Food & Beverage

2nd MayMarket Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

The Residue Testing Market Report is Segmented by Residue Type (Pesticides, Heavy Metals, and More), Technology (HPLC-Based, LC-MS/MS-based, and More), Application (Feed and Pet Food, Agricultural Crops, and Food and Beverage), Testing Mode (Lab Testing and Testing Kits) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

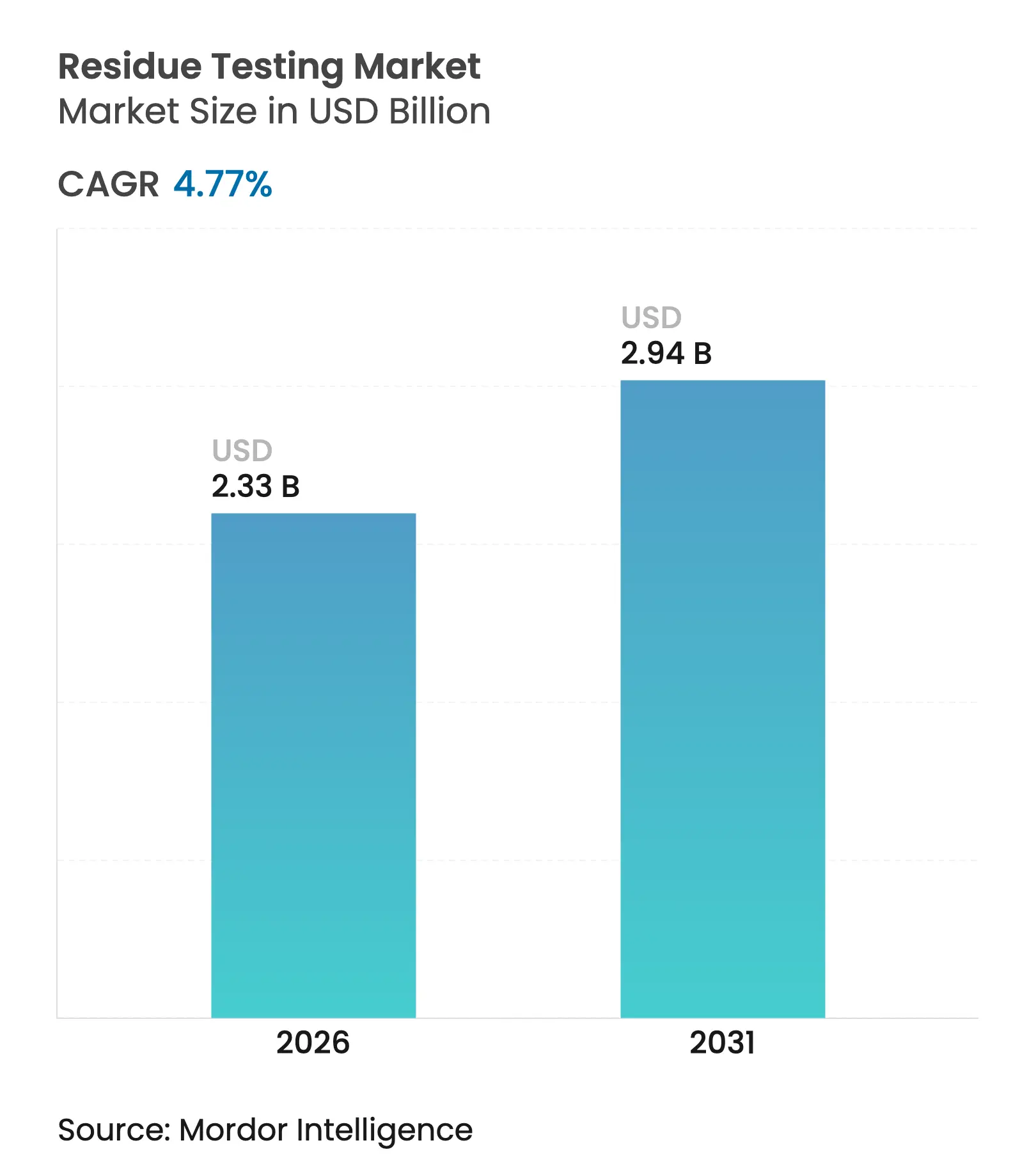

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 4.77 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The residue testing market size is expected to grow from USD 2.22 billion in 2025 to USD 2.33 billion in 2026 and is forecast to reach USD 2.94 billion by 2031 at 4.77% CAGR over 2026-2031. Growth is fuelled by stricter global maximum residue limits, rapid technology upgrades, and rising consumer insistence on verifiable food purity. The European Food Safety Authority's 2023 annual report indicated that 99% of food samples complied with EU regulations, yet 2% exceeded maximum residue levels, underscoring the critical need for robust testing infrastructure [1]Source: European Food Safety Authority, "The 2022 European Union report on pesticide residues in food", efsa.europa.eu . Governments tighten rules faster than most producers can adapt, extending mandatory testing to new residue classes and mandating real-time monitoring across import and domestic supply chains. Convergence of mass-spectrometry, sequencing, and biosensor platforms shortens analysis cycles, while the accelerating cadence of food recalls keeps testing demand structurally high. The residue testing market remains fragmented, creating meaningful scope for consolidation as service providers seek scale advantages in instrumentation investment, data analytics, and geographic reach.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent global food-safety regulations

Stringent global food-safety regulations

| +1.2% | Europe, North America, progressively worldwide | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:Europe, North America, progressively worldwide |

Impact Timeline

:

Long term (≥ 4 years)

|

Surge in demand for clean-label products

Surge in demand for clean-label products

| +0.8% | North America, Europe, moving into Asia-Pacific | Medium term (2-4 years) | |||

Technological advancements in testing techniques

Technological advancements in testing techniques

| +0.9% | Global, led by developed economies | Medium term (2-4 years) | |||

Rise in outbreaks of foodborne illnesses

Rise in outbreaks of foodborne illnesses

| +0.6% | Global, higher intensity in emerging markets | Short term (≤ 2 years) | |||

Widespread agrochemical use in farming

Widespread agrochemical use in farming

| +0.7% | Asia-Pacific core; spill-over to Latin America and Africa | Long term (≥ 4 years) | |||

Increased incidence of food recalls

Increased incidence of food recalls

| +0.5% | North America, Europe, gradually global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent global food-safety regulations

Regulatory tightening accelerates testing demand as governments implement more restrictive maximum residue limits and expand monitoring scope. The EU's implementation of Regulation 2023/915 established comprehensive contaminant thresholds, while the FDA's [2]Source: U.S Food and Drug Administration, "Mycotoxin monitoring program", fda.gov updated mycotoxin monitoring program now includes T-2/HT-2 toxins and zearalenone using multi-mycotoxin analytical methods. China's release of 47 new national food safety standards in 2024, including 7 dedicated testing methodologies, signals regulatory convergence toward international best practices. In July 2024 Taiwan's introduction of safety tolerance levels for 5 additional mycotoxins in pet food, including vomitoxin and fumonisin, demonstrates expanding regulatory scope beyond human consumption. The FDA's Laboratory Accreditation for Analyses of Foods (LAAF) program mandate for mycotoxin testing starting December 2024 creates structural demand for accredited testing capabilities. Brazil's adoption of new regulatory frameworks for food products and revised technical regulations for food contact metals further exemplifies global regulatory harmonization driving systematic testing requirements. These regulatory developments across major markets necessitate increased investment in testing infrastructure and analytical capabilities. The harmonization of international standards creates opportunities for testing service providers while ensuring consistent food safety measures across global supply chains.

Surge in demand for clean-label products

Consumer preference for transparent, minimally processed foods drives manufacturers to implement comprehensive residue testing protocols that verify clean-label claims. This trend particularly impacts premium food segments where brands differentiate through certified purity levels and absence of synthetic residues. The clean-label movement extends beyond pesticides to encompass heavy metals, processing aids, and packaging contaminants, expanding the testing scope per product. Retailers increasingly require third-party verification of clean-label assertions, creating systematic testing demand across supply chains. The premium pricing associated with clean-label products justifies enhanced testing investments, making comprehensive residue analysis economically viable for manufacturers targeting health-conscious consumers. The rise of social media and instant information sharing has amplified consumer scrutiny of product ingredients, forcing companies to maintain rigorous testing standards. Additionally, the growing number of food safety incidents and recalls has heightened awareness about residue testing, making it an essential component of quality assurance programs.

Technological advancements in testing techniques

Innovation in detection technologies enhances sensitivity, reduces analysis time, and enables multiplex testing capabilities that transform laboratory economics. Agilent's launch of the 7010D Triple Quadrupole GC/MS System specifically targets food and environmental markets with enhanced sensitivity and regulatory compliance features including FDA 21 CFR Part 11 compatibility. CRISPR-Cas12a biosensors integrated with G-quadruplex structures achieve detection limits of 101 CFU/mL for foodborne pathogens while eliminating fluorescent labeling requirements. 3D-printed microfluidic chips integrated with nanointerferometers enable simultaneous detection of multiple foodborne pathogens at 10 CFU/mL sensitivity, offering cost-effective alternatives to traditional methods. Nanobiosensor development leverages unique nanoscale properties to enhance detection capabilities while addressing commercialization challenges through improved validation protocols. These technological advances reduce per-test costs while expanding analytical scope, making comprehensive residue testing economically accessible to smaller food producers.

Rise in outbreaks of foodborne illnesses

High-profile contamination incidents intensify regulatory scrutiny and drive systematic testing adoption across food supply chains. The E. coli outbreak linked to McDonald's Quarter Pounders resulted in 104 infections across 14 states, highlighting supply chain vulnerabilities and prompting enhanced testing protocols for fresh produce [3]Source: Centers for Disease Control and Prevention (CDC), "E. coli Outbreak", cdc.gov . In November 2024, Listeria outbreaks connected to ready-to-eat foods caused 10 hospitalizations, while Yu Shang brand RTE meats resulted in 11 illnesses including an infant death, demonstrating the severe consequences of inadequate testing according to CDC. The decade-long Listeria outbreak linked to Rizo Lopez Foods' queso fresco resulted in 26 illnesses, 23 hospitalizations, and 2 deaths, leading to court-ordered production cessation until FDA compliance approval. These incidents create regulatory pressure for enhanced testing frequency and scope, particularly for high-risk products. The economic impact of recalls, including legal liabilities and brand damage, makes preventive testing investments increasingly attractive compared to post-incident costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of advanced testing technologies

High cost of advanced testing technologies

| -0.4% | Global, pronounced in low-income economies | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.4%

|

Geographic Relevance

:

Global, pronounced in low-income economies

|

Impact Timeline

:

Medium term (2-4 years)

|

Lack of standardization in residue limits across regions

Lack of standardization in residue limits across regions

| -0.3% | Worldwide, affecting trade corridors | Long term (≥ 4 years) | |||

Limited infrastructure in developing countries

Limited infrastructure in developing countries

| -0.5% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) | |||

Lack of awareness among small producers

Lack of awareness among small producers

| -0.2% | Rural areas, especially emerging markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High cost of advanced testing technologies

Capital-intensive analytical equipment creates barriers for smaller laboratories and food producers, particularly in price-sensitive markets. Advanced LC-MS/MS systems require substantial upfront investments and ongoing maintenance costs that strain operational budgets for mid-tier testing facilities. The complexity of modern testing platforms demands specialized technical expertise, adding personnel costs that compound equipment expenses. Regulatory compliance requirements for instrument validation and calibration create additional cost layers that particularly impact laboratories serving local markets. However, technology providers increasingly offer leasing models and shared-access platforms that democratize advanced testing capabilities. These financial constraints have led to market consolidation, with larger laboratories dominating the residue testing landscape. Small and medium-sized enterprises often resort to outsourcing their testing needs to third-party laboratories, creating a secondary market for testing services.

Limited infrastructure in developing countries

Inadequate laboratory infrastructure constrains testing capacity in emerging markets despite growing regulatory requirements and food safety awareness. Power grid instability and limited cold chain logistics compromise sample integrity and instrument performance in many developing regions. The shortage of trained analytical chemists and quality assurance professionals limits operational capacity even where equipment is available. Regulatory frameworks often lack enforcement mechanisms or accreditation systems that would drive systematic testing adoption. International development initiatives and technology transfer programs gradually address these limitations, though progress remains uneven across regions and commodity types. High initial investment costs for advanced analytical instruments and maintenance requirements create significant barriers to entry for smaller laboratories. The lack of standardized protocols and reference materials across different jurisdictions further complicates the expansion of residue testing capabilities.

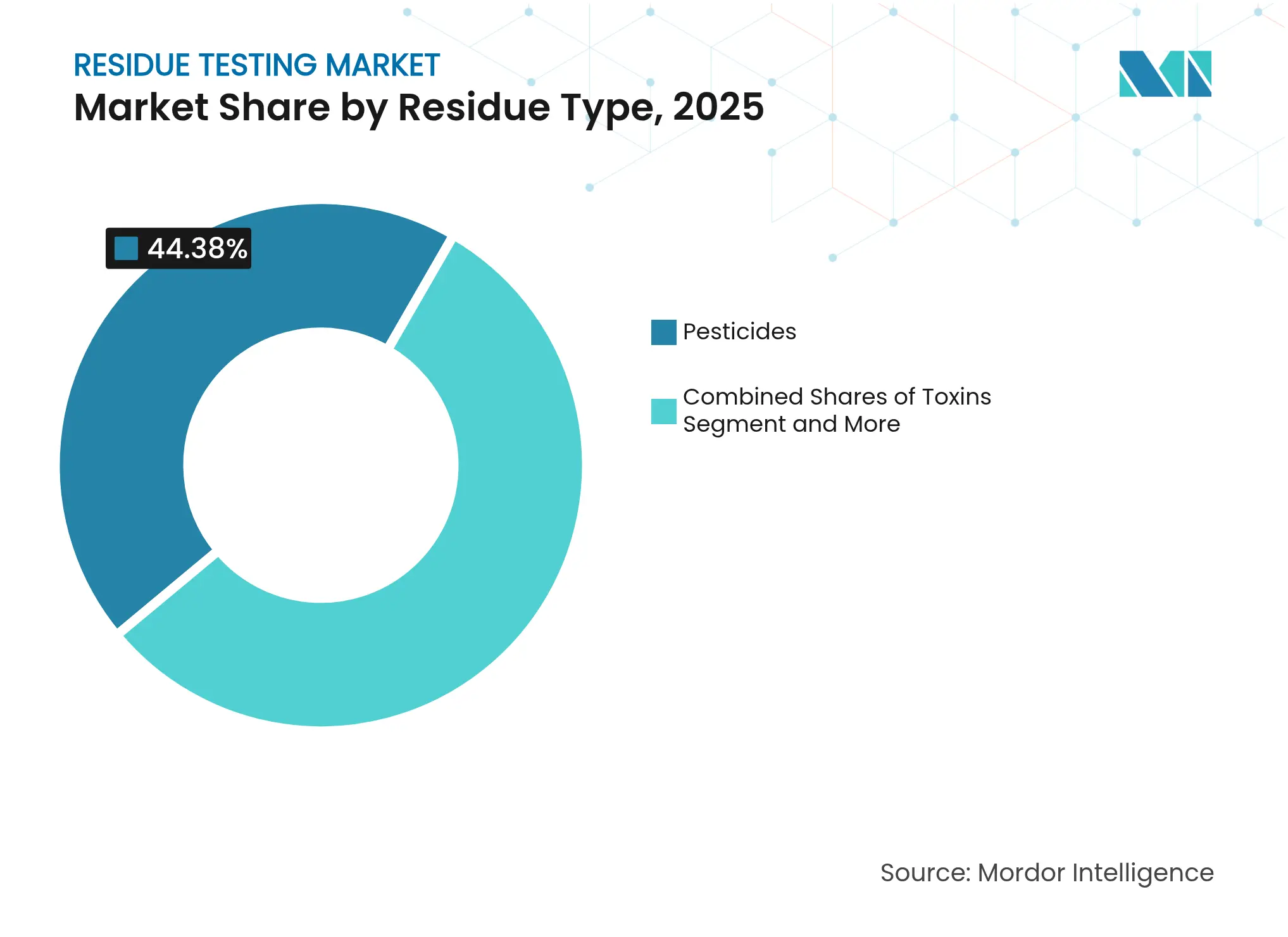

By Residue Type: Pesticides Lead Amid Toxin Acceleration

Pesticides commanded 44.38% market share in 2025, reflecting widespread agrochemical usage and comprehensive regulatory monitoring across global food systems. Heavy metals represent the second-largest category, driven by environmental contamination concerns and tightening limits for lead, cadmium, and mercury in food products. Toxins emerge as the fastest-growing segment at 4.86% CAGR through 2031, propelled by expanding mycotoxin testing requirements and novel biotoxin detection needs. The "Others" category, encompassing drugs, antibiotics, and chemical contaminants, benefits from increased scrutiny of veterinary drug residues and emerging contaminants like PFAS.

The EU's updated mycotoxin regulations, including Regulation 2024/1022 setting new maximum levels for DON, T-2, and HT-2 toxins effective July 2024, exemplify regulatory drivers accelerating toxin testing demand. Taiwan's introduction of tolerance levels for 5 additional mycotoxins in pet food, including 2 ppm vomitoxin for dog food and 5 ppm for cat food, demonstrates expanding regulatory scope beyond human consumption. Advanced detection methods like lipopolysaccharide-imprinted polymers achieve 10 CFU/mL sensitivity for Salmonella detection, enabling rapid on-site pathogen identification without complex preprocessing

Note: Segment shares of all individual segments available upon report purchase

By Technology: LC-MS/MS Dominance Faces NGS Disruption

In 2025, LC-MS/MS technology commands a dominant 35.02% market share, bolstered by its regulatory endorsement and consistent analytical prowess across various residue types. This technology is widely adopted due to its ability to deliver high sensitivity and specificity, making it suitable for complex residue analysis in food safety, environmental testing, and pharmaceutical applications. HPLC methods cater to budget-conscious applications, prioritizing high-throughput screening over peak sensitivity. These methods are particularly favored in industries where cost efficiency and rapid processing are critical, such as routine quality control in manufacturing. GC-MS/MS platforms shine in analyzing volatile compounds, especially pesticide residues in processed foods. Their robust performance in detecting and quantifying volatile organic compounds ensures compliance with stringent food safety regulations. Meanwhile, ICP-MS technology excels in the precise detection of heavy metals, ensuring accuracy in trace elemental analysis. Its application spans across sectors like environmental monitoring, food safety, and pharmaceuticals, where detecting minute concentrations of toxic metals is crucial.

NGS/biosensor technology is on a growth trajectory, projected to expand at a 5.12% CAGR through 2031. This surge is fueled by their swift detection capabilities and the ability to conduct multiplex analyses, revolutionizing laboratory workflows. These technologies enable simultaneous detection of multiple targets, significantly reducing analysis time and improving efficiency in diagnostic and research settings. Highlighting the regulatory spotlight, the FDA is assessing Q20+ Nanopore Sequencing for its potential in bacterial outbreak investigations. This technology could drastically shorten the current 2-4 week sequencing timelines to almost real-time results, enhancing public health responses to foodborne illnesses. Addressing the challenges of traditional methods, CRISPR-Cas systems offer a rapid, specific, and cost-effective solution for detecting pathogenic E. coli. These systems are increasingly being integrated into food safety protocols due to their ability to deliver accurate results in a fraction of the time required by conventional methods. While immunoassay platforms remain the go-to for routine screenings, the "Others" category is gaining traction, featuring emerging technologies like surface-enhanced Raman scattering and electrochemical sensors, both known for their portable detection capabilities. These innovative tools are particularly valuable in field-based applications, offering real-time analysis without the need for extensive laboratory infrastructure.

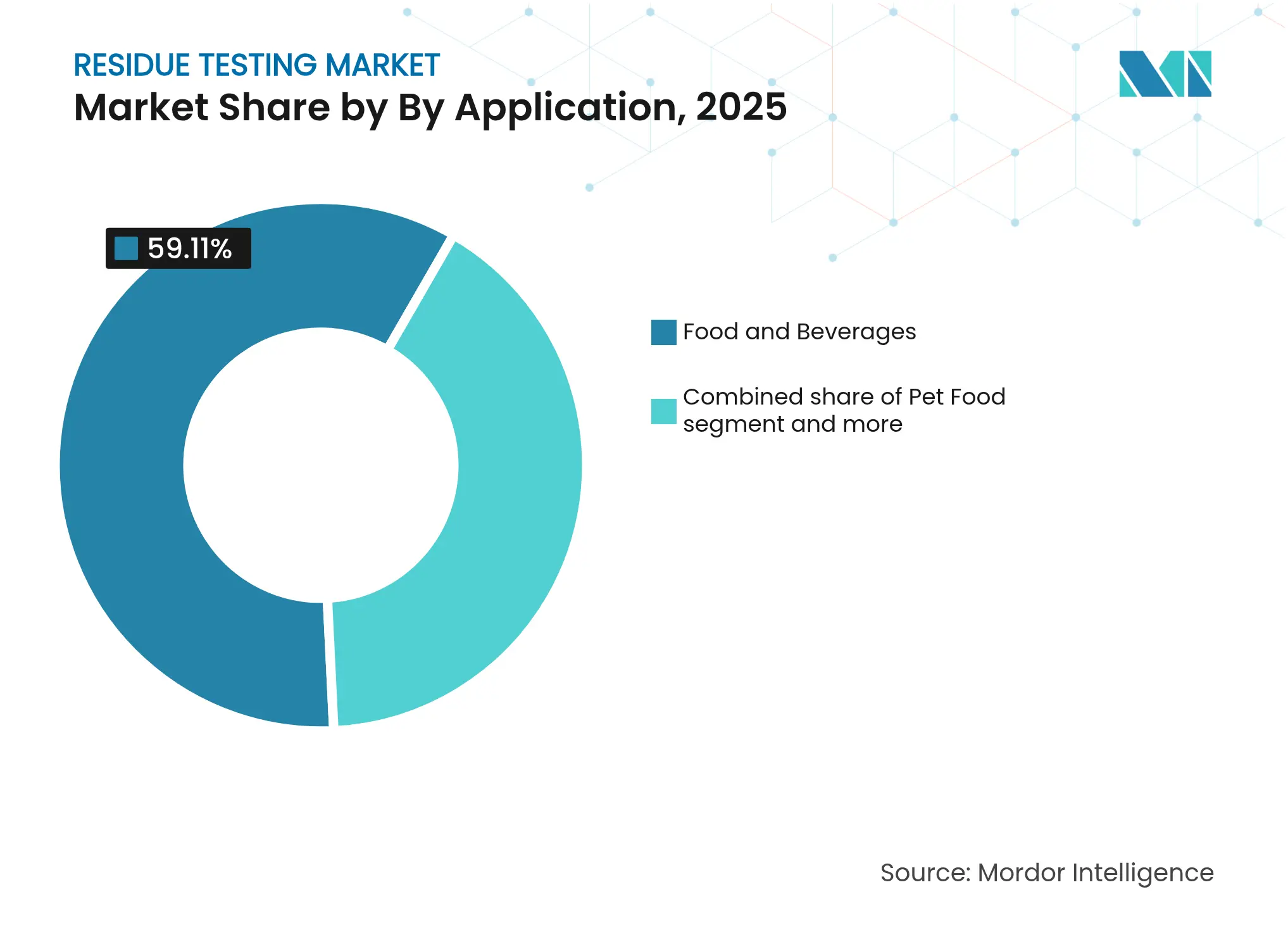

By Application: Food and Beverage Leadership Amid Feed Acceleration

In 2025, the Food and Beverage sector commands a dominant 59.11% share of the market, conducting thorough tests on meat, poultry, dairy, fruits, vegetables, processed foods, and beverages. Within this sector, testing for meat and poultry has intensified, driven by concerns over antimicrobial resistance and the need for pathogen detection to ensure food safety and compliance with regulatory standards. In dairy testing, the spotlight is on antibiotic residues and mycotoxin contamination, often stemming from feed sources, as these contaminants pose significant health risks to consumers. Meanwhile, fruits and vegetables are under increased scrutiny for pesticide residues, especially imports that have a history of higher violation rates, as regulatory bodies aim to mitigate potential health hazards and ensure adherence to international safety norms.

Feed and Pet Food emerges as the fastest-growing application at 5.69% CAGR through 2031, driven by regulatory expansion and contamination incidents that heightened safety awareness. The FDA's Animal Food Contaminants Program monitors mycotoxins, pesticides, and trace elements with increasing frequency, while the proposed PURR Act of 2024 seeks to modernize pet food regulation under unified FDA oversight. Agricultural Crops testing remains essential for pre-harvest monitoring and export certification, particularly as global trade partners implement stricter import requirements. Recent mycotoxin contamination incidents in pet food have prompted enhanced testing protocols and regulatory oversight, with Taiwan introducing tolerance levels for 5 additional mycotoxins including ochratoxin at 0.01 ppm

Note: Segment shares of all individual segments available upon report purchase

By Testing Mode: Lab Testing Dominance Challenged by Kit Innovation

Lab Testing maintains commanding 83.62% market share in 2025, supported by regulatory requirements for certified analytical methods and comprehensive residue panels. Laboratory-based analysis provides the sensitivity, specificity, and documentation required for regulatory compliance and international trade. Accreditation requirements under programs like the FDA's LAAF create structural advantages for established laboratory networks with validated methodologies. The extensive infrastructure and expertise available in laboratory settings enable complex multi-residue analysis across diverse sample matrices. Modern laboratories also offer automated high-throughput screening capabilities that reduce per-sample costs while maintaining analytical precision.

Testing Kits accelerate at 5.91% CAGR through 2031, driven by demand for rapid, on-site detection that enables real-time decision-making across food supply chains. Handheld devices for bacterial detection, such as those developed by Osaka Metropolitan University, connect to smartphone apps and detect multiple bacterial species within one hour. The development of dual-method immunochromatographic strips for procymidone residues enables both rapid screening and quantitative analysis, enhancing efficiency in food safety monitoring. The integration of artificial intelligence and machine learning algorithms improves the accuracy and reliability of rapid testing solutions. These portable testing platforms significantly reduce the time and resources required for preliminary screening, allowing facilities to optimize their testing workflows.

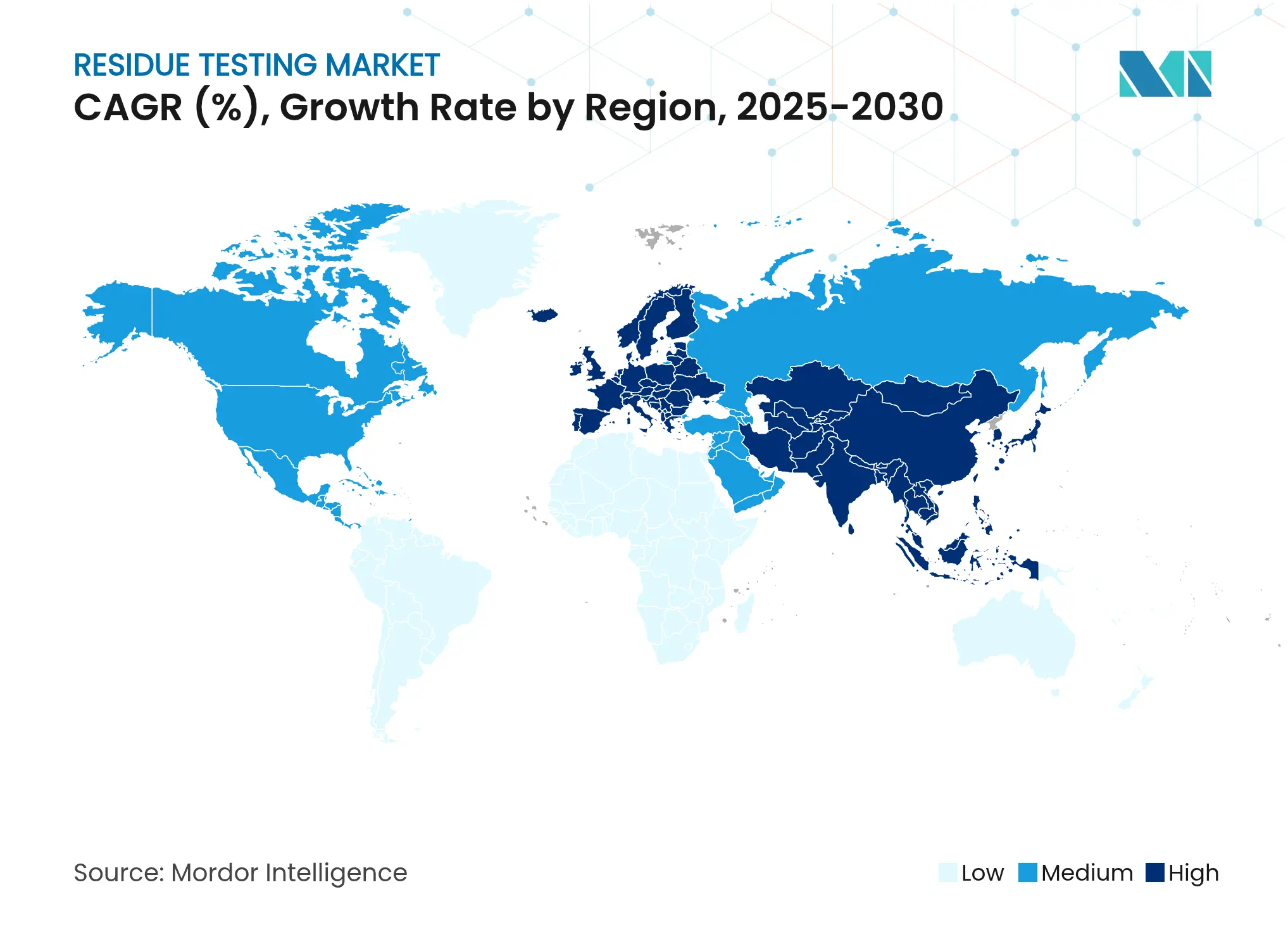

Europe maintains market leadership with 34.51% share in 2025, anchored by the EU's comprehensive regulatory framework including the updated Contaminants Regulation 2023/915 that establishes maximum levels for various food contaminants. The region's testing infrastructure benefits from harmonized analytical standards and robust enforcement mechanisms that drive systematic adoption across member states. Germany, United Kingdom, and France lead in analytical capabilities, while Netherlands and Belgium serve as critical import gateways requiring extensive testing protocols. The EFSA's 2023 annual report indicating 99% regulatory compliance yet 2% exceedance of maximum residue levels underscores the region's rigorous monitoring approach according to European Food Safety Authority. Recent regulatory updates include new maximum residue levels for fluxapyroxad, lambda-cyhalothrin, metalaxyl, and nicotine effective January 2025, demonstrating ongoing refinement of safety standards.

Asia-Pacific accelerates as the fastest-growing region at 4.98% CAGR through 2031, driven by regulatory modernization initiatives and expanding food production capacity across major economies. China's release of 47 new national food safety standards in 2024, including 7 dedicated testing methodologies, signals regulatory convergence toward international best practices. India's FSSAI re-operationalization of food labeling standards effective January 2023 strengthens oversight mechanisms, while Agilent's strategic partnership with ICAR-National Research Centre for Grapes develops advanced analytical workflows for emerging contaminants including PFAS and polar pesticides. Japan's revision of maximum residue limits for pesticides and veterinary drugs aligns with international standards, while South Korea's updates to pesticide tolerance standards and food labeling requirements enhance consumer protection. Australia and Indonesia represent significant growth opportunities as export-oriented economies implement stricter testing protocols to meet international market requirements.

North America maintains substantial market presence supported by stringent FDA and USDA oversight mechanisms that drive comprehensive testing across domestic and imported food supplies. The FDA's FY 2022 Pesticide Residue Monitoring Report revealed 96.2% compliance for domestic samples versus 89.5% for imports, highlighting the critical role of testing in global food trade. The region benefits from advanced laboratory infrastructure and technological innovation, with companies like SGS expanding food testing capacity through facility upgrades in key manufacturing hubs . South America emerges as a growth opportunity driven by Brazil's adoption of new regulatory frameworks and revised technical regulations for food contact materials, while Argentina, Colombia, and Chile enhance export testing capabilities to meet international requirements. Middle East and Africa represent developing markets where infrastructure investments and regulatory framework development create long-term growth potential as food safety awareness increases and export ambitions expand.

Market Concentration

The residue testing market exhibits a fragmented competitive structure, indicating substantial consolidation opportunities and intense competition among numerous players. Market dynamics favor companies with comprehensive service portfolios spanning multiple testing methodologies, geographic reach, and regulatory expertise across diverse food categories. Major players include SGS Société Générale de Surveillance SA, Eurofins Scientific, Bureau Veritas, Mérieux Nutrisciences Corporation, and Thermo Fisher Scientific, among others.

Leading testing service providers like SGS, Eurofins, and Bureau Veritas leverage global laboratory networks and technological capabilities to capture market share, while analytical instrument manufacturers, including Thermo Fisher Scientific, Agilent Technologies, and Waters Corporation, compete on innovation and regulatory compliance features. Strategic patterns emphasize technological differentiation and geographic expansion, with companies investing heavily in rapid detection capabilities and multiplex testing platforms that reduce time-to-result while expanding analytical scope.

In October 2024, Bureau Veritas's divestment of its food testing business to Mérieux NutriSciences for EUR 360 million exemplifies portfolio optimization strategies as companies focus on core competencies. Eurofins demonstrated resilient growth with 7.1% organic expansion in 2023 and continued investment in laboratory capacity, while SGS expanded North American food testing capabilities through facility upgrades targeting the multi-billion dollar nutraceutical market. Technology convergence toward NGS, biosensors, and AI-enhanced analytics creates opportunities for disruptive entrants, while established players maintain competitive advantages through regulatory relationships and validated methodologies that ensure compliance across global markets.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The global residue testing market has been segmented by product type, application, and technology. By product type, the market is sub-segmented aspesticides, heavy metals, toxins, allergens and others, and by application, it is sub-segmented as feed & pet food and food. The technology has been further categorized into HPLC-based technology, LC-MS/MC-based, immunoassay-based, and other technologies.

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.