Laminating Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.09 Billion |

| Market Size (2031) | USD 5.49 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laminating Adhesives Market Analysis by Mordor Intelligence

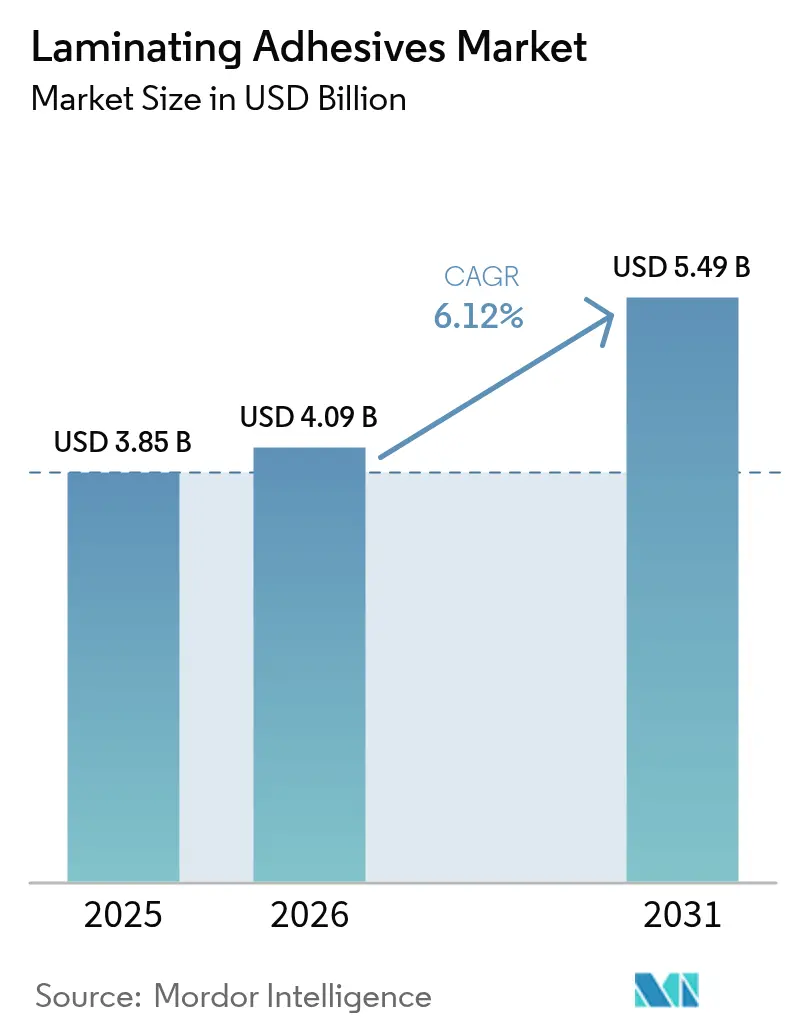

laminating adhesives market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.85 billion with 2031 projections showing USD 5.49 billion, growing at 6.12% CAGR over 2026-2031. Sustained demand for flexible packaging in food, pharmaceuticals and e-commerce parcels, alongside tightening chemical regulations, underpins this steady expansion. Brand owners now specify solvent-free or water-borne solutions to lower volatile organic compound (VOC) emissions, driving accelerated adoption of advanced polyurethane (PUR) and acrylic chemistries. Accelerating Asia-Pacific industrialization, robust medical device output in North America and stringent circular-economy rules in Europe collectively shape product development priorities. Competitive advantage hinges on vertical integration, regulatory fluency and the ability to scale bio-based raw materials that meet cost and performance targets.

Key Report Takeaways

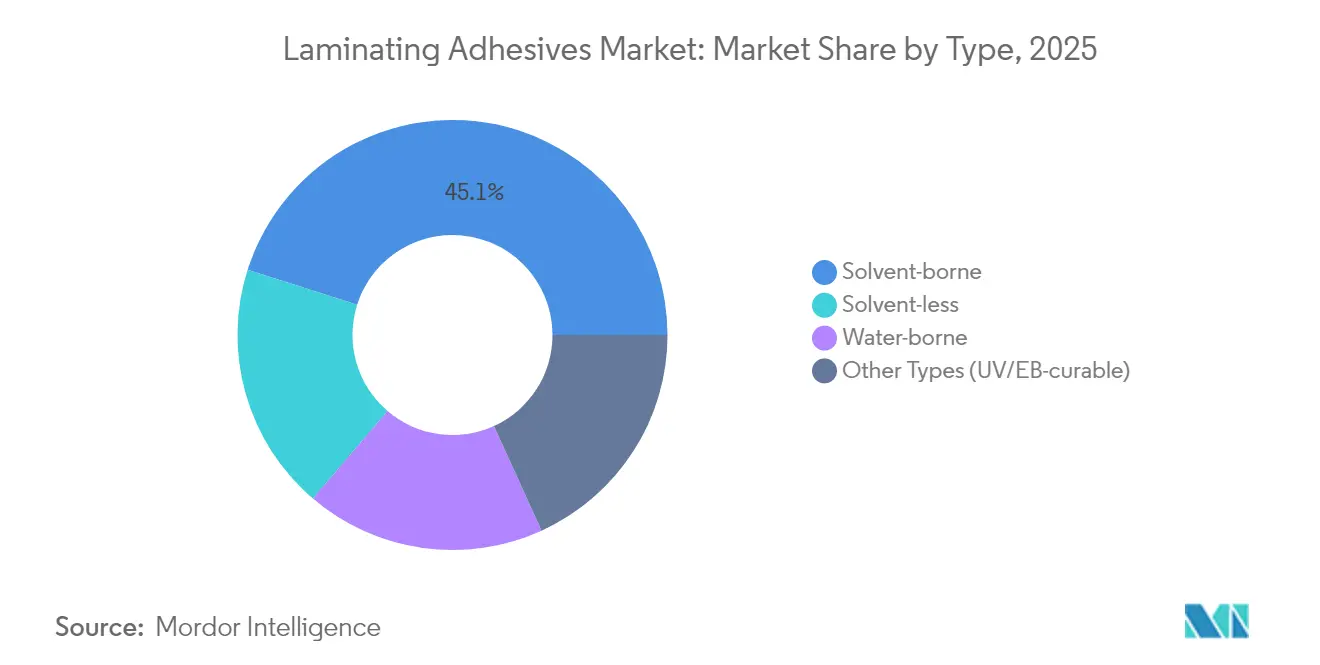

- By type, solvent-borne formulations led with 45.10% of laminating adhesives market share in 2025; solvent-less systems are projected to grow at a 7.36% CAGR to 2031.

- By resin chemistry, polyurethane held a 46.72% share of laminating adhesives market size in 2025, while acrylic is set to expand at an 7.95% CAGR through 2031.

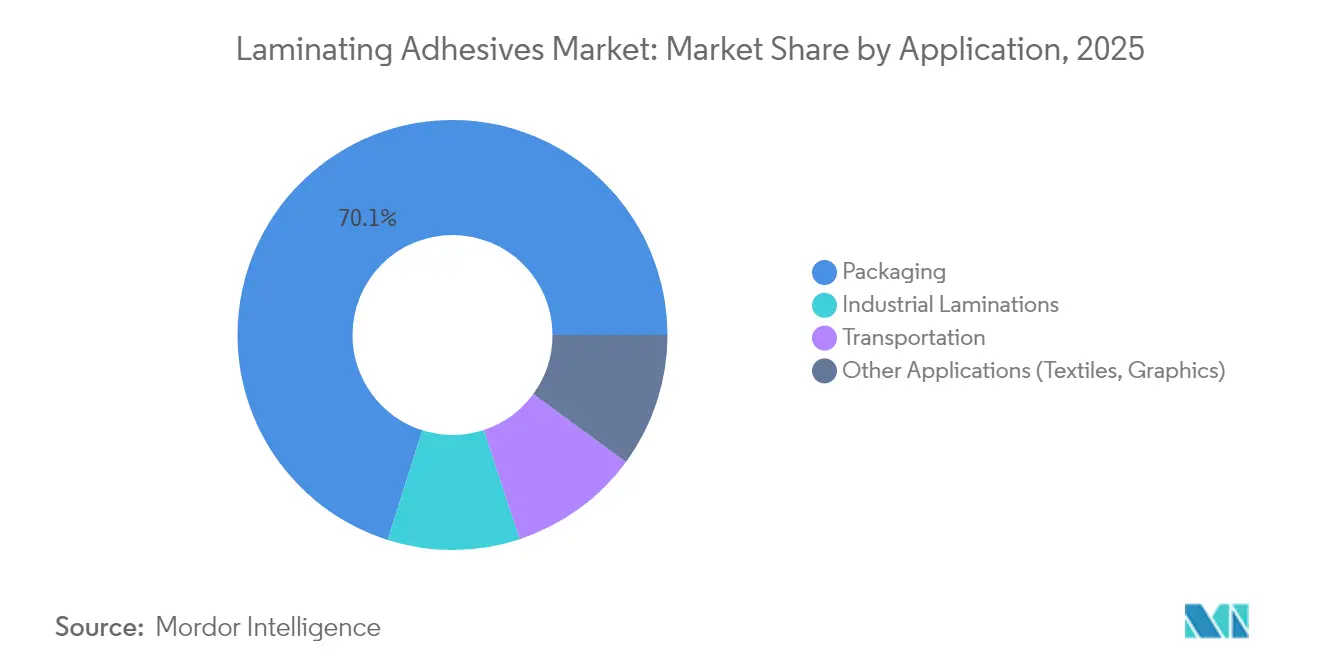

- By application, packaging captured 70.12% of laminating adhesives market size in 2025 and is advancing at an 7.88% CAGR to 2031.

- By geography, Asia-Pacific commanded 48.70% of laminating adhesives market share in 2025 and is forecast to record a 6.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laminating Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth in flexible food packaging | +1.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Surge in medical flexible pouches & IV-bag laminations | +1.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| E-commerce parcel boom demanding high-performance mailer laminates | +1.5% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Adoption of solvent-free PUR systems in high-speed tandem lines | +0.9% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Brand-owner push for mono-material recycle-ready laminates | +1.1% | EU leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Flexible Food Packaging

Flexible packaging’s 3.2% annual expansion toward a projected USD 341.6 billion by 2028 continues to lift demand for migration-resistant laminating adhesives that comply with FDA 21 CFR Part 175 and China’s GB 4806.15-2024 national food-contact adhesive standard. Converter requirements for precise thermal activation profiles ensure seal integrity during high-retort processes while preventing flavor transfer across multilayer structures. Leading suppliers differentiate through low-monomer PUR grades that fall beneath EU diisocyanate thresholds, shortening compliance lead times. Global food brands increasingly mandate quantitative migration testing, favoring vendors with in-house analytics and global regulatory dossiers. The laminating adhesives market capitalizes on this shift by scaling solvent-less lines that cut energy use and elevate workplace safety.

Surge in Medical Flexible Pouches & IV-Bag Laminations

Cast-extruded films deliver crystal clarity vital for IV-bag visual inspection, whereas blown-film laminates boost puncture resistance for pharmaceutical pouches. ISO 10993 biocompatibility testing poses high barriers, restricting new entrants and reinforcing premium pricing for validated grades. Wearable medical devices drive innovation in skin-friendly adhesives that balance adhesion and painless removal. Regulatory bodies demand sterilization stability across gamma, e-beam and ethylene oxide processes, pushing R&D toward chemistries that retain mechanical strength post-sterilization. North American producers leverage GMP facilities and track-record documentation to secure long-term hospital contracts.

E-Commerce Parcel Boom Demanding High-Performance Mailer Laminates

Global parcel volumes surged with double-digit growth in major urban corridors, and right-sized packaging initiatives demand adhesives compatible with automated form-fill-seal lines. Henkel’s Technomelt E-COM G5 Eco-Cool lowers application temperatures, cutting energy by up to 20% while offering high bio-based content. Extended producer-responsibility laws in the US and EU create fiscal incentives for material-efficient designs, rewarding laminating adhesives that maintain integrity despite thinner substrates. Consumer desire for effortless unboxing fosters tear-tape and debond-on-demand technologies. Service-temperature ranges spanning warehouse freezing to last-mile heat remain a core specification, driving multi-polymer or reactive systems.

Brand-Owner Push for Mono-Material Recycle-Ready Laminates

The EU Packaging and Packaging Waste Regulation institutes a 30% recycled-content mandate for PET food packaging by 2030, rising to 50% by 2040. Adhesive suppliers must ensure clean debonding during mechanical recycling to avoid polymer contamination. Collaborative R&D, such as Dow, Henkel and Kraton’s 25% carbon-footprint reduction tackifier program, illustrates industry commitment[1]Dow Chemical, “Dow, Henkel and Kraton Collaboration on Biobased Tackifiers,” corporate.dow.com. Flexible Packaging Association guidelines further codify adhesive compatibility with recycling streams, shaping formulation roadmaps Market pull from global CPG brands accelerates the commercialization of olefin-compatible one-component systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC & PFAS regulatory tightening on legacy solvents | -1.4% | EU leading, North America following | Short term (≤ 2 years) |

| Cost-inflation of bio-based polyols limiting green transition | -0.8% | Global, particularly impacting price-sensitive segments | Medium term (2-4 years) |

| Thermal-budget limits with heat-sensitive sustainable films | -0.6% | Global, concentrated in food packaging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

VOC & PFAS Regulatory Tightening on Legacy Solvents

The US EPA’s 40 CFR Part 59 sets stringent VOC ceilings for industrial adhesives, forcing reformulation of long-standing solvent products. California’s listing of vinyl acetate under Proposition 65 effective December 2025 increases labeling and reformulation costs across the region. Concurrently, EU rules cap total PFAS to 250 ppb in food packaging by August 2026, catalyzing rapid migration toward PFAS-free chemistries. Compliance expenditures and re-qualification testing stretch R&D budgets, disproportionately affecting smaller converters and accelerating consolidation within the laminating adhesives market.

Cost-Inflation of Bio-Based Polyols Limiting Green Transition

BASF’s bio-based ethyl acrylate showcases a 30% lower carbon footprint yet trades at a premium that suppresses mass adoption in cost-sensitive applications[2]BASF SE, “Bio-Based Ethyl Acrylate—Lower Carbon Footprint Adhesive Feedstock,” basf.com. Feedstock competition with biofuels and food crops intensifies price volatility, complicating long-term supply contracts. Limited global capacity heightens supply-risk perceptions, and certain bio-based grades still trail petrochemical counterparts in high-temperature resistance, necessitating further R&D spend. Without supportive carbon-pricing or green-subsidy mechanisms, widespread substitution remains gradual, moderating the pace of sustainability upgrades inside the laminating adhesives industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solvent-Less Systems Drive Technology Evolution

Solvent-borne products retained a 45.10% share of the laminating adhesives market in 2025, reflecting versatile adhesion and entrenched converter familiarity. The segment expands modestly, yet regulatory clampdowns on VOCs spur processors to reassess energy-intensive drying tunnels. Solvent-less grades are therefore registering a vigorous 7.36% CAGR toward 2031 as converters adopt high-speed tandem lines that eliminate ovens and curb energy bills by up to 40%. Water-borne dispersions occupy an intermediary niche, easing the learning curve for firms transitioning away from solvents while offering environmental benefits. Emerging UV- and electron-beam-curable systems target niche applications requiring instant green-strength and low migration.

Processing economics underpin this migration. Reactive PUR hot-melts supply the handling simplicity of hot-melts and the final strength of thermosets, making them prime candidates on duplex and triplex laminators. Microwave-triggered light-activated adhesives demonstrated by Hebrew University researchers hint at next-generation cure mechanisms that could enable on-demand recycling. Suppliers with broad technology portfolios gain strategic leverage by supporting converters through phased equipment upgrades while guaranteeing consistent performance across packaging, industrial and transportation end uses.

By Resin Chemistry: Polyurethane Dominance Faces Acrylic Challenge

Polyurethane’s 46.72% laminating adhesives market share in 2025 anchors on its wide service-temperature range and superior adhesion to multilayer structures. Decades of formulation refinement and an extensive library of FDA and EU dossiers make PUR indispensable for demanding food-contact, automotive and medical applications. Acrylic systems, however, are growing fastest at an 7.95% CAGR thanks to intrinsic weatherability, UV stability and compatibility with recycling-oriented mono-material packaging. Regulatory regimes favor acrylic’s non-isocyanate backbone, reducing worker training obligations under new EU diisocyanate rules.

Innovation within incumbents continues. BASF’s Lupasol additive suite elevates PUR adhesion to low-energy surfaces without compromising sterilization or retort requirements. Epoxies and ethylene-vinyl acetate (EVA) occupy smaller niches where extreme chemical resistance or cost efficiency prevail. Chemistry choice increasingly considers end-of-life scenarios; products that debond cleanly and minimize contamination during recycling gain procurement preference among multinational brand owners committed to circular economy targets.

By Application: Packaging Supremacy Drives Market Dynamics

Packaging accounted for 70.12% of laminating adhesives market size in 2025 and is advancing at an 7.88% CAGR through 2031 as converters prioritize lightweight films that extend shelf life and reduce logistics costs. Food packaging dominates, demanding low-migration, high-retort adhesives that pass rigorous organoleptic testing. Medical packaging forms a high-value sub-niche where ISO 10993 biocompatibility and sterilization stability justify premium pricing. Consumer goods and industrial packaging similarly embrace solvent-less solutions to align with corporate sustainability pledges.

Beyond packaging, industrial laminations span construction panels, electronic assemblies and insulation layers, demanding heat, vibration and chemical resilience. Transportation applications employ structural laminating adhesives in automotive interiors and aerospace composites, combining low weight and high fatigue strength. Smaller niches such as textile lamination and graphic films present tailored opportunities for high-margin specialty manufacturers like Sika that leverage application-specific know-how. This diverse demand matrix supports steady volume growth while allowing specialized players to defend premium positions.

Geography Analysis

Asia-Pacific commanded 48.70% of laminating adhesives market share in 2025 and is forecast to grow at a 6.95% CAGR through 2031. China’s USD 1.6 billion acrylic acid investment leveraging propane feedstock underlines cost-innovation synergies. India’s growing middle class and infrastructure projects, coupled with Henkel’s Loctite facility expansion in Maharashtra, anchor regional capacity. Japan and South Korea contribute high-precision formulations for electronics and EV battery modules, benefiting from tight supply chains and robust IP protections.

North America leverages advanced R&D ecosystems and stringent regulatory oversight that accelerate sustainable-formulation breakthroughs. The region’s leading role in medical device and pharmaceutical manufacturing drives specialized adhesive demand aligned with FDA requirements. Canada’s restriction on polycyclic aromatic hydrocarbon (PAH) sealants highlights the continent’s regulatory influence on global suppliers. Mexico’s cost-competitive plants support NAFTA supply chains in automotive interiors and consumer packaging.

Europe continues to shape global standards. The EU’s escalating recycled-content mandates steer converter investments toward recyclable PUR and acrylic systems. Germany’s engineering base fosters continuous process improvements, while France and Italy retain sizable converting clusters that rely on solvent-less upgrades. South America and Middle East & Africa, though smaller today, display above-average growth as infrastructure and consumer markets expand. Saint-Gobain’s USD 1.025 billion FOSROC deal underscores rising interest in these regions’ construction and industrial segments.

Mordor Intelligence provides coverage of the laminating adhesives market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Regulation for laminating adhesives is being shaped by overlapping food-contact, chemical-safety, and circular-economy requirements across major end-use regions. In the United States, food packaging laminations commonly align with FDA food-contact provisions such as 21 CFR 175.105 (adhesives) and 21 CFR 175.125 (pressure-sensitive adhesives), which constrain allowable raw materials, residuals, and compliance documentation for converters and brand owners.

In Europe, REACH and CLP implementation continues to tighten obligations on both formulations and upstream inputs. REACH Annex XVII has already introduced use-based controls such as mandatory diisocyanate training (Entry 74, in force since August 2023) and restrictions on DMF in articles above 0.3% (Entry 71a, since December 2023), while CLP labeling changes under Regulation (EU) 2024/2865 begin full application on July 1, 2026. Packaging circularity adds an additional compliance layer: the EU Packaging and Packaging Waste Regulation (PPWR 2025/40) becomes compulsory on August 12, 2026, pushing adhesive selection toward recycle-ready structures and raising the importance of supplier regulatory dossiers and downstream recyclability compatibility testing.

Value Chain Analysis

The laminating adhesives value chain runs from petrochemical and specialty-chemical feedstocks (polyols, isocyanates, acrylic monomers, tackifiers, solvents and additives) through adhesive formulators with reactor and blending assets, to packaging converters operating duplex and triplex laminators, and finally to brand owners that set performance and compliance specifications. Because packaging is the dominant application, qualification workflows are heavily influenced by food-contact and migration requirements, which increases demand for suppliers able to deliver consistent batch quality, analytical support, and multi-region regulatory documentation.

Supply and distribution are also shaped by logistics constraints and hazardous-material handling needs, particularly for solvent-borne products and sensitizing or reactive chemistries such as isocyanate-based systems. Industry consolidation and portfolio realignment are further reshaping manufacturing footprints and channel access; for example, Dow completed the USD 150 million sale of its flexible-packaging laminating adhesives business to Arkema in December 2024, transferring assets across Italy, the United States, and Mexico. Alongside M&A-driven scale, recent moves such as hubergroup localizing production for its Gecko LA laminating adhesives in Europe (introduced to the European market in March 2026) reflect the push for closer-to-customer supply to reduce lead times and improve supply assurance.

Competitive Landscape

The laminating adhesives market exhibits moderate fragmentation. Henkel, 3M and BASF leverage integrated feedstocks, global technical centers and broad regulatory dossiers to sustain leadership. Competitive intensity centers on sustainability credentials. 3M earmarked USD 1 billion over 20 years to decarbonize operations and eliminate PFAS, raising the bar on transparency for the broader laminating adhesives industry. Arkema targets rapid integration of Dow’s plants, promising accelerated solvent-less production and expanded regional service reach.

Niche innovators pursue bio-polyurethane grades using castor-oil polyols, while start-ups develop enzyme-degradable acrylics aimed at truly compostable packages. Large players defend share by bundling adhesives with ancillary coatings, primers and dispensing equipment, locking customers into long-term technology roadmaps.

Laminating Adhesives Industry Leaders

3M

Henkel AG & Co. KGaA

Arkema (Bostik)

Dow

H.B. Fuller

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity lies in accelerated product and process substitution away from legacy solvent-borne systems toward solvent-free and low-migration chemistries that fit tightening VOC, labeling, and packaging circularity requirements. The EU PPWR 2025/40 becoming compulsory from August 12, 2026 provides a concrete compliance anchor for recycle-ready packaging design, increasing pull for laminating adhesives that support mono-material structures and cleaner recycling outcomes rather than acting as polymer contaminants. Food-contact compliance remains a commercial gatekeeper, so suppliers that pair solvent-less or water-borne platforms with robust FDA and EU dossiers, migration testing support, and converter line-startup expertise have room to capture qualification-driven switching.

Capacity and footprint moves by packaging-adjacent participants also support investment-led opportunities in regional supply where converters prioritize shorter lead times and safer handling. Arkema finalized the acquisition of Dow's flexible packaging laminating adhesives business in December 2024, adding five production sites spanning Italy, the United States, and Mexico, which can widen supply options for converters and expand technical service coverage. On the demand side, brand-owner sustainability requirements translate into new product introductions and platform refreshes in solvent-free lamination, including Sun Chemical's solvent-free ultra-low monomer (ULM) lamination adhesive product line in January 2026 and broader supplier emphasis on circularity-enabling packaging adhesives, as highlighted by Henkel Adhesive Technologies ahead of Interpack 2026.

Recent Industry Developments

- July 2026: Brilliant Polymers announced a next-generation solvent-free laminating adhesive platform to be unveiled at the ElitePlus 2026 flexible packaging summit. The announcement points to continued product-cycle acceleration around solvent-free lamination for high-speed packaging lines and increases competitive pressure on established suppliers among converters focused on VOC reduction.

- April 2026: Bostik unified its flexible materials laminating adhesives and coatings portfolio under the global ADCOTE brand following the integration of Dow's acquired laminating adhesives business. The change streamlines product positioning and technical selling across regions, supporting faster cross-selling into flexible packaging accounts served from the enlarged manufacturing footprint.

- December 2024: Dow completed the USD 150 million sale of its flexible packaging laminating adhesives business to Arkema, transferring assets across Italy, the United States, and Mexico. The transaction reshaped capacity ownership and expanded Arkema's direct presence in laminating adhesives, strengthening its ability to serve multinational packaging customers with local supply and technical support.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the laminating adhesives market covers adhesive formulations used to bond two or more layers of films, foils, paper, or other substrates into a laminate. Here, the adhesive layer has to deliver the required bond strength and end-use performance for the finished laminate.

Scope exclusions: pressure-sensitive label adhesives, construction sealants, and non-lamination bonding applications are excluded unless the adhesive is sold and used specifically for lamination.

Segmentation Overview

- By Type

- Solvent-borne

- Water-borne

- Solvent-less

- Other Types (UV/EB-curable)

- By Resin Chemistry

- Polyurethane

- Acrylic

- Epoxy

- Other Resin Chemistries (EVA, Polyolefin, Nitrile)

- By Application

- Packaging

- Food

- Medical

- Other Packaging

- Industrial Laminations

- Transportation

- Other Applications (Textiles, Graphics)

- Packaging

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the value chain and identifying where demand is created, which is mainly in flexible packaging and other industrial laminations. We pull baseline indicators and definitions from public sources such as US Census Bureau manufacturing data, Eurostat industrial statistics, UN Comtrade trade flows for relevant polymer and chemical categories, and publications from packaging and adhesives trade associations. To keep assumptions grounded, we also review technical literature such as peer-reviewed journals on polyurethane and acrylic adhesive chemistries, and public patent databases, to understand formulation direction.

We then check company filings, annual reports, and investor presentations for capacity additions, plant utilization commentary, and regional revenue splits that can be tied back to laminating systems. When needed, paid subscriptions are used for company financials and intelligence, patent analytics, and shipment-level import and export screening, primarily to cross-check volumes and identify gaps that public datasets do not explain well. The sources listed here are illustrative only, and many other public documents were referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions and refine inputs that are usually not stated in public sources, including typical dry-bond coating weights, yield losses, and how pricing changes by technology and end-use. We spoke with stakeholders across resin suppliers, adhesive formulators, converters, and packaging buyers, then validated the major regional demand shifts across APAC, EMEA, and the Americas so the model reflects what buyers report as actual purchasing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 41% |

| Mid tier: 55% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 17% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where packaging output and laminated substrate demand are reconstructed by region, then converted into adhesive consumption using typical coating weight ranges and the penetration of solvent-borne, water-borne, and solvent-less systems. After the demand pool is established, average selling prices are applied by technology and region, since price behavior differs across solvent-free systems versus conventional grades, and because feedstock swings transmit at different speeds.

To keep totals realistic, we corroborate the results with selective bottom-up approximations, such as rolling up sampled supplier revenues tied to laminating lines, checking distributor and converter channel feedback, and using volume times price sanity checks for key end uses. Inputs that matter most include flexible packaging production trends, regulatory pressure on VOC emissions that shifts mix, resin and solvent cost direction, converter run rates, and trade movement of laminate films and foils as a demand signal. For forecasting, scenario analysis is used around packaging growth, technology mix shifts, and price normalization, with assumptions aligned to what primary respondents describe as the most likely path. When a data point is missing for smaller countries, proxies like packaging output shares and import dependence are applied, then reviewed again with regional interviews.

Data Validation & Update Cycle

Validation is done in layers so outliers are caught early, starting with unit-consistency checks on volumes, coating weights, and price inputs before totals are finalized. We compare the model outputs against independent signals such as packaging production direction, resin price movements, and trade patterns, then flag variances that do not match what converters and suppliers described. A separate analyst review is performed to re-check formulas, currency conversions, and year mapping, and follow-up calls are triggered when a region shows an unusual jump or drop.

The report is refreshed annually, and interim updates are made when major capacity changes, regulation shifts, or sharp feedstock moves are observed. Before delivery, a final analyst pass is completed so the published numbers reflect the latest available information and the same assumptions are applied consistently across the full time series.

Mordor Intelligence's Laminating Adhesives Market Size Versus Other Published Estimates

Published market sizes for laminating adhesives often do not line up because the boundary between lamination and adjacent adhesive uses is applied differently across studies, and because base-year selection can shift the entire series. Differences also come from how prices are handled when resin and solvent costs move quickly, and from whether the estimate is anchored to packaging output signals or to supplier-side reporting.

When currency timing is updated to the latest annual averages, and when price progression is validated with converter checks instead of using a single inflation factor, the resulting total can change even if underlying demand is stable. This refresh-led treatment is a key reason the 2026 value in Mordor Intelligence reads higher than some 2024 anchored figures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.09 B (2026) | |

| Industry Publisher A | USD 3.64 B (2024) | Uses an earlier base year and often blends lamination adhesives with adjacent bonding uses, and the price series is typically tied to a broad chemical inflation proxy rather than technology-specific ASP movements. |

| Industry Publisher B | USD 3.60 B (2024) | Relies on a mixed timeline and stated market value for 2024 without clearly showing how coating weight, packaging output, and currency conversion timing are applied across regions, which can compress or expand totals. |

The table indicates that the spread is mainly explained by base-year choice, scope boundary around lamination-only demand, and how pricing and currency are updated over time. By keeping the demand build tied to laminate production signals and then re-checking implied prices with primary feedback, the final number becomes easier to trace and repeat in future updates.

Key Questions Answered in the Report

What is the current Laminating Adhesives Market size?

The laminating adhesives market stands at USD 4.09 billion in 2026 and is projected to reach USD 5.49 billion by 2031.

Which application accounts for the largest portion of laminating adhesives demand?

Packaging dominates with 70.12% of laminating adhesives market size in 2025, led by food, e-commerce and medical pouches.

Why are solvent-less systems growing faster than solvent-borne adhesives?

Solvent-less systems eliminate drying ovens, cut energy consumption by up to 40% and help converters comply with stricter VOC limits, driving a 7.36% CAGR through 2031.

How are regulations shaping adhesive chemistry choices?

EU PFAS limits and US VOC caps push converters toward acrylic and solvent-free PUR chemistries that offer safer profiles and easier regulatory clearance.

Page last updated on: