Memristor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

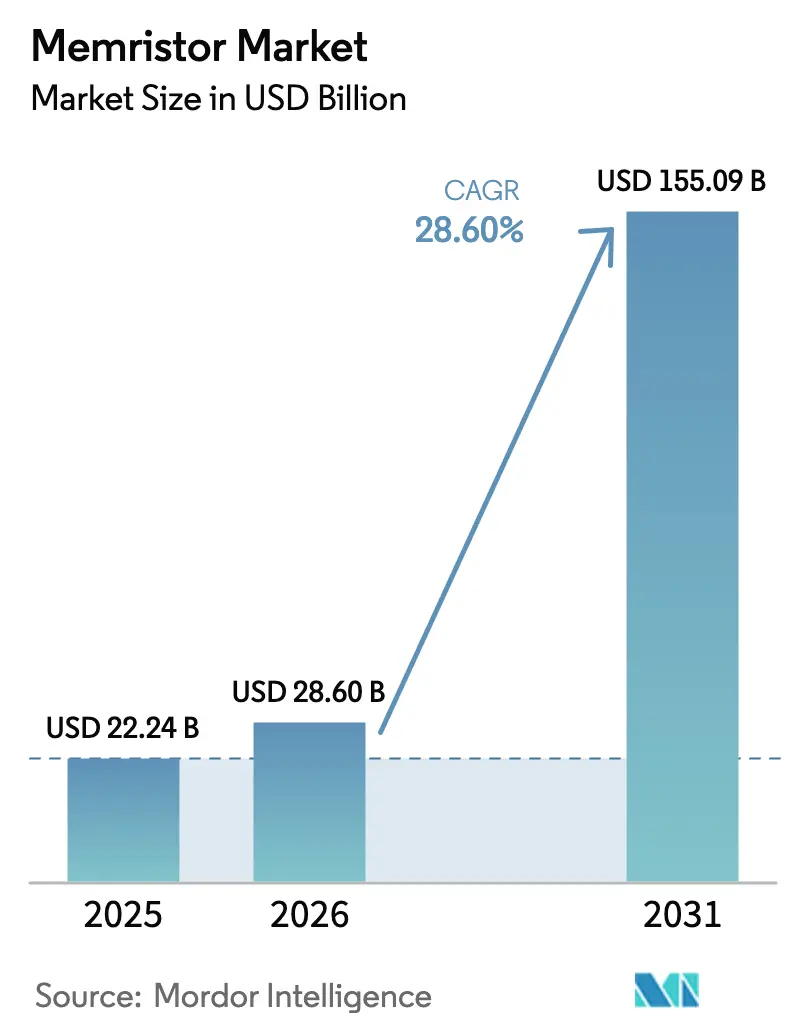

| Market Size (2026) | USD 28.60 Billion |

| Market Size (2031) | USD 155.09 Billion |

| Growth Rate (2026 - 2031) | 28.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Memristor Market Analysis by Mordor Intelligence

The memristor market size reached USD 28.6 billion in 2026 and is forecast to climb to USD 155.09 billion by 2031, advancing at a 28.6% CAGR over the period. This acceleration reflects three converging forces, namely shrinking CMOS scalability, surging edge-AI workloads, and space-grade non-volatile memory requirements. Vendor focus has shifted toward compute-centric deployments as neuromorphic arrays begin displacing pure storage use cases. Materials advances, especially in low-temperature chalcogenide and ferroelectric stacks, are improving switching speed, while heterogeneous 3D integration is allowing foundries to co-package memristive crossbars with advanced logic. On the demand side, electric-vehicle platforms, edge data centers, and autonomous robots are driving double-digit unit growth, and defense contracts are underwriting radiation-hardened variants. Competitive intensity remains high because incumbents and startups are racing to lock in first-mover design wins, yet overall pricing pressure is muted thanks to differentiated device architectures and limited high-volume supply.

Key Report Takeaways

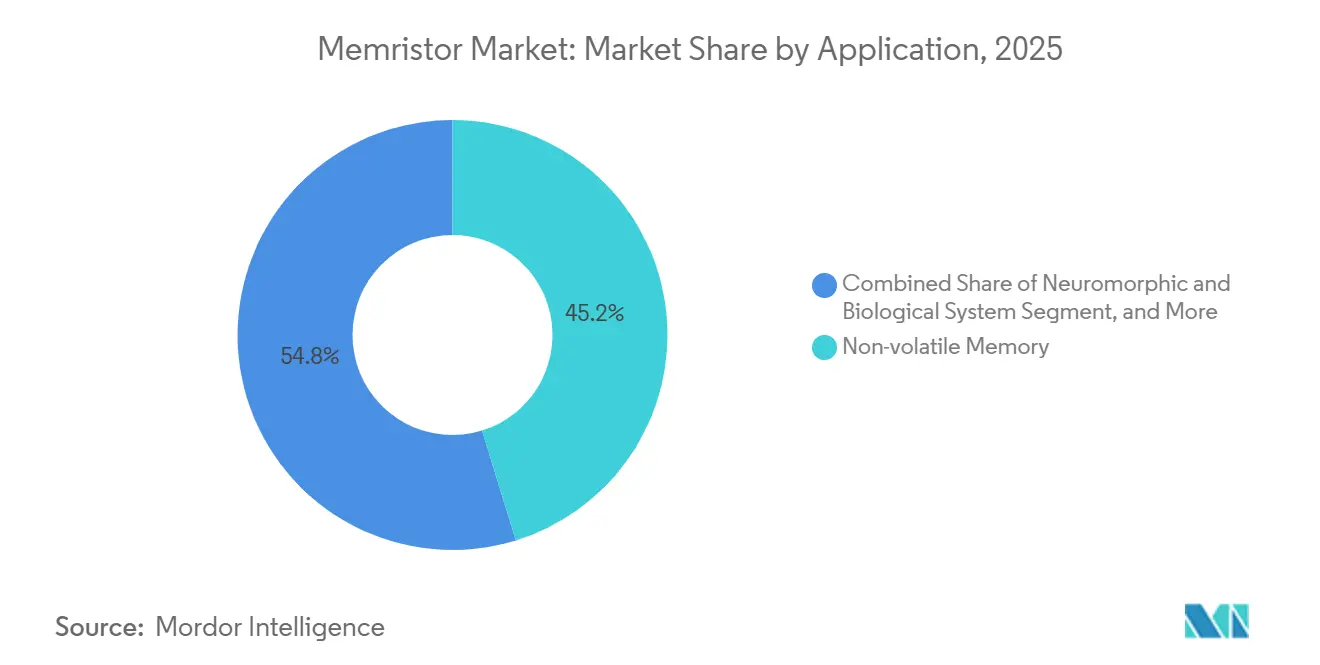

- By application, non-volatile memory led with 45.22% revenue share in 2025, while neuromorphic and biological systems are projected to expand at a 36.22% CAGR through 2031.

- By end-user industry, automotive recorded the fastest growth, posting a 27.53% CAGR through 2031, whereas consumer electronics commanded 31.55% of the memristor market share in 2025.

- By technology, spin-based and magnetic devices captured 40.22% share in 2025; molecular and ionic thin films are forecast to rise at a 32.11% CAGR to 2031.

- By material, chalcogenide layers are advancing at a 32.40% CAGR, even as metal oxides retained 37.25% share in 2025.

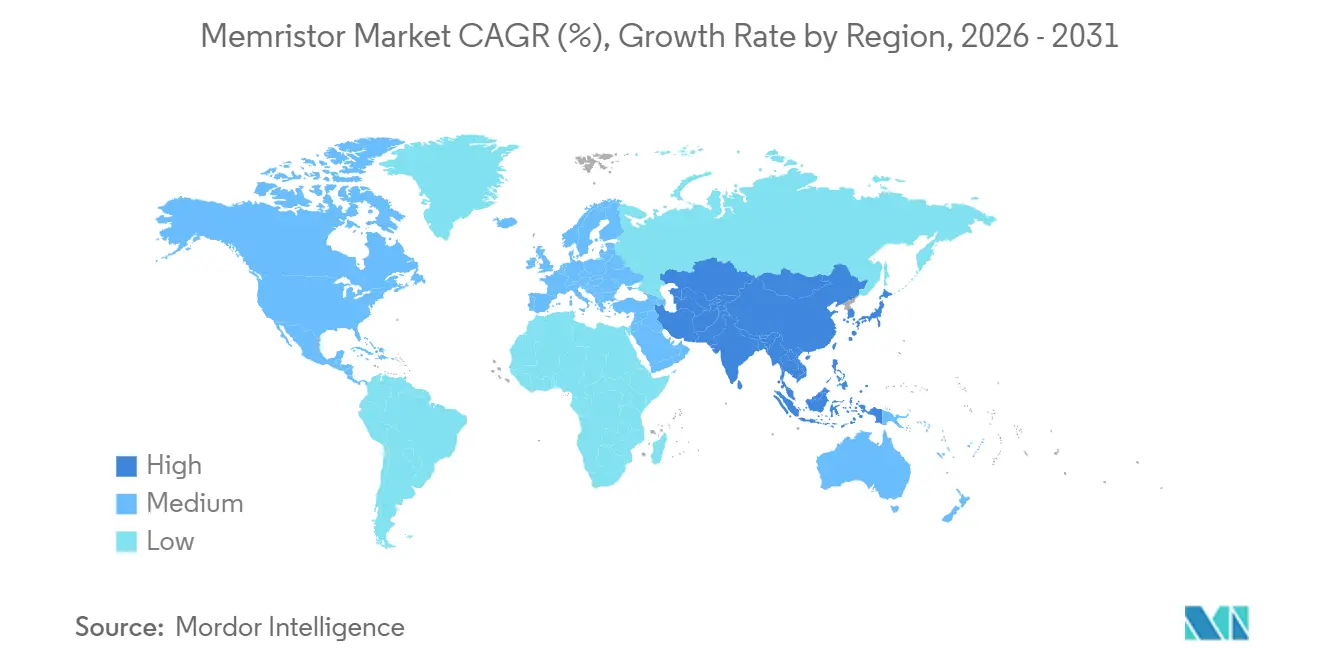

- By geography, Asia-Pacific dominated with 53.33% revenue in 2025 and is set to grow at a 21.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Memristor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for IoT, Cloud Computing, and Big Data | +12.5% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Surging Adoption of Autonomous Robots | +8.2% | Asia-Pacific manufacturing hubs, North America logistics, Europe industrial automation | Medium term (2-4 years) |

| Rising Adoption of Edge AI Accelerators Requiring In-Memory Computing | +14.3% | Global, led by Asia-Pacific consumer electronics and North America automotive | Short term (≤2 years) |

| Semiconductor Scaling Limits Pushing Beyond CMOS Memory Designs | +9.7% | Global, with foundry clusters in Taiwan, South Korea, United States | Long term (≥4 years) |

| Defense Funding for Radiation-Hardened Space Memory | +4.1% | North America and Europe, spillover to Asia-Pacific satellite builders | Long term (≥4 years) |

| Growing Focus on Carbon-Neutral Data Centers | +3.8% | Global, early adoption in Europe and North America hyperscalers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for IoT, Cloud Computing, and Big Data

Hyperscalers are deploying memristive compute-in-memory arrays to curb the 80% energy overhead linked to data movement in von Neumann cores. A fully integrated chip from Tsinghua consumes 3% of ASIC baselines, enabling real-time learning on wearables and autonomous vehicles.[1]Tsinghua University. "China makes breakthrough in system-integrated memristor computing-in-memory chips-Tsinghua University." January 1, 2024. In June 2025, SoftBank, Intel, and the University of Tokyo formed SAIMEMORY with JPY 3 billion (USD 22.2 million) seed capital to commercialize high-capacity low-power memory. Edge devices profit from zero standby leakage, and Asia-Pacific consumer-electronics vendors are quick to integrate such arrays. North American hyperscalers are piloting neuromorphic accelerators for recommendation engines, expanding the immediate addressable memristor market.

Surging Adoption of Autonomous Robots

Warehouse and factory robots demand deterministic latency that legacy DRAM-GPU stacks cannot meet. KAIST demonstrated an insect-mimicking motion detector consuming 92.9% less energy than existing designs while raising prediction accuracy. BrainChip’s Akida processor, embedding memristive synapses, has attracted OEMs that require millisecond responses. Collaborative robots across East Asian factories have become early volume customers, and Europe’s industrial automation sector is following in medium-term procurement cycles. These deployments push up unit demand for ruggedized memristors with high endurance and low-temperature drift.

Rising Adoption of Edge AI Accelerators Requiring In-Memory Computing

Edge inference in smartphones, drones, and medical monitors benefits when multiply-accumulate operations occur inside memory. A selector-less 32×32 memristor crossbar reported by KAIST in 2025 matches ideal-simulation accuracy for video background subtraction while eliminating cloud latency. TSMC’s mixed-precision processor, featuring Al₂O₃ analog cells and MoS₂ selectors, achieved 91.2% array yield plus 85% CIFAR-10 accuracy. Asia-Pacific handset brands have committed to embed such chips in 2026 flagships, and U.S. automotive Tier-1 suppliers are lining up for in-vehicle AI boards, indicating a short-term pull on the memristor market.

Semiconductor Scaling Limits Pushing Beyond CMOS Memory Designs

SRAM and DRAM scaling stalls below 5 nm, whereas memristor cells store state as resistance, achieving sub-10 nm footprints in passive crossbars. A self-rectifying Hf-SiO₂ stack delivered 320×320 arrays with 10,000:1 selectivity and 5 nW read power. Foundries in Taiwan, South Korea, and the United States now offer back-end ReRAM and MRAM options. The amended U.S. National Strategy on Microelectronics Research has prioritized memristive materials, ensuring funding lines for process development. Adoption timelines stretch over four years because of qualification cycles, yet pilot lines are already active.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity in Technological Application | -5.4% | Global, acute where design expertise is sparse | Short term (≤2 years) |

| High Switching Variability and Endurance Issues | -6.8% | Global, with strong effect on automotive and industrial users | Medium term (2-4 years) |

| Immature Design Automation Toolchains | -3.2% | Global, hitting fabless houses hardest | Medium term (2-4 years) |

| Supply-Chain Dependence on Rare-Earth Materials | -2.9% | North America and Europe exposed to Asia-Pacific mining | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Complexity in Technological Application

System-on-chip designers must co-optimize materials, analog circuits, and network algorithms, yet such multidisciplinary talent is scarce. The University of Tokyo’s multilevel TaOₓ test chip balanced 10-year retention with higher density using new activation functions unrecognized by standard frameworks. This gap forces bespoke toolchains, extends time-to-market, and raises non-recurring engineering cost. Regions with nascent ecosystems feel the pinch most, but shared reference designs expected from 2026 products should gradually reduce barriers.

High Switching Variability and Endurance Issues

Oxygen-vacancy drift in oxide devices causes stochastic resistance shifts that erode neural-network accuracy. KAIST directly imaged TiO₂ paths and showed oxygen injection stabilizes the high-resistance state, yet achieving uniformity at scale demands tight process control. Endurance often trails below 10⁶ cycles, short of automotive Grade 1 requirements. Weebit Nano’s 2025 AEC-Q100 pass proves mitigation is feasible, though qualification adds capital outlays. Research into interfacial engineering and self-compliance is forecast to alleviate the issue by 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Neuromorphic Computing Drives Next-Generation Deployments

In 2025, non-volatile memory represented 45.22% revenue, anchored by embedded flash replacements in microcontrollers. The memristor market size tied to neuromorphic and biological systems is set to grow at 36.22% CAGR as laboratories transition from simulation to production silicon. KAIST’s selector-less array demonstrated real-time learning for security cameras, proving commercial viability. Programmable logic uses, such as adaptive filters in 5G radio, are also increasing. As compute-centric architectures outpace pure storage, the memristor market will witness value shifting toward devices optimized for multiply-accumulate precision.

The pivot is underscored by Tsinghua’s integrated compute-in-memory chip, which operates at 3% of ASIC energy. Storage-class memory pilots by hyperscalers further blend the boundary between memory and logic. Secondary roles like random-number generation and physically unclonable functions add incremental demand, reinforcing the memristor market’s diversification.

By End-User Industry: Automotive Electrification Accelerates Adoption

Consumer electronics held 31.55% revenue in 2025, leveraging on-device AI for voice and camera tasks. Automotive demand is accelerating at a 27.53% CAGR as electric vehicles embed advanced driver assistance requiring sub-millisecond inference. BrainChip’s Akida processor is already integrated into pedestrian-detection modules. Edge telecom and IT buyers deploy memristive accelerators in 5G base stations to trim backhaul latency, boosting the memristor market share inside carrier infrastructure.

Healthcare devices enjoy long battery life thanks to zero leakage, while industrial automation uses memristors for adaptive robot controllers. Defense contracts, such as DARPA’s REMIND award, secure revenue streams for radiation-hardened variants. Emerging sectors, agriculture and retail among them, experiment with sensor nodes, signaling broadening addressable opportunities for the memristor market.

By Technology: Molecular Films Gain Ground in Foundry Roadmaps

Spin-based and magnetic variants captured 40.22% share in 2025 because MRAM matches high cycling needs. Yet molecular and ionic thin-film devices are forecast to climb 32.11% CAGR as atomic-layer deposition enables sub-5 nm stacks with precise stoichiometry. A ferroelectric oxide switch from the University of Tokyo exhibited giant resistance ratios suited for high-precision synapses.[2]University of Tokyo. "低電力エッジAI半導体、ReRAM CiM(Computation-in-Memory)の多値記憶による大容量化と10年記憶の両立に成功." University of Tokyo News, September 11, 2025. Hybrid CMOS-memristor chips from Weebit Nano and Crossbar underline how process compatibility opens embedded opportunities, amplifying the memristor market presence inside mainstream nodes.

3D crosspoint layouts derived from Optane concepts are re-emerging for storage-class memory, delivering byte-addressability near DRAM latency. Fujitsu’s 12-Mbit ReRAM in a 2 mm × 3 mm package exemplifies ultra-compact designs for wearables. As no single device type dominates, materials-process tailoring will persist, sustaining healthy product segmentation across the memristor market.

By Material: Chalcogenide Switching Layers Enable Passive Arrays

Metal oxides led with 37.25% share in 2025 due to established hafnium-oxide recipes. Chalcogenides, however, are racing ahead at a 32.40% CAGR, backed by sub-nanosecond switching in passive arrays. A Cu₂-ₓS device showed 10,000:1 on-off ratio with 0.5 V set voltage, fabricated at room temperature, aligning with flexible electronics roadmaps. Ferroelectric hafnia-zirconia stacks offer up to 1,000 conductance levels, opening analog precision for neuromorphic chips. Two-dimensional materials such as MoS₂ deliver atomic-scale layers and 10 million-cycle endurance, suggesting long-term integration paths.

Spintronic tunnel junctions remain valuable for high endurance although process complexity is higher. Organic polymers fit large-area printed sensors but still face retention limits. The broad palette empowers designers to fine-tune devices for sector-specific needs, a trend that sustains differentiation within the global memristor market.

Geography Analysis

Asia-Pacific led the memristor market with 53.33% revenue in 2025 and is projected to grow at 21.90% CAGR through 2031. Japan earmarked JPY 10 trillion (USD 67 billion) for semiconductor programs, underpinning ventures like SAIMEMORY. China’s Tsinghua University delivered a compute-in-memory chip consuming 3% of ASIC baselines, while South Korea’s KAIST unveiled phase-change and neuromorphic breakthroughs during 2024-2025.[3]KAIST News Center. "KAIST NEWS CENTER." January 17, 2025. Taiwan’s TSMC co-authored multiple Nature papers on memristive integration, signaling foundry scale-up. India and Southeast Asian states are enhancing design education, yet their memristor ecosystems remain early-stage.

North America ranked second in 2025, propelled by defense needs and hyperscaler AI investment. DARPA’s USD 11.6 million REMIND grant funds space-grade ReRAM, and amended U.S. microelectronics strategy lists memristive materials as national priorities. IBM and Intel continue research on phase-change and neuromorphic architectures, while Canada and Mexico contribute packaging and design talent.

Europe followed, with Germany, France, and the United Kingdom piloting advanced driver assistance and predictive-maintenance accelerators. The European Space Agency evaluates memristor radiation tolerance for deep-space probes. South America, the Middle East, and Africa show nascent but rising interest, especially in smart-city deployments, yet supply-chain constraints limit rapid scaling. Asia-Pacific and North America are therefore set to maintain dominant memristor market positions through 2031.

Regulatory Landscape

Technical standardization and trade policy are increasingly tied to memristor commercialization, especially for neuromorphic and embedded non-volatile memory use cases. In September 2024, BSI published BS EN IEC 63550-3 to standardize evaluation of spike-dependent plasticity in memristor devices, which helps align device characterization across suppliers and research-to-product transitions. In China, the State Administration for Market Regulation implemented GB/T 46567.1-2025 on October 31, 2025, specifying test methods for two-terminal bipolar memristor basic characteristics, supporting more consistent qualification and procurement specifications.

Cross-border shipments and supply planning are also affected by semiconductor trade measures that can influence memristor-containing ICs and related process flows. USTR actions under Section 301 (effective December 23, 2025, with a scheduled rate increase on June 23, 2027) and U.S. enforcement actions in January 2026 tied to semiconductor import adjustments add compliance workload around classification and performance-based thresholds, with downstream impacts across foundry sourcing, packaging location, and customer qualification timelines.

Value Chain Analysis

The memristor value chain begins with materials and device-stack inputs (metal oxides, chalcogenides, ferroelectric stacks, and selectors), then moves into wafer fabrication and integration steps that typically use CMOS-compatible back-end-of-line modules. Commercialization increasingly depends on access to established foundry flows and PDKs, as indicated by Weebit Nano taping out an embedded ReRAM demonstration in DB HiTek's 130 nm BCD process (July 2024) and by TetraMem completing silicon validation of its MLX200 analog in-memory computing SoC on TSMC 22 nm (May 2026). Equipment, metrology, and reliability test providers then support characterization, variability control, and endurance screening, which remain key bottlenecks for automotive and industrial-grade adoption.

On the downstream side, device vendors and IP holders work with system companies and OEMs across consumer electronics, automotive Tier-1s, and industrial automation to qualify parts and design in compute-in-memory or neuromorphic accelerators. Partnerships are a common route to scale, including TetraMem and NY CREATES collaborating to demonstrate memristor-based RRAM arrays on a 300 mm platform (July 2024), and CHIPS-linked programs such as the Microelectronics Commons award supporting collaborations among UMass Amherst, TetraMem, NY CREATES, and GlobalFoundries (October 2024). Distribution and deployment typically run through module and board integrators for edge AI hardware, where software tooling and model mapping, along with customer qualification, remain gating steps.

Competitive Landscape

Competition is fragmented, reflecting rapid materials innovation and divergent application targets. Samsung, Micron, SK hynix, and Intel exploit mature fabs and client bases, integrating memristors into hybrid products, although DRAM and NAND remain their revenue anchors. Startups such as Crossbar, Weebit Nano, and 4DS Memory leverage agility, focusing on automotive-qualified embedded ReRAM. Weebit Nano secured AEC-Q100 Grade 1 in 2025 and taped out with onsemi, marking a key reliability milestone. Crossbar announced production-ready 1 nm cells suitable for high-density logic integration. University spin-outs like SAIMEMORY bridge academic IP with industrial scale.

Heterogeneous 3D integration offers a white-space opportunity. TSMC’s mixed-precision compute-in-memory test chip validated commercial viability for stacking analog arrays atop logic. U.S. CHIPS funds support shared pilot lines, lowering barriers for smaller firms. Differentiation now hinges on accelerating materials advances, ferroelectric for precision, chalcogenide for speed, 2D films for thickness, and matching them to sector demands. The memristor market therefore exhibits healthy rivalry yet no single dominant player, supporting steady innovation.

Memristor Industry Leaders

-

Crossbar Inc.

-

IBM Corporation

-

Knowm Inc.

-

Samsung Group

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace sits at the intersection of energy-constrained edge AI and manufacturable in-memory computing, where proof points are shifting beyond single-device demos toward SoC validation and wafer-level integration. In July 2026, SK hynix and TetraMem validated a memristor-based in-memory computing SoC reported at 21.3 TOPS/W at 100 MHz in a 65 nm process, reinforcing demand for memristive compute fabrics in edge deployments. On the manufacturability side, DGIST reported wafer-level progress (a 4-inch wafer crossbar circuit with about 95% yield in November 2025), showing that yield engineering and co-design approaches are being used to narrow the gap between laboratory arrays and scalable hardware.

Opportunities also cluster around standards-driven qualification and CMOS-compatible stacks that can fit into established semiconductor supply chains. New device approaches reported in 2026, including CMOS-compatible self-rectifying memristors using HfO2-ZrO2 with 10 Gb storage capacity (Nature Communications, May 2026), point to routes for addressing sneak currents and integration constraints that limit dense arrays. As more programs target toolchains and end-to-end system benchmarks (for example, published neuromorphic benchmarks in June 2026), vendors that combine reliable device behavior with software mapping and qualification support have a clearer path to design wins in automotive electronics, industrial automation, and security-oriented hardware modules.

Recent Industry Developments

- July 2026: SK hynix and TetraMem validated a memristor-based in-memory computing SoC for edge AI, reporting 21.3 TOPS/W at 100 MHz in a 65 nm process. The result highlights rising collaboration between memory manufacturers and memristor compute startups to translate device concepts into measurable system-level efficiency. It also increases competitive focus on throughput, toolchains, and manufacturability needed to turn efficiency demonstrations into deployable silicon platforms.

- June 2026: IBM announced a sub-1 nanometer chip technology based on a 3D nanostack transistor architecture aimed at high-performance AI workloads. While not a memristor product launch, the milestone reflects the industry's push toward 3D integration to overcome planar scaling limits that also support compute-in-memory roadmaps. This strengthens the strategic backdrop for heterogeneous stacking of emerging memories, including memristive arrays, alongside advanced logic.

- October 2024: TDK, CEA, and Tohoku University announced a joint development partnership for a spin memristor targeting neuromorphic AI applications. The collaboration signals sustained R&D investment in alternative memristor modalities beyond oxide ReRAM, with an emphasis on low-power operation and neuromorphic functionality. It also expands the supplier and IP ecosystem that downstream OEMs can draw on when evaluating device architectures for edge inference hardware.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the memristor market is defined as revenues generated from memristor devices and related implementations used in memory, logic, and neuromorphic computing across key end-use industries, counted at the point of sale in USD.

Scope exclusions: This sizing excludes the broader non-volatile memory market, conventional CMOS-only components, and downstream system-level services where memristors are not the primary value driver.

Segmentation Overview

-

By Application

- Non-volatile Memory

- Neuromorphic and Biological System

- Programmable Logic and Signal Processing

- Emerging Data Storage

- Other Applications

-

By End-user Industry

- Consumer Electronics

- IT and Telecom

- Automotive

- Healthcare

- Industrial Automation

- Defense and Aerospace

- Other End-user Industries

-

By Technology

- Molecular and Ionic Thin Film

- Spin-based and Magnetic Memristor

- Hybrid CMOS-Memristor

- 3D Crosspoint

- Other Technologies

-

By Material

- Metal Oxide

- Chalcogenide

- Spintronic

- Organic Polymer

- Ferroelectric

- Other Materials

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with grounding the market in what can be checked publicly, and then building a clean list of use cases where memristors are actually designed in. We relied on sources such as IEEE and other peer-reviewed journals, USPTO and WIPO patent databases, and standards or research notes from bodies like ISO or IEC where relevant for electronics materials and reliability.

To anchor the demand side, we also reviewed statistics and publications from sources such as the World Bank, OECD, and national statistical agencies that track electronics production, trade, and industrial output. On the supply and ecosystem side, we used company filings, investor presentations, conference papers, association websites, and reputed press coverage to map commercialization timelines and likely shipment readiness. For cross-checking financial context and product positioning, we also used a paid subscription for company financials and intelligence. These desk sources are illustrative, and many additional public references were used to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary inputs were used to sanity-check what desk sources cannot fully confirm, especially adoption timing, pricing expectations, and where pilots convert into repeat orders. We spoke with a mix of device ecosystem participants, system integrators, and end-user engineering or procurement roles across major regions so assumptions could be corrected before the model was finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 43% | EMEA: 32% |

| Smaller Players: 19% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing uses a top-down build that reconstructs the addressable demand pool from electronics output and compute adoption signals, and then filters by realistic memristor penetration by application. We then corroborated totals with selective bottom-up approximations, such as sampled average selling price ranges multiplied by plausible volumes in a few priority applications, followed by channel and expert checks to adjust outliers.

Key inputs for this market include wafer and fab capacity expansion signals tied to advanced nodes, the pace of edge AI deployments that favor in-memory compute, the shipment outlook for automotive electronics, and the cadence of new embedded non-volatile memory design wins. We also tracked typical device learning curves that influence ASP progression, plus the mix shift between memory, programmable logic, and neuromorphic use cases, since this mix changes the value per unit shipped.

For forecasting, scenario analysis was applied around commercialization timing, qualification cycles, and ASP decline paths, and then the chosen path was aligned to what primary respondents considered achievable under current manufacturing readiness. Where bottom-up pieces had gaps, conservative ranges were used and then tightened using application-level adoption constraints so the final totals stayed realistic.

Data Validation & Update Cycle

Outputs were checked in several steps so the final numbers stay consistent with real-world signals. We compared year-by-year results against independent indicators like electronics output trends, regional manufacturing activity, and adoption timelines discussed in interviews, and then investigated any sharp jumps before internal sign-off.

When large variances appeared across regions or applications, assumptions were revisited and experts were re-contacted to confirm what changed and what did not. The report is refreshed annually, and interim updates are made when material events affect demand or supply expectations. Before delivery, a final review pass is completed so clients receive the most current view possible.

Mordor Intelligence's Memristor Market Size Compared Against Other Published Estimates

Published market sizes for memristors can look far apart because the category is still early, and many sources use different cutoffs for what counts as a memristor revenue versus adjacent non-volatile memory products. Differences also come from which applications are counted as in-scope, how quickly pricing is assumed to fall, and whether forecasts assume fast qualification in automotive and industrial uses.

The table shows a much higher 2026 value than several 2025 base-year snapshots, and in Mordor Intelligence's model the scope counts revenues across applications like non-volatile memory, programmable logic, and neuromorphic systems across end-use industries, rather than limiting the market to near-term commercial shipments only.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 28.60 B (2026) | |

| Global Consultancy A | USD 0.41 B (2025) | Uses a 2025 base year and appears to emphasize currently commercialized volumes, which can undercount pilot-to-production ramps in neuromorphic and embedded memory use cases, and it may apply a tighter definition of memristor device revenues. |

| Industry Publisher B | USD 0.59 B (2025) | Bases the market on a different timing window and may bundle or exclude certain technology groupings inconsistently, and the ASP decline and adoption speed assumptions can be more aggressive or conservative without clear external checks. |

Overall, the spread mainly comes from scope boundaries, base-year choice, and how adoption timing is treated in early-stage applications. By tying assumptions to observable electronics and compute indicators and then pressure-testing them through interviews, the estimate stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the projected revenue for the global memristor market in 2031?

The memristor market is forecast to reach USD 155.09 billion by 2031.

Which region leads current memristor adoption?

Asia-Pacific commanded 53.33% revenue in 2025 and maintains the lead through 2031.

Why are memristors favored for edge AI hardware?

Memristors perform multiply-accumulate operations inside memory, cutting energy and latency compared with DRAM-GPU architectures.

How fast is automotive demand for memristors growing?

Automotive applications are expanding at a 27.53% CAGR between 2026 and 2031.

Which material category is growing the quickest?

Chalcogenide switching layers are advancing at a 32.40% CAGR as demonstrations of sub-nanosecond switching scale toward production.

What is the main technological hurdle facing memristor commercialization?

High switching variability and limited endurance still constrain reliability, especially for automotive-grade and industrial uses.

Page last updated on: