Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

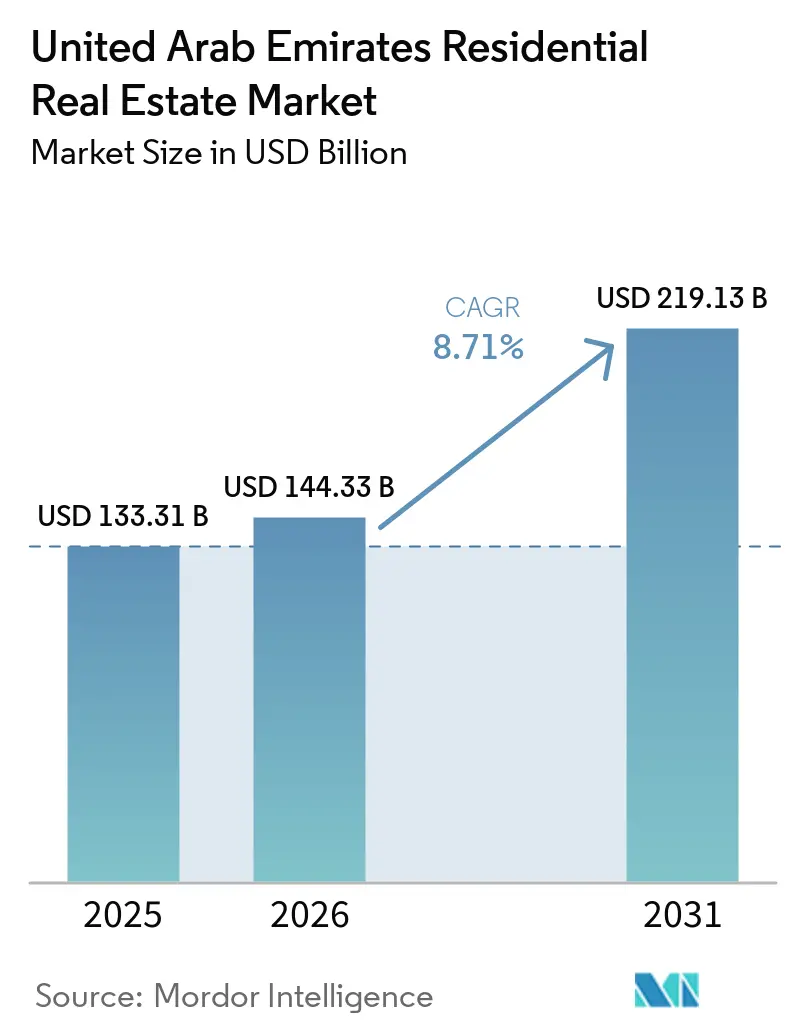

| Base Year Market Size (2025) | USD 133.31 Billion |

| Market Size (2026) | USD 144.33 Billion |

| Market Size (2031) | USD 219.13 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

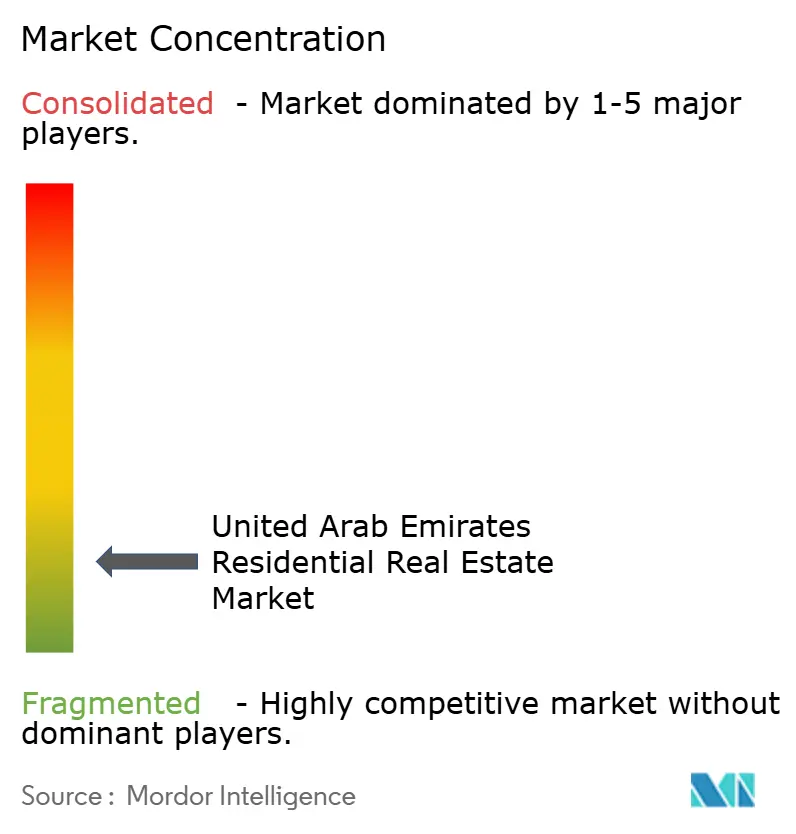

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Residential Real Estate Market Analysis by Mordor Intelligence

The UAE residential real estate market size is projected to be USD 133.31 billion in 2025 and estimated at USD 144.33 billion in 2026 and is expected to reach USD 219.13 billion by 2031, at a CAGR of 8.71% during the forecast period (2026-2031). Robust investor inflows generated by visa reforms, rapid population growth, and sustained spending on infrastructure continue to reinforce demand across Dubai, Abu Dhabi, and the northern emirates. The streamlined Golden Visa rules, large-scale smart-city mandates, and a visible pipeline of branded residences have widened the buyer base, while healthy rental yields cushion owners from fluctuations in mortgage costs. Developers respond by balancing high-rise supply in urban cores with villa-led master plans on the city periphery. At the same time, competitive intensity remains moderate, creating space for mid-sized firms to target affordable housing and PropTech-enabled communities.

Key Report Takeaways

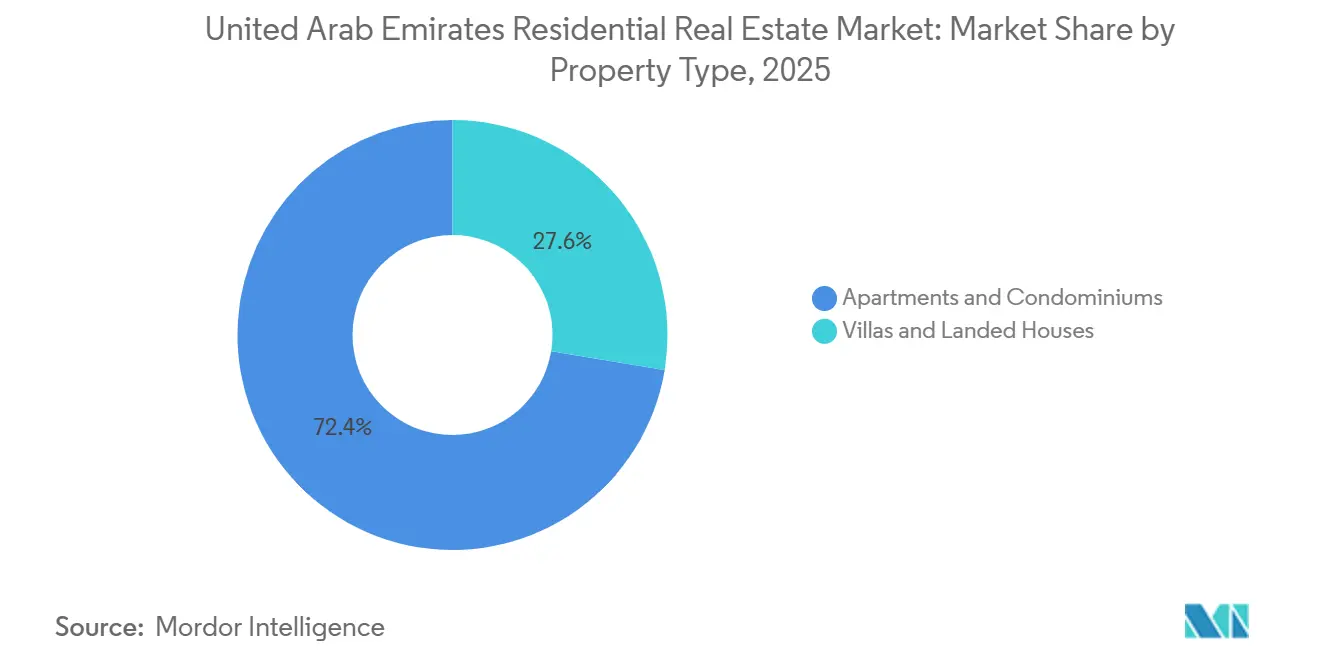

- By property type, apartments & Condominiums captured 72.40% market share in 2025, whereas villas & landed houses are forecast to expand at a 9.15% CAGR through 2031.

- By price band, mid-market listings led with 46.50% share in 2025, but luxury stock is set to post a 10.28% CAGR to 2031.

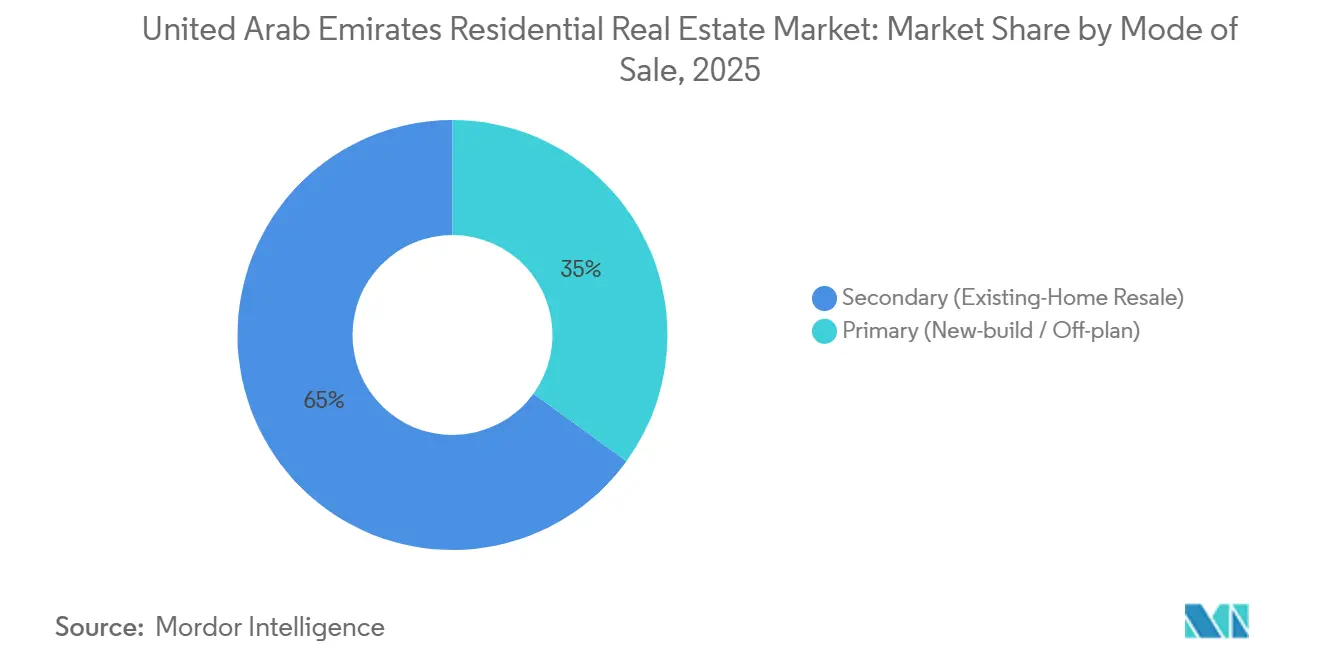

- By mode of sale, secondary resales accounted for 65.00% of 2025 transactions, and primary off-plan deals are expected to register a 10.89% CAGR by 2031.

- By business model, sales accounted for 75.00% of 2025, and rentals are expected to register a 9.58% CAGR by 2031.

- By emirate, Dubai held a 44.00% share in 2025, while Ras Al Khaimah is anticipated to record a 10.36% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Visa Reforms (Golden & Retirement Visas) Broadening Buyer Base | +1.8% | Global, strongest in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Surge in Ultra-High-Net-Worth Individuals Fuelling Luxury Segment | +1.5% | Dubai (Emirates Hills, Palm Jumeirah), Abu Dhabi (Saadiyat Island) | Short term (≤ 2 years) |

| Expo 2020 Legacy Stimulating Long-term In-migration & Housing Demand | +1.2% | Dubai, with spillover to Sharjah | Medium term (2-4 years) |

| GCC Remote-Work Policies Increasing Expat Tenant Retention | +1.0% | Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Smart-home Mandates in Dubai 2040 Master Plan Accelerating Tech-ready Units | +0.9% | Dubai, with gradual adoption in Abu Dhabi | Long term (≥ 4 years) |

| E-commerce Logistics Hubs Driving Peripheral Villa Demand | +0.7% | Dubai South, Ras Al Khaimah, Ajman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Visa Reforms (Golden & Retirement Visas) Broadening Buyer Base

The 2024 revision of Golden Visa criteria reduced the property investment threshold from AED 5 million to AED 2 million, instantly expanding the eligible pool to include mid-career professionals and small-business owners who previously lacked the capital for qualifying purchases[1]https://u.ae/en/information-and-services/visa-and-emirates-id/residence-visas/golden-visa. Retirement visas, requiring AED 1 million in property or savings, attracted retirees from Europe and Asia seeking tax-efficient residency, with anecdotal evidence suggesting a 20 to 25 percent uptick in inquiries from over-55 buyers in the first half of 2025. The Federal Tax Authority's guidance clarifying that property ownership alone does not confer tax residency—applicants must spend 183 days per year in the UAE—filtered speculative investors, ensuring that visa-linked purchases translate into genuine occupancy rather than vacant investment units. Remote-work visa holders, who must earn at least USD 3,500 per month, often lease rather than buy, but their presence stabilizes rental markets by filling units that would otherwise remain vacant during seasonal downturns. The Abu Dhabi Global Market's regulatory sandbox for remote workers further legitimizes this cohort, signaling that visa reforms are not temporary stimulus measures but structural shifts in residency policy.

Surge in Ultra-High-Net-Worth Individuals Fuelling Luxury Segment

The UAE attracted between 6,700 and 9,800 millionaires in 2024 and early 2025, a migration wave driven by geopolitical instability in Europe and Asia, zero personal income tax, and proximity to emerging markets in Africa and South Asia. Knight Frank recorded 435 residential sales exceeding USD 10 million in 2024, with Palm Jumeirah villas commanding AED 14,679 per square foot in secondary transactions, the second-highest per-square-foot price that year. Branded residences—properties affiliated with hotel operators such as Bulgari, Armani, or Four Seasons—captured 64% premiums in Dubai and 87% in Abu Dhabi over comparable unbranded stock, reflecting buyers' willingness to pay for concierge services, guaranteed rental yields, and brand prestige[2]https://www.cbre.com/. Developer 25 Degrees sold a renovated Palm Jumeirah villa for AED 62 million in 2024, then acquired a 90,000-square-foot undeveloped plot for AED 365 million in June 2025, partnering with Killa Design to deliver bespoke ultra-luxury units. This segment's resilience stems from wealth diversification strategies; UHNW buyers treat Dubai real estate as a hedge against currency devaluation and political risk in their home markets, prioritizing asset security over rental income or capital appreciation.

Expo 2020 Legacy Stimulating Long-term In-migration & Housing Demand

Expo 2020's physical footprint converted into Expo City Dubai, a mixed-use district targeting 35,000 residents by 2030, anchoring demand for mid-market apartments and serviced units within a 15-minute radius. The event's infrastructure investments—AED 30 billion in drainage networks and AED 7 billion in smart-grid upgrades—lowered the cost of connecting peripheral land parcels to utilities, enabling developers to launch affordable villa communities in formerly underdeveloped zones. Dubai's population grew at approximately 1,000 residents per day in 2024, a pace sustained by multinational firms that relocated regional headquarters to capitalize on the city's enhanced connectivity and talent pool. The legacy effect extends beyond housing; retail and hospitality operators secured long-term leases in Expo City, creating employment clusters that attract mid-tier professionals who prefer proximity to workplaces over commuting from established neighborhoods. This spatial redistribution fragments demand, compelling developers to offer differentiated amenities—co-working lounges, shuttle services, on-site childcare—that were previously confined to premium districts.

GCC remote-work policies increasing expat tenant retention

GCC countries employ 24.6 million expatriate workers, representing 78% of the region's labor force, and remote-work policies introduced during the pandemic have become permanent fixtures in Saudi Arabia, Qatar, and Kuwait. UAE-based expatriates working for GCC employers can now retain UAE residency while spending up to 50% of their time in neighboring countries, reducing the churn that historically plagued tenant rosters when employees relocated for new assignments. Dubai's Smart Rental Index, launched in January 2025 by the Dubai Land Department, provides transparent benchmarking of rents across 200+ communities, enabling landlords to justify rate adjustments while giving tenants data to negotiate renewals, which stabilizes occupancy at the expense of landlords' pricing power. Abu Dhabi's Rental Index, introduced in August 2024, similarly caps annual increases, with some submarkets experiencing 1 to 2 percent quarterly growth and others posting 5 to 10 percent annual gains depending on supply-demand imbalances. The Ministry of Human Resources and Emiratisation's talent-attraction strategy emphasizes knowledge-economy roles—fintech, AI, biotechnology—that command higher salaries and longer tenures, reducing the transient nature of the expatriate workforce and supporting multi-year lease commitments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mortgage Rates Compressing Affordability for Mid-income Buyers | -1.3% | Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Oversupply Risk in High-rise Apartment Pipeline | -1.0% | Dubai (Business Bay, JLT), Abu Dhabi (Al Reem Island) | Short term (≤ 2 years) |

| Volatile Oil Prices Limiting Federal Spending & Subsidies | -0.8% | Federal programs (Sheikh Zayed Housing), Abu Dhabi | Medium term (2-4 years) |

| Title-deed Registration Delays in Northern Emirates | -0.5% | Sharjah, Ras Al Khaimah, Ajman, Umm Al Quwain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mortgage Rates Compressing Affordability for Mid-income Buyers

The Central Bank of the UAE's 3-month EIBOR rate reached 5.31% in December 2024, and the 1-year EIBOR stood at 5.09% in November 2024, pushing retail mortgage rates to a range of 3.99% to 5.50% across major banks[3]https://www.centralbank.ae/ar/. Debt-burden-ratio regulations cap monthly debt service at 50% of gross income, effectively excluding buyers earning less than AED 15,000 per month from qualifying for mortgages on properties priced above AED 1.5 million. Damac Properties partnered with Abu Dhabi Islamic Bank in March 2025 to offer 35% completion financing, enabling buyers to defer principal payments until construction milestones are met, a structure that mitigates rate sensitivity but concentrates credit risk on the developer's balance sheet. Loan-to-value limits—80% for UAE nationals on first homes, 75% for expatriates—require down payments of AED 300,000 to AED 500,000 on median-priced units, a hurdle for mid-career professionals whose savings rates lag property-price inflation. The interplay between rising rates and static income growth suggests that affordability pressures will persist unless developers shift toward smaller unit sizes or modular construction techniques that lower per-unit costs without sacrificing quality.

Oversupply Risk in High-rise Apartment Pipeline

Dubai's development pipeline included over 66,000 apartment units scheduled for delivery in 2025, concentrated in Business Bay, Jumeirah Lake Towers, and Dubai Marina, submarkets where vacancy rates already exceeded 10% in select buildings. Abu Dhabi's Al Reem Island and Saadiyat Island similarly face absorption challenges as developers race to complete projects initiated during the 2021-2023 price surge, when pre-sales momentum masked underlying demand fragility. Rental yields in oversupplied corridors compressed to 4 to 5 percent gross, below the 6 to 7 percent returns investors expect to justify illiquidity and maintenance costs, prompting some landlords to offer rent-free periods or furniture packages to secure tenants. The concentration of institutional capital in high-rise segments—pension funds, sovereign wealth vehicles, and listed REITs favors towers with 200-plus units for operational efficiency—exacerbates supply imbalances, as these players prioritize scale over market timing. Developers with diversified portfolios that include villas and townhouses in peripheral zones face lower oversupply risk, but those locked into high-rise projects must navigate a multi-year absorption cycle that could depress pricing power and force distressed sales if pre-delivery cancellations spike.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Villas Outpace Apartments Despite Smaller Base

Apartments accounted for 72.40% of the UAE residential real estate market in 2025, mirroring the vertical skyline of Dubai Marina, Business Bay, and Al Reem Island. Villas, however, are projected to mark a 9.15% CAGR through 2031 as families value private outdoor space and remote workers seek home offices. Apartment supply benefits from quicker permitting and access to metro links, yet concentrated completions have trimmed yields in oversupplied clusters to 4-5%. Villas command 15-20% per-square-foot premiums in established suburbs like Arabian Ranches, while Dubailand and Ras Al Khaimah offer similar finishes at 30-40% discounts, dispersing demand.

Azizi Milan’s USD 20.4 billion (AED 75 billion) mixed-use community blends 70-story towers with mid-rise blocks to capture both investor and end-user appetite. Emaar launched 62 projects in 2024, booking USD 17.8 billion (AED 65.4 billion) in sales across 42,000 units under construction. The shift toward villas reflects lifestyle recalibration: post-pandemic buyers favor gardens and parking over metro proximity. Developers must weigh peripheral land prices against required roads, utilities, and schools, a balance easier for firms with deep capital bases and long horizons.

By Price Band: Luxury Stock Defies Affordability Pressures

Mid-market homes represented a 46.50% share in 2025, serving dual-income expatriates and first-time buyers. The luxury tier is forecast to deliver a 10.28% CAGR to 2031 as UHNW investors pay 64% premiums for branded residences in Dubai and 87% in Abu Dhabi. Government-funded Emirati housing worth USD 1.47 billion (AED 5.4 billion) will place 3,004 citizen homes in Latifa City, Al Yalayis, and Hatta, lightening demand at the sub-USD 272,000 bracket.

Mid-market developers like Danube deploy post-handover plans that defer 40-50% of the price until keys are handed over, effectively providing vendor finance. Luxury buyers, typically cash-rich, sidestep Central Bank LTV rules altogether. The divergent funding mechanics mean the two segments rarely substitute each other; someone priced out of a USD 544,000 marina apartment tends to shift to Sharjah, not to a USD 15 million Palm Jumeirah villa.

By Mode of Sale: Off-plan Gains on Flexible Terms

Secondary resales captured 65.00% of transactions in 2025 as buyers valued ready possession and visible community amenities. Primary off-plan volumes are forecast to compound at 10.89% through 2031 as developers sweeten deals with milestone-based payments, furniture packages, and guaranteed rental returns. Sellers who bought during the 2017-2019 dip are exiting at 30-50% gains, feeding resale inventory.

Dubai Residential REIT raised USD 583 million (AED 2.145 billion) in May 2025, offering a liquid 7.7% yield versus 4-5% direct-ownership yields in oversupplied towers. Developers protect cash flows by requiring 20-30% deposits and using escrow rules that release funds only on verified construction progress. Cancellations still hurt buyers more than developers, but stricter regulations have reduced outright project failures.

By Business Model: Rental market gains traction

Sales still prevailed in 2025 with a 75.00% share of the UAE residential real estate market size, a product of freehold legislation and residency incentives. Capital gains combine with rental income to create a powerful draw for global investors.

Rentals are advancing at a 9.58% CAGR as rate hikes bolster yields. Average Dubai rents climbed 16% in 2024, and short-term lets earned 7% returns in premier zones. AI-driven rent indices are embedding transparency, which in turn boosts institutional landlord participation inside the UAE residential real estate industry.

Geography Analysis

Dubai's dominance stems from policy continuity, infrastructure depth, and the Dubai Land Department's Smart Rental Index launched in January 2025, which provides transparent rent benchmarking across 200-plus communities and stabilizes landlord-tenant negotiations. The emirate's population reached approximately 3.8 million in 2024, growing at roughly 1,000 residents per day, a pace sustained by multinational firms relocating regional headquarters and the Expo 2020 legacy that converted event infrastructure into permanent residential and commercial districts. Dubai's 2040 Urban Master Plan targets 5.8 million residents by 2040, mandating smart-home readiness in new developments and reserving 60% of land for parks and green spaces, constraints that push developers toward vertical density and mixed-use projects that maximize land efficiency. The concentration of branded residences—Bulgari, Armani, Four Seasons—commands 64% premiums over unbranded stock, reflecting buyers' willingness to pay for concierge services and guaranteed rental yields. Oversupply risk persists in Business Bay and Jumeirah Lake Towers, where 66,000 apartment units were scheduled for 2025 delivery, yet villa communities in Dubai Hills Estate and Arabian Ranches maintain occupancy above 95% due to limited supply and family-buyer demand.

Abu Dhabi's market benefits from sovereign capital and long-term urban planning; Aldar Properties partnered with Mubadala in September 2024 on multiple joint ventures exceeding AED 30 billion in gross development value, including island developments and mixed-use districts on Saadiyat Island. The Abu Dhabi Housing Authority launched a Rental Index in August 2024, capping annual rent increases and providing landlords with data-driven justifications for rate adjustments, a balance that stabilizes occupancy while preserving landlord returns. The emirate's AED 6.75 billion housing benefits package announced in early 2025 prioritized loan repayment exemptions for senior citizens and low-income retirees, signaling a shift toward targeted relief rather than broad-based subsidies. Branded residences in Abu Dhabi command 87% premiums, the highest in the UAE, driven by scarcity; fewer than 10 branded projects exist compared to over 30 in Dubai, creating pricing power for developers who secure hotel-operator partnerships. Modon, an Abu Dhabi master developer, became the first UAE real estate company to commit to green steel in December 2024, partnering with EMSTEEL to source low-carbon steel produced using certified renewable hydrogen, a move that aligns with the UAE Net Zero 2050 Strategy and positions Modon as a sustainability leader.

Sharjah, Ras Al Khaimah, and the northern emirates capture buyers priced out of Dubai and Abu Dhabi, yet title-deed registration delays and limited freehold zones constrain foreign participation. Sharjah's land department faced a backlog in 2024 and 2025, with some transactions requiring four to six weeks for final documentation, compared to same-day electronic settlements in Dubai. The Sharjah Executive Council approved land grants for 2,000 beneficiaries in February 2025—1,200 residential plots and 800 investment parcels—yet manual verification processes delay final ownership transfer and deter institutional investors. Ras Al Khaimah's affordability advantage—villa prices 30 to 40 percent below Dubai equivalents—attracts first-time buyers and remote workers, yet the emirate's industrial base remains narrow, limiting employment diversity and long-term population retention. Ajman and Umm Al Quwain serve niche segments—retirees, small-business owners, and buyers seeking low living costs—but the absence of international schools, healthcare facilities, and entertainment options caps addressable demand. Fujairah's tourism investments and port expansion create localized housing demand, yet the emirate's geographic isolation on the UAE's east coast limits integration with the Dubai-Abu Dhabi economic corridor.

Competitive Landscape

The UAE residential real estate market exhibits moderate concentration, with the top five developers—Emaar Properties, Aldar Properties, Damac Properties, Nakheel, and Azizi Developments—controlling an estimated 40 to 45 percent of new-build supply, leaving mid-tier players to capture niche segments such as affordable housing, PropTech-enabled communities, and peripheral villa developments. Emaar reported AED 65.4 billion in sales across 62 project launches in 2024, with 42,000 units under construction, underscoring its strategy of launching multiple phases within master-planned communities to sustain sales velocity and defer completion risk. Aldar's partnership with Mubadala on AED 30 billion in joint ventures and its December 2024 acquisition of a DIFC tower for AED 2.3 billion signal a pivot toward income-generating assets that complement its development pipeline. Azizi Developments signed a 50-year land lease with AD Ports Group in December 2025 for nearly 440,000 square meters, representing an AED 2 billion investment to expand manufacturing and logistics capabilities, a vertical integration strategy that reduces reliance on third-party contractors and accelerates project delivery.

White-space opportunities exist in affordable housing and PropTech; Dubai's AED 5.4 billion housing package announced in January 2025 will deliver 3,004 homes for Emirati citizens, yet private developers have underserved the sub-AED 1 million segment due to thin margins and the perception that government programs crowd out commercial supply. The Dubai PropTech Hub, launched in July 2025, targets over 200 startups and USD 300 million in investment by 2030, creating an ecosystem where developers can pilot blockchain-based title registries, AI-driven property management, and digital-twin simulations. Smaller developers such as Danube Properties and Binghatti Developers compete on price and payment flexibility, offering 40 to 50 percent post-handover plans that appeal to mid-income buyers unable to secure bank financing, a strategy that converts vendor financing into a competitive advantage. Dubai Holding's Dubai Residential REIT, which raised AED 2.145 billion in May 2025 and manages 35,700 units, provides a template for asset-light growth; developers can monetize completed portfolios through REIT listings, recycling capital into new projects while retaining management fees.

United Arab Emirates Residential Real Estate Industry Leaders

Aldar Properties

Nakheel PJSC

Damac Properties

Deyaar Development

Emaar Properties PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Azizi Developments signed a 50-year land lease with AD Ports Group for 440,000 m² in KEZAD, investing AED 2 billion (USD 544 million) to build 12 factories .

- October 2025: Alec Holdings raised AED 1.4 billion (USD 381 million) in the UAE’s largest construction IPO, with ICD retaining 80% .

- May 2025: Dubai Residential REIT floated on DFM, collecting AED 2.145 billion (USD 583 million) and targeting a 7.7% 2025 yield .

- April 2025: Azizi unveiled the AED 75 billion (USD 20.4 billion) Azizi Milan master plan on Sheikh Mohammed Bin Zayed Road .

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates residential real estate market as every primary or secondary transaction and rental contract for apartments, condominiums, villas, and landed houses that are legally zoned for dwelling across all seven emirates.

Scope Exclusion: Commercial, hospitality, and worker-accommodation assets remain outside this perimeter.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-market

- Luxury

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build / Off-plan)

- Secondary (Existing-home Resale)

- By Emirates

- Dubai

- Abu Dhabi

- Sharjah

- Ras Al Khaimah

- Rest of UAE

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews and short polls with developers, brokerages, mortgage lenders, facilities managers, and urban-planning officials across Dubai, Abu Dhabi, Sharjah, and the Northern Emirates.

Insights on off-plan absorption, rental yield expectations, foreign-buyer mix, and handover timetables help us plug data voids and stress-test desk findings before numbers are frozen.

Desk Research

Government data streams such as Dubai Land Department registries, Abu Dhabi Department of Municipalities and Transport dashboards, the Federal Competitiveness and Statistics Center, and UAE Central Bank mortgage filings supply raw transaction values, unit completions, and lending trends.

We also review thematic releases from trade bodies like the Real Estate Regulatory Agency and Gulf Cooperation Council Housing Council that contextualize policy shocks and cross-border demand shifts.

News archives housed in Dow Jones Factiva and company financials drawn from D&B Hoovers shed light on developer pipelines and average selling prices, while academic journals add long-run price index series.

These sources underpin base-year metrics and triangulate interim quarters.

The list is illustrative; many additional public and subscription feeds further enrich, validate, and clarify our evidence base.

Market-Sizing and Forecasting

A top-down reconstruction starts with registry transaction values and rental turnover, which are then adjusted for unreported deals using population-based household formation ratios and customary cash purchases.

Select bottom-up checks, such as sampled developer revenue roll-ups and ASP times unit counts, validate totals and flag anomalies.

Key drivers inside the multivariate regression engine include net-migration gains, mortgage cost spreads, new-unit completions, median income growth, foreign ownership rule changes, and emirate-level price indices; each variable is forecast through 2030 using ARIMA or exponential smoothing aligned with central-bank rate paths.

Where bottom-up gaps appear, such as private transfer deeds in smaller emirates, we extrapolate from comparable districts after anchoring to credit-bureau loan data.

Data Validation and Update Cycle

Outputs pass a two-step analyst review, variance testing against independent price and supply monitors, and peer sign-off.

Reports refresh annually, with mid-cycle revisions triggered by policy shifts or market-moving events, and a final pre-publication audit ensures clients receive the most recent view.

Why Our UAE Residential Real Estate Baseline Commands Credibility

Published market values often diverge; scope width, data freshness, and revenue inclusions typically drive the gaps.

Key gap drivers include whether rentals are counted, if only Dubai is covered, treatment of off-plan escrow releases, currency conversion timing, and update cadence. Mordor's disciplined inclusion of rentals and every emirate, its annual refresh, and its mixed-method cross-checks collectively anchor a dependable benchmark.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 143.22 B (2025) | Mordor Intelligence | - |

| USD 36.32 B (2024) | Global Consultancy A | Excludes rentals and limits scope to primary sales in two emirates. |

| USD 18.30 B (2024) | Industry Consultancy B | Counts only registered freehold transfers, omitting off-plan and lease revenue. |

| USD 390 B (2024) | Trade Journal C | Aggregates online listing prices without time-frame filters, creating double counts. |

Taken together, these comparisons show that Mordor's balanced, transparent baseline is rooted in clearly documented variables and repeatable steps, giving decision-makers a figure they can trust.

Key Questions Answered in the Report

How large is the UAE residential real estate market in 2026?

The market reached USD 144.33 billion in 2026 and is forecast to hit USD 219.13 billion by 2031.

What is the expected CAGR for UAE homes through 2031?

The UAE residential real estate market is projected to expand at an 8.71% CAGR over the forecast period.

Which property type is growing fastest?

Villas are set to post a 9.15% CAGR, outpacing apartment growth as families seek outdoor space and home offices.

Why are off-plan sales gaining popularity?

Flexible milestone-based payment plans and guaranteed rental returns drive a 10.89% CAGR forecast for primary off-plan deals.

What segments lead by price band?

Mid-market units held 46.50% share in 2025, while the luxury tier is projected to grow at 10.28% CAGR on continued UHNW inflows.

Which emirate offers the strongest growth outlook?

Ras Al Khaimah is expected to register a 10.36% CAGR as buyers seek more affordable villas yet retain access to Dubai’s job market.

Page last updated on: