Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Roofing Adhesives Market Report is Segmented by Resin Type (Epoxy, Polyurethane, Acrylic, Other Resin Types), Technology (Water-Borne, Solvent-Borne, Other Technologies), End-User Industry (Residential, Non-Residential), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

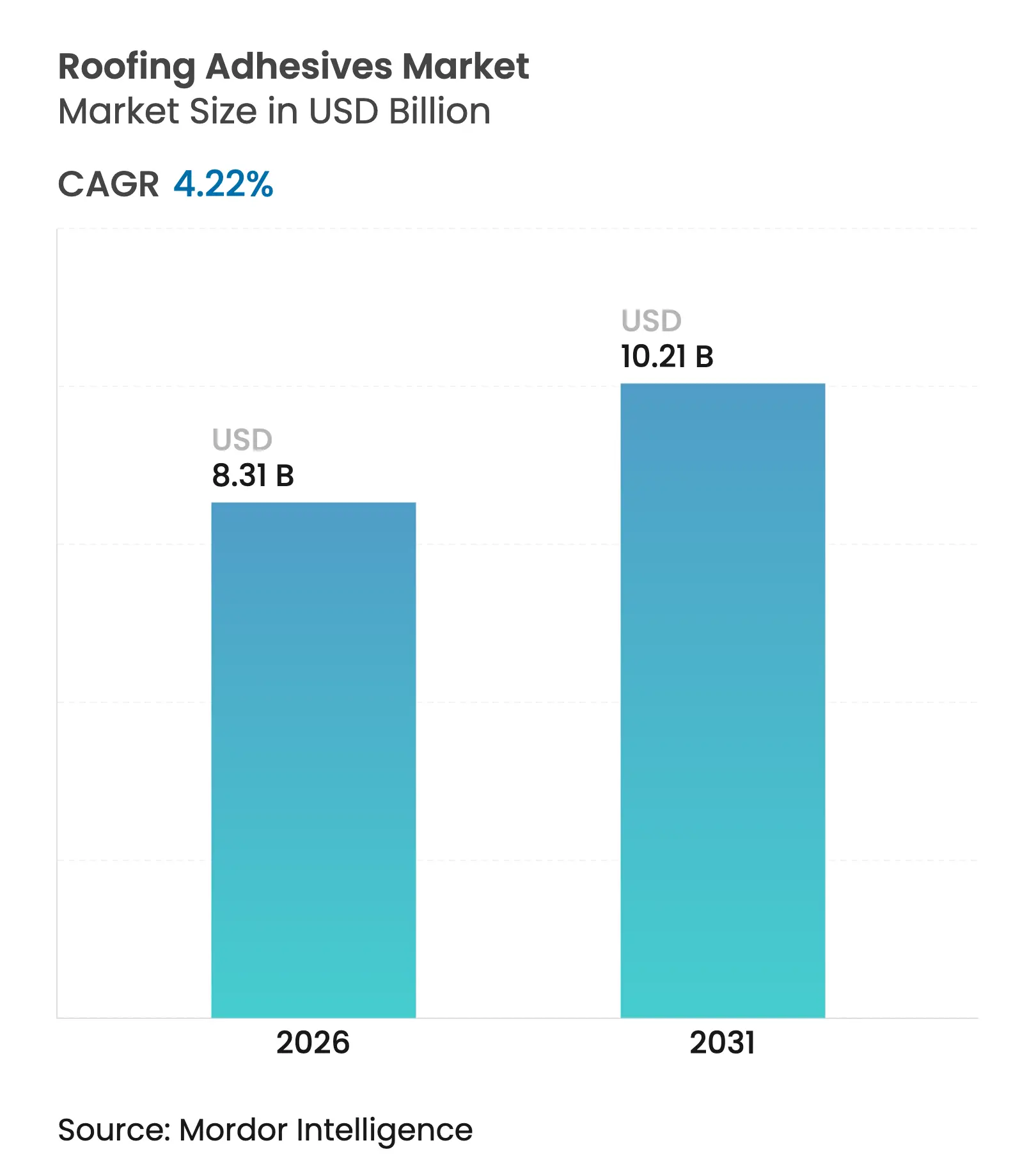

| Market Size (2026) | USD 8.31 Billion |

| Market Size (2031) | USD 10.21 Billion |

| Growth Rate (2026 - 2031) | 4.22 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Roofing Adhesives market size in 2026 is estimated at USD 8.31 billion, growing from 2025 value of USD 7.97 billion with 2031 projections showing USD 10.21 billion, growing at 4.22% CAGR over 2026-2031. The expansion reflects the construction sector’s gravitation toward high-performance, environmentally aligned bonding systems that accelerate installation and withstand severe weather. Consistent re-roofing cycles in mature economies, infrastructure build-outs in developing nations, and stricter energy-saving codes combine to lift demand for adhesive-based assemblies. Contractors value the elimination of fastener penetrations, the improved wind-uplift profile, and the labor savings enabled by factory-controlled bonding technologies. Material suppliers respond with hybrid chemistries and bio-based feedstocks that meet upcoming solvent-VOC limits while safeguarding long-term joint integrity. The aggregate of these forces positions the roofing adhesives market for steady, margin-accretive growth through the decade.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing global construction industry

Growing global construction industry

| +1.2% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, with concentration in Asia-Pacific and North

America

|

Impact Timeline

:

Long term (≥ 4 years)

|

Accelerated shift from mechanical fastening to adhesives

Accelerated shift from mechanical fastening to adhesives

| +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Demand for energy-efficient, lightweight roofing systems

Demand for energy-efficient, lightweight roofing systems

| +0.8% | Global, led by developed markets with green building standards | Long term (≥ 4 years) | |||

Rapid urbanization boosting reroofing demand in developing

economies

Rapid urbanization boosting reroofing demand in developing

economies

| +0.7% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) | |||

Rise of modular off-site construction with pre-applied

adhesive panels

Rise of modular off-site construction with pre-applied

adhesive panels

| +0.5% | North America & EU, early adoption in urban centers | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Global Construction Industry

Construction spending continues to expand, pushing the roofing adhesives market upward. New commercial towers in major Asian cities require fully adhered membranes that tolerate typhoon-level wind. United States re-roofing projects, exceeding 80% of domestic demand, sustain baseline consumption even during economic pauses. Government green-infrastructure outlays add further volume because bonded assemblies meet air-sealing targets better than mechanical systems. The International Finance Corporation links reduced operational carbon to high-performance envelopes, tying adhesive uptake to ESG capital flows[1]International Finance Corporation, “Building Resilience in Construction,” ifc.org. Contractors meanwhile favor liquid-applied systems that shorten labor schedules and avoid torch-on risks, reinforcing long-horizon demand for the roofing adhesives market.

Accelerated Shift from Mechanical Fastening to Adhesives

Hurricane testing shows fully adhered single-ply roofs dissipate wind uplift across the membrane, outperforming screw-and-plate anchors. Building owners in coastal Florida therefore specify two-component polyurethane foam beads that create continuous bonds without membrane perforations. European retrofits also pivot away from metal fasteners as energy-code upgrades tighten air-leak thresholds. Mechanical removal costs during reroofing further motivate owners to adopt adhesives that leave substrates intact for future overlay work. Equipment advances—such as high-output spatter applicators—cut installation times, making the switch economical even on tight bid margins. These practical and regulatory gains converge, accelerating penetration of adhesive assemblies throughout the roofing adhesives market.

Demand for Energy-Efficient, Lightweight Roofing Systems

Cool-roof mandates propel reflective liquid membranes that rely on specialized elastomeric binders. GAF’s TCPP-free polyiso panels bond with novel low-density foams that maintain R-value while trimming dead load. Adhesive suppliers must ensure cohesive strength at service temperatures from -40 °C to 80 °C while also resisting plasticizer migration from PVC membranes. Builders chasing LEED points select low-VOC water-borne acrylics that pass GREENGUARD Gold testing. Solar rooftop adoption compounds these needs because adhesive layers must withstand concentrated thermal cycling beneath photovoltaic modules. Collectively, these performance targets channel premium demand toward advanced chemistries, reinforcing value capture in the roofing adhesives market[2]“Thermal Reflectivity of White Polyurethane Membranes,” Revista Ingeniería de Construcción, revistainingenieriadeconstruccion.cl .

Rapid Urbanization Boosting Reroofing Demand in Developing Economies

China’s tier-two cities now overhaul 1990s housing blocks, replacing bitumen sheets with SBS membranes anchored by moisture-cure polyurethanes that tolerate monsoon humidity. India’s Smart Cities Mission triggers public-building refurbishments that specify low-odor water emulsions to minimize tenant disruption. Urban planners in Jakarta and Ho Chi Minh City embrace lightweight steel decks, requiring flexible adhesives that accommodate high building sway. The IFC estimates emerging-market construction must mobilize USD 1.5 trillion by 2035 to hit decarbonization goals, a pipeline that embeds adhesives in every energy-efficient roof assembly. As infrastructure outlays cascade through supply chains, the roofing adhesives market secures a structural growth anchor.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Petro-feedstock price volatility

Petro-feedstock price volatility

| -0.6% | Global, with highest impact in import-dependent regions | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.6%

|

Geographic Relevance

:

Global, with highest impact in import-dependent regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

Tightening solvent-VOC regulations

Tightening solvent-VOC regulations

| -0.4% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Thermal-cycling bond failures in extreme climates

Thermal-cycling bond failures in extreme climates

| -0.3% | Global, concentrated in temperature-extreme regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Petro-Feedstock Price Volatility

Adhesive production depends on acrylate and isocyanate chains susceptible to geopolitical shocks and refinery turnarounds. A sharp crude spike squeezes margins because formulators cannot instantly re-price annual roofing contracts. Regional suppliers with backward integration into propylene oxide manage swings better, pressuring independents in the roofing adhesives market. Some producers hedge through bio-based polyols, but limited capacity means premiums persist. Currency fluctuations in import-reliant economies add another layer of unpredictability, complicating inventory planning for distributors who already face tight credit terms. These unit-cost uncertainties drag on near-term market acceleration even as long-range fundamentals stay positive.

Tightening Solvent-VOC Regulations

California Rule 1168 now caps single-ply membrane adhesive VOC at 250 g/L, with deeper cuts coming in 2028. Comparable limits spread across the Northeast Ozone Transport Region, effectively setting a de-facto national standard. The EU’s REACH clamp on di-isocyanates above 0.1% compels reformulation of legacy polyurethane lines. Compliance demands new dispensing gear, worker training, and costly third-party emissions testing. Smaller manufacturers risk losing distribution if they cannot fund these transitions. In emerging Asia, governments replicate western guidelines, extending the compliance burden worldwide. The requirement accelerates water-borne and reactive-hot-melt adoption yet adds cost friction that tempers growth for the broader roofing adhesives market.

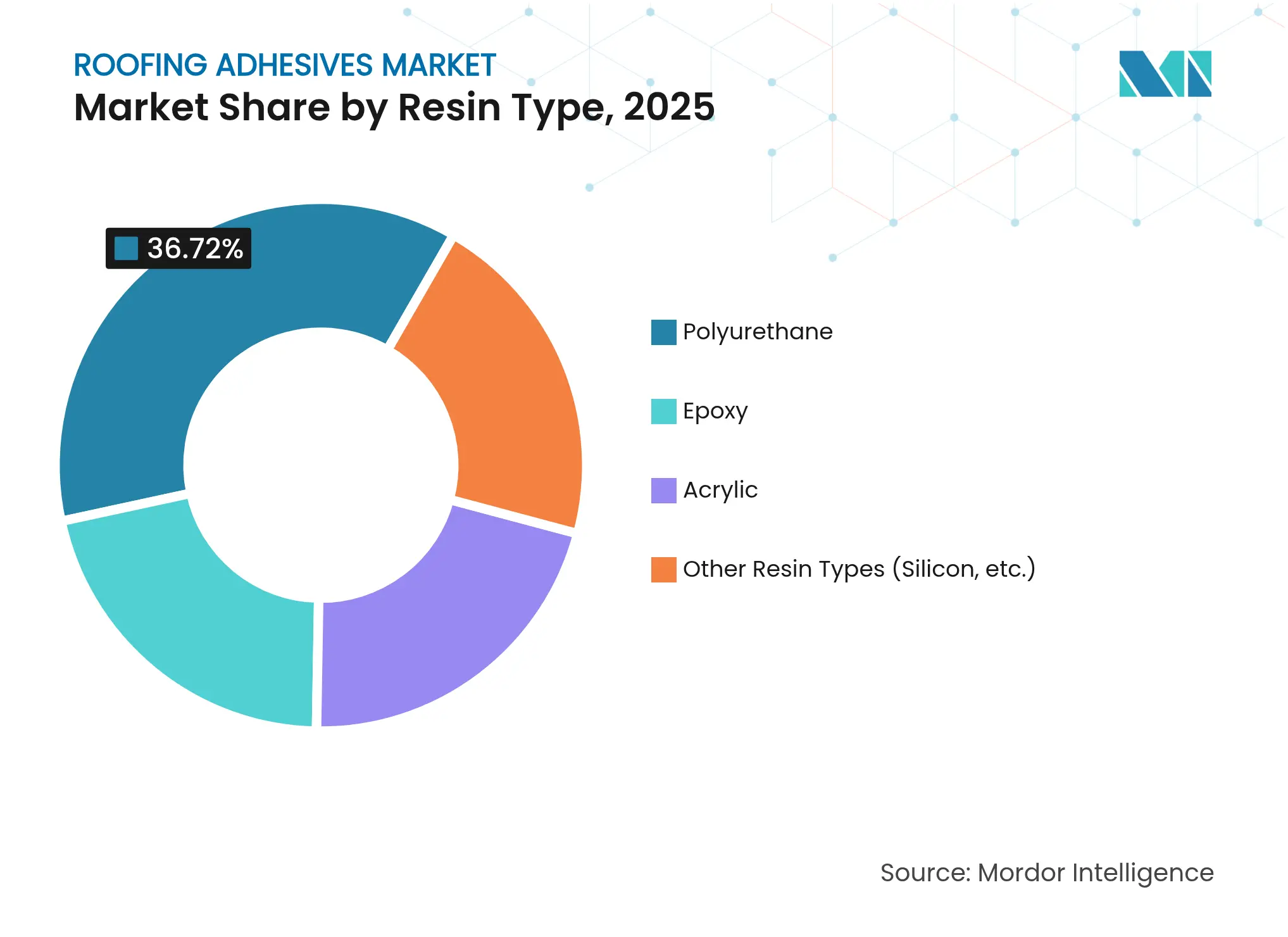

By Resin Type: Polyurethane Holds Scale, Epoxy Unlocks High-Strength Niches

Polyurethane adhesives captured 36.72% roofing adhesives market share in 2025 because their elasticity absorbs deck movement and thermal shock with minimal cohesive loss. They cure reliably across a broad humidity range, making them staples in both residential shingles and commercial single-ply assemblies. Epoxy formulations grow at a 5.35% CAGR and will widen their foothold where tensile and peel strength trump flexibility, especially on metal roofs subject to foot traffic or point loads. Silicones, though modest in volume, protect mission-critical installations that confront continuous >150 °C exposure, such as data-center generator housings. Di-isocyanate restrictions in Europe tilt incremental demand toward epoxy hybrids prompted by worker-safety training mandates. Covestro’s partially bio-based polyurethane families may slow share erosion, yet cost parity with petro-PU remains distant. These shifts confirm that resin innovation will continue to set the competitive tempo inside the roofing adhesives market.

Contractors balancing price and performance still default to PU for steep-slope reroofing because familiar application techniques reduce field errors. Epoxy uptake accelerates where codes impose uplift thresholds beyond mechanically fastened assemblies. Roofing warranties exceeding 30 years increasingly specify dual-curing chemistries mixing cyanoacrylate speed with epoxy endurance, compressing downtime on logistic hubs that cannot risk water ingress. Resin suppliers meanwhile expand customization services, tailoring modulus and open-time windows to accommodate seasonal temperature spreads. Such formulation agility underpins brand loyalty, influencing purchasing behaviors across the roofing adhesives industry.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Water-Borne Systems Champion VOC Compliance, Reactive Platforms Chase Speed

Water-borne formulations accounted for 45.28% of the roofing adhesives market in 2025, aided by regulatory tailwinds and homeowner aversion to solvent odors. Polymer-emulsion advances now deliver shear strength once achievable only with solvent-borne chloroprenes, opening substitution pathways on fully adhered TPO membranes. Spray rigs that atomize high-solids acrylics at low pressures further cut jobsite emissions, helping contractors navigate urban air-quality permits without schedule delays. Reactive hot-melt and UV-curing lines post a 4.74% CAGR because factories producing modular roof cassettes demand bond strength within minutes to sustain takt-time. UV systems integrate inline inspection where fluorescence reveals application voids before panels exit the conveyor.

Solvent-borne technologies retreat as state and national rules harden; nevertheless they persist in cold climates where water-borne latex may freeze. Suppliers counter with winter-grade emulsions stabilized by anti-freeze packages, broadening seasonal applicability and chipping at solvent residual niches. Field applicators appreciate moisture-cure foams that expand to fill deck irregularities, eliminating time-consuming substrate repairs. Such foam lines now include pre-gassed canister kits that trim waste and simplify yield calculations. Digital flow meters attached to plural-component proportioners improve cure ratio accuracy, a requirement when warranties exceed 20 years. Together these advances reinforce water-borne and reactive platforms as the twin growth engines inside the roofing adhesives market.

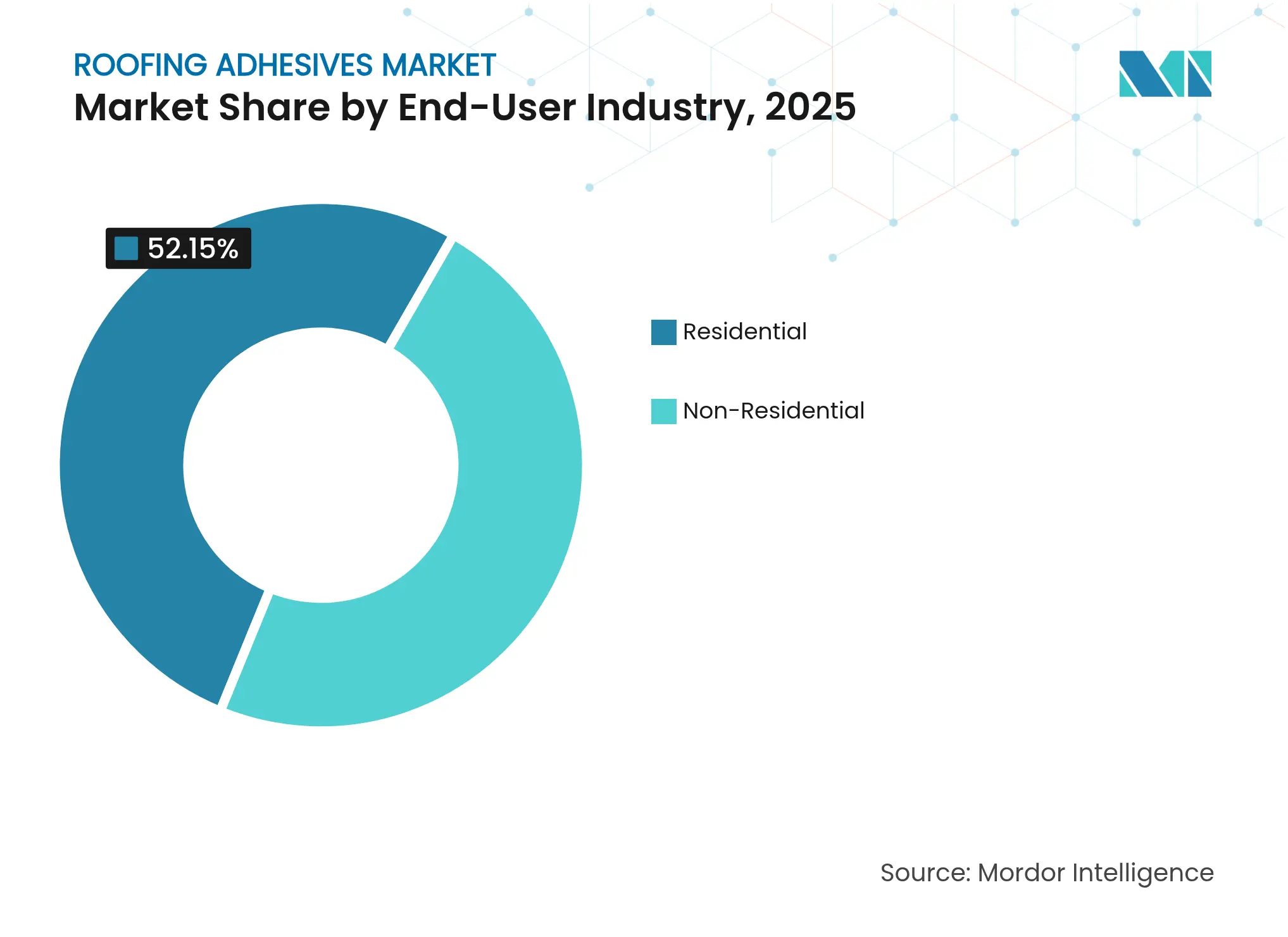

By End-User Industry: Residential Volume Dominates, Non-Residential Value Rises

Residential reroofing maintains 52.15% share of the roofing adhesives market size in 2025, grounded in the endless replacement cycle of asphalt shingles and low-slope membranes on single-family homes. DIY retailers push polyurethane sealants packaged in sausage foil that cut plastic waste, expanding homeowner adoption. However, non-residential demand advances 5.05% annually as corporate ESG targets accelerate cool-roof retrofits in office towers and logistics sheds. Hospitals and data centers prefer fully adhered systems for leak control under critical equipment, raising average adhesive spend per square meter.

Government infrastructure programs, such as United States school modernization grants, stipulate low-VOC criteria that steer procurement toward water-borne and bio-based lines. Industrial facilities in India and Vietnam select moisture-cure systems tolerant of high substrate moisture, avoiding production downtime associated with deck dry-out. Private equity roll-ups of roofing contractors aggregate purchasing power, encouraging negotiated rebates that influence brand hierarchy within the roofing adhesives market. In turn, suppliers bundle adhesives with compatible primers and walk-pad coatings to lock in specification control across the entire roof assembly. These ecosystem dynamics elevate non-residential segments as the fastest value generators in the roofing adhesives industry.

Note: Segment shares of all individual segments available upon report purchase

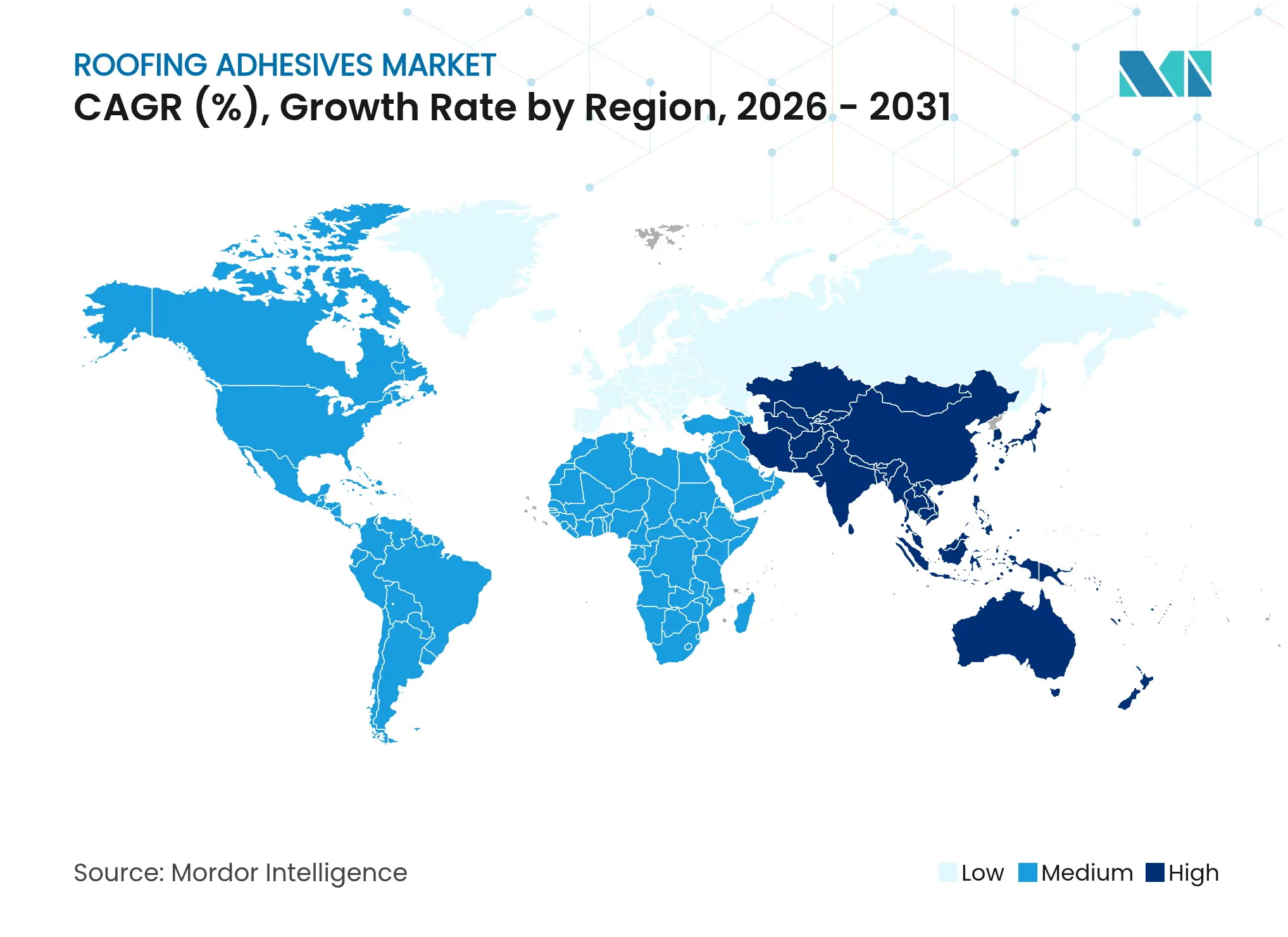

Asia-Pacific’s 44.83% share underscores its centrality to the roofing adhesives market, and its 4.71% CAGR through 2031 confirms unmatched expansion momentum. China renovates prefabricated housing estates erected during the 1990s, replacing failing tar layers with SBS sheets bonded using moisture-cure polyurethane to meet seismic resilience updates. India’s impetus comes from warehouse booms under the Goods and Services Tax regime, where TPO membranes bonded with low-VOC water emulsions eliminate flame hazards near stored goods. Indonesia and Vietnam deploy thermoplastic polyolefin fully adhered roofs on new semiconductor fabs that require particulate-free interiors. Regional producers, such as Nippon Soda’s adhesive unit, leverage proximity to petro feedstock hubs, lowering freight costs and sharpening competition against multinationals in this vital node of the roofing adhesives market.

North America delivers steady revenues due to the mature reroofing cycle and reconstruction after severe storms. The United States International Building Code now references ASCE 7-22 wind-uplift tables, prompting architects in hurricane corridors to specify adhesive fastening on mechanically fastened high-risk zones, lifting the roofing adhesives market further. Canada’s National Research Council champions net-zero-ready building envelopes, fostering adoption of reflective polyurethane liquid membranes on school boards that must meet provincial energy targets. Mexico gains traction within automotive industrial parks built to near-zero downtime tolerances, using fast-curing epoxy foams delivered in pressurized cardboard kegs that dodge steel cylinder import duties.

Europe follows with moderate but consistent growth tied to Green Deal directives requiring deep renovation of existing building stock. Germany’s federal KfW subsidy rewards low-permeability roofs, steering contractors toward water-borne adhesives that achieve Sd < 0.3 m ratings. United Kingdom logistics developers standardized EPDM wraps pre-bonded in factories using UV-curing lines that guarantee adhesion along complex parapet transitions. France’s RE2020 decree mandates life-cycle carbon disclosure, spurring demand for bio-sourced polyurethane containing 40% renewable carbon, as pioneered by BASF. Nordics rely on silicone adhesives for Arctic research stations confronting -50 °C winters, demonstrating the breadth of performance niches that sustain innovation and dispersion within the roofing adhesives market.

Market Concentration

The roofing adhesives market sits in a moderate concentration band. Sika builds on its acquisition of Parex and the 2024 startup of its Singapore plant, providing regional stock of water-borne PU hybrids tailored for tropical humidity. BASF channels ChemCycling waste-oil feedstocks into MDI precursors that feed its Elastan roofing line, giving end users a Scope 3 carbon reduction narrative. 3M expands its patent portfolio around acrylic pressure-sensitive roofing tapes, enabling cold weather application without primer, a differentiation that resonates with unionized installers tasked to finish roofs in tight winter windows.

Carlisle Companies extends its vertical stack, purchasing MTL Holdings to integrate edge metal and adhesive accessory kits, ensuring specification lock-in from vapor barrier to coping cap. Saint-Gobain’s acquisition of FOSROC for USD 1.025 billion broadens access to Asia-Pacific distribution and brings methyl-methacrylate chemistry that tolerates fast conveyor speeds in modular factories. Emerging challenger ICP Group releases bio-based moisture-cure cartridges marketed under the Polyset brand, capturing sustainability-minded reroofers in Sun Belt states.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The roofing adhesive market report includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.