Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

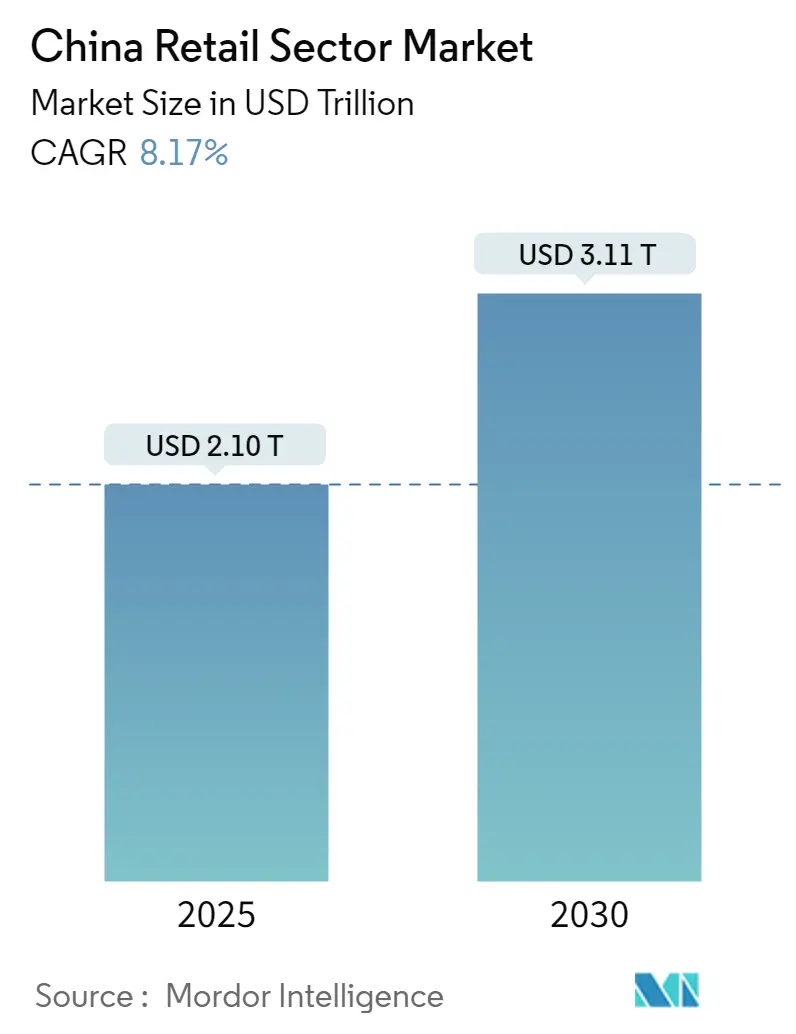

| Market Size (2025) | USD 2.10 Trillion |

| Market Size (2030) | USD 3.11 Trillion |

| Growth Rate (2025 - 2030) | 8.17% CAGR |

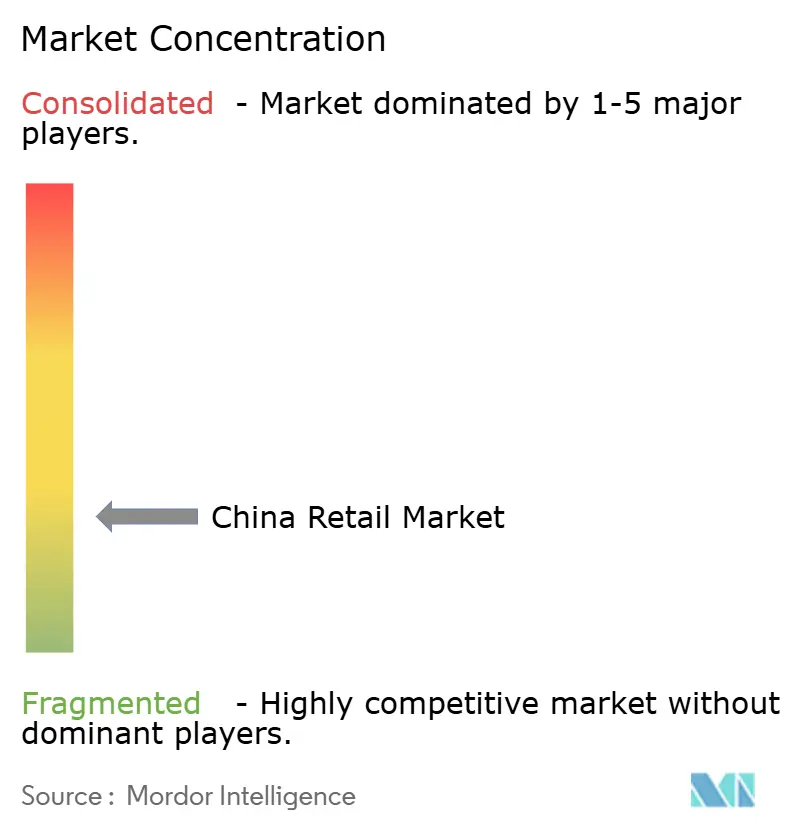

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Retail Market Analysis by Mordor Intelligence

The China retail market is valued at USD 2.1 trillion in 2025 and is forecast to reach USD 3.1 trillion by 2030, posting an 8.2% CAGR during the period. This sustained expansion reflects resilient household demand, a steady rise in disposable income and deliberate public-policy efforts to encourage domestic consumption, including the designation of 2024 as “Consumption Promotion Year” and large-scale voucher programs in major cities[1]Ministry of Commerce, “Consumption Promotion Year Notice,” english.mofcom.gov.cn. Live-stream commerce in lower-tier cities, warehouse-club expansion and tourism-linked duty-free spending add fresh momentum. Government pilots of the digital yuan and incentives for “Smart Retail” keep omnichannel investments high, while the silver-economy boom lifts premium health, wellness and leisure categories. A shrinking working-age population and tighter data-privacy rules act as headwinds, yet retailers that pivot to quality, service and technology still benefit from deep consumer pockets in key urban clusters.

Key Report Takeaways

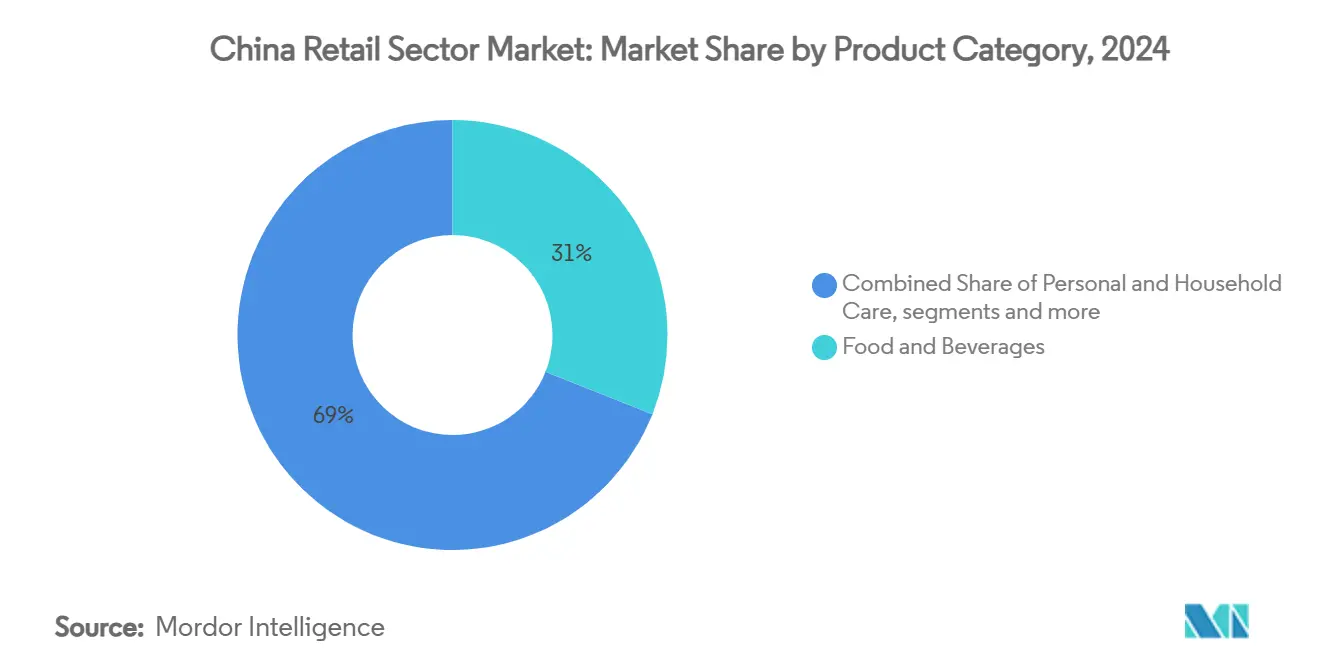

- By product category, food & beverages led with 31% revenue share in 2024; consumer electronics & appliances is projected to expand at a 9.5% CAGR to 2030 in the China retail market.

- By distribution channel, e-commerce platforms held a 34.7% share of the China retail market size in 2024, while discount & membership-club stores are forecast to grow at 13.8% CAGR through 2030.

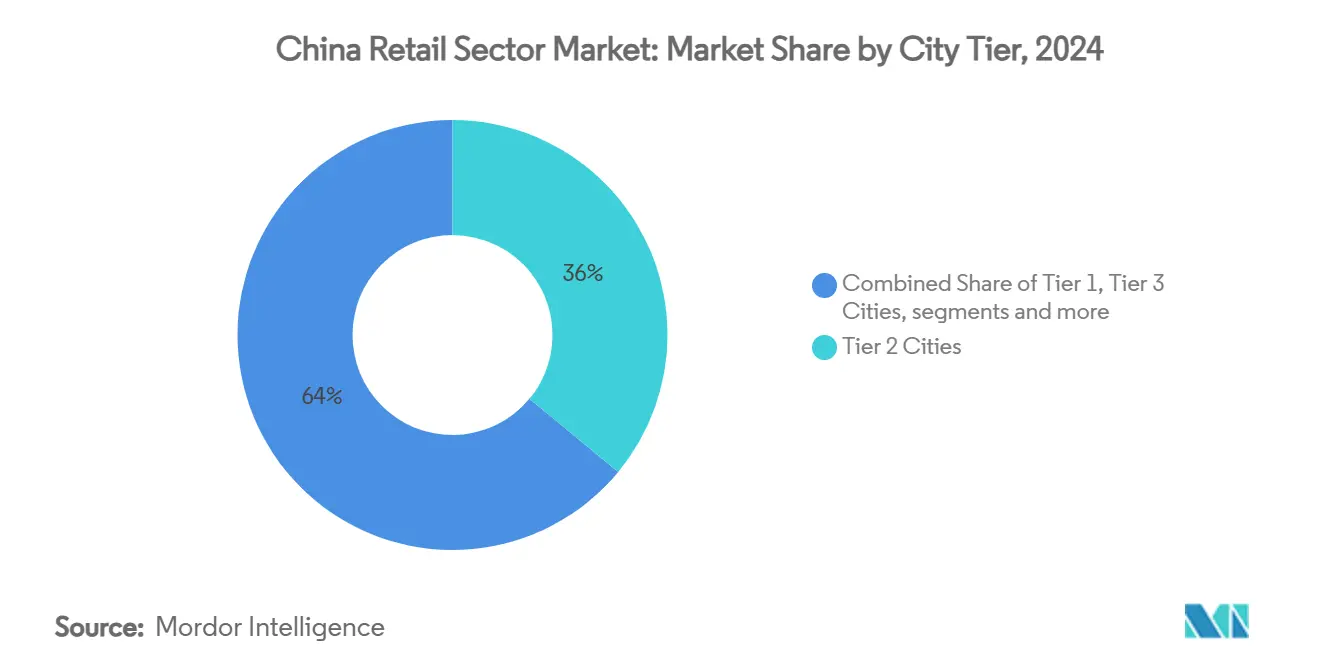

- By city tier, Tier 2 cities accounted for 36% of China retail market share in 2024; Tier 3 cities are advancing at an 11.2% CAGR between 2025 and 2030.

- By store format size, small-format outlets captured 82% of China retail market share in 2024; warehouse clubs are poised to rise at 14.4% CAGR over the forecast period.

- Alibaba, JD.com, Sun Art, Walmart and Yonghui jointly controlled more than half of sector revenue in 2024, underscoring scale advantages in logistics and technology.

China Retail Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of social & live-stream commerce in lower-tier cities | +1.8% | Tier 3 & 4 cities, with spillover to rural areas | Medium term (2-4 years) |

| Expansion of membership-based warehouse clubs lifting average basket size | +1.2% | Tier 1 & 2 cities, expanding to Tier 3 | Short term (≤ 2 years) |

| Growing silver-economy demand driving premium health & wellness categories | +1.5% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Government push for "Smart Retail" and digital-yuan pilots boosting omnichannel investment | +0.9% | 26 pilot cities, expanding nationwide | Medium term (2-4 years) |

| Rising penetration of autonomous convenience stores & community group-buy models | +0.6% | Urban centers, expanding to suburban areas | Medium term (2-4 years) |

| Rebound in experiential retail (duty-free & themed malls) via tourism revival policies | +0.8% | Hainan, major tourist destinations | Short term (≤ 2 years) |

Source: Mordor Intelligence

Rapid Adoption of Social & Live-Stream Commerce in Lower-Tier Cities

Live-stream sales reached USD 694.5 billion in 2024 with interactive formats bridging trust gaps in smaller markets. More than 600 million shoppers tune in daily, fueling direct-to-consumer growth for brands that once relied on Tier 1 outlets. Scarcity messaging and real-time chat encourage impulse purchases, while lower logistics costs help retailers penetrate vast county-level areas. The model democratizes access to premium goods, sidesteps traditional hierarchies and lifts the overall China retail market through incremental demand.

Expansion of Membership-Based Warehouse Clubs Lifting Average Basket Size

Warehouse club sales topped CNY 300 billion in 2024, and Sam’s Club alone added six outlets after notching 25% membership growth. High-quality, low-SKU assortments support bulk buying and predictable revenue streams. Curated imported food, smart appliances and private labels drive ticket sizes above traditional supermarkets, reinforcing the value-for-money narrative that resonates with the urban middle class.

Growing Silver-Economy Demand Driving Premium Health & Wellness Categories

Citizens aged 60 and above already make up 18.7% of the population, guiding retail innovation toward nutrition, mobility aids and leisure services. Digitally savvy seniors view live streaming as a trusted channel, prompting brands to launch senior-friendly interfaces and concierge delivery. Policy support for eldercare investment accelerates product diversification and helps cushion demographic drag on the China retail market.

Government Push for “Smart Retail” and Digital-Yuan Pilots Boosting Omnichannel Investment

The digital-yuan roll-out across 26 cities and an MIIT mandate that 80% of consumer-goods firms adopt e-commerce tools by 2025 widen cashless acceptance. JD.com processed nearly 20,000 digital-yuan orders during a recent festival, proving the demand for seamless payments. Coupled with AI, IoT, and blockchain upgrades, these pilots lower friction, integrate data flows, and enable retailers to tailor promotions in real-time.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price wars on e-commerce platforms eroding retailer margins | -1.4% | National, concentrated in major e-commerce hubs | Short term (≤ 2 years) |

| Demographic headwinds: shrinking working-age population | -0.8% | National, more pronounced in developed regions | Long term (≥ 4 years) |

| Regulatory crack-downs on data privacy & influencer marketing raising compliance cost | -0.6% | National, stricter enforcement in Tier 1 cities | Medium term (2-4 years) |

| Rural-urban logistics gaps limiting cold-chain coverage for fresh grocery | -0.5% | Rural areas and smaller cities | Medium term (2-4 years) |

Source: Mordor Intelligence

Intensifying Price Wars on E-Commerce Platforms Eroding Retailer Margins

The escalation of price competition among China's e-commerce giants has created a destructive cycle that threatens long-term market sustainability, with the 618 shopping festival experiencing its first decline in eight years, dropping 7% to USD 102.3 billion in 2024. Market-cap erosion of USD 157 billion across consumer stocks illustrates investor concern over profitability. Major platforms now pivot to quality and merchant support, yet the margin squeeze persists as last-mile costs rise and consumers chase bargains.

Demographic Headwinds: Shrinking Working-Age Population

The shrinking working-age population reduces the core consumer base for many retail categories while simultaneously increasing the dependency ratio, creating pressure on household spending capacity. Central bank adviser Cai Fang emphasizes the need for immediate government action to address these demographic challenges, advocating for the development of the silver economy to mitigate the conflict between consumer demand and demographic structure. The demographic shift is particularly pronounced in developed regions where birth rates have declined more rapidly, creating regional variations in consumption patterns and retail demand.

Segment Analysis

By Product Category: Electronics Drive Growth Despite Food Dominance

Food & Beverages held 31% of China's retail market share in 2024. Consumer Electronics & Appliances is projected to grow at a 9.5% CAGR on subsidies for smart-home upgrades. The segment captures rising interest in energy-efficient refrigerators and AI voice-controlled devices. Personal & Household Care rides premium skincare and hygiene habits, while sports gear gains from outdoor lifestyles. Furniture and toys enjoy stay-at-home demand, and luxury pet care emerges as a niche. The China retail market size for electronics is forecast to widen as disposable income shifts from daily essentials to functional upgrades. Apparel and accessories lag amid cautious spending, yet online-only labels use live streams to offset footfall drops.

A quality-over-quantity mindset drives willingness to pay for durable appliances and health-centric foods. Electric-vehicle peripherals such as home chargers spur cross-category bundles. Retailers leverage AI promotions tailored to product-usage scenarios, lifting attachment rates. As the silver-economy scales, ergonomic appliances, and nutritional foods strengthen loyalty. Food safety regulation improves trust in premium grocery, further anchoring Food & Beverages at the core of the China retail market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Membership Clubs Challenge E-Commerce Dominance

E-commerce claimed 34.7% of China retail market size in 2024 through frictionless payments and social-commerce integration. Membership-club stores grow 13.8% annually by curating imports, offering value packs and enhancing in-store tasting. Consumers accept annual fees for exclusive SKUs and superior cold-chain reliability. Supermarkets experiment with smaller, service-oriented setups. Convenience stores benefit from urban densification and instant-delivery apps that extend shelf space virtually. Department stores rationalize floor space toward experiential zones. Other channels like vending and community group-buy diversify reach in peri-urban districts.

The warehouse-club boom pushes omnichannel incumbents to open pick-up lockers and partner with clubs for joint promotions. Live-stream features inside club aisles create hybrid experiences. E-commerce pure-plays roll out offline showrooms to humanize engagement. Resulting channel convergence enriches consumer choice and fuels overall China retail market growth.

By City Tier: Lower-Tier Cities Accelerate Retail Modernization

Tier 2 cities controlled 36% of China's retail market share in 2024 to balanced wages and manageable rents. Tier 3 centers post 11.2% CAGR as transport links improve and local influencers spur demand via live-stream flash sales. Tier 1 markets remain innovation labs yet face saturation. Tier 4 and below enjoy policy support for rural revitalization, enabling fresh-produced e-commerce. Warehouse clubs entering Chengdu and Nanjing signal rising sophistication outside coastal hubs. Wide-area logistics networks narrow delivery gaps, distributing stock closer to county seats. These shifts extend the China retail market beyond megacity confines.

Migrating graduates and returning entrepreneurs inject new consumption styles into hometowns. Payment apps bundled with short video content educate first-time shoppers. Retailers tailor SKUs to regional taste profiles, thereby maximizing inventory turns.

Note: Segment shares of all individual segments available upon report purchase

By Store Format Size: Warehouse Clubs Disrupt Small-Format Dominance

Small-format stores under 3,000 m² accounted for 82% of China retail market share in 2024 due to high-frequency trips for staples. Warehouse clubs above 10,000 m² expand at 14.4% CAGR as families consolidate grocery runs and seek imported goods. Mid-sized supermarkets rethink floor allocation toward ready-to-eat counters and dark-store fulfilment zones. Economies of scale let large clubs price competitively without constant flash sales, easing reliance on promotions. Smaller stores counter with 24-hour self-checkout kiosks and neighborhood-driven assortments. The China retail market size for large-format outlets rises in tandem with car ownership and suburban housing.

Real-estate developers court warehouse operators to anchor mixed-use sites. Clubs launch proprietary media studios to stream cooking tutorials that stimulate in-club purchases. QR-based navigation shortens shopping time despite store girth, maintaining convenience appeal.

Geography Analysis

East China remains the most valuable region with dense urban clusters, advanced logistics and strong purchasing power. Shanghai attracts luxury brands, and 36% of convenience shops there run integrated online operations that add 10% to revenue. The Yangtze River Delta’s port network simplifies import clearance, sustaining ample SKU variety across channels. Retailers pilot AI inventory tools in the region, then roll them out nationally.

South China records the highest growth as tourism rebounds. Hainan’s duty-free success, with USD 6.13 billion in sales in 2024, underlines the power of policy-driven retail zones. Proximity to Hong Kong and Macau facilitates cross-border purchasing. Guangdong’s manufacturing base ensures fast restocking of fast-fashion and consumer electronics, aiding customer satisfaction for same-day delivery promises.

North and Central China post steady gains supported by state efforts to streamline agricultural supply chains. Cold-chain expansion boosts fresh grocery penetration beyond 65% in provincial capitals. Northeast China tackles population decline by rebranding malls as community hubs with eldercare clinics and sports halls. Southwest China benefits from high-speed rail connectivity that opens scenic cities like Chongqing and Kunming to domestic tourists. Northwest China, though smaller, presents untapped potential as e-commerce platforms build bonded warehouses to cut lead times. These diverse trajectories demonstrate how regional tailoring maximizes China retail market performance across a broad geography.

Competitive Landscape

Competition intensifies as online and offline borders fade. Alibaba, JD.com, Sun Art, Walmart, and Yonghui collectively control just over half of sector turnover yet must fend off agile newcomers. Alibaba will invest CNY 380 billion in AI and cloud through 2027 to personalize marketing and streamline supply chains[2]Alibaba Group, “Alibaba Announces RMB 380 Billion AI and Cloud Investment Plan,” alibabagroup.com. JD.com doubles down on autonomous delivery pods that cut last-mile costs. Yonghui leans on Miniso’s design expertise to refresh store layouts and reduce shrinkage.

Social-commerce stars such as Douyin shift from rock-bottom pricing to quality positioning, giving merchants better margins. Warehouse clubs expand rapidly; Sam’s Club topped CNY 80 billion in 2024 sales and plans six new openings[3]Walmart China, “Sam’s Club China Surpasses RMB 80 Billion in FY 2024 Sales,” corporate.walmart.com. Foreign grocers experiment with joint ventures to navigate compliance and local sourcing. AI chatbots like Tencent’s Yuanbao support post-purchase engagement, boosting loyalty for multiple chains.

Consolidation emerges in community groups as platforms converge on shared warehouses. Retailers collaborate with fintechs to offer installment payments that widen basket sizes. Brands invest in in-house content studios to create always-on streams that shorten discovery cycles. Despite headline risks, technology adoption and format innovation give incumbents tools to defend share while letting disruptors carve their own niches within the China retail market.

China Retail Industry Leaders

-

Alibaba Group Holding Ltd.

-

Walmart Inc.

-

JD.com Inc.

-

Sun Art Retail Group Ltd.

-

Yonghui Superstores Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Alibaba and Tencent channel CNY 380 billion into AI infrastructure and roll out consumer chatbots to elevate shopping recommendations

- May 2025: Alibaba partners with RedNote to deepen content-commerce integration amid fiercer social-commerce rivalry.

- May 2025: Walmart has broken ground on its largest Sam's Club in northern China, underscoring the U.S. retail giant's confidence in the country's expansive consumer market.

China Retail Market Report Scope

Retail is the sale of goods and services to consumers, in contrast to wholesaling, which is a sale to business or institutional customers. The report on the China retail industry provides a comprehensive evaluation of the market, with an analysis of the segments in the market. Moreover, the report provides drivers, restraints, and the competitive profile of the key players.

The China retail market is segmented by products and distribution channels. By products, the market is sub-segmented into food and beverages, personal and household care, apparel, footwear and accessories, furniture, toys and hobbies, electronic and household appliances, and other products. By distribution channels, the market is sub-segmented into supermarkets/hypermarkets, convenience stores, department stores, specialty stores, online, and other distribution channels. The report offers market size and forecasts in value (USD) for all the above segments.

| By Product Category | Food & Beverages | Fresh Food | |

| Packaged Food | |||

| Beverage - Alcoholic | |||

| Beverage - Non-Alcoholic | |||

| Personal & Household Care | Beauty & Personal Care | ||

| Home Care | |||

| Apparel, Footwear & Accessories | Apparel | ||

| Footwear | |||

| Accessories & Luxury Goods | |||

| Furniture, Toys & Hobby | Furniture & Home Decor | ||

| Toys & Baby Products | |||

| Sports & Leisure Equipment | |||

| Consumer Electronics & Appliances | Mobile & IT | ||

| Home Appliances | |||

| Other Electronics | |||

| Other Products | |||

| By Distribution Channel | Supermarkets & Hypermarkets | ||

| Convenience Stores | |||

| Department Stores | |||

| Specialty Stores | |||

| Discount & Membership Club Stores | |||

| E-commerce Online Marketplaces | |||

| Other Channels (Direct selling, vending, community group-buy) | |||

| By City Tier Tier 1 Cities | Tier 2 Cities | ||

| Tier 3 Cities | |||

| Tier 4 & Below | |||

| By Store Format Size | Large-Format | ||

| Mid-Sized | |||

| Small-Format | |||

| By Region (China) | East China | ||

| North China | |||

| Northeast China | |||

| South China | |||

| Central China | |||

| Southwest China | |||

| Northwest China | |||

By Product Category

| Food & Beverages | Fresh Food |

| Packaged Food | |

| Beverage - Alcoholic | |

| Beverage - Non-Alcoholic | |

| Personal & Household Care | Beauty & Personal Care |

| Home Care | |

| Apparel, Footwear & Accessories | Apparel |

| Footwear | |

| Accessories & Luxury Goods | |

| Furniture, Toys & Hobby | Furniture & Home Decor |

| Toys & Baby Products | |

| Sports & Leisure Equipment | |

| Consumer Electronics & Appliances | Mobile & IT |

| Home Appliances | |

| Other Electronics | |

| Other Products |

By Distribution Channel

| Supermarkets & Hypermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Discount & Membership Club Stores |

| E-commerce Online Marketplaces |

| Other Channels (Direct selling, vending, community group-buy) |

By City Tier Tier 1 Cities

| Tier 2 Cities |

| Tier 3 Cities |

| Tier 4 & Below |

By Store Format Size

| Large-Format |

| Mid-Sized |

| Small-Format |

By Region (China)

| East China |

| North China |

| Northeast China |

| South China |

| Central China |

| Southwest China |

| Northwest China |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the China retail market?

The sector is worth USD 2.1 trillion in 2025 and is projected to hit USD 3.1 trillion by 2030.

Which product category is growing fastest?

Consumer electronics & appliances is expected to post a 9.5% CAGR between 2025 and 2030.

Why are warehouse-club stores expanding so quickly?

They offer curated imports and bulk value, driving 13.8% annual growth and higher average basket sizes.

How does the digital yuan affect retailers?

Pilots across 26 cities reduce payment friction and support real-time promotions, lifting omnichannel efficiency.

Which city tiers present the highest growth opportunity?

Tier 3 cities lead with an 11.2% CAGR because of urbanization, rising incomes and live-stream commerce penetration.

Page last updated on: July 8, 2025