In-memory Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

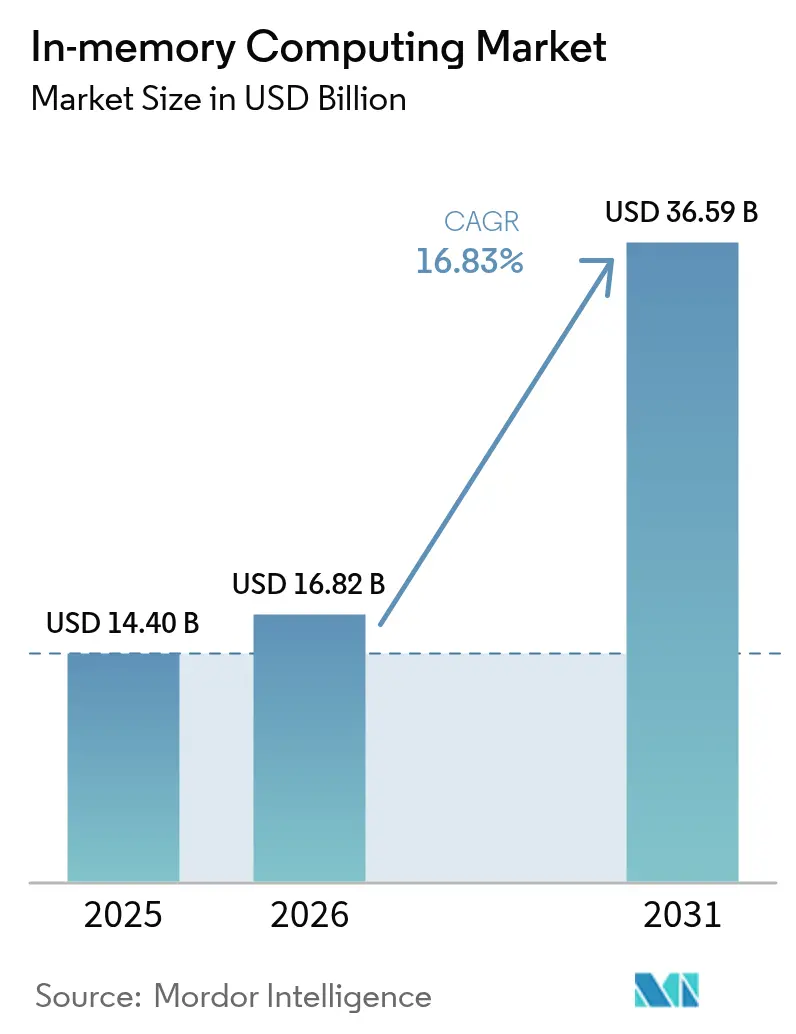

| Market Size (2026) | USD 16.82 Billion |

| Market Size (2031) | USD 36.59 Billion |

| Growth Rate (2026 - 2031) | 16.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

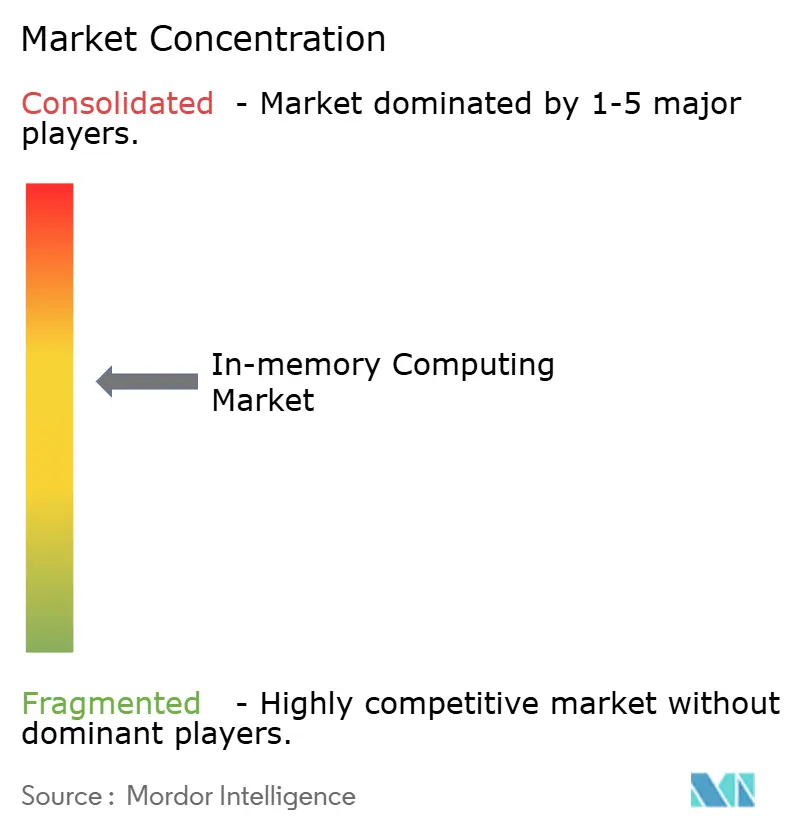

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-memory Computing Market Analysis by Mordor Intelligence

The global in-memory computing market size is expected to grow from USD 14.4 billion in 2025 to USD 16.82 billion in 2026 and is forecast to reach USD 36.59 billion by 2031 at 16.83% CAGR over 2026-2031. A steep rise in AI-driven workloads, plummeting persistent-memory pricing, and mounting expectations for sub-millisecond response times are pushing enterprises to redesign data architectures around memory-resident processing. Declining cost per gigabyte of storage-class memory enables larger data sets to remain in-memory, while CXL-enabled disaggregated clusters make capacity additions almost frictionless. Cloud hyperscalers now expose serverless in-memory services that scale instantly, letting even mid-market firms match the speed once reserved for the largest banks. Edge deployments are accelerating as sovereign AI regulations steer latency-sensitive inference to national boundaries. Together, these factors elevate data velocity to a strategic differentiator across every major industry vertical.[1]Christine Donato, “Mercedes-AMG Intensifies Speed with Real-Time Analytics,” SAP Community, community.sap.com

Key Report Takeaways

- By component, in-memory data management platforms held 61.34% of the in-memory computing market share in 2025, while in-memory application platforms are forecast to achieve a 21.85% CAGR through 2031.

- By deployment mode, cloud/SaaS led with 70.88% revenue share in 2025 and is advancing at a 26.95% CAGR to 2031.

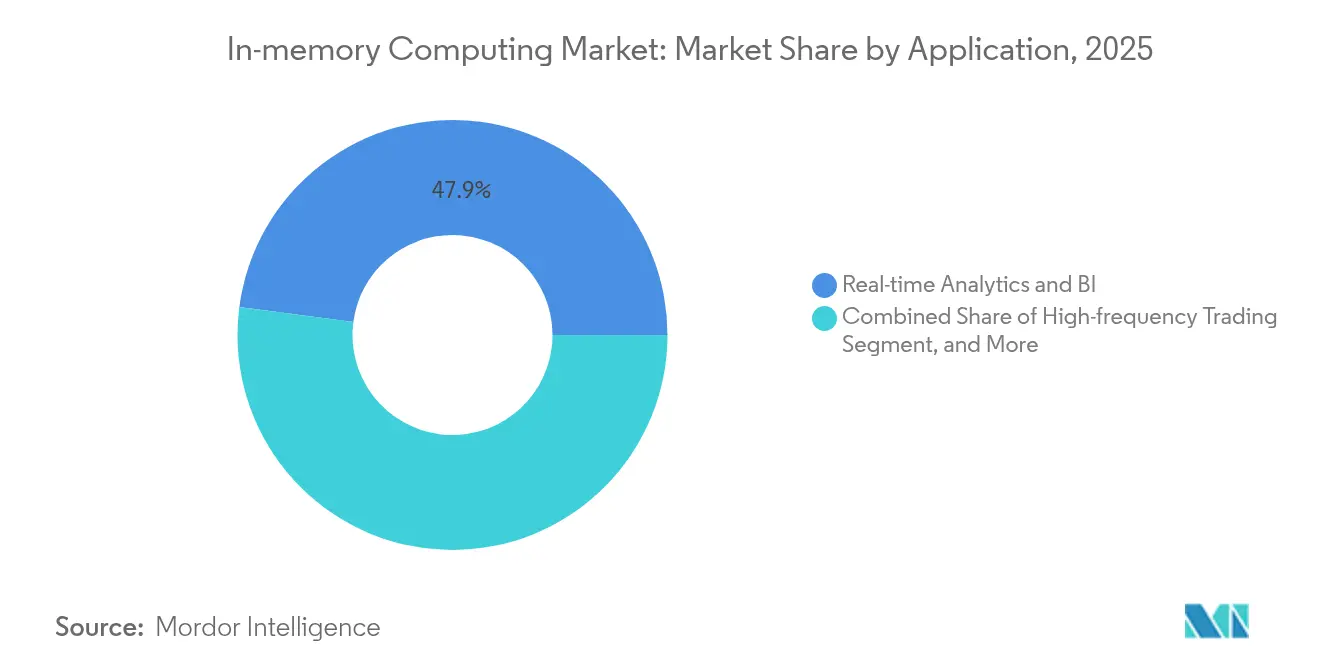

- By application, real-time analytics captured 47.92% of revenue in 2025; IoT/edge stream processing is projected to expand at a 30.18% CAGR through 2031.

- By end-user vertical, BFSI commanded 29.12% of spending in 2025, whereas healthcare and life sciences are growing fastest at a 23.05% CAGR.

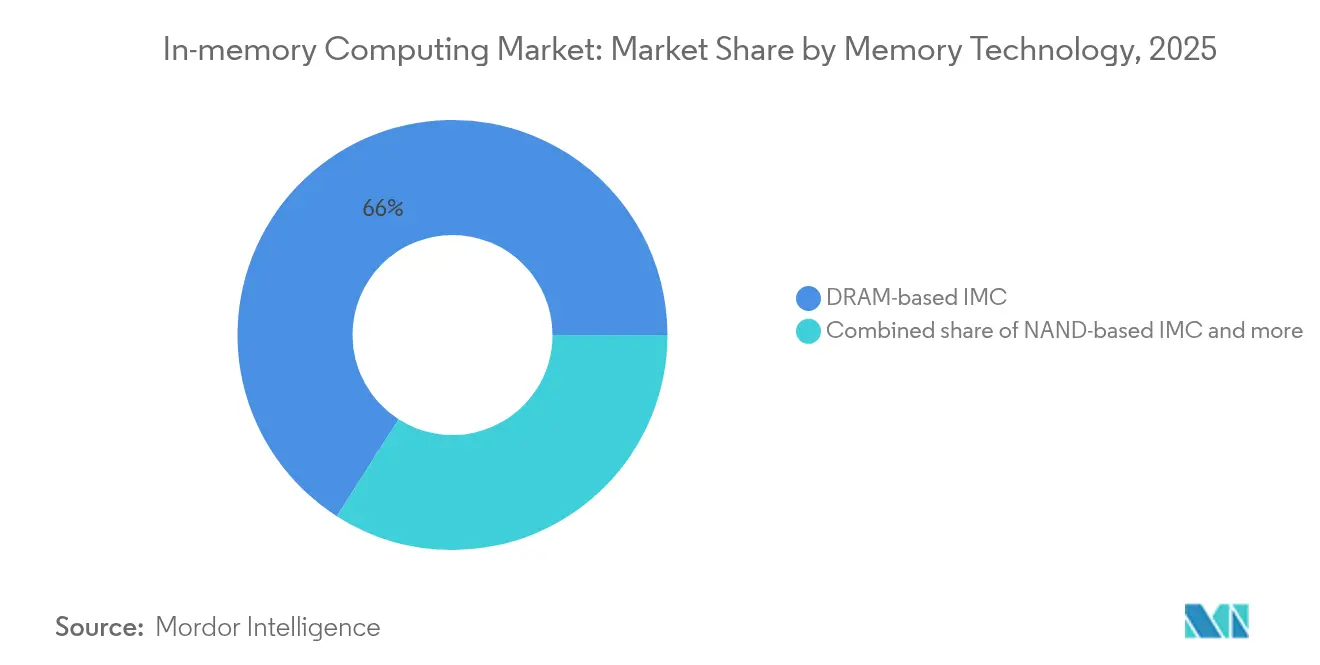

- By memory technology, DRAM accounted for 65.95% of revenue in 2025, while storage-class memory is poised for a 28.62% CAGR over the forecast period.

- By geography, North America contributed 37.25% of 2025 revenue; Asia-Pacific is the fastest-growing region with a 20.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of In-memory Computing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of Big Data | +4.20% | Global | Medium term (2-4 years) |

| Growing Need for Rapid Data Processing | +3.80% | North America and EU | Short term (≤ 2 years) |

| Proliferation of AI-centric Workloads (LLMs, vector search) | +5.10% | Global, concentrated in US and China | Short term (≤ 2 years) |

| Declining Cost/GB of Persistent Memory | +2.30% | Global | Long term (≥ 4 years) |

| Rising Adoption of Real-time Fraud Detection in BFSI | +1.20% | North America and EU | Medium term (2-4 years) |

| Edge-side In-Memory Analytics for 5G Telco Clouds | +0.50% | APAC core, spill-over to global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of Big Data

Organizations now generate multi-quintillion-byte data streams that must be queried in real time, forcing a shift from batch processing to streaming architectures anchored in memory-centric platforms. Healthcare providers run continuous patient-monitoring pipelines that flag clinical anomalies within seconds, while high-frequency traders move billions of dollars on microsecond calculations. [2]Jieyi Li, “High-Performance Computing in Healthcare: An Automatic Literature Analysis Perspective,” Journal of Big Data, journalofbigdata.springeropen.com

Growing Need for Rapid Data Processing

Customer interactions, factory automation, and connected vehicles demand latencies measured in microseconds. Mercedes-AMG cut engine test-cycle times by 94% after adopting a real-time in-memory analytics layer, effectively gaining an extra production day each week.

Proliferation of AI-centric Workloads

Large language models, vector search, and embedding stores saturate traditional memory bandwidth. Processing-in-memory architectures show up to 6.94× lower TCO per queries-per-second than GPU-only baselines, making specialized in-memory fabrics integral to future inference clusters.

Declining Cost/GB of Persistent Memory

Next-generation ferroelectric HfO2 DRAM+ promises near-DRAM speed, non-volatility, and node scalability below 10 nm, narrowing the cost gap with NAND and spurring broader enterprise trials. [4]Skye Jacobs, “Next-Gen DRAM+ Could Transform AI and Edge Computing,” TechSpot, techspot.com

Restraints Impact Analysis of In-memory Computing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of DRAM at Hyperscale | -2.80% | Global | Short term (≤ 2 years) |

| Data Gravity and Inter-cluster Latency | -1.50% | Global | Medium term (2-4 years) |

| Vendor Lock-in Concerns for Proprietary IMC Appliances | -1.20% | North America and EU | Long term (≥ 4 years) |

| Shortage of Skilled IMC Architects & Developers | -0.80% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of DRAM at Hyperscale

DRAM price spikes of 50% in early 2025 raised the total cost of ownership for large clusters, delaying refresh cycles for memory-intensive workloads.

Shortage of Skilled IMC Architects and Developers

Limited pools of distributed-systems specialists lengthen project timelines and push enterprises toward managed cloud services that mask complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

In-memory Computing Market Segment Analysis

By Component:

Platforms Drive Enterprise AdoptionIn-memory data management platforms held 61.34% revenue in 2025, underscoring demand for ACID-compliant, drop-in replacements to entrenched databases. Many banks migrated core analytics workloads without rewriting applications, capturing latency cuts of 20-40 ms per query. In contrast, in-memory application platforms are forecast to grow at 21.85% CAGR as digital-native firms design real-time microservices from the ground up. The component landscape is converging vendors weave SQL, streaming, and vector search into unified fabrics that house operational and analytical workloads side-by-side, shrinking data-movement overheads and easing DevOps.

By Deployment Mode:

Cloud Dominance AcceleratesCloud models accounted for 70.88% revenue in 2025 and will outpace the overall in-memory computing market through 2031. Hyperscalers bundle high-memory instances, CXL-attached pools, and serverless scaling under pay-as-you-go terms, lowering the barrier for midsize adopters. AWS’s Valkey-based ElastiCache tier costs 33% less than equivalent Redis clusters while boosting throughput over 2×, proving price-performance gains attractive to cost-sensitive SaaS providers.

By Application:

Real-time Analytics Leads GrowthReal-time analytics commanded 47.92% of 2025 spend, as enterprises monetize instant insights from transactional and sensor data. PayPal leverages an in-memory fraud engine to inspect transactions in flight, curbing loss events before authorization completes. IoT and edge stream processing will grow fastest at 30.18% CAGR, propelled by 5G rollouts and federated learning scenarios that pre-process data near the source to cut backhaul traffic.

By End-user Vertical:

BFSI Leads, Healthcare AcceleratesFinance retained 29.12% share in 2025 for high-frequency trading, real-time risk scoring, and compliance queries. Healthcare will grow 23.05% CAGR due to new data-sharing mandates such as the European Health Data Space, which entrusts life-critical analytics to low-latency platforms. Manufacturers also broaden usage, embedding memory-resident digital twins on production floors to slash downtime.

By Memory Technology:

DRAM Dominance Faces DisruptionDRAM accounted for 65.95% of spending in 2025, anchoring latency-critical workloads. However, storage-class memory is on a 28.62% CAGR trajectory as enterprises adopt byte-addressable persistence that eliminates cache-warm-up windows after failover events. China’s push for domestic HBM3 supply by 2026 signals rising regional self-sufficiency and additional competitive pressure on global suppliers.

Geography Analysis

North America In-memory Computing Market

North America generated 37.25% of 2025 revenue, underpinned by deep capital markets, a robust talent ecosystem, and hyperscaler appetite for AI acceleration. Real-time payment rails, autonomous-vehicle pilots, and precision-medicine platforms keep memory footprints climbing across every state.

APAC In-memory Computing Market

Asia-Pacific is scaling fastest at a 20.25% CAGR. China’s state-backed semiconductor programs and India’s Digital India cloud corridors are spawning megawatt-class data centers, many pre-wired for CXL fabric expansion. Regional 5G densification plus data-locality mandates pull inference tasks to country-level edges, favouring in-memory fabrics tuned for micro-services.

Europe In-memory Computing Market

Europe is wrestling with capacity constraints yet funnelling record capital into new builds. Vantage Data Centers’ EUR 720 million securitization—the first of its kind on the continent—signals growing investor confidence that AI workloads will soak up new racks quickly. The EU AI Act and sustainability rules are nudging enterprises toward energy-efficient in-memory architectures that balance throughput with power caps.

Regulatory Landscape

Regulation affecting in-memory computing spans data residency, AI governance, and controls on advanced computing hardware that underpins high-memory clusters. In the United States, the Department of Commerce Bureau of Industry and Security (BIS) revised its license review policy for advanced computing commodities in January 2026, adding compliance friction for cross-border sourcing of leading-edge compute and memory configurations that many IMC deployments rely on. In February 2026, a Federal Register notice tied to NDAA FY2023 Section 5949 advanced procurement restrictions for certain covered semiconductor products in federal contracting increased due diligence expectations for vendors selling memory-centric appliances and cloud services into government workloads.

Standards and industrial policy are also shaping platform choices and supplier strategies. NIST published a CHIPS R&D Standardization Readiness Level workshop summary in 2026 that flagged system-centric standardization gaps, including chiplet interfaces, thermal modeling, and testing for advanced multi-die systems, which connect directly to how IMC architectures are moving toward disaggregated memory and heterogeneous integration. In Europe, the European Commission put forward a 2026 proposal to strengthen the semiconductor ecosystem, often discussed as a next-phase Chips framework, with emphasis on advanced logic and memory for AI, reinforcing strategic-autonomy priorities that influence where memory fabrication, packaging, and sovereign AI infrastructure are located.

Value Chain Analysis

The in-memory computing value chain starts with memory technology innovation (DRAM, storage-class memory, and emerging RRAM/memristor approaches) and runs through semiconductor design, fabrication, advanced packaging, and system integration into servers, cloud instances, and software platforms. Memory manufacturers and ecosystem partners supply core silicon, while architecture and IP specialists co-develop compute-in-memory concepts that can move from prototypes into manufacturable silicon. On the software side, database and in-memory data grid vendors bundle runtime engines, connectors, and operational tooling that help enterprises place hot datasets in memory across on-premises and cloud/SaaS deployments.

Bottlenecks increasingly shift toward integration and enablement layers rather than basic compute throughput. Emerging analog compute-in-memory approaches face precision, temperature sensitivity, and reliability challenges, and system-level constraints such as thermal management and test and validation complexity become more visible as designs move to multi-die and chiplet-centric architectures. Ecosystem readiness, compilers, and programming models remain key friction points, which pushes many buyers toward hyperscaler-managed in-memory services and vendor-integrated stacks that hide deployment complexity. Partnerships aimed at standardization and interoperability, such as the August 2025 SanDisk and SK hynix MOU to collaborate on high bandwidth flash standardization, show how suppliers are trying to reduce integration risk for AI inference and memory-heavy pipelines.

Competitive Landscape

The in-memory computing market shows moderate concentration. SAP, Oracle, and Microsoft expand bundled offerings that let customers unlock memory-resident performance within familiar ERP and database environments, reinforcing renewal stickiness. Redis and Aerospike pursue low-latency use cases such as fraud prevention and ad-tech bidding, carving high-growth adjacencies. GridGain marries compute and storage into a single in-memory layer to support AI pipelines that mix streaming events, SQL queries, and vector similarity search.

Vector-database start-ups attracted more than USD 350 million in 2024 funding rounds, highlighting investor conviction in memory-optimized retrieval for generative AI. IBM’s acquisition of DataStax further tightens links between in-memory key-value stores and model-training frameworks, reflecting a strategy to own the full AI lifecycle from data ingest to inference. Hardware-adjacent players are also entering Samsung and Micron outline CXL-aware DIMMs that promise multi-socket sharing without NUMA penalties, aimed squarely at cloud builders that need elastic memory footprints.

Price volatility on DRAM and HBM remains a wild card. Vendors with multi-sourcing contracts hedge exposure, whereas smaller ISVs ride cloud-provider roadmaps to buffer raw silicon risk. Talent scarcity in distributed memory systems gives an edge to service providers that wrap turnkey design, deployment, and managed operations in monthly subscriptions.

In-memory Computing Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

International Business Machines Corporation

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

In-memory Computing Market Companies Covered in this Report

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- International Business Machines Corporation (IBM)

- Amazon Web Services, Inc.

- Altibase Corporation

- GridGain Systems, Inc.

- GigaSpaces Technologies Ltd.

- Software AG

- TIBCO Software Inc.

- Hazelcast Inc.

- SAS Institute Inc.

- MongoDB, Inc.

- DataStax, Inc.

- Redis Ltd. (Redis Labs)

- MemVerge, Inc.

- Hewlett Packard Enterprise Company

- Fujitsu Limited

- KX Systems, Inc.

- Volt Active Data, Inc.

- Aerospike Inc.

Market Opportunities and Future Outlook

Whitespace is building around AI inference and agentic application stacks that require fast, repeated access to large working sets (vectors, embeddings, and long-context KV state) without absorbing constant data-movement penalties. This is showing up in the shift from general-purpose in-memory databases toward specialized memory stores and retrieval layers. In May 2026, MinIO introduced MemKV as a context memory store for AI inference, highlighting demand for purpose-built, low-latency memory services that sit alongside existing object storage and analytics stacks. Another opportunity is in-memory fabrics that combine SQL, streaming, and vector search in unified runtimes, reducing inter-cluster latency and data gravity issues for real-time analytics and fraud or risk pipelines.

Hardware opportunity concentrates on heterogeneous integration and chiplet-based designs that align with system-centric standardization efforts and the practical limits of monolithic scaling. Research disclosures in 2026 for heterogeneous multi-chiplet in-memory computing accelerators and programmable compute-in-memory designs point to the breadth of architectures being explored for LLM workloads and edge AI. At the supply ecosystem level, elevated memory investment supports scaling of memory-centric infrastructure: SEMI cited worldwide 300 mm memory fab equipment investment reaching USD 52 billion in 2026, and Micron highlighted progress at its Clay, New York fab site in July 2026, which extends the manufacturing runway for DRAM and advanced memory capacity used in many IMC deployments. For buyers, that translates into more packaging, capacity, and form-factor options for high-memory servers and disaggregated pools, while for vendors it reinforces the case for portable software layers that can exploit DRAM, storage-class memory, and emerging compute-in-memory devices as they become available.

Recent Industry Developments in In-memory Computing Market

- July 2026: TetraMem and SK hynix announced the successful completion of a joint technology collaboration advancing memristor-based analog in-memory computing research, publicizing results tied to memory-centric AI computing. The milestone improves the credibility of RRAM/memristor approaches as candidates for energy-constrained edge AI and helps pull more of the semiconductor value chain toward compute-in-memory enablement.

- May 2026: MinIO launched MemKV, positioning it as a purpose-built context memory store for AI inference with a focus on low-latency retrieval of large context. The release reflects a move toward specialized in-memory layers closer to LLM serving and agentic workloads than traditional cache-only patterns.

- March 2026: MariaDB announced an agreement to acquire GridGain to combine relational database capabilities with an in-memory data grid for real-time and AI-oriented applications. The acquisition agreement tightens integration between transactional persistence and in-memory compute layers, supporting unified architectures for streaming, operational analytics, and latency-sensitive decisioning.

In-memory Computing Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the in-memory computing market is defined as software and related services that process and analyze data primarily in RAM to deliver faster, near real-time performance for transactions, analytics, and application workloads.

Scope exclusions: Hardware-only memory components and general-purpose server infrastructure are excluded unless they are priced and sold as part of an in-memory computing solution or service.

Segments Covered in This Report

- By Component

- In memory Data Management Platforms

- In memory Application Platforms

- By Deployment Mode

- On-premises

- Cloud / SaaS

- By Application

- Real-time Analytics & BI

- High-frequency Trading

- Fraud & Risk Management

- IoT/Edge Stream Processing

- By End-user Vertical

- BFSI

- Healthcare & Life Sciences

- IT & Telecom

- Government & Public Sector

- Manufacturing & Automotive

- By Memory Technology

- DRAM-based IMC

- NAND-based IMC (Redis on-flash, etc.)

- Persistent / Storage-class Memory (SCM)

- By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SME)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the product boundary and to collect stable input indicators that can be checked over time. We reviewed public sources such as US Census Bureau and Eurostat ICT and services data, OECD digital economy indicators, ITU connectivity statistics, and World Bank macro series that help normalize IT spend cycles across regions.

To keep assumptions grounded, company filings and investor presentations were screened for in-memory product revenue mentions, cloud adoption commentary, and large deal signals. Those signals were then compared with coverage from reputed press outlets and association websites. In a few places, paid subscriptions for company financials and patent databases were used to fill gaps on product positioning and solution overlap, without relying on them as the only evidence. The sources named above are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were run with a mix of software providers, cloud and channel participants, and enterprise buyers that run high frequency analytics or transaction systems. We used these interviews to test what gets counted as in-memory computing in specific deal scopes, to sanity-check regional adoption patterns across APAC, EMEA, and the Americas, and to confirm pricing direction for subscriptions and support services. Coverage was kept global so that demand signals could be compared side-by-side and then reconciled into one set of assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 38% |

| Mid tier: 53% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 15% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs the demand pool from enterprise data and analytics software spend, then applies in-memory adoption and attach rates by major region and industry. Once that first cut was formed, the totals were corroborated using selective bottom-up approximations, such as sampled vendor revenue splits, channel checks on deal mix, and ASP times volume logic for common deployments, which then helped adjust outliers.

Inputs that mattered most included the share of workloads moving to real-time analytics, cloud deployment penetration for data platforms, typical subscription and support pricing progression, memory-intensive workload growth (for example, streaming analytics and fraud detection), and enterprise modernization timelines that shift refresh cycles. For forecasting, scenario analysis was used around adoption speed and pricing, and then the yearly path was smoothed using trend consistency checks so abrupt jumps did not appear without a clear driver. Where supplier disclosures were incomplete, gaps were handled by using proxy splits from comparable solution categories and then re-tested in primary calls before finalizing.

Data Validation & Update Cycle

Validation was done by comparing the model outputs to independent signals like enterprise software budget direction, cloud migration momentum, and vendor commentary on data platform pipelines, and then checking whether the implied per-customer spend looked realistic. Any major variance triggers a second pass where assumptions are re-checked, and respondents are re-contacted if a change is material or region-specific.

Before sign-off, the numbers go through a multi-step internal review so calculation logic, currency handling, and year-to-year consistency are verified. Reports are refreshed annually, and interim updates are made when large events change spend patterns, pricing, or deployment behavior. Right before delivery, an analyst performs a fresh review pass so clients receive the latest updated view.

Mordor Intelligence's In Memory Computing Market Size Compared With Other Published Estimates

Different published market sizes for in-memory computing usually come from where the boundary is drawn between software versus hardware, how cloud subscriptions are annualized, and whether adjacent data platform categories are blended into one number. Timing choices also matter because some sources use different base years and exchange-rate assumptions, which changes the reported USD value.

Deal-mix signals from public filings, enterprise software budget direction, and regional cloud adoption checks are the evidence that keeps Mordor Intelligence's estimate tied to in-memory software and services that are actually purchased for real-time processing, rather than broader compute or memory infrastructure spending.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.40 B (2025) | |

| Global Consultancy A | USD 15.16 B (2025) | This figure appears to treat the 2025 value as a base year and may include a slightly wider set of in-memory application platform revenues, which can lift the total versus a stricter in-memory processing boundary. |

| Industry Publisher B | USD 24.50 B (2025) | The higher number is consistent with counting adjacent infrastructure and broader real-time data stack spending, and it may also reflect a different currency timing and more aggressive inclusion of application and deployment categories. |

The spread across sources is mainly explained by scope and counting rules, not by arithmetic differences. By using clear inclusion tests around in-memory software and services, then validating assumptions with multiple demand-side signals, the resulting market size stays traceable to practical inputs and can be repeated during updates.

Key Questions Answered in the Report

What is the current value of the in-memory computing market?

The market stands at USD 16.82 billion in 2026.

How fast is the in-memory computing market growing?

It is projected to post a 16.83% CAGR, doubling to USD 36.59 billion by 2031.

Which deployment model is growing quickest?

Cloud/SaaS deployments, already 70.88% of revenue, are expanding at 26.95% CAGR.

Why are AI workloads important to in-memory computing adoption?

Large language models and vector search saturate traditional memory bandwidth, making specialized in-memory fabrics essential for low-latency inference.

Which region is the fastest growing?

Asia-Pacific is forecast to expand at a 20.25% CAGR due to aggressive datacentre builds and 5G proliferation.

What is the biggest restraint to wider adoption?

Volatile DRAM pricing can raise total cost of ownership and delay large-scale refreshes, especially for hyperscale operators.

Page last updated on: