Mycotoxin Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

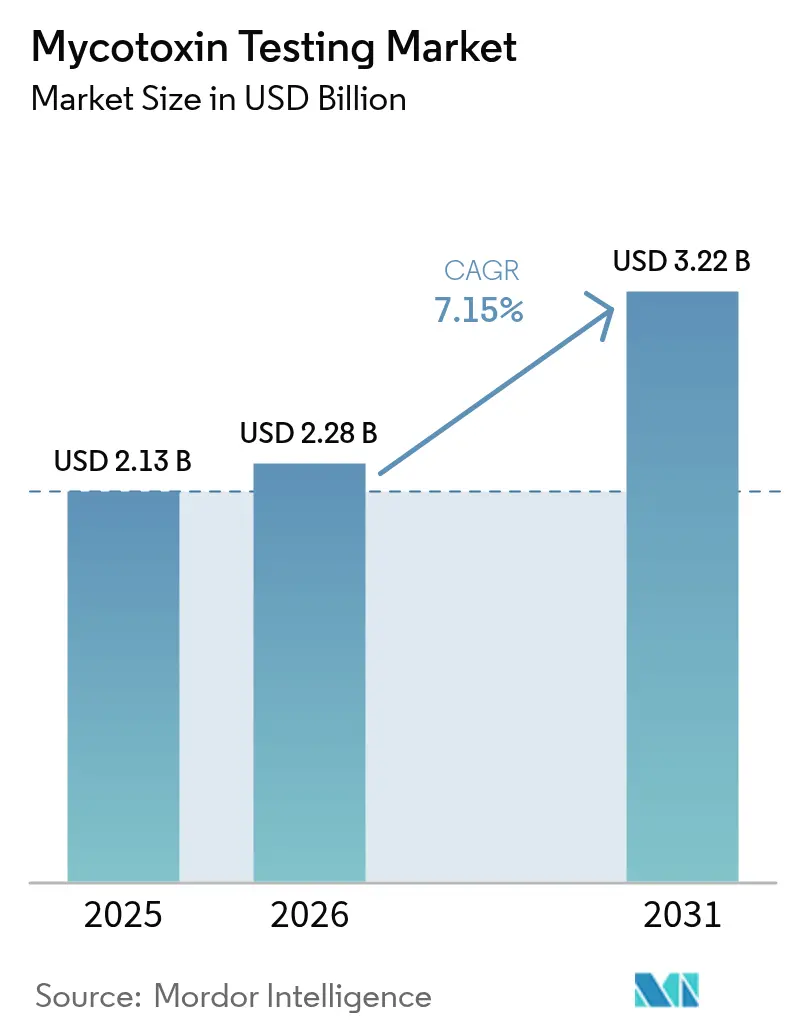

| Market Size (2026) | USD 2.28 Billion |

| Market Size (2031) | USD 3.22 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

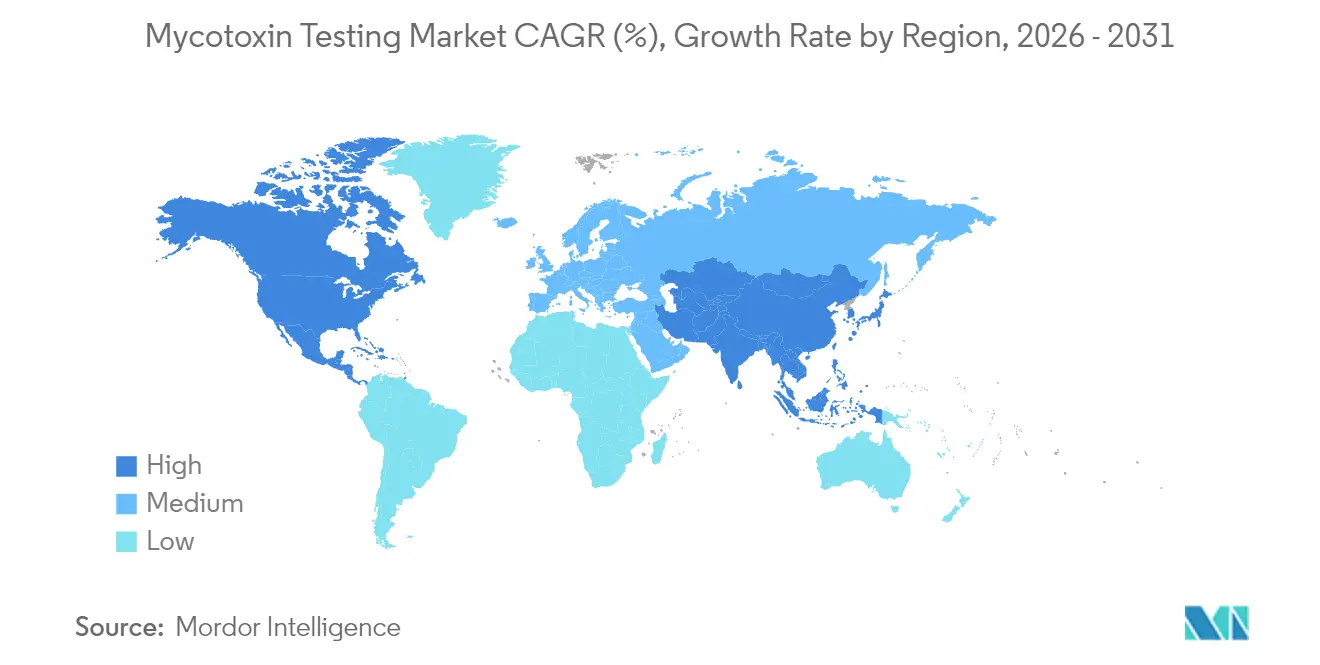

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mycotoxin Testing Market Analysis by Mordor Intelligence

The mycotoxin testing market size was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.28 billion in 2026 to reach USD 3.22 billion by 2031, at a CAGR of 7.15% during the forecast period (2026-2031). This growth trajectory reflects the escalating regulatory pressure following high-profile contamination incidents, including France's rejection of Turkish dried figs due to aflatoxin levels exceeding legal limits by 20 times in December 2024 and the tragic death of 450 dogs in Malawi from aflatoxin-contaminated maize. Chromatography-based platforms remain the benchmark for confirmatory analysis, yet rapid test kits are gaining ground as processors seek point-of-use screening. Climate-linked shifts in fungal prevalence, such as the surge in Fusarium toxins, further underpin routine testing demand. Global laboratories scale capacity in response to the European Union’s Regulation 2023/915 and the United States’ LAAF mandates, while Asia-Pacific laboratories add accredited instrumentation to serve rising export volumes according to FDA (Food and Drug Administration [1]Source: European Union,"Commission Regulation (EU)", eur-lex.europa.eu.

Key Report Takeaways

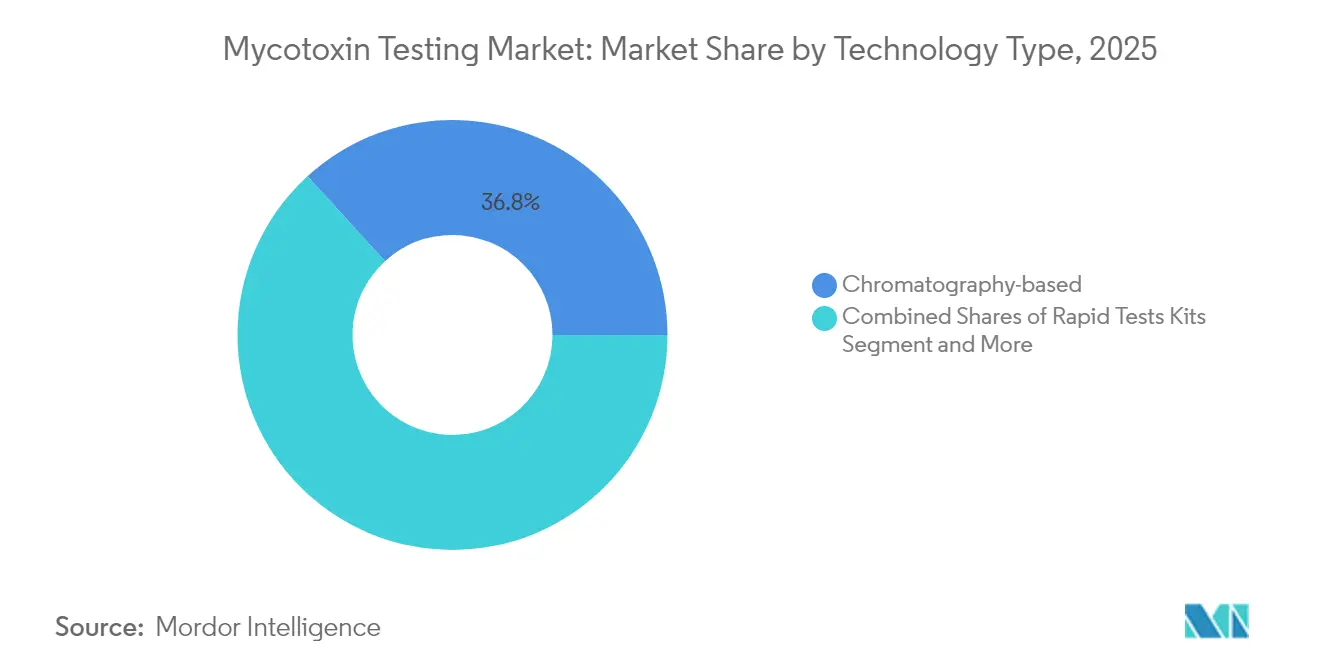

- By technology type, the chromatography-based segment led with 36.78% revenue share in 2025; rapid test kits are forecast to expand at a 8.98% CAGR through 2031.

- By mycotoxin type, aflatoxins accounted for 29.85% of the mycotoxin testing market share in 2025, while Fusarium toxins are projected to grow at 9.34% CAGR through 2031.

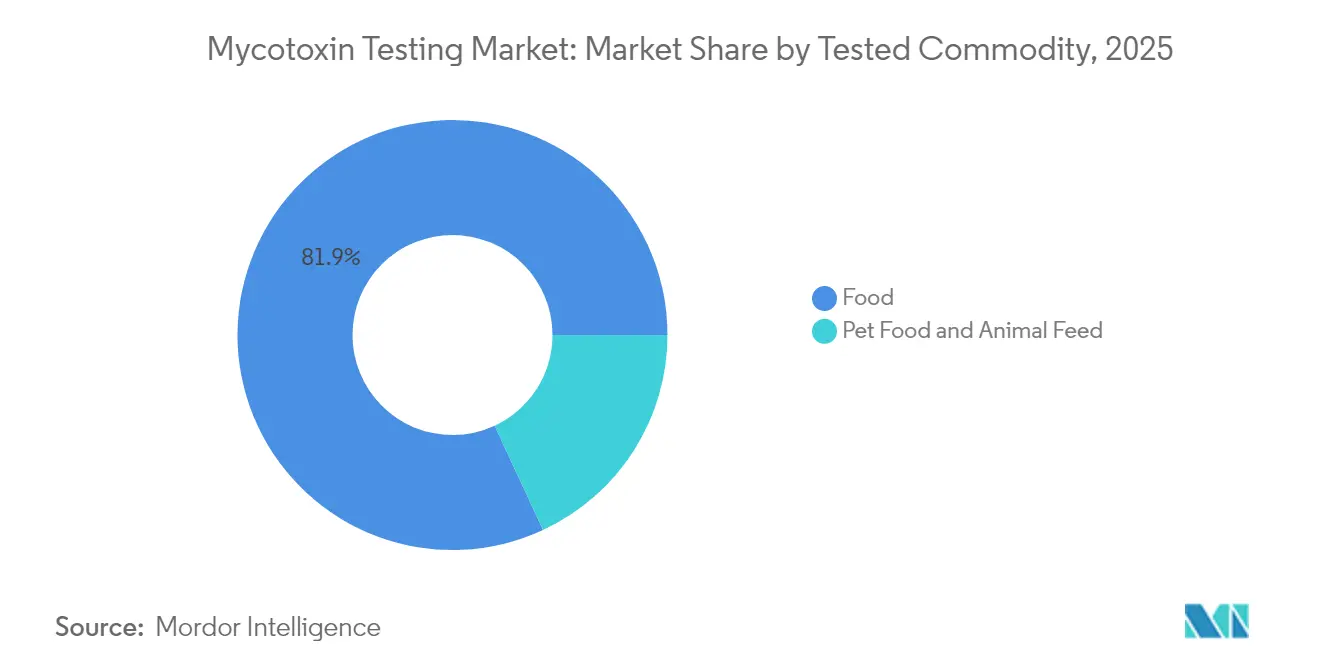

- By tested commodity, the food segment held 81.92% share of the mycotoxin testing market size in 2025, whereas pet food and animal feed testing are set to rise at an 8.62% CAGR between 2026-2031.

- By geography, North America contributed 34.45% revenue share in 2025 and Asia-Pacific is forecast to advance at a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mycotoxin Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness among consumers about food safety | +1.2% | North America, European Union | Medium term (2-4 years) |

| Stringent food safety regulations | +2.1% | European Union, North America | Long term (≥ 4 years) |

| Increased contamination incidents in grains, nuts, and processed foods | +1.8% | Climate-vulnerable regions worldwide | Short term (≤ 2 years) |

| Advancements in testing technologies | +1.5% | Developed markets | Medium term (2-4 years) |

| Expansion of certified testing laboratories in emerging markets | +1.3% | Asia-Pacific, Latin America, Africa | Medium term (2–4 years) |

| Increased adoption of rapid testing kits | +1.6% | Global (especially food-exporting countries) | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety Regulations

Regulatory tightening has fundamentally reshaped testing requirements, with the EU's Regulation 2023/915 consolidating maximum contaminant levels and introducing binding limits for T-2 and HT-2 toxins effective July 2024. The FDA's [2]Source: Food and Drug Administration, "Mycotoxins in Domestic and Imported Human Foods Compliance Program", www.fda.gov expansion of its Mycotoxins in Domestic and Imported Human Foods Compliance Program to include T-2/HT-2 toxins and zearalenone monitoring represents a parallel enforcement escalation. These regulatory shifts create cascading compliance costs that favor larger testing laboratories with advanced analytical capabilities. The implementation of limit of quantification requirements differentiating screening from confirmatory methods has particularly advantaged chromatography-based testing over traditional approaches. Australia's integration of food safety requirements into the Biosecurity Import Conditions system effective June 2025 exemplifies the global trend toward streamlined yet more rigorous import controls [3]Source: Australian Department of Agriculture, " Improving access to imported food safety requirements", www.agriculture.gov.auaccording to the Australian Department of Agriculture.

Increased Contamination Incidents in Grains, Nuts, and Processed Foods

Driven by climate-induced contamination patterns, testing demand has surged. In 2022, Serbia reported that 73.2% of its maize samples surpassed EU aflatoxin B1 limits, with peak levels hitting 527 µg/kg, as noted by MDPI (Multidisciplinary Digital Publishing Institute). The European Food Safety Authority has broadened testing protocols, identifying emerging risks like engineered nanomaterials and rare earth elements infiltrating food chains. Highlighting the ongoing fungal threats, Japan's Ministry of Health, Labour and Welfare flagged multiple mold detection incidents in 2024-2025, including in sweet potato products and rice cakes. There's a growing recognition of the link between temperature and humidity fluctuations and mycotoxin levels, with elevated warmth and moisture leading to heightened contamination. This heightened climate sensitivity has shifted the focus towards proactive testing strategies, moving away from mere reactive contamination management.

Advancements in Testing Technologies

VICAM's Vertu TOUCH strip test reader, a testament to the rapid evolution in technology, delivers quantitative results for six primary mycotoxins in just 10 minutes, all without the necessity for specialized training.Hyperspectral imaging integrated with machine learning algorithms has emerged as a non-destructive detection method, offering real-time monitoring capabilities for industrial applications. The development of silicon-core quantum dot fluorescent probes has achieved detection limits as low as 0.25 ng/mL for vomitoxin in cereals, with average recovery rates exceeding 92%. By integrating with nanomaterials, surface-enhanced Raman spectroscopy platforms have boosted their sensitivity, overcoming past challenges like signal stability and interference from intricate food matrices. Thanks to these technological leaps, results that once took hours can now be achieved in mere minutes, all while upholding the analytical precision of conventional chromatographic methods.

Expansion of Certified Testing Laboratories in Emerging Markets

Laboratory infrastructure development in Asia-Pacific has accelerated, with Japan Food Research Laboratories expanding mycotoxin testing capabilities using LC-MS/MS and PCR technologies. India's FSSAI extended the implementation date for mandatory registration of foreign food manufacturing facilities to September 2024, creating demand for accredited testing services according to USDA [4]Source: U.S Department of Agriculture, "India's FSSAI Extends Effective Implementation Date for Mandatory Registration of Foreign Food Manufacturing Facilities", www.fas.usda.gov. The CDC's [5]Source: Centers for Disease Control and Prevention (CDC),"NOFO CD-25-0019", www.cdc.govfunding opportunity NOFO CD-25-0019 allocated resources to enhance public health laboratory capabilities, with a 5-year funding period starting July 2025. Michigan's groundbreaking of a 300,000-square-foot public health and environmental science laboratory, scheduled for completion in late 2026 with a USD 326 million budget, exemplifies the infrastructure investments driving capacity expansion. These developments reflect the strategic shift toward distributed testing networks that reduce dependency on centralized facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced equipment and reagents | -1.4% | Developing regions | Medium term (2-4 years) |

| Lack of standardized testing regulations | -1.1% | Global (especially low-regulation markets) | Long term (≥ 4 years) |

| Limited access to accredited labs in developing regions | -1.2% | Asia-Pacific, Africa, Latin America | Medium term (2–4 years) |

| Shortage of skilled technicians for handling complex instruments | -0.9% | Emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Testing Equipment and Reagents

Advanced LC-MS/MS systems, pivotal for mycotoxin testing, demand hefty investments surpassing USD 500,000. This figure doesn't account for the annual reagent expenses, which can soar to USD 100,000, especially in high-throughput labs. Adding to the industry's woes, the FDA is reportedly eyeing a 17% budget cut for FY 2026. Such a move could halt the Proficiency Testing Program for food labs, jeopardizing quality control and inflating compliance costs for private entities. Furthermore, crafting certified reference materials for intricate matrices—like corn/peanut blended vegetable oil—demands significant outlays in method validation and inter-laboratory studies. These financial and operational challenges are further compounded by the need for continuous training of laboratory personnel to handle advanced systems effectively. Additionally, the lack of uniform global regulations for mycotoxin testing creates inconsistencies in testing standards, complicating international trade. As cost pressures mount, many are turning to rapid testing alternatives, albeit often at the expense of analytical precision in favor of quicker results.

Shortage of Skilled Technicians for Handling Complex Instruments

Laboratories, especially those delving into advanced analytical techniques like chromatography and mass spectrometry, grapple with workforce limitations that hinder their capacity expansion. For instance, analyzing multiple mycotoxins with integrated systems, such as the ASAG563 for trichothecenes, necessitates a high level of expertise in method optimization and troubleshooting. Moreover, as laboratories adopt emerging technologies like gas chromatography-ion mobility spectrometry for early detection of Aspergillus contamination, they face heightened training demands. The shift from conventional methods to AI-driven detection systems underscores the need for a blend of skills, merging analytical chemistry with data science. However, workforce development initiatives have lagged behind these technological strides, leading to productivity bottlenecks and curtailing the adoption of cutting-edge testing protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Rapid Innovation Drives Market Evolution

In 2025, chromatography-based technologies held a commanding 36.78% market share, bolstered by regulatory mandates for confirmatory analyses and the heightened precision required for trace-level detections. Meanwhile, rapid test kits emerged as the industry's fastest-growing segment, boasting a 8.98% CAGR projected through 2031, underscoring a pronounced shift towards point-of-use testing. Waters Corporation's launch of the waters_connect Data Intelligence software in November 2024 highlights the industry's pivot, steering chromatographic platforms towards cloud-centric business intelligence and heightened audit readiness. While immunoassay methods remain the go-to for primary screenings, there's a noticeable uptick in the adoption of spectroscopy and biosensor methods for real-time monitoring.

Artificial intelligence's integration with conventional analytical techniques is carving out a competitive edge. Notably, machine learning algorithms are refining hyperspectral imaging's accuracy for mycotoxin detection in cereal grains, as highlighted by MDPI (Multidisciplinary Digital Publishing Institute). Innovations in nanotechnology and microfluidics are propelling the momentum of other technologies, such as novel biosensor platforms and portable detection devices. Furthermore, advancements like time-resolved fluorescence immunoassays, which now detect aflatoxin B1 at an impressive 0.3 µg/kg limit, underscore the industry's relentless pursuit of heightened sensitivity across all platforms.

By Mycotoxin Type: Fusarium Toxins Emerge as Growth Driver

In 2025, aflatoxins held a dominant 29.85% share of the market, underscoring their position as the world's most stringently regulated mycotoxin class. Meanwhile, Fusarium toxins emerged as the fastest-growing category, boasting a 9.34% CAGR projected through 2031. The European Union's introduction of binding limits for T-2 and HT-2 toxins, set to take effect in July 2024, has spurred a surge in testing demand for these compounds, which were previously not as closely monitored. Testing for Ochratoxin A remains consistently in demand, largely due to the needs of the wine and coffee sectors, whereas patulin testing is predominantly centered on fruit products.

Advancements in multi-mycotoxin detection platforms have revolutionized the economics of testing. For instance, lateral flow immunoassays can now simultaneously detect aflatoxin B1, zearalenone, and T-2 toxin in just 20 minutes, as reported by MDPI (Multidisciplinary Digital Publishing Institute). A tragic reminder of the dangers posed by aflatoxins is the incident in Malawi, where 450 dogs lost their lives due to aflatoxin-contaminated maize. On a proactive note, Spectral Blue has pioneered a Multi-Wavelength, High-Intensity blue light technology, aiming to diminish deoxynivalenol levels in tainted grains, marking a significant stride in post-harvest mycotoxin management.

By Tested Commodity: Pet Food Segment Accelerates

In 2025, the food segment dominated the market with an 81.92% share, covering categories like meat, poultry, dairy, fruits, vegetables, and processed foods. However, the pet food and animal feed testing segment is emerging as the fastest-growing, boasting an 8.62% CAGR projected through 2031. A notable driver of this growth is Taiwan's July 2024 move to set safety tolerance levels for five additional mycotoxins in pet food. This includes specific limits for vomitoxin and fumonisin. Within the broader food category, testing has intensified: processed food scrutiny heightened after contamination incidents, dairy testing zeroes in on aflatoxin M1, and fruits and vegetables testing targets patulin and other mycotoxins.

Advanced optical sorting technologies are reshaping pet food safety. Bühler's SORTEX LumoVision, for instance, can slash aflatoxin levels by up to 90% using fluorescence to detect contaminated kernels. As regulatory frameworks broaden, there's a surge in testing demands for other food categories, notably specialty products and nutraceuticals. The FDA's post-October 2024 enforcement policy for AAFCO-defined animal feed ingredients has set clear regulatory expectations for novel feed components, all while upholding stringent safety standards.

Geography Analysis

In 2025, North America secured a commanding lead with a 34.45% market share, thanks to stringent FDA enforcement and a robust testing infrastructure. Demonstrating its dedication, the FDA has set aside USD 15 million in its FY 2025 budget, zeroing in on microbiological and chemical safety. Canada's 2024-2025 departmental plan prioritizes regulatory modernization and boosts laboratory capacity for disease detection, reinforcing the region's testing infrastructure.

The Asia-Pacific region, however, is making waves, projecting a notable 9.18% CAGR through 2031. Japan's swift action on mold detection, following several contamination incidents in 2024-2025, underscores the region's dedication to food safety. India's FSSAI has extended foreign facility registration requirements to September 2024, signaling the shifting regulatory landscape in emerging markets.

Europe benefits from harmonized regulations under EU Regulation 2023/915, yet Brexit has complicated trade dynamics between the UK and the EU. Meanwhile, the European Environment Agency warns of mycotoxin exposure due to shifting climate conditions, stressing the urgency for adaptive testing strategies. In South America, key grain-producing regions are battling climate-induced contamination issues. Concurrently, the Middle East and Africa are bolstering their testing infrastructures to meet export standards.

Note: Segment shares of all Individual segments will be available upon report purchase

Regulatory Landscape

Mycotoxin testing requirements are shaped by a mix of maximum-level regulations, prescribed sampling plans, and laboratory competence rules that govern both domestic control and cross-border trade. In the European Union, Regulation (EU) 2023/915 anchors maximum levels for contaminants in food, and Regulation (EU) 2024/1038 introduced binding maximum levels for T-2 and HT-2 toxins effective 1 July 2024, expanding routine monitoring beyond legacy aflatoxin-centric programs.

Method and sampling harmonization is tightening alongside limits. Commission Implementing Regulation (EU) 2023/2782 (effective 1 April 2024) updated EU sampling and analysis methods for mycotoxins, with specific updates for certain dried commodities via Implementing Regulation (EU) 2024/885 (20 March 2024). In the United States, the FDA updated its Mycotoxins in Domestic and Imported Human Foods Compliance Program (CP 7307.001) in September 2024, and its Chemical Contaminants Transparency Tool (updated March 2025) consolidates current action levels and guidance used by industry and labs for method selection and enforcement readiness. The EEA framework also incorporated relevant contaminant rules through Decision 2026/970 effective 7 February 2026, reinforcing alignment across the wider European market.

Value Chain Analysis

The mycotoxin testing value chain starts upstream with risk surveillance and sampling across farms, storage silos, and grain handling systems, where inhomogeneous toxin distribution makes sampling design as critical as the analytical method. Food and feed operators commonly use in-house screening (immunoassays and strip tests) for rapid lot disposition, then route positives and export lots to accredited laboratories for confirmatory chromatography (LC-MS/MS/HPLC) aligned to official methods, including those under EU Implementing Regulation (EU) 2023/2782 (effective 1 April 2024).

Midstream and downstream, the value chain is anchored by accredited contract labs (global networks and local providers), reference material and reagent suppliers, and instrument OEMs supplying UHPLC/LC-MS/MS platforms, sample-prep consumables, and LIMS/data tools for audit trails. Public-sector and standards bodies also shape day-to-day workflows: USDA AMS runs the Laboratory Approval Program for Analysis of Mycotoxins (aligned with ISO/IEC 17025) for nuts such as almonds, peanuts, and pistachios, while ISO 23719:2025 defines a validated UHPLC-MS/MS method for 17 mycotoxins in cereals, supporting method harmonization for trade. Key bottlenecks center on advanced instrument cost, technician availability, and the operational load created by tighter, commodity-specific sampling plans, which lifts demand for automation, multiplexed workflows, and distributed sample intake close to origin.

Competitive Landscape

The mycotoxin testing market is moderately fragmented, marked by fierce competition among established laboratory service providers and manufacturers of analytical instruments. Some of the major players include Eurofins Scientific SE, SGS S.A., Thermo Fisher Scientific Inc., and Institut Mérieux, among others. A notable instance of strategic consolidation is Mérieux NutriSciences' acquisition of Bureau Veritas' food testing business for EUR 360 million in October 2024. This move has birthed a unified entity boasting 34 laboratories worldwide and a workforce exceeding 1,900.

Companies are heavily investing in AI-driven analytical solutions and cloud-based data management systems, focusing on technology differentiation through automation capabilities, multi-analyte detection platforms, and seamless integration with digital infrastructure. Eurofins Scientific's revenue surged by 6.7% in the first three quarters of 2024, hitting EUR 5,142 million, underscoring the market's significant growth potential. Patent filings are predominantly centered on enhancing analytical methods and innovating detection technologies, with a notable emphasis on novel biosensor designs and advanced sample preparation techniques.

New entrants, particularly specialized biosensor developers and manufacturers of rapid testing kits, are redefining the landscape, offering point-of-use solutions that rival traditional laboratory models. While technology frontrunners harness proprietary analytical methods and navigate regulatory landscapes for a competitive edge, smaller entities carve out niches in specific applications or regional markets. The FDA's Laboratory Flexible Funding Model Cooperative Agreement Program, with its allocation of USD 23.2 million aimed at bolstering state laboratory capabilities, paves the way for collaborative ventures between public entities and private firms in advancing testing infrastructure.

Mycotoxin Testing Industry Leaders

-

Eurofins Scientific SE

-

SGS S.A.

-

Thermo Fisher Scientific Inc.

-

Institut Mérieux

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven method harmonization and multi-analyte requirements create clear demand for labs and technology vendors that can industrialize high-throughput, standardized UHPLC-MS/MS workflows and digital audit readiness. ISO 23719:2025 (published July 2025) provides a concrete framework for determining 17 mycotoxins in cereals and cereal products, supporting rollouts of validated multi-mycotoxin panels across grain supply chains and export programs that need comparable results between internal QC labs and external confirmatory providers.

A second opportunity is the more structured operational split between rapid, on-site screening and confirmatory lab analysis under updated EU sampling and analysis rules (Implementing Regulation (EU) 2023/2782, effective 1 April 2024, with transitional provisions extending legacy method acceptance until January 2029). This dynamic supports investment in point-of-use tools that reduce cycle time for lot release while keeping chromatography capacity focused on confirmatory and multi-residue work. Industry practice reflects this hybridization: COCERALs 2025 mycotoxin management survey notes broad use of EU official sampling plans and internal ELISA-based checks, with external validation frequently performed via high-performance liquid chromatography, which supports a service model for networked labs offering both fast screening pathways and accredited confirmation for trade-facing lots.

Recent Industry Developments

- June 2026: Eurofins WEJ Contaminants reported detection of aflatoxin B1 in Austrian maize and highlighted its screening services across relevant matrices. The update points to how harvest-season surveillance and rapid lot screening are used to triage risk before confirmatory workflows, supporting more continuous testing demand tied to climate and crop variability.

- October 2025: Thermo Fisher Scientific launched the Thermo Scientific Orbitrap Exploris EFOX Mass Detector, positioned for routine environmental and food safety laboratories and applicable to contaminant testing including mycotoxins. The instrument refresh supports broader adoption of high-resolution accurate-mass screening for multi-residue workflows as labs expand beyond targeted panels and need stronger non-target and suspect-screen capability.

- September 2024: SGS South Africa introduced a SANAS-accredited multi-mycotoxin screening method using HPLC/MS with a stated turnaround of within three days, covering toxins such as aflatoxins, DON, zearalenone, fumonisins, and T-2/HT-2. The accreditation-backed offering strengthens local compliance capacity for exporters and processors that require defensible results under tightened sampling and maximum-level regimes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from laboratory and rapid methods used to detect and quantify mycotoxins in food and feed samples, including testing carried out for compliance, quality checks, and release decisions across the supply chain.

Scope exclusions: It excludes broader food-safety tests that are not mycotoxin-specific, plus on-farm visual screening that does not generate a paid testing revenue line.

Segmentation Overview

-

By Technology Type

- Chromatography-based

- Immunoassay-based

- Rapid Test Kits

- Spectroscopy and Biosensor-based

- Other Technologies

-

By Mycotoxin Type

- Aflatoxins

- Ochratoxin A

- Patulin

- Fusarium Toxins

- Other Mycotoxins

-

By Tested Commodity

-

Food

- Meat and Poultry

- Dairy

- Fruits and Vegetables

- Processed Food

- Other Food

- Pet Food and Animal Feed

-

Food

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with pulling the basic demand context for grains, nuts, spices, and other higher-risk commodities, because these flows drive routine sampling volumes. We referenced public sources such as USDA, FAO, the European Commission food and feed safety portals, and Codex Alimentarius updates to map common mycotoxin limits and how often rules get tightened.

To keep the revenue model grounded, we also used sources like UN Comtrade for trade direction signals, peer reviewed articles for method adoption patterns (for example, LC-MS/MS versus immunoassays), and association and regulator websites that publish alert trends and testing guidance. Company filings, investor presentations, and trusted press were then used to sanity check service mix and geographic exposure, and we supplemented that with paid subscriptions for company financials, patents, and shipment level import export cues where needed. The examples above are not exhaustive, and many other sources were referred to for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with testing laboratories, instrument and kit ecosystem participants, and procurement and quality leaders in food, beverage, and feed value chains. We used these discussions to confirm real testing frequency, typical price bands by method, and what portion of samples move from screening into confirmatory workflows, where revenue can shift the most. For a global market, inputs were balanced across APAC, EMEA, and the Americas so assumptions were not built from a single regulatory environment.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 48% |

| Mid tier: 41% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 20% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where food and feed production and trade data are translated into a testable sample pool using realistic sampling intensity assumptions, and then converted into revenue using method mix and average pricing. To keep the totals practical, we corroborated the outputs with selective bottom-up checks such as sampled lab revenue run rates, channel feedback on kit volumes, and typical throughput per instrument setup, and then applied adjustments where gaps appeared.

A few inputs carried most of the model weight, including commodity risk exposure by region, regulatory limit changes that trigger more frequent testing, the share of samples routed to confirmatory testing, average tests per lot (seasonality was reflected where harvest cycles matter), and price progression by method as lab automation rises. For forecasting, scenario analysis was used so adoption shifts (for example, faster movement to LC-MS/MS confirmatory testing) and policy tightening could be reflected without forcing one single growth path. Where primary inputs were missing for smaller countries, assumptions were proxied from comparable regulatory regimes and trade baskets, and then re-checked in validation calls.

Data Validation & Update Cycle

Model outputs were checked against independent signals, such as changes in food and feed alert volumes, method adoption commentary from labs, and visible capacity expansion announcements, and then large variances were reviewed line by line. When a number looked off, we re-contacted sources to confirm whether the issue came from scope, pricing, or a temporary demand spike, and the logic was corrected before sign-off.

The report is refreshed annually, and interim updates are made when there are material events like major regulation changes, large lab network expansions, or sharp currency moves that can distort price points. Before delivery, an analyst performs a final pass so the numbers reflect the latest available public data and recent expert feedback.

Mordor Intelligence's Mycotoxin Testing Market Size Measured Against Other Published Estimates

Published market sizes for mycotoxin testing often differ because teams make different choices on what counts as testing revenue, which year is treated as the current base, and how pricing changes are carried forward when method mix shifts.

In this study, the spread is mainly explained by refresh timing and currency timing, followed by how average selling prices are handled between screening and confirmatory methods, since real lab pricing can move even when sample volumes are stable. A tighter validation loop using commodity risk signals and method mix checks can also pull the estimate closer to what labs report as actual run-rate revenue, and that is why the 2026 baseline aligns differently than figures anchored to earlier or longer-horizon base years, a refresh-led choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.28 B (2026) | |

| Global Consultancy A | USD 1.43 B (2025) | Anchored to a prior base year, which can understate recent method-mix driven ASP uplift, and may apply different currency conversion timing that dampens the latest reported revenue level. |

| Industry Publisher B | USD 1.81 B (2026) | Uses a broader long-horizon forecast frame that can smooth near-term pricing and volume swings, and may treat service and product revenue boundaries differently across screening and confirmatory workflows. |

Looking across the three figures, the main takeaway is that the market size moves noticeably when the base year is updated, prices are translated consistently into USD, and screening versus confirmatory economics are modeled separately. By keeping these steps explicit and then checking them against real-world demand signals, the final value becomes easier to reproduce and audit during client planning discussions.

Key Questions Answered in the Report

What is the current size of the mycotoxin testing market?

The market is valued at USD 2.28 billion in 2026 and is forecast to reach USD 3.22 billion by 2031.

Which testing technology holds the largest share?

Chromatography platforms lead with 36.78% revenue share in 2025, reflecting their role in confirmatory analysis.

Why are Fusarium toxins attracting more attention?

Climate shifts have raised Fusarium contamination levels, and new EU limits introduced in 2024 mandate greater surveillance.

Which region is growing the fastest?

Asia-Pacific is projected to register a 9.18% CAGR through 2031, driven by expanding export-oriented testing capacity.

How will rapid test kits impact the future landscape?

Rapid kits are set to grow at 8.98% CAGR, enabling on-site screening and faster release of shipments without sacrificing accuracy.

Page last updated on: