Rhamnolipids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

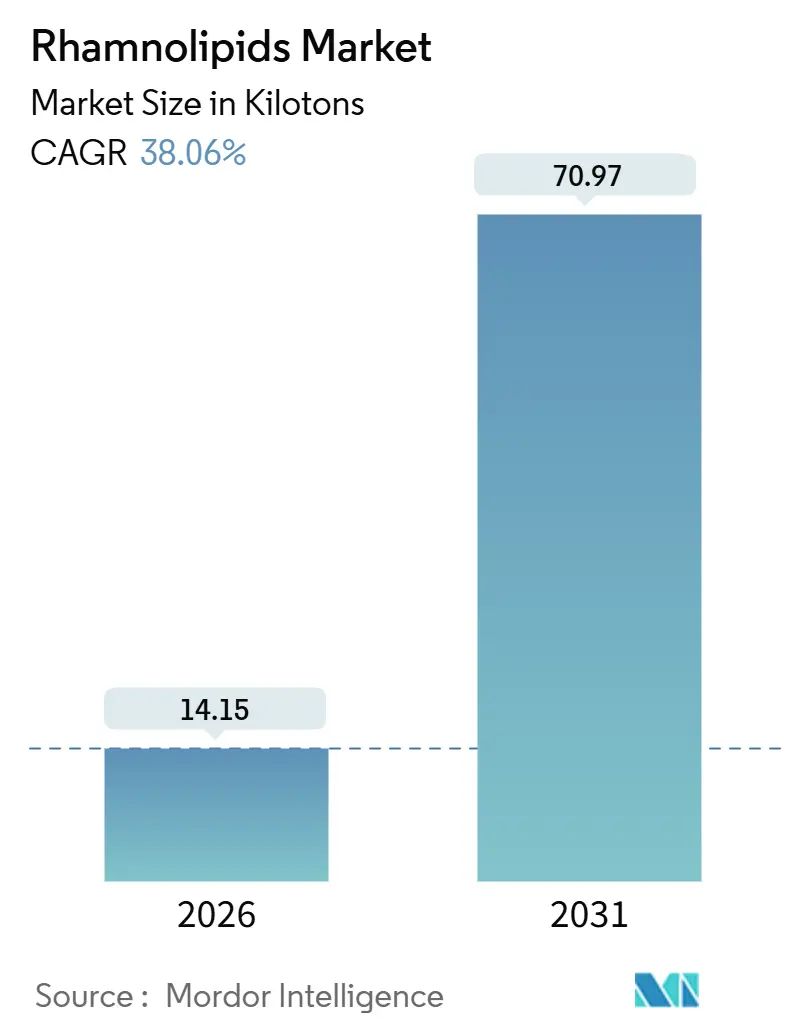

| Market Volume (2026) | 14.15 kilotons |

| Market Volume (2031) | 70.97 kilotons |

| Growth Rate (2026 - 2031) | 38.06% CAGR |

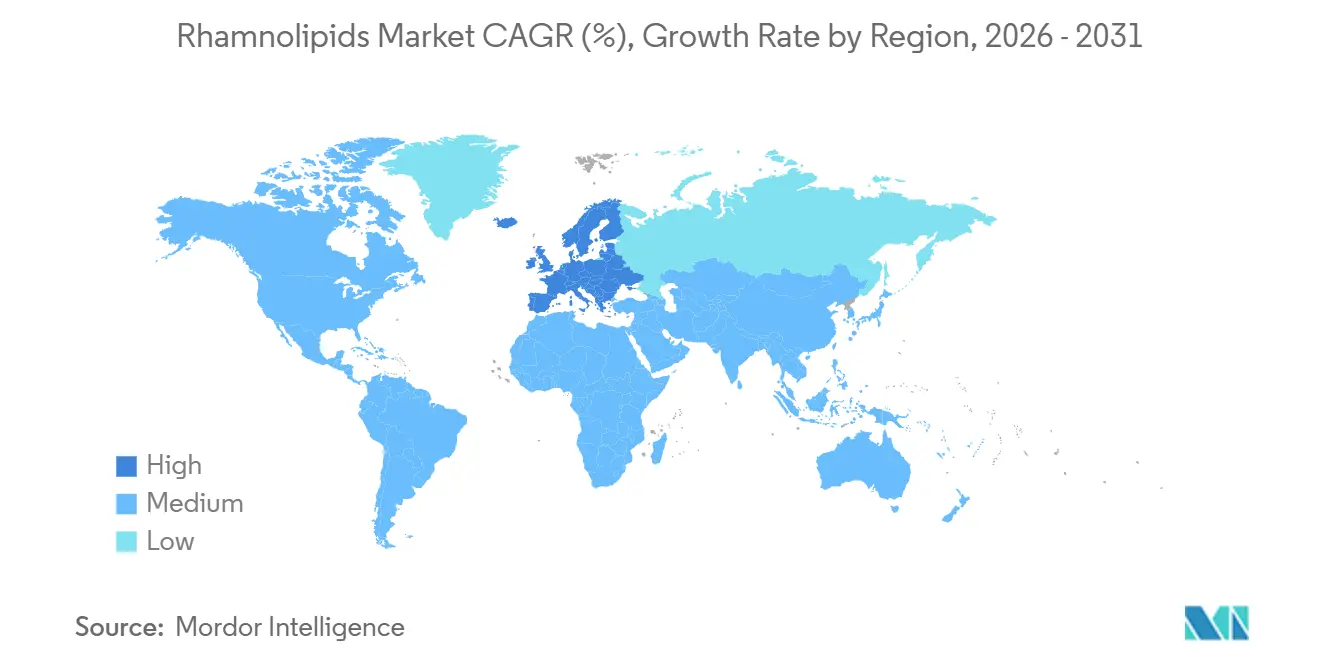

| Fastest Growing Market | Europe |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rhamnolipids Market Analysis by Mordor Intelligence

The Rhamnolipids Market size is estimated at 14.15 kilotons in 2026, and is expected to reach 70.97 kilotons by 2031, at a CAGR of 38.06% during the forecast period (2026-2031). Shifting preference toward fermentation-derived surfactants, mounting regulatory pressure on petrochemical ingredients, and commercial‐scale capacity additions in Europe and Asia place the rhamnolipids market on an accelerated growth path. Europe currently dominates demand as Unilever launches dishwashing liquids sourced from Evonik’s Slovakian plant, while Asia rapidly scales owing to AGAE Technologies’ 1,000-metric-ton facility and growing personal-care consumption in China, Japan, and India. Surfactant formulators value rhamnolipids’ lower critical micelle concentration, skin-mildness profile, and 28–30 mN/m surface-tension performance, enabling clean-label positioning without sacrificing foaming or detergency. Feedstock flexibility, from waste glycerol to renewable methanol, further reinforces supply resilience and cost competitiveness in the rhamnolipids market. Competitive intensity is tightening as Holiferm, Biotensidon, and other fermentation specialists draw fresh capital to close the price gap with synthetic lauryl ether sulfates.

Key Report Takeaways

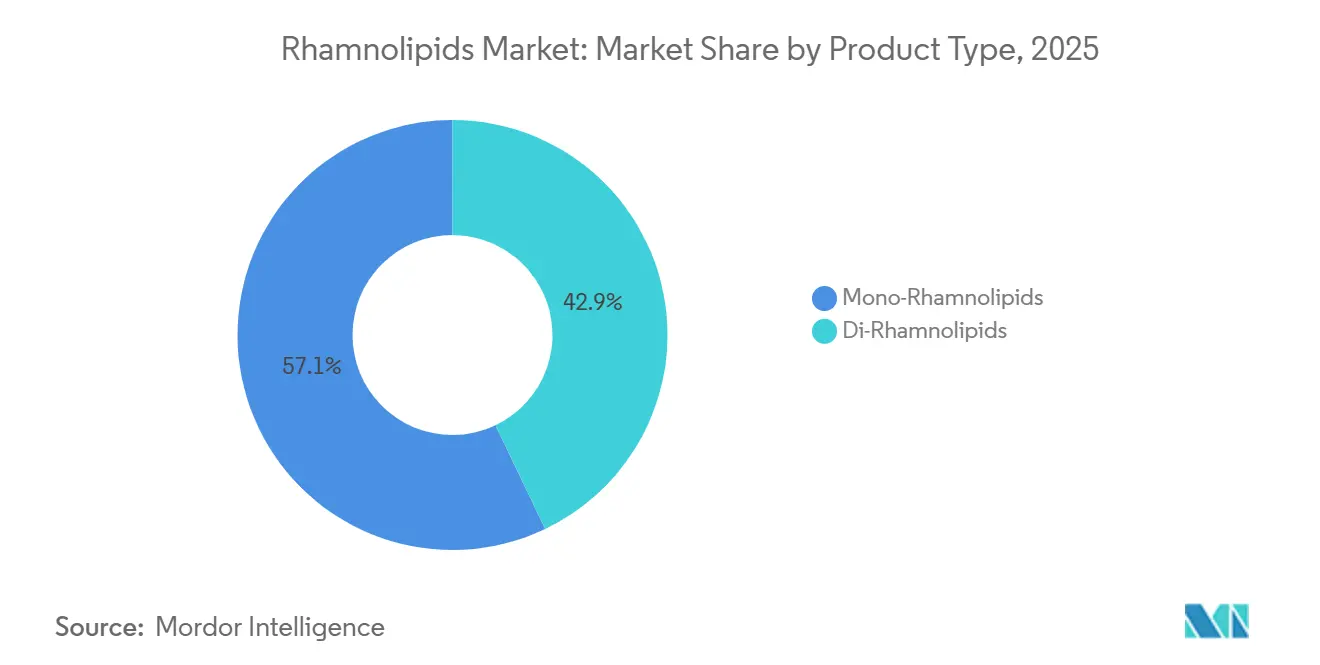

- By product type, mono-rhamnolipids captured 57.09% of global volume in 2025, and their market share is expected to grow with a CAGR of 40.42% during the forecast period (2026-2031).

- By feedstock, vegetable-oils-derived feedstock held a 44.16% share in 2025, whereas waste glycerol feeds are advancing at a 41.18% CAGR, reflecting superior cost and carbon metrics.

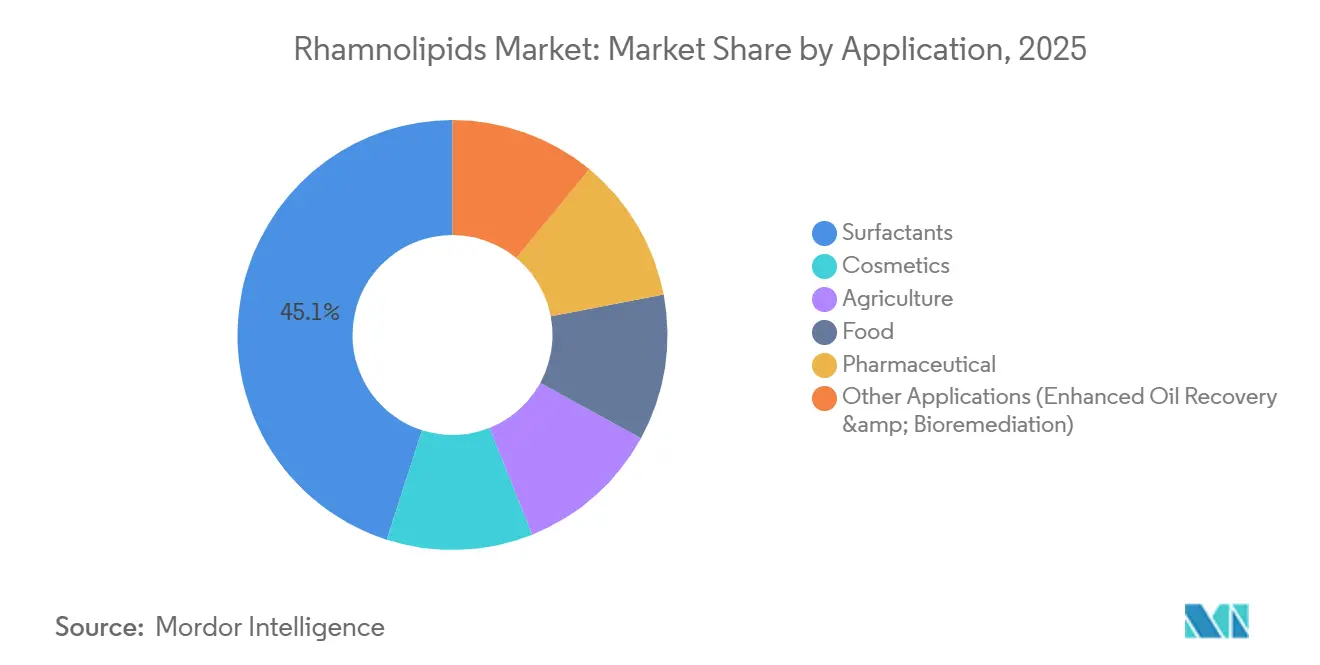

- By application, surfactant uses accounted for 45.05% of demand in 2025 and are expanding at a 47.74% CAGR to 2031, outpacing all other end uses.

- By geography, Europe led with 62.76% of the rhamnolipids market share in 2025, and this share is expected to grow with a CAGR of 43.76% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rhamnolipids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for eco-friendly surfactants in Home & Personal Care | +9.2% | Global, with concentration in Western Europe and North America | Medium term (2–4 years) |

| Regulatory push for biodegradable, low-toxicity ingredients | +8.5% | North America & EU, spillover to APAC urban markets | Short term (≤ 2 years) |

| Increasing usage in agriculture and biopesticide applications | +6.8% | Brazil, India, ASEAN countries | Long term (≥ 4 years) |

| Adoption of rhamnolipid nano-micelles as alcohol-free hospital sanitizers | +5.3% | Global, early traction in Middle East and Asia-Pacific healthcare systems | Medium term (2–4 years) |

| Increasing demand from oil recovery and remediation applications | +4.7% | Middle East (Saudi Arabia, UAE), North America (shale basins) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Eco-Friendly Surfactants in Home & Personal Care

Penetration of certified eco-label detergents exceeded 28% in Germany, France, and the United Kingdom during 2025 as millennials and Gen Z consumers prioritized ingredient transparency. Holiferm’s partnership with Trichem South illustrates adoption by tier-two detergent brands seeking mildness and sustainability without compromising foam or grease cutting.[1]Holiferm, “Holiferm Partners with Trichem South,” holiferm.com. Dermatological patch tests confirm rhamnolipids’ reduced irritation, supporting deployment in baby-care and sensitive-skin products. Retail price premiums of 15–20% for bio-based micellar waters and shower gels reduce price elasticity, translating directly to volume displacement of sodium lauryl ether sulfate. As private-label and mass brands emulate early movers, the +9.2 percentage-point effect will remain visible through 2029, reinforcing the rhamnolipids market trajectory.

Regulatory Push for Biodegradable, Low-Toxicity Ingredients

The 2024 REACH Annex XIV update added three alkylphenol ethoxylates to Europe’s authorization list, effectively phasing them out by 2027. The U.S. EPA’s Safer Choice revisions tightened Daphnia magna LC₅₀ requirements above 10 mg/L, spurring formulators to adopt rhamnolipids, which display LC₅₀ values over 100 mg/L and >90% biodegradation within 28 days. Brand reformulations to meet 2026–2027 cut-off dates anchor near-term market growth, though momentum stabilizes post-2028 as compliant formulations gain wide penetration.

Increasing Usage in Agriculture and Biopesticide Applications

Brazil’s Bio-inputs Law reduced microbial registration times to one year, enabling multifunctional rhamnolipid products that pair pest suppression with nutrient uptake. Field trials in São Paulo showed 18–22% gains in glyphosate efficacy when paired with rhamnolipid adjuvants, cutting herbicide volumes. India mirrors this trajectory as smallholders pursue organic certification and integrated pest management. Long-term impact rests on extension-service training and distribution, positioning agriculture as a sustained growth pillar for the rhamnolipids market.

Adoption of Rhamnolipid Nano-Micelles as Alcohol-Free Hospital Sanitizers

Hospitals in high-temperature regions find alcohol gels suboptimal because evaporation shortens contact time below 20 seconds, the threshold for pathogen inactivation. Rhamnolipid nano-micelles achieve log-4 MRSA reduction within 15 seconds without flammability, enhancing safety in oxygen-rich environments. Saudi Arabia piloted rhamnolipid sanitizers in 12 tertiary hospitals during 2025, and wider procurement decisions are underway. FDA approval for over-the-counter U.S. use remains a gating factor, shifting full commercialization toward 2027–2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foaming & downstream-processing costs | -6.4% | Global, acute in Asia-Pacific greenfield projects | Short term (≤ 2 years) |

| Safety concerns over endotoxins | -3.8% | North America, EU pharmaceutical and food-grade applications | Medium term (2–4 years) |

| Vegetable-oil price volatility | -4.2% | Palm-oil supply chains in Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Foaming & Downstream-Processing Costs at Industrial Scale

Fermentation foam can exceed reactor capacity by 3–5 times, demanding mechanical breakers or antifoams that complicate purification. AGAE Technologies installed rapid foam-recycling loops and pressure-modulated aeration at its Asian plant to keep yields intact[2]Chemical Engineering, “Foam-Control Solutions in Biosurfactant Fermentation,” chemengonline.com. Downstream operations, solvent extraction, ultrafiltration, and spray drying still account for as much as 50% of the cost of goods, double the citric acid benchmarks. Continuous membrane contactors and in-situ product removal could halve recovery costs by 2028, but the learning curve remains a -6.4 percentage-point drag in the near term.

Safety Concerns Over Endotoxins

Gram-negative Pseudomonas strains shed lipopolysaccharides; residual endotoxin above 0.5 EU/mL can trigger pyrogenic responses. Depyrogenation via activated carbon or affinity chromatography adds USD 8–12/kg and trims yields by up to 15%. Biotensidon’s non-pathogenic strains are promising yet pre-commercial. Pharmaceutical and oral-care formulators, representing 12% of 2025 demand but commanding premium margins, remain risk-averse, imparting a -3.8 percentage-point constraint until engineered strains gain regulatory clearance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mono-Rhamnolipids Dominate on Solubility Advantage

Mono-rhamnolipids commanded 57.09% volume in 2025, capturing the largest rhamnolipids market share due to water solubility and lower critical micelle concentration. Mono-rhamnolipids' market share is expected to increase at a CAGR of 40.425 during the forecast period (2026-2031). Evonik’s pH-controlled fermentation tunes mono-to-di ratios without costly fractionation, trimming production costs 15–18%. Waste glycerol substrates further tilt yields toward mono species, linking raw-material strategy to product mix. Patent filings center on rhamnosyltransferase gene optimization, with AGAE Technologies targeting more than 85% mono purity. Di-rhamnolipids retain a niche for antimicrobial cosmetics and industrial degreasers owing to heightened membrane disruption, but viscosity limits adoption where quick dissolution is critical.

Second-generation blends leveraging both species could emerge as suppliers pursue performance-cost trade-offs. If di-rhamnolipid titers improve through genetic knockouts of competing pathways, formulators may adopt tailored ratios for leave-on skincare and disinfectants, reinforcing product-type diversification within the rhamnolipids market.

By Feedstock: Waste Glycerol Gains on Cost and Carbon Metrics

Vegetable oils held 44.16% share in 2025, but waste glycerol feeds grew at 41.18% CAGR, compressing feedstock costs to 15–20% of total production expense. Global biodiesel output generated 4.7 million tons of crude glycerol in 2025, creating a low-value substrate priced around USD 200–300/t. Fed-batch fermentation titers above 60 g/L on glycerol underscore commercial viability. Evonik’s European corn sugar approach meets EU locality criteria, whereas BASF’s renewable methanol collaboration with Acies Bio aims to bypass agricultural inputs entirely. Should OneCarbonBio yield top 40 g/L by 2027, carbon-negative pathways could remake the rhamnolipids market cost curve.

Hydrocarbon substrates stay niche for enhanced oil recovery, and sugar feedstocks risk price swings and food-fuel debates. A portfolio approach, glycerol for cost, methanol for carbon neutrality, may prove optimal as producers hedge volatility and sustainability scrutiny.

By Application: Surfactants Lead, Agriculture Accelerates

Surfactants represented 45.05% of demand in 2025 and will advance at 47.74% CAGR to 2031, as retailers impose ingredient-count limits and detergent makers pivot to transparent labels. Rhamnolipids’ dual role as primary surfactant and foam booster enables streamlined formulations meeting clean-label scorecards. Cosmetics follow, leveraging antimicrobial action against Cutibacterium acnes in acne treatments.

Agriculture, though smaller in volume, posts the fastest percentage growth as Brazil and India institutionalize bioinputs. Rhamnolipid adjuvants lifted herbicide rainfastness by 30–35%, saving USD 12-15/ha for Punjab growers. Pharmaceutical uptake hinges on endotoxin mitigation, yet excipient demand for skin and transdermal delivery remains promising. Enhanced oil recovery rounds out applications; field pilots demonstrate 8–12% incremental crude extraction, pending cost reductions below USD 8/kg.

Geography Analysis

Europe accounted for 62.76% of the Rhamnolipids market size in 2025 and is set to grow at a 43.76% CAGR through 2031. Germany and France anchor demand, supported by Henkel and Unilever commitments to replace 50% of petrochemical surfactants by 2030. Evonik’s Slovakian plant supplies Unilever’s global dishwashing liquids, aligning regional supply chains with EU sustainability mandates. Post-Brexit UK regulations shorten review cycles for bio-based ingredients, accelerating market entry and spurring adoption by private-label producers in Italy and Spain.

Asia-Pacific is the fastest-growing region by volume. AGAE Technologies’ 1,000-t plant, commissioned in 2025, positions the region as a supply hub amid rising personal-care consumption. China’s 2025 Cosmetic Ingredient Safety update allows 2.0% rhamnolipid inclusion in leave-on products, unlocking a potential 10,000 t annual market if 5 % penetration is achieved. Japan authorized rhamnolipids as food emulsifiers at 0.5% in May 2025, pioneering direct food-contact approvals. India emphasizes agriculture, integrating rhamnolipid biopesticides under its National Mission for Sustainable Agriculture.

North America is led by industrial and institutional cleaners certified under EPA’s Safer Choice program. Domestic full-scale production remains prospective; AGAE plans a US plant leveraging foam-control learnings from Asia. Canada’s modest adoption reflects limited personal-care manufacturing but could surge as exporters seek REACH-compliant formulations. Mexico lags given cheap synthetic imports, though USMCA rules may spur regional biosurfactant production.

Competitive Landscape

The Rhamnolipids market is moderately consolidated. Strategic white space lies in food emulsifiers for plant-based proteins, oil-field chemicals where price thresholds near USD 8/kg approach viability, and organic agriculture adjuvants barred from synthetic surfactants. Patent filings intensified in 2024–2025: Evonik’s continuous foam-recycling bioreactors and AGAE Technologies’ membrane-contactor systems aim to slash downstream costs. With capacity additions projected to outpace short-term demand, margin compression may spark consolidation among smaller players lacking distinct IP or feedstock synergies. Investors monitor unit cost trajectories and regulatory milestones to gauge winners in the evolving rhamnolipids market.

Rhamnolipids Industry Leaders

Evonik Industries AG

AGAE Technologies, LLC

Stepan Company

Jeneil Biotech

Holiferm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AGAE Technologies, a rhamnolipid producer, in collaboration with its partners, inaugurated Asia's largest retrofitted manufacturing plant complex. Spanning 41,000 square feet, this facility boasts an annual production capacity exceeding 1,000 metric tons of rhamnolipids, and it has the potential to expand production lines in response to growing demand.

- January 2024: Evonik Industries AG launched production at its newly completed facility for sustainable biosurfactants in Slovakia. This plant is the world's first to manufacture sustainable rhamnolipid biosurfactants. Leveraging its biotechnology platform from the life sciences division, Nutrition & Care, Evonik produces rhamnolipids and other sustainable biosurfactants.

Global Rhamnolipids Market Report Scope

Rhamnolipids (RL) are members of the glycolipid biosurfactant family. The amphiphilic properties of rhamnolipids allow them to reduce the interfacial tension between two substances that normally would not mix.

The Rhamnolipids market is segmented by product type, feedstock, application, and geography. By type, the market is segmented into Mono-Rhamnolipids and Di-Rhamnolipids. By feedstock, the market is segmented into vegetable oil-derived, waste glycerol / crude glycerin, sugar-based, and hydrocarbon-based. By application, the market is segmented into surfactants, cosmetics, agriculture, food, pharmaceuticals, and other applications. The report also covers the market size and forecast for the market in 16 countries across major regions. For each segment, the market sizing and forecast have been done based on volume (tons).

| Mono-Rhamnolipids |

| Di-Rhamnolipids |

| Vegetable-Oil Derived |

| Waste Glycerol / Crude Glycerin |

| Sugar-Based |

| Hydrocarbon-Based |

| Surfactants |

| Cosmetics |

| Agriculture |

| Food |

| Pharmaceutical |

| Other Applications (Enhanced Oil Recovery & Bioremediation, etc.) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Mono-Rhamnolipids | |

| Di-Rhamnolipids | ||

| By Feedstock | Vegetable-Oil Derived | |

| Waste Glycerol / Crude Glycerin | ||

| Sugar-Based | ||

| Hydrocarbon-Based | ||

| By Application | Surfactants | |

| Cosmetics | ||

| Agriculture | ||

| Food | ||

| Pharmaceutical | ||

| Other Applications (Enhanced Oil Recovery & Bioremediation, etc.) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the rhamnolipids market and its growth outlook?

The market stood at 14.15 kilotons in 2026 and is projected to reach 70.97 kilotons by 2031, growing at a 38.06% CAGR.

Which product type leads demand?

Mono-rhamnolipids held 57.09% share in 2025, favored for low critical micelle concentration and rapid solubility.

Why are waste-glycerol feedstocks gaining traction?

Waste glycerol cuts feedstock costs to 15–20% of production expense and delivers fermentation titers above 60 g/L, accelerating commercial viability.

Which application segment is expanding fastest?

Surfactant formulations dominate volume and are rising at 47.74% CAGR, boosted by regulatory curbs on conventional ethoxylates.

What regions offer the highest growth potential?

Asia-Pacific posts the fastest volume growth as China, Japan, and India relax regulatory hurdles and capacity scales through new plants.

Page last updated on: