Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

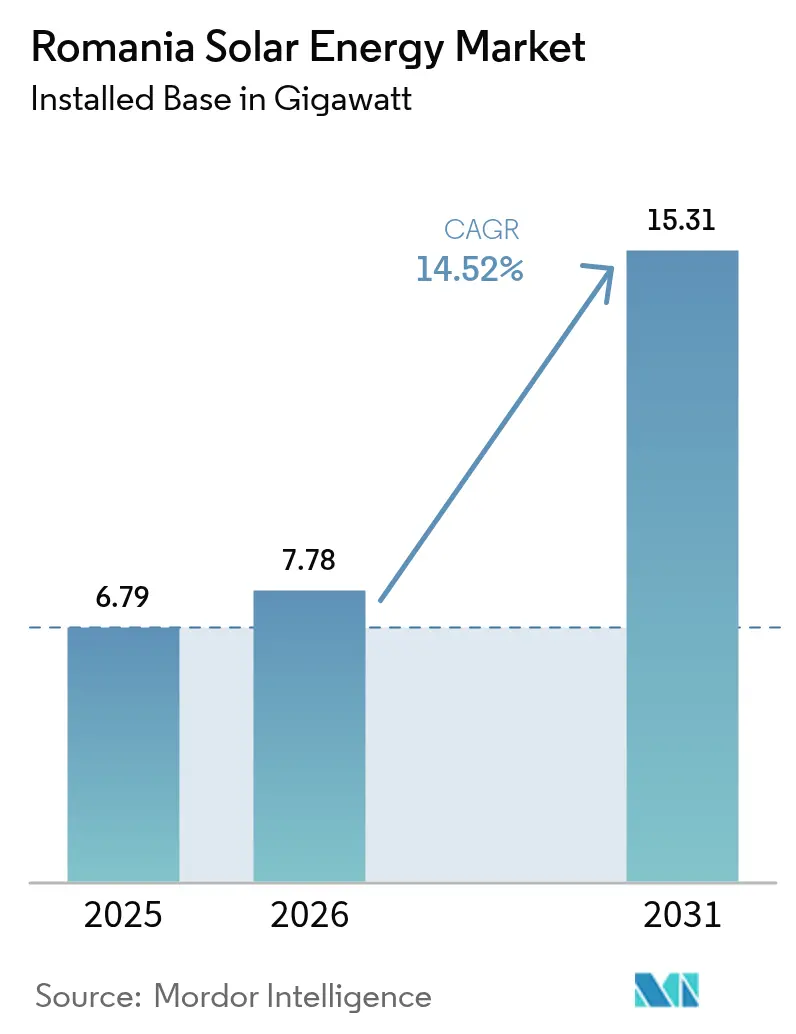

| Base Year Market Size (2025) | 6.79 gigawatt |

| Market Volume (2026) | 7.78 gigawatt |

| Market Volume (2031) | 15.31 gigawatt |

| Growth Rate (2026 - 2031) | 14.52% CAGR |

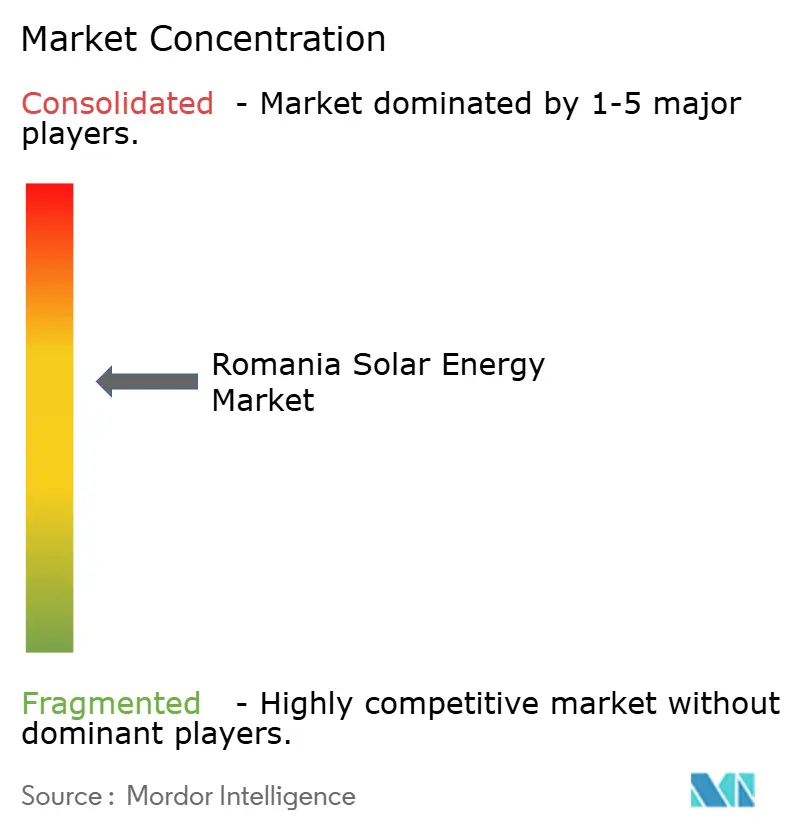

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Solar Energy Market Analysis by Mordor Intelligence

Romania Solar Energy Market size in 2026 is estimated at USD 7.78 gigawatt, growing from 2025 value of USD 6.79 gigawatt with 2031 projections showing USD 15.31 gigawatt, growing at 14.52% CAGR over 2026-2031.

This acceleration is powered by Recovery and Resilience Facility grants, streamlined dual-use agricultural rules, and surging corporate PPAs that anchor new capacity to long-term offtake contracts. Grid digitalization, falling solar PV costs, and a EUR 3 billion Contracts for Difference (CfD) scheme further enhance revenue certainty for utility-scale projects. Romania’s pivot away from coal has also re-positioned distribution utilities as active enablers of rooftop programs, while local manufacturing incentives are shortening supply chains and supporting job creation. Together, these factors advance the Romanian solar energy market as a central and eastern European deployment hub.

Key Report Takeaways

- By technology, solar photovoltaic accounted for 100.00% of the Romania solar energy market share in 2025.

- By grid type, on-grid systems dominated the Romanian solar energy market with a 95.10% share in 2025.

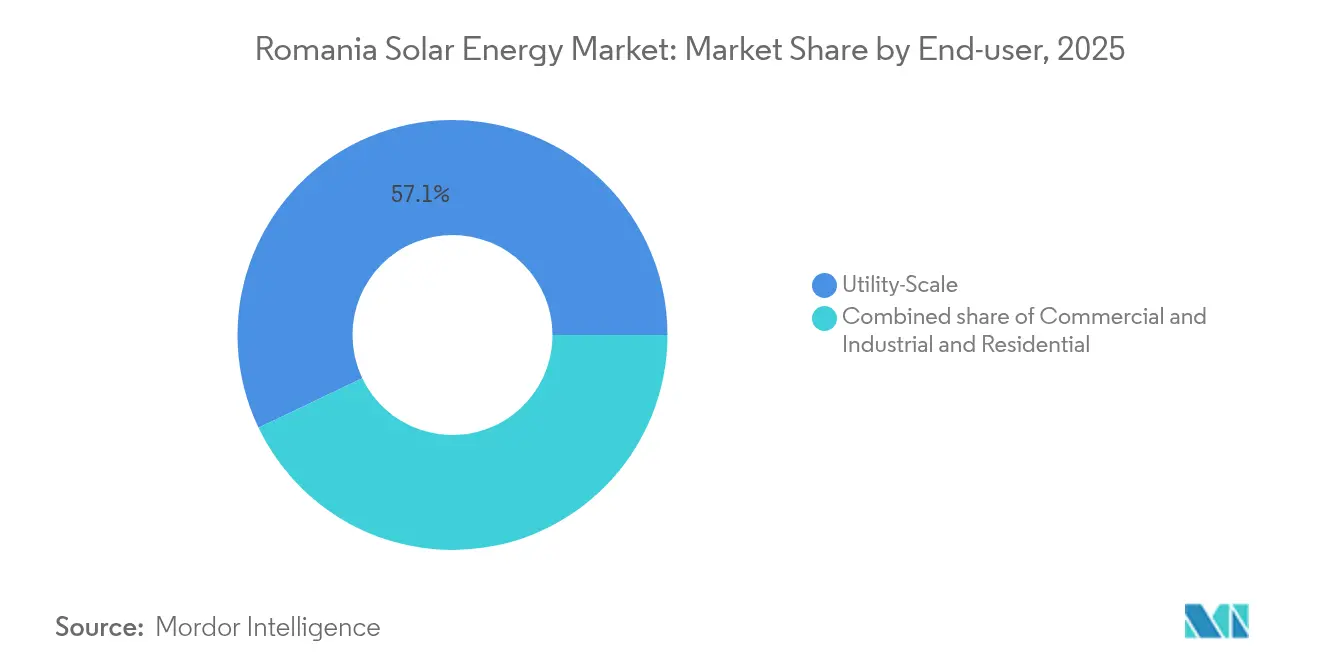

- By end-user, utility-scale plants led the Romanian solar energy market with a 57.10% share in 2025, while the residential segment is projected to grow at an 18.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-funded renewable stimulus (RRF) | +3.20% | National, south and west counties | Medium term (2-4 years) |

| Supportive feed-in premiums & green certificates | +2.80% | National, rural focus | Long term (≥ 4 years) |

| Corporate PPA demand surge | +2.10% | Industrial corridors nationwide | Short term (≤ 2 years) |

| Declining LCOE of solar PV | +1.90% | Global cost dynamic, local uptake | Medium term (2-4 years) |

| Grid digitalization enabling distributed PV | +1.50% | Urban and peri-urban areas | Long term (≥ 4 years) |

| Agri-PV pilots unlocking dual land use | +1.30% | Southern agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-funded renewable stimulus (RRF)

Romania’s National Recovery and Resilience Plan allocates EUR 2.8 billion to renewables, with an additional EUR 400 million from the Modernisation Fund dedicated to solar and wind energy. Contracts already cover 831 public-sector PV projects, totaling 296.76 MW, and are backed by €367.6 million in grants.(1)Newsweek Romania, “Fabrica de soare a României: 831 de proiecte…,” newsweek.roThese programs remove capital-cost barriers, target 3 GW of new capacity by 2026, and stimulate private co-investment that multiplies public outlays. Spillover estimates imply each public euro attracts roughly 1.1 euros of private spending EIB.ORG. The model also scales installer skills and supply-chain depth, accelerating subsequent commercial and residential solar uptake.

Supportive feed-in premiums & green certificates

The dual incentive framework combines feed-in premiums with tradable green certificates, offering stable income streams that enhance the bankability of installations up to 400 kW. Streamlined ANRE rules reduce permitting times and transaction costs, allowing small systems to monetize surplus power while enjoying premium tariffs. Although Emergency Ordinance 20/2025 removes certificate obligations for major industrial buyers, it steers those consumers toward direct solar procurement, preserving demand for new rooftop and ground-mounted plants. The blended policy approach reduces financing spreads relative to full merchant exposure.

Corporate PPA demand surge

Long-term solar PPAs are now a preferred hedge for manufacturers facing volatile wholesale prices. DRI-OMV Petrom signed a 100 GWh annual physical delivery contract, the country’s largest corporate renewable energy agreement, setting price discovery benchmarks for future deals.(2)European Investment Bank, “Investment Report 2023/2024,” eib.org Source: Green-Forum, “nextE,” green-forum.eu Independent power producers are building plants expressly around such agreements, while Emergency Ordinance 143/2021 lifted bilateral-trading restrictions and simplified risk-sharing structures. Daytime PV production coincides with industrial load profiles, making solar PPAs more attractive than wind for certain sectors.

Declining LCOE of solar PV

Module prices fell by about 60% between 2022 and 2024, enabling Romanian projects to secure CfD strike prices near EUR 51/MWh—already under fossil-fuel benchmarks. Domestic manufacturing is emerging through a 1.5 GW-per-year plant, which is receiving EUR 32.92 million in PNRR aid.(3)TaiyangNews, “Government Backs 1.5 GW Solar Module Production…,” taiyangnews.info Lower capex, better module efficiency, and cheaper debt combine to keep the Romania solar energy market on a steep growth path despite maturing incentives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy grid-connection permitting | −2.4% | National, rural peripheries | Short term (≤ 2 years) |

| Competition from on-shore wind repowering | −1.8% | Coastal and mountain zones | Medium term (2-4 years) |

| Farmland-protection zoning limits sites | −1.6% | High-value agricultural land | Long term (≥ 4 years) |

| Rising domestic interest rates post-2023 | −1.1% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy grid-connection permitting

Transelectrica’s application backlog tops 31.74 GW, stretching approval times beyond 12 months and inflating carrying costs. Planned auction-based capacity allocation from 2026 may prioritize shovel-ready assets, yet network reinforcements remain critical, especially in solar-rich south-east counties.(4)Profit.ro, “Panouri solare flotante…,” profit.roDelays compress developers’ CfD windows and raise execution risk.

Competition from on-shore wind repowering

Recent CfD auctions saw wind bids at EUR 65/MWh compared to solar’s EUR 51/MWh, supporting 1.1 GW of repowering versus 432 MW of new PV. Established wind farms have existing grid ties and faster permitting, prompting developers to chase repower premiums that may outcompete greenfield solar on prime sites. Solar operators answer with hybrid PV-storage concepts that raise capacity factors and grid-service revenues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Dominates Through Cost Leadership

Solar PV accounted for the entire Romania solar energy market share in 2025, underscoring the absence of CSP due to modest direct normal irradiance and higher capital intensity. The Romania solar energy market size for PV is projected to grow at a 14.52% CAGR to 2031, propelled by rooftop incentives and utility-scale CfDs. Local module plants with a total annual output of 1.779 GW are eligible for Net-Zero Industry Act procurement bonuses, thereby improving domestic content competitiveness.

Romanian solar energy market developers are increasingly integrating battery storage and tracker systems to enhance capacity factors and secure grid-service revenue. Manufacturing localization lowers logistics costs and de-risks supply chains amid global trade tensions. CSP remains sidelined due to uneconomical LCOE relative to PV plus storage.

By Grid Type: Off-Grid Surge Driven by Rural Electrification

On-grid plants represented 95.10% of the 2025 capacity, a share expected to remain above 90% through 2031, as CfD auctions favor utility-connected projects. The Romania solar energy market size for on-grid systems benefits from €56.2 million earmarked for transmission upgrades. Distributed automation and smart meters help networks absorb rising daytime injections, lowering curtailment.

Off-grid capacity, although modest, is projected to grow at a 20.80% CAGR through 2031, driven by agrivoltaics and rural microgrid pilots. Emergency Ordinance 134/2024 removed double taxation on batteries, enabling solar-plus-storage packages that replace diesel gensets for farms and telecom towers. These solutions unlock energy access and cost savings where grid extensions are uneconomic.

By End-User: Residential Segment Accelerates Through Prosumer Growth

Utility-scale parks held 57.10% of the Romania solar energy market share in 2025, favored by CfDs and economies of scale. Projects such as the 155 MW Rătești plant illustrate improvements in bankability due to a predictable offtake. The segment retains volume leadership, though its growth rate moderates as the base expands.

Residential systems post the fastest 18.55% CAGR to 2031, catalyzed by financing aimed at homeowner associations that mandates ≥10 kWp PV plus storage sized at ≥50% of array capacity. Net-metering and simplified 400 kW licensing also spur commercial rooftops. Corporate PPAs provide support for behind-the-meter C&I arrays that reduce grid charges and carbon liabilities.

Geography Analysis

Southern counties, such as Constanța, Călărași, and Giurgiu, host the bulk of utility-scale pipelines due to their 1,900-2,400 annual sunshine hours and flat topography, which eases construction. Projects pair PV with wind and storage to optimize grid usage. Western industrial clusters favor on-site C&I arrays that align generation with daytime loads, trimming power bills and Scope 2 emissions.

Bucharest’s metropolitan area leads rooftop deployment. Higher retail tariffs and municipal incentives accelerate the uptake of prosumer systems in apartment blocks, while abundant installation capacity shortens project cycles. Smart-meter penetration supports granular billing and flexible tariffs.

Northern and mountainous zones utilize distributed PV to supplement hydroelectric and biomass energy sources. Agrivoltaic pilots in high-value horticultural regions protect revenue diversity amid climate risks, ensuring that solar deployment extends beyond resource-rich south-east corridors.

Competitive Landscape

Romania’s solar arena is moderately concentrated, with Photon Energy Group and Enel Green Power Romania anchoring the top tier, while Nofar Energy, Econergy, and NextE Renewable are expanding aggressively. International developers form local joint ventures to navigate the permitting and community engagement processes. Strategies differentiate through vertical integration, corporate PPA portfolios, and storage co-location.

Domestic manufacturing entrants, such as SC Heliomit SRL and KBK Kraft Projekt, strengthen supply security and qualify for EU content bonuses, creating a cost advantage. Lenders such as the EIB and EBRD channel green loans to developers that meet ESG standards, thereby lowering the weighted average cost of capital relative to purely commercial debt.

Value-added services, such as digital O&M, grid-support inverters, and energy-as-a-service offerings, serve as market differentiators. Players that bundle these capabilities with bankable pipelines position themselves to capture long-run share as Romania's solar energy market additions scale beyond 1 GW per year.

Romania Solar Energy Industry Leaders

Sunshine Solar Energy SRL

Danagroup.hu

Amerisolar AP

Enel Green Power SpA

Photon Energy Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: OMV Petrom completed the acquisition of a 710 MW solar portfolio from Jantzen Energy for an undisclosed amount, expanding renewable capacity to support petrochemical operations and corporate sustainability targets across Romania.

- November 2024: Huadian Romania acquired the 134 MW Studina solar project from a local developer, marking the Chinese state-owned enterprise's entry into the Romanian renewable market with plans for an additional 300 MW by 2026.

- October 2024: The Monsson Group secured EUR 45 million in financing from the EBRD for a 216 MWh battery storage expansion, creating Romania's largest utility-scale energy storage facility integrated with solar generation.

- September 2024: PPC Renewables initiated the construction of a 727 MW solar project in Dolj County, representing Romania's largest single-site solar installation with a total investment of EUR 400 million.

- August 2024: Restart Energy announced a 500 MW solar development pipeline across 5 counties, supported by a EUR 300 million financing package from international investors and development banks.

Romania Solar Energy Market Report Scope

Solar energy is one of the renewable energies. It is made by converting the energy that is already in the sun. Once the sunlight passes through the earth's atmosphere, most of it is in the form of visible light and infrared radiation. Solar cell panels are used to convert this energy into electricity.

The Romanian solar energy market is segmented by end-user. By end-user, the market is segmented into residential, commercial & industrial , and utility-scale users. For each segment, market sizing and forecasts have been done based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is Romania’s installed solar capacity in 2026?

The Romania solar energy market size reached 7.78 GW in 2026.

What is the projected capacity for 2031?

Installed capacity is forecast to rise to 15.31 GW by 2031.

What growth rate is expected between 2026 and 2031?

Capacity is set to expand at a 14.52% CAGR over the forecast period.

Which segment is growing the fastest?

Residential installations are advancing at an 18.55% CAGR through 2031.

How dominant is solar PV technology?

Solar PV accounts for 100.00% of capacity, with no commercial CSP presence.

What policy supports rooftop adoption?

Net-metering, simplified 400 kW licensing, and financing for ≥10 kWp systems with storage spur residential uptake.

Page last updated on: