Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The High Strength Laminating Adhesives Market Report is Segmented by Resin Type (Polyurethane, Acrylic, Epoxy, Other Resin Types), Technology (Water-Borne, Solvent-Based, Hot-Melt, UV-Curable), Application (Packaging, Automotive, Industrial, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

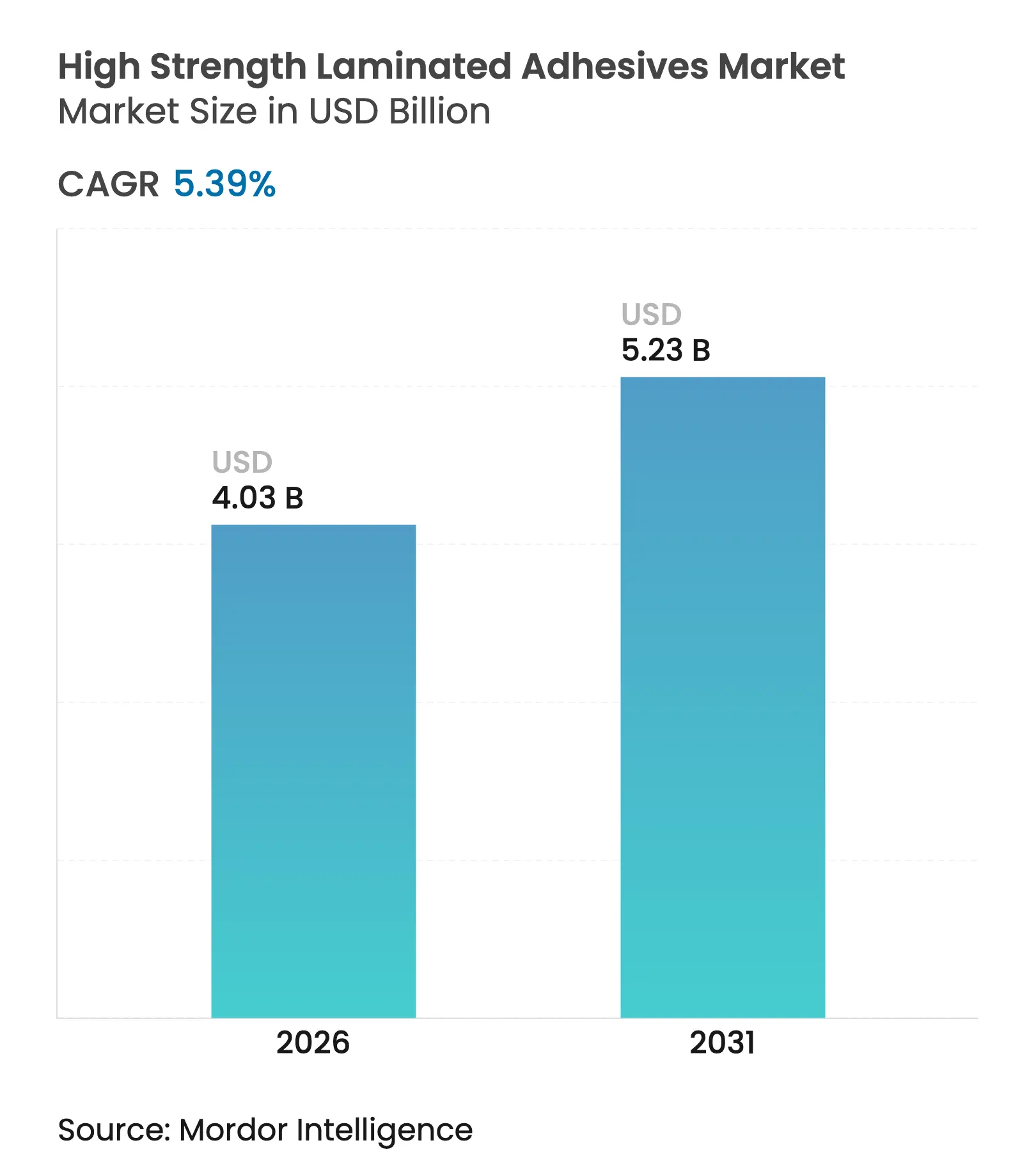

| Market Size (2026) | USD 4.03 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 5.39 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

High Strength Laminated Adhesives Market size in 2026 is estimated at USD 4.03 billion, growing from 2025 value of USD 3.82 billion with 2031 projections showing USD 5.23 billion, growing at 5.39% CAGR over 2026-2031. Robust flexible-packaging demand, accelerating automotive lightweighting and rapid electronics miniaturization keep the market firmly on a growth track despite tighter environmental rules. Producers are racing to introduce low-VOC chemistries, develop bio-based feedstocks and localize production in Asia-Pacific to capture rising downstream output. Strategic divestments, such as Dow’s sale of its flexible-packaging laminating adhesives line, illustrate an industry streamlining around high-value niches while raw-material volatility pressures margins. Technology migration toward UV-curable and water-borne systems is gathering pace, yet solvent-based products still dominate critical high-performance laminations, highlighting a market in transition. Consolidation among tier-one players is tempered by a long tail of regional specialists that anchor supply close to converters and car plants.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating Demand for Flexible and Lightweight Packaging

Escalating Demand for Flexible and Lightweight Packaging

| + 1.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+ 1.8% |

Geographic Relevance

:

Global, with concentration in Asia-Pacific and North

America

|

Impact Timeline

:

Medium term (2-4 years)

|

Automotive Lightweighting Replacing Mechanical Fasteners

Automotive Lightweighting Replacing Mechanical Fasteners

| + 1.2% | Global, led by North America and Europe | Long term (≥ 4 years) | |||

Regulatory Push Toward Low-Volatile Organic Compound (VOC) and Solvent-Free

Chemistries Regulatory Push Toward Low-Volatile Organic Compound (VOC) and Solvent-Free

Chemistries | + 1.0% | Europe and North America, expanding to Asia-Pacific | Short term (≤ 2 years) | |||

Electronics Miniaturization in Global Manufacturing Hubs

Electronics Miniaturization in Global Manufacturing Hubs

| + 0.9% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) | |||

Ultraviolet (UV)-Curable Lines for On-Demand Short-Run Packaging Ultraviolet (UV)-Curable Lines for On-Demand Short-Run Packaging | + 0.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Demand for Flexible and Lightweight Packaging

Flexible packaging volumes keep rising as brand owners pursue down-gauging and consumer convenience. The sector is projected to hit USD 341.6 billion by 2028, lifting multilayer laminate output that relies on high-performance bonding systems [1]H.B. Fuller, “Flexible Packaging Market Outlook,” hbfuller.com. Mono-material pouches and recyclable barrier films mandated under the European Green Deal require adhesives compatible with closed-loop recycling, opening premium niches for product formulators. E-commerce adds urgency, with Packsize and Henkel reporting a 32% greenhouse-gas cut across 340 million shipper boxes when using Eco-Pax bio-based hot-melt solutions. Suppliers able to certify food-contact safety, low migration and de-inking debonding gain a pricing edge in the laminating adhesives market.

Automotive Lightweighting Replacing Mechanical Fasteners

Modern vehicles average more than 400 linear feet of adhesive versus 30 feet two decades ago, underscoring the structural shift from rivets and welds to bonding lines [2]3M, “Automotive Adhesive Solutions,” 3m.com. Mixed-material bodies in white, battery-pack encapsulation and noise-damping laminates all raise the technical bar for shear strength and thermal-cycling durability. Mexico’s auto sector, contributing 6% to national GDP, is on track for 13% production growth, amplifying localized demand in North American supply corridors. Thermoplastic polyurethane formulations gain share as OEMs prioritize dismantlability and end-of-life recycling.

Regulatory Push Toward Low-Volatile Organic Compound (VOC) and Solvent-Free Chemistries

The EU’s 2023 diisocyanate rule compels specialized training for polyurethane (PU) products above 0.1% monomer content, accelerating a pivot to non-isocyanate polyurethane (PU) and water-borne systems. Henkel and Celanese are piloting captured-CO₂ feedstocks for water-based grades in a drive to decarbonize upstream raw materials. BASF’s switch to 40% bio-content ethyl acrylate cuts product carbon footprint by 30%, illustrating how large suppliers translate policy pressure into portfolio renewal. The laminating adhesives market rewards producers who deliver compliance without compromising line speed or heat resistance.

Electronics Miniaturization in Global Manufacturing Hubs

Wafer-level packaging, foldable displays and high-density interposers need ultra-thin, optically clear and thermally stable adhesives. DELO generates half its revenue in Asia, reflecting semiconductor clustering in China, South Korea and Southeast Asia. Near Field Communication (NFC)-enabled smart labels extend adhesive applications into connected packaging, blending electronics with converting know-how. New grades must withstand extreme reflow profiles yet release under selective laser debonding, creating technical differentiation in the laminating adhesives industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Raw-Material Price Volatility Raw-Material Price Volatility | -0.8% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Global, with acute impact in Asia-Pacific manufacturing | Impact Timeline:Short term (≤ 2 years) |

Stringent Solvent-Emission Regulations Stringent Solvent-Emission Regulations | -0.5% | Europe and North America, expanding globally | Medium term (2-4 years) | |||

Supply Bottlenecks in Bio-Based Polyurethane Feedstocks Supply Bottlenecks in Bio-Based Polyurethane Feedstocks | -0.3% | Europe and North America, with spillover to Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Raw-Material Price Volatility

Raw material price volatility continues to pressure laminating adhesives manufacturers, with BASF implementing price increases of USD 0.08-0.10 per pound for key polyurethane precursors including 1,4-Butanediol and N-Methylpyrrolidone effective April 2025. Seventy-nine percent of composites fabricators cite resin shortages, exposing formulators to unpredictable lead times. Petroleum dependency keeps polyurethane inputs tethered to crude swings, while bio-based feedstocks face limited scale. Suppliers respond with quarterly pricing clauses and dual-sourcing strategies, yet the uncertainty still trims margin expansion in the laminating adhesives market.

Stringent Solvent-Emission Regulations

Increasingly stringent solvent-emission regulations are constraining traditional adhesive formulations, with the South Coast Air Quality Management District's Rule 1168 establishing volatile organic compound (VOC) limits as low as 25 g/L for super-compliant products. PFAS litigation surpassed USD 11 billion in 2023 settlements, heightening scrutiny of fluorinated surfactants in certain formulations. H.B. Fuller closed one-third of its sites to streamline compliant capacity and balance fixed costs. Smaller regional blenders risk exit if capital needs for abatement and reformulation outstrip cash flow.

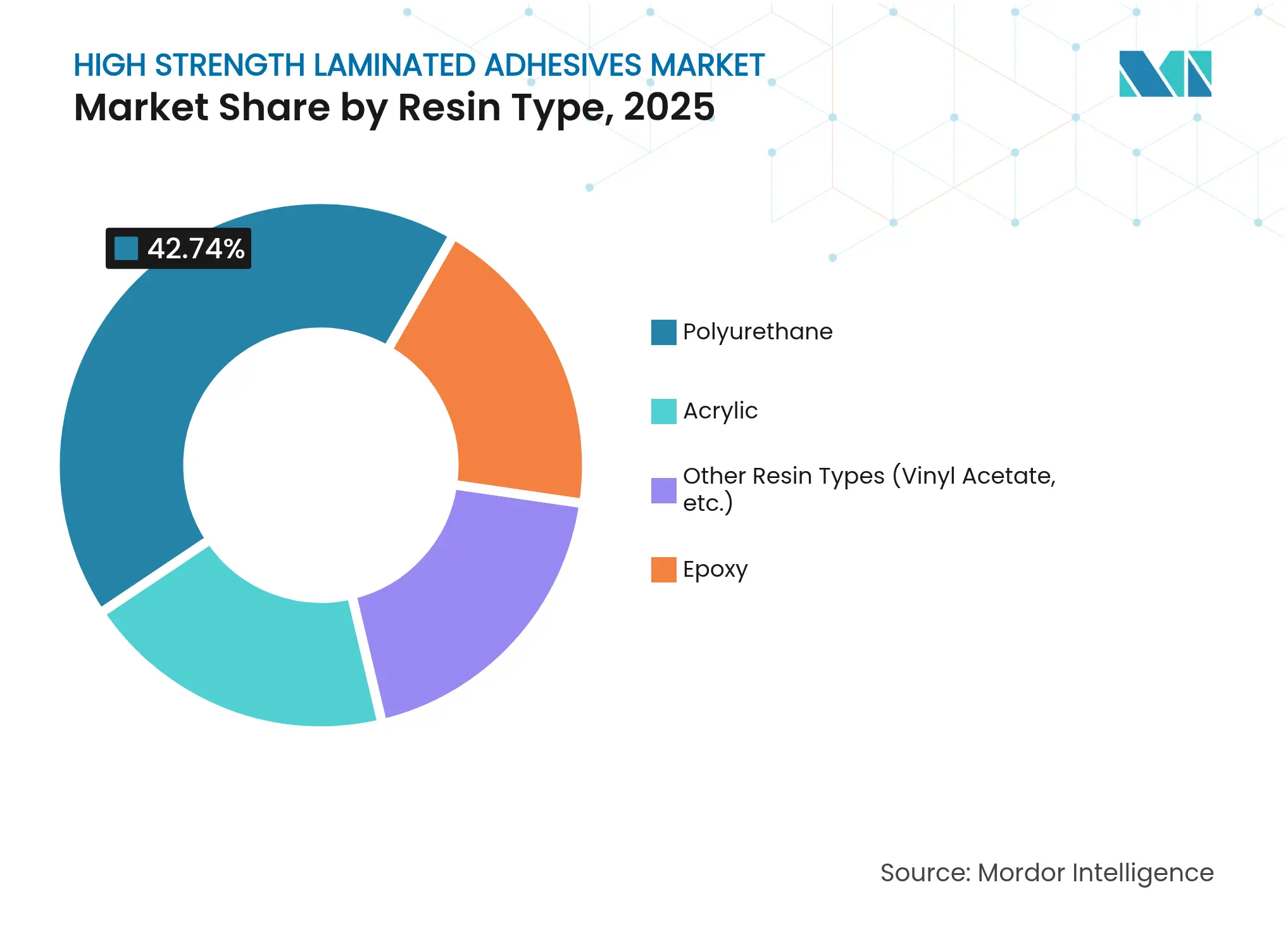

By Resin Type: Polyurethane Dominance Drives Innovation

Polyurethane (PU) claimed 42.74% of global revenue in 2025, underscoring its versatility in high-flexibility pouch laminations and resilient automotive interior skins. The segment is projected to grow at a 5.78% CAGR through 2031, keeping its lead in the laminating adhesives market as converters favor robust adhesion across heterogeneous substrates. Regulatory pressure on diisocyanates accelerates migration to non-isocyanate polyurethane (PU) and bio-based polyol routes that curb hazard labeling without sacrificing bond strength.

Bio-content gains momentum with lignin-, soy-, and castor-derived precursors enabling partially renewable polyurethane chains. Research demonstrates successful Non-Isocyanate Polyurethane (NIPU) syntheses that retain hydrolysis resistance equal to incumbent grades. Acrylic systems pick up share in ultraviolet (UV)-curable electronics laminations where optical clarity and rapid line speed are paramount. Epoxies continue to serve niche aerospace and wind-blade fabrics demanding extreme chemical stability, yet their relative market slice stays modest. Overall, innovation in polyurethane keeps the laminating adhesives market moving toward lower-carbon yet high-performance solutions.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Ultraviolet (UV)-Curable Emergence Challenges Solvent Dominance

Solvent-based lines still represent 38.67% of sales in 2025 and remain indispensable for demanding barrier film and retort pouch structures that need deep-penetrating adhesion. Yet regulatory headwinds and energy-cost inflation channel fresh investment toward waterborne and ultraviolet (UV)-curable alternatives. Ultraviolet (UV)-curable technology, forecast to post a 6.27% CAGR, benefits from on-press curing, minimal emissions, and sharply reduced drying footprints that suit contract packers with space constraints.

Water-borne grades capitalize on FEICA (Association of the European Adhesive & Sealant Industry) findings that label them the fastest-growing low-VOC option in Europe . Hybrid formulations emerge, blending moisture-curing polyurethane dispersions with radiation-sensitive photoinitiators to deliver broad substrate compatibility. Hot-melt solutions defend their territory in instant-tack automotive carpets and roof-liner stacks where cycle times dominate cost models. Technology diversification means converters specify adhesive performance windows rather than chemistry families, nudging suppliers to build multi-platform portfolios across the laminating adhesives market.

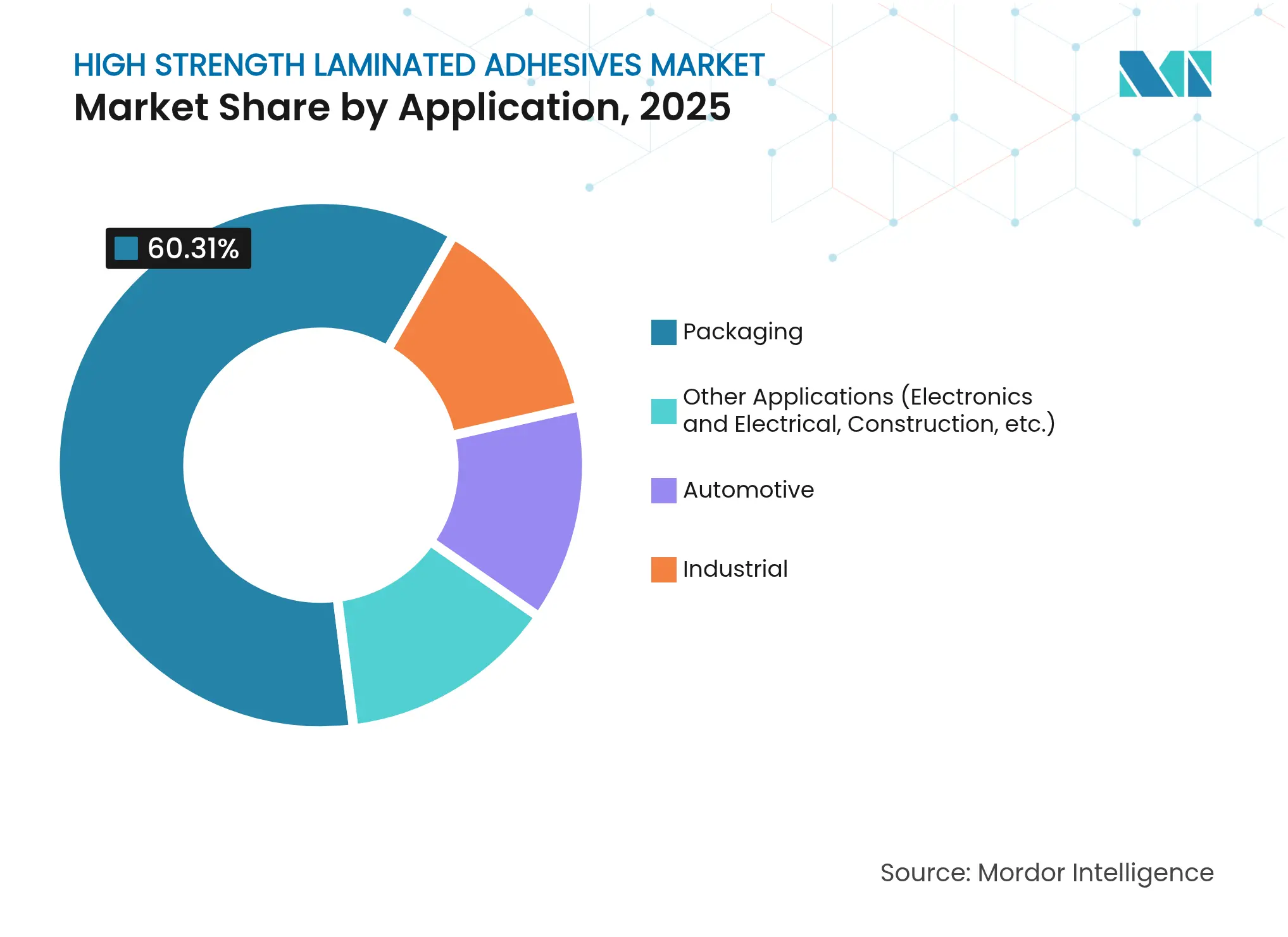

By Application: Packaging Leadership Faces Electronics Challenge

Packaging accounted for 60.31% of 2025 revenue and remains the volume anchor of the laminating adhesives market size. Pouch structures with ethylene vinyl alcohol (EVOH) barriers, retort lids and perforated snack laminations all depend on robust interlayer bonds. Mono-material designs push adhesion engineering to deliver comparable gas barriers without aluminum foil, driving specification upgrades that lift unit value.

Electronics, forecast to climb at a 5.86% CAGR, is the breakout growth engine. Foldable organic light emitting diode (OLED) screens, camera module encapsulation and high-frequency antenna wraps need adhesives that balance optical clarity, dielectric stability and rapid thermal cycling endurance. Automotive applications leverage the same laminating technologies in battery modules, interior trims and lightweight composites. Industrial laminations in furniture, textiles and flooring maintain steady but slower growth, reflecting substitutability and price sensitivity outside highly engineered sectors.

Note: Segment shares of all individual segments available upon report purchase

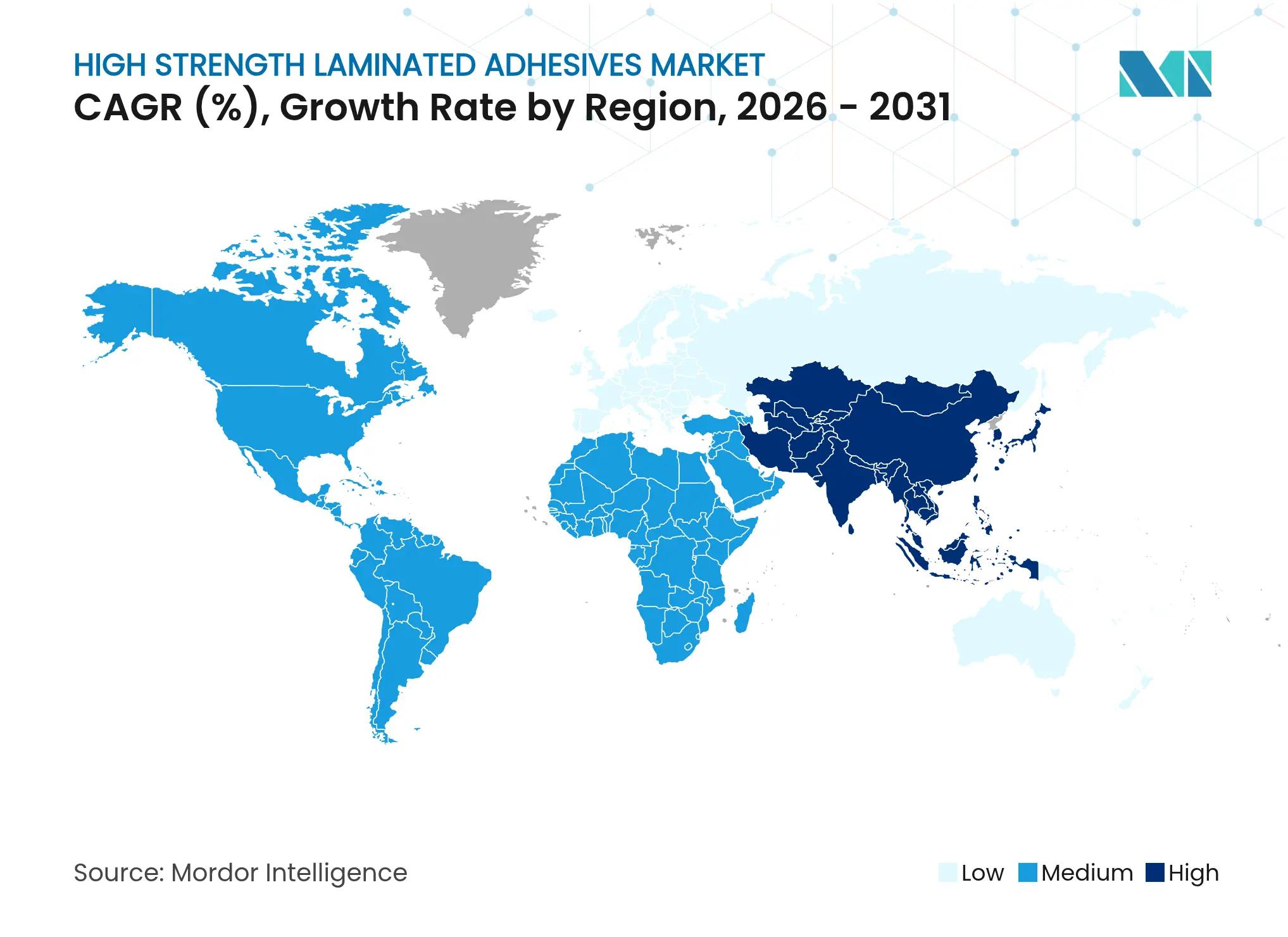

Asia-Pacific commanded 44.02% of global demand in 2025 and is anticipated to expand at a 5.79% CAGR through 2031, fueled by chemical cluster investment and rising per-capita packaged-goods consumption. Regional heavyweights, including China’s converters and India’s new Loctite plant, localize supply, shorten lead times and cut currency risk for multinationals.

North America remains a high-value arena where automotive lightweighting and food-contact safety standards steer innovation. Lubrizol’s USD 20 million acrylic-emulsion expansion in North Carolina illustrates continued capacity reinforcement for specialty grades.

Europe’s stringent emission rules catalyze technology pivots and extend producer-responsibility schemes that prioritize recycle-ready laminations, pushing regional formulators into low-monomer polyurethane and water-borne recipes. Latin America and the Middle East present emergent demand nodes linked to industrialization projects and consumer spending catch-up, albeit from lower bases. The geography split shows that proximity to downstream packagers and automakers remains decisive for success in the laminating adhesives market.

Market Concentration

The global high strength laminated adhesives market is a fragmented market with the presence of a large number of players globally. Bostik, Arkema’s adhesive unit, earmarked USD 27 million for Massachusetts hot-melt capacity upgrades aimed at e-commerce packaging. H.B. Fuller Company rationalized one-third of plants to trim fixed costs amid shifting technology mix. Competitive advantage now tilts toward sustainability credentials, multi-technology portfolios, and regional proximity. Suppliers with cradle-to-gate carbon data, recyclable-pack certified grades and compliance expertise gain preferred-supplier status among converters mapping Scope 3 emissions.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The high strength laminated adhesives market report includes:

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.