Robotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 88.27 Billion |

| Market Size (2031) | USD 218.56 Billion |

| Growth Rate (2026 - 2031) | 19.86% CAGR |

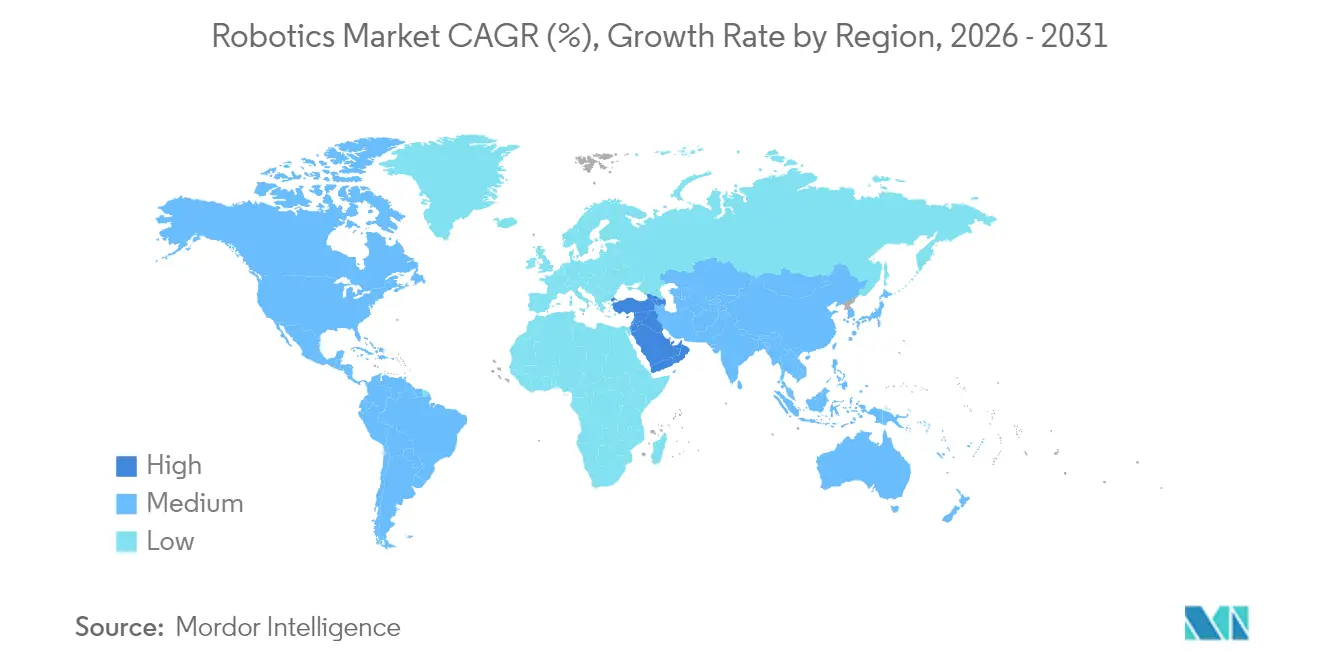

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

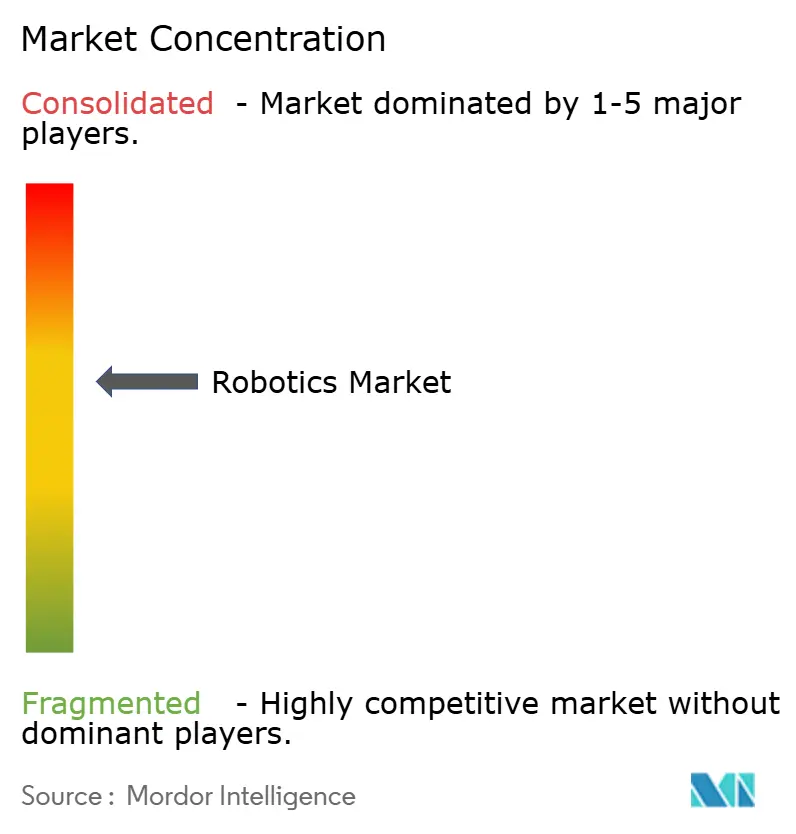

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotics Market Analysis by Mordor Intelligence

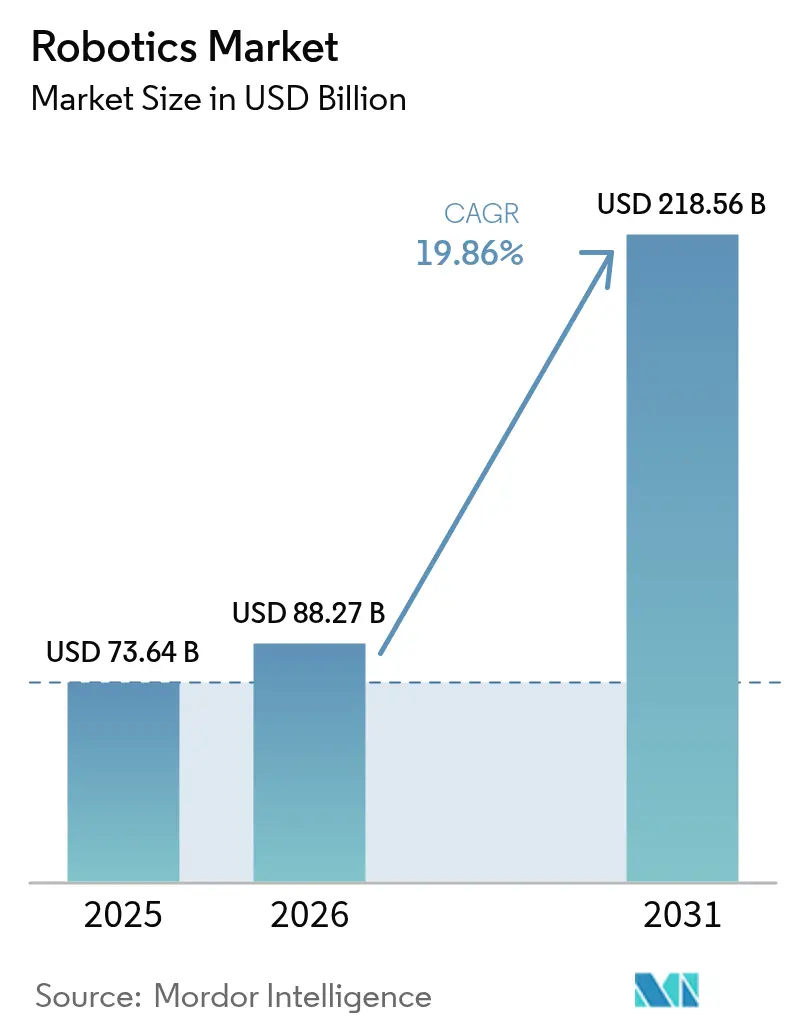

Robotics market size in 2026 is estimated at USD 88.27 billion, growing from 2025 value of USD 73.64 billion with 2031 projections showing USD 218.56 billion, growing at 19.86% CAGR over 2026-2031. This growth trajectory reflects structural labor shortages in advanced economies, systematic cost deflation in automation hardware, and government-backed reshoring programs that treat robots as strategic infrastructure rather than optional capital goods. Large enterprises accelerate adoption to stabilise production amid wage pressure, while small and medium firms now gain access through collaborative systems and Robot-as-a-Service contracts. Regional momentum is shifting: Asia-Pacific retains volume leadership, but the Middle East shows the quickest pace as sovereign funds pursue technology-driven diversification. On the supply side, declining component costs and low-code programming platforms reshape the value chain toward software intelligence, setting up recurring revenue streams for vendors that master artificial-intelligence-based control. Cyber-security weaknesses, export-control friction, and skill gaps among smaller users remain braking forces, yet they also open specialist service niches, especially around secure deployment and lifecycle support.

Key Report Takeaways

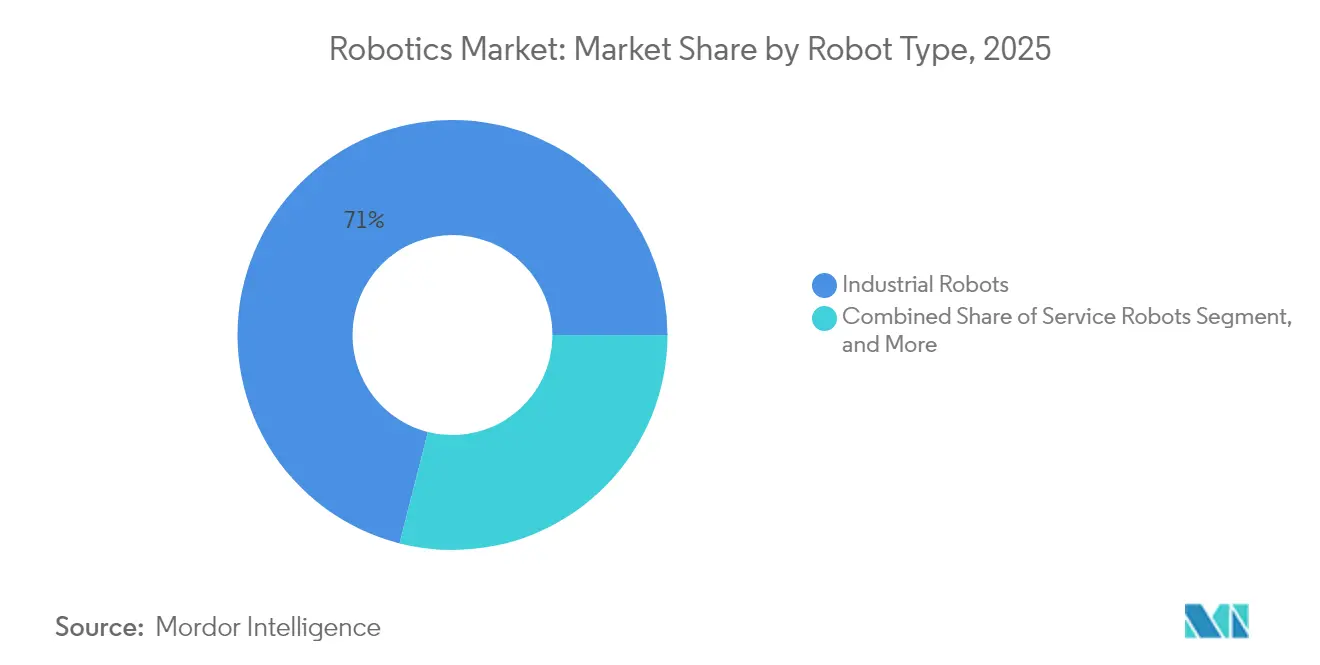

- By robot type, industrial robots led with 71.04% revenue share in 2025; collaborative robots are projected to post a 25.64% CAGR to 2031.

- By component, hardware captured 63.12% of the global robotics market share in 2025, while software is expected to rise at a 22.91% CAGR through 2031.

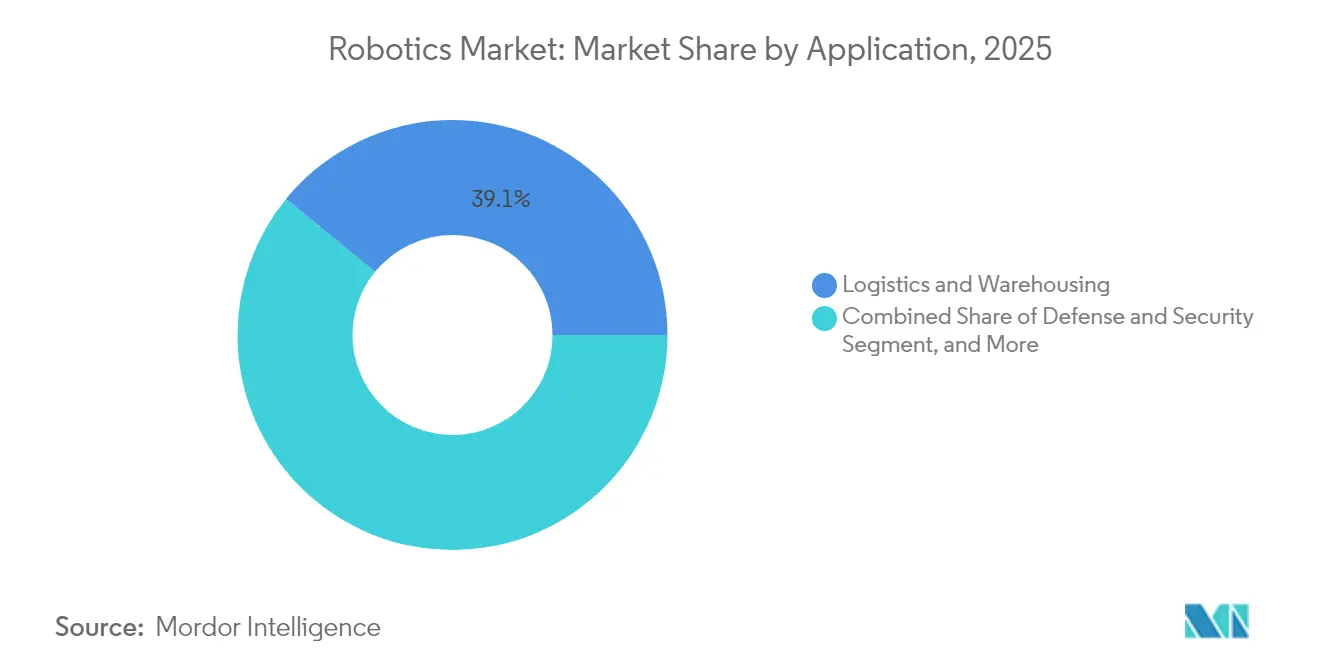

- By application, logistics and warehousing accounted for 39.10% share of the global robotics market size in 2025; medical and surgical robots are advancing at a 21.52% CAGR to 2031.

- By end-user industry, automotive held 28.78% share in 2025, whereas healthcare providers are forecast to expand at a 21.55% CAGR up to 2031.

- By geography, Asia-Pacific commanded 37.72% of the global robotics market share in 2025, while the Middle East registers the fastest expansion at a 21.31% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labour-shortage led automation demand | +4.2% | Global, with acute impact in North America, Europe, Japan | Medium term (2-4 years) |

| Declining average robot price per functional hour | +3.8% | Global, particularly emerging markets in APAC and MEA | Short term (≤ 2 years) |

| Proliferation of low-code robot-programming platforms | +2.9% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Fiscal incentives for reshoring manufacturing in G-7 | +3.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Warehouse AMR roll-outs by e-commerce 3PLs | +3.7% | Global, concentrated in major e-commerce markets | Short term (≤ 2 years) |

| Nation-level humanoid R&D missions | +2.5% | China, Japan, South Korea, with spillover to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Labour-Shortage Led Automation Demand

Demographic headwinds in Japan, the United States, and much of Western Europe have shifted automation from cost-saving to capacity-assurance mode. Unfilled factory vacancies topped 2 million roles across G-7 manufacturing in 2024, while Japan’s robot density reached 399 units per 10,000 employees, the highest on record.[1]Asian Robotics Review, “Why So Little Robot Automation in America?,” asianroboticsreview.com Automakers such as Stellantis adopted human-centric robotic cells that trim repetitive strain injuries yet safeguard headcount, signalling a nuanced push toward collaborative deployment.[2]Wall Street Journal, “Robots Are Looking Better to Detroit as Labor Costs Rise,” wsj.com The global robotics market benefits because these structural gaps persist through economic cycles, giving vendors a predictable demand base that decouples from GDP volatility.

Declining Average Robot Price Per Functional Hour

Component commoditisation and scale production cut collaborative robot prices by roughly 15% a year post-2024, while software upgrades doubled performance relative to price.[3]Machinery Market, “Cobot market exceeds USD 1 billion in 2023,” machinery-market.co.uk Chinese suppliers even marketed entry-level humanoids at CNY 199,000 (USD 27,512), placing robots within small-factory capital budgets. As hardware costs slide, adoption curves steepen among small and emerging-market manufacturers, thereby widening the addressable pool for the global robotics market.

Proliferation of Low-Code Robot-Programming Platforms

Low-code interfaces built on Robot Operating System 2 now let domain specialists configure tasks via drag-and-drop tools or speech, compressing deployment cycles from months to weeks and slicing integration bills by roughly 40%. French developer Inbolt logged 70% faster go-lives at SME clients that previously lacked in-house automation engineers. The shift reallocates complexity from plant floors to cloud platforms, raising the software revenue pie within the global robotics market.

Fiscal Incentives for Reshoring Manufacturing in G-7

The USA CHIPS Act funnels USD 52 billion toward domestic semiconductor fabs that embed advanced robotics by mandate, while the EU dedicates 20% of its recovery fund to digital automation. Japan’s Society 5.0 programme grants accelerated depreciation on collaborative systems, prompting a 25% investment jump among enrolled firms. These policy levers inject counter-cyclical demand, sheltering the global robotics market from private-sector slowdowns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent SME integration skill-gap | -2.8% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Geopolitical export-control on advanced servos | -2.1% | Global, with concentrated impact on China-US trade | Short term (≤ 2 years) |

| Rare-earth magnet price volatility | -1.9% | Global, affecting high-performance robotics | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in ROS deployments | -1.6% | Global, with higher impact in critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent SME Integration Skill-Gap

Sixty-eight percent of SMEs still lack engineering talent for robotics deployment, prolonging payback periods and dampening utilisation rates. Integrators cluster in urban hubs, leaving regional firms underserved. Without accelerated skills development or turnkey service models, the global robotics market leaves considerable latent demand untapped.

Geopolitical Export-Control on Advanced Servos

Tightened US chip rules and China’s rare-earth restrictions pushed servo prices up by 15-25% for some western buyers, prompting redesigns or dual-sourcing moves that slow roll-outs. The global robotics market absorbs higher input costs and buffers supply risk through localisation strategies, but near-term friction hampers smooth scaling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Collaborative Upswing Within Industrial Dominance

Industrial robots accounted for 71.04% of the global robotics market in 2025, riding sustained demand from high-throughput automotive and electronics assembly lines. Yet collaborative robots expand at a 25.64% CAGR to 2031, underpinned by safety-certified force-sensing and sub-USD 30,000 price tags that place them within SME budgets. This pivot signals that flexible, human-supervised cells, rather than fenced-off lines, will drive the next deployment wave of the global robotics market.

A surge in Chinese cobot makers lifted their domestic share from 35% to 73% between 2017 and 2024, heightening price competition and accelerating worldwide unit growth. Service-robot niches also flourish: surgical systems surpassed USD 4.18 billion in 2025, reaffirming healthcare as the fastest-rising end-use. This diversification reduces cyclicality for the global robotics market and cushions hardware vendors against single-sector downturns.

By Component: Hardware Leadership Shifts Toward Software Intelligence

Hardware still represented 63.12% of 2025 spending, but software revenue is set to grow 22.91% annually as artificial intelligence becomes the primary value driver. Higher-level control stacks now incorporate cloud analytics and reinforcement learning that deliver 25% faster cycle times with 20% lower electricity use on ABB’s OmniCore platform. The global robotics market size for subscription-based Robot-as-a-Service is projected to treble by 2031 as customers migrate from capital expenditure toward operating expenditure models.

Service revenues, covering integration, remote monitoring, and predictive maintenance, further solidify vendor lock-in. As a result, software and services blur, embedding update rights and cyber-security patches into multi-year contracts. This trend rewires profit pools and raises entry barriers for purely hardware-centric challengers within the global robotics market.

By Application: Logistics Leadership Meets Medical Momentum

E-commerce fulfilment hubs drove logistics and warehousing robots to 39.10% share in 2025, underpinned by autonomous mobile platforms that can be installed without layout overhauls. Meanwhile, medical and surgical systems record 21.52% CAGR thanks to evidence of shorter hospital stays and higher procedural precision compared with laparoscopic methods. The global robotics market size for surgical platforms is on track to hit USD 8.11 billion by 2031, indicating robust health-sector appetite.

Defence programmes, such as DARPA’s RACER Heavy autonomous vehicle, underscore rising demand for off-road and maritime unmanned systems, diversifying application risk. Cleaning and sanitation robots post 30% sales growth as hospitality chains standardise hygiene protocols. This breadth of use cases reinforces long-term momentum for the global robotics market.

By End-User Industry: Automotive Plateau vs Healthcare Surge

Automotive retained 28.78% share in 2025, yet its growth curve flattens as most paint, welding, and assembly lines already employ mature automation. In contrast, hospitals and outpatient centres, propelled by regulatory approvals and demographic necessity, exhibit 21.55% CAGR, positioning healthcare as the new frontier for global robotics market revenue.

Electronics and semiconductor players maintain steady robotics investments to preserve precision and clean-room compliance. Government grants worth JPY 5.15 billion (USD 46 million) to Fab projects in Japan further stimulate uptake. Food and beverage enterprises apply guided changeover modules that cut downtime by 70% and save USD 9,000 per month. This cross-sector mix diversifies cash flows for solution vendors inside the global robotics market.

Geography Analysis

Asia-Pacific secured 37.72% of global robotics market share in 2025, anchored by China’s 430,000 annual industrial-robot installations and two-thirds of worldwide robotics patent grants. Chinese factories integrate robots into lithium-ion battery and consumer-electronics lines, while domestic brands escalate exports, embedding regional cost competitiveness into the global robotics market. Japan posted JPY 180.2 billion (USD 1.64 billion) profit at Fanuc in 2024 on revived Chinese demand and domestic demographic pressure. South Korea’s USD 2.6 billion public-private programme channels humanoid expertise toward battery-plant automation, underscoring strategic prioritisation.

The Middle East registers the highest 21.31% CAGR to 2031 as sovereign wealth vehicles divert hydrocarbons surplus into industrial digitalisation, logistics, and healthcare robotics. Free-trade zones in the United Arab Emirates trial warehouse AMRs to service regional e-commerce flows, reducing over-reliance on seasonal migrant labour. National programmes additionally fund advanced manufacturing hubs that attract global integrators, amplifying the addressable base for the global robotics market.

North American demand remains resilient, propelled by CHIPS-Act-backed fabs and defence contracts such as the USD 642.2 million Navy counter-drone award to Anduril. Europe focuses on safe human–robot collaboration standards and sustainability targets, helped by EUR 69 million (USD 75 million) in annual German funding for artificial-intelligence integration. Both regions increasingly outsource commodity sub-assemblies to Asia while investing in high-value software and integration, reflecting a barbell strategy within the global robotics market.

Mordor Intelligence provides coverage of the robotics market across other key regional markets. Detailed country-level analysis extends to Indonesia incorporating local coverage and market participation, as required.

Competitive Landscape

The global robotics market remains moderately fragmented, with top players dominating specific niches yet facing vigorous challenge from focused entrants. Japanese and European incumbents such as Fanuc, ABB, and KUKA continue to control high-payload industrial segments via proprietary servo technology and worldwide service reach. Chinese vendors, aided by scale and state backing, undercut hardware prices and now hold 73% of the domestic cobot market, accelerating export ambitions.

Strategically, leading firms pursue vertical integration and software stacking to defend margins. ABB intends to spin off its robotics division, estimated at USD 2.3 billion 2024 revenue, to unlock balance-sheet flexibility for aggressive acquisition of AI software assets. Fanuc boosts cloud analytics through partnerships to broaden recurring revenue. Meanwhile, service-robot disruptors such as Locus Robotics leverage Robot-as-a-Service contracts to lower customer entry barriers and capture long-run annuity streams, eroding incumbents’ traditional product-sale foothold.

Specialists exploit white-space in medical, defence, and sanitation robots where domain complexity and regulatory burden create protective moats. Intuitive Surgical deepens hospital stickiness through procedural analytics, while Anduril secures multi-year defence contracts that require sovereign-grade cyber-security. Cyber-risk mitigation services and integration consultancies thus emerge as high-margin adjuncts, adding layers of competitiveness to the global robotics market.

Robotics Industry Leaders

Yaskawa Electric Corporation

Denso Corporation

Fanuc Corporation

ABB Ltd.

KUKA AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ABB unveiled a plan to list its Robotics division by Q2 2026, aiming to separate high-growth automation assets and sharpen strategic clarity for investors.

- May 2025: DARPA’s RACER programme moved into Phase 2 with 12-ton off-road platforms, demonstrating state support for ruggedised autonomous systems with potential dual-use applications.

- April 2025: RLWRLD raised USD 14.8 million, while Standard Bots secured USD 63 million to accelerate AI-native control stacks, underscoring venture capital appetite for software-first robotics players.

- March 2025: Anduril won a 10-year, USD 642.2 million Navy deal for counter-drone solutions, reinforcing defence robotics as a stable demand vertical.

Global Robotics Market Report Scope

The robotics market study defines the revenues generated from the types of industrial and service robotics used in various end-user industries across the world. The study includes qualitative coverage of the most adopted strategies and an analysis of the critical base indicators in emerging markets. Industrial robots covered under the scope include linear robots (cartesian and gantry robots), SCARA robots, articulated robots, parallel robots (delta), cylindrical robots, etc. For the service robots market estimates, the types of service robots considered under the scope of the study include professional (professional, personal/domestic, and entertainment, among others.

The robotics market is segmented by technology type (industrial and service), by end user (end users of industrial robots[(automotive, food & beverage, electronics, and other end users of industrial robots] and by end users of service robots [logistics, military & defense, medical and healthcare, and other end users of service robots)], and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Industrial Robots |

| Service Robots |

| Collaborative (Cobots) |

| Mobile/AMR |

| Hardware |

| Software |

| Services (Integration, RaaS) |

| Manufacturing and Assembly |

| Logistics and Warehousing |

| Medical and Surgical |

| Defense and Security |

| Inspection and Maintenance |

| Cleaning and Sanitation |

| Automotive |

| Electronics and Semiconductor |

| Food and Beverage |

| Healthcare Providers |

| Military and Defense |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Robot Type | Industrial Robots | |

| Service Robots | ||

| Collaborative (Cobots) | ||

| Mobile/AMR | ||

| By Component | Hardware | |

| Software | ||

| Services (Integration, RaaS) | ||

| By Application | Manufacturing and Assembly | |

| Logistics and Warehousing | ||

| Medical and Surgical | ||

| Defense and Security | ||

| Inspection and Maintenance | ||

| Cleaning and Sanitation | ||

| By End-User Industry | Automotive | |

| Electronics and Semiconductor | ||

| Food and Beverage | ||

| Healthcare Providers | ||

| Military and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the global robotics market?

The global robotics market stands at USD 88.27 billion in 2026 and is projected to reach USD 218.56 billion by 2031 at a 19.86% CAGR.

Which segment is growing the fastest in the global robotics market?

Collaborative robots show the highest growth, expanding at a 25.64% CAGR through 2031 as safety features, low costs, and ease of programming attract SMEs.

Which region will record the quickest expansion?

The Middle East leads regional growth at a 21.31% CAGR on the back of sovereign-fund automation investments and logistics-hub developments.

Why is software becoming more important than hardware?

Artificial-intelligence control, cloud connectivity, and Robot-as-a-Service contracts deliver performance and continuous updates, shifting value capture to software and recurring services.

What are the biggest barriers for small manufacturers?

Skill shortages in integration and programming, alongside cybersecurity risk and component-supply friction, slow adoption among SMEs despite lower hardware prices.

How fragmented is the vendor landscape?

Top five manufacturers hold around 55% of revenue, indicating moderate concentration; niche entrants thrive in healthcare, defence, and service-robot applications.

Page last updated on: