender ground on high-volume laser hair removal to spas that maintain lean overhead.

Home-use devices, although still modest in value, scale rapidly on the back of subscription models launched by L’Oréal and Panasonic. Telemedicine follow-ups let doctors supervise home regimens, blending professional oversight with consumer independence. Such hybrid care loops expand patient reach and anchor loyalty, reinforcing growth in the France aesthetic devices market.

By Gender: Male Segment Surges from a Low Base

Women drove 71.42% of procedures in 2025, but male demand is expanding at a brisk 12.42% CAGR as stigma recedes and body-sculpting gains visibility. Devices blending RF with high-intensity electromagnetic pulses resonate because they enhance muscle tone and jawline definition, priorities for male clients. Clinics now allocate about a quarter of digital ad budgets to male-centric creatives.

Female volume grows more moderately because urban saturation approaches. Providers tailor protocols, using higher RF energy for thicker male dermis, while staff undergo training in gender-specific consultation tactics. As momentum continues, male procedures may account for nearly 40% of the France aesthetic devices market volume by 2031, notably reshaping service menus.

By Age Group: Younger Cohorts Drive Preventive Demand

Patients aged 35-50 represented 39.83% of 2025 sessions, largely focused on corrective wrinkle reduction and pigmentation fixes. Millennials and Gen-Z (18-34) are accelerating at 12.63% CAGR by embracing prophylactic laser resurfacing and micro-dosed neuromodulators long before lines appear. These younger users readily experiment with at-home LEDs and dermal rollers, enlarging the ecosystem beyond clinic walls.

Older adults above 50 still spend the most per capita on multi-modality lifting programs that unite fractional lasers, RF, and HIFU. Yet as preventive measures spread, severity of aging markers may lessen, encouraging a shift from major corrections to lifelong maintenance—a change that sustains recurring revenue in the France aesthetic devices market while adjusting protocol intensity.

Geography Analysis

Île-de-France and Auvergne-Rhône-Alpes harbor dense networks of academic hospitals and premium medical spas, commanding a disproportionate share of advanced consoles and talent. Disposable income in these metros stands well above the national mean, which supports higher average selling prices and bundled maintenance contracts. Coastal Provence-Alpes-Côte d’Azur enjoys seasonal spikes in demand tied to tourism, keeping device utilization high during peak months.

Secondary hubs—Bordeaux, Marseille, Toulouse—register the fastest growth from lower bases, thanks to clinic expansion and technology upgrades encouraged by vendor financing packages. Yet independent practices outside the major metros continue to wrestle with capital cost, pausing investment in multifunction consoles and referring patients to urban centers. This uneven spread shapes service availability and waiting times across the France aesthetic devices market.

National compliance with EU-MDR means every region follows the same regulatory script, although clinics in Paris and Lyon access notified-body consultants more easily, moving new devices to market sooner. The cumulative effect is a two-speed landscape: metropolitan areas showcase the latest AI-guided combinations while provincial towns adopt innovations more gradually.

Competitive Landscape

Five global manufacturers includes Candela, Lumenis, BTL, Cutera, and Alma Lasers hold an good share of 2025 revenue, giving the France aesthetic devices market a moderate concentration profile. They differentiate through multi-modality integration, consumables, and bundled training, erecting switching costs that discourage defection. BTL Exilis Ultra 360 and Cutera Secret PRO typify this arms race, each cleared in 2024-2025 for combined RF microneedling and fat remodeling.

Consumer-oriented disruptors such as L’Oréal and FOREO pursue recurring revenue with subscription LEDs, pulling the market’s frontier toward home-use ecosystems. Patent activity clusters around AI parameter optimization, fractional RF electrodes, and coupled laser-ultrasound handpieces, suggesting further refinement rather than wholesale technology leaps. EU-MDR certification backlogs inflict 18-24-month lags that reinforce incumbent grip while slowing new-entrant momentum.

Strategic collaborations intensify distribution reach; Cynosure Lutronic’s 2026 alliance with Seriderm extends service capacity across France and neighboring markets, illustrating how vendors scale after-sales support to hold turf in the France aesthetic devices market.

France Aesthetic Devices Industry Leaders

BTL Industries

Candela Medical

Lumenis Be Ltd.

Alma Lasers Ltd.

Hologic Inc. (Cynosure)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: L’Oréal unveiled the Light Straight + Multi-styler and an ultra-thin LED face mask, both CES Innovation Award honorees, deploying infrared and LED to safeguard hair and skin.

- January 2026: Professional brand MEDIPEEL accelerated its European rollout with key launches in France and the United Kingdom.

- January 2026: Cynosure Lutronic EMEA formed a long-term commercial pact with Seriderm UK, covering France and five other territories to reinforce service and clinical support for energy-based aesthetics.

France Aesthetic Devices Market Report Scope

As per the scope of the report, Aesthetic devices are tools used for non-surgical or minimally invasive cosmetic procedures to improve appearance through technologies like lasers, radiofrequency, ultrasound, and light.

The France Aesthetic Devices Market Report is segmented by Device Type, Application, End User, Gender, Age Group, and Geography. By Device Type, the market is segmented into Energy‑Based Devices (Laser‑Based, IPL, RF, Ultrasound, Plasma) and Non‑Energy Devices (Microdermabrasion, Dermal Rollers, Implants). By Application, the market is segmented into Skin Rejuvenation, Body Contouring, Hair Removal, Scar Treatment, and Tattoo Removal. By End User, the market is segmented into Clinics, Hospitals, Medical Spas, and Home‑Use. By Gender, the market is segmented into Female and Male. By Age Group, the market is segmented into 18–34, 35–50, and Above 50. The report offers the value (in USD) for the above segments.

| Energy-Based Devices | Laser-Based Devices |

| Intense Pulsed Light (IPL) Devices | |

| Radiofrequency Devices | |

| Ultrasound (HIFU) Devices | |

| Plasma & Others | |

| Non-Energy Devices | Microdermabrasion Devices |

| Dermal Rollers | |

| Aesthetic Implants |

| Skin Rejuvenation & Tightening |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Scar, Acne & Pigmentation Treatment |

| Tattoo & Vascular Lesion Removal |

| Others |

| Dermatology & Plastic Surgery Clinics |

| Hospitals & Out-patient Centers |

| Medical Spas |

| Home-Use / Consumer |

| Female |

| Male |

| 18–34 Years |

| 35–50 Years |

| Above 50 Years |

| By Device Type | Energy-Based Devices | Laser-Based Devices |

| Intense Pulsed Light (IPL) Devices | ||

| Radiofrequency Devices | ||

| Ultrasound (HIFU) Devices | ||

| Plasma & Others | ||

| Non-Energy Devices | Microdermabrasion Devices | |

| Dermal Rollers | ||

| Aesthetic Implants | ||

| By Application | Skin Rejuvenation & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Scar, Acne & Pigmentation Treatment | ||

| Tattoo & Vascular Lesion Removal | ||

| Others | ||

| By End User | Dermatology & Plastic Surgery Clinics | |

| Hospitals & Out-patient Centers | ||

| Medical Spas | ||

| Home-Use / Consumer | ||

| By Gender | Female | |

| Male | ||

| By Age Group | 18–34 Years | |

| 35–50 Years | ||

| Above 50 Years | ||

Key Questions Answered in the Report

How large is the France aesthetic devices market today?

The France aesthetic devices market size reached USD 580.02 million in 2026 and is on track to hit USD 964.79 million by 2031.

What is the growth outlook between 2026 and 2031?

Revenue is forecast to grow at a 10.71% CAGR over the five-year span as minimally invasive demand rises and multifunction platforms proliferate.

Which device type commands the highest revenue?

Energy-based systems, including laser and radiofrequency platforms, held 69.36% of 2025 value and remain the dominant revenue source.

Which application is expanding fastest?

Skin rejuvenation and tightening procedures are advancing at a 14.53% CAGR, outperforming hair removal and other indications.

How are medical spas influencing distribution?

Medical spas post the quickest end-user growth at 12.33% CAGR by offering non-invasive treatments in lifestyle settings, diverting volume from hospital clinics.

Page last updated on: