Market Overview

| Study Period | 2021 - 2031 |

|---|---|

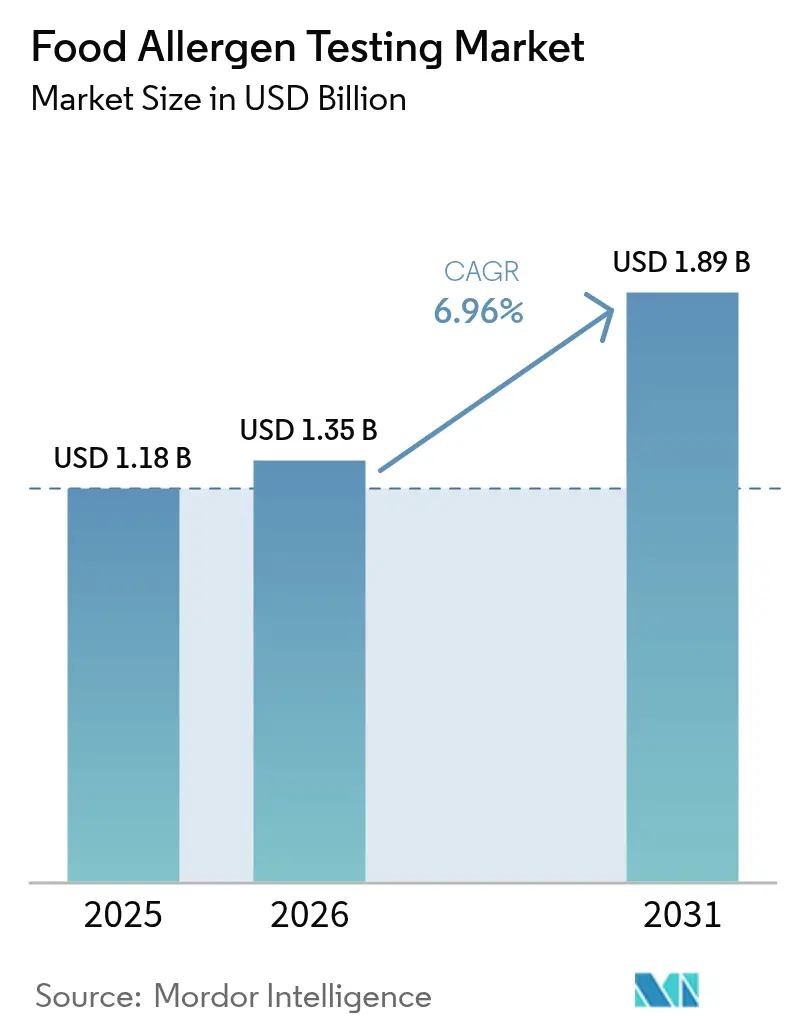

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.89 Billion |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Allergen Testing Market Analysis by Mordor Intelligence

The food allergen testing market size is projected to grow from USD 1.18 billion in 2025 to USD 1.35 billion in 2026, reaching USD 1.89 billion by 2031, with a CAGR of 6.96% during 2026-2031. Manufacturers are transitioning from end-line checks to in-process verification, as undeclared allergens remain the leading cause of food recalls, significantly increasing brand-risk costs that often surpass withdrawal expenses. While Europe remains the primary market, demand in the Asia-Pacific region is rising due to export growth and the adoption of EU-style labeling regulations. Immunoassay methods dominate in terms of volume due to their portability; however, polymerase chain reaction (PCR) platforms are experiencing faster growth as retailers require sequence-level verification for ISO 17025 audits. Additionally, capital-intensive mass spectrometry is gaining popularity in high-value categories, such as infant formula, where sub-ppm limits are essential.

Key Report Takeaways

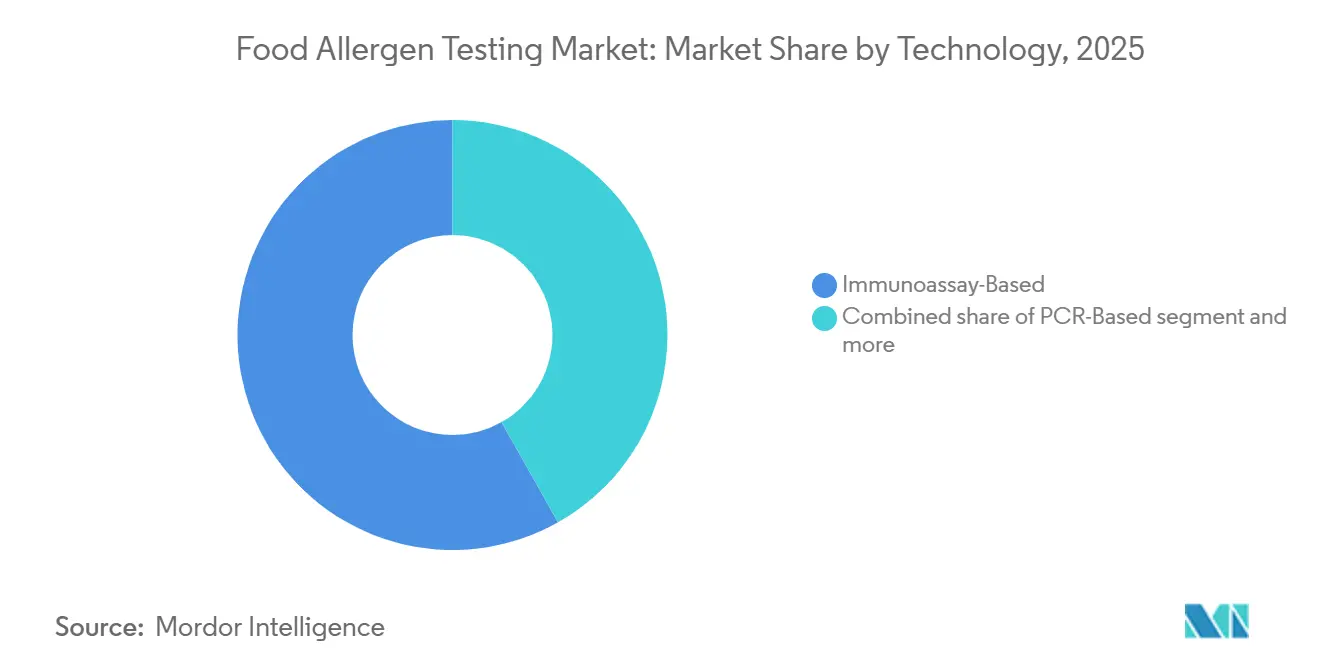

- By technology, immunoassay methods accounted for 58.17% of the food allergen testing market share in 2025, while polymerase chain reaction-based platforms are expected to grow at a CAGR of 7.38% through 2031.

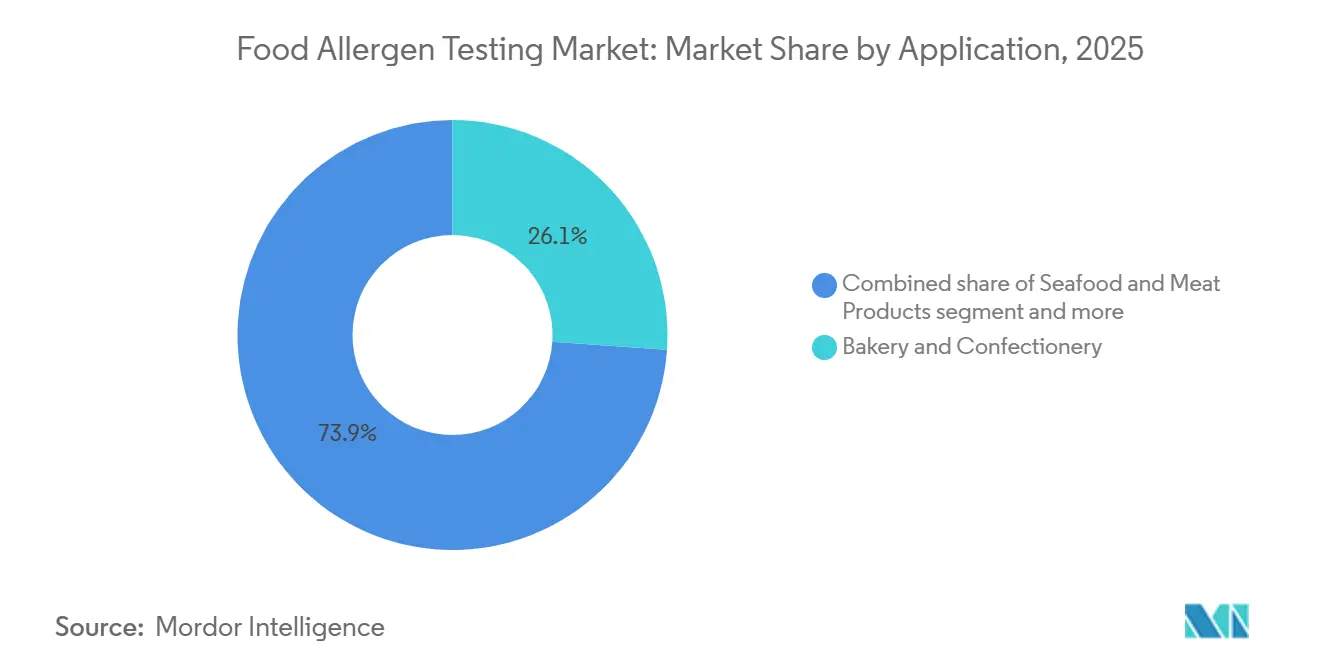

- By application, bakery and confectionery represented 26.09% of the food allergen testing market size in 2025, whereas seafood and meat products are projected to achieve a CAGR of 9.56% between 2026 and 2031.

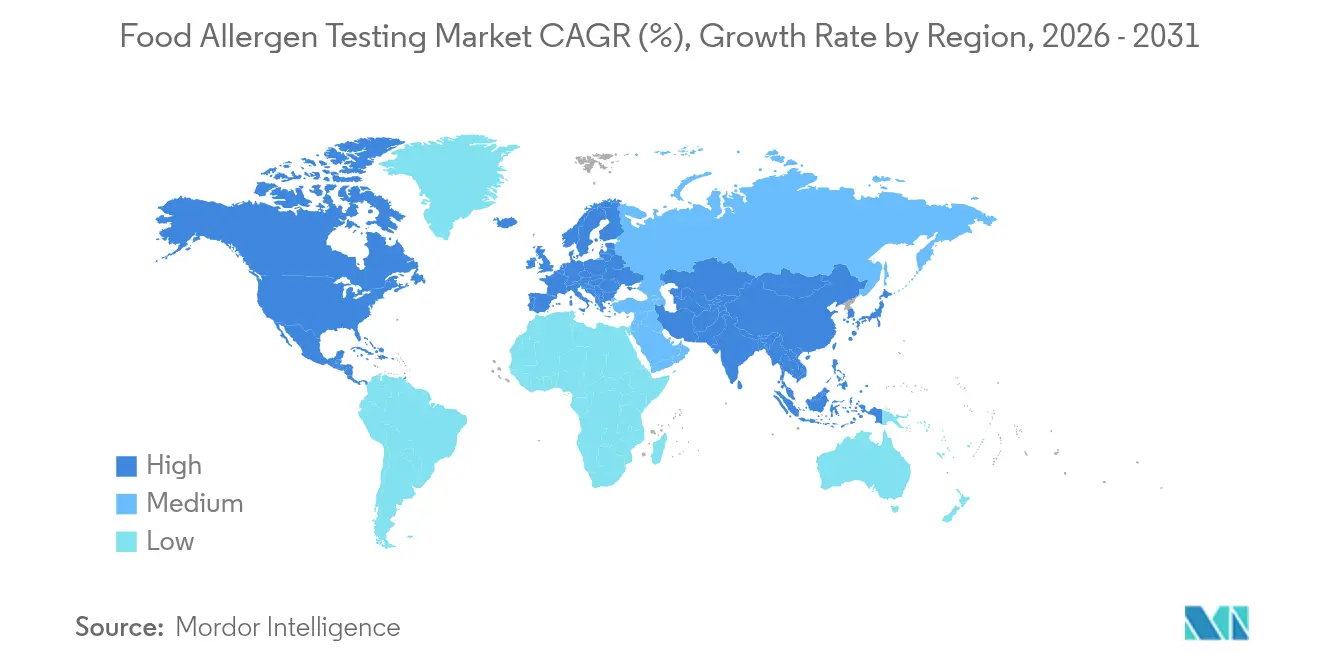

- By geography, Europe held 34.47% of the food allergen testing market share in 2025, while Asia-Pacific is anticipated to grow at a CAGR of 8.98% during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Allergen Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in food recalls and brand-risk costs | +1.4% | North America, European Union (EU) | Short term (≤ 2 years) |

| Tightening allergen labeling laws and enforcement | +1.6% | North America, European Union (EU), Asia-Pacific | Medium term (2-4 years) |

| Expansion of global processed-food trade | +1.2% | Asia-Pacific export hubs, Middle East, Africa | Medium term (2-4 years) |

| Harmonized reference-dose rules lowering LOQs | +0.9% | European Union (EU) first, adoption in Asia-Pacific and South America | Long term (≥ 4 years) |

| Consumer demand for clean-label and allergen-free foods | +1.1% | North America, European Union (EU), urban Asia-Pacific | Medium term (2-4 years) |

| Accredited labs and audit readiness standardize test protocols | +0.7% | Global, led by ISO 17025 uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in food recalls and brand-risk costs

The increasing frequency and economic impact of allergen-related food recalls are driving significant changes in the food industry's approach to risk management. Undeclared allergens remain the primary cause of global recalls. In the United Kingdom, 53 cases of undeclared allergen recalls were reported in 2024, representing a 10% increase and highlighting ongoing challenges in preventing cross-contamination [1]Source: Food Safety, "Proactive Allergen Prevention in the Foodservice Industry", food-safety.com. Regulatory changes are also shaping industry practices. The FDA’s Food Safety Modernization Act (FSMA) Section 204, scheduled for enforcement in January 2026, requires digital traceability systems to improve visibility into allergen control failures and their associated legal and financial risks. This regulation is encouraging manufacturers to focus on proactive testing and preventive measures rather than reactive responses to recalls, leading to a steady increase in the adoption of rapid allergen detection technologies. Risk reduction and regulatory compliance are particularly crucial in the foodservice sector, which reports the second-highest rate of allergic incidents after household consumption.

Tightening allergen labeling laws and enforcement

The push for regulatory alignment across major global markets is increasing pressure on food manufacturers, extending beyond traditional labeling requirements to encompass production practices and supply chain verification protocols. In 2024, the FDA released Edition 5 guidance on allergen control, introducing more stringent requirements for cleaning validation and environmental monitoring. Concurrently, the USDA’s Food Safety and Inspection Service launched a dedicated allergen verification initiative targeting meat and poultry processors. Similarly, the Dutch Food and Consumer Product Safety Authority revised its guidelines on preventing cross-contact, detailing testing frequencies and analytical methods for manufacturers. These regulatory updates significantly affect multinational food companies, which must manage varying levels of enforcement across regions, with Europe imposing some of the most stringent compliance standards. Emerging markets are also impacted, as export-driven producers adopt international allergen testing protocols to access high-value markets.

Expansion of global processed-food trade

The globalization of food supply chains presents significant challenges in allergen management, surpassing the capabilities of conventional testing methods. With ingredients sourced from multiple regions governed by varying regulatory frameworks, manufacturers must adopt standardized testing protocols to comply with destination market requirements while mitigating contamination risks from source countries. The emergence of alternative proteins, such as plant-based, fungal, and insect-derived ingredients, introduces new allergen-related complexities that demand specialized analytical techniques beyond traditional immunoassays [2]Source: National Center for Biotechnology Information, "Allergenicity of Alternative Proteins: Reduction Mechanisms and Processing Strategies," pmc.ncbi.nlm.nih.gov. Furthermore, processing methods like heat treatment, enzymatic hydrolysis, and fermentation can modify protein structures, potentially impacting their detectability. This necessitates the use of advanced analytical tools, including mass spectrometry and peptidomics. This challenge is particularly evident in the Asia-Pacific region, where urbanization and an expanding middle class are driving increased demand for imported processed foods. These factors create substantial opportunities for internationally accredited allergen testing service providers, as manufacturers prioritize reliable solutions to ensure regulatory compliance and protect consumer safety within increasingly intricate supply chains.

Harmonized reference-dose rules lowering LOQs

The global effort to standardize reference-dose methodologies is driving the adoption of advanced and highly sensitive analytical platforms for allergen detection, as regulators enforce stricter quantification limits. This shift from basic presence/absence testing to quantitative risk assessment requires measurements at sub-parts-per-million levels, which traditional methods often fail to achieve. Complex food formulations pose additional challenges for conventional Enzyme-Linked Immunosorbent Assay (ELISA) techniques due to their limited sensitivity and specificity. This has led to an increasing preference for Liquid Chromatography–Tandem Mass Spectrometry (LC-MS/MS) and other advanced analytical methods. Laboratories utilizing these technologies gain a competitive advantage, while those dependent on traditional immunoassays face operational limitations. The adoption of ISO 16140-2 validation standards for alternative testing methods ensures consistency and reliability across global supply chains, but also raises entry barriers for new analytical technologies [3]Source: Royal Society of Chemistry, "Advancements in Food Quality monitoring: integrating biosensors for precision detection", rsc.org . This regulatory-driven transformation is reshaping the competitive dynamics of allergen testing, encouraging investments in high-precision instrumentation and validated methodologies.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of testing technologies | -1.3% | Global, acute in South America and Middle East and Africa SMEs | Short term (≤ 2 years) |

| Complexity of multi-allergen testing | -0.8% | Global, multi-product plants | Medium term (2-4 years) |

| Limited shelf-life of rapid test kits | -0.6% | Asia-Pacific the Middle East and Africa with long supply chains | Short term (≤ 2 years) |

| Lack of harmonized global methods | -0.7% | Trade interfaces between regulatory zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of testing technologies

The substantial capital requirements for advanced allergen testing platforms pose significant entry barriers, particularly for small and medium-sized food manufacturers, which represent the majority of global food production capacity. Confirmatory allergen analysis using LC-MS/MS systems demands an initial investment exceeding USD 500,000, with annual maintenance and consumable costs amounting to approximately USD 100,000 per instrument. Beyond equipment expenses, additional costs include specialized personnel training, method validation, and regulatory compliance documentation, collectively surpassing USD 1 million for comprehensive allergen testing capabilities. This cost structure has led to a segmented market, where large multinational corporations operate in-house testing facilities. At the same time, smaller manufacturers rely on contract testing services, potentially causing delays during periods of high demand. The financial barrier is particularly pronounced in emerging markets, where local laboratories often lack the resources to acquire advanced analytical platforms, resulting in reliance on international testing providers and extended turnaround times for safety assessments.

Complexity of multi-allergen testing

The simultaneous detection of multiple allergens in complex food matrices presents significant technical challenges, limiting market growth and testing efficiency within the industry. Cross-reactivity among allergen proteins can lead to false-positive results. At the same time, matrix interference from food components may suppress analytical signals, resulting in false-negative outcomes that undermine food safety assurance. Regulatory authorities mandate separate validation documentation for each allergen-matrix combination, adding considerable complexity as food manufacturers diversify their product portfolios across various allergen categories. Additionally, processing-induced protein modifications can affect allergen detectability, necessitating specialized extraction methods and analytical techniques, which increase both costs and analytical uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PCR-Based Methods Drive Innovation

In 2025, immunoassay-based techniques are expected to dominate the market, accounting for 58.17% of the share due to their reliability, cost-effectiveness, and broad compliance with international food safety standards. PCR-based approaches are projected to grow at a CAGR of 7.38% through 2031, driven by their high specificity and ability to detect multiple allergens simultaneously. Mass spectrometry is increasingly utilized for confirmatory testing, particularly in processed foods where protein modifications can affect the accuracy of immunoassays. Spectroscopy and imaging tools are mainly used for rapid screening, while nanobiosensor platforms are advancing on-site testing through smartphone integration and AI-driven analysis.

The market is shifting toward hybrid systems that integrate multiple detection methods to address technical limitations while maintaining cost efficiency for routine testing. Advanced biosensors employing gold nanoparticles and graphene-based transducers are achieving femtomolar-level sensitivity, surpassing the performance of traditional ELISA methods and enabling the detection of trace allergens that were previously undetectable. However, regulatory approval remains a significant challenge, as compliance with ISO 16140-2 requires extensive validation studies, often delaying market entry by 2–3 years.

By Application: Seafood and Meat Products Accelerate

In 2025, bakery and confectionery products are expected to dominate the allergen testing market, holding a 26.09% share. These products frequently contain multiple allergenic ingredients, such as wheat, eggs, milk, nuts, and soy. The production processes for these items present significant challenges for allergen management due to shared equipment, airborne flour contamination, and complex supply chains, which increase the risk of cross-contact. The seafood and meat segment is projected to grow at the fastest rate, with a CAGR of 9.56%, driven by the expansion of global trade in processed proteins and stricter regulatory oversight on undeclared allergens. Dairy products require extensive testing due to the high prevalence of lactose intolerance and the widespread use of milk-based ingredients in various food categories. The beverage industry is also experiencing increased testing requirements as protein additives and botanical extracts, some of which may contain allergens, are increasingly incorporated into products.

Baby food and infant formula undergo particularly stringent testing, surpassing standard food safety requirements. Regulatory authorities mandate higher analytical sensitivity and more frequent testing to ensure the safety of infants. Alternative protein sources present additional challenges, as plant-based, insect-derived, and fermentation-produced proteins may cross-react with traditional allergens or introduce novel allergenic proteins for which testing protocols are not yet established. This diverse application landscape is driving demand for adaptable analytical platforms that enable rapid method development and validation for emerging food categories, without necessitating entirely new systems.

Geography Analysis

In 2025, Europe leads the allergen testing market with a 34.47% share, driven by robust regulatory frameworks and a well-established testing infrastructure across government laboratories and private service providers. Continuous updates from the European Food Safety Authority on allergen assessment, coupled with stringent cross-contact prevention standards set by the Dutch Food and Consumer Product Safety Authority, highlight the region's strict regulatory environment. These factors sustain consistent demand for allergen testing in the region. North America operates under established FDA and USDA frameworks, with market growth primarily fueled by technological innovations rather than regulatory changes. The region benefits from advanced testing infrastructure and protocols, focusing on integrating emerging allergen detection technologies to enhance efficiency and optimization. This approach emphasizes technological progress over fundamental regulatory reform.

The Asia-Pacific region is the fastest-growing allergen testing market, with a projected CAGR of 8.98% through 2031. Growth is supported by evolving food safety regulations in China and India as they align with international standards to enhance food export capabilities. Additionally, the rising prevalence of food allergies in Japan drives demand, while South Korea and Australia serve as key testing hubs for multinational food companies operating in the region. South America, along with the Middle East and Africa, presents emerging growth opportunities due to developing regulatory systems and export-driven compliance requirements. However, market growth in these regions is limited by insufficient local analytical capacity and reliance on international testing services.

The global allergen testing market demonstrates a clear correlation between regulatory maturity and testing adoption. Regions with stronger regulatory frameworks invest in analytical capabilities to ensure food safety and enhance competitiveness in global trade. Meanwhile, emerging markets are progressively building their testing infrastructure to align with international standards, fostering long-term growth potential. Despite challenges in developing regions, increasing awareness of international food safety standards is driving gradual improvements in testing infrastructure, supporting the overall expansion of the allergen testing market.

Competitive Landscape

The food allergen testing market is moderately fragmented, with a few key players maintaining a strong presence. Prominent companies such as Eurofins Scientific, SGS, and Intertek lead the market through extensive global laboratory networks and diverse service offerings. Their competitive advantage is further strengthened by advancements in AI-driven analytics and rapid testing platforms. Competition in the market increasingly centers on regulatory compliance, with companies achieving ISO 17025 accreditation and validating methods to meet international standards.

Emerging markets present significant growth opportunities, as local testing capabilities often fail to meet regulatory requirements, driving demand for international laboratory services and technology partnerships. Traditional laboratory-based testing is facing growing competition from innovative technologies such as nanobiosensors and smartphone-enabled analytical tools, which offer point-of-use testing solutions. The adoption of these technologies challenges conventional centralized testing models, encouraging companies to develop alternatives that bypass standard laboratory infrastructure.

Market dynamics are also shaped by the importance of comprehensive service offerings and technological differentiation, as companies strive to gain market share from regional providers. Smaller niche players focus on specialized areas, such as alternative protein testing and the detection of emerging allergens, addressing specific needs that larger firms may not prioritize. These smaller companies benefit from their agility, enabling them to respond quickly to new demands. Regulatory validation requirements play a critical role in shaping the competitive landscape, creating barriers to entry for new technologies while solidifying the position of established companies with proven methodologies and extensive documentation. Overall, the regulatory framework continues to influence market structure and competitive dynamics across the industry.

Food Allergen Testing Industry Leaders

-

SGS S.A.

-

Intertek Group PLC

-

Eurofins Scientific SE

-

Bureau Veritas S.A.

-

Microbac Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: SGS North America (SGS) has announced the expansion of its food safety and quality assurance testing capabilities for the North American food and nutraceutical markets. This expansion includes relocating to a larger facility in Fairfield, New Jersey, to better meet client requirements. The services provided encompass rapid and traditional food pathogen testing using DNA and protein-based detection methods, food hygiene and quality indicator testing, as well as environmental monitoring in food production, including pathogen and indicator testing.

- March 2024: Gold Standard Diagnostics has introduced the first product in its new allergen PowerLine test series: the SENSIStrip Gluten PowerLine Lateral Flow Device. This product features a sensitive detection system based on a monoclonal antibody, enabling the detection of gluten residues in food matrices, rinse water, and swabs.

- March 2024: ALS has strategically expanded its presence in the European and U.S. Life Sciences markets. The company has acquired York Analytical Laboratories, based in the Northeastern United States, and Wessling Holding GmbH & Co., based in Western Europe.

Global Food Allergen Testing Market Report Scope

A food allergen is a specific substance, typically a protein, present in certain foods that can trigger an abnormal immune response in some individuals. Food allergen testing involves identifying and quantifying the presence of specific allergens in food products.

The food allergen testing market is segmented into technology, application, and geography. Based on technology, the market is segmented into immunoassay-based /ELISA, PCR, and other technologies. Based on application, the market is segmented into bakery and confectionery products, baby food and infant formula, seafood and meat products, dairy products, beverages, and other applications. Based on geography, the global food allergen testing market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.

For each segment, the market sizing and forecasts have been done based on value (in USD).

By Technology

| Immunoassay-Based |

| Polymerase Chain Reaction-Based |

| Mass-Spectrometry-Based |

| Spectroscopy and Imaging |

| Others |

By Application

| Bakery and Confectionery |

| Dairy Products |

| Seafood and Meat Products |

| Beverages |

| Baby Food and Infant Formula |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Immunoassay-Based | |

| Polymerase Chain Reaction-Based | ||

| Mass-Spectrometry-Based | ||

| Spectroscopy and Imaging | ||

| Others | ||

| By Application | Bakery and Confectionery | |

| Dairy Products | ||

| Seafood and Meat Products | ||

| Beverages | ||

| Baby Food and Infant Formula | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the food allergen testing market be by 2031?

It is projected to reach USD 1.89 billion by 2031, growing at a 6.96% CAGR from 2026 to 2031.

Which technology is expanding fastest in allergen detection?

PCR methods are advancing at a 7.38% CAGR because retailers and auditors now require DNA-level confirmation.

Why is Asia-Pacific the fastest-growing region?

Accelerating processed-food exports and adoption of EU-style labeling rules are driving an 8.98% regional CAGR.

What drives the high testing intensity in infant formula?

EU rules mandate allergen screening on every production batch, pushing manufacturers toward rapid PCR assays for sub-ppm limits.

Page last updated on: