Autonomous Mobile Robot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

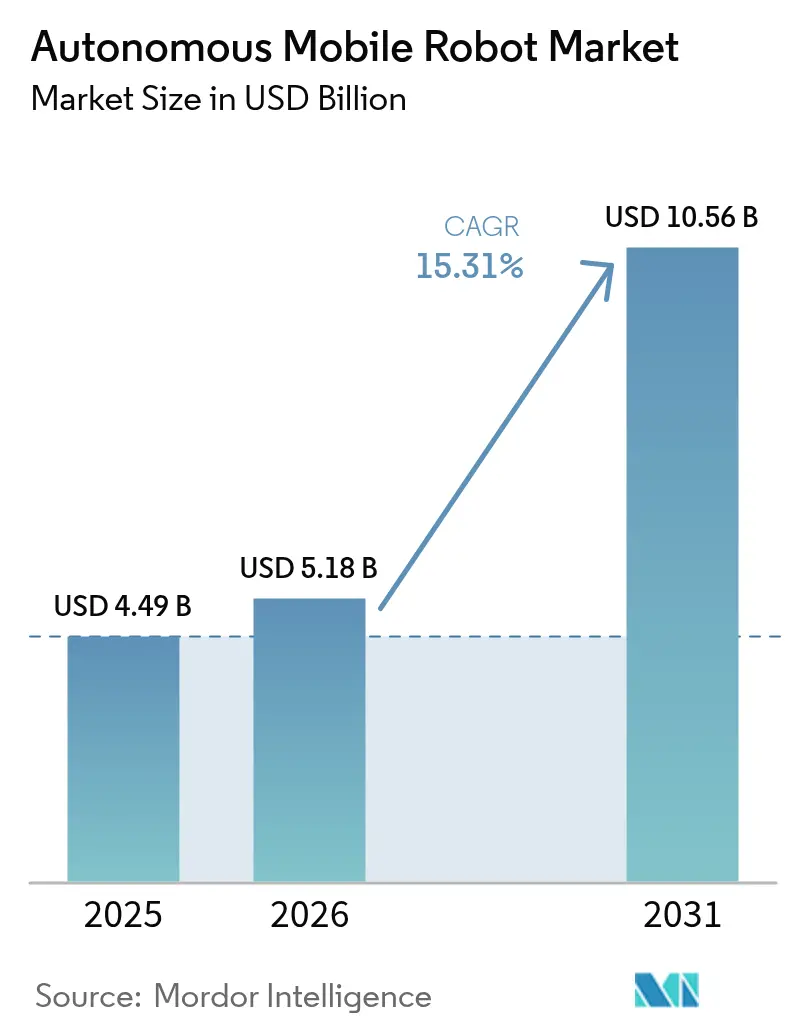

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 10.56 Billion |

| Growth Rate (2026 - 2031) | 15.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

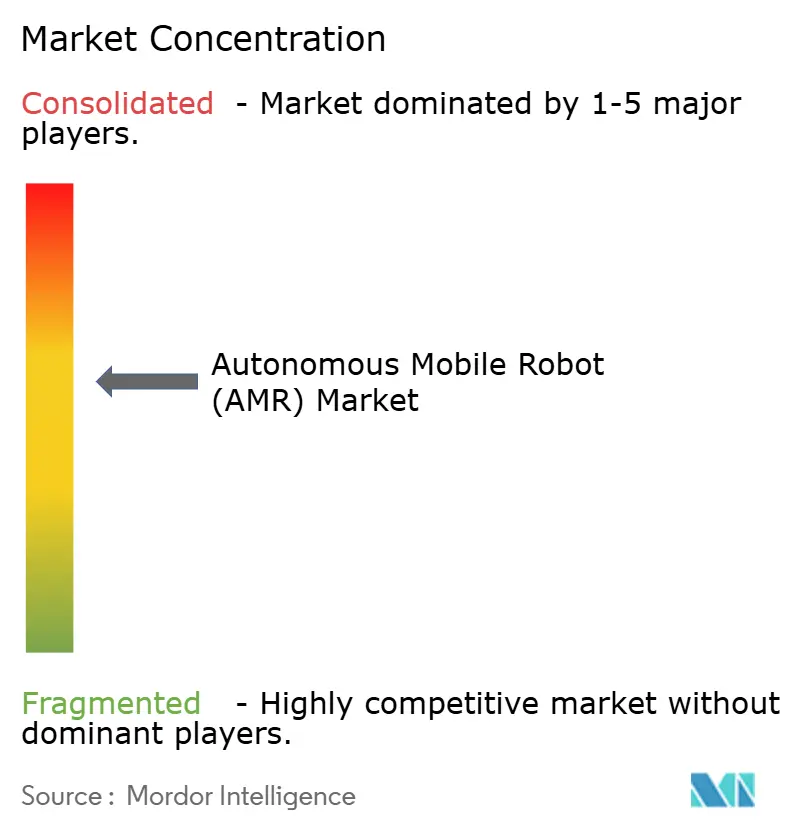

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Mobile Robot Market Analysis by Mordor Intelligence

Autonomous Mobile Robot Market size in 2026 is estimated at USD 5.18 billion, growing from 2025 value of USD 4.49 billion with 2031 projections showing USD 10.56 billion, growing at 15.31% CAGR over 2026-2031.

Fast adoption of artificial intelligence, 5G-Advanced connectivity and lower-cost lithium-ion batteries together accelerate commercial feasibility across fulfilment, manufacturing and healthcare environments. Operators deploy robots to offset persistent labour shortages, to gain 24/7 throughput without building fixed conveyor infrastructure and to improve workplace safety. Asia-Pacific leads adoption thanks to Chinese suppliers that blend software-centric design and aggressive pricing, while Middle East mega-projects generate fresh demand for heavy-duty systems. Competitive intensity rises as vendors race to embed fleet-level orchestration software and to secure channel partnerships that shorten time-to-value. Regulatory incentives, such as EU “Factory of the Future” grants, further stimulate uptake by subsidizing capital outlays for small and mid-sized enterprises.

Key Report Takeaways

- By type, unmanned ground vehicles held 45.42% of autonomous mobile robot market share in 2025, while humanoids are projected to grow at 18.74% CAGR to 2031.

- By navigation technology, LiDAR SLAM commanded 40.88% revenue share in 2025; vision-based systems are set to expand at 20.64% CAGR through 2031.

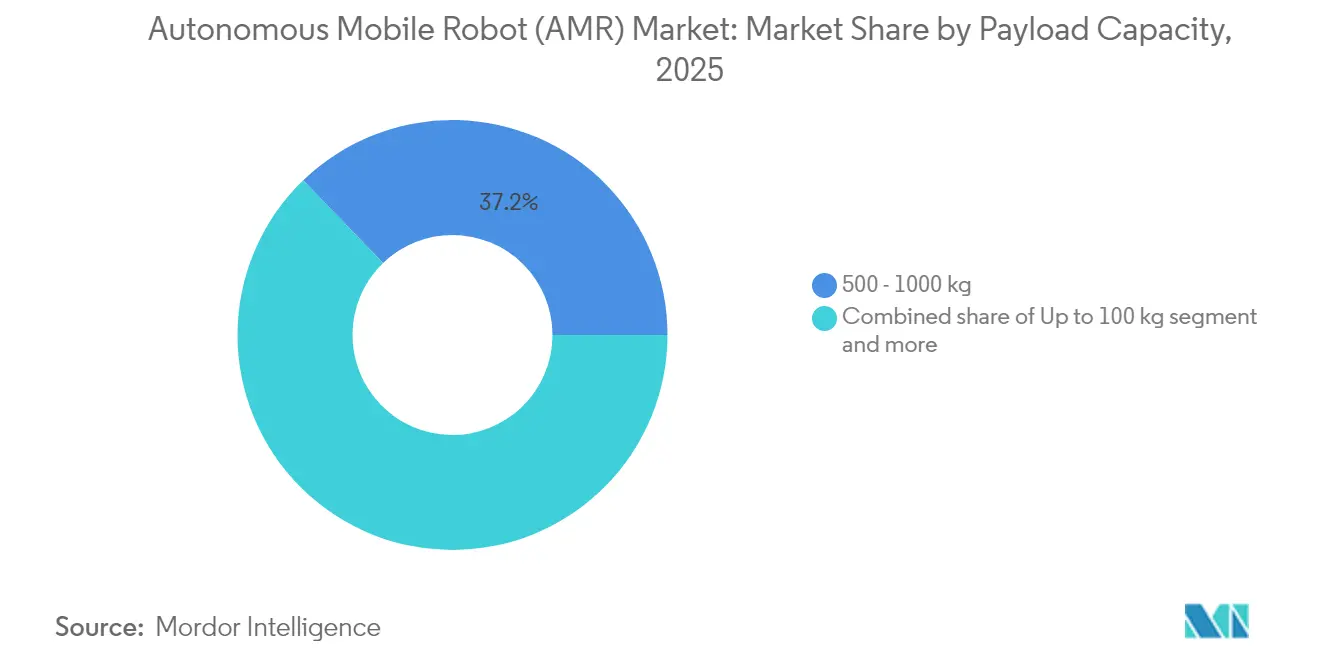

- By payload capacity, the 100–500 kg class captured 37.22% share of the market size in 2025, whereas robots above 1,000 kg will advance at 18.21% CAGR over the outlook period.

- By end-user industry, warehouse and logistics accounted for 32.94% of the autonomous mobile robot market size in 2025; healthcare is forecast to post the fastest 19.04% CAGR to 2031.

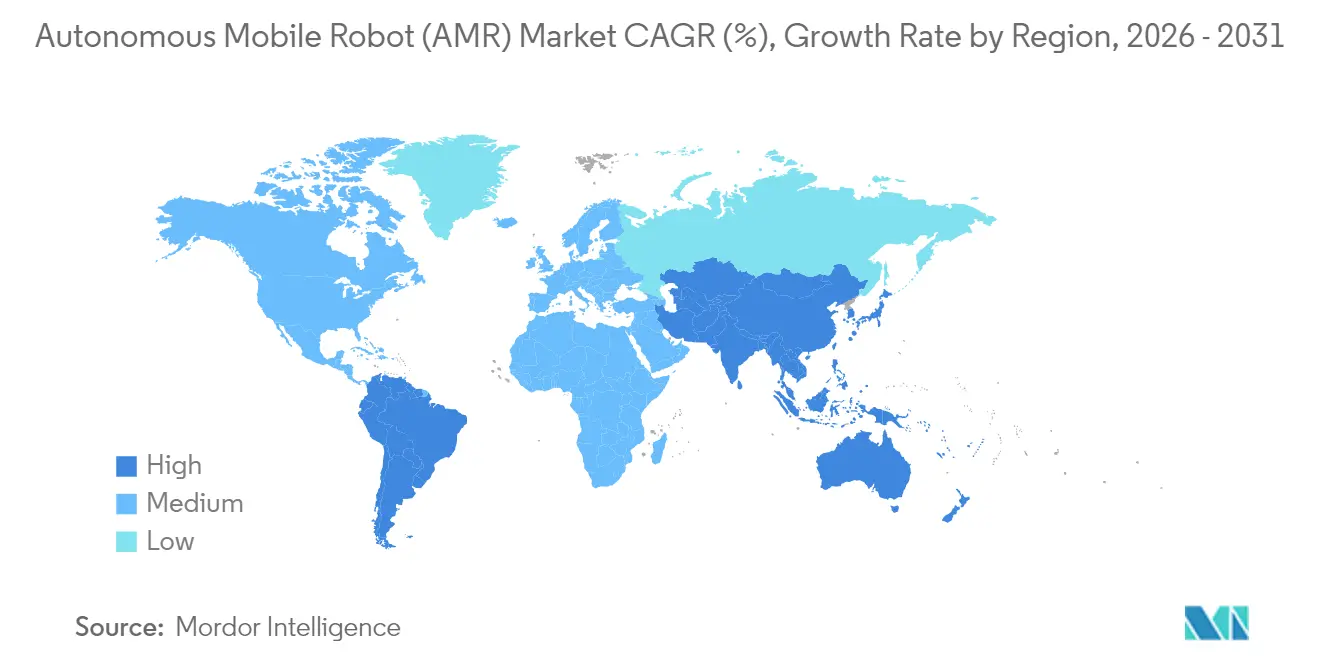

- By geography, Asia-Pacific dominated with a 37.12% revenue share in 2025, while the Middle East and Africa region is poised for a 18.46% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autonomous Mobile Robot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-commerce fulfilment demand | 3.20% | Global, with concentration in North America & APAC | Short term (≤ 2 years) |

| Scarcity of warehouse labor in OECD markets | 2.80% | North America & EU primarily, spillover to APAC | Medium term (2-4 years) |

| Falling Li-ion battery $/kWh below USD 70 | 2.10% | Global | Medium term (2-4 years) |

| Post-2025 EU "Factory of the Future" grants | 1.40% | Europe, with technology transfer to other regions | Long term (≥ 4 years) |

| 5G-Advanced private network roll-outs | 1.80% | APAC core, spillover to North America & EU | Long term (≥ 4 years) |

| AI-enabled "swarm orchestration" platforms | 2.30% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid e-commerce fulfilment demand

Online retail now hinges on same-day delivery expectations. Amazon surpassed 1 million deployed robots by July 2025 and cut travel time per pick by 10% through DeepFleet fleet intelligence, proving that mobile automation can quadruple throughput using the same headcount. Locus Robotics crossed 3 billion picks after integrating its LocusOne software, which doubled to tripled productivity while reducing injuries by 80%. Retailers are therefore adopting compact autonomous mobile robot market solutions that flex with seasonal volumes and require minimal facility changes. Vision-only navigation, showcased in the Geek+-Intel design, trims installation cost and time because no fixed markers are needed. [1]Amazon, “DeepFleet AI Cuts Travel Time,” aboutamazon.com

Scarcity of warehouse labour in OECD markets

OECD operators report persistent vacancies for night and peak-season shifts. The European Agency for Safety and Health at Work highlights automation as essential for offsetting shrinking working-age populations. Skechers logged 80% energy savings after replacing conveyors with robots, validating the return on investment where skilled labour is scarce. Employers now redesign rolls around robot supervision and maintenance, making warehouse jobs less physically demanding and more attractive.[2]European Agency for Safety and Health at Work, “Automation and Workforce Demographics,” osha.europa.eu

Falling Li-ion battery cost below USD 70/kWh

Battery pack prices crossing below USD 70/kWh enable opportunity charging strategies that keep fleets online around the clock. Automotive scale has pushed cell energy density higher, allowing heavy-payload robots to operate longer without adding chassis weight. Predictive battery management further reduces total cost of ownership by optimizing charge cycles.

AI-enabled swarm orchestration platforms

Fleet-level optimization boosts capacity beyond individual robot efficiency. Amazon’s DeepFleet algorithms cut redundant travel by crowd-sourcing route data from the entire fleet. A joint 5G-robotics testbed showed 15% energy savings when compute loads shifted to edge servers. Such orchestration is central as operators integrate multiple robot types in a single site.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented interoperability standards | -1.90% | Global, particularly affecting multi-vendor deployments | Medium term (2-4 years) |

| Cyber-physical security vulnerabilities | -1.50% | Global, with heightened concern in critical infrastructure | Short term (≤ 2 years) |

| High up-front capex for heavy-payload AMRs | -1.20% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Union push-back on robot density limits | -0.80% | Primarily North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented interoperability standards

ISO 3691-4 and ANSI/RIA R15.08 detail safety, yet they omit fleet communication protocols, forcing buyers into single-vendor ecosystems and inflating integration cost. Middleware suppliers attempt to bridge gaps, but proprietary data formats slow deployment and reduce bargaining power. [3]ANSI, “ISO 3691-4 and R15.08 Safety Standards,” ansi.org

Cyber-physical security vulnerabilities

Robots now link operational technology with enterprise IT, widening the attack surface. The European Union’s NIS2 directive raises compliance hurdles, and a breach could hijack fleets or leak sensitive inventory data. Manufacturers increasingly mandate encrypted command channels and zero-trust architectures before approving new market projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Humanoids Drive Next-Generation Versatility

Unmanned ground vehicles controlled 45.42% revenue in 2025. Humanoids, although young, are forecast to expand at 18.74% CAGR because they navigate human-designed spaces without layout changes. Amazon is piloting humanoid couriers that load parcels from Rivian electric vans, hinting at outdoor extension of the autonomous mobile robot market. Unmanned aerial and marine robots remain niche but critical for inspection in energy assets. The autonomous mobile robot market size for humanoids is likely to rise quickly once manipulation reliability reaches warehouse performance benchmarks.

Traditional fleets rely on specialized form factors that optimize one task but lack versatility. Humanoids promise fleet simplification because one platform can switch roles, from shelving to sorting. Investment has therefore shifted from pure mobility hardware to artificial intelligence vision and grasping capability that matches human dexterity. This transition will lower life-cycle cost and unlock new service models such as robot-as-a-service subscriptions.

By Navigation Technology: Vision Systems Challenge LiDAR Dominance

LiDAR SLAM held 40.88% share in 2025 because of millimetre-level repeatability in congested aisles. Vision-based systems, expanding at 20.64% CAGR, eliminate expensive sensors and reflective targets, which reduces capital outlay for mid-market operators. Geek+ demonstrated LiDAR-equivalent accuracy through Intel RealSense depth cameras and onboard AI. The autonomous mobile robot market size for vision navigation will further increase as edge processors handle real-time image segmentation at lower power budgets.

Hybrid sensor fusion combines cameras, LiDAR and inertial sensors so fleets can switch modes when dust, glare or bandwidth constraints appear. This adaptive approach supports mixed indoor-outdoor operations that warehouses at ports now demand. Standards that certify performance across modalities will accelerate multi-sensor adoption, ensuring safety as robots cross public walkways.

By Payload Capacity: Heavy-Duty Applications Accelerate Growth

Robots that move between 100 kg and 500 kg hold 37.22% of autonomous mobile robot market share in 2025 because this weight class is ideal for shuttling totes, cartons and light parts around busy warehouses. The very largest machines—those rated above 1,000 kg—are catching up fast with an 18.21% CAGR through 2031 as car makers and other heavy industries look for mobile platforms that can carry engines, frames and other bulky loads that fixed conveyors cannot handle. At the opposite end, sub-100 kg units carve out niches in hospitals and labs where gentle, contamination-free transport matters more than brute strength.

The mid-range 500–1,000 kg category bridges warehouse and factory work. These robots can lift full pallets yet still weave through narrow aisles, giving operators the best of both worlds. Recent gains in lithium-ion battery density let every class, and especially the heavy rigs, run longer shifts without adding excess weight. Looking ahead, engineers are designing modular decks that let the same base unit switch between payload brackets, a change that should make the autonomous mobile robot market size grow as buyers invest in one platform instead of several.

By End-user Industry: Healthcare Leads Growth Transformation

Warehouse and logistics users remain the backbone of demand with 32.94% of the autonomous mobile robot market size in 2025, driven by e-commerce peaks that require fast, flexible picking lines. Healthcare, however, is the breakout story: hospitals are adopting cleaning and medicine-delivery robots at a 19.04% CAGR to curb staff shortages and improve infection control. Manufacturers follow close behind as assembly lines rely on fleets for just-in-time parts runs, while automotive plants add specialized mobile robots that can adjust when model mixes change.

Food and beverage processors favor stainless-steel robots that meet hygiene codes; KUKA’s automated cheese line, which doubled capacity while holding food-safety standards, shows the payoff. Defense sites use robots for base logistics and patrols, and mining and energy operators send them into zones too risky for people. Even oil and gas facilities now deploy explosion-rated units that inspect remote wellheads where traditional automation would be costly and hard to maintain. This widening spread of use cases underlines how far the technology has matured since the early single-task days.

Geography Analysis

Asia-Pacific generated 37.12% of 2025 revenue. Chinese firms such as Geek+ export over one-third of production, leveraging cost advantages and government support programs that expedite piloting. Many Japanese and Korean factories now source robots from Chinese brands to cut payback periods. North America remains the second-largest autonomous mobile robot market owing to Amazon’s multi-site expansion and a deep ecosystem of software startups that tailor orchestration layers for third-party logistics providers.

Europe benefits from structured subsidies. The EU “Factory of the Future” initiative reimburses up to 20% of automation hardware capital expenditure, which accelerates adoption among mid-sized manufacturers. The autonomous mobile robot market share for Europe will rise as grants kick in post-2025. The Middle East and Africa is the fastest-growing region at a 18.46% CAGR, driven by Saudi Arabia’s Vision 2030 and NEOM’s USD 774.6 million commitment to construction robotics. High logistics spend and greenfield warehouses allow operators to design around robots from day one.

South America remains early stage. Duty exemptions on imported automation in Brazil and Mexico encourage pilots, yet currency volatility slows wide rollout. Africa’s uptake concentrates in South Africa and Morocco where automotive assembly plants demand just-in-time delivery to lineside.

Competitive Landscape

Competition is moderately fragmented. Amazon’s fleet of more than 1 million robots gives it scale benefits and proprietary data that trains DeepFleet traffic models. Teradyne integrates Mobile Industrial Robots with Universal Robots and AI vision to offer turnkey cells. Traditional automation giants such as ABB now bundle mobile platforms with collaborative arms for a complete order-to-pack solution.

Software is the new battleground. Locus Robotics, valued near USD 2 billion after its Series F round, licenses LocusOne to brands that prefer a hardware-agnostic route. Geek+ focuses on vision-only navigation to underprice LiDAR rivals by up to 20% while maintaining safety compliance. Siemens partners with Teradyne to showcase edge orchestration at its Chicago MxD center, signalling a move toward open ecosystems.

Start-ups carve niches in healthcare, mining and heavy payloads. However, consolidation pressure rises because global customers prefer vendors that can certify cybersecurity, provide 24/7 support and finance robot-as-a-service contracts. Expect more mergers as incumbents acquire AI route-planning or battery analytics specialists.

Autonomous Mobile Robot Industry Leaders

Zebra Technologies Corporation (Fetch Robotics)

Geek+ Technology Co., Ltd.

Teradyne Inc. – Mobile Industrial Robots A/S

Seegrid Corporation

Vecna Robotics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Teradyne and Siemens opened an automation showcase at the MxD center in Chicago.

- March 2025: Locus Robotics raised USD 117 million in Series F funding to extend global deployments.

- February 2025: Teradyne posted USD 98 million robotics revenue in Q4 2024 and projected 2025 acceleration.

- January 2025: Zebra Technologies completed the acquisition of Photoneo from the Photoneo Brightpick Group.

Global Autonomous Mobile Robot Market Report Scope

Autonomous robots are intelligent machines that can do real-world tasks without human intervention. Autonomous mobile robots (AMRs) can comprehend and navigate their surroundings without direct human supervision. An autonomous mobile robot navigates utilizing maps generated on-site by its software or facility designs that have been pre-loaded. An autonomous mobile robot uses technology, such as LiDAR sensors and simultaneous localization and mapping (SLAM), to determine the best path between waypoints.

The autonomous mobile robots market is segmented by type (unmanned ground vehicles, humanoids, unmanned aerial vehicles, and unmanned marine vehicles), end-user industry (defense and security, warehouse and logistics, energy and power, automotive, manufacturing, oil and gas, mining and minerals, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Unmanned Ground Vehicles (UGV) |

| Humanoids |

| Unmanned Aerial Vehicles (UAV) |

| Unmanned Marine Vehicles (UMV) |

| LiDAR SLAM |

| Vision-based (2D/3D camera) |

| Magnetic / Inductive / QR Guided |

| Hybrid & Multi-Sensor Fusion |

| Up to 100 kg |

| 100 - 500 kg |

| 500 - 1,000 kg |

| Above 1,000 kg |

| Warehouse and Logistics |

| Manufacturing |

| Automotive |

| Food and Beverage |

| Healthcare |

| Retail and E-commerce |

| Defense and Security |

| Mining and Minerals |

| Energy and Power |

| Oil and Gas |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Unmanned Ground Vehicles (UGV) | |

| Humanoids | ||

| Unmanned Aerial Vehicles (UAV) | ||

| Unmanned Marine Vehicles (UMV) | ||

| By Navigation Technology | LiDAR SLAM | |

| Vision-based (2D/3D camera) | ||

| Magnetic / Inductive / QR Guided | ||

| Hybrid & Multi-Sensor Fusion | ||

| By Payload Capacity | Up to 100 kg | |

| 100 - 500 kg | ||

| 500 - 1,000 kg | ||

| Above 1,000 kg | ||

| By End-user Industry | Warehouse and Logistics | |

| Manufacturing | ||

| Automotive | ||

| Food and Beverage | ||

| Healthcare | ||

| Retail and E-commerce | ||

| Defense and Security | ||

| Mining and Minerals | ||

| Energy and Power | ||

| Oil and Gas | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the autonomous mobile robot market through 2031?

The market is projected to expand from USD 5.18 billion in 2026 to USD 10.56 billion in 2031, registering a 15.31% CAGR.

Which region leads autonomous mobile robot adoption today?

Asia-Pacific holds 37.12% of 2025 revenue, driven by Chinese manufacturers that combine software differentiation with lower cost structures.

What segment shows the fastest growth by robot type?

Humanoid robots lead with a forecast 18.74% CAGR because they work in human-oriented spaces without infrastructure changes.

Why are vision-based navigation systems gaining share?

They remove pricey LiDAR and reflective targets, cutting commissioning time and capital cost while maintaining navigational accuracy.

How do AI fleet orchestration platforms improve performance?

Fleet-level algorithms optimize traffic flow and task allocation, reducing travel time by up to 10% and boosting overall throughput.

Page last updated on: