Defoaming Coating Additive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 2.61 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

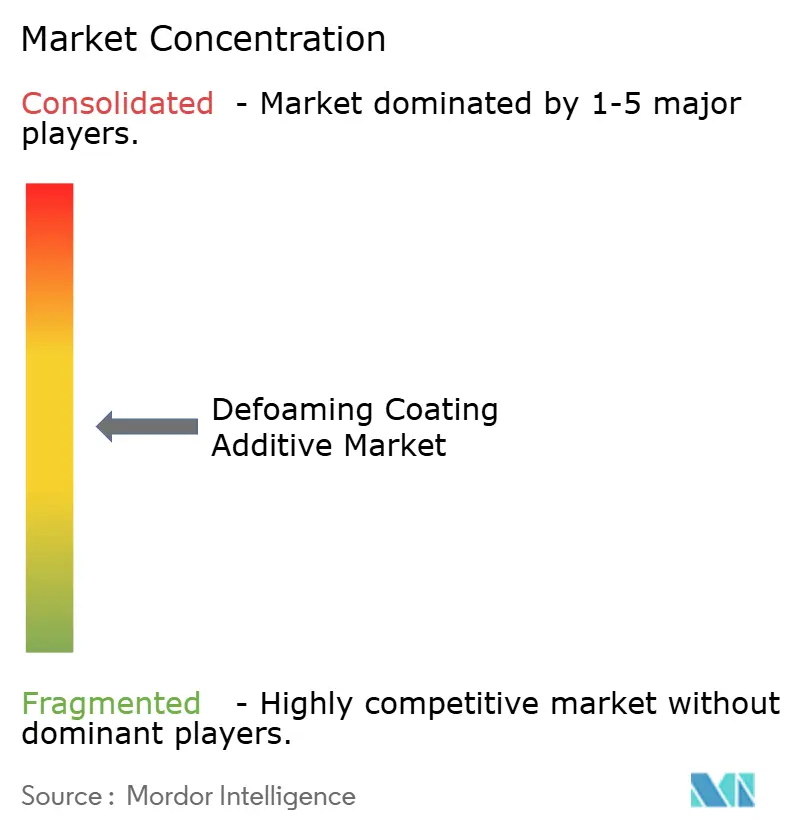

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defoaming Coating Additive Market Analysis by Mordor Intelligence

Defoaming Coating Additive Market size market size in 2026 is estimated at USD 2.12 billion, growing from 2025 value of USD 2.03 billion with 2031 projections showing USD 2.61 billion, growing at 4.32% CAGR over 2026-2031. A steady shift toward water-based, low-VOC formulations is the core driver behind this expansion, with advanced defoamer chemistries ensuring film integrity across architectural, automotive, and industrial lines. Asia-Pacific remains the demand anchor for the defoaming coating additive market as large-scale building activity and vehicle output accelerate additive uptake. Suppliers continue to broaden product lines around silicone emulsions, bio-based polymers, and VOC-free powders, thereby securing resilience against raw-material volatility. On the opportunity side, digital décor printing, battery component coatings, and high-build spray systems generate fresh volume and margin pockets, even as price-sensitive customers demand cost-stable alternatives to traditional silicone oils.

Key Report Takeaways

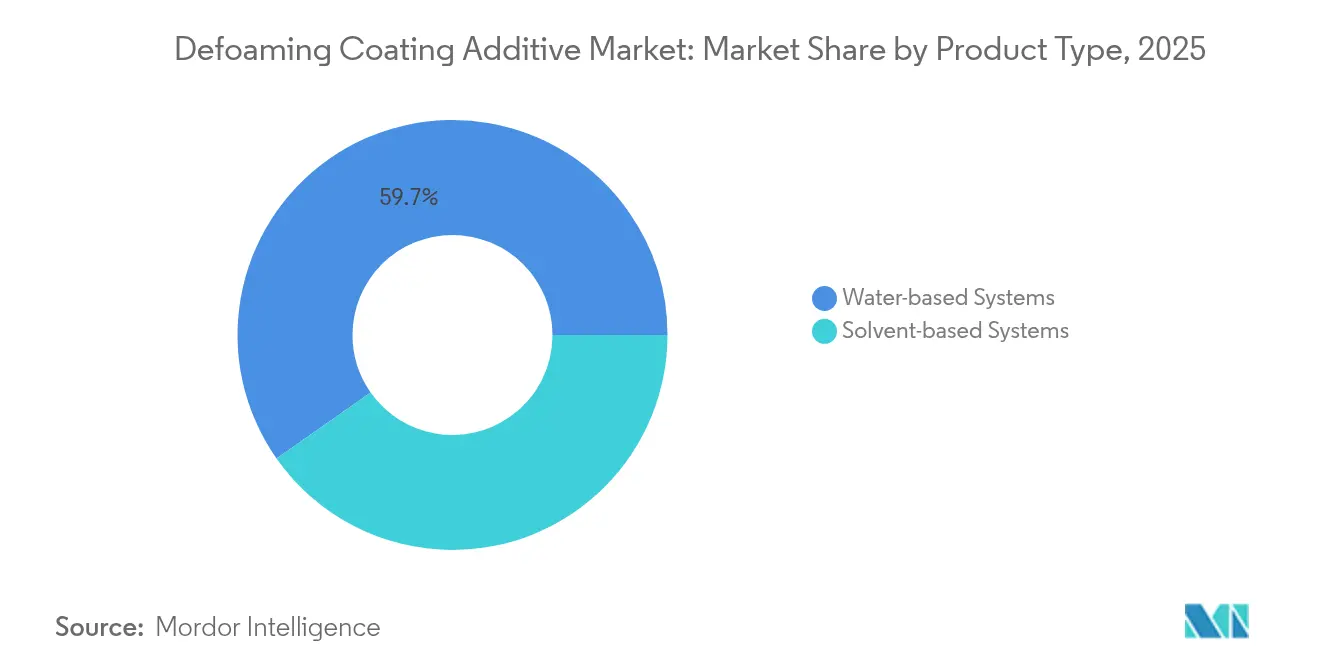

- By product type, water-based systems commanded 59.74% of the defoaming coating additive market share in 2025, while the sub-segment is projected to post a 5.18% CAGR through 2031.

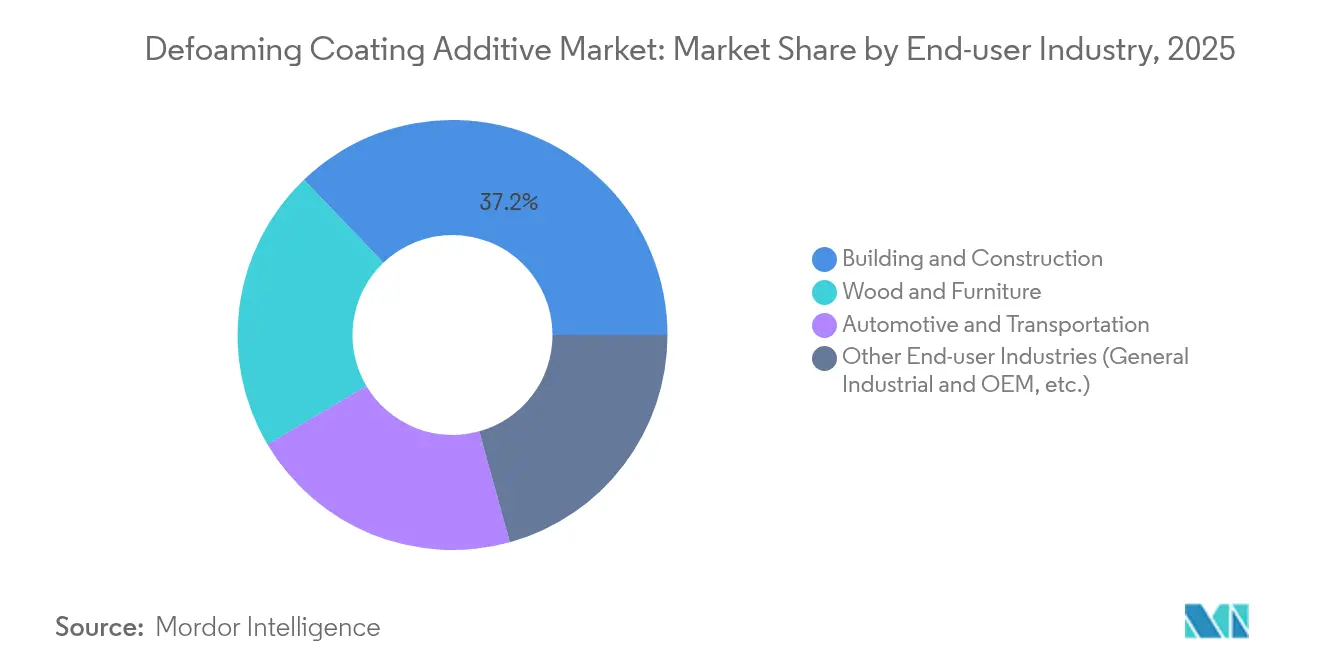

- By end-user industry, building and construction held 37.15% of the defoaming coating additive market size in 2025, whereas wood and furniture is the fastest-growing category with a 5.02% CAGR to 2031.

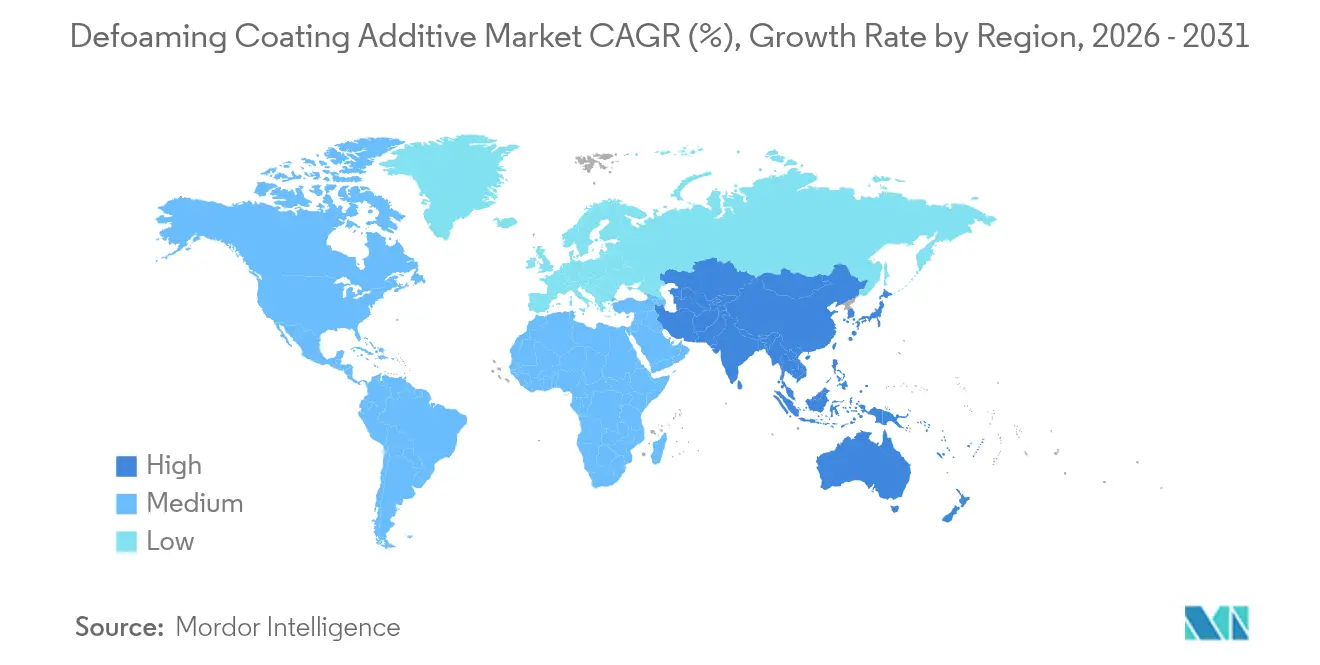

- By geography, Asia-Pacific dominated with 44.10% revenue share in 2025; the region is set to expand at a 5.03% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Defoaming Coating Additive Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from construction coatings | 1.2% | Global, with concentration in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Increasing requirement in automotive coatings | 0.8% | North America, Europe, Asia-Pacific core markets | Long term (≥ 4 years) |

| Expansion of wood and furniture production | 0.6% | Asia-Pacific, North America, with spillover to Europe | Medium term (2-4 years) |

| Surge in digital decor printing lines | 0.4% | Europe, North America, with adoption in Asia-Pacific | Short term (≤ 2 years) |

| Rising usage in industrial applications | 0.3% | Global, with emphasis on manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Construction Coatings

Rapid urbanization and infrastructure renewal elevate foam-control requirements for architectural finishes worldwide. Spray-applied, high-build systems are now commonplace on commercial facades and civil structures, yet even micro-air entrapment compromises adhesion and long-term durability. The push toward low-VOC paints heightens the technical challenge because water-rich formulations entrain more air than solventborne predecessors. BASF boosted its Nanjing additives output in 2024 to supply water-compatible defoamers that reconcile these issues. Emerging economies, led by China, India, and Indonesia, continue to commission mass housing, transport corridors, and industrial parks, embedding sustained pull for high-efficiency defoamers able to maintain gloss uniformity on concrete, metal, and composite substrates.

Increasing Requirement in Automotive Coatings

Electric-vehicle platforms, lightweight substrates, and multi-layer paint stacks create fresh foam-control pain points. Modern primer-surfacer lines run at elevated line speeds, where improperly dispersed air causes crater, pinhole, and blister defects. Allnex’s solventborne ADDITOL VXL 4951 N illustrates how the defoaming coating additive market now delivers narrow-range surface-tension control to avoid haze without silicone print-transfer risks. Battery housings, e-motor components, and electrode slurries present additional niches that require zero-silicone formulas for voltage-sensitive zones, nudging OEMs to lock in long-term supply contracts with additive vendors able to certify cleanliness.

Expansion of Wood and Furniture Production

Consumers favor sustainably sourced timber and low-odor water-based finishes for cabinetry and flooring. Yet wood grain absorbs air during roller and vacuum coating, forcing operators to dose defoamers precisely. Research on UV-cured polyurethane-acrylate confirms that optimized defoamer loadings at 120 g/m² deliver higher gloss and scratch resistance on oak panels while holding VOCs below legislative thresholds. Asian production clusters around Vietnam and Malaysia add volume, whereas North American mills push for premium matte looks that demand finer microfoam removal. These converging needs explain why the defoaming coating additive market records its fastest segmental CAGR in wood and furniture lines.

Surge in Digital Décor Printing Lines

High-resolution inkjet heads apply decorative patterns on laminates, wall panels, and luxury furniture fronts. Any residual foam in primer or topcoat distorts print quality, leading to banding or color drift. European printers shifted to inline waterborne protective coats, requiring defoamers compatible with pigment dispersants and photoinitiators. Brands supplying wide-format presses now collaborate directly with additive formulators to pre-qualify low-silicone emulsions that leave no surface residue. Adoption waves are visible in Turkey, Poland, and coastal China plants, ensuring short-term growth spurts for niche defoamers tailored to digital décor lines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicone-oil price volatility | -0.5% | Global, with particular impact on cost-sensitive markets | Short term (≤ 2 years) |

| Rise of UV-powder coatings | -0.3% | Europe, North America, with gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Stricter food-contact migration limits | -0.2% | Europe, North America, with regulatory spillover globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicone-Oil Price Volatility

Slim supply chains, purity specifications and energy-intensive synthesis periodically lift silicone-oil costs, unsettling formulators who rely on the material as the cornerstone of high-efficiency defoamers. Coating makers operating on narrow margins, particularly in Southeast Asia, pivot toward lower-priced mineral-oil or polymer alternatives despite minor performance trade-offs. BYK’s silicone-free BYK-1642 caters to this budget-centric cohort while giving additive suppliers a hedge against price spikes.

Stricter Food-Contact Migration Limits

North American and European regulators tighten extraction limits on specific defoamer chemistries such as polyethylene glycol. In parallel, REACH classifies certain cyclic silicones as substances of very high concern, curbing their use in packaging coatings that contact food[1]U.S. Government, “21 C.F.R. Subpart C—Coatings, Films and Related Substances,” law.justia.com. Additive suppliers must redesign portfolios around higher-molecular-weight silicones or bio-derived polymers, incurring elevated research and development spends that may pass through to customers as price premiums, thereby tempering uptake in cost-focused converter plants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Water-Based Systems Drive Sustainability Transition

Water-based chemistries secured 59.74% of the defoaming coating additive market in 2025 and are forecast to advance at 5.18% CAGR through 2031 as formulators pursue VOC-compliant architectures. Silicone emulsions remain the workhorse class, combining rapid micro-bubble rupture with negligible surface-defect risk even at dosages below 0.2%. Meanwhile, the push for silicone-free labelling stimulates polymer microemulsions derived from vegetable oils. Allnex’s bio-based ADDITOL VXW 4926 exemplifies this direction, offering equivalent dynamic surface-tension control without triggering substance-of-concern audits.

Solvent-based packages persist where extreme humidity resistance or high-temperature bake cycles make water a liability. Marine topcoats, chemical-plant linings, and specialty refinish fat lines still pick high-flashpoint carriers paired with silicone-polyacrylate defoamers that withstand 200 °C cure schedules. Powder-format defoamers, such as BYK-1693 SD, serve customers migrating to VOC-free zero-flow powder paints. These granules contain 54% bio-carbon, illustrate how the defoaming coating additive market blends sustainability and process convenience without sacrificing efficacy.

By End-User Industry: Construction Leads While Wood Furniture Accelerates

Construction retained a 37.15% share of the defoaming coating additive market in 2025, riding infrastructure buildouts across Asia-Pacific mega-cities and refurbishment cycles in Western economies. The segment favors high-build elastomeric walls and low-sheen exterior emulsions that rely on defoamers to avoid pinholes on porous masonry. Builders now specify defect-free finishes to minimize call-backs, encouraging paint makers to tighten additive quality.

Wood and furniture trails in absolute dollar terms yet delivers the highest 5.02% CAGR, reflecting consumer shift toward eco-philic wooden décor across global households. UV-curable clearcoats on cabinetry and flooring demand ultra-fast defoamers to support flash-off times below 60 seconds, ensuring high throughput on automated lines. Automotive and general industrial sectors provide steady baseline volume, hedging suppliers against cyclical swings in housing and furnishings.

Geography Analysis

Asia-Pacific captured 44.10% of the defoaming coating additive market in 2025 on the back of construction expansions and vehicle assembly clusters in China, India, and the ASEAN bloc. Regional CAGR of 5.03% reflects government-funded smart-city projects, new metro corridors, and aggressive EV production mandates. Multinational producers operate integrated Verbund sites and local joint ventures to curtail logistics costs and satisfy country-specific compliance audits.

Federal infrastructure modernization, battery-plant investments, and resilient housing demand keep coatings factories running near capacity in North America. Regulatory pressure against PFAS drives transfer from fluorinated defoamers to silicone or bio-based families, prompting formulators to fast-track new product qualifications. Europe maintains a similar regulatory tone, further complicated by REACH candidate-listing of additional cyclic silicones in 2025, spurring additive vendors to market PFAS-free, cyclic-siloxane-free lines.

South America, and Middle-East and Africa collectively account for a smaller yet rising slice of the defoaming coating additive market. Brazil’s construction stimulus and Saudi Arabia’s giga-projects draw in advanced waterborne coatings that cannot tolerate foam. Coating producers in these regions often license European technology, integrating defoamers sourced from global majors until local capacity matures. These dynamics translate into above-average growth trajectories, albeit from a comparatively low base.

Competitive Landscape

The defoaming coating additive market is moderately fragmented. Large incumbents wield integrated silicone capacity, pilot plants, and application labs that shorten cycle time from concept to customer approval. Mid-tier challengers differentiate via local service, cost-competitive mineral-oil blends, and niche claims such as food-contact compliance. Chinese producers leverage scale and proximity to Asia-Pacific buyers, although their export reach is sometimes capped by Western regulatory gaps. Product roadmaps focus on PFAS-free certification, biogenic carbon content disclosure, and circular feedstock sourcing.

Defoaming Coating Additive Industry Leaders

Dow

Evonik Industries AG

Arkema

ALTANA

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BYK, a subsidiary of ALTANA, unveiled BYK-1693 SD and a PFAS-free defoamer series for coatings at ECS 2025, strengthening sustainable offerings.

- April 2024: Evonik Industries AG launched TEGO Foamex 8051, extending its siloxane line of defoaming additives for waterborne décor paints.

Global Defoaming Coating Additive Market Report Scope

The defoaming coating additive market report includes:

| Water-based Systems | Silicone |

| Emulsion | |

| Polymer | |

| Powder | |

| Others | |

| Solvent-based Systems | Polymer |

| Silicone |

| Building and Construction |

| Automotive and Transportation |

| Wood and Furniture |

| Other End-user Industries (General Industrial and OEM, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| Product Type | Water-based Systems | Silicone |

| Emulsion | ||

| Polymer | ||

| Powder | ||

| Others | ||

| Solvent-based Systems | Polymer | |

| Silicone | ||

| End-user Industry | Building and Construction | |

| Automotive and Transportation | ||

| Wood and Furniture | ||

| Other End-user Industries (General Industrial and OEM, etc.) | ||

| Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the defoaming coating additive market in 2026?

The market is valued at USD 2.12 billion in 2026.

What compound annual growth rate (CAGR) is forecast for the market to 2031?

The market is projected to expand at a 4.32% CAGR, reaching USD 2.61 billion by 2031.

Which product type currently holds the biggest share?

Water-based defoaming systems account for 59.74% of global revenue.

Which end-use industry is expanding the fastest?

Wood and furniture coatings lead growth with a 5.02% CAGR through 2031.

Which region contributes the most demand?

Asia-Pacific dominates with 44.10% market share, supported by ongoing construction and automotive activity.

Page last updated on: