Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

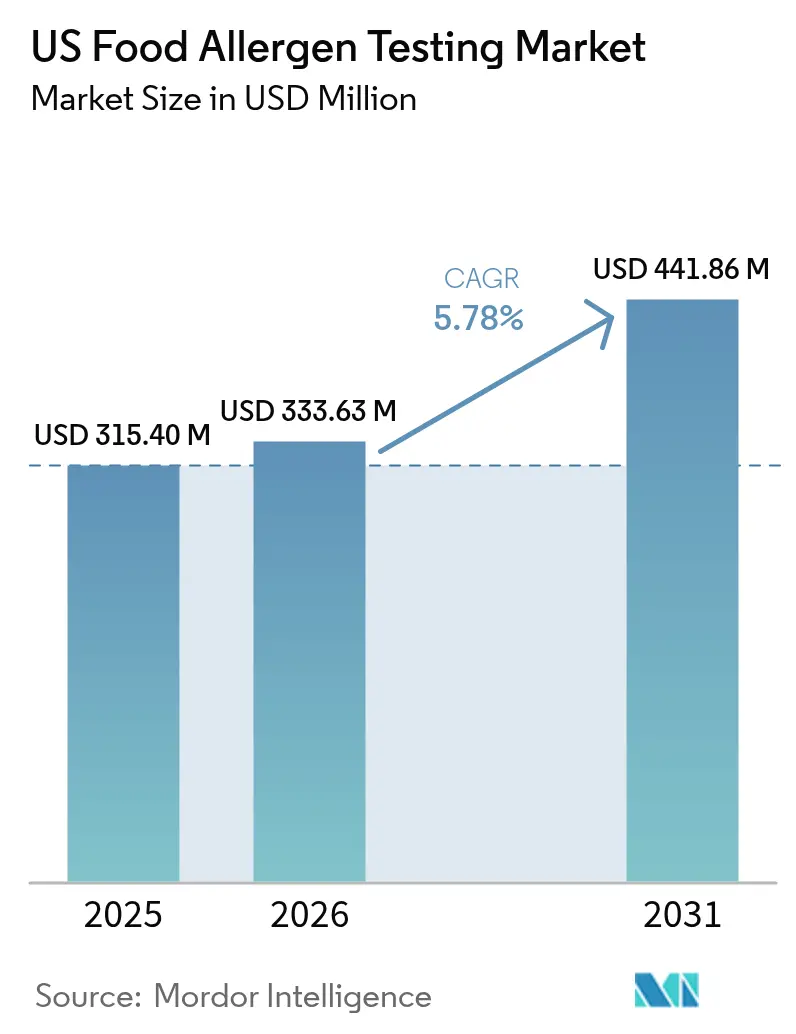

| Base Year Market Size (2025) | USD 315.4 Million |

| Market Size (2026) | USD 333.63 Million |

| Market Size (2031) | USD 441.86 Million |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Food Allergen Testing Market Analysis by Mordor Intelligence

The United States food allergen testing market size in 2026 is estimated at USD 333.63 million, growing from 2025 value of USD 315.4 million with 2031 projections showing USD 441.86 million, growing at 5.78% CAGR over 2026-2031. This growth trajectory reflects the market's response to heightened regulatory scrutiny following the Food Allergy Safety, Treatment, Education, and Research (FASTER) Act, which designated sesame as the ninth major food allergen effective January 2023 [1]Source: U.S Food and Drug Administration, "Sesame Is the Ninth Major Food Allergen", www.fda.gov. The growth reflects stricter enforcement following the FASTER Act, a rising incidence of food allergies, and a shift toward rapid, cost-effective testing solutions. Immunoassay/ELISA platforms continue to dominate because of validated methods and favorable economics, yet next-generation sequencing (NGS) is gaining notice for detecting multiple allergens in highly processed foods. Regionally, the South holds the largest share, while the West registers the strongest expansion, helped by its plant-based innovation ecosystem. The competitive intensity remains moderate; acquisitions and large-scale capital programs illustrate a race to broaden service portfolios, integrate technology, and secure regulatory credentials.

Key Report Takeaways

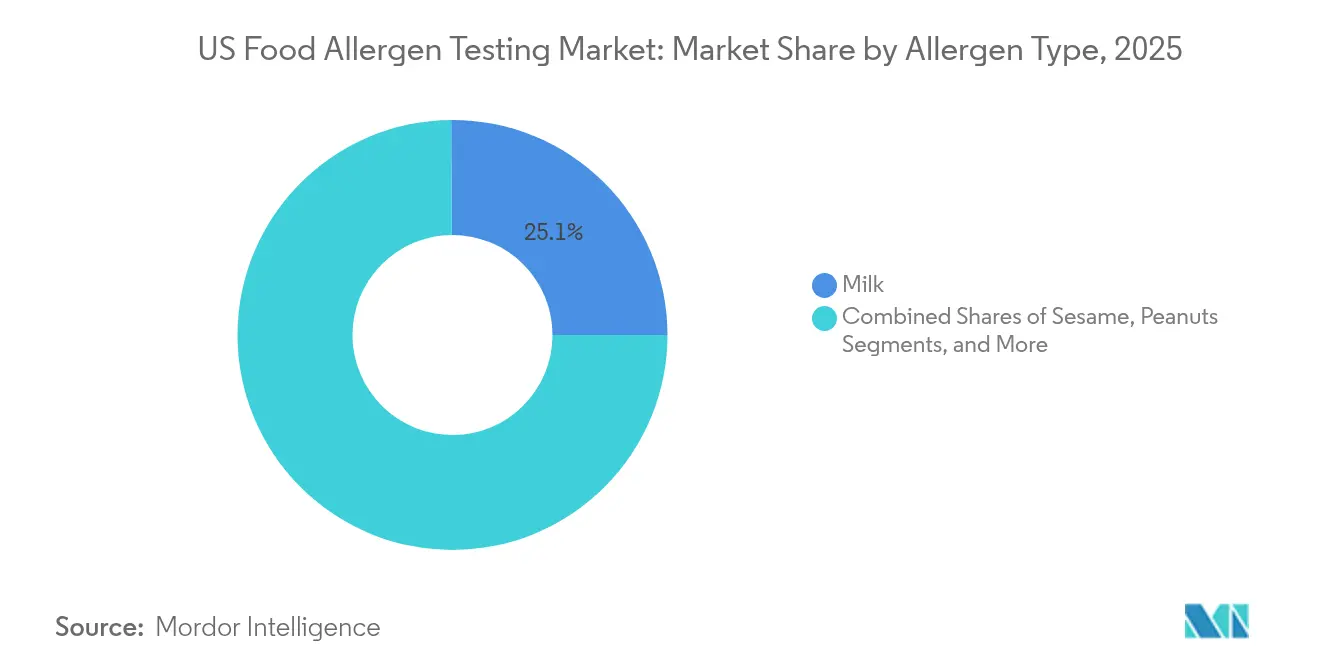

- By allergen type, milk led with 25.10% revenue share in 2025, while sesame testing is forecast to rise at an 7.84% CAGR.

- By technology, immunoassay/ELISA maintained 45.85% of the food allergen testing market share in 2025; NGS is projected to post a 6.55% CAGR through 2031.

- By food tested, dairy products accounted for a 32.85% share of the food allergen testing market size in 2025, whereas plant-based and novel proteins are on track to expand at a 7.42% CAGR to 2031.

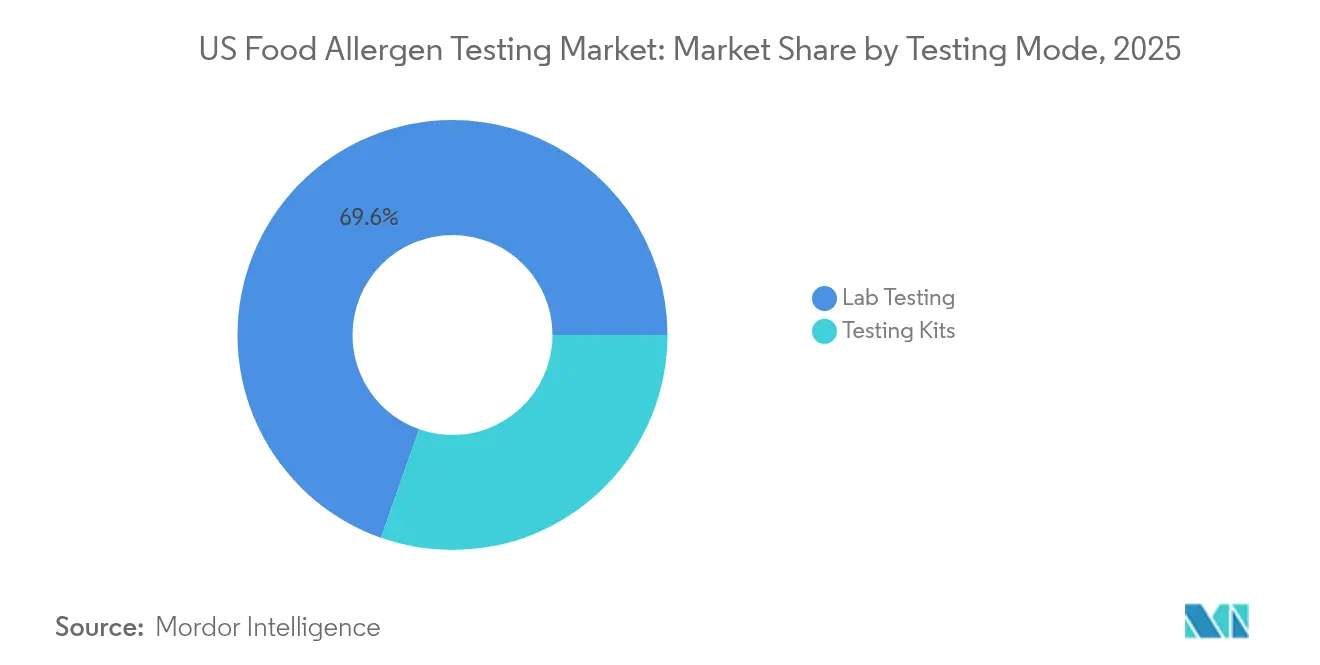

- By testing mode, laboratory services dominated with 69.60% of the food allergen testing market share in 2025; kits are growing the fastest at 7.25% CAGR.

- By geography, the South held 28.40% of the food allergen testing market share in 2025; the West is expected to register a 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Food Allergen Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising food allergy incidence | +1.2% | National (urban focus) | Long term (≥ 4 years) |

| Stringent food safety regulations | +1.8% | National (state nuances) | Medium term (2-4 years) |

| Growth in packaged and processed foods | +0.9% | National (processing hubs) | Long term (≥ 4 years) |

| Technological advances in testing methods | +1.1% | Northeast, West early use | Medium term (2-4 years) |

| Consumer demand for transparency | +0.7% | Premium market segments | Long term (≥ 4 years) |

| Increase in allergen-related recalls | +0.4% | Supply-chain clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Food Allergies in the United States

The increasing incidence of food allergies in the United States is a major driver for the growth of the food allergen testing market. As more consumers become aware of severe allergic reactions, including anaphylaxis, there is heightened demand for transparency and safety in food production. This has prompted food manufacturers to implement comprehensive allergen testing to prevent cross-contamination and protect brand reputation. Regulatory bodies like the FDA have also tightened labeling and compliance requirements, making allergen testing a critical step in meeting safety standards. Additionally, the surge in popularity of “free-from” foods—such as gluten-free, nut-free, and dairy-free products—has created a need for accurate verification through testing. Retailers and foodservice providers increasingly require documentation of allergen controls from suppliers to protect sensitive consumers. Technological advancements in testing methods, such as PCR and ELISA, have also made allergen detection faster and more reliable, further supporting market growth. Overall, rising allergy prevalence is reshaping industry practices, placing allergen testing at the core of food safety strategies.

Stringent Food Safety Regulations

The FASTER Act's designation of sesame as the ninth major allergen triggered comprehensive labeling and testing requirement updates across the food industry, with compliance enforcement intensifying throughout 2024. The FDA's warning letter to Bimbo Bakeries in June 2024 for allergen mislabeling demonstrates the agency's aggressive enforcement posture, signaling heightened compliance risks for manufacturers. The USDA's expanded Allergen Verification Sampling Program, effective September 2024, now covers 14 allergens including the 'Big 9' for ready-to-eat products, substantially broadening testing requirements[2]Source: U.S Department of Agriculture, "Allergen Verification Sampling Program", www.fsis.usda.gov . State-level variations in enforcement create compliance complexity, particularly for multi-state food processors who must navigate differing interpretation standards and inspection frequencies. The FDA's Laboratory Accreditation for Analyses of Foods program establishes mandatory third-party testing requirements for specific import scenarios, driving demand for accredited testing services. Regulatory uncertainty around emerging allergens beyond the major nine creates strategic testing challenges, as manufacturers must balance comprehensive protection against cost optimization in an evolving regulatory landscape.

Technological Advancements in Testing Methods

Nanobody technology from camelid antibodies offers superior stability and specificity compared to traditional antibodies, with research demonstrating effective detection of macadamia, peanut, lupin, and milk proteins with minimized cross-reactions. Next-generation sequencing platforms enable simultaneous detection of multiple allergens with enhanced sensitivity, though adoption remains limited by cost considerations and technical complexity in routine testing environments. Artificial intelligence integration in allergen prediction models, such as AllergenAI, demonstrates potential for identifying novel allergenic proteins based on sequence analysis, though regulatory acceptance for these predictive tools remains uncertain. Biosensor technology advances, including smartphone-based detection systems and electrochemical methods, promise point-of-use testing capabilities that could revolutionize supply chain allergen monitoring. The integration of mass spectrometry with liquid chromatography provides enhanced specificity for processed foods where traditional immunoassays may fail, though equipment costs limit widespread adoption to larger testing facilities.

Growing Consumer Awareness and Demand for Transparency

Consumer litigation risks have intensified following high-profile allergen-related lawsuits, compelling manufacturers to adopt more comprehensive testing protocols as legal protection strategies. Social media amplification of allergen-related incidents creates reputational risks that extend beyond immediate health concerns, driving demand for third-party testing verification to support marketing claims. The rise of specialty diet segments, including gluten-free, dairy-free, and plant-based categories, requires dedicated testing protocols to validate allergen-free claims that command premium pricing. Consumer education initiatives by organizations like Food Allergy Research and Education create more informed buyers who actively scrutinize ingredient labels and testing certifications. The emergence of allergen-free certification programs creates competitive differentiation opportunities, though the proliferation of different standards creates confusion and compliance complexity. Direct-to-consumer food brands face unique testing challenges, as they lack the infrastructure of established manufacturers but must meet identical safety standards to access mainstream distribution channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced testing technologies | -0.8% | National, with greater pressure on small and mid-size plants | Medium term (2-4 years) |

| Lack of standardized testing protocols across facilities | -0.6% | National, with region-to-region implementation disparities | Long term (≥ 4 years) |

| Complexity of allergen detection in processed foods | -0.5% | National, acute in multi-ingredient production clusters | Medium term (2-4 years) |

| Evolving allergen regulations | -0.7% | National, intensified in states with stricter enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Testing Technologies

Advanced testing equipment, including LC-MS/HPLC-MS systems and next-generation sequencing platforms, requires capital huge investments, creating barriers for smaller food processors and regional testing laboratories. The Bureau of Labor Statistics [3]Source: Bureau of Labor Statistics, "Median wages per hour for testing laboratory personnel", www.bls.govreports median wages of USD 28.79 per hour for testing laboratory personnel, with specialized technicians commanding premium salaries that compound operational cost pressures. FARRP's (Food Allergy Research and Resource Program) testing services range from USD 55 to USD 205 per allergen test, with rush processing commanding additional premiums, illustrating the cost sensitivity that drives many manufacturers toward less comprehensive testing protocols. Maintenance and calibration costs for sophisticated testing equipment can go high, creating ongoing financial pressure that may discourage technology upgrades. The geographic concentration of advanced testing capabilities in major metropolitan areas creates logistical costs and time delays for manufacturers in rural regions, particularly affecting agricultural processors with seasonal testing demands.

Lack of Standardized Testing Protocols Across Facilities

The absence of harmonized testing methodologies creates validation challenges when manufacturers work with multiple testing laboratories, as different analytical approaches may yield inconsistent results for identical samples. Cross-reactivity issues in immunoassay-based testing, particularly for closely related proteins, require facility-specific validation studies that increase implementation costs and complexity. The proliferation of testing kit manufacturers, each with proprietary methodologies and sensitivity thresholds, creates procurement complexity and results interpretation challenges for quality assurance teams. International supply chain integration requires reconciliation of different national testing standards, creating compliance complexity for manufacturers serving both domestic and export markets. The evolution of food processing techniques, including novel thermal treatments and ingredient modifications, outpaces standardization efforts, leaving manufacturers to develop proprietary testing protocols without regulatory guidance. Training standardization across testing personnel remains inconsistent, as different laboratories may emphasize different aspects of testing procedures, creating variability in results quality and interpretation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Allergen Type: Sesame Drives Regulatory Compliance

Milk allergens command the largest market share at 25.10% in 2025, reflecting their ubiquity in processed foods and the complexity of dairy-derived ingredients that require comprehensive testing across multiple protein fractions. The sesame allergen segment demonstrates the fastest growth at 7.84% CAGR through 2031, driven by the FASTER Act's January 2023 implementation that mandated sesame labeling as the ninth major allergen according to FDA (Food and Drug Administration). Tree nuts maintain significant testing demand due to cross-contamination risks in shared processing facilities, while peanut testing remains critical given the severity of allergic reactions and legal liability concerns. Egg allergens present unique challenges in processed foods where protein modifications during cooking may affect detectability, requiring specialized testing protocols for heat-treated products.

Wheat and soy allergens benefit from established testing methodologies, though the rise of alternative grain processing creates new contamination pathways that traditional protocols may not adequately address. Fish and shellfish allergens face increasing complexity as aquaculture practices diversify and processing facilities handle multiple species simultaneously. The "Others" category encompasses emerging allergens like mustard and celery that lack standardized testing protocols, creating market opportunities for specialized testing service providers. Aptamer-based detection systems, such as AYA22AR321 for peanut allergens, demonstrate potential for enhanced specificity and reduced cross-reactivity compared to traditional antibody-based methods

By Technology: NGS Emerges Despite ELISA Dominance

Immunoassay/ELISA technology maintains market leadership with 45.85% share in 2025, supported by established validation protocols, cost-effectiveness, and widespread laboratory familiarity that enables rapid implementation across diverse testing environments. Next-generation sequencing represents the fastest-growing segment at 6.55% CAGR through 2031, driven by its ability to simultaneously detect multiple allergens and provide definitive identification even in highly processed foods where protein structures may be altered. PCR-based methods offer enhanced sensitivity for detecting allergenic DNA sequences, particularly valuable for processed foods where protein-based detection may fail due to thermal degradation or chemical modification. Lateral-flow and biosensor technologies gain traction for point-of-use applications, enabling real-time testing in production environments though sensitivity limitations restrict their use to screening applications.

LC-MS/HPLC-MS systems provide superior specificity for complex food matrices, with university research demonstrating their effectiveness in analyzing processed foods' allergenic potential, though high equipment costs limit adoption to larger testing facilities. Other rapid methods, including nanobody-based assays, offer enhanced stability and reduced cross-reactivity compared to traditional antibodies, with research demonstrating effective detection of macadamia, peanut, and milk proteins. The integration of artificial intelligence in testing interpretation, exemplified by AllergenAI's protein sequence analysis capabilities, suggests future automation potential though regulatory acceptance remains uncertain. Technology selection increasingly depends on food matrix complexity, with highly processed foods requiring more sophisticated analytical approaches than raw ingredients.

By Food Tested: Plant-Based Innovation Drives Growth

Dairy products command the largest testing market share at 32.85% in 2025, reflecting both the prevalence of milk allergens and the complexity of dairy-derived ingredients that require testing across multiple processing stages and product formulations. Plant-based and novel proteins emerge as the fastest-growing segment at 7.42% CAGR through 2031, driven by consumer adoption of alternative proteins and the associated cross-contamination risks that require specialized testing protocols for emerging food categories. Bakery and confectionery products maintain substantial testing demand due to the common use of multiple allergenic ingredients and shared processing equipment that creates cross-contamination risks. Meat and seafood testing faces increasing complexity as processing facilities diversify protein sources and implement novel preservation techniques that may affect allergen detectability.

Baby food and infant formula represent a critical testing segment where regulatory requirements are most stringent, given the vulnerability of the target population and the potential severity of allergic reactions in infants. Beverage testing encompasses both traditional dairy-based products and emerging plant-based alternatives, with the latter requiring validation of allergen-free claims that command premium pricing. Other processed foods encompass specialty diet products and ethnic foods that may contain non-traditional allergens requiring customized testing approaches. The emergence of precision fermentation and cellular agriculture introduces novel protein sources with unknown allergenic profiles, creating demand for comprehensive safety assessment protocols.

By Testing Mode: Kits Gain Ground on Laboratory Dominance

Laboratory testing maintains dominance with 69.60% market share in 2025, supported by regulatory requirements for third-party validation and the analytical complexity required for definitive allergen identification in processed foods. Testing kits demonstrate the fastest growth at 7.25% CAGR through 2031, driven by manufacturers' desire for rapid, cost-effective screening capabilities that enable immediate production decisions without laboratory turnaround delays. Rapid testing adoption for pathogen analysis, suggesting similar growth potential for allergen testing kits as technology improves and regulatory acceptance increases.

Laboratory testing provides the analytical rigor required for regulatory compliance and legal protection, particularly for products entering interstate commerce or export markets where documentation requirements are stringent. Testing kits offer operational advantages including reduced sample handling, faster results, and lower per-test costs, though sensitivity limitations may restrict their use to screening applications rather than definitive analysis. The integration of smartphone-based readers and cloud connectivity in testing kits enables real-time data collection and trend analysis that supports continuous improvement in allergen control programs. Hybrid approaches combining kit-based screening with laboratory confirmation for positive results optimize both cost and analytical confidence, particularly for high-volume production environments where comprehensive testing would be prohibitively expensive.

Geography Analysis

The South region's market leadership at 28.40% share in 2025 stems from its concentration of food processing infrastructure, particularly in states like Texas, Georgia, and North Carolina, where major food manufacturers maintain production facilities that require comprehensive allergen testing protocols. The region benefits from established agricultural supply chains and ingredient processing facilities that create natural clusters of testing demand, supported by universities with food science programs that provide technical expertise and workforce development.

The South's growth trajectory benefits from continued food manufacturing investment and the expansion of plant-based protein production facilities that require specialized allergen testing protocols. However, the region faces challenges from seasonal agricultural production variations that create testing demand fluctuations and capacity constraints during peak processing periods. The West region's fastest growth at 6.85% CAGR through 2031 reflects its leadership in food innovation, particularly in plant-based and alternative protein categories that require novel testing approaches and specialized analytical capabilities. California's stringent food safety regulations often exceed federal requirements, creating demand for enhanced testing protocols that other states subsequently adopt, positioning Western laboratories as early adopters of advanced testing technologies.

The Northeast and Midwest regions maintain steady market positions, with the Northeast benefiting from dense population centers with high food allergy awareness and proximity to regulatory agencies that drive compliance requirements, while the Midwest leverages its agricultural processing infrastructure and established food manufacturing base. The FDA's Laboratory Flexible Funding Model allocated USD 23.2 million across 55 state programs in 2024, with significant investments in Northeastern and Midwestern laboratories that enhance regional testing capacity. Regional testing capacity distribution reflects historical food industry development patterns, though emerging food categories and changing consumer preferences are driving geographic shifts in testing demand that favor regions with innovation ecosystems and regulatory leadership.

Competitive Landscape

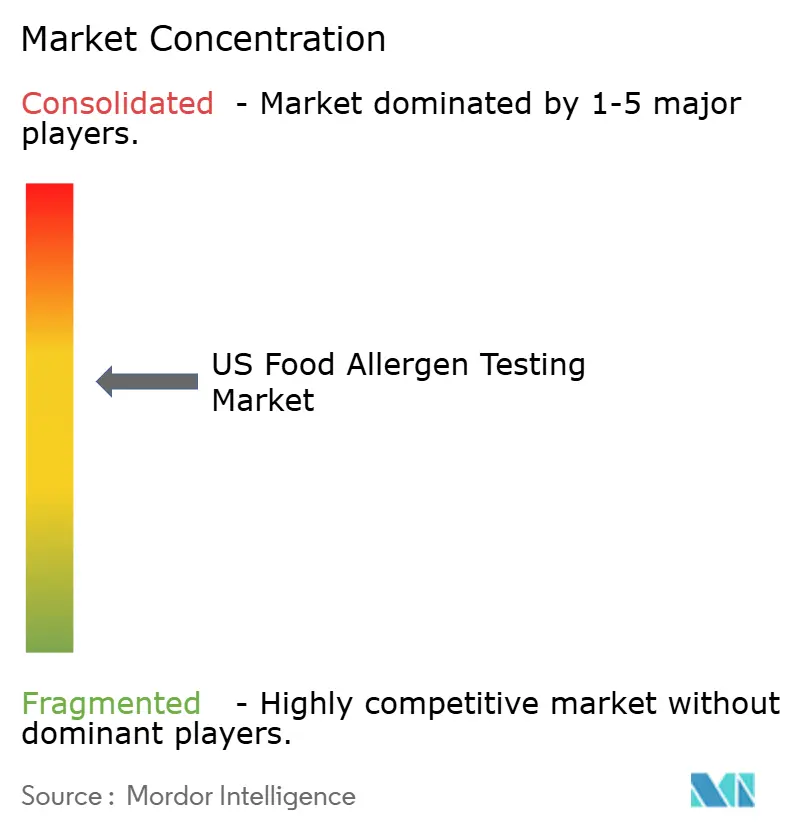

The food allergen testing market exhibits moderate consolidation, indicating substantial opportunities for both established players and specialized service providers to capture market share through technological differentiation and service innovation. Major players pursue vertical integration strategies, combining laboratory services with testing kit manufacturing and regulatory consulting to create comprehensive solutions that address the full spectrum of allergen control requirements. The competitive landscape increasingly favors companies that can provide rapid turnaround times, regulatory expertise, and technology integration capabilities that enable real-time monitoring and data analytics for continuous improvement in allergen control programs.

Emerging disruptors focus on technology innovation, particularly in rapid testing solutions and AI-enhanced analytical capabilities that promise to reduce costs and improve accuracy compared to traditional laboratory methods. In April 2025, Thermo Fisher Scientific's USD 2 billion U.S. investment commitment over four years signals the industry's confidence in sustained growth and the importance of domestic manufacturing capabilities for analytical instruments and diagnostics.

Strategic partnerships between testing service providers and food manufacturers create integrated solutions that embed allergen monitoring throughout the production process, from ingredient sourcing through final product validation. The market's moderate concentration creates opportunities for niche players specializing in specific allergens, food categories, or analytical techniques, particularly as regulatory requirements evolve and new food technologies emerge that require specialized testing approaches.

US Food Allergen Testing Industry Leaders

-

Eurofins Scientific

-

SGS Société Générale de Surveillance SA.

-

Mérieux NutriSciences Corporation

-

BeaconPoint Labs, LLC

-

DSM-Firmenich AG (Romer Labs Division Holding)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific announced a USD 2 billion investment in U.S. manufacturing and innovation over four years, including USD 1.5 billion in capital expenditures and USD 500 million in R&D, aimed at enhancing the domestic healthcare supply chain and analytical instrument production capabilities critical for food allergen testing

- April 2025: Beckman Coulter Life Sciences launched a Next-Generation Basophil Activation Test following a USD 1 million award from Food Allergy Research and Education, enabling safer food allergy research through blood-based testing that eliminates the anaphylaxis risks associated with traditional oral food challenges

- February 2025: Bio-Rad Laboratories reported plans to acquire Stilla Technologies to enhance its digital PCR product portfolio, supporting diverse applications including food safety monitoring and allergen detection, as part of its strategy to expand analytical capabilities in the food testing market

- January 2025: The FDA published final guidance on food allergen labeling requirements and evaluation of non-listed allergens, providing industry clarity on compliance requirements and establishing frameworks for assessing emerging allergens beyond the nine major categories

US Food Allergen Testing Market Report Scope

The US food allergen testing market is segmented by technology, into biosensors-based, immunoassay-based/ELISA, PCR, and other technologies. By food testing, the market is segmented into dairy products, bakery and confectionery, meat and seafood, baby food and infant formula, beverages, and other processed foods. The market is also segmented on the basis of geography.

By Allergen Type

| Peanuts |

| Tree Nuts |

| Milk |

| Eggs |

| Wheat |

| Soy |

| Sesame |

| Fish |

| Shellfish |

| Others |

By Technology

| Immunoassay/ELISA |

| PCR |

| Lateral-flow and Biosensors |

| LC-MS/HPLC-MS |

| Next-Generation Sequencing (NGS) |

| Other Rapid Methods |

By Food Tested

| Dairy Products |

| Bakery and Confectionery |

| Meat and Seafood |

| Baby Food and Infant Formula |

| Beverages |

| Plant-based/Novel Proteins |

| Other Processed Foods |

By Testing Mode

| Lab Testing |

| Testing Kits |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Allergen Type | Peanuts |

| Tree Nuts | |

| Milk | |

| Eggs | |

| Wheat | |

| Soy | |

| Sesame | |

| Fish | |

| Shellfish | |

| Others | |

| By Technology | Immunoassay/ELISA |

| PCR | |

| Lateral-flow and Biosensors | |

| LC-MS/HPLC-MS | |

| Next-Generation Sequencing (NGS) | |

| Other Rapid Methods | |

| By Food Tested | Dairy Products |

| Bakery and Confectionery | |

| Meat and Seafood | |

| Baby Food and Infant Formula | |

| Beverages | |

| Plant-based/Novel Proteins | |

| Other Processed Foods | |

| By Testing Mode | Lab Testing |

| Testing Kits | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the U.S. food allergen testing market?

The food allergen testing market reached USD 333.63 million in 2026.

Which allergen category is growing the fastest?

Sesame testing is projected to expand at an 7.84% CAGR through 2031 following its inclusion as the ninth major allergen.

Why are testing kits gaining popularity?

Kits deliver rapid, on-site screening with a 7.25% CAGR, helping processors make immediate line decisions before confirmatory laboratory analysis.

What technology is currently dominant in allergen testing?

Immunoassay/ELISA holds the lead with a 45.85% market share due to cost-effectiveness and validated protocols, although NGS is rising steadily.

Page last updated on: