Risers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.86 Billion |

| Market Size (2031) | USD 13.01 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

| Fastest Growing Market | South America |

| Largest Market | South America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Risers Market Analysis by Mordor Intelligence

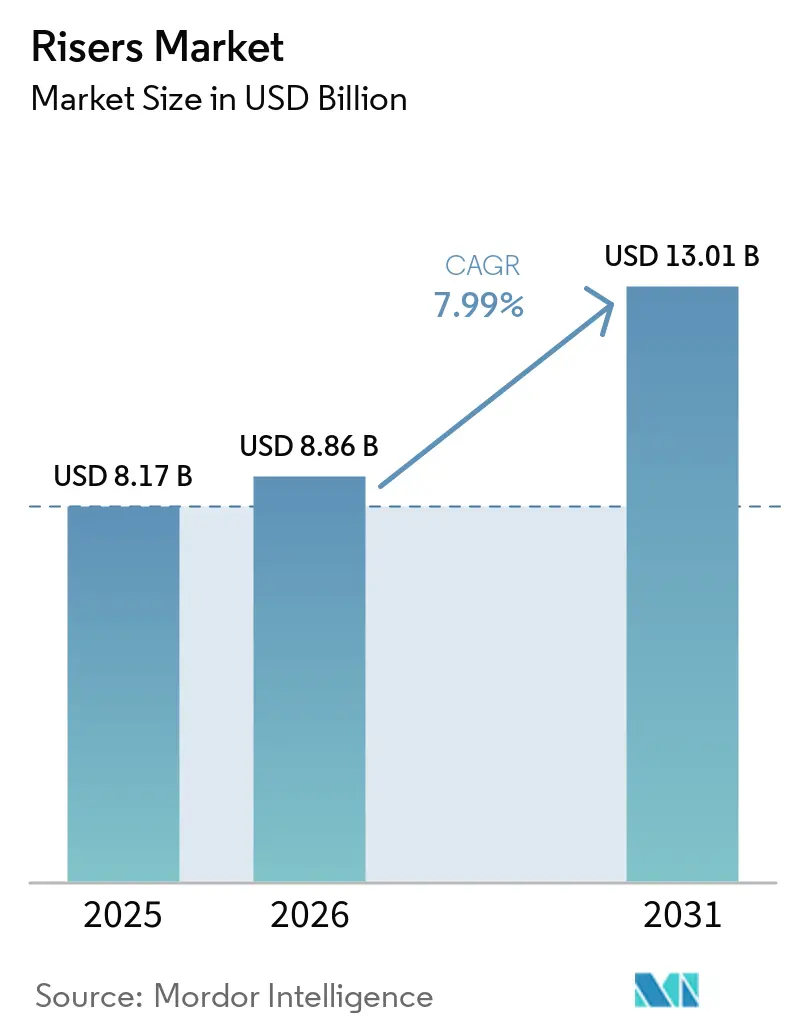

The Risers Market size was valued at USD 8.17 billion in 2025 and is estimated to grow from USD 8.86 billion in 2026 to reach USD 13.01 billion by 2031, at a CAGR of 7.99% during the forecast period (2026-2031). The growth trajectory reflects a wave of deep- and ultra-deepwater final investment decisions in Brazil and Guyana, life-extension programs across aging shallow-water assets, and swift commercialization of thermoplastic composite pipe that cuts weight and installation costs. A confluence of standardized rigid-riser designs, aggressive local-content policies in pre-salt provinces, and rising demand for carbon-capture retrofits is reshaping procurement strategies. At the same time, digital-twin adoption and embedded fiber-optic sensing are unlocking predictive maintenance models that reduce unplanned shutdowns, while supply-chain constraints for specialty forgings continue to push operators toward early material commitments. Taken together, these forces underpin a durable demand cycle that keeps the risers market well supported through the forecast horizon.

Key Report Takeaways

- By type, flexible risers led with 45.3% of the risers market share in 2025, whereas rigid designs are forecast to deliver the fastest 8.7% CAGR through 2031.

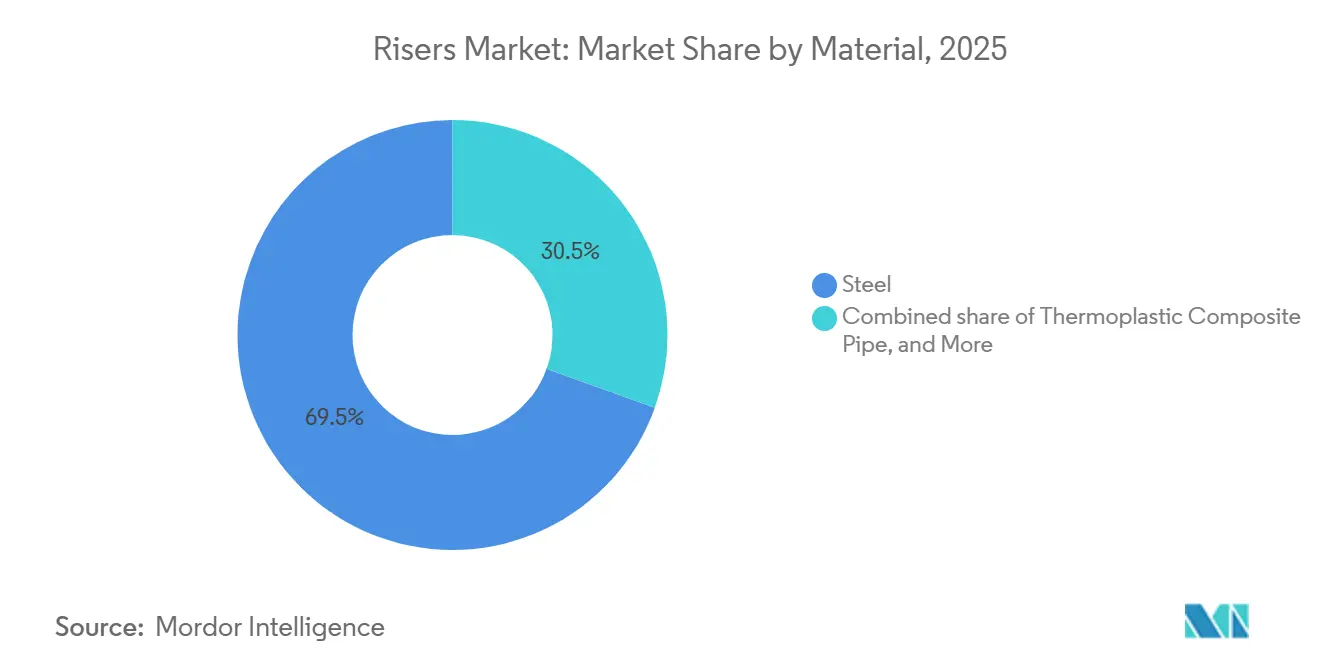

- By material, steel accounted for 69.5% of the risers market size in 2025, while composite alternatives are poised for a 9.1% CAGR over 2026-2031.

- By deployment depth, shallow-water installations represented 49.8% of 2025 volumes, yet deepwater segments are advancing at a 9.0% CAGR to 2031.

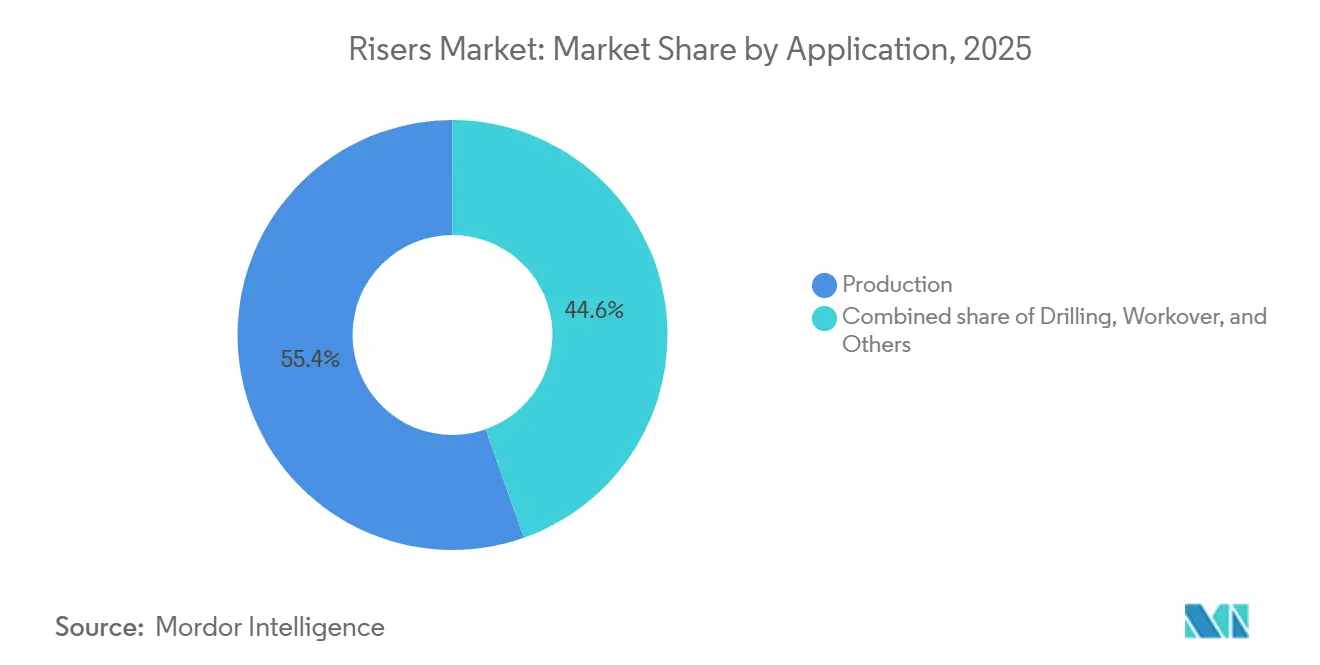

- By application, production held 55.4% of 2025 demand, whereas workover risers are expected to log an 8.9% CAGR on the back of CCS retrofits.

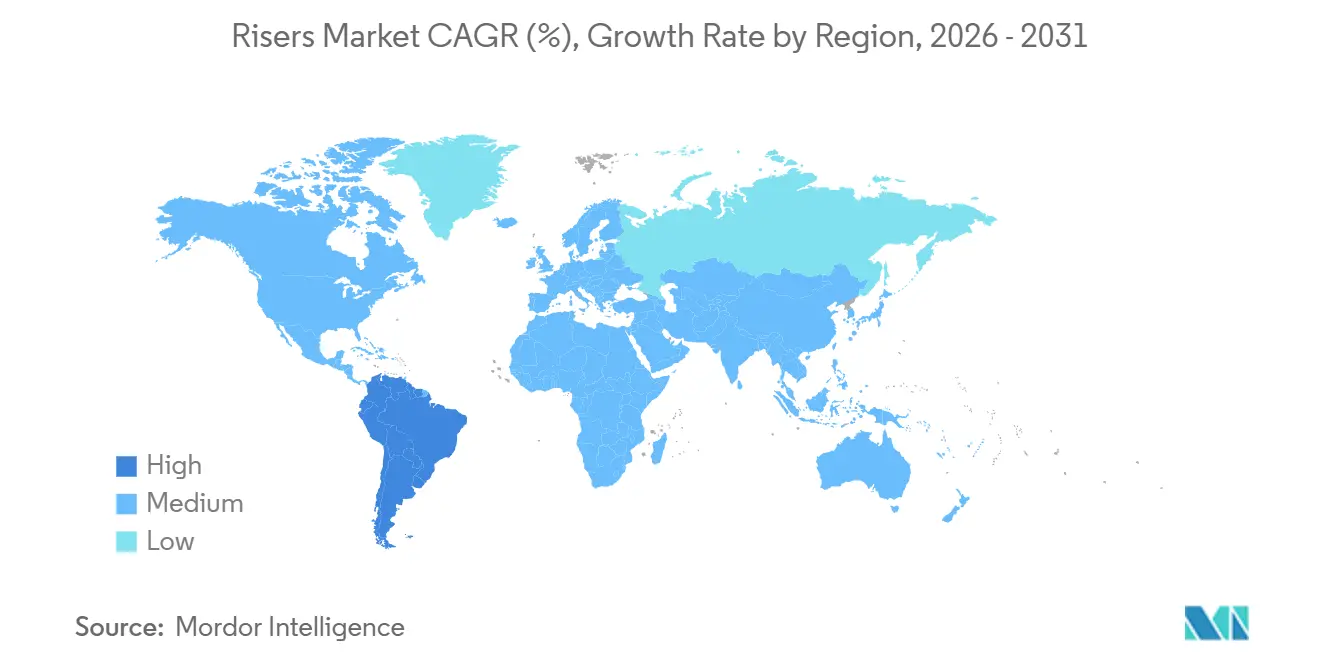

- By geography, South America commanded 35.7% of 2025 volumes and will remain the fastest-growing region at 8.4% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Risers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Revival of deep and ultra-deepwater project FIDs | +1.8% | South America, North America (Gulf of Mexico) | Medium term (2-4 years) |

| Surge in SURF package awards in Brazil and Guyana | +1.5% | South America (Brazil, Guyana) | Short term (≤2 years) |

| Life-extension demand for ageing shallow-water risers | +1.2% | North America, Europe (North Sea) | Medium term (2-4 years) |

| Rapid adoption of thermoplastic composite pipe risers | +1.0% | Global, early traction in South America, Asia-Pacific | Long term (≥4 years) |

| CCS retrofit opportunities for offshore riser infrastructure | +0.9% | Europe (North Sea), North America | Long term (≥4 years) |

| AI-enabled digital twins for predictive riser integrity | +0.7% | Global, led by South America (Petrobras) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Revival of Deep and Ultra-Deepwater Project FIDs

ExxonMobil sanctioned USD 6.8 billion for Hammerhead in Guyana, with start-up set for 2029 and riser lengths 30%-40% above shallow-water norms, while Petrobras approved SEAP II, adding 120,000 barrels per day of pre-salt capacity that requires 24 steel catenary risers rated for 2,200-meter depths [1]Petrobras Investor Relations, “SEAP II Development Plan,” petrobras.com.br. The clustering of large-scale FIDs in Brazil and Guyana, which together hold 60% of sanctioned deepwater barrels to 2028, benefits integrated SURF contractors owning local yards. Early locking of EPC contracts at stable steel prices has insulated these developments from recent metallurgy cost swings, anchoring a multiyear floor under risers market demand.

Surge in SURF Package Awards in Brazil and Guyana

Subsea7 won a USD 1.4 billion Búzios 11 award covering 18 flexible risers, whereas TechnipFMC secured a USD 250-500 million Hammerhead scope that bundles rigid-riser supply with umbilicals. Average SURF packages now exceed USD 800 million because operators consolidate supply, installation, and integrity services under single tenders, transferring performance risk and compressing fabrication lead times. Mandatory 60% local sourcing on Petrobras projects drives competitive advantage toward contractors with Brazilian fabrication capacity, creating barriers for foreign pure-play fabricators.

Life-Extension Demand for Aging Shallow-Water Risers

2H Offshore is refurbishing steel catenary and flexible risers on more than 30 Gulf of Mexico platforms, extending service life by up to seven years at one-quarter the replacement cost. Operators now embed fiber-optic DAS lines along riser spans to detect vortex-induced-vibration hotspots, cutting inspection cycles from annual to biennial. In the North Sea, 40% of installed risers have exceeded their original 20-year design life but remain structurally sound following integrity reassessment, producing a steady retrofit pipeline that sustains the risers market.

Rapid Adoption of Thermoplastic Composite Pipe Risers

Strohm obtained a DNV qualification in 2025 for thermoplastic composite pipe and has live deployments with Petrobras and Shell that achieve 70% weight savings and eliminate cathodic-protection systems. Magma Global’s carbon-fiber-reinforced m-pipe targets high-temperature wells where steel would require active cooling. Composite designs enable coilable reel-lay installation, trimming vessel days by 30% and lowering installed cost to USD 4-5 million versus USD 7-9 million for steel flexible alternatives, propelling a 9.1% CAGR for the composite segment of the risers market.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility impacting FID timing | -0.9% | Global, acute in marginal basins (West Africa, Southeast Asia) | Short term (≤2 years) |

| Escalating HSE and environmental compliance costs | -0.7% | Europe (North Sea), North America | Medium term (2-4 years) |

| Scarcity of deepwater fatigue-analysis specialists | -0.5% | Global, most acute in North America, Europe | Medium term (2-4 years) |

| Long-lead forgings and metallurgy supply-chain bottlenecks | -0.6% | Global, impacts all offshore basins | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Impacting FID Timing

The International Energy Agency foresees a 1.5-2.5 million-barrel-per-day supply surplus in 2026, which could pressure Brent below USD 70 per barrel [2]International Energy Agency, “Oil 2026,” iea.org. Deepwater projects in Brazil and Guyana remain insulated with breakevens at USD 28-35, but marginal West African prospects face deferrals of six to 12 months, trimming near-term order flow for the risers market.

Escalating HSE and Environmental Compliance Costs

UK rules effective April 2026 require operators to post financial assurance for 50-year CO₂ monitoring, adding 3%-5% to project costs [3]UK Government, “Offshore CO₂ Transportation and Storage Regulations 2026,” gov.uk. The U.S. BOEM now bases bonding on P50 rather than P70 metrics, raising upfront guarantees by USD 10-15 million for mid-tier players. These measures disproportionately impact flexible-riser installations that demand specialized annulus monitoring.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Standardization Drives Rigid Riser Velocity

Rigid designs will post an 8.7% CAGR, the fastest growth in the risers market, as operators replicate proven templates that compress engineering cycles and enable bulk sourcing. Shell’s Gulf of Mexico brownfield program achieved 95% equipment commonality across three fields, trimming front-end engineering by 40%. Flexible risers still hold 45.3% of 2025 demand thanks to superior motion compliance, with TechnipFMC’s Hammerhead order featuring electrically heated flexible lines to combat wax deposition. Hybrid concepts remain niche but vital in ultra-deepwater where top tension exceeds 1,000 tons, blending a seabed-anchored rigid section with a fatigue-resistant composite top string. The shift toward standardized rigid systems underpins procurement predictability, tilting market share toward contractors with high-capacity spoolbases.

Industry modularization also boosts aftermarket revenue: cataloged designs simplify spares stocking and streamline inspection protocols, lowering total cost of ownership. Nonetheless, flexible lines remain indispensable for complex tiebacks and life-extension programs where existing infrastructure dictates serpentine routing. Composite-steel hybrids are likely to proliferate as carbon-fiber tensile armor clears final qualification hurdles, offering weight savings that widen vessel choice and shrink installation windows in the risers market.

By Material: Composites Erode Steel’s Metallurgy Moat

Composite alternatives will advance at 9.1% CAGR, eroding steel’s 69.5% 2025 hold on the risers market size. Strohm’s thermoplastic pipe is already moving beyond water-injection service toward full production duty with Petrobras in 2027. Magma Global targets high-temperature West African wells where steel would need costly active cooling. Field data show 77.7% weight reduction and comparable tensile capability, making composites attractive for reel-lay campaigns that cannot tolerate the deck loads of steel.

Regulatory acceptance removed the last barrier when DNV endorsed non-metallic risers for permanent service. Integrated fiber-optic sensing baked into the laminate turns each composite riser into a self-monitoring asset, obviating external instrumentation. Yet steel retains primacy in ultra-high-pressure sour service above 15,000 psi, where hydrogen embrittlement of polymer matrices is still a concern. Limited availability of reel-lay vessels and high initial material cost temper adoption speed, but the lifecycle economics remain compelling, ensuring composites capture incremental risers market share through the forecast period.

By Deployment Depth: Deepwater Outpaces Shallow on Project Scale

Deepwater installations will climb at a 9.0% CAGR, eclipsing shallow-water’s mature base. Petrobras awarded Subsea7 the USD 1.4 billion Búzios 11 scope, adding 18 flexible risers at 2,100 meters, a metric emblematic of the deepwater momentum [4]Subsea7 SA, “Búzios 11 Contract Award,” subsea7.com. Shallow-water activity is pivoting toward integrity extensions, as 2H Offshore’s Gulf program illustrates, preserving existing lines rather than installing new ones. Ultra-deepwater fields above 1,500 meters require exotic alloys and advanced fatigue modeling that lengthen project cycles yet raise unit demand.

High-productivity reservoirs in Brazil and Guyana justify subsea systems with 8-12 risers per field, elevating absolute volumes even though project counts are lower than shallow peers. Shallow basins stay relevant through brownfield workovers such as Shell’s Kaikias waterflood, which injects seawater through existing rigid risers to unlock incremental barrels. Deepwater’s design complexity is being mitigated by digital twins that simulate 10,000-year storms, de-risking fatigue failure, and cementing Deepwater as the primary growth engine for the risers market.

By Application: Workover Gains as CCS Retrofits Accelerate

Production remained dominant at 55.4% of 2025 demand, yet workover risers will post an 8.9% CAGR as carbon-capture retrofits scale. Baker Hughes supplies CO₂-compatible flexible pipe rated for 5,000 psi service to Northern Lights and other European projects, opening a recurring inspection and replacement stream. Workover lines also support sidetrack operations in the Gulf of Mexico and the North Sea, where operators access bypassed pay zones using temporary riser strings.

Drilling risers maintain a presence tied to exploration cycles, but budgets have migrated toward development of proven reserves. Subsea processing trends add incremental production risers per field to handle separated or boosted fluids, intensifying hardware density on floating production vessels. Regulatory mandates for 50-year monitoring of CO₂ storage wells guarantee a multidecade service opportunity, tightening the link between the risers market and the broader decarbonization agenda.

Geography Analysis

South America accounted for 35.7% of global demand in 2025 and will expand at an 8.4% CAGR, the fastest among all regions. Petrobras’s SEAP II alone requires 24 risers rated for 10,000-psi pressures, while ExxonMobil’s Hammerhead development in Guyana adds six production risers by 2029. Streamlined Brazilian permitting now cuts approval times to 12 months, and Guyana’s USD 30 billion investment pipeline promises more than 40 new risers through 2028. The risers market benefits from predictable local-content rules that encourage regional fabrication and generate shorter logistics chains.

North America centers on brownfield optimization. Shell’s Kaikias waterflood and multiple Gulf of Mexico refurbishments keep service demand elevated, while U.S. BOEM bonding changes lift up-front cost burdens. In Europe, the North Sea consolidates around super-operators; Shell and Equinor’s Adura venture manages 140,000 boe/d under unified inspection programs that harvest economies of scale. UK carbon-capture regulations, effective in 2026, compel feasibility studies on new developments, tying future FIDs to integrated CCS concepts.

The Middle East and Asia-Pacific emerge as secondary poles. ADNOC’s SARB Deep Gas and Nasr-115 expansions add corrosion-resistant alloy risers for sour-gas production, while CNOOC ramps up South China Sea activity with rigid strings at Kaiping 18-1. Southeast Asia lags due to price uncertainty and financing constraints, but Malaysia and Indonesia remain incremental contributors. Combined, these trends diversify the geographic revenue mix and insulate the global risers market from single-basin shocks.

Competitive Landscape

The Risers Market is moderately concentrated. The pending merger of Saipem and Subsea7 will form Saipem7, amassing a €43 billion backlog and concentrating up to 40% of worldwide SURF installation capacity under one banner. The enlarged fleet of 25 pipelay vessels and six fabrication yards positions the entity to exert pricing power in Brazil and West Africa, heightening competitive pressure on mid-tier contractors. Subsea7’s record 20,000-foot riser installs at Shenandoah exemplify deepwater execution credentials that the combined firm will leverage across pre-salt tenders.

Composite specialists Strohm and Magma Global exploit weight and lifecycle advantages to win pilot projects with Petrobras and Shell, eroding the metallurgy moat of incumbents. Their DNV-qualified thermoplastic and carbon-fiber designs eliminate cathodic protection and enable reel-lay installation, opening prospects previously dominated by steel. Baker Hughes captures early-mover status in CO₂-compatible flexible pipe, while digital-twin providers 2H Offshore and CESAR expand software-as-a-service revenues by integrating physics-based models with neural networks.

Local-content policies reshape supply chains. TechnipFMC’s joint venture with Prysmian in Vila Velha secures preferential treatment in Petrobras bids, while SBM Offshore bundles FPSO leasing with riser-supply packages, offering turnkey solutions that appeal to capital-constrained operators. Competitive intensity remains high, yet supply-chain bottlenecks for specialty forgings act as a natural cap on near-term capacity expansion, keeping the risers market structurally tight through 2031.

Risers Industry Leaders

TechnipFMC

Aker Solutions

Subsea 7

NOV Inc.

Saipem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TechnipFMC was awarded an integrated engineering, procurement, construction, and installation (iEPCI®) contract for BP’s Tiber development in the Keathley Canyon area of the Gulf of Mexico. The project encompasses subsea infrastructure, including production systems, flowlines, and riser-related components, designed for one of the industry's first 20,000-psi deepwater developments, enabling next-generation high-pressure offshore production.

- April 2025: Subsea7 won Shell’s Sparta installation contract in the Garden Banks block 959, valued at USD 50-150 million, with first oil targeted for 2027.

- March 2025: Shell awarded TechnipFMC the EPCI scope for Brazil’s Gato do Mato alongside MODEC’s FPSO charter, exceeding USD 1 billion.

- March 2025: Valaris inked a two-year, USD 352 million drillship deal for DS-10 offshore West Africa, bolstering regional deepwater backlog.

Global Risers Market Report Scope

Risers in the oil and gas industry are vertical or near-vertical pipelines that link subsea wells and seabed equipment to surface facilities, such as offshore platforms or floating units. They facilitate the safe transport of hydrocarbons, drilling fluids, and control signals. Designed to endure harsh marine environments, risers can be either rigid or flexible and are critical for efficient offshore drilling, production, and intervention operations.

The global Risers Market is segmented by type, material, deployment depth, application, and geography. By type, the market is segmented into flexible risers, rigid risers, and hybrid risers. By material, the market is segmented into steel, composite, thermoplastic composite pipe, and others. By deployment depth, the market is segmented into shallow water, deepwater, and ultra-deepwater. By application, the market is segmented into drilling, production, workover, and others. The report also covers market sizes and forecasts for the global risers market across major countries in key regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Flexible Risers |

| Rigid Risers |

| Hybrid Risers |

| Steel |

| Composite |

| Thermoplastic Composite Pipe |

| Others |

| Shallow Water (Up to 500 m) |

| Deepwater (500 to 1,500 m) |

| Ultra-Deepwater (Above 1,500 m) |

| Drilling |

| Production |

| Workover |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Flexible Risers | |

| Rigid Risers | ||

| Hybrid Risers | ||

| By Material | Steel | |

| Composite | ||

| Thermoplastic Composite Pipe | ||

| Others | ||

| By Deployment Depth | Shallow Water (Up to 500 m) | |

| Deepwater (500 to 1,500 m) | ||

| Ultra-Deepwater (Above 1,500 m) | ||

| By Application | Drilling | |

| Production | ||

| Workover | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected global risers market size by 2031?

The risers market size is projected to reach USD 13.01 billion by 2031.

Which region will lead demand growth through 2031?

South America is set to expand at an 8.4% CAGR, the fastest of all regions.

Why are thermoplastic composite pipe risers gaining traction?

They cut weight by about 70%, eliminate cathodic protection, and reduce installation costs, driving a 9.1% CAGR for composite materials.

How will the Saipem-Subsea7 merger affect competition?

The deal concentrates up to 40% of global SURF capacity in one firm, raising competitive pressure on mid-tier contractors.

What role does carbon capture play in future riser demand?

CCS retrofits are boosting workover-riser orders and introduce decades-long monitoring contracts, adding a new demand stream.

Page last updated on: