Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

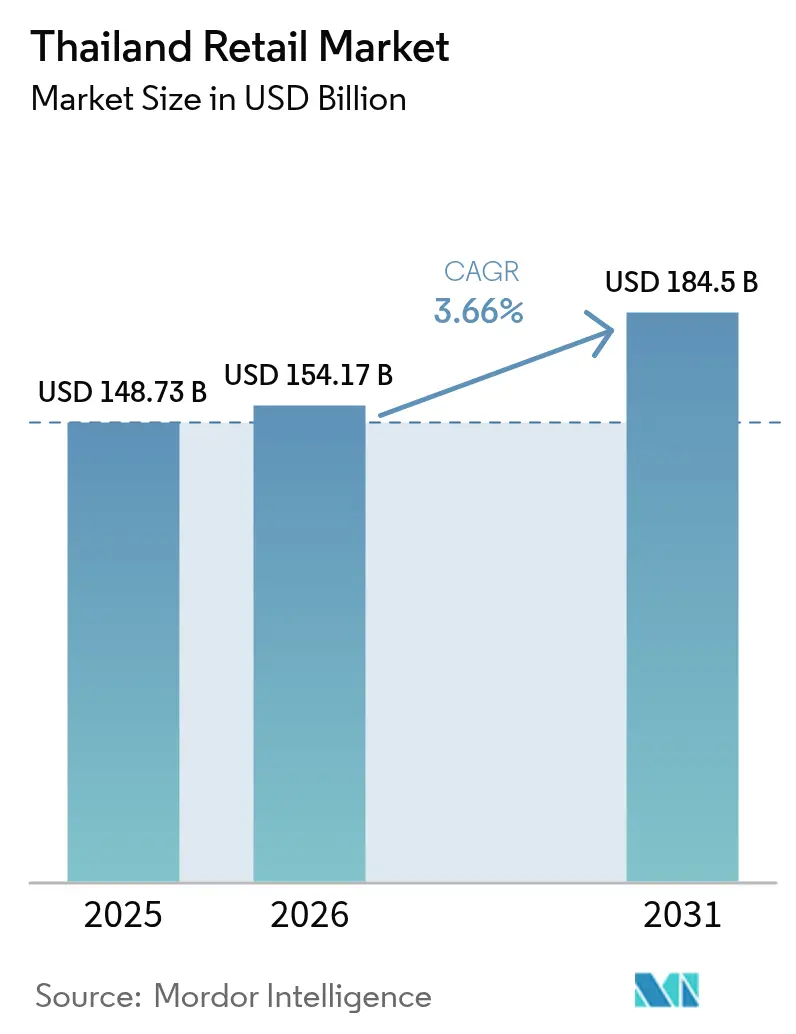

| Base Year Market Size (2025) | USD 148.73 Billion |

| Market Size (2026) | USD 154.17 Billion |

| Market Size (2031) | USD 184.5 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Retail Market Analysis by Mordor Intelligence

The Thailand retail market size is expected to grow from USD 148.73 billion in 2025 to USD 154.17 billion in 2026 and is forecast to reach USD 184.5 billion by 2031 at 3.66% CAGR over 2026-2031. Household deleveraging, evolving payment systems, and sustained tourism inflows form the bedrock of growth, while persistent cost pressures and muted credit expansion temper the outlook. Omnichannel integration accelerates as PromptPay usage tops 52.7 million accounts, steering consumers toward friction-free shopping journeys[1]Source: Bank of Thailand, “PromptPay: The Game Changer for Payments,” bot.or.th. Quick-commerce fulfillment networks continue to proliferate, raising the competitive bar for inventory localization and same-hour delivery propositions. Modern trade chains extend footprints into rural provinces, leveraging mobile wallets and data-driven category management to capture rising up-country spending.

Key Report Takeaways

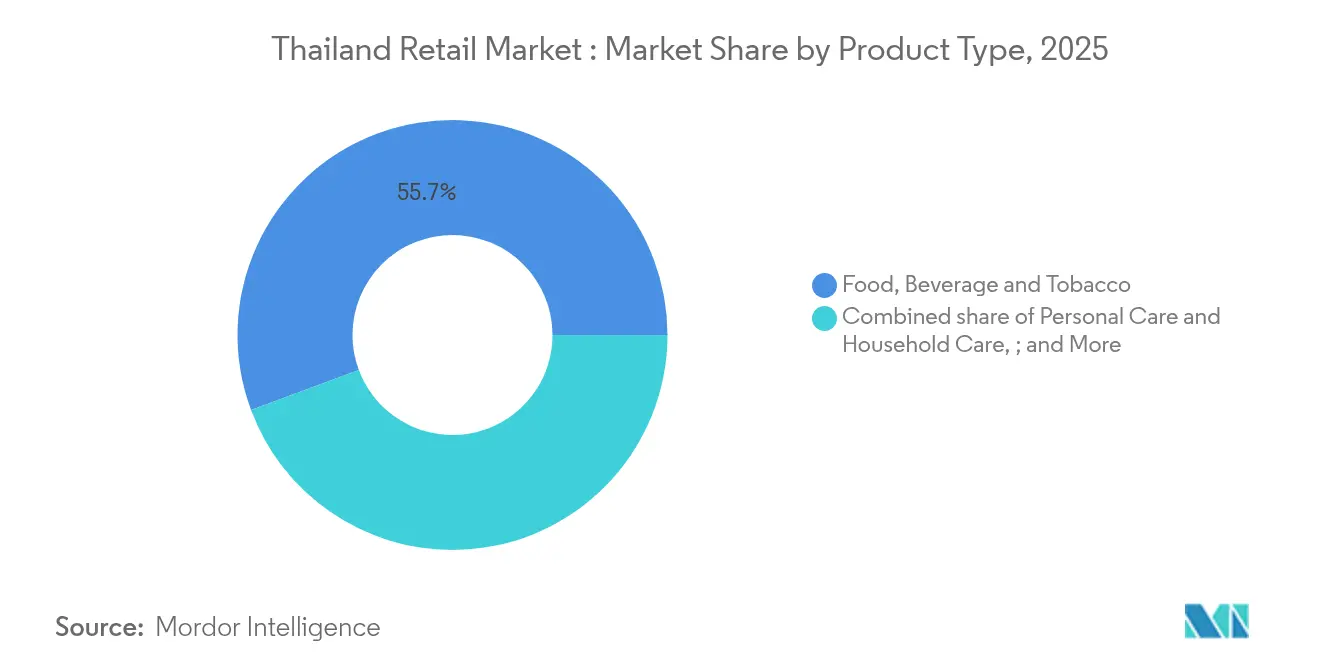

- By product type, food, beverage & tobacco captured 55.68% of the Thailand retail market share in 2025, while personal care & household care is projected to grow at a CAGR of 11.15% between 2026 and 2031.

- By retail channel, traditional mom & pop outlets accounted for 44.10% of the Thailand retail market share in 2025, whereas e-commerce & others are expected to expand the Thailand retail market size at a CAGR of 16.85% during 2026–2031.

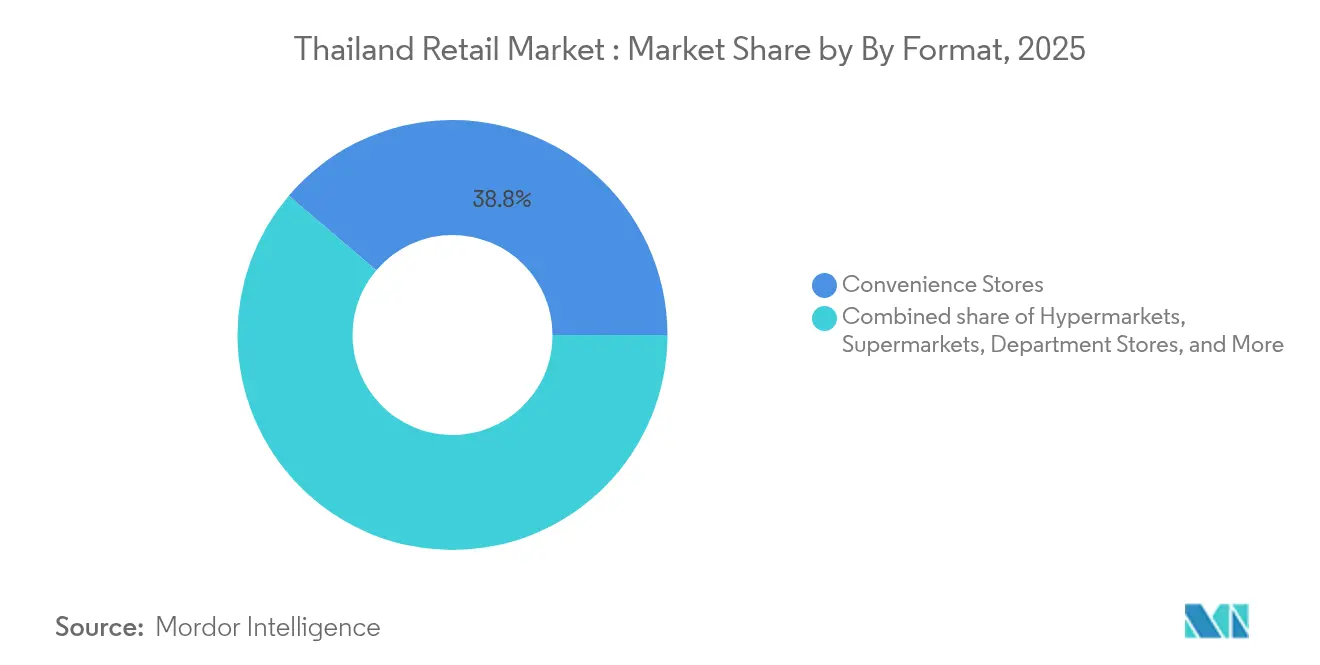

- By format, convenience stores held 38.78% of the Thailand retail market share in 2025, and the segment is forecast to advance the Thailand retail market size with a CAGR of 10.15% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quick-commerce demand in Bangkok & tier-2 cities | +1.2% | Bangkok, Chiang Mai, Phuket | Short term (≤ 2 years) |

| Tourism rebound lifting discretionary spend | +0.8% | Bangkok, Phuket, Pattaya | Medium term (2-4 years) |

| Modern trade push into rural provinces | +0.6% | Northeast & North | Long term (≥ 4 years) |

| “Thailand 4.0” digital-payment incentives | +0.4% | National | Medium term (2-4 years) |

| E-commerce platform expansion and logistics improvements | +1.0% | Nationwide | Short to Medium term (1–3 years) |

| Rising middle-class incomes driving premium product demand | +0.7% | Bangkok, Chiang Mai, Khon Kaen | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging Quick-Commerce Demand in Bangkok & Tier-2 Cities

Dark stores and micro-fulfillment hubs redefine urban logistics as consumers embrace 30-minute delivery promises. Operators deploy AI-based demand forecasting to trim spoilage and raise pick-accuracy, enabling higher service levels without inflating costs. Parcel-sorting automation at Thailand Post complements private last-mile fleets, ensuring consistent peak-season throughput[2]Source: Parcel and Postal Technology International, “Exclusive Interview: Thailand Post,” parcelandpostaltechnologyinternational.com. Food-focused aggregators consolidate, leaving capitalized players to widen assortment beyond meals into daily essentials. Retailers test “shop-in-app” livestreams to blend impulse discovery with rapid fulfillment, capturing incremental basket value. Regulatory attention centers on traffic congestion and rider-safety mandates, potentially reshaping service geographies over time.

Tourism Rebound Lifting Discretionary Retail Spend

Tourist arrivals rose past 35 million in 2024, restoring footfall across flagship malls and duty-free stores. Average international trip expenditure climbed to THB 50,900 (USD 1,450), with more than half of bookings executed online, signaling heightened digital engagement[3]Source: International Trade Administration, “Thailand Digital Wallet,” trade.gov.. Luxury beauty, travel retail exclusives, and local craft items see higher conversion as visitors pursue experiential purchases. Retail landlords allocate incremental space to F&B and themed zones that capture tourist dwell-time. Currency strength of key source markets China, Malaysia, South Korea directly shapes SKU mix and promotional calendars. While geopolitical shocks could disrupt flows, ongoing infrastructure upgrades at Bangkok’s airports enhance long-term capacity and retail tenancy demand.

Modern Trade Expansion into Rural Provinces

The strategic push by major retailers into previously underserved provincial markets represents a fundamental shift in Thailand's retail geography, driven by rising rural purchasing power and infrastructure improvements. Major operators plan approximately 1,000 new store openings in 2024, with significant focus on smaller format stores designed for provincial markets, including Big C's 200 Mini branches and Lotus's 100 Go Fresh branches. This expansion strategy capitalizes on limited competition in rural areas while addressing evolving consumer preferences for modern shopping experiences and product variety. The franchise sector's 9% growth to THB 300 billion (USD 9.25 billion) in 2024, particularly driven by young entrepreneurs in provincial areas, demonstrates increasing market sophistication and purchasing power beyond traditional urban centers. Success in provincial markets requires careful adaptation to local preferences, supply chain optimization for smaller volumes, and community engagement strategies that respect traditional retail relationships while offering superior value propositions.

Government “Thailand 4.0” Digital-Payment Incentives

Thailand's comprehensive digital transformation initiative accelerates retail sector modernization through infrastructure investments and consumer incentive programs that reshape payment behaviors and business models. The government's digital wallet program distributing approximately USD 276 to 45-50 million citizens through the 'Tang Rat' application represents a USD 12.5 billion stimulus directly targeting consumer spending. The PromptPay system, with 52.7 million users and widespread QR code adoption, has made seamless digital payments a new normal across retail formats. These initiatives not only increase transaction efficiency and transparency but also expand financial inclusion, empowering small businesses and supporting the rise of omnichannel retail. Regulatory influence from the Bank of Thailand and the Digital Economy Promotion Agency ensures robust frameworks for digital transactions, while ongoing infrastructure upgrades position Thailand as a regional leader in cashless commerce.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High household debt curbing big-ticket buys | -1.0% | National | Short term (≤ 2 years) |

| Rising minimum wages squeezing margins | -0.6% | National | Medium term (2-4 years) |

| Fragmented cold-chain limiting fresh e-grocery | -0.3% | Rural & peri-urban | Long term (≥ 4 years) |

| Grey-market imports diluting brand equity | -0.2% | Border provinces & online | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Household Debt Curbing Big-Ticket Purchases

Debt-to-GDP ratios exceeding 90% constrain credit appetites as lenders tighten scoring models. Auto and consumer-durable loans decelerate, prompting retailers to emphasize entry-level SKUs, refurbishment programs, and subscription models. Promotional calendars pivot toward value packs and zero-interest installments shorter than 12 months. Government debt-relief pilots for vulnerable households alleviate stress but lack scale to spark immediate spending surges. Retailers counter by bundling financial services—micro-insurance, layaway—within loyalty ecosystems, spreading payments without impairing cashflow. The trajectory implies muted volume growth for white goods until mid-2027, when income gains are projected to restore affordability.

Rising Minimum Wages Squeezing Retail Margins

Nationwide wage floor adjustments elevate labor costs, particularly in convenience and department stores where staffing densities are high. Chains deploy self-checkout kiosks and shelf-scanning robots to offset payroll inflation, reallocating associates to advisory roles that enhance upsell rates. Smaller independents face disproportionate strain due to limited capex capacity, accelerating consolidation or formal franchise affiliation. Retailers explore flexible scheduling and senior hiring programs to tap a growing 60-plus talent pool, aligning with demographic realities. Productivity gains from workforce digitization are essential to preserve EBITDA margins amid rising utilities and logistics expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Anchors, Wellness Accelerates

Food, Beverage & Tobacco retained a 55.68% Thailand retail market share in 2025, underpinned by dependable domestic demand and menu innovation that appeals to tourists and locals alike. The segment benefits from resilient agri-supply chains and government food-security initiatives that stabilize farm-gate prices. Modern grocery chains amplify local sourcing to hedge currency swings and shorten replenishment cycles. In contrast, Personal Care & Household Care posts an 11.15% CAGR through 2031 as aging consumers pursue functional skincare, nutraceuticals, and eco-friendly detergents. Cross-border e-commerce introduces niche J-beauty and K-beauty lines, elevating competitive benchmarks on ingredient transparency. Brands emphasize recyclable packaging and halal certification to capture diverse urban cohorts. Electronics and home appliances record softer momentum as deferred upgrades coincide with debt overhang, yet premium smart-home bundles retain a tech-savvy niche.

The Thailand retail market size for Personal Care & Household Care is projected to climb from USD 15.45 billion in 2026 to USD 26.18 billion by 2031, while Food, Beverage & Tobacco expands steadily to USD 104.12 billion, confirming both defensive and aspirational consumption poles. Parallel-import and counterfeit challenges prompt multinationals to deploy serialization and QR-based authenticity checks, educating shoppers on safe-channel purchases. Specialty food exporters leverage origin-tracing platforms to differentiate at modern trade shelves. Regulatory enforcement of intellectual-property laws intensifies at customs points, curbing grey flows and shielding authorized distributors’ price architecture. Overall, product diversification and premium-tier development mitigate topline reliance on core staple categories.

By Retail Channel: Informal Resilience Meets Digital Disruption

Traditional Mom & Pop outlets captured 44.10% of Thailand retail market size in 2025 as community trust, micro-credit extension, and proximity remain compelling among lower-income shoppers. Wholesaler route-to-market models support these stores with direct drop-offs and short credit terms, minimizing stock-out risk. The rise of QR payments empowers small proprietors to lower cash-handling costs and join loyalty coalitions sponsored by FMCG majors. Conversely, E-Commerce & Others grows at a 16.85% CAGR, propelled by live-stream shopping, gamified vouchers, and cross-border campaigns originating from China-based platforms. National data-privacy regulations mandate local data-center residency, pushing platforms to upgrade compliance infrastructure.

Marketplace operators enhance regional fulfillment centers, achieving next-day coverage across 90% of postal codes. Hybrid pickup points embedded in convenience stores widen delivery options, bridging last-mile gaps in rural districts. Modern trade banners respond by integrating endless-aisle kiosks and click-and-collect bays, converging physical and digital paths. Meanwhile, government consumer-protection laws require transparent seller identification and return policies, bolstering trust. The competitive narrative shifts toward retail media networks that monetize first-party data streams, an arena where big-box incumbents enjoy traffic advantages over pure-plays.

By Format: Convenience Stores Extend the Lead

Convenience Stores held 38.78% of Thailand retail market size in 2025, outperforming other formats through strategic density in mass-transit nodes and residential clusters. Operators roll out AI-driven planograms that tailor SKU mixes to 200-meter catchment demographics, maximizing turns. Differentiated food-service counters offering freshly prepared meals elevate ticket averages and combat margin erosion. Cashless self-checkout lanes shrink queue times and liberate staff for value-added engagement. Hypermarkets reposition as multi-purpose “retail-tainment” hubs, incorporating indoor playgrounds and wellness clinics to revive weekend traffic. Department stores revamp beauty halls with augmented-reality mirrors and curated local designer pop-ups, catering to experience-seeking tourists. Specialty stores focus on high-touch advisory categories such as pet care, cycling, and DIY, leveraging expert staff to justify price premiums.

The format race tightens as operators invest in solar-powered rooftops and energy-efficient refrigeration to lower opex and meet ESG targets. Regulatory zoning continues to cap hypermarket footprints in dense districts, fueling smaller-box experimentation. Franchise-based convenience concepts accelerate in provincial towns, enhancing brand visibility while harnessing local market knowledge. By 2030, convenience outlets are forecast to exceed 27,000, anchoring last-mile parcel networks and reinforcing the Thailand retail market’s omnichannel backbone.

Competitive Landscape

In 2024, the top players held a significant share of Thailand’s retail market, reflecting a moderately concentrated landscape where scale provides bargaining power, but local agility continues to play a critical role. Leading chains deploy machine-learning engines that recalibrate prices multiple times daily, enhancing value perception and raising basket sizes. Strategic acquisitions extend capabilities; prominent examples include a Thai conglomerate acquiring a European department-store chain, broadening private-label sourcing options and luxury know-how. Retailers forge cross-border alliances with Japanese convenience giants to co-develop food-to-go menus tuned to Thai palates while exploiting procurement synergies.

Digital-wallet and loyalty-app ecosystems evolve into data-rich advertising platforms, birthing new revenue streams. For example, a cash-and-carry wholesaler partners with a global media agency to launch a retail-media network that targets SME shoppers inside and outside physical stores. Sustainability gains momentum as leading grocers sign MoUs on recyclable packaging and commit to halving single-use plastic by 2030. Exit of a foreign food-delivery platform accelerates consolidation, empowering remaining players to invest in autonomous delivery pilots and dark-kitchen expansions. Cold-chain specialists and parcel integrators vie for contracts as grocery players scale e-commerce.

Fragmentation persists in niche categories such as specialty fashion and DIY, where local brands leverage cultural resonance and agile replenishment cycles to fend off global entrants. Intellectual-property enforcement intensifies; customs authorities deploy AI-powered image recognition to intercept counterfeit shipments, safeguarding authorized retailers’ margins. Competitive intensity is expected to heighten as 5G-enabled in-store analytics mature, leveling decision-making across store sizes. Strategic emphasis on omnichannel profitability over sheer footprint growth characterizes the next strategic horizon.

Thailand Retail Industry Leaders

CP All PCL (7-Eleven Thailand)

Central Retail Corporation

Lotus’s (Ek-Chai Distribution System)

Big C Supercenter PCL

Siam Makro PCL (Makro/Cash & Carry)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: 7-Eleven announced plans to open 700 new stores in Thailand, investing THB 13 billion (USD 380 million), signaling continued confidence in the convenience store format and rural market expansion.

- June 2024: Makro launched the 'Makro Retail Media Network' in partnership with GroupM Thailand, enhancing omni-channel marketing and digital advertising for entrepreneurs.

- May 2025: Foodpanda exited the Thai market after 13 years, with the food delivery sector consolidating among Grab and Line Man Wongnai.

- October 2024: Central Group completed the acquisition of Swiss department store Globus, reinforcing its position in the global luxury retail market.

Thailand Retail Market Report Scope

A complete background analysis of the Thailand retail industry, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and market overview, is covered in the report. The Market is Segmented By Product (Food and Beverage and Tobacco Products, Personal and Household Care, Apparel, Footwear, and Accessories, Furniture, Toys, and Hobby, Industrial and Automotive, Electronic and Household Appliances, and Other Products), and By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, and Department Stores, Specialty Stores, Online and Other Distribution Channels). The report offers Market Size and forecasts for Thailand Retail Industry in Value (USD Billion) for all the above segments.

By Product Type

| Food, Beverage, and Tobacco Products |

| Personal Care and Household Care |

| Apparel, Footwear, and Accessories |

| Furniture, Toys, and Hobby |

| Industrial and Automotive |

| Electronic and Household Appliances |

| Other Products |

By Retail Channel

| Traditional Mom and Pop Retail |

| Modern Trade Retail |

| E-Commerce and Others |

By Format

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (drugstore, cash & carry, wholesaler) |

| By Product Type | Food, Beverage, and Tobacco Products |

| Personal Care and Household Care | |

| Apparel, Footwear, and Accessories | |

| Furniture, Toys, and Hobby | |

| Industrial and Automotive | |

| Electronic and Household Appliances | |

| Other Products | |

| By Retail Channel | Traditional Mom and Pop Retail |

| Modern Trade Retail | |

| E-Commerce and Others | |

| By Format | Hypermarkets |

| Supermarkets | |

| Convenience Stores | |

| Department Stores | |

| Specialty Stores | |

| Others (drugstore, cash & carry, wholesaler) |

Key Questions Answered in the Report

How large is the Thailand retail market in 2026?

The Thailand retail market size is USD 154.17 billion in 2026 and is projected to grow at a 3.66% CAGR to 2031.

Which product category leads sales value?

Food, Beverage & Tobacco accounts for 55.68% of 2025 sales, reflecting the country’s strong food culture and steady tourist demand.

What retail channel is growing fastest?

E-Commerce & Others is expanding at a 16.85% CAGR to 2031, fueled by live-stream shopping and improved nationwide fulfillment.

Why are convenience stores proliferating?

Convenience formats blend proximity, extended hours, and integrated financial services, driving a 10.15% CAGR through 2031.

How is digital payment influencing retail?

Government-backed wallets and PromptPay QR codes accelerate cashless adoption, enabling seamless omnichannel experiences and data-driven promotions.

Page last updated on: