Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

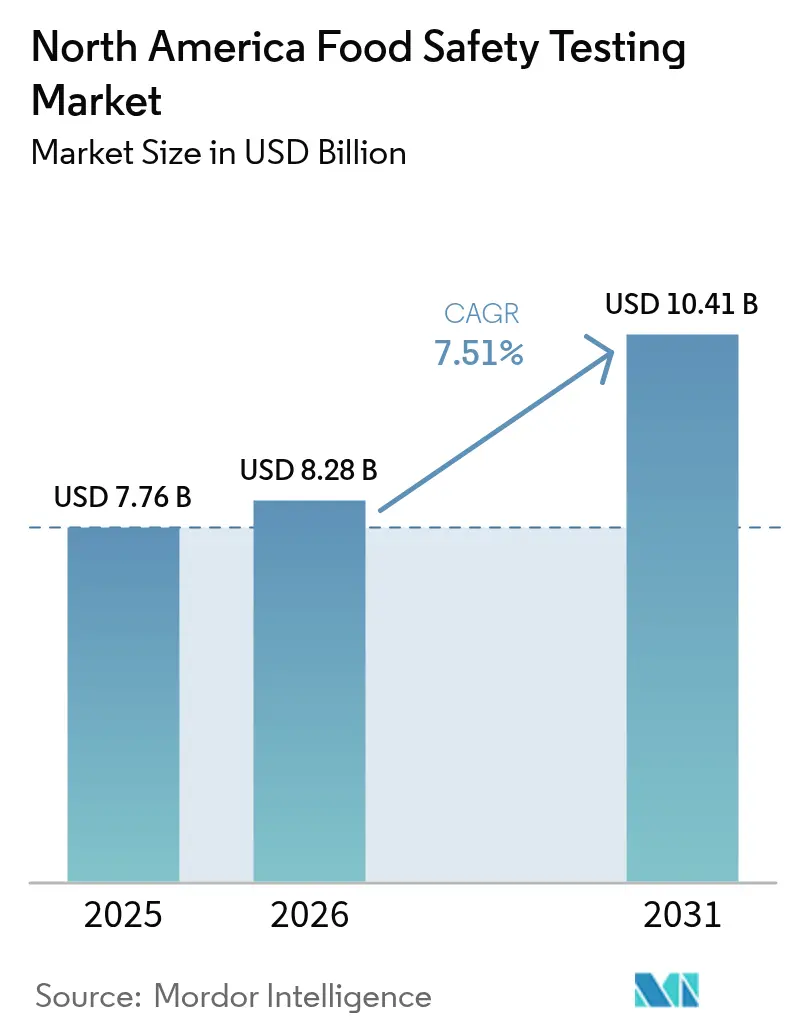

| Base Year Market Size (2025) | USD 7.76 Billion |

| Market Size (2026) | USD 8.28 Billion |

| Market Size (2031) | USD 10.41 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

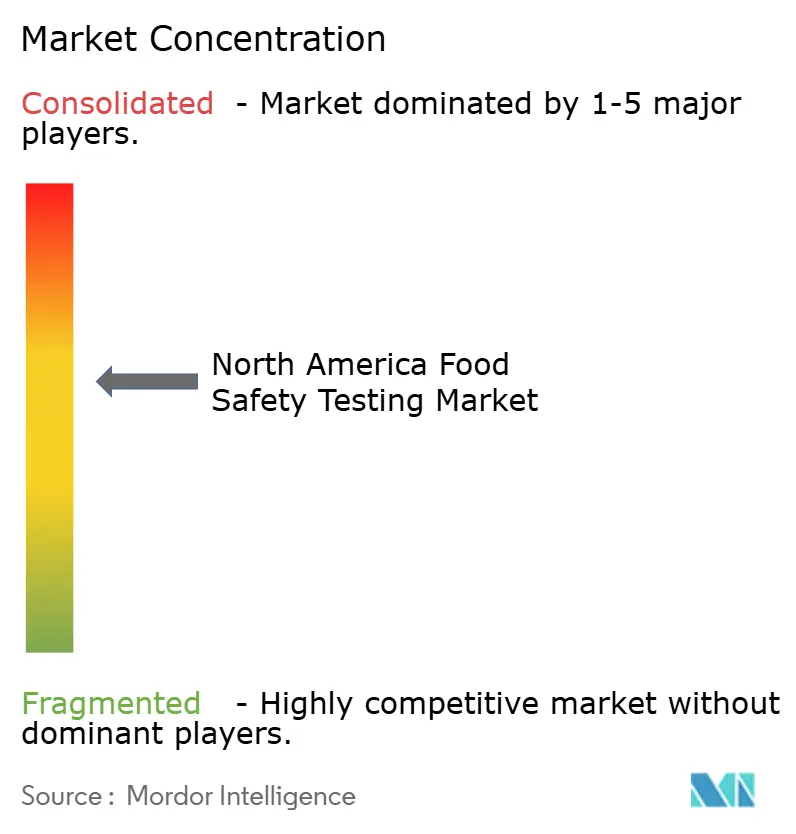

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Food Safety Testing Market Analysis by Mordor Intelligence

The North America food safety testing market size is projected to expand from USD 7.76 billion in 2025 and USD 8.28 billion in 2026 to USD 10.41 billion by 2031, registering a CAGR of 7.51% between 2026 and 2031. Regulators continue to tighten preventive-control, sampling, and traceability rules, prompting manufacturers to embed routine microbiological, chemical, and authenticity testing directly into production workflows rather than relying on finished-product sampling. Adoption of real-time polymerase chain reaction (PCR) systems, whole-genome sequencing, and high-resolution mass spectrometry is escalating as retailers demand same-day certificates of analysis before releasing shipments. Meanwhile, blockchain pilots in large retail chains compress outbreak investigations from weeks to hours, reinforcing the business case for rapid, high-throughput testing capacity. Labor shortages persist across accredited laboratories, extending turnaround times in rural catchments and driving automation investments that favor larger market participants.

Key Report Takeaways

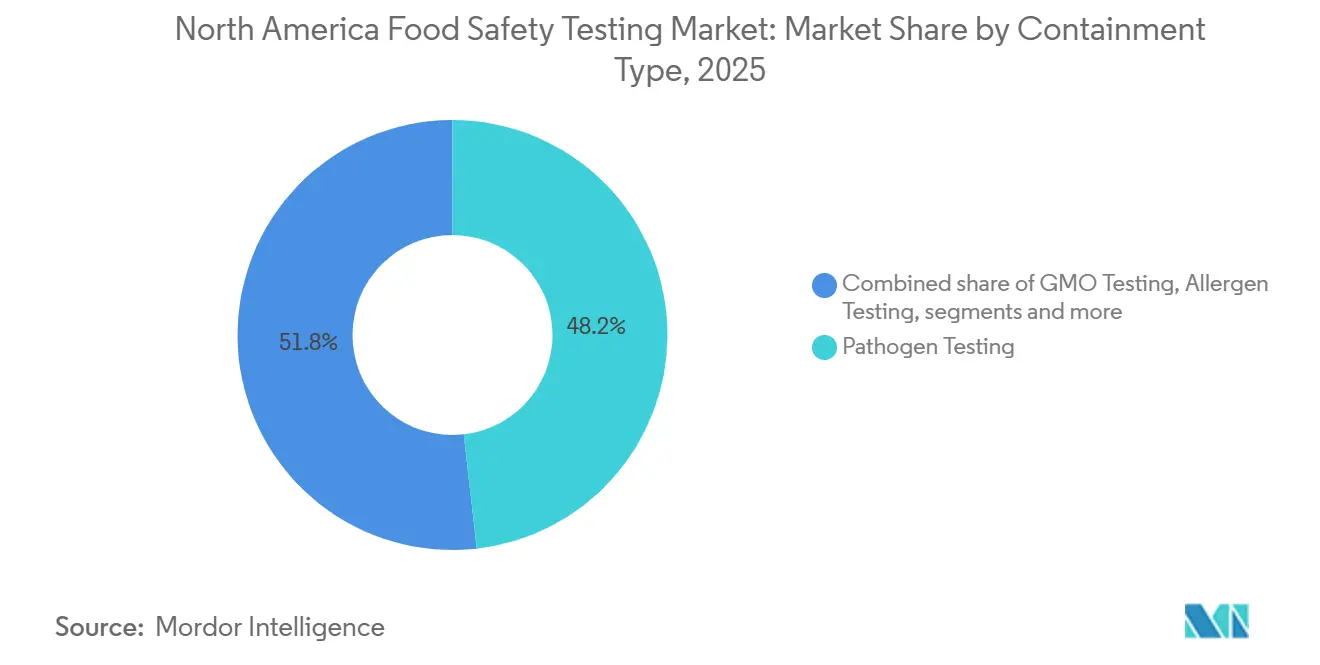

- By containment type, pathogen testing led with 48.21% of the North America food safety testing market share in 2025, while GMO testing recorded the fastest projected CAGR at 8.25% through 2031.

- By technology, PCR platforms held a 45.32% revenue share in 2025, while chromatography and spectrometry recorded the fastest projected CAGR at 9.05% through 2031.

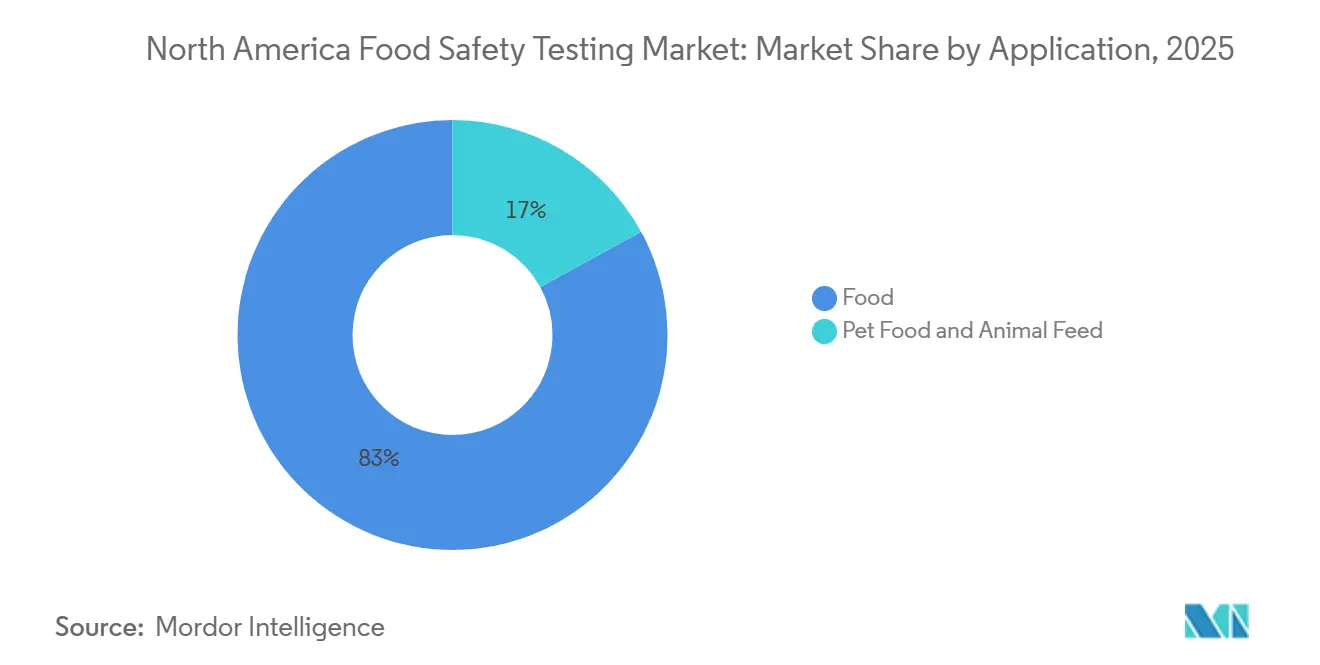

- By application, Food ed with 48.21% of the North America food safety testing market share in 2025, while pet food and animal feed testing is forecast to expand at an 8.11% CAGR between 2026-2031.

- By geography, the United States commanded 75.11% of regional revenue in 2025, while Mexico exhibits the strongest growth trajectory at an 8.28% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Food Safety Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand For Stringent Food Safety Compliance | +1.5% | Global, with strongest enforcement in United States and Canada | Medium term (2-4 years) |

| Rising Frequency Of Foodborne Illness Outbreaks | +1.2% | United States and Canada, with spillover to Mexico | Short term (≤ 2 years) |

| Widespread Adoption Of Blockchain For Supply Chain Traceability | +0.8% | United States retail and distribution networks, early pilots in Canada | Long term (≥ 4 years) |

| Heightened Focus On Food Allergen Detection And Prevalence | +1.0% | United States and Canada, driven by FASTER Act and SFCR | Medium term (2-4 years) |

| Escalating Cases Of Adulteration And Toxicity In Processed Goods | +0.9% | North America-wide, with concentrated enforcement in United States | Short term (≤ 2 years) |

| Growing Need For Extended Shelf Life And Fewer Product Recalls | +1.1% | United States and Canada, affecting all food categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand For Stringent Food Safety Compliance

Under the FDA's Food Safety Modernization Act, manufacturers are required to integrate routine microbiological and chemical testing into their production processes. This strategy emphasizes preventive controls, hazard-analysis plans, and enhanced traceability for high-risk foods, moving away from the traditional reliance on end-product sampling. Similarly, USDA-FSIS's FY2025 sampling plan intends to collect approximately 88,031 microbiological samples and 12,400 chemical-residue samples[1]Source: U.S. Department of Agriculture, “Sampling Programs and Results,” usda.gov. This extensive effort highlights the agency's shift toward data-driven risk assessments and the use of whole-genome sequencing to trace outbreak sources. In Canada, the Safe Food for Canadians Regulations mandate that all licensed food businesses implement preventive-control plans and maintain traceability records. This alignment with U.S. standards aims to streamline processes and facilitate cross-border trade. The FDA's Food Traceability Rule, with a compliance deadline set for July 2028, allows small processors time to enhance their record-keeping systems. However, many early adopters are already utilizing digital traceability to differentiate their brands and secure premium shelf space. In Mexico, COFEPRIS is modernizing its import-export testing protocols to comply with USMCA commitments. This modernization is driving demand for accredited laboratories capable of issuing certificates recognized by both U.S. and Canadian authorities. Additionally, regulatory requirements are influencing standards such as ISO 17025 accreditation for testing laboratories. Retailers are increasingly relying on certifications from GFSI schemes, including SQF and BRC, as benchmarks for supplier approval.

Rising Frequency Of Foodborne Illness Outbreaks

During 2024 and 2025, the Centers for Disease Control and Prevention monitored 17 to 36 multistate foodborne-illness investigations weekly[2]Source: Centers for Disease Control and Prevention, “Outbreak Investigations,” cdc.gov. Listeria monocytogenes and Salmonella were the leading causes of Class I recalls in ready-to-eat meats, dairy, and produce. A 104-case Salmonella outbreak tied to charcuterie products extended from 2023 into 2024, prompting the USDA-FSIS to enhance Salmonella quantification protocols and expand whole-genome sequencing capabilities for faster contamination source identification. The detection of H5N1 avian influenza in U.S. dairy herds in 2024 initiated a federal testing program that collected over 800 raw-milk samples, highlighting how emerging zoonotic threats can rapidly increase testing demands. Retailers are responding by strengthening supplier requirements and enforcing third-party verification of pathogen-control plans, benefiting accredited laboratories equipped for high-throughput PCR and immunoassay workflows. The cross-border nature of contamination events is evident in Canada’s E. coli O157:H7 outbreak in romaine lettuce and Mexico’s sporadic Cyclospora cases in fresh produce, emphasizing the need for harmonized testing standards and real-time data sharing among North American regulators, including Health Canada. Compliance remains critical, focusing on HACCP principles and routine validation of critical control points through environmental monitoring.

Widespread Adoption Of Blockchain For Supply Chain Traceability

Walmart utilizes IBM Food Trust to power its blockchain-enabled traceability system, requiring leafy-green suppliers to rapidly upload farm-to-store data. This capability reduces outbreak investigation times from weeks to hours, driving the need for faster pathogen screening at packing facilities. The system incorporates IoT sensors that continuously track temperature and humidity, triggering automated alerts when conditions exceed safe thresholds and initiating immediate microbiological testing. While large retailers and branded manufacturers have widely adopted this technology, smaller processors face barriers such as interoperability issues and high upfront costs. However, pilot programs in seafood and organic produce are demonstrating returns on investment through lower recall expenses and increased consumer trust. The FDA's Food Traceability Rule, which requires lot-level tracking for foods listed on the Food Traceability List, aligns with blockchain's detailed data capture and is expected to drive adoption ahead of the July 2028 compliance deadline. In Mexico, export-focused producers are investing in blockchain to meet U.S. retailer requirements, fueling demand for accredited testing laboratories that can issue digital certificates compatible with distributed-ledger platforms. The integration of blockchain with advanced testing technologies, such as whole-genome sequencing, creates a feedback loop where faster contamination source identification supports higher testing frequency.

Heightened Focus On Food Allergen Detection And Prevalence

In 2024 and 2025, allergen mislabeling became the leading cause of Class I recalls. This pattern, which represents a significant portion of USDA and FDA enforcement actions, underscores the economic and reputational risks of inadequate testing. Multiplex immunoassays, which enable the simultaneous detection of multiple allergens in a single run, help reduce costs and turnaround times. However, they require laboratories to invest in automated platforms and maintain validated protocols for each food matrix. Canada's allergen-labeling requirements, aligned with U.S. standards under the Safe Food for Canadians Regulations, have created a unified North American market for allergen-testing services. The growing popularity of plant-based and alternative proteins has introduced new allergen profiles, such as pea protein, lupin, and novel legumes. Furthermore, regulatory initiatives, including the FDA's voluntary allergen-control programs and GFSI certification schemes, emphasize the need for allergen-management plans.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Costs Of Advanced Food Safety Testing Technologies | -0.7% | United States and Canada, affecting small and mid-sized processors | Medium term (2-4 years) |

| Challenges In Detecting Emerging And Novel Contaminants | -0.5% | North America-wide, with regulatory gaps in PFAS and microplastics | Long term (≥ 4 years) |

| Shortage Of Skilled Personnel In Food Safety Laboratories | -0.6% | United States and Canada, concentrated in rural and secondary markets | Short term (≤ 2 years) |

| Prolonged Timelines Of Traditional Testing Methodologies | -0.4% | United States and Canada, affecting USDA-FSIS protocols | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Costs Of Advanced Food Safety Testing Technologies

High-resolution mass spectrometry systems, required for multi-residue pesticide analysis and PFAS quantification, involve capital investments exceeding USD 500,000. This significant expense discourages small and mid-sized processors from performing in-house testing, driving demand primarily toward third-party laboratories [peer-reviewed research]. Laboratories serving rural or secondary markets face challenges due to recurring costs linked to whole-genome sequencing platforms and bioinformatics infrastructure, including cloud storage, software licenses, and the need for skilled personnel. The transition from presumptive to confirmatory testing, mandated by certain USDA-FSIS protocols, increases both turnaround time and costs. As a result, manufacturers either negotiate volume discounts with accredited laboratories or invest in rapid screening technologies to reduce the number of samples requiring confirmatory analysis. In contrast to the U.S., where economies of scale benefit the laboratory market, Canada’s smaller laboratory sector experiences higher per-test costs and longer lead times, particularly for specialized assays like mycotoxin quantification and allergen validation. Mexico’s testing infrastructure remains fragmented, with limited accredited facilities for advanced chromatography and molecular diagnostics. This forces exporters to send samples to U.S. laboratories, incurring additional cross-border logistics costs. Large manufacturers with diverse product portfolios can balance the economic trade-off between proactive testing and recall risks, whereas smaller processors often delay testing until compelled by regulatory inspections or customer audits.

Challenges In Detecting Emerging And Novel Contaminants

Between 2019 and 2024, the FDA's monitoring program identified PFAS compounds in seafood, produce, and food-contact materials. However, the lack of federal action limits and standardized testing protocols has created compliance challenges for manufacturers. At the same time, microplastics in processed foods and beverages have become a growing concern, though they remain unregulated. Researchers are advancing methods such as Fourier-transform infrared spectroscopy and pyrolysis-GC-MS to measure particle counts and determine polymer types. In 2024, the detection of H5N1 avian influenza in dairy herds highlighted the rapid emergence of zoonotic pathogens. This situation compels laboratories to swiftly reallocate resources and validate new assays. Furthermore, the discovery of novel mycotoxins and fungal metabolites in grains and nuts is outpacing the capabilities of current chromatography methods. The development of reference standards and validated protocols has not kept pace with these findings. Antibiotic-resistant bacteria in meat and poultry require whole-genome sequencing to identify resistance genes, but only a limited number of laboratories, including those under USDA-FSIS, are equipped for this. The delay in setting action limits for detected contaminants discourages proactive testing. Manufacturers are concerned that voluntarily disclosing new contaminants could result in recalls or enforcement actions without clear compliance pathways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Containment Type: Pathogen Testing Dominates, GMO Verification Accelerates

Pathogen testing accounted for 48.21% of 2025 revenue, underpinned by zero-tolerance Salmonella and Listeria mandates in meat, poultry, and ready-to-eat foods. GMO verification is forecast to grow at 8.25% CAGR through 2031, supported by USDA’s bioengineered-food disclosure standard and voluntary non-GMO seals sought by upscale retailers. Pesticide and residue testing gains relevance as the EPA tightens maximum-residue limits and states set independent PFAS thresholds for food packaging. Mycotoxin testing remains essential for grain and nut exports targeting EU and Asian standards. Allergen assays received a boost from sesame’s inclusion as a major allergen, while other contaminant testing segments, covering heavy metals and microplastics, advance as research builds regulatory momentum.

Historically, per-sample costs for pathogen testing fell as multiplex PCR throughput improved, yet absolute volumes kept rising due to retail-driven finished-product checks. GMO testing benefited from dual demand: mandatory disclosure on labels and voluntary certification for marketing claims. Digital PCR is now preferred for quantifying below-0.9% GMO thresholds required in European export markets, which elevates the service value of labs offering this specialty. Laboratories that integrate isotope-ratio mass spectrometry into authenticity programs capture higher margins as adulteration incidents spur premium audit requirements.

By Technology: PCR Leads, Chromatography and Spectrometry Gain Ground

In 2025, PCR technologies accounted for 45.32% of the revenue, recognized for their speed, sensitivity, and compatibility with automated sample-prep robots. From 2026 to 2031, chromatography and spectrometry platforms are expected to grow at a strong 9.05% CAGR, driven by their capability to manage multi-residue pesticide, mycotoxin, PFAS, and authenticity workflows, areas where traditional immunoassays fall short. While immunoassays remain cost-effective for high-throughput allergen screening, the demand for confirmatory LC-MS/MS testing is rising among buyers and auditors. Additionally, biosensors, lateral-flow devices, and portable sequencing are gaining traction in early adoption scenarios, where quick on-site decisions lead to operational efficiencies.

Real-time PCR alleviates release-time bottlenecks for perishable goods, though the USDA's culture confirmation requirements still result in inventory delays. Multiplex assays, which can detect up to five pathogens in a single run, lower the cost per data point and are particularly beneficial for large processors screening incoming raw materials. Ultra-high-performance liquid chromatography combined with Orbitrap mass spectrometry enables the detection of hundreds of contaminants in a single run, addressing retailers' demands for comprehensive certificates of analysis. Isothermal amplification is becoming more popular due to its ability to operate without thermocyclers, significantly reducing capital costs, although it still awaits widespread regulatory validation.

By Application: Food Segment Anchors Revenue, Pet Food and Animal Feed Outpace

Human-food applications generated 82.98% of 2025 revenue, led by meat, poultry, and dairy categories that face stringent pathogen and chemical-residue protocols. Pet food and animal feed testing is projected to outpace at 8.11% CAGR through 2031, driven by FDA Center for Veterinary Medicine surveillance following dilated cardiomyopathy investigations and AAFCO’s tighter mycotoxin thresholds. Meat processing continues as the largest single subsegment owing to FSIS sampling plans exceeding 88 000 microbiological tests per year. Fruits and vegetables experience sustained growth as Cyclospora and pesticide concerns rise alongside broader adoption of digital traceability for leafy greens.

Pet food recalls for Salmonella and undeclared ingredients surged during 2024-2025, prompting retailers to mandate third-party verifications before shelf placement. AAFCO’s updated guidelines for aflatoxin in corn-based feed force processors to invest in LC-MS/MS methods. Dairy testing intensity rose after the 2024 H5N1 detections, elevating scrutiny of raw-milk supplies and pasteurization efficiency. Crop commodity exporters continue routine aflatoxin and ochratoxin screening to meet EU import thresholds. Processed-food manufacturers rely on authenticity and shelf-life testing to protect against brand damage from adulteration or premature spoilage.

Geography Analysis

The United States claimed 75.11% of North American market share in 2025, underpinned by FDA and USDA-FSIS regulatory mandates, a dense network of accredited laboratories, and high per-capita food consumption that drives testing volumes across meat, dairy, and processed-food categories. Mexico accelerates at 8.28% CAGR through 2031, propelled by COFEPRIS's modernization of import-export testing protocols under USMCA commitments, expansion of domestic food-processing capacity, and rising consumer awareness of food safety following high-profile adulteration cases. Canada's market grows steadily, anchored by Health Canada's Safe Food for Canadians Regulations and CFIA enforcement, yet the country's smaller population and geographic dispersion constrain laboratory density and extend turnaround times for specialized assays, according to Health Canada. The rest of North America, encompassing Caribbean and Central American territories, remains a minor contributor but benefits from cross-border trade and alignment with U.S. food-safety standards.

U.S. growth drivers include the FDA's Food Traceability Rule compliance deadline in July 2028, which will amplify testing volumes for foods on the Food Traceability List, and USDA-FSIS's expansion of whole-genome sequencing capacity to approximately 88,031 microbiological samples in FY2025 FDA. Mexico's export-oriented producers, particularly in fresh produce, seafood, and processed foods, face heightened scrutiny from U.S. importers demanding third-party verification of pathogen control and pesticide-residue compliance, a dynamic that is driving investment in accredited testing laboratories and cold-chain infrastructure.

Canada's recall statistics mirror U.S. trends, with Listeria and Salmonella dominating enforcement actions, reinforcing the need for harmonized testing standards and real-time data sharing among North American regulators[3]Source: Health Canada, “Safe Food for Canadians Regulations,” canada.ca. Blockchain-enabled traceability pilots by U.S. retailers such as Walmart are setting de facto standards that Mexican exporters must meet to retain market access, a dynamic that is accelerating adoption of digital traceability and real-time testing. Regulatory influence includes FDA's FSMA rules, USDA-FSIS sampling protocols, Health Canada's SFCR, and COFEPRIS's NOM standards, all of which mandate routine testing and third-party verification.

Regulatory Landscape

Food safety testing demand in North America is anchored by preventive-control and verification regimes led by the US FDA (FSMA rules and guidance) and USDA-FSIS sampling programs, alongside Canada’s Safe Food for Canadians Regulations (SFCR) and CFIA enforcement. USDA-FSIS continues high-volume verification activity, including sampling plans that cover microbiological and chemical-residue hazards across meat, poultry, and egg products, which supports routine pathogen, residue, and allergen testing requirements across regulated supply chains.

Traceability and labeling remain central compliance themes. In the United States, the FDA Food Traceability Rule implementation track continues, with industry engagement activities in 2026 and a compliance date referenced as July 2028 in the report context. In Canada, front-of-package (FOP) labeling requirements moved into full compliance from January 1, 2026, and Health Canada’s December 2024 regulatory updates modernized microbiological criteria, food additives, and methods of analysis, supporting standardized laboratory methods and documentation for cross-border trade.

Value Chain Analysis

The value chain spans test method and consumable inputs (reagents, kits, reference materials), analytical instruments (PCR systems, sequencing, chromatography and mass spectrometry), sample collection and logistics, and testing execution through in-house quality labs and third-party ISO/IEC 17025-accredited TIC networks. Results feed into customer release decisions and compliance documentation, increasingly linked to digital traceability data flows demanded by retailers and regulators (for example, FDA traceability rule planning toward a July 2028 compliance milestone referenced in the report context).

In North America, capacity and capability are shaped by consolidation and digitization across laboratory networks, along with method-standard updates from regulators. Health Canada’s December 2024 modernization of microbiological criteria and methods of analysis increases the need for validated workflows and consistent reporting across food matrices. On the service-delivery side, major TIC firms are expanding footprint and tooling, including SGS acquiring Murray-Brown Laboratories in 2026 to add microbial and analytical chemistry capacity, and launching the SGS FoodNexus platform to connect compliance intelligence with risk analytics, reflecting a shift toward integrated testing plus data services rather than standalone certificates of analysis.

Competitive Landscape

The North American food safety testing market is a competitive space where established leaders and emerging players are leveraging technological advancements to gain an edge. Industry leaders like Eurofins Scientific and SGS are actively expanding their presence through strategic acquisitions, such as Eurofins' acquisition of Modern Testing Services in September 2024. In this market, businesses that deliver both rapid and accurate testing services are highly valued, as food manufacturers prioritize quick results without compromising quality.

Equipment manufacturers, including Thermo Fisher Scientific and Agilent Technologies, are making notable progress by introducing advanced testing platforms. Their cutting-edge chromatography and mass spectrometry systems enable them to compete effectively with traditional testing providers. For example, Thermo Fisher's iCAP MX Series ICP-MS for trace element analysis highlights how innovative equipment can provide testing laboratories with a competitive advantage.

Smaller laboratories are establishing their presence by focusing on specialized testing areas, such as food fraud detection. These companies are integrating spectroscopic methods with machine learning to differentiate themselves through expertise rather than scale. Food manufacturers increasingly prefer testing partners capable of handling multiple contaminant types, opting for comprehensive providers over managing multiple specialized laboratories. Additionally, new opportunities are emerging in testing for substances like PFAS and microplastics, where evolving regulations demand specialized expertise.

North America Food Safety Testing Industry Leaders

SGS SA

Eurofins Scientific

Bureau Veritas

Intertek Group PLC

ALS Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest opportunity sits at the intersection of faster release testing and traceability-linked documentation. Retail and regulator focus on lot-level visibility (with the FDA Food Traceability Rule compliance timing referenced as July 2028 in the report context) is pushing laboratories and technology vendors to present test results as digital, audit-ready records that connect to customer traceability systems. Platforms built around this workflow, such as SGS FoodNexus (launched in 2026), show how demand is moving from isolated assays toward continuous risk monitoring, supplier onboarding support, and standardized data outputs that fit multiple buyer requirements.

Emerging contaminant and advanced-matrix testing remains constrained by method readiness and accreditation, which preserves room for differentiation. PFAS is one reference point in the report context: Certified Group reported FDA acceptance of a validated method for PFOA and PFOS analysis in specific seafood matrices in 2026, giving laboratories a defined pathway to expand offerings in residue and contaminant testing for import and retailer-driven specifications. Rapid microbiology also continues to be a practical opportunity for facilities that need more frequent environmental monitoring without long enrichment steps, supported by developments such as Neogen receiving AOAC Performance Tested Methods certification in 2026 for an enrichment-free Listeria environmental monitoring test.

Recent Industry Developments

- March 2026: SGS acquired Murray-Brown Laboratories in Denver, Colorado, expanding its North American food safety and nutraceutical testing footprint with added microbiology and analytical chemistry capabilities. The deal strengthens regional capacity for pesticide and mycotoxin detection and supports faster turnaround for customers consolidating vendors across multiple contaminant categories.

- January 2025: Mérieux NutriSciences completed the acquisition of Bureau Veritas food testing activities in the United States and Canada, integrating 12 laboratories and about 400 employees into its network. The combination increases scale across routine microbiology and chemistry testing and reshapes competitive dynamics for national contracts with large processors and retailers.

- September 2024: Eurofins Consumer Product Assurance acquired Modern Testing Services, adding capabilities relevant to food-related consumer product testing. The move broadened Eurofins service coverage for customers that require aligned testing and compliance support across food, packaging, and adjacent consumer-product safety requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue generated from food safety testing done for food and feed products in North America, including pathogen, allergen, chemical residue, GMO, and related contaminant testing performed using common lab methods.

Scope exclusions: This sizing does not count routine food quality checks that are not tied to safety compliance (such as basic sensory grading), nor does it count broad environmental testing that is not linked back to food or feed samples.

Segmentation Overview

- By Containment Type

- Pathogen Testing

- Pesticide and Residue Testing

- Mycotoxin Testing

- GMO Testing

- Allergen Testing

- Other Contaminant Testing

- By Technology

- Polymerase Chain Reaction

- Immunoassay-based

- Chromatography and Spectrometry

- Others

- By Application

- Pet Food and Animal Feed

- Food

- Meat and Poultry

- Dairy

- Fruits and Vegetables

- Processed Food

- Crops

- Other Foods

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and anchor the model on traceable signals that do not change with individual company marketing claims. We referred to public health and food regulatory materials and testing guidance, such as resources from USDA and FDA, along with CDC surveillance updates that indicate high priority hazards and recall patterns.

We also used public standards and method references (such as AOAC and ISO method listings), plus trade and laboratory accreditation information, to understand which test formats are being used at scale, and how pricing can differ by method and turnaround time. For market context, we reviewed company filings and investor presentations for labs and instrument providers, and we also used paid database subscriptions for company financials and intelligence, patent databases, and selective import and export shipment level data where it helped sanity check reagent and instrument flow. These desk research sources are illustrative only, and many other public and paid sources were also used to collect, cross check, and clarify data points.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with food manufacturers, contract testing labs, in house quality teams, and upstream suppliers who support test kits and analytical instruments. Coverage was balanced across the United States, Canada, Mexico, and broader North America, so assumptions on test frequency, sample mix, and pricing could be checked and corrected when secondary indicators did not line up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 50% |

| Mid tier: 51% | Functional/Unit leaders: 23% | EMEA: 32% |

| Smaller Players: 17% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

The core model is built using a top-down structure where food production and processing activity, along with compliance driven testing intensity, are translated into a demand pool for tests across North America. After the demand pool is set, pricing is applied using a blended view that reflects method mix and typical turnaround expectations, and then the totals are checked with selective bottom-up approximations (such as sampled lab revenue splits and ASP x volume logic) before final totals are locked.

Inputs used in the model include, for example, the mix of high risk food categories under routine monitoring, the share of rapid methods (like PCR and immunoassay) versus confirmatory workflows (like chromatography and spectrometry), average samples per batch or lot for major processors, recall and alert patterns that temporarily lift testing volume, and outsourcing share versus in house testing. When data is thin for smaller end users, gaps are handled through calibrated ranges taken from interviews, and then adjusted using country level production and import exposure so the totals stay realistic.

For forecasting, scenario analysis was used to reflect how changes in regulations, outbreak events, and method adoption can shift both volumes and average pricing. The forward view was then stress tested by revisiting a few expert inputs on expected adoption curves, and by checking whether the implied testing load matches practical lab capacity and turnaround constraints.

Data Validation & Update Cycle

Each model output is validated through triangulation across independent signals, and then reviewed for unusual jumps by contaminant type, method mix, and country. If an output drifts away from known operational realities, such as implied test volumes exceeding reasonable lab throughput, we recheck assumptions, revisit the desk sources, and re contact selected respondents to confirm what changed.

Before sign off, the work goes through a multi step analyst review that focuses on variance checks, currency consistency, and scope alignment. Reports are refreshed annually, and interim updates are done if a material event occurs, such as major regulatory shifts or high impact recall waves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's North American Food Safety Testing Market Market Size Compared Against Other Published Estimates

Published market sizes for food safety testing in North America often vary because the underlying count of tests and the pricing logic are not built the same way, even when the report titles look similar. Differences also come from which country set is included, how in house testing is treated, and whether the scope blends food testing with adjacent categories.

Recall and alert activity, plus method level adoption indicators from lab workflow inputs, are the checks that keep Mordor Intelligence's estimate tied to a practical testing demand pool and to realistic pricing by technology mix (rather than a single broad average rate). When these signals are not used, totals can drift, either by undercounting pathogen and allergen work that is routine, or by folding in broader food testing that is not strictly safety oriented.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.76 B (2025) | |

| Regional Consultancy A | USD 6.30 B (2024) | Uses a 2024 base and a slower growth profile, and the scope appears to rely more on high level revenue and volume framing without clearly separating method mix and routine testing intensity by food category, which can compress the implied demand pool. |

| Global Publisher B | USD 5.54 B (2024) | Covers only selected countries (primarily the US and Canada) and reports a longer horizon with a lower implied testing expansion, which can reduce totals when Mexico and broader North America activity and faster method adoption are not fully captured. |

Overall, the spread is mainly explained by geography coverage, base year choice, and how test volumes and pricing are built from method mix and routine compliance needs. By keeping the scope tied to food and feed safety testing and then validating the implied workload with real world signals, the estimate stays transparent and repeatable from clear inputs.

Key Questions Answered in the Report

What is the forecast value of the North America food safety testing market in 2031?

The market is projected to reach USD 10.41 billion by 2031.

Which containment type currently generates the highest revenue?

Pathogen testing commands 48.21% of regional revenue.

Which technology segment is expected to grow the fastest through 2031?

Chromatography and spectrometry platforms are projected to expand at 9.05% CAGR.

Which country will post the highest growth rate through 2031?

Mexico is set to grow at an 8.28% CAGR as COFEPRIS modernizes testing standards.

Page last updated on: