Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Packaging Coating Additives Market Report is Segmented by Formulation (Water-Based, Solvent-Based, and Powder-Based), Function (Slip, Anti-Static, Anti-Fog, and More), Application (Food & Beverage, Healthcare, and More), Substrate Material (Plastic Films, Glass, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

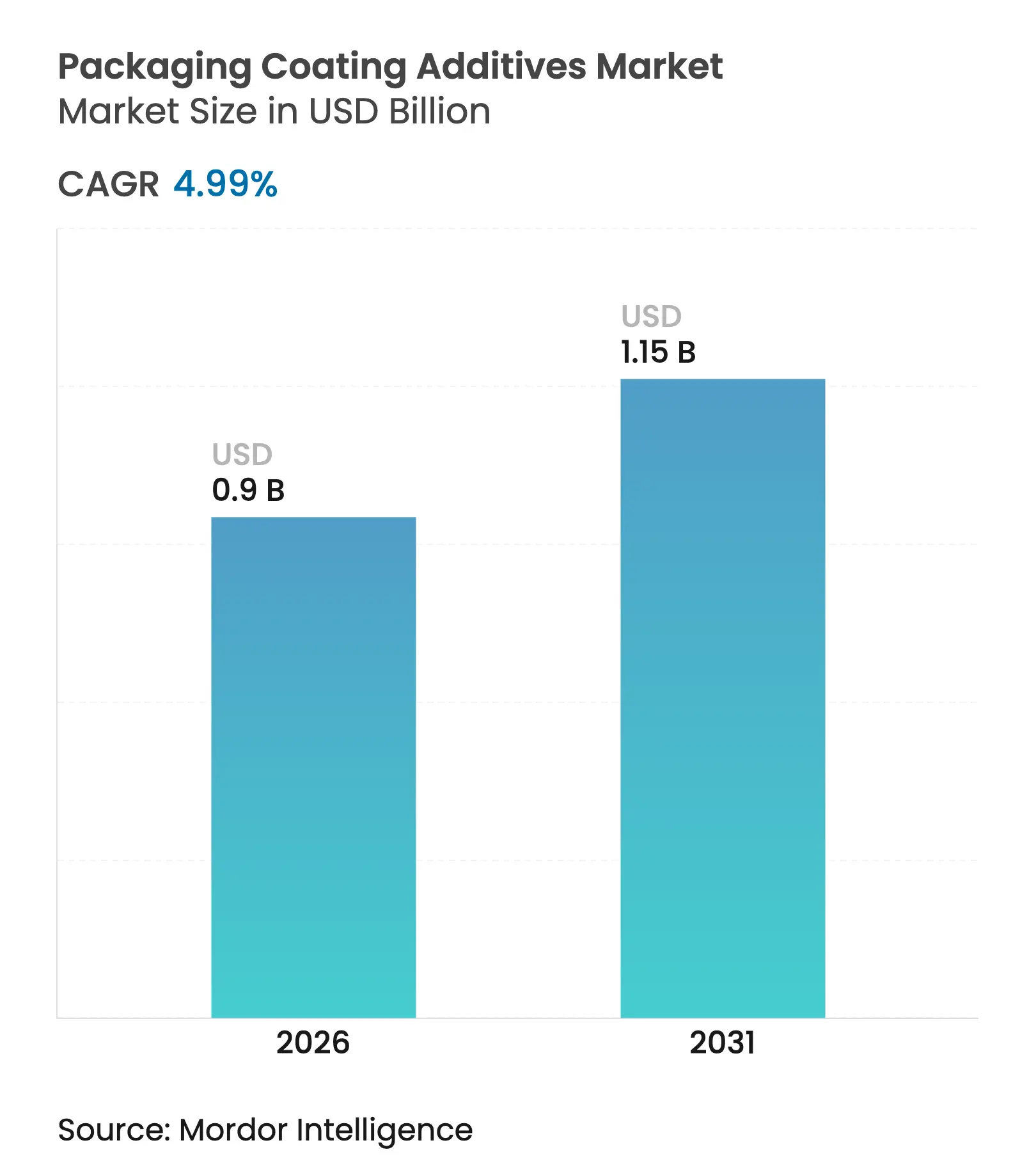

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 4.99 % CAGR |

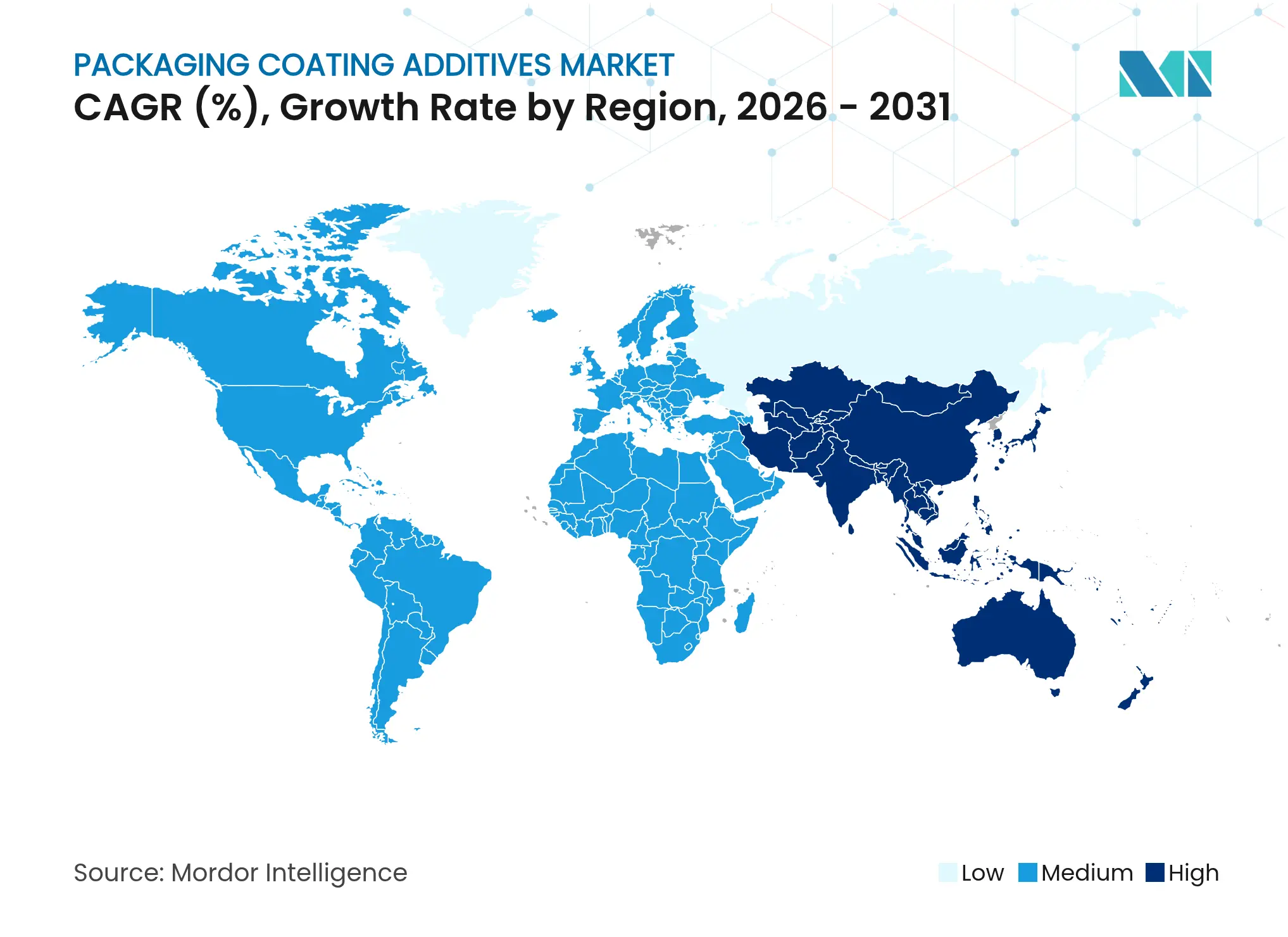

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

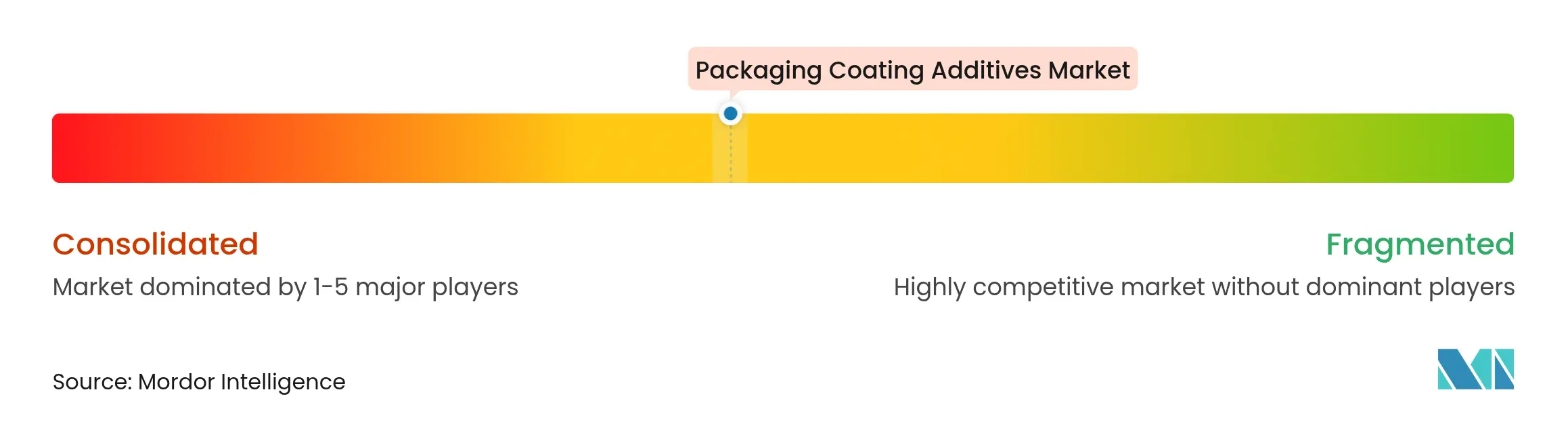

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Packaging Coating Additives Market size was valued at USD 0.86 billion in 2025 and estimated to grow from USD 0.9 billion in 2026 to reach USD 1.15 billion by 2031, at a CAGR of 4.99% during the forecast period (2026-2031). Rising demand for hygienic, visually appealing, eco-friendly packs across food, beverage, healthcare, and consumer goods channels reinforces the growth trajectory. Regulatory momentum favoring water-based technologies, combined with the rapid rollout of antimicrobial solutions, reshapes product portfolios and accelerates material substitution. Manufacturers are scaling bio-based chemistries to ease volatile organic compound (VOC) restrictions without sacrificing barrier or slip performance. At the same time, e-commerce logistics and cold-chain expansion are expanding the addressable opportunity, particularly for anti-fog and antimicrobial offerings. Strategic mergers and acquisitions (M&A) activity redefines competitive positioning as firms seek geographic reach, feedstock security, and next-generation research and development (R&D) talent.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Demand in Food & Beverages Packaging Growing Demand in Food & Beverages Packaging | + 1.2% | Global, with APAC core markets leading | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+ 1.2% |

Geographic Relevance

:Global, with APAC core markets leading |

Impact Timeline

:Medium term (2-4 years) |

Expansion of Industrial Bulk Packaging Expansion of Industrial Bulk Packaging | + 0.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) | |||

E-commerce Cold-chain Spurring Anti-fog & Antimicrobial Additives E-commerce Cold-chain Spurring Anti-fog & Antimicrobial Additives | + 0.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) | |||

Growth of Personal Care and Cosmetics Industry Growth of Personal Care and Cosmetics Industry | + 0.5% | North America, Europe, and premium APAC segments | Medium term (2-4 years) | |||

Enhanced Aesthetic and Printability Requirements Enhanced Aesthetic and Printability Requirements | + 0.4% | Global, with premium market focus | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Demand in Food & Beverages Packaging

The packaged food boom is elevating additive functionality expectations, with shelf-life extension and pathogen control now baseline requirements. Emerging economies, buoyed by rising disposable incomes, present sizeable volume upside and favor cost-effective water-based systems that comply with stricter food-contact codes. Regulatory bodies, especially in the European Union, are mandating antimicrobial and barrier credentials that previously were optional, prompting formulators to integrate multi-functional chemistries into single coatings. Partnerships such as Dow’s work with Procter & Gamble on dissolution-enabled recycling show how sustainability and safety are converging in additive design [1]Dow, “Dow and P&G Advance Dissolution Technology Collaboration,” dow.com. As a result, premium water-borne packages that meet VOC and hygiene standards are gaining purchasing preference across supermarket chains and online grocery platforms.

Expansion of Industrial Bulk Packaging

Chemical, agro, and pharmaceutical producers are switching to bulk formats that reduce logistics costs yet impose higher stress on packaging surfaces. This behavior ignites demand for slip and anti-block additives that eliminate scuffing and adhesion during automated handling. Investments in warehouse robotics intensify the need for a consistent coefficient of friction, driving suppliers to refine wax, silicone, and polyethylene-based formulations for thicker films and rigid containers. Asia-Pacific is hosting new additive dispersion plants to align output with end-user migration, while North American converters focus on premium high-purity grades for hazardous contents. Cost-down pressures also motivate formulators to integrate performance boosters that tolerate recycled resins without diminishing line throughput.

E-commerce Cold-chain Spurring Anti-fog & Antimicrobial Additives

Direct-to-consumer grocery and temperature-sensitive pharmaceutical shipping have multiplied cold-chain touchpoints, making package clarity and microbiological integrity critical for brand trust. Anti-fog agents preserve visibility under cyclical humidity, whereas antimicrobial coatings inhibit spoilage and cross-contamination. Brands catering to online shoppers treat packaging as a customer-experience node, prompting innovation in clear, printable films that resist condensation. Early adopters in North America and Europe demonstrate revenue spikes linked to premium cold-chain compliance, fueling replication across emerging markets adapting to rising urban e-commerce penetration. These dynamics accelerate the pivot to hydrophilic polymers and bio-derived surfactants that fulfil performance and Environmental, Social, and Governance (ESG) scorecards.

Growth of Personal Care and Cosmetics Industry

High-end skincare and color-cosmetic lines depend on tactile and visual differentiation, encouraging coating additives that enhance gloss, metallic shimmer, or matte uniformity while safeguarding sensitive formulations. Premium labels re-evaluate substrate choices, integrating bio-content or post-consumer recycled (PCR) plastic but demanding identical ink adhesion and abrasion resistance. Additive producers liaise with design houses to co-develop texture-enabling dispersions, such as silica-based matting agents blended with slip modifiers for airless pumps. Consumer prioritization of clean-label packaging steers the adoption of solvent-free dispersions that meet cruelty-free and vegan certifications. Regulatory scrutiny of microplastic shedding further stimulates research and development (R&D) programs to engineer degradable particles without compromising haptic appeal.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent Global VOC & Plastics Regulations Stringent Global VOC & Plastics Regulations | -0.9% | Global, with EU and California leading | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.9% |

Geographic Relevance

:Global, with EU and California leading |

Impact Timeline

:Short term (≤ 2 years) |

Raw-material Price Volatility Raw-material Price Volatility | -0.8% | Global, with emerging markets most affected | Short term (≤ 2 years) | |||

PFAS Phase-outs Curbing Fluorinated Slip Additives PFAS Phase-outs Curbing Fluorinated Slip Additives | -0.7% | North America & Europe, expanding globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Global VOC & Plastics Regulations

Tightening emission caps and single-use plastic bans raise compliance costs and prolong validation cycles for solvent-based coating recipes. The European Union’s VOC ceilings and California’s Air Resources Board standards impose immediate reformulation on converters reliant on high-solid or solvent-borne systems. Original Equipment Manufacturers (OEMs) invest in transition audits and pilot runs to qualify water-based or powder formats, yet these alternatives can demand longer cure windows. Certification agencies mandate exhaustive migration and odor testing, extending time-to-market for novel chemistries. Capital expenditure for capture and abatement upgrades diverts budgets from growth initiatives, moderating near-term adoption rates.

PFAS Phase-outs Curbing Fluorinated Slip Additives

Global regulators are outlawing per- and polyfluoroalkyl substances because of persistence and toxicity concerns, eliminating a class of additives revered for low surface energy and release properties. Coaters scramble to replace established fluorinated waxes with non-fluorinated analogs that achieve similar coefficient of friction reduction. Clariant’s PFAS-free Ceridust 8170 M and AddWorks PPA range illustrate how technical pivot is achievable, yet qualification pathways remain rigorous for medical or food contact applications [2]Clariant, “Clariant Introduces PFAS-Free Additive Portfolio,” clariant.com. Smaller suppliers lacking polymer research depth risk market exit, consolidating demand around multinationals prepared to finance lengthy toxicology trials.

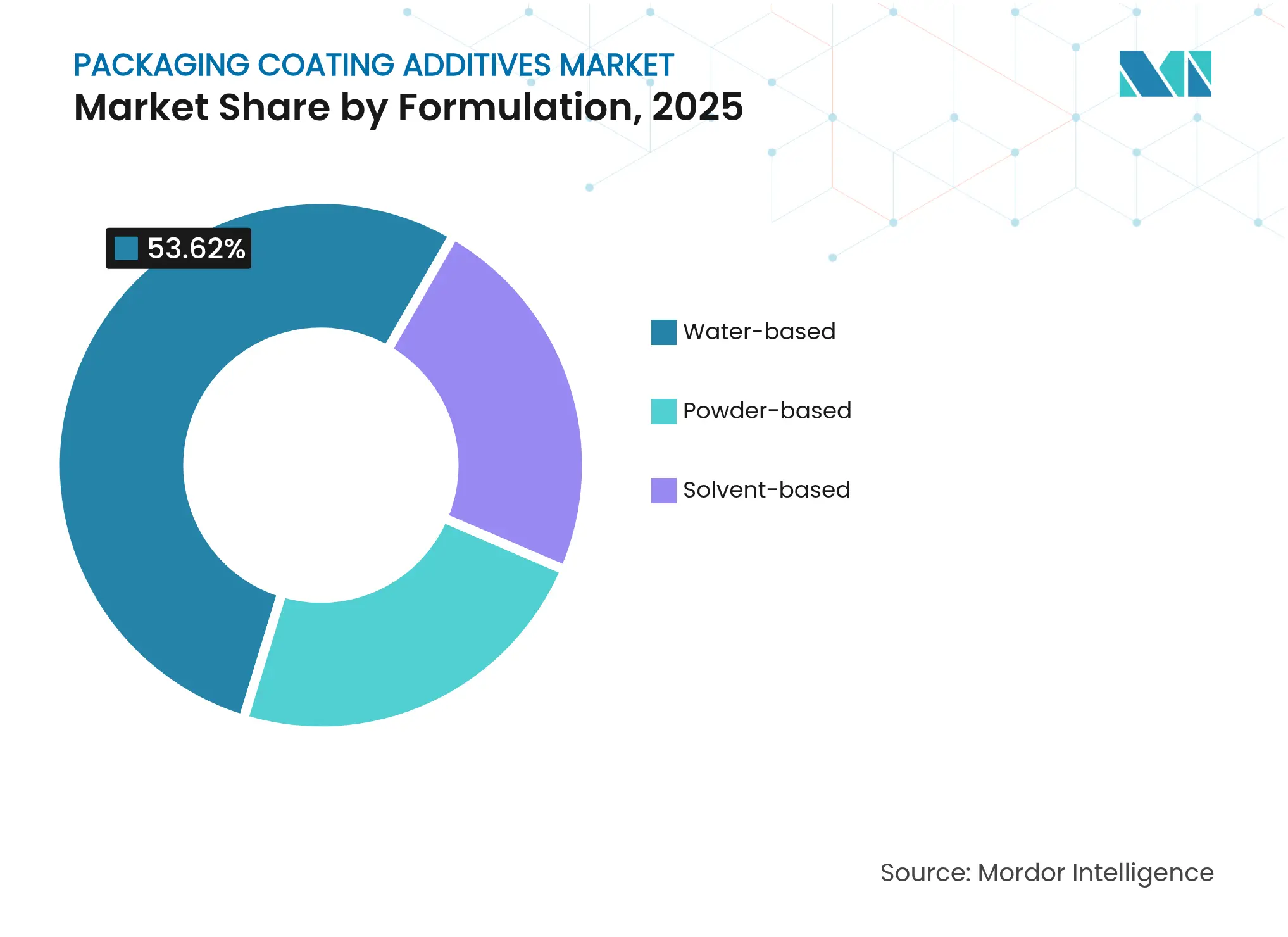

By Formulation: Water-Based Solutions Drive Regulatory Compliance

Water-based products accounted for 53.62% of the Packaging Coating Additives market share in 2025 and are expanding at 5.72% CAGR, mirroring intensified enforcement of VOC caps and brand sustainability mandates. Volatile legislation gaps are closing across Asia-Pacific as policymakers emulate European norms, making solvent-borne migration less viable. Continuous resin innovation, especially self-crosslinking acrylics, narrows performance disparities once favoring solvent grades. Powder-based systems grow from a niche base by offering solvent-free processing hygiene, although capital requirements for electrostatic lines limit uptake to high-volume converters.

Broader adoption of water-based dispersions correlates with brandowner commitments to Science Based Targets and plastics pacts that penalize high-VOC footprints. Formulators integrate low-foaming surfactants and carbodiimide crosslinkers to overtake legacy adhesion benchmarks. Stahl’s 2025 Hypac series demonstrates tensile and heat resistance improvements once considered exclusive to solvent epoxy networks. Meanwhile, solvent-based coatings, such as metal drum interiors, survive where abrasion, oil, or chemical exposure extremes prevail. Hybrid strategies involving water-bornes for outer artwork and solvent polysiloxanes for inner linings balance compliance with durability needs.

Note: Segment shares of all individual segments available upon report purchase

By Function: Antimicrobial Growth Outpaces Traditional Slip Applications

Slip agents held 36.21% market weight in 2025 due to entrenched film extrusion demand, yet antimicrobial additives capture the fastest CAGR at 5.64% through 2031 on the back of post-pandemic hygiene vigilance. Hospitals and cold-chain grocers pursue coatings that can inhibit bacterial growth between factory fill and end-use, adding premium value above basic process aids. Anti-fog agents witness renewed momentum thanks to transparent meal kits and vaccine vials shipped under fluctuating temperatures, while anti-static materials remain essential for electronics fillings.

Multi-functional grades that merge slip, anti-block, and antimicrobial traits into a single dispersion are gaining currency, simplifying inventories and offsetting cost premiums. Nanotechnology leverages silver-ion or zinc-oxide carriers in food-contact compliant matrices that release ions gradually, balancing efficacy with migration limits. Anti-block additives shift toward mineral blends with engineered particle geometry to minimize haze on thinner gauges. “Other functions,” such as defoamers and rheology modifiers, register steady demand as converters optimize high-speed lamination lines, supporting broader functional ecosystem value.

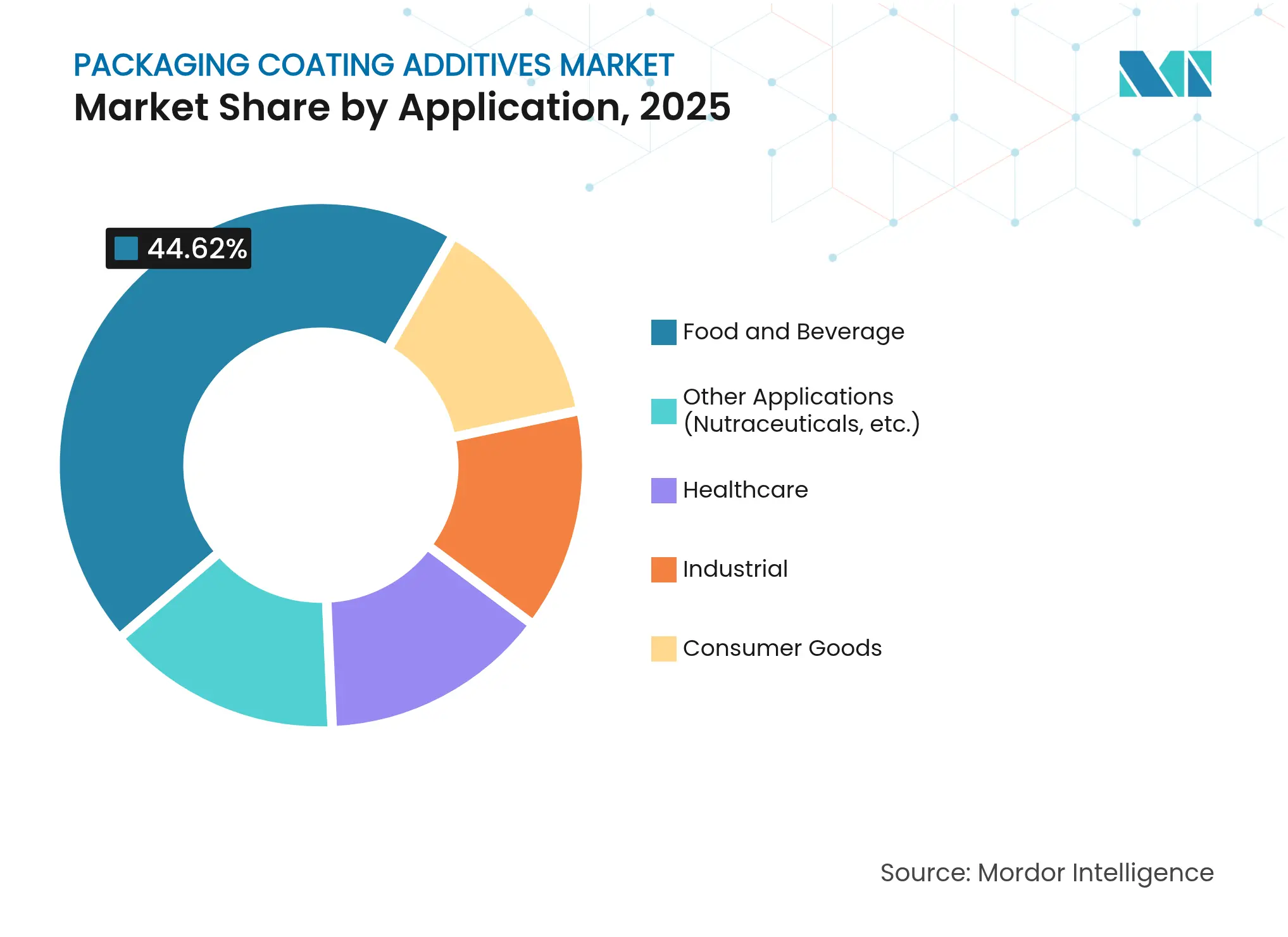

By Application: Healthcare Drives Premium Growth Despite Food Dominance

Food and beverage retained 44.62% of the Packaging Coating Additives market size in 2025, supported by constant stock-keeping unit (SKU) proliferation and fresh-produce growth. Packagers integrate oxygen scavengers with antimicrobial agents to extend shelf life, especially for ready-to-eat meals. Industrial applications hinge on bulk shipments of hazardous or high-purity goods, stressing film strength and lubricity for drum liners and flexible intermediate bulk containers (FIBCs).

Healthcare, while smaller in base value, is accelerating at 5.81% CAGR as pharma cold-chain and medical device sterility standards tighten. International Organization for Standardization (ISO) 11607 protocols require traceable, low-leach additives that pass accelerated aging and Ethylene Oxide (ETO) sterilization tests. Manufacturers co-create formulations with drug developers to avoid extractable interference, commanding price premiums. Consumer goods categories such as personal care capitalize on visual and texture cues that justify higher additive budgets despite lower barrier needs. Cross-pollination arises when antimicrobial systems proven in medical pouches migrate into deli meats or infant nutrition pouches, broadening revenue horizons.

Note: Segment shares of all individual segments available upon report purchase

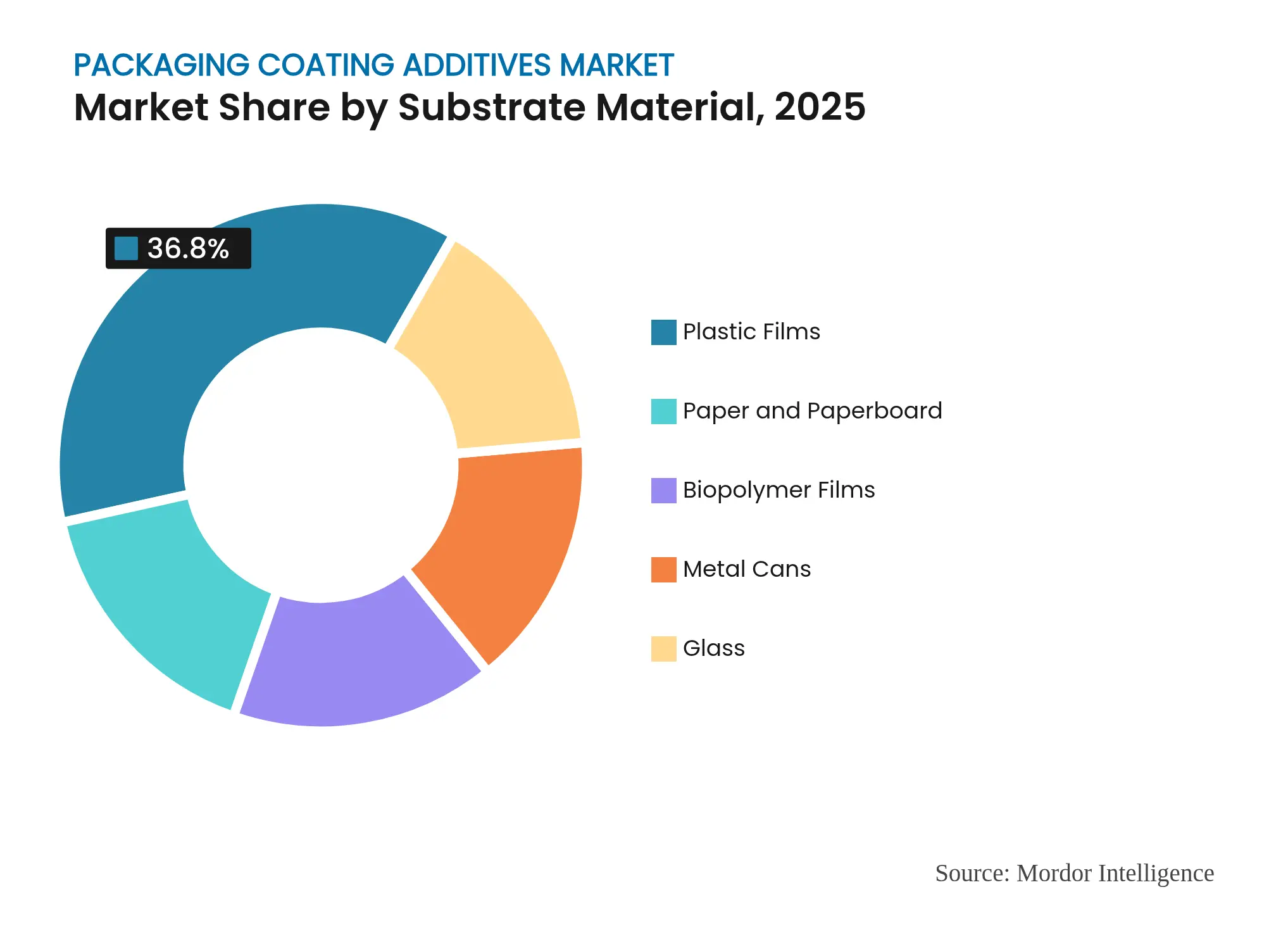

By Substrate Material: Paper Innovation Challenges Plastic Film Dominance

Plastic film represented 36.80% market share in 2025, anchored by cost, sealing versatility, and well-established supply chains. Nevertheless, paper & paperboard solutions are charting a 5.34% CAGR as brand owners commit to fiber-based formats for curbside recyclability claims. Coating additives address paper’s porosity and moisture barrier deficits, enabling functional parity with polyolefin laminates. BYK-Chemie’s BYKO2BLOCK-1200 improved Polylactic acid (PLA) gas impermeability by more than 30%, equipping bio-films to vie for snack, produce, and personal care wrap opportunities.

Metal cans rely on corrosion-resistant epoxy and polyester layers enhanced by slip wax dispersions that ease filling efficiency. Demand remains steady in beverage and aerosol lines, with per- and polyfluoroalkyl substances (PFAS) replacement a near-term priority. Glass substrates employ surface modifiers to increase scratch resistance and label adhesion. Biopolymer films emerge as a strategic play for retailers transitioning from fossil plastics, yet their cost structure necessitates additive packages that reinforce puncture resilience and heat seal thresholds.

Note: Segment shares of all individual segments available upon report purchase

Asia-Pacific controlled 39.51% Packaging Coating Additives market size in 2025 and is progressing at 5.46% CAGR as governments promote domestic value addition and global Foreign Direct Investment (FDI) targets processing hubs in China, India, and Southeast Asia. Local converters scale capacity to serve expanding food, beverage, and personal care manufacturing clusters. Regional authorities adopt European Union (EU)-style plastics directives, prompting early water-based conversion and PFAS substitution, which favors suppliers with proven compliant chemistries. In India, incentives for pharma and medical device parks contribute to upticks in sterile packaging additive orders.

North America exhibits a mature yet innovation-intensive profile. United States brand owners focus on premium cold-chain, advanced recycling compatibility, and carbon-label claims, rewarding additive vendors that validate Life Cycle Assessment gains. Mexico’s near-shoring trend lures investment in flexible packaging plants equipped with energy-efficient curing lines that default to low-VOC dispersions. Canada’s single-use plastics regulation accelerates the shift from solvent lacquers to aqueous primers for fiber-based cups, prompting joint trials among pulp mills, coating formulators, and quick-service restaurant chains.

Europe remains a bellwether for environmental rule-making and circular economy policy. Germany and France intensify Extended Producer Responsibility fees tied to recyclability indices, nudging pack owners to adopt mono-material laminates enhanced by new-generation water-borne coatings. Dow, Henkel, and Kraton reduced adhesive carbon intensity by 25% by deploying bio-based feedstocks, illustrating supplier collaboration to meet EU Green Deal benchmarks. Nordic states pioneer deposit schemes for flexible pouches, creating return on investment (ROI) for high-barrier paper structures additives. Eastern Europe offers capacity for contract converting, leveraging lower labor costs while adhering to common EU technical standards.

Markets in South America and the Middle East & Africa contribute modest value, but infrastructure upgrades in chilled logistics and growing urban populations foreshadow wider additive penetration. Brazilian converters experiment with tropical-climate-resistant anti-fog coatings, whereas Gulf petrochemical giants explore backward integration opportunities into specialty wax dispersions to leverage captive feedstock.

Market Concentration

The Packaging Coating Additives market features moderate consolidation, with diversified chemical majors such as BASF, ALTANA Group, Arkema, and Clariant AG leveraging extensive R&D bases and integrated feedstock positions. These leaders allocate robust budgets to PFAS-free, bio-based, and multifunctional technologies to stay ahead of shifting compliance landscapes. Mid-sized specialists carve niches in high-purity, region-specific, or performance-critical segments. Raw material volatility remains a primary risk as crude-linked feedstocks fluctuate. Suppliers possessing backward integration or multi-sourcing agreements mitigate margin compression. Digital formulation platforms and AI-driven simulation shorten development loops, offering a first-mover edge.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Packaging coating additives are crucial components that enhance the performance and lifespan of packaging materials. These additives, including anti-fog, antimicrobial, slip, and anti-static agents, modify the surface properties of packaging materials, enabling them to withstand external factors like heat, light, moisture, and mechanical stress. Packaging coating additives are extensively used in the food and beverage, pharmaceutical, cosmetic, and consumer goods industries. They contribute to safeguarding product safety, quality, and longevity. Additionally, they improve the strength and durability of packaging materials, provide resistance to wear and tear, and extend shelf life.

The packaging coating additives market is segmented by formulation, function, application, and geography. By formulation, the market is segmented into water-based, solvent-based, and powder-based. By function, the market is segmented into slip, anti-static, anti-fog, antimicrobial, and anti-block. By application, the market is segmented into food and beverage, industrial, healthcare, consumer goods, and other applications (nutraceuticals). The report also covers the market size and forecasts for the packaging coating additives market in 15 countries across major regions.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.