Hydrophilic Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

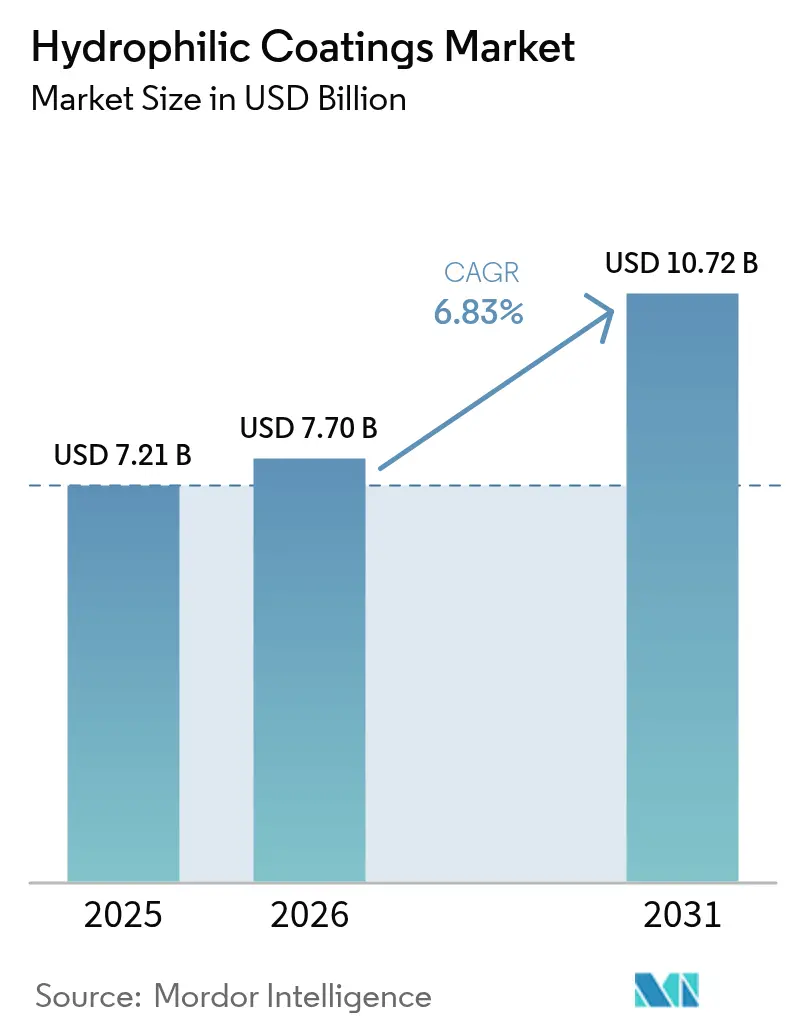

| Market Size (2026) | USD 7.70 Billion |

| Market Size (2031) | USD 10.72 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

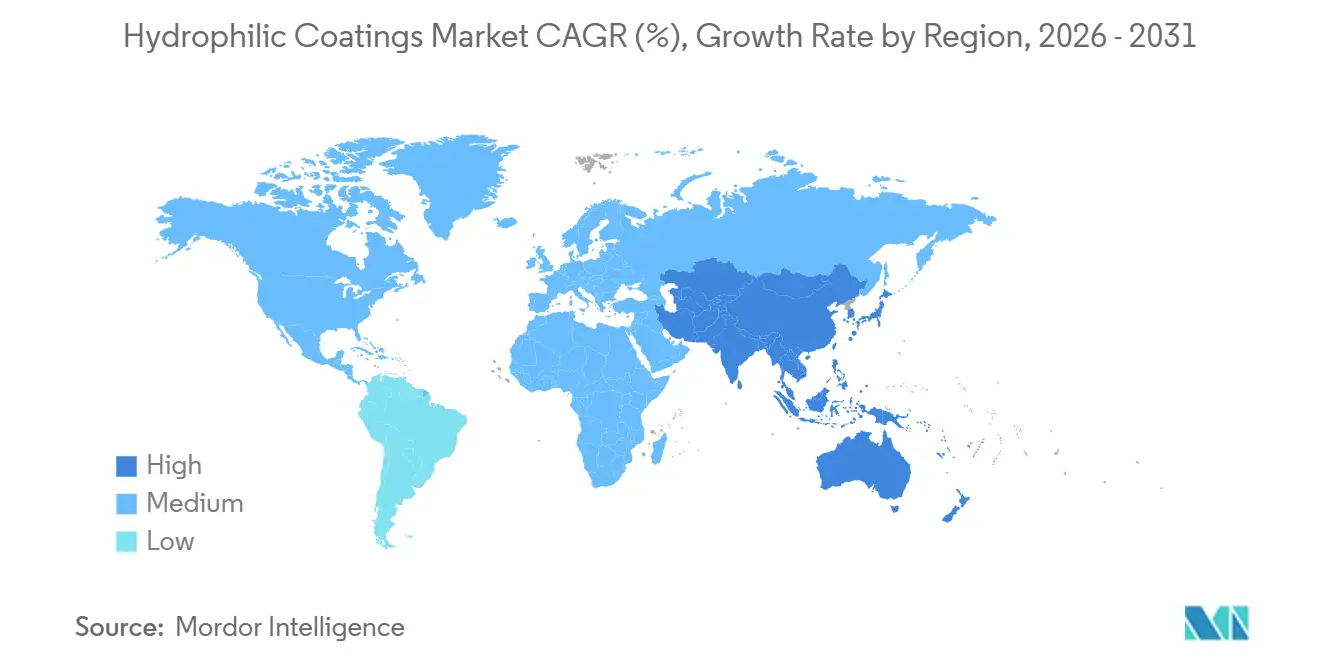

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrophilic Coatings Market Analysis by Mordor Intelligence

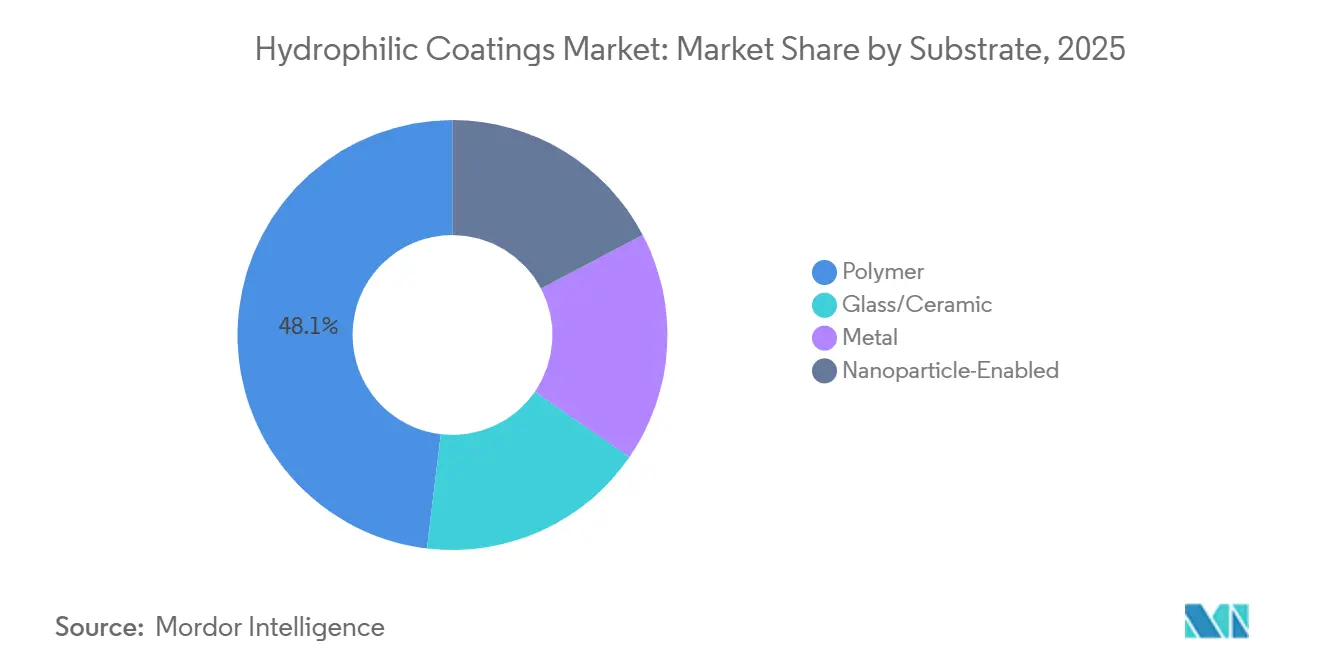

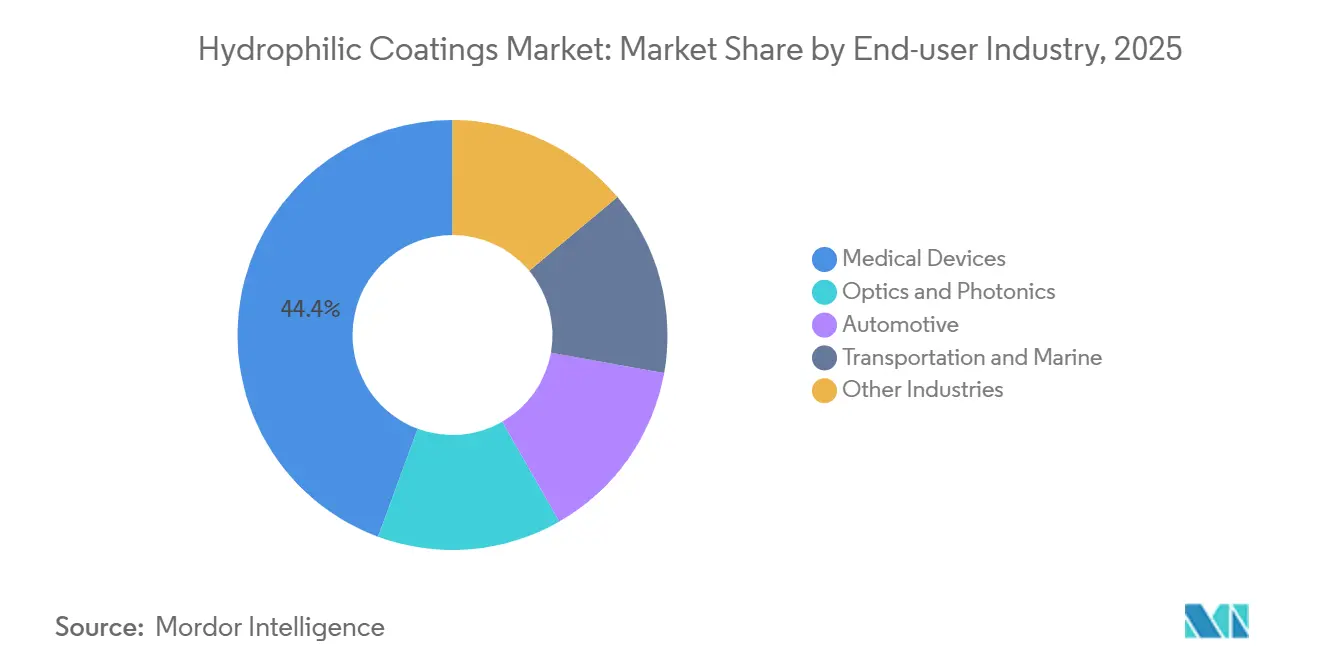

The Hydrophilic Coatings Market size is expected to increase from USD 7.21 billion in 2025 to USD 7.70 billion in 2026 and reach USD 10.72 billion by 2031, growing at a CAGR of 6.83% over 2026-2031. End-user demand is pivoting toward polymer substrates, which held a 48.11% share in 2025, as catheter and guidewire volumes keep rising. Regulatory moves that ban per- and polyfluoroalkyl substances (PFAS) in medical devices are accelerating a shift toward plasma and UV-graft deposition methods that enable PFAS-free chemistries. Nanoparticle-enabled surfaces are gaining traction in optical, electronics, and autonomous-vehicle sensor windows because they marry ultra-low friction with anti-fog performance. Asia-Pacific remains the fastest-growing regional consumer thanks to streamlined device approvals in China and Japan, while North American original-equipment manufacturers (OEMs) continue to shape global intellectual-property (IP) norms.

Key Report Takeaways

- By substrate, polymer surfaces commanded 48.11% of the Hydrophilic Coatings market size in 2025; nanoparticle-enabled substrates are set to expand at a 7.51% CAGR through 2031.

- By deposition technology, dip-coating maintained 41.45% revenue share in 2025, while plasma and UV-graft processes are projected to grow 7.42% annually to 2031.

- By application, catheters and guidewires led with 34.67% revenue share in 2025. However, stents and implantables will post the fastest 7.68% CAGR to 2031.

- By end-user industry, medical devices held 44.36% of the Hydrophilic Coatings market share in 2025 and will advance at a 7.83% CAGR to 2031.

- By geography, Asia-Pacific captured 33.12% of global revenue in 2025 and is forecast to grow 7.61% a year through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrophilic Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward VOC-free, water-borne and UV-cure chemistries | +1.2% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Expanding optical and electronics anti-fog lens demand | +1.4% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| AI-enabled endoscopy requiring low-friction sensor windows | +1.3% | North America & EU, early gains in Japan | Medium term (2-4 years) |

| Autonomous-vehicle LIDAR lens self-cleaning initiatives | +1.1% | North America, China, Germany | Long term (≥ 4 years) |

| Microfluidics-on-a-chip for point-of-care diagnostics | +0.9% | Global, concentrated in US and Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward VOC-Free, Water-Borne and UV-Cure Chemistries

Environmental rules that cap volatile-organic-compound emissions have pushed formulators to replace solvent-borne systems with water-borne dispersions or UV-cured networks that cross-link within seconds under 365-nanometer light. Over 60% of new hydrophilic formulations launched in 2025 complied with European Directive 2004/42/EC and the US Clean Air Act limits[1]European Commission, “Directive 2004/42/EC,” europa.eu. UV-cure solutions also safeguard heat-sensitive polymers such as polyurethane, cutting thermal deformation risks during production. From a cost angle, water-borne lines avoid solvent-recovery hardware, trimming capital outlay by up to USD 500,000 per coating line. However, slower ambient drying still hampers takt times in just-in-time catheter factories, so many OEMs integrate hybrid UV-flash stations to close the gap.

Expanding Optical and Electronics Anti-Fog Lens Demand

Wearable electronics vendors in Asia-Pacific embed superhydrophilic titanium dioxide nanofilms on lenses and waveguides to stop fog that appears during quick temperature swings. Contact angles below 5° force droplets to sheet into an invisible film, preserving pixel clarity for augmented-reality displays. Automotive rear-view cameras and autonomous-vehicle LIDAR (Light Detection and Ranging) domes apply similar coatings to sustain sensor accuracy in rain or snow, while building-integrated glazing uses hydrophilic outer panes to cut manual cleaning costs nearly in half. Plasma-deposited organosilicon stacks now survive more than 500 cleaning cycles, a durability threshold that dip-coated lenses rarely meet.

AI-Enabled Endoscopy Requiring Low-Friction Sensor Windows

Next-generation colonoscopy platforms from Medtronic and Olympus rely on AI to spot polyps in real time, demanding sensor windows with friction coefficients below 0.05 so that rapid insertion does not distort the image stream. UCLA (University of California, Los Angeles) researchers proved in 2025 that atmospheric-plasma grafting of sulfobetaine polymers can lock in ultra-low friction while resisting bile exposure for over eight hours. Clinical data show a 30% reduction in insertion force, shortening procedure times, and boosting adenoma detection without adding silicone lubricants that migrate into tissue.

Autonomous-Vehicle LIDAR Lens Self-Cleaning Initiatives

Automakers must keep 905-nanometer and 1,550-nanometer laser windows clear for reliable object detection. Tesla’s hardware applies hydrophilic nanofilms coupled with ultrasonic shakers, sustaining detection accuracy within 2% of lab benchmarks even in hard rain[2]Tesla Engineering Blog, “Sensor Cleaning Architecture,” tesla.com. Waymo patents a dual-layer stack, hydrophobic outside, hydrophilic inside, that slashes scheduled cleaning by 60%. Capital costs have dropped as new atmospheric-pressure plasma tools eliminate vacuum chambers, putting roll-to-roll coated domes within reach of tier-2 suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability and delamination under cyclic loads | -0.8% | Global, acute in high-volume medical device manufacturing | Short term (≤ 2 years) |

| PFAS-free raw-material transition risk | -0.6% | North America & EU, regulatory spill-over to APAC | Medium term (2-4 years) |

| IP clustering blocking new entrants in medical OEM tier-I | -0.4% | Global, concentrated in US and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Durability and Delamination Under Cyclic Loads

Guidewires often fail ASTM D6677 flex tests after only 50 insertion-retraction cycles if adhesion promoters do not raise surface energy above 45 mN/m. Inline plasma activation fixes the issue but forces manufacturers to coat within hours because hydrophobic recovery erodes surface polarity. Installing continuous-flow plasma tunnels that cost USD 150,000 - 300,000 allows statistical process control of energy levels, yet throughput pressure can still shorten exposure times below the five-second optimum, causing sporadic delamination.

PFAS-Free Raw-Material Transition Risk

The US Environmental Protection Agency’s 2024 rule bans PFAS in medical devices from 2026 onward, obliging formulators to switch to alkyl-polyglucoside surfactants that lift contact angles by 6-10°, reducing anti-fog clarity by up to 20%. Re-qualifying ISO 10993 biocompatibility costs between USD 50,000-100,000 per blend and delays launches by as much as a year. Supply chains also narrow; only a handful of suppliers offer cold-chain zwitterionic monomers, pushing raw-material premiums into the 10-15% range.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Polymer Uptake Dominates Medical Devices

Polymer surfaces accounted for 48.11% of 2025 revenue as low-modulus catheters, guidewires, and sheaths rely on lubricious coatings that cut insertion force by up to 60%. Glass and ceramic panes continue to serve optics, solar, and aerospace niches that need high thermal stability, while nanoparticle-enabled variants are forecast to clock a 7.51% CAGR during the forecast period (2025-2031) on the back of self-cleaning LIDAR and AR visor demand. Titanium-dioxide-doped polymer blends yield superhydrophilicity that standard films cannot reach, supporting next-gen diagnostic sensors.

The Hydrophilic Coatings market size for nanoparticle coatings is on track for growth, reflecting rapid adoption in autonomous-vehicle optics. Metal substrates retain a single-digit share, but novel halogen-free primers launched in 2025 by AGC Plasma now post peel strengths above 1.5 N/25 mm, encouraging stent and guidewire makers to revisit stainless or nitinol designs without PFAS primers.

By Deposition Technology: Plasma & UV-Graft Gain Momentum

Dip-coating still held 41.45% share in 2025 because a basic line costs under USD 100,000 and supports billion-unit catheter runs. Yet plasma and UV-graft stations will grow 7.42% per year during the forecast period (2026-2031) owing to near-zero solvent use, better lumen coverage, and easy pivot to PFAS-free recipes. Plasma-enhanced chemical-vapor deposition now runs at atmospheric pressure, slicing 40-60% from tool capital versus legacy vacuum chambers, a breakthrough HZO captured in a 2025 patent set.

Hydrophilic coatings market share for plasma technologies is poised to reach the mid-30% range by 2031 as inline curing aligns with high-speed extrusion lines. UV-graft units add only nanometers of cross-linked polymer yet deliver covalent bonding that endures 500 autoclave cycles at 121°C, meeting reusability benchmarks for endoscope optics. Spray and slot-die remain popular for architectural sheets that move through float-glass plants at meters-per-second speeds.

By Application: Stents & Implantables Lead Growth Curve

Catheters and guidewires contributed 34.67% of 2025 sales, but stents and implantables are projected to be the fastest riser, with a 7.68% CAGR into 2031. Zwitterionic grafts on drug-eluting stents cut platelet adhesion enough to shorten dual-antiplatelet therapy to three months, a benefit echoed in multiple 510(k) clearances granted in 2025. Optical lenses for AR headsets and safety glasses form a vibrant secondary market as consumer gear requires fog-free clarity across indoor-outdoor transitions.

Automotive sensors and cameras represent a white-space niche that blends self-cleaning films with active vibration modules for higher sensor uptime in adverse weather. Architectural glazing continues to leverage photocatalytic titania sol-gel stacks to keep skyscraper facades cleaner for longer.

By End-User Industry: Medical Devices Remain Prime Consumer

Medical devices already capture 44.36% of 2025 revenue and should outpace all other user groups at a 7.83% CAGR during the forecast period (2026-2031). Hospital demand for PFAS-free, infection-control-ready catheters aligns with tightening procurement rules under the US Centers for Medicare and Medicaid Services, which withholds reimbursement for avoidable bloodstream infections. Optics and photonics come second, fueled by head-mounted displays, lab instruments, and machine-vision rigs that must keep lenses clear without external heaters.

The Hydrophilic Coatings market share for automotive uses is small today but climbing steadily as LIDAR mandates appear in draft European and Chinese safety rules for 2028. Marine and transportation fleets adopt photocatalytic windows that de-salt and de-fog without wipers, trimming maintenance hours on offshore rigs by up to 70%. Surmodics logged USD 9.383 million in Serene revenue for Q1 FY 2025, a 14% rise year on year, highlighting sustained cardio-vascular demand.

Geography Analysis

Asia-Pacific delivered 33.12% of 2025 turnover because China’s National Medical Products Administration shaved device approval cycles to 12-16 months, encouraging local coating plants to scale. Regional CAGR is pegged at 7.61% through 2031 as catheter OEMs in Suzhou and Shenzhen pair with Japanese plasma-equipment builders to roll out PFAS-free lines. South Korean handset and AR-wearable firms deploy superhydrophilic nanofilms on camera modules, while India’s catheter imports jumped above 20% during 2025, owing to higher cardiovascular case loads.

North America stands second by value, anchored by OEM clusters in Minnesota and Massachusetts that collectively hold more than 40% of global interventional-device revenue. The Environmental Protection Agency’s 2026 PFAS ban is catalyzing early adoption of alternative surfactants, a compliance edge US firms hope to leverage overseas. Canada’s winter-testing fleets trial hydrophilic LIDAR domes against freezing rain and road salt, while Mexico’s maquiladora corridor adds new plasma cabins to serve cross-border guidewire assembly.

Europe’s Medical Device Regulation and REACH statutes tighten material disclosures, nudging suppliers toward vertically integrated operations that combine in-house compounding and full biocompatibility suites. German automakers refine dual-layer sensor windows at research and development hubs in Bavaria, and the United Kingdom’s National Health Service favors hydrophilic catheter sets that cut infection risks on vascular wards. France’s aerospace majors layer cockpit windows with anti-icing hydrophilic coatings to lower electrical-de-icing power draw at altitude, and Italian eyewear brands integrate anti-fog stacks on frames sold to mask-wearing industrial users.

Competitive Landscape

The Hydrophilic Coatings market is moderately consolidated. The hydrophilic coatings industry is in a transition phase as atmospheric-pressure plasma tools undercut vacuum capital by up to 60%, opening the door for mid-tier firms. Future differentiation will hinge on balancing fog elimination, durability beyond one million cycles, and ISO 10993 cytotoxicity tolerances. Automotive giants seek coast-to-coast warranties on sensor uptime, pushing the field toward predictive maintenance models that pair surface-energy IoT tags with cloud analytics.

Hydrophilic Coatings Industry Leaders

Surmodics, Inc.

Harland Medical Systems, Inc.

Biocoat Incorporated

AST Products, Inc.

Specialty Coating Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Freudenberg Medical unveiled LUBRITEQ, its latest high-performance hydrophilic coating solution, complemented by an extensive range of development and manufacturing services.

- January 2026: Formacoat unveiled HydroMark, its proprietary hydrophilic coatings platform, signifying a pivotal shift for the company from merely offering contract coating applications to emerging as a trailblazer in comprehensive coating services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hydrophilic coatings market as the annual value of specialty, water-attracting surface finishes applied to new medical devices, optics, automotive glass, aerospace skins, and marine parts that improve lubricity, anti-fog, and bio-compatibility. We account for factory-applied polymer, glass, metal, and nanoparticle-enabled films supplied by coating formulators as well as in-house OEM lines across all regions.

Scope Exclusions: We purposely leave out hydrophobic, antifouling, and broader multifunctional paint systems that lack permanent hydrophilicity.

Segmentation Overview

- By Substrate

- Polymer

- Glass / Ceramic

- Metal

- Nanoparticle-Enabled

- By Deposition Technology

- Dip-Coating

- Spray and Slot-Die

- Plasma and UV-Graft

- Chemical Vapor Deposition

- Other Technologies

- By Application

- Catheters and Guidewires

- Stents and Implantables

- Optical and Eyewear Lenses

- Automotive Sensors and Cameras

- Architectural and Solar Glass

- Others (Marine, Textile, Aerospace)

- By End-User Industry

- Medical Devices

- Optics and Photonics

- Automotive

- Transportation and Marine

- Other Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview coating formulators, catheter assemblers, optical component buyers, and procurement heads across North America, Europe, and Asia. These discussions validate average selling prices, substrate penetration shifts, and emerging regulations, while short surveys of hospital supply managers reveal real-world usage rates and re-order triggers.

Desk Research

We first build a fact base from open datasets, trade flows in the UN Comtrade portal, U.S. FDA 510(k) device clearances, Eurostat production indices, and patent families mined through Questel. Industry ratios are enriched with domain associations such as the Medical Device Innovation Consortium, American Coatings Association, and Japan Paint Manufacturers Federation. Annual reports, investor decks, and tender notices captured via Dow Jones Factiva and D&B Hoovers round out pricing and capacity clues. The sources listed illustrate the breadth we tap; numerous other public records underpin additional checks and clarifications.

A second sweep tracks resin cost curves, single-use catheter shipments, and regional procedure volumes released by bodies like the OECD Health Directorate, giving us granular demand fingerprints.

Market-Sizing & Forecasting

We start with a top-down reconstruction of global demand using production and trade data, which are then calibrated with selective bottom-up supplier roll-ups and sampled ASP × volume checks. Key variables like interventional cardiology procedure counts, polymer film conversion yields, average dip-coat layer thickness, and propylene glycol price trends feed a multivariate regression that projects value through 2030. Gap pockets in bottom-up inputs are bridged with primary confirmed load factors and regional adjustment coefficients.

Data Validation & Update Cycle

Every model iteration passes a three-layer review: automated variance scans, senior analyst logic checks, and sector lead sign-off. Reports refresh yearly, with interim updates triggered by material events such as major regulatory approvals or raw material price swings. A last-mile review occurs just before client delivery, ensuring numbers remain current.

Why Mordor's Hydrophilic Coatings Baseline Deserves Confidence

Published estimates often diverge because firms pick differing substrate groups, apply varied ASP ladders, or stretch forecast horizons. Our disciplined scope and annually refreshed variables minimize these misalignments.

Key gap drivers include certain publishers bundling non-hydrophilic functional coatings, others inflating value by applying list rather than realized prices, and still others modeling on outdated surgical procedure counts. By contrast, Mordor's cadence, scope purity, and dual-path validation keep the baseline grounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.09 B (2025) | Mordor Intelligence | - |

| USD 19.94 B (2025) | Global Consultancy A | Includes hydrophobic and antimicrobial films; employs list pricing |

| USD 17.83 B (2024) | Regional Consultancy B | Uses broad chemicals trade code without device-level filtration |

| USD 16.8 B (2022) | Trade Journal C | Relies on aging production baseline and five-year-old ASPs |

In sum, our approach gives decision-makers a transparent, reproducible baseline that traces each dollar to clear variables and real-world cross-checks, letting users plan with confidence.

Key Questions Answered in the Report

What CAGR is forecast for hydrophilic coatings from 2026-2031?

The market is projected to grow at a 6.83% CAGR during the period (2026-2031) and reach USD 10.72 billion by 2031 from USD 7.70 billion in 2026..

Which substrate segment is growing the fastest?

Nanoparticle-enabled substrates are expected to expand at a 7.51% CAGR through 2031.

Why are plasma and UV-graft methods gaining share?

They eliminate PFAS, cut solvent waste, and deliver uniform coverage on complex geometries.

Which region leads growth?

Asia-Pacific shows the highest regional CAGR at 7.61% to 2031.

What is the main regulatory headwind?

A 2026 US ban on PFAS in medical devices forces reformulation and re-qualification efforts.

Page last updated on: