Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 44.96 Billion |

| Market Size (2026) | USD 46.73 Billion |

| Market Size (2031) | USD 56.7 Billion |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh Rice Market Analysis by Mordor Intelligence

The Bangladesh Rice Market size was valued at USD 44.96 billion in 2025 and estimated to grow from USD 46.73 billion in 2026 to reach USD 56.7 billion by 2031, at a CAGR of 3.95% during the forecast period (2026-2031). This growth trajectory reflects the market's resilience despite facing significant headwinds from climate volatility and import dependencies that have shaped procurement strategies across the value chain. The government's procurement price of Tk49 per kilogram for Boro rice in 2024 established a baseline that influenced private sector pricing mechanisms, while rice prices reached 12-year highs due to supply disruptions and hoarding activities. Climate-resilient varieties, strategic cold-chain financing, and e-commerce penetration collectively reinforce long-term growth prospects. Local conglomerates are expanding capacity, while potential export liberalization for aromatic grains could open premium revenue streams. Bangladesh’s rice market growth in 2025 is fueled by a rising population, increasing urbanization, and higher disposable incomes, which drive strong demand for rice as the nation’s staple food. Consumer preferences are shifting toward more convenient packaged rice and premium aromatic varieties, supported by the expansion of distribution channels such as supermarkets and online retail platforms. The industry benefits from government programs to ensure food security, stable pricing, and modernization of agricultural practices, alongside ongoing product innovation and improved supply chain management among leading processors and brands. These dynamics collectively sustain growth, despite occasional price fluctuations and challenges related to climate variability and input costs.

Key Report Takeaways

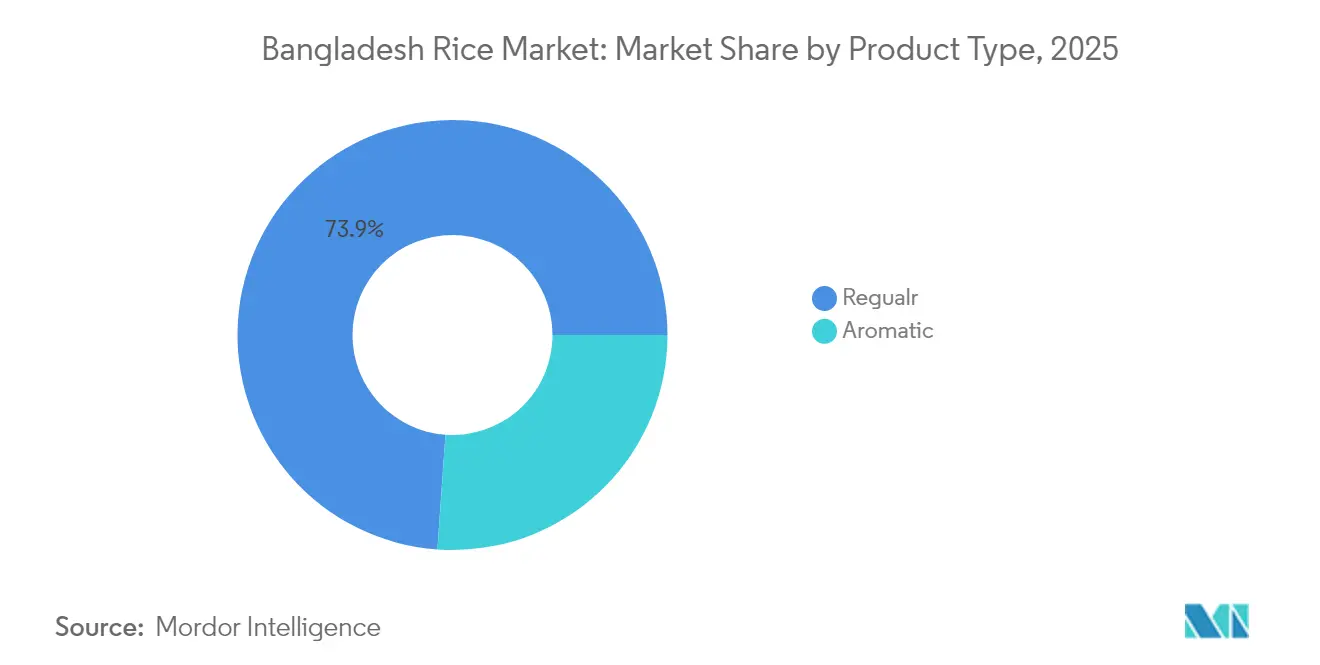

- By product type, regular rice held 73.88% of Bangladesh rice market share in 2025, whereas aromatic rice is projected to register the fastest 5.12% CAGR to 2031.

- By category, white rice accounted for 84.95% share of the Bangladesh rice market size in 2025 and is expected to grow at a 4.18% CAGR through 2031.

- By nature, conventional rice dominated with 95.05% share in 2025, while organic rice is poised for a 6.78% CAGR during 2026-2031.

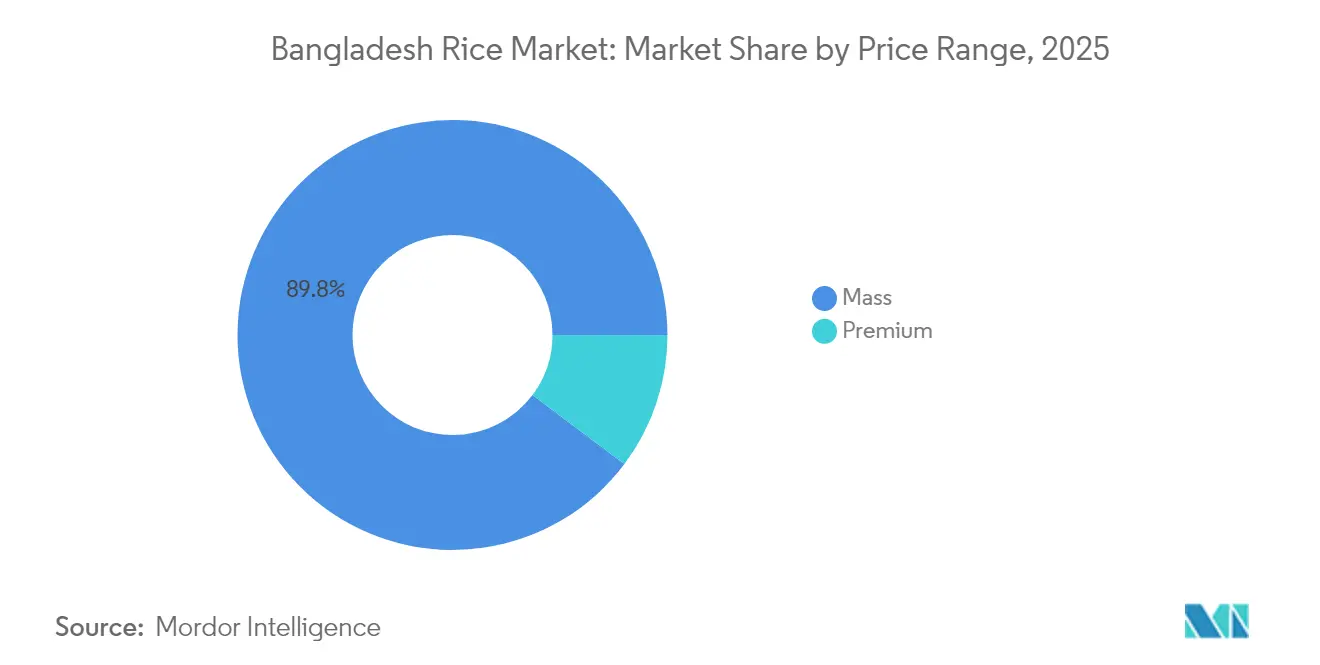

- By price range, the mass segment commanded 89.75% revenue share in 2025; the premium segment is expanding at a 5.74% CAGR to 2031.

- By distribution channel, convenience and grocery stores led with 35.10% share in 2025, while online retail platforms are advancing at a 5.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Rice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rice as Staple Food Driving Cultural and Consumption Patterns | + 0.8% | National, with higher consumption in rural areas | Long term (≥ 4 years) |

| Government Support and Subsidies | + 0.6% | National, concentrated in major producing regions | Medium term (2-4 years) |

| Adoption of High-Yield Rice Varieties | + 0.4% | Rangpur, Rajshahi, Dhaka divisions primarily | Medium term (2-4 years) |

| Rising Demand for Aromatic Rice | + 0.9% | Urban centers and export markets | Short term (≤ 2 years) |

| Growing Organic and Fortified Rice Interest | + 0.5% | Urban areas, particularly Dhaka and Chittagong | Long term (≥ 4 years) |

| Expansion of Modern Farming Practices | + 0.3% | Technology-adopting regions, government pilot areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rice as Staple Food Driving Cultural and Consumption Patterns

Cultural embedding of rice consumption creates inelastic demand that insulates the market from economic volatility, with per capita consumption remaining stable despite income fluctuations. Bangladesh's position as the world's fourth-largest rice producer stems from this deep-rooted dietary dependence, where rice constitutes approximately 70% of daily caloric intake across demographic segments [1]Source: Food and Agriculture Organization, "The state of food security and nutrition in the world", fao.org. The cultural significance extends beyond nutrition to religious and social ceremonies, creating predictable consumption cycles that enable supply chain planning. Urban migration patterns are shifting consumption toward processed and branded rice products, generating premium segment opportunities. This cultural foundation provides market stability that attracts long-term investments in processing and distribution infrastructure. Traditional rice consumption practices remain deeply embedded in family customs and celebrations, ensuring sustained demand across generations. Regional festivals and harvest seasons create cyclical spikes in rice consumption, allowing retailers and distributors to optimize their inventory management strategies.

Government Support and Subsidies

Government procurement mechanisms through the Trading Corporation of Bangladesh (TCB) and direct subsidies create price floors that stabilize farmer incomes while influencing private sector pricing strategies. The procurement price of Tk49 per kilogram for Boro rice in 2024 represented a strategic intervention to maintain production incentives amid input cost inflation. Import duty reductions and authorized private sector imports of 392,000 tonnes through December 2024 demonstrate policy flexibility in managing supply shortfalls. Rice fortification programs supported by the World Food Programme across 20 districts create new market segments while addressing nutritional deficiencies. These interventions generate market predictability that encourages private sector investment in storage and processing capabilities. The government's multi-faceted approach has helped maintain a delicate balance between producer profitability and consumer affordability in the domestic rice market. The establishment of modern storage facilities and enhanced distribution networks has further strengthened the rice value chain, improving food security across the country.

Adoption of High-Yield Rice Varieties

High-yield variety adoption accelerates through IRRI-BRRI collaborative development of climate-resilient strains like BRRI dhan96, 101, 104, and 105, which offer superior productivity under stress conditions. DNA fingerprinting studies reveal increasing farmer acceptance of improved varieties, with hybrid rice seeds supplied 95.68% by the private sector, indicating market-driven adoption patterns International Rice Research Institute. Heat-tolerant varieties developed for climate adaptation provide yield stability that reduces production risks and encourages expansion into marginal lands. The private sector's dominance in seed supply creates competitive dynamics that drive innovation and farmer education programs. Technology transfer mechanisms through agricultural extension services amplify adoption rates across traditional farming communities. Government subsidies and financial incentives further support farmers in transitioning to these improved varieties, reducing initial adoption barriers. Regional success stories and demonstration plots serve as practical evidence for skeptical farmers, accelerating the shift toward modern rice cultivation methods.

Rising Demand for Aromatic Rice

Aromatic rice demand acceleration reflects evolving consumer preferences toward premium products, with varieties like Chinigura and Nazirshail commanding price premiums that incentivize production expansion. Government consideration of lifting the export ban on aromatic rice signals recognition of international market opportunities, particularly in Middle Eastern and European markets where Bangladeshi varieties compete with Basmati rice. Urban consumers increasingly differentiate between regular and aromatic varieties, creating segmented pricing structures that reward quality improvements. Export potential generates foreign exchange earnings that could offset import dependencies for regular rice varieties. Processing investments in aromatic rice packaging and branding create value-added opportunities for domestic companies. The development of specialized storage and transportation infrastructure supports the preservation of aromatic qualities throughout the supply chain. Research institutions focus on developing new aromatic rice varieties with enhanced yield potential and disease resistance to meet growing market demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate Change Impact on Harvests | -0.7% | Coastal and flood-prone regions primarily | Long term (≥ 4 years) |

| Seasonal Floods Damaging Crops | -0.5% | Rangpur, Sylhet, and northern districts | Short term (≤ 2 years) |

| Competition from Imported Rice | -0.4% | Urban markets and border regions | Medium term (2-4 years) |

| Lack of Cold Chain Facilities | -0.3% | Rural production areas and storage hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate Change Impact on Harvests

Climate variability increasingly disrupts traditional cropping patterns, with temperature fluctuations and irregular rainfall affecting yield predictability across major producing regions. Heat-tolerant rice varieties developed through IRRI-BRRI partnerships represent adaptive responses, yet adoption rates lag behind climate change acceleration International Rice Research Institute. Coastal salinity intrusion threatens productive agricultural land, forcing farmers to adopt salt-tolerant varieties or abandon cultivation entirely. The Bangladesh Climate Change Strategy and Action Plan identify agriculture as a priority sector requiring USD 2.3 billion in adaptation investments through 2030. Long-term productivity declines could necessitate increased import dependencies, undermining food security objectives and creating fiscal pressures on government procurement programs. Rising sea levels and increased frequency of extreme weather events further compound these challenges, with projections indicating up to 15% of arable land could be lost to salinity by 2050. The combination of reduced cultivable area and climate stress on existing cropland may require significant shifts in agricultural policy and investment priorities to maintain food production levels.

Seasonal Floods Damaging Crops

Seasonal flooding patterns have intensified, with Aman crop damage in 2024 contributing to supply shortfalls that necessitated emergency imports from Vietnam and India. Flood-prone regions experience recurring production losses that create supply volatility and price spikes during harvest seasons. Traditional flood management infrastructure requires modernization to protect agricultural areas, yet investment gaps persist in drainage and embankment systems. Early warning systems and flood-resistant varieties offer mitigation potential, though farmer adoption remains limited by access to improved seeds and technical knowledge. Insurance mechanisms for crop protection remain underdeveloped, leaving farmers vulnerable to weather-related losses that discourage production expansion. The lack of comprehensive flood risk assessment tools hampers effective policy responses and infrastructure planning at both regional and national levels. Climate projections indicate an increasing frequency of extreme weather events, highlighting the urgent need for systemic changes in agricultural resilience strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aromatic Varieties Drive Premium Shift

The aromatic rice segment's 5.12% CAGR through 2031 outpaces regular rice growth, reflecting consumer willingness to pay premiums for quality differentiation and sensory attributes. Regular rice maintains its dominant 73.88% market share in 2025 due to affordability and widespread availability, yet aromatic varieties like Chinigura and Nazirshail are capturing urban market share through superior taste profiles and cultural associations with special occasions. Government consideration of lifting the aromatic rice export ban creates international market opportunities that could incentivize production expansion and quality improvements.

Processing investments in aromatic rice packaging and branding enable value capture beyond farm-gate prices, with companies developing premium product lines that target affluent consumers. Regular rice remains essential for food security programs and mass market consumption, ensuring stable demand despite premium segment growth. The Bangladesh Standards and Testing Institution (BSTI) provides quality certification frameworks that support market differentiation between product categories, enabling consumers to make informed purchasing decisions based on quality parameters. Modern processing facilities incorporate advanced sorting and grading technologies to maintain consistent quality standards across different rice varieties and price points. The integration of automated packaging lines and quality control systems has improved operational efficiency while reducing post-harvest losses in the processing chain.

By Category: White Rice Dominance Reflects Processing Preferences

White rice commands 84.95% market share in 2025 while maintaining 4.18% CAGR through 2031, demonstrating consumer preference for processed rice over brown alternatives. Processing technologies that remove bran and germ layers align with traditional cooking methods and taste preferences, creating barriers to brown rice adoption despite nutritional advantages. Brown rice and other categories serve niche health-conscious segments but face challenges in mainstream market penetration due to longer cooking times and different texture profiles.

Fortification initiatives supported by the World Food Programme across 20 districts create opportunities for value-added white rice products that address micronutrient deficiencies without altering taste preferences . Modern milling technologies enable consistent quality and extended shelf life for white rice, supporting distribution to remote areas where storage conditions may be suboptimal. The Food Safety Authority of Bangladesh regulates processing standards that ensure consumer safety while maintaining product quality across the supply chain. The implementation of automated quality control systems in rice processing facilities has improved the efficiency of fortification processes and reduced production costs. Additionally, partnerships between local rice processors and international nutrition organizations have facilitated knowledge transfer and technical expertise in fortification methods.

By Nature: Organic Segment Emerges Despite Certification Gaps

Organic rice accelerates at 6.78% CAGR through 2031 despite conventional rice maintaining 95.05% market share in 2025, indicating nascent consumer interest in chemical-free production methods. Limited authentic organic certification creates market confusion, with many products marketed as "organic" without proper verification, constraining premium pricing opportunities. The lack of standardized verification processes across regions further complicates the certification landscape. Consumer trust issues arising from fraudulent organic claims have led to increased scrutiny of product authenticity in key markets.

Conventional rice production benefits from established input supply chains and farmer familiarity with chemical fertilizers and pesticides, maintaining cost advantages that support mass market pricing. Organic certification bodies like the Bangladesh Organic Products Manufacturers Association (BOPMA) work to establish standards that could legitimize the organic segment and enable premium pricing. Government support for organic farming through subsidy programs and technical assistance could accelerate adoption rates among farmers willing to transition from conventional methods. The economies of scale in conventional farming continue to provide significant cost benefits to producers. Infrastructure development and technological advancements in conventional farming methods further reinforce its market dominance.

By Price Range: Premium Segment Gains Traction

Premium rice segments achieve 5.74% CAGR through 2031 while mass market products maintain 89.75% share in 2025, reflecting income growth and evolving consumer preferences toward quality differentiation. Mass market dominance stems from price sensitivity among most consumers, where affordability remains the primary purchasing criterion for staple food products. Premium segments benefit from urbanization trends and rising disposable incomes that enable consumers to prioritize quality over price considerations. The growing middle class in developing economies further accelerates the shift toward premium rice varieties. Consumer awareness of nutritional benefits and food safety concerns also drives the transition to higher-quality rice products.

Brand development and packaging innovations enable companies to command premium pricing for superior rice varieties, with modern retail channels facilitating access to quality-conscious consumers. The premium segment includes aromatic varieties, organic products, and specialty rice types that serve specific culinary applications or health requirements. Market segmentation strategies allow companies to serve both mass and premium segments through differentiated product portfolios and distribution approaches. Investment in sustainable farming practices and certification programs strengthens premium positioning in the market. Digital marketing and e-commerce platforms enhance consumer reach and education about premium rice attributes.

By Distribution Channel: Digital Transformation Reshapes Access

Online retail stores achieve 5.38% CAGR through 2031 while convenience and grocery stores maintain 35.10% market share in 2025, demonstrating digital adoption's impact on food purchasing behaviors. Traditional channels including municipal corporation stores and local markets continue serving rural and price-sensitive consumers who prioritize proximity and cash transactions. These traditional markets remain resilient due to their deep community connections and understanding of local preferences. The accessibility and familiarity of these channels make them indispensable for daily shopping needs, particularly in areas with limited digital infrastructure. Supermarkets and hypermarkets capture urban market share through product variety and quality assurance, with chains like Shwapno targeting 3,000 stores within 3-5 years from the current 300+ outlets.

E-commerce platforms like Chaldal and ShopUp's B2B operations reach 31 million people through small shop networks, creating hybrid distribution models that combine digital efficiency with local accessibility. Modern retail growth of 25% annually over the past two years indicates structural shifts toward organized retail that could reach USD 1.9 billion by 2030. The integration of technology in retail operations has enabled real-time inventory tracking and enhanced customer service capabilities. Supply chain digitization enables inventory optimization and demand forecasting that reduces waste and improves product availability across distribution channels. The implementation of advanced analytics tools has strengthened decision-making processes in procurement and distribution. These technological advancements have significantly improved operational efficiency and customer satisfaction across the retail sector.

Regulatory Landscape

Bangladesh rice regulation focuses on food safety compliance and food security procurement. The Bangladesh Food Safety Authority (BFSA) enforces the Food Safety Act 2013 for contaminants and permissible limits, while product quality and labeling requirements are supported by standards and certification frameworks used in the packaged rice segment, including BSTI-aligned specifications. On the trade side, the Ministry of Food (via the Directorate General of Food) manages public stocks and administers private import permissions during supply stress; in January 2026 it issued permits for private traders to import 200,000 tonnes of parboiled rice to stabilize prices.

Import compliance increasingly runs through digital processes, with documentation and clearance routed via the National Food Import Information Management System (NFIIMS). Market conduct and anti-hoarding controls were tightened under the Foodgrains Supply (Prevention of Prejudicial Activity) Act 2023, which governs production, storage, transport, and marketing of foodgrains. Tariffs remain an adjustable lever managed by the National Board of Revenue (NBR), with standard rice customs duty commonly referenced at 25% across key rice categories but subject to discretionary reductions to manage inflation and food security outcomes.

Value Chain Analysis

Bangladesh's rice value chain starts with input supply (seed, fertilizer, irrigation, mechanization services) and farm production across major rice seasons. It then moves through aggregation intermediaries (forias, beparis, arothdars), milling (small and larger corporate mills), wholesale, and retail, spanning traditional markets, modern trade, and online platforms.

Public channels operate in parallel through the Ministry of Food-led procurement and the Public Food Distribution System (PFDS), including Open Market Sale (OMS) operations. The government operated 1,066 OMS centers in July 2025 to distribute subsidized grains and manage affordability during high-price periods. Bottlenecks persist at storage and logistics nodes, and import-side frictions can amplify volatility during deficit periods, with port congestion reported as extending vessel discharge times to over a month in some crunch scenarios, raising costs and delaying supply relief. Policy actions have increasingly targeted speed and control of emergency sourcing and stock-building, such as the October 2025 move to shorten the public tender process by 27 days to expedite emergency imports of 400,000 tonnes of rice. Bangladesh Bank commentary in 2025 also highlighted how layered intermediation and stockholding can concentrate margins during shortages, reinforcing the competitive advantage of large millers with capital and storage capacity.

Competitive Landscape

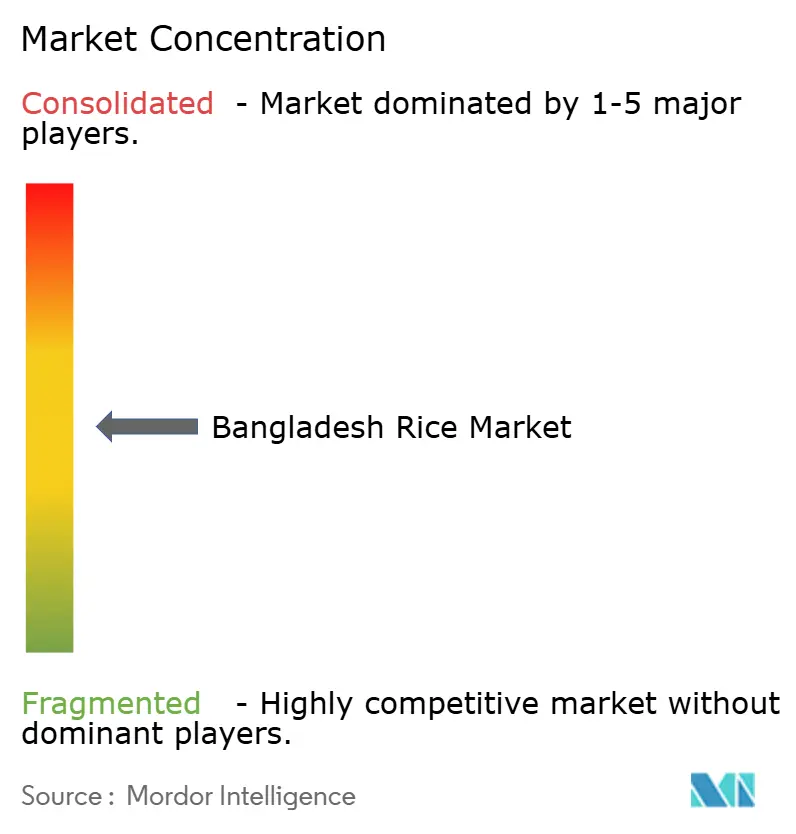

The Bangladesh rice market exhibits moderate concentration with balanced competition between established conglomerates and specialized players, creating opportunities for both scale-driven and niche strategies. Market leaders leverage vertical integration from seed development through retail distribution, while smaller companies focus on regional specialization or premium product segments that require less capital intensity. The market structure encourages innovation across different operational scales, fostering healthy competition. The diverse competitive landscape enables multiple business models to coexist, serving different consumer segments effectively.

Technology adoption patterns vary significantly, with larger players investing in IoT devices for food processing and quality control systems that enable consistent product standards International Rice Research Institute. Strategic positioning centers on supply chain control and brand development, as companies seek to capture value beyond commodity pricing through processing capabilities and distribution networks. PRAN-RFL Group's international presence in 147 countries demonstrates export-oriented strategies, while ACI Limited's partnerships with IRRI and USAID focus on seed development and agricultural technology transfer ACI Limited Annual Report 2023. The integration of advanced technologies has improved operational efficiency across the value chain. The industry's technological transformation has enhanced product quality and reduced post-harvest losses significantly.

Opportunities exist in organic certification, cold chain development, and rural market penetration where infrastructure gaps limit competitive intensity. The Bangladesh Standards and Testing Institution (BSTI) provides regulatory frameworks that ensure product quality while enabling market differentiation based on certified standards. The growing demand for certified organic products has created new market segments for producers. The development of cold chain infrastructure presents significant potential for reducing waste and improving market access.

Bangladesh Rice Industry Leaders

-

Alin Foods Ltd

-

Pran-RFL Group

-

Square Food and Beverages Ltd

-

Ovijat Food & Beverage Industries Ltd

-

ACI Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Storage and stock management infrastructure still leaves room for resilience improvements, particularly alongside the government's silo build-out. In FY 2025/26, Bangladesh completed four modern silos in Madhupur, Barishal, Mymensingh, and Narayanganj, lifting storage capacity to 2.388 million metric tons. Seven additional 50,000-metric-ton silo warehouses are under construction nationwide. These investments, together with procurement activity such as the May 2026 Boro season campaign that began May 3, 2026 targeting 1.2 million metric tons of rice, support opportunities for millers, logistics providers, and packaging players supplying into public procurement specifications, where better handling and standardized quality can reduce post-harvest loss.

On the production side, climate-smart intensification and mechanization programs create commercialization room for seed, equipment, and advisory services tied to yield stability and cost reduction. IRRI-led initiatives, including digital decision-support tools and climate-smart value chain programs, anchor adoption pathways for direct-seeded rice and mechanized establishment, including the 2024-2027 HSBC-funded Haor-region work integrating tools like Rice Crop Manager and Rice Doctor. Premiumization also stays investable within domestic channels, particularly aromatic and fortified rice, supported by ongoing fortification programs and regulatory emphasis on quality compliance. At the same time, import management measures and fast-track tenders keep trade-facing participants focused on compliance readiness and flexible sourcing during supply disruptions.

Recent Industry Developments

- May 2026: Bangladesh's Directorate General of Food began the Boro rice procurement campaign on May 3, 2026, targeting 1.2 million metric tons of rice for public stocks. The scale of procurement supports demand visibility for millers and aggregators that can meet government quality and delivery requirements, while strengthening the Public Food Distribution System during periods of price volatility.

- July 2025: ACI Limited received National Seed Board approval for new rice varieties, including an aromatic variety (ACI dhan2) and a short-duration, high-yielding variety (ACI dhan3). The approvals expand the portfolio of commercial seed options tied to premium aromatic demand and cropping-cycle flexibility, supporting upstream differentiation in a market that is sensitive to climate and seasonal supply shocks.

- June 2024: Bangladesh's government set a procurement price of Tk49 per kilogram for Boro rice. This intervention established a pricing anchor that influenced private trade and milling procurement, while signaling continued use of public purchasing to stabilize farmer incentives and consumer affordability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the total value of rice sold and consumed within Bangladesh across the supply chain that serves domestic demand, using consistent pricing and currency assumptions so the output stays comparable year to year.

Scope exclusions: It excludes rice produced in Bangladesh but sold outside the country, and it does not count non-rice staple substitutes.

Segmentation Overview

-

By Product Type

- Regular

- Aromatic

-

By Category

- White

- Brown

- Others

-

By Nature

- Organic

- Conventional

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/ Hypermarkets

- Convinience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic data spine for Bangladesh rice, before assumptions were stress-tested using field inputs. We mainly looked for repeatable public series that explain how much rice is produced, how much moves across borders, and what prices look like across seasons and years.

Sources used typically include official agriculture and food statistics from the Bangladesh Bureau of Statistics, crop and food outlook publications from FAO, trade and tariff statistics from UN Comtrade, and global macro indicators from the World Bank. We also referred to items such as policy notes and procurement updates published by relevant government departments, peer reviewed agronomy and food security papers, and credible press coverage to understand harvest timing, price spikes, and import duty changes. Company disclosures, investor presentations, and a paid subscription for company financials, news, and import and export shipment level checks were used selectively to validate directional movements. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to confirm how the market operates in practice, especially around pricing behavior, seasonal availability, and channel mix across Bangladesh. We spoke with a spread of stakeholders such as millers, distributors, large retailers, institutional buyers, and sector advisors, and we used these inputs to close data gaps and to sanity check the model outputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 18% | Managers: 44% | Americas: 20% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where production and trade data reconstruct the domestic rice availability, which is then converted into value using price indicators that reflect Bangladesh market realities. To keep the totals grounded, the result is corroborated with selective bottom-up approximations such as sampled price per kg times estimated channel volumes, plus distributor and retail channel checks, and then adjusted when the implied consumption looks inconsistent.

Key model inputs include paddy and rice production trends by season, yield and acreage direction, import and export quantities, wholesale and retail price trends, and government procurement and stock release signals that can tighten or ease market pricing. Where product mix matters, regular versus aromatic split and the shift across channels like traditional trade versus organized formats is treated as an input rather than an afterthought. For forecasting, scenario analysis is used so expected weather outcomes, input cost changes (fertilizer and fuel), and policy levers such as import duties are translated into demand and price paths. When any bottom-up check has missing pieces, we fill the gap using conservative ranges agreed in interviews and then re-test the totals against independent indicators.

Data Validation & Update Cycle

Validation is done through repeated triangulation of the modeled market value against independent signals, such as implied per capita availability, trade balance shifts, and the direction of domestic price indices. Outliers are flagged, the drivers are rechecked, and assumptions are tightened until the variance is explainable with real market events like harvest shocks or policy moves.

Before sign-off, the work goes through multi-step analyst review so the logic, units, and year mapping stay consistent. Reports are refreshed annually, and interim updates are triggered when material events occur, such as large import policy changes or unusual price inflation. Right before delivery, a final pass is completed so clients receive the most current view available in our model.

Mordor Intelligence's Bangladesh Rice Market Sizing Compared With Other Published Estimates

Published market values for Bangladesh rice can look far apart, even when everyone is studying the same country and staple. The differences usually come from what exactly is counted, which year is treated as the anchor, and whether the value is closer to farmgate, wholesale, or a more consumer-linked spend view.

By tracking production availability, trade inflows, and price series consistently, Mordor Intelligence keeps the estimate tied to domestic rice value in Bangladesh for 2025, while some sources lean on narrower category boundaries or different price points that pull the total down. Gaps also show up when a study mixes milled and paddy definitions without stating it clearly, uses a one-time price snapshot instead of season-aware averages, or applies currency conversion from a different timing that shifts USD values.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 44.96 B (2025) | |

| Global Consultancy A | USD 16.45 B (2024) | Uses a different base year and likely a tighter definition of rice value that can sit closer to a specific processing level or category scope, which can understate the broader domestic value captured in a season-linked pricing model. |

| Regional Consultancy B | USD 15.00 B (2024) | Presents a single point value with limited clarity on whether the pricing basis is farmgate, wholesale, or retail, and the scenario framing to 2030 does not show a transparent bridge from production and trade balance to value totals. |

The spread in the table is mainly explained by scope and pricing basis, plus base-year selection that shifts the starting point. A method that explicitly connects domestic availability, channel realities, and price behavior produces a balanced number that can be re-created and updated when new harvest, trade, or policy data is released.

Key Questions Answered in the Report

How large is the Bangladesh rice market in 2026?

It is valued at USD 46.73 billion with a 3.95% CAGR outlook to 2031.

Which rice category leads consumer preference in Bangladesh?

White rice leads with 84.95% share of 2025 demand because it aligns with traditional cooking practices.

What is driving premium rice demand?

Rising urban incomes and interest in aromatic, organic, and fortified grains are lifting the premium segment at a 5.74% CAGR.

How are online platforms changing rice distribution?

E-commerce channels are growing at a 5.38% CAGR, bundling rice with staples and improving last-mile delivery efficiency.

Page last updated on: