Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

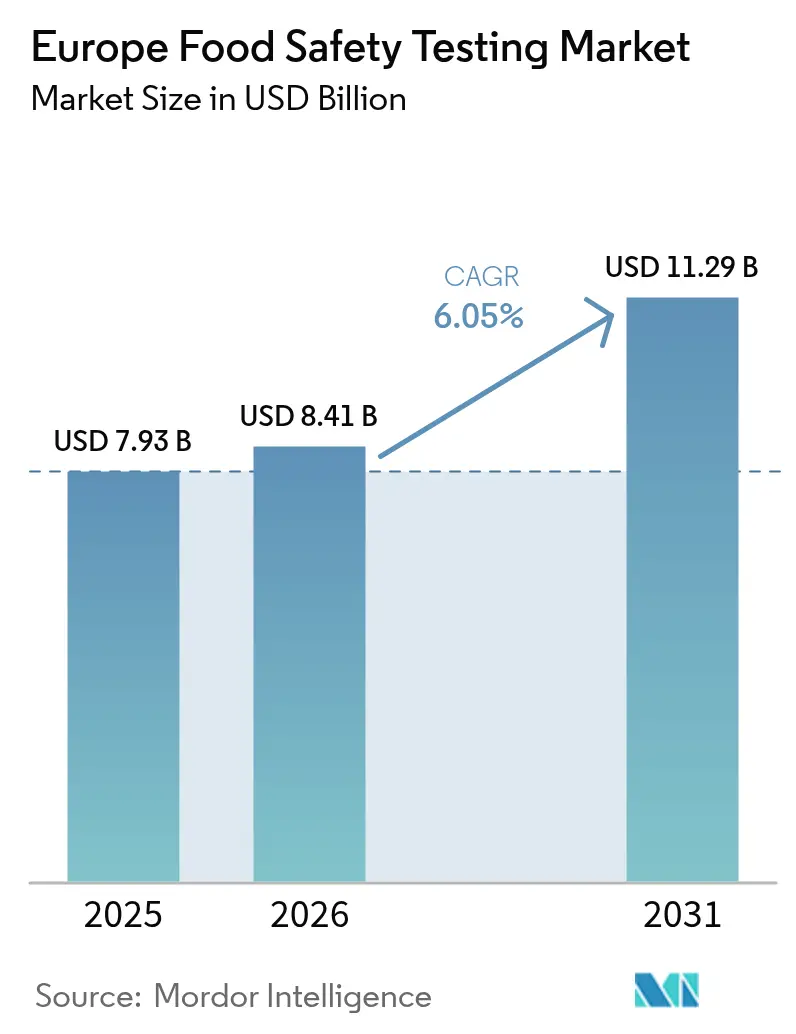

| Base Year Market Size (2025) | USD 7.93 Billion |

| Market Size (2026) | USD 8.41 Billion |

| Market Size (2031) | USD 11.29 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Food Safety Testing Market Analysis by Mordor Intelligence

Europe food safety testing market size in 2026 is estimated at USD 8.41 billion, growing from 2025 value of USD 7.93 billion with 2031 projections showing USD 11.29 billion, growing at 6.05% CAGR over 2026-2031. This growth trajectory reflects the region's heightened focus on food safety compliance amid escalating foodborne illness incidents and evolving regulatory frameworks. The market's expansion is underpinned by technological advancements in rapid testing methods and increasing consumer demand for transparency in food labeling and authenticity verification. Momentum is powered by stricter enforcement of food‐safety rules, continued innovation in rapid methods, and rising public demand for transparent labeling and authenticity checks. Heightened surveillance programs, high‐profile pathogen outbreaks, and the spread of premium organic and allergen-free foods further expand analytical workloads across the region. Laboratories that deploy high-throughput automation and molecular diagnostics capture share as manufacturers seek quicker turnaround times. Consolidation among independent players and strategic technology alliances signal sustained investment in specialized capabilities and geographic coverage.

Key Report Takeaways

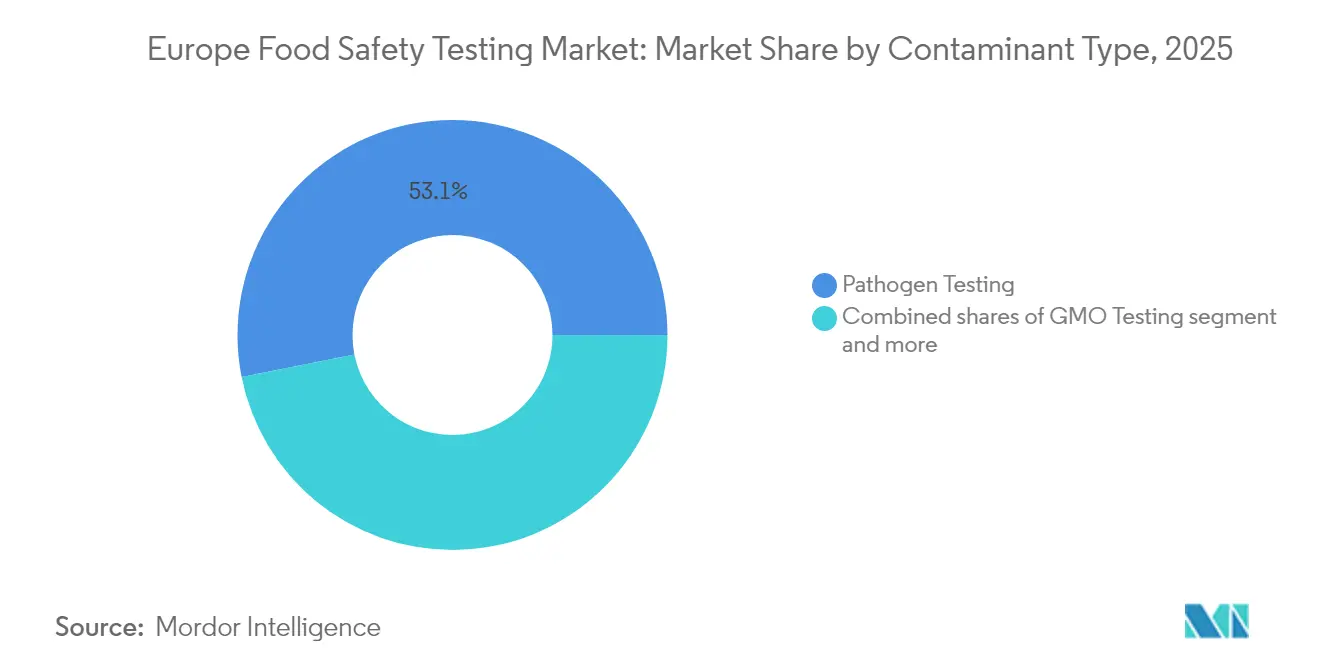

- By contaminant type, pathogen testing held 53.12% of the Europe food testing market share in 2025, while GMO testing is projected to post the fastest 6.56% CAGR to 2031.

- By technology, PCR commanded 48.85% share of the Europe food testing market size in 2025; chromatography and spectrometry are expected to register the highest 7.01% CAGR through 2031.

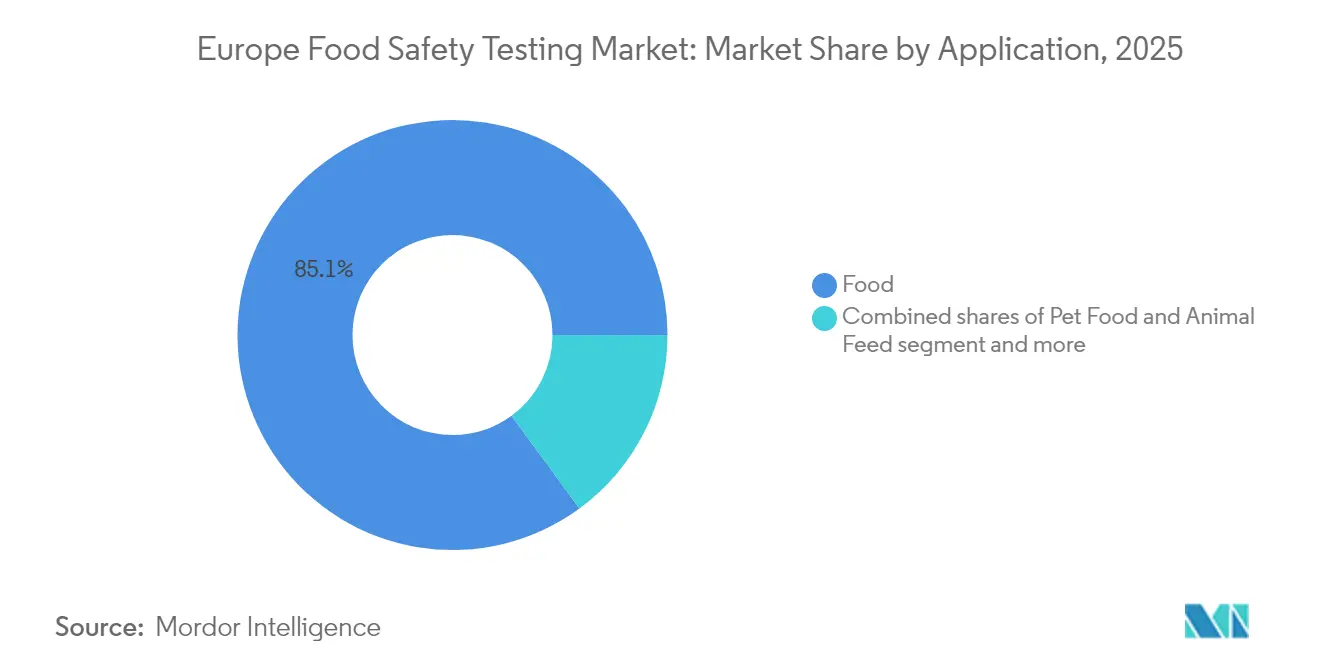

- By application, food accounted for 85.05% of the Europe food testing market size in 2025, whereas pet food and animal feed are forecast to expand at an 7.92% CAGR between 2026-2031.

- By geography, Germany led with 22.40% revenue share of the Europe food testing market in 2025 and is set to grow at a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Food Safety Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Foodborne Illness Incidence and Outbreaks | +1.2% | Germany, United Kingdom, France core markets | Short term (≤ 2 years) |

| Advancements in Testing Technologies and Rapid Methods | +0.8% | Global, with early adoption in Germany, Netherlands | Medium term (2-4 years) |

| Growing Consumer Awareness and Demand for Transparency and Label Accuracy | +0.6% | Western Europe, spillover to Eastern Europe | Medium term (2-4 years) |

| Demand for Organic, Pesticide-free, Allergen-free Products | +0.5% | Germany, France, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Focus on Allergen and Mycotoxin Testing Needs | +0.3% | EU-wide, with concentration in food manufacturing hubs | Medium term (2-4 years) |

| Food Adulteration and Authenticity Concerns | +0.2% | Southern Europe, cross-border trade corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Foodborne Illness Incidence and Outbreaks

The surge in foodborne illness cases across Europe has created unprecedented demand for comprehensive pathogen testing services. UK Health Security Agency data reveals Salmonella cases reached a decade high of 10,388 cases in 2024, representing a 17.1% increase from 2023 levels. The multi-country Salmonella Mbandaka outbreak linked to pre-cooked frozen chicken demonstrated the critical role of whole-genome sequencing in cross-border outbreak investigation, driving adoption of molecular diagnostic capabilities across European testing laboratories. This trend particularly benefits laboratories with advanced WGS infrastructure and rapid turnaround capabilities, as regulatory authorities increasingly rely on molecular epidemiology for source attribution and control measures. The emphasis on ready-to-eat product testing has intensified following multiple contamination events, creating sustained demand for specialized microbiological testing protocols.

Advancements In Testing Technologies and Rapid Methods

Laboratory automation and rapid analytical methods are transforming European food testing operations, driven by workforce shortages and demand for faster turnaround times. The integration of robotics-based solutions, NMR automation, and AI-enabled data analysis is enabling laboratories to increase throughput while reducing manual handling errors. Near-infrared spectroscopy (NIR) and laser-induced breakdown spectroscopy (LIBS) are gaining regulatory acceptance as sustainable alternatives to traditional wet chemistry methods, eliminating solvent usage and reducing environmental footprint. However, regulatory acceptance remains constrained, particularly in Germany, where normative methods still dominate official controls. The development of portable mass spectrometry and handheld spectroscopy devices is creating new market opportunities for on-site testing, though validation and standardization challenges persist. These technological advances are particularly relevant for ISO 17025 accredited laboratories seeking to maintain competitive advantage through operational efficiency.

Growing Consumer Awareness and Demand for Transparency and Label Accuracy

European consumers increasingly demand verifiable information about food origin, processing methods, and ingredient authenticity, driving growth in analytical testing services beyond basic safety parameters. The implementation of blockchain-based traceability solutions, such as Intertek's HoneyTrace system for honey authentication, reflects the market's evolution toward comprehensive supply chain transparency. This trend is particularly pronounced in premium and organic food segments, where consumers pay significant price premiums for verified authenticity claims. The convergence of analytical testing with digital verification technologies creates opportunities for integrated service offerings that combine laboratory analysis with tamper-proof documentation systems. Regulatory frameworks supporting this trend include EU requirements for origin labeling and the growing emphasis on sustainability claims verification, which require sophisticated analytical capabilities to substantiate marketing assertions.

Demand For Organic, Pesticide-free, Allergen-free Products

The European organic food market's continued expansion drives specialized testing requirements for pesticide residue analysis, mycotoxin screening, and authenticity verification. EFSA's 2023 pesticide residue monitoring report documented comprehensive testing across 88,141 food samples, revealing the scale of analytical requirements for regulatory compliance [1]Source: EFSA (European Food Safety Authority), "EFSA's 2023 pesticide residue monitoring", efsa.europa.eu. Climate change impacts on mycotoxin prevalence, particularly in grain crops, necessitate enhanced monitoring capabilities and more frequent testing protocols. The development of optimized ELISA methods and co-occurrence studies for multiple mycotoxin detection reflects the industry's adaptation to emerging contamination patterns. Allergen testing requirements continue expanding as food manufacturers reformulate products to address diverse dietary restrictions, creating sustained demand for cross-contamination monitoring and label verification services. These trends particularly benefit laboratories with specialized capabilities in trace-level detection and method validation for novel food matrices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Costs of Advanced Testing Equipment and Methods | -0.7% | Smaller laboratories across Europe, Eastern Europe focus | Short term (≤ 2 years) |

| Complex Regulatory Heterogeneity Across Countries | -0.4% | Cross-border operations, multi-country suppliers | Medium term (2-4 years) |

| Sample Contamination and Handling Issues in Testing Chain | -0.3% | All European markets, supply chain dependent | Short term (≤ 2 years) |

| Data Security, Privacy, and Traceability Infrastructure Gaps | -0.2% | Digital transformation laggards, smaller operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs of Advanced Testing Equipment and Methods

The substantial capital requirements for state-of-the-art analytical instrumentation create barriers for smaller testing laboratories seeking to expand service capabilities. Advanced mass spectrometry systems, automated sample preparation equipment, and molecular diagnostic platforms require investments often exceeding USD 500,000 per instrument, constraining market entry for regional players. This cost structure favors larger, established laboratories with sufficient scale to justify equipment investments and maintain utilization rates. The ongoing shift toward more sophisticated testing methods, including untargeted screening approaches and multi-residue analysis, further escalates operational costs through specialized consumables and highly trained personnel requirements. Smaller laboratories increasingly rely on outsourcing arrangements or consolidation strategies to access advanced analytical capabilities, contributing to market concentration trends.

Complex Regulatory Heterogeneity Across Countries

Despite EU harmonization efforts, significant regulatory variations persist across European markets, creating compliance complexity for multinational food companies and testing service providers. Differences in sampling protocols, analytical methods, and reporting requirements necessitate jurisdiction-specific expertise and multiple accreditations. The challenge is particularly acute for emerging contaminants and novel testing technologies, where regulatory acceptance timelines vary significantly between member states. Brexit has further complicated regulatory alignment, requiring separate validation and approval processes for UK market access. These regulatory inconsistencies increase operational costs for testing laboratories serving multiple European markets and create barriers for smaller players lacking resources to navigate diverse compliance requirements across jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Contaminant Type: Pathogen Testing Dominates Safety Priorities

Advanced molecular diagnostic methods are revolutionizing pathogen detection capabilities across European food testing laboratories, with Pathogen Testing commanding 53.12% market share in 2025. The segment's dominance reflects the critical importance of microbiological safety in preventing foodborne illness outbreaks, particularly following high-profile incidents like the multi-country Salmonella Mbandaka outbreak that highlighted the need for rapid, accurate pathogen identification European Centre for Disease Prevention and Control. GMO Testing emerges as the fastest-growing segment at 6.56% CAGR (2026-2031), driven by evolving EU regulations on New Genomic Techniques and increasing consumer scrutiny of bioengineered ingredients.

Pesticide and Residue Testing maintains significant market presence, supported by EFSA's comprehensive monitoring programs that analyzed 88,141 food samples in 2023, demonstrating the scale of regulatory requirements. Mycotoxin Testing gains importance due to climate change impacts on crop contamination patterns, while Allergen Testing expands alongside growing dietary restriction awareness and cross-contamination prevention requirements. Other Contaminant Testing, including heavy metals and process contaminants, addresses emerging regulatory concerns such as PFAS limits and acrylamide monitoring. The segment's evolution toward multi-analyte screening platforms reflects laboratories' efforts to improve efficiency while meeting diverse analytical requirements across food categories.

By Technology: PCR Leadership Challenged by Chromatography Advances

Polymerase Chain Reaction technology maintains market leadership with 48.85% share in 2025, reflecting its versatility in pathogen detection, GMO identification, and species authentication applications. However, Chromatography and Spectrometry demonstrates the highest growth potential at 7.01% CAGR (2026-2031), driven by advances in ultra-high-performance liquid chromatography coupled with high-resolution mass spectrometry for contaminant screening. The technology's ability to perform untargeted analysis and identify unknown compounds positions it as essential for emerging contaminant detection and food fraud investigation.

Immunoassay-based methods retain importance for rapid screening applications, particularly in field testing scenarios where immediate results are required. The technology benefits from continuous improvements in antibody specificity and assay sensitivity, enabling detection of trace-level contaminants in complex food matrices. Other technologies, including biosensors and spectroscopic methods, are gaining traction through portable device development and on-site testing capabilities. The integration of artificial intelligence and machine learning algorithms across all technology platforms enhances data interpretation capabilities and enables predictive analytics for food safety risk assessment. Regulatory frameworks such as ISO 17025 continue influencing technology adoption patterns by establishing validation requirements for analytical methods.

By Application: Food Segment Dominance with Pet Food Growth

The Food application segment's commanding 85.05% market share in 2025 reflects the vast scale of human food production and consumption across Europe, encompassing diverse categories from fresh produce to processed foods. Within this segment, Meat and Poultry testing drives significant demand due to pathogen risks and regulatory requirements, while Dairy testing focuses on adulterant detection and quality parameters. Fruits and Vegetables testing emphasizes pesticide residue analysis and pathogen screening, particularly for ready-to-eat products that have been implicated in recent outbreak investigations.

Pet Food and Animal Feed emerges as the fastest-growing application at 7.92% CAGR (2026-2031), driven by premiumization trends and regulatory alignment with human food safety standards. The segment benefits from increasing pet ownership rates and consumer willingness to pay premium prices for verified nutrition and safety claims. Processed Food testing addresses complex analytical challenges related to multi-ingredient formulations and novel processing technologies. Crops testing supports agricultural supply chain integrity through mycotoxin monitoring and authenticity verification. The application diversity creates opportunities for specialized testing laboratories to develop niche expertise while larger players benefit from comprehensive service portfolios across all food categories.

Geography Analysis

Germany leads the European food testing market with 22.40% share in 2025 and demonstrates the strongest growth trajectory at 7.18% CAGR (2026-2031), reflecting the country's robust food manufacturing sector and stringent regulatory enforcement. The German Federal Office of Consumer Protection and Food Safety (BVL) reported comprehensive surveillance activities, including extensive Salmonella testing in livestock that revealed significant contamination rates requiring enhanced monitoring protocols. The country's leadership in analytical instrumentation manufacturing and research creates synergies between technology development and testing service capabilities. Major testing companies maintain significant operations in Germany, with SGS Institut Fresenius operating multiple accredited laboratories across Berlin, Hamburg, Taunusstein, and other key locations. The market benefits from strong automotive and chemical industries that drive demand for specialized analytical capabilities applicable to food testing applications.

France represents a significant market driven by its extensive agricultural production and food processing industries, with regulatory oversight from ANSES (French Agency for Food, Environmental and Occupational Health and Safety). Recent regulatory developments include new plant protein labeling requirements and livestock sovereignty initiatives that create additional testing requirements for authenticity verification and nutritional analysis . The United Kingdom maintains substantial testing demand despite Brexit-related regulatory changes, with the Food Standards Agency continuing to drive safety requirements while developing independent regulatory frameworks. The UK's focus on environmental health officer capacity building reflects ongoing challenges in maintaining adequate inspection and testing capabilities.

Italy, Spain, Netherlands, Poland, Belgium, and Sweden collectively represent significant market opportunities, each with distinct regulatory requirements and industry focus areas. The Netherlands demonstrates strength in agricultural innovation and sustainable food production, creating demand for specialized testing services related to organic certification and environmental impact assessment. Poland's growing food processing sector and EU integration drive increasing testing requirements, while Nordic countries emphasize sustainability and quality parameters. The Rest of Europe category encompasses emerging markets in Eastern Europe where EU accession processes and harmonization requirements create growth opportunities for testing service providers. Regional variations in regulatory enforcement and industry development create diverse market dynamics, with opportunities for both specialized niche players and comprehensive service providers across the European landscape.

Competitive Landscape

The European food testing market exhibits moderate concentration with established global players competing alongside specialized regional laboratories and emerging technology providers. Market leaders leverage comprehensive service portfolios, extensive geographic coverage, and advanced analytical capabilities to serve multinational food companies requiring standardized testing protocols across multiple jurisdictions. Major players include TÜV SÜD, Eurofins Scientific, SGS Société Générale de Surveillance SA, Mérieux NutriSciences, and Intertek Group plc, among others.

Strategic consolidation continues reshaping competitive dynamics, exemplified by Mérieux NutriSciences' EUR 360 million acquisition of Bureau Veritas' food testing operations, which demonstrates the premium valuations commanded by specialized testing capabilities and established client relationships. Technology differentiation increasingly drives competitive positioning, with leaders investing in automation, rapid testing methods, and digital integration capabilities to improve turnaround times and operational efficiency. Intertek's development of blockchain-based traceability solutions and SGS's expansion of molecular diagnostic capabilities reflect the industry's evolution toward comprehensive quality assurance services beyond traditional analytical testing.

Emerging opportunities exist in portable testing technologies, AI-enabled data analysis, and integrated supply chain monitoring solutions that address growing demand for real-time quality assurance and transparency. Regulatory compliance requirements, particularly ISO 17025 accreditation and method validation protocols, create barriers to entry while favoring established players with proven quality management systems and technical expertise [3]Source: U.S Department of Agriculture, "Key Facts: ISO Accreditation", fsis.usda.gov. The market's fragmented nature in specialized testing niches allows smaller players to compete effectively through technical expertise and customer service excellence in specific geographic regions or analytical domains.

Europe Food Safety Testing Industry Leaders

-

TÜV SÜD

-

Eurofins Scientific

-

SGS Société Générale de Surveillance SA

-

Mérieux NutriSciences

-

Intertek Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vienna-based ViruSure, a pathogen safety testing company for biopharmaceuticals, launched a new viral contamination detection test. The first of its kind, the test uses Oxford Nanopore technology for rapid, sensitive, and affordable viral screening during manufacturing.

- July 2025: Sysmex Europe SE partnered with SMD GmbH to distribute geneLEAD VIII Platform and SMD lead kits for advanced pathogen detection. The geneLEAD VIII platform and compatible SMD lead kits were distributed in France, Germany, Austria, and Switzerland as a part of the Sysmex Life Science portfolio.

- January 2025: The UK Health Security Agency (UKHSA) launched the metagenomics Surveillance Collaboration and Analysis Programme (mSCAPE). This is described as the world's first biosecurity surveillance system using metagenomic data for national pathogen monitoring. It analyzes anonymized data from UK labs to track outbreaks, monitor for treatment resistance, and detect previously unknown pathogens.

Europe Food Safety Testing Market Report Scope

Food testing plays a crucial role in ensuring food safety and consumer health. This involves supporting a network of food testing laboratories, maintaining high standards in food testing, investing in skilled personnel, conducting surveillance activities, and educating consumers.

The Europe food safety testing market is segmented by contaminant testing, technology, application, and country. Based on contaminant testing, the market is segmented into pathogen testing, pesticide and residue testing, mycotoxin testing, GMO testing, allergen testing, and other types. By technology, the market is segmented into polymerase chain reaction (PCR), chromatography and spectrometry, immunoassay-based, and other technologies. By application, the market is segmented into pet food and animal feed and food. By food, the market is segmented into meat and poultry, dairy, fruits and vegetables, processed food, crops, and other foods. By country, the market is segmented into the United Kingdom, France, Germany, Spain, Italy, Russia, Poland, Romania, Lithuania, Serbia, and the Rest of Europe. For each segment, the market sizing and forecasting have been done in value terms (USD).

By Contaminant Type

| Pathogen Testing |

| Pesticide and Residue Testing |

| Mycotoxin Testing |

| GMO Testing |

| Allergen Testing |

| Other Contaminant Testing |

By Technology

| Polymerase Chain Reaction |

| Immunoassay-based |

| Chromatography and Spectrometry |

| Others |

By Application

| Pet Food and Animal Feed | |

| Food | Meat and Poultry |

| Dairy | |

| Fruits and Vegetables | |

| Processed Food | |

| Crops | |

| Other Foods |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Contaminant Type | Pathogen Testing | |

| Pesticide and Residue Testing | ||

| Mycotoxin Testing | ||

| GMO Testing | ||

| Allergen Testing | ||

| Other Contaminant Testing | ||

| By Technology | Polymerase Chain Reaction | |

| Immunoassay-based | ||

| Chromatography and Spectrometry | ||

| Others | ||

| By Application | Pet Food and Animal Feed | |

| Food | Meat and Poultry | |

| Dairy | ||

| Fruits and Vegetables | ||

| Processed Food | ||

| Crops | ||

| Other Foods | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the European food testing segment today and how fast is it growing?

The segment is valued at USD 8.41 billion in 2026 and is forecast to advance at a 6.05% CAGR to USD 11.29 billion by 2031.

Which contaminant category sees the highest testing demand across Europe?

Pathogen testing commands 53.12% share, reflecting regulators’ priority on preventing Salmonella, Listeria, and Campylobacter outbreaks.

What technology platforms are laboratories adopting most for food safety analysis?

PCR retains 48.85% share for its versatility, while chromatography and spectrometry are the fastest‐growing at a 7.01% CAGR thanks to ultra-high-performance LC-HRMS upgrades.

Why is Germany the key geography for food testing service providers?

Germany controls 22.40% of regional revenue and is projected to grow at a 7.18% CAGR, supported by stringent enforcement and a dense network of accredited labs.

Page last updated on: