Ring Main Unit (RMU) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.08 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

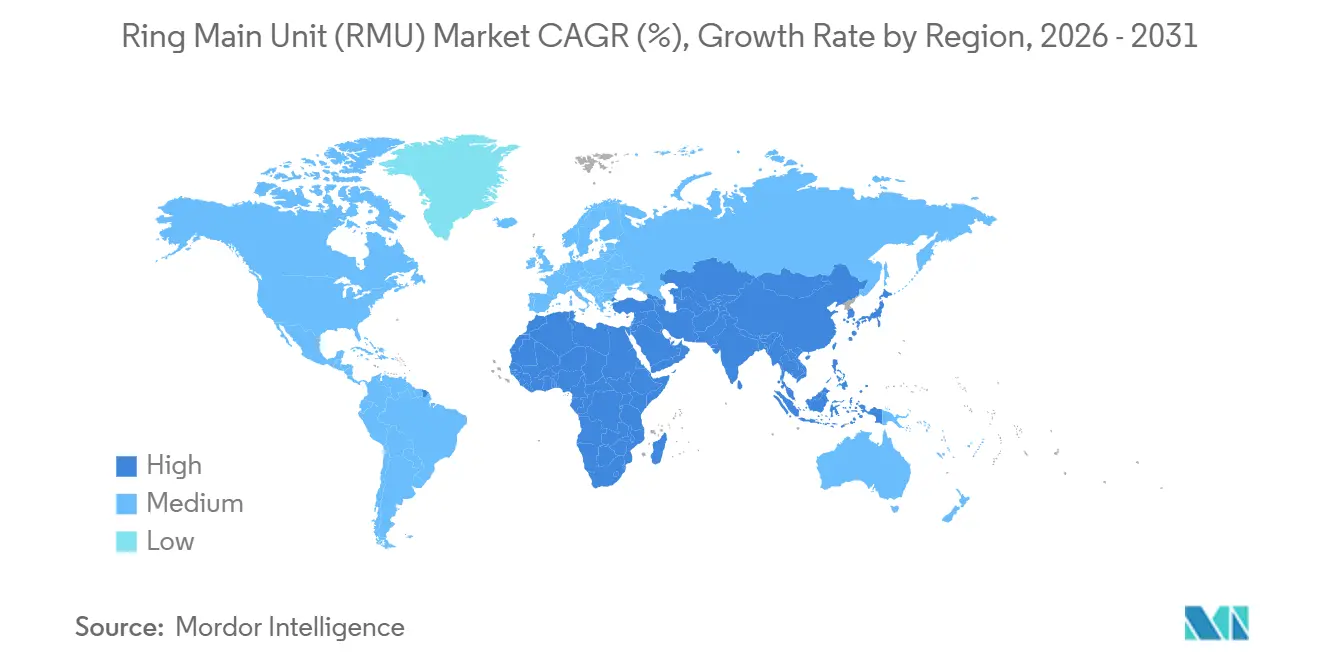

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

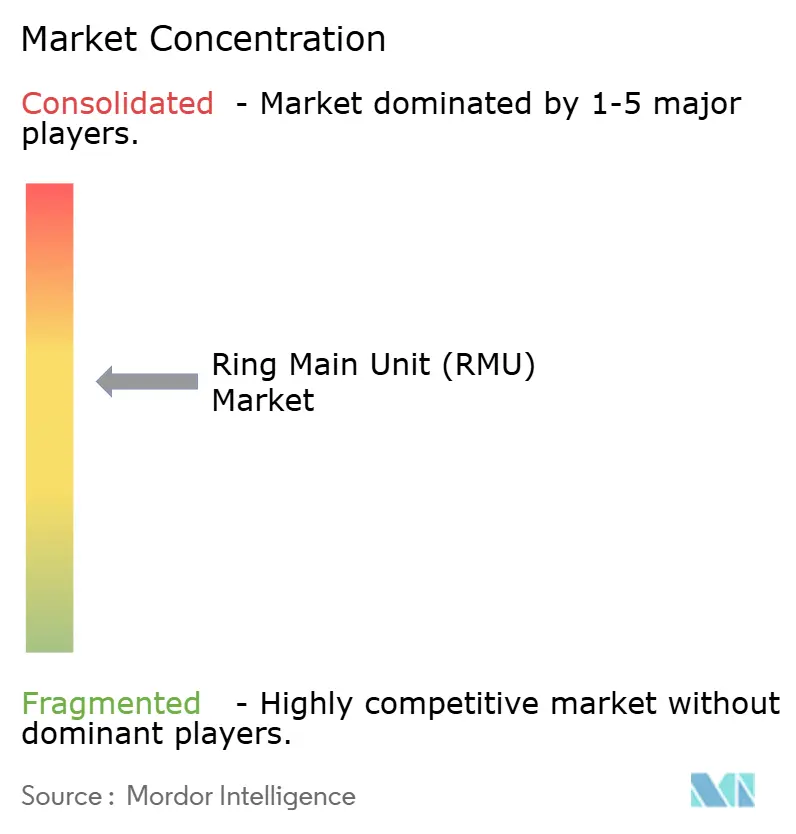

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ring Main Unit (RMU) Market Analysis by Mordor Intelligence

The ring main unit market size reaches USD 3.08 billion in 2026 and is forecast to grow to USD 4.26 billion by 2031 at a 6.72% CAGR, underscoring how medium-voltage distribution architecture is pivoting toward SF₆-free insulation, digital automation, and distributed-generation readiness. Gas-insulated platforms still dominate revenue because of long-lived installed bases, yet impending regulatory bans, particularly Europe’s F-Gas Regulation (EU) 2024/573, are redirecting research and procurement budgets to vacuum and solid-dielectric technologies. At the same time, North American utilities deploy IEC 61850-compliant secondary substations to meet SAIDI targets under NERC, while Asia-Pacific mega-cities bury feeders to free surface space and reduce storm-related faults. End-user behavior reflects these shifts: distribution utilities upgrade aging assets to harden networks, renewable developers specify medium-voltage collector loops for solar and wind parks, and hyperscale data-center owners demand 99.995% uptime. Competitive intensity is moderate, with the top five vendors controlling roughly 55% of 2025 global revenue, but localized manufacturing by Chinese challengers compresses margins in price-sensitive regions.

Key Report Takeaways

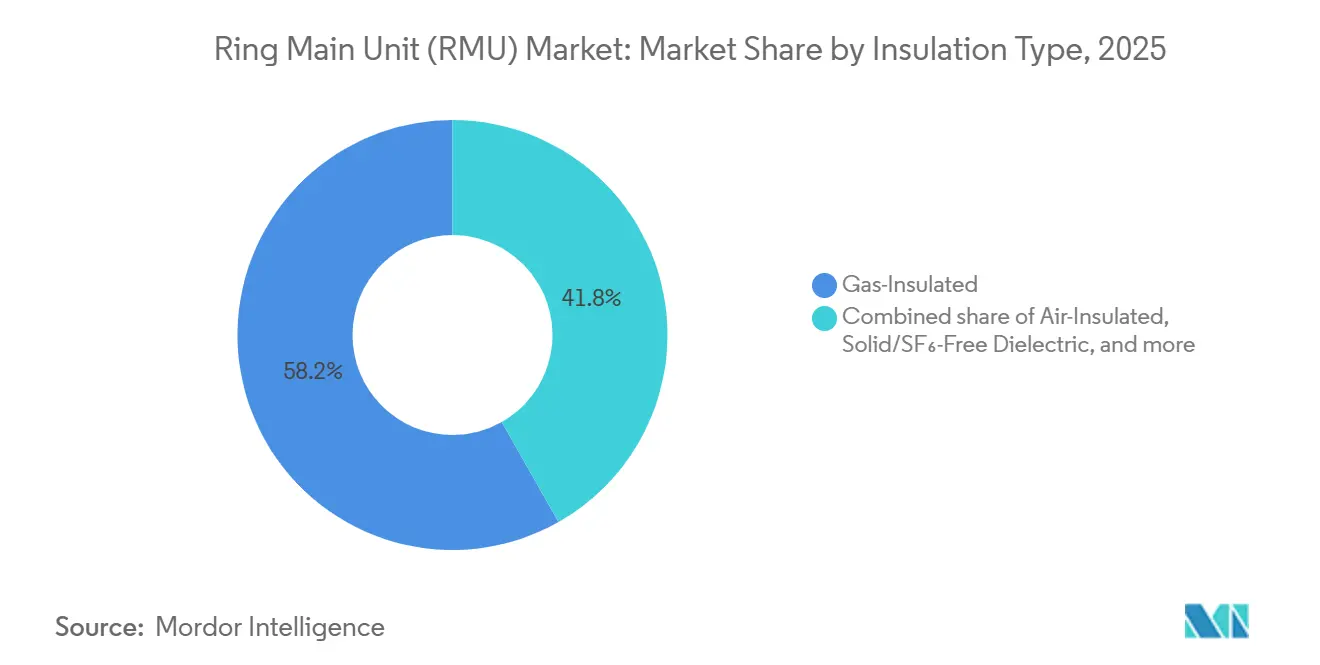

- By insulation type, gas-insulated configurations captured 58.2% of 2025 revenue, while solid and SF₆-free variants are projected to expand at a 9.5% CAGR to 2031.

- By installation, outdoor units held a 57.5% share in 2025, whereas indoor designs are forecast to compound at 8.4% through 2031.

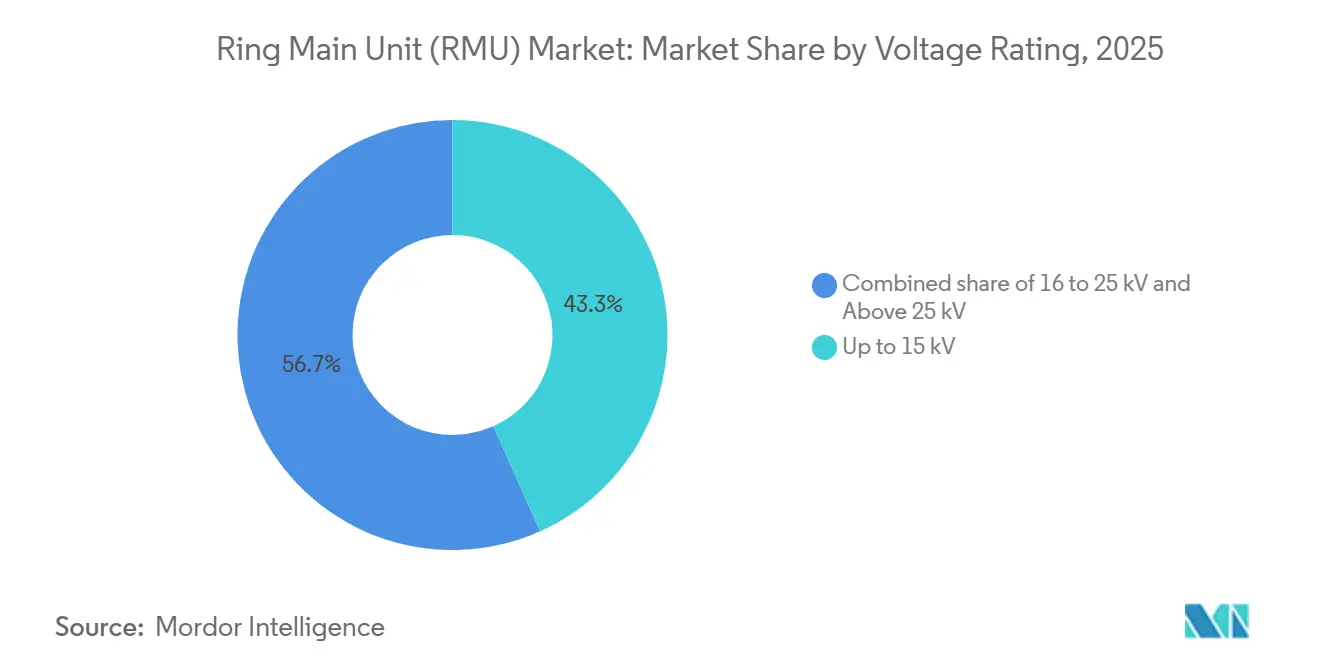

- By voltage rating, the up-to-15 kV segment accounted for 43.3% of 2025 demand, but the above-25 kV class is set to grow at 7.7% through 2031.

- By automation level, conventional manually operated RMUs comprised 77.7% of 2025 shipments, yet smart and motorized variants will register a 9.0% CAGR to 2031.

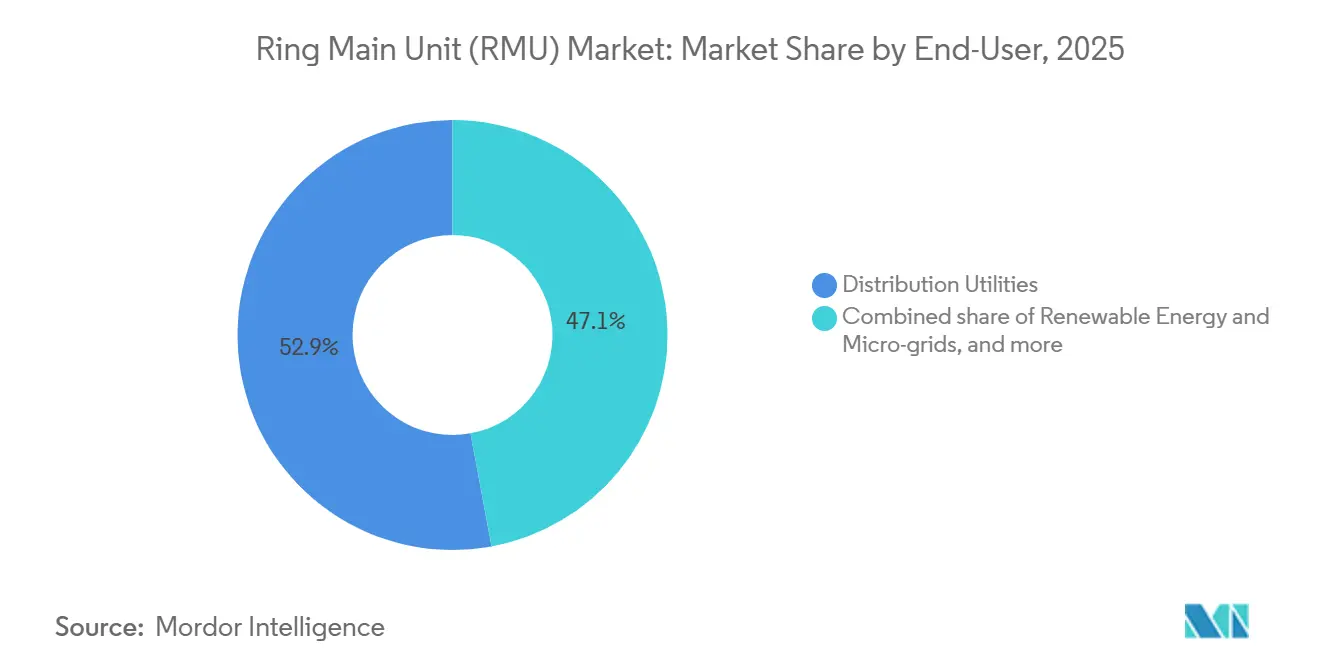

- By end-user, distribution utilities commanded 52.9% of 2025 revenue, while renewable energy and micro-grids represent the fastest-growing bracket at an 8.8% CAGR.

- By geography, Asia-Pacific led with 43.2% of 2025 sales and is expected to advance at an 8.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ring Main Unit (RMU) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SF₆-free RMU Adoption Accelerated by EU F-Gas Phase-Out | 1.8% | Europe, North America, APAC (Japan, South Korea) | Medium term (2-4 years) |

| Urban Underground Distribution Upgrades in Asia Mega-Cities | 1.5% | APAC core (China, India, ASEAN), spill-over to Middle East | Long term (≥ 4 years) |

| Grid-Automation Investments by North-American Utilities | 1.2% | North America, Europe | Medium term (2-4 years) |

| Medium-Voltage Collector Circuits in Renewable Parks | 1.0% | Global, with concentration in APAC, Europe, North America | Long term (≥ 4 years) |

| Sub-Transmission Retrofit Programs across GCC States | 0.7% | Middle East (UAE, Saudi Arabia, Qatar, Kuwait) | Short term (≤ 2 years) |

| High-Reliability Demand from Hyperscale Data-Centres | 0.6% | North America, Europe, APAC (Singapore, Hong Kong) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

SF₆-Free RMU Adoption Accelerated by EU F-Gas Phase-Out

Regulation (EU) 2024/573 bans SF₆-insulated switchgear up to 24 kV from January 2026 and up to 52 kV by January 2030, forcing utilities to migrate toward vacuum interrupters and solid dielectrics.[1]European Commission, “Regulation (EU) 2024/573,” europa.eu Suppliers such as ABB and Eaton have already commercialized SF₆-free RMUs that replicate 25 kA short-circuit ratings while removing fluorinated gases. Certification costs for technicians handling residual SF₆ equipment also climb under Regulation 2025/627, accelerating fleet turnover. Across the Atlantic, Pacific Gas & Electric now specifies vacuum technology for any secondary substation commissioned after 2024 in anticipation of future EPA restrictions. Newly revised IEC 62271 series tests assure interoperability across the emerging dielectric mix, further derisking adoption.

Urban Underground Distribution Upgrades in Asia Mega-Cities

State Grid Corporation of China directs CNY 520 billion (USD 73 billion) per year to bury 10 kV feeders in Beijing, Shanghai, Shenzhen, and Guangzhou, curbing visual clutter and storm damage.[2]State Grid Corporation of China, “Annual Investment Plan,” sgcc.com.cn India’s Revamped Distribution Sector Scheme allocates INR 3 lakh crore (USD 36 billion) through 2027 for similar ring-main topologies in Delhi, Mumbai, and Bangalore. ASEAN utilities echo the trend as Singapore enforces 100% underground distribution. Compact indoor RMUs occupy 40–60% less footprint than outdoor enclosures, fitting basements beneath high-rise developments. High downtown land prices of USD 10,000 per m² in Hong Kong and Tokyo make below-grade installations financially rational despite higher switchgear unit prices.

Grid-Automation Investments by North-American Utilities

The U.S. Department of Energy’s Grid Modernization Initiative invests USD 3.5 billion annually to embed sensors and automate distribution gear, targeting a SAIDI below 100 minutes by 2030.[3]U.S. Department of Energy, “Grid Modernization Initiative,” energy.gov Utilities install IEC 61850-enabled RMUs that isolate faults in seconds, slashing truck-roll expenses. National Grid’s 2024 filing earmarked USD 47.7 million for digital ring-main retrofits. Schneider Electric’s EcoStruxure analytics forecast insulation degradation up to 18 months in advance, reducing unscheduled outages by 35% at Duke Energy pilot sites. NERC CIP standards now obligate cybersecurity modules in any IP-connected RMU, adding USD 5,000–10,000 per unit.

Medium-Voltage Collector Circuits in Renewable Parks

Every 100 MW solar farm typically needs 10–15 RMUs to segment inverters into switchable blocks, improving O&M flexibility. IEEE 1547-2018 ride-through rules push suppliers to integrate fast-clearing vacuum interrupters that operate within three cycles. Offshore wind demands IP67-rated enclosures; Siemens Gamesa specifies marine-grade RMUs for 33 kV collector hubs. Battery storage adds bidirectional power flow, so four-quadrant switching logic becomes mandatory, while NREL studies show ring-main topologies lowering balance-of-system cost 8–12% relative to radial schemes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-Ex & Limited Local Assembly in Sub-Saharan Africa | -0.9% | Sub-Saharan Africa (Nigeria, Kenya, Ghana, Tanzania) | Long term (≥ 4 years) |

| SF₆ Phase-Out Transition-Cost Uncertainty for Utilities | -0.6% | Europe, North America | Short term (≤ 2 years) |

| Lengthy Utility Type-Approval Cycles in South America | -0.5% | South America (Brazil, Argentina, Colombia) | Medium term (2-4 years) |

| Vacuum Interrupter & Semiconductor Supply Volatility | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex & Limited Local Assembly in Sub-Saharan Africa

Electrification lags at 48% and utilities prioritize generation over distribution, leaving RMU adoption restrained by unit prices of USD 15,000–50,000 versus USD 5,000–10,000 for pole-mounted gear.[4]World Bank, “Tracking SDG 7,” worldbank.org Ninety percent of switchgear is imported, exposing projects to currency swings such as Nigeria’s 40% naira devaluation in 2024. Local assembly remains nascent, with only a few Schneider Electric and ABB facilities serving South Africa and Kenya. Skills shortages prolong commissioning by 6–12 months, eroding investor confidence.

SF₆ Phase-Out Transition-Cost Uncertainty for Utilities

Vacuum and solid-dielectric RMUs carry a 15–20% purchase-price premium, so business cases depend on assumptions around carbon pricing and disposal fees. Regulation 2024/573 allows SF₆ maintenance until 2035, letting operators sweat assets and defer capital outlays. U.S. utility decisions are left to state commissions, causing patchwork adoption: California’s IOUs pledged voluntary reduction targets, while southeastern cooperatives still procure gas-insulated designs. Limited vacuum-interrupter production capacity, expanded only 12% between 2022 and 2024, sustains premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulation Type: Vacuum Technology Reshapes Dielectric Mix

Gas-insulated units held 58.2% of 2025 revenue. Solid and SF₆-free designs, however, will advance at a 9.5% CAGR, pushing gas-insulated share below 50% by 2028. Eaton’s Xiria achieves 630 A continuous current and 25 kA short-circuit within a footprint 20% smaller than gas units, appealing where vault space is fixed. Utilities face retraining costs of USD 10,000–20,000 per maintenance crew for vacuum diagnostics. The ring main unit market share for solid dielectrics is forecast to reach 35% in 2031, up from 18% in 2025.

Gas-insulated incumbency remains strong in high-fault networks up to 40 kA, but voluntary SF₆ bans in California and Japan signal a global pivot. Air-insulated RMUs thrive in dust-free rural networks under 20 kA, while oil-insulated variants edge toward obsolescence. Lifecycle carbon disclosures, now required by many European tenders, are hastening the shift.

By Installation: Space Economics Favor Indoor Configurations

Outdoor RMUs generated 57.5% of 2025 sales, yet indoor installations will compound at 8.4% through 2031, buoyed by real-estate premiums in dense cities. When land acquisition, fencing, and aesthetic mitigation are included, indoor options often undercut the outdoor total installed cost. Singapore already records an indoor penetration above 90%. In contrast, the ring main unit market size for outdoor gear remains higher in the GCC because ventilation and land availability outweigh space constraints.

Schneider’s SM6 series (0.8 m² per feeder bay) exemplifies how compact indoor gear enables retrofit without civil expansion. IEEE C37.20.7 environmental tests add USD 5,000–10,000 certification overhead for outdoor variants exposed to solar radiation, sand, and seismic risk. As urban ordinances ban visible equipment, utilities in Europe, Japan, and South Korea pivot to indoor.

By Voltage Rating: Sub-Transmission Boosts High-Voltage Segment

The up-to-15 kV class captured 43.3% of 2025 demand, fueled by residential feeders. Above-25 kV units will, however, log a 7.7% CAGR as cities and heavy industry migrate to 33–40.5 kV loops to curb copper mass and improve voltage drop. A 100 MW data-center campus needs only 8–10 RMUs at 40.5 kV versus 15–20 units at 24 kV, yielding a 12–15% installed-cost gain.

Mining conveyor, arc-furnace, and mega-project applications push short-circuit duties to 31.5 kA, so vacuum interrupters designed to IEC 62271-100 dominate. GCC states, and Australia already specify 36 kV ratings for sub-transmission rings, while European utilities begin piloting 40.5 kV urban feeders.

By Automation Level: Digital Integration Accelerates Smart Adoption

Conventional units still count for 77.7% of 2025 installations, mostly in emerging markets. Smart and motorized RMUs, however, will grow at 9.0% per year. NERC CIP-required cybersecurity modules cost USD 5,000–10,000 per unit but cut outage restoration time by 40% by enabling remote segmentation. The ring main unit market size for smart variants is projected to climb to USD 1.9 billion by 2031.

ABB’s Ability and Siemens SICAM suites link real-time data to asset-management dashboards, lengthening maintenance cycles 10–15%. Asia-Pacific adoption lags at 10–15% penetration because manual switching labor remains cheap, yet regulators are moving to performance-based incentives that reward automation.

By End-User: Renewables Reshape Demand Patterns

Distribution utilities own 52.9% of 2025 revenue, but renewables and micro-grids rise fastest at 8.8% CAGR. A 100 MW solar plant typically deploys 10–15 RMUs to segment collectors; offshore wind requires IP67 durability, adding 30–40% cost. The ring main unit market size for renewable parks is expected to exceed USD 700 million by 2031.

Industrial users such as steel and cement integrate 36 kV RMUs rated 31.5 kA to handle high-fault currents. Commercial complexes select indoor gear for aesthetics and real-estate reasons, with Schneider’s SM6 popular in Singapore malls and European CBDs. IEEE 1547-2018 fully embeds medium-voltage ride-through, tightening component specifications across all renewables.

Geography Analysis

Asia-Pacific generated 43.2% of 2025 revenue and will persist at an 8.4% CAGR, driven by China’s annual CNY 520 billion (USD 73 billion) grid budget and India’s INR 3 lakh crore (USD 36 billion) modernization scheme. Solid and SF₆-free adoption in the region is forecast to reach 25% of sales by 2028. Japan and South Korea retrofit substations with smart RMUs to align with METI guidelines on fluorinated-gas alternatives. Europe, the second-largest market, accelerates due to the 2026 and 2030 SF₆ bans. Germany, France, Spain, and the Nordics already see SF₆-free products capturing 40% of 2025 new installations. Ofgem’s RIIO-ED2 in the U.K. links expenditure to outage penalties, spurring digital RMU uptake.

North America benefits from USD 3.5 billion in annual DOE funding but remains fragmented by state regulation. Mexico’s CFE will spend MXN 80 billion (USD 4.7 billion) in 2024 on ring-main upgrades in urban centers. South America wrestles with 12–18-month certification lags that keep gas-insulated dominance intact. Brazil’s ring main unit market will, however, recover as ANEEL channels R$20 billion (USD 4 billion) into distribution 2024–2025. The Middle East invests heavily, with DEWA allocating AED 86 billion (USD 23.4 billion) and SEC spending SAR 50 billion (USD 13.3 billion) yearly on 33–36 kV loops suited to giga-projects. Sub-Saharan Africa remains constrained by high cap-ex and currency volatility. Yet localized assembly efforts by CHINT and TGOOD, plus IFC-backed electrification funding, could unlock latent demand if cost curves fall.

Competitive Landscape

Five incumbents, ABB, Schneider Electric, Siemens, Eaton, and Larsen & Toubro, control around 55% of the 2025 global revenue. ABB markets the SafeRing vacuum-solid platform up to 24 kV, whereas Eaton’s Xiria offers a 20% smaller footprint. Schneider’s EcoStruxure analytics yielded a 35% drop in unplanned outages during Duke Energy pilots. Chinese entrants CHINT, TGOOD, and Shanghai Electric gain share by localizing assembly and underpricing rivals 20–30% in emerging regions.

Alfanar leverages Vision 2030 local-content rules to secure turnkey Saudi contracts, assembling RMUs with 60% indigenous parts. Hyundai Electric expanded into the Middle East sub-transmission by leveraging KRW 3.2 trillion (USD 2.4 billion) in 2023 revenue. Patent filings center on vacuum-interrupter metallurgy and solid-dielectric formulations, signaling a race toward reliability rather than price.

Ring Main Unit (RMU) Industry Leaders

ABB Ltd.

Schneider Electric SE

Siemens AG

Eaton Corporation plc

Lucy Electric Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Noida completed the installation of RMUs to enhance network reliability under the Revamped Distribution Sector Scheme (RDSS). L&T surveyed plans for future substations under the same scheme.

- June 2025: Alliander N.V. sought supplier feedback on tender documents through a final market consultation (RFI) for Ring Main Units (RMUs). This move precedes a formal European tender slated for late 2025 or early 2026, targeting supplies in the Netherlands.

- February 2025: In a move to modernize the grid, RMC Switchgears Ltd clinched a notable INR 108.05 crore order in Gujarat. The order, channeled through MGVCL under the government's RDSS scheme, emphasizes the development of power distribution infrastructure, spotlighting 11 kV underground (UG) cables and Ring Main Unit (RMU) systems.

- November 2024: Kerala State Electricity Board (KSEB) issued a tender for two 11 kV, 630 A Ring Main Units (RMUs), under Tender Reference Number TDT/09/2024-25.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the ring main unit (RMU) market as all factory-built, medium-voltage switchgear assemblies (up to 36 kV) in which two incoming feeders and one outgoing feeder are linked through a common bus, permitting ring or radial operation for safer, uninterrupted distribution. The count covers gas, air, oil, and solid-dielectric insulated RMUs supplied as new equipment to utilities, renewables, industry, and infrastructure projects worldwide.

Scope Exclusions: We do not include retrofitted switchgear panels, ring main units sold only as spare parts, or after-sales service revenues.

Segmentation Overview

- By Insulation Type

- Gas-Insulated

- Air-Insulated

- Oil-Insulated

- Solid/SF₆-Free Dielectric

- By Installation

- Outdoor

- Indoor

- By Voltage Rating

- Up to 15 kV

- 16 to 25 kV

- Above 25 kV (incl. 36/40.5 kV)

- By Automation Level

- Conventional

- Smart/Motorized/Digital RMU

- By End-User

- Distribution Utilities

- Industrial Facilities

- Commercial and Residential Infrastructure

- Renewable Energy and Micro-grids

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We complemented desk insights with interviews and short surveys covering distribution utility engineers in Asia-Pacific, renewable park EPC firms in Europe, and switchgear distributors in North America. These conversations helped us validate typical feeder ratings, clarify the shift toward SF6-free dielectrics, and fine-tune regional price curves.

Desk Research

Our desk work starts with public datasets that anchor installed network size and spending: International Energy Agency electricity statistics, World Bank infrastructure capex tables, IEA-IRENA renewable additions, European Commission F-gas regulation timelines, and IEEE papers on compact switchgear safety. Annual reports and 10-Ks from major switchgear manufacturers help us track shipment mix and average selling price trends.

Paid resources such as D&B Hoovers sales analytics, Dow Jones Factiva news archives, and Questel patent counts let us gauge competitive intensity, while power-grid tenders gathered through Tenders Info highlight upcoming capacity pockets. This list is illustrative only; many further open and paid sources feed our evidence pool.

Market-Sizing & Forecasting

We construct a top-down demand pool that begins with medium-voltage line-kilometer additions, renewable capacity pipelines, and urban building completions, which are then translated into feeder counts using benchmark RMU-per-kilometer and RMU-per-MW ratios. Selective bottom-up cross-checks, supplier shipment roll-ups, and sampled ASP x volume flag gaps and adjust totals. Key input variables include average feeder length, renewable share of new substations, ASP erosion from SF6-free designs, planned smart-grid automation spending, and regional currency shifts. Multivariate regression with scenario analysis projects these drivers to 2030, giving a baseline CAGR that our expert panel confirms.

Data Validation & Update Cycle

Analysts at Mordor run variance screens against import data, trade press installation tallies, and company guidance. Outliers trigger a second review before sign-off. We refresh the model annually and issue mid-cycle updates when material policy or technology events occur. A final sense check happens just before every client delivery.

Why Mordor's Ring Main Unit Baseline Commands Reliability

Published estimates often differ because firms pick dissimilar scopes, price assumptions, and refresh cadences. We preview below how such choices shift headline numbers.

Key gap drivers include whether indoor units are counted, how ASPs are deflated, and if hybrid switchgear or service contracts creep into totals. Mordor reports only new RMU hardware and updates the model every twelve months, which limits drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.85 Bn (2025) | Mordor Intelligence | - |

| USD 3.20 Bn (2024) | Global Consultancy A | Includes semi-urban MV switchgear and bundled maintenance contracts |

| USD 2.50 Bn (2024) | Industry Journal B | Excludes indoor RMUs and solid-dielectric products |

| USD 2.10 Bn (2024) | Market Observer C | Uses aggressive ASP compression and single economic scenario |

The comparison shows that once scope creep or overly narrow coverage is removed, figures converge toward our balanced midpoint. That disciplined, transparent approach is why decision-makers rely on Mordor's baseline when planning grid modernization investments.

Key Questions Answered in the Report

What is the current ring main unit market size and expected growth?

The ring main unit market size is USD 3.08 billion in 2026 and is projected to reach USD 4.26 billion by 2031, growing at a 6.72% CAGR.

Which dielectric technology is gaining share fastest?

Solid and other SF₆-free designs are forecast to expand at a 9.5% CAGR because of Europe’s F-Gas ban and voluntary North American adoption.

Why are indoor RMUs growing quicker than outdoor units?

Urban land prices and undergrounding mandates push utilities to choose compact indoor RMUs, which are expected to grow at 8.4% annually through 2031.

How are renewables influencing RMU demand?

Utility-scale solar, wind, and battery parks need medium-voltage collector circuits; this end-user bracket is the fastest growing at an 8.8% CAGR.

Which regions lead future RMU installations?

Asia-Pacific leads with 43.2% of 2025 revenue and maintains the highest regional CAGR of 8.4% driven by China and India’s grid modernization budgets.

Who are the key RMU suppliers today?

ABB, Schneider Electric, Siemens, Eaton, and Larsen & Toubro hold about 55% of global revenue, while CHINT and TGOOD are advancing in emerging markets.

Page last updated on: