Turkey Residential Real Estate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

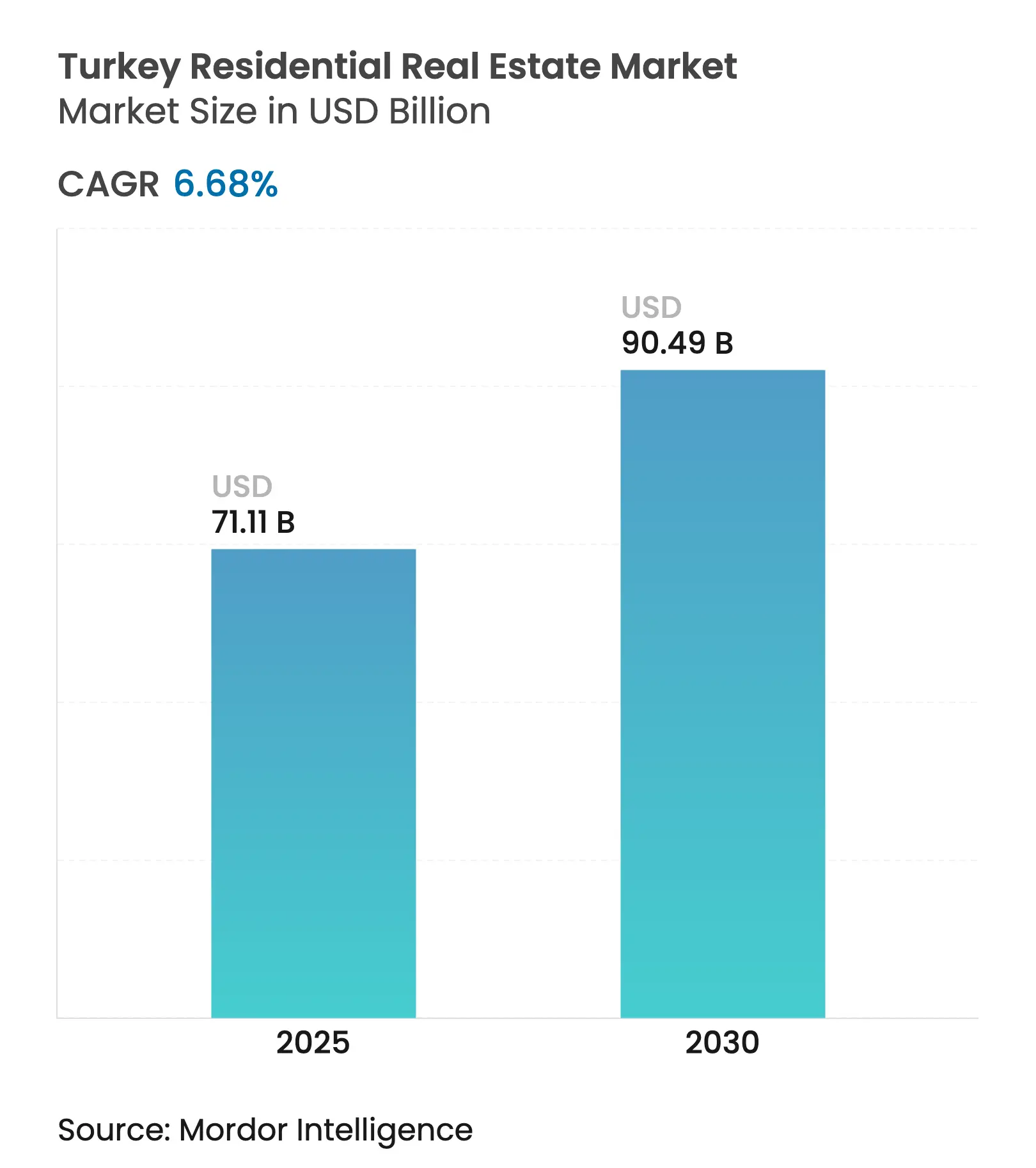

| Market Size (2025) | USD 71.11 Billion |

| Market Size (2030) | USD 90.49 Billion |

| Growth Rate (2025 - 2030) | 6.68 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Turkey Residential Real Estate Market Analysis by Mordor Intelligence

Turkey residential real estate market is valued at USD 71.11 billion in 2025 and is forecast to reach USD 90.49 billion by 2030, advancing at a 6.68% CAGR. The Turkey residential real estate market is anchored by large-scale urban renewal programs, preferential mortgage policies in selected segments, and sustained foreign capital inflows. Earthquake-driven reconstruction, notably after the 2023 Kahramanmaraş disaster, continues to underpin construction volumes, while infrastructure megaprojects such as the Istanbul Canal are opening new development corridors that support long-term price appreciation. Against persistent inflation, demand resilience stems from housing’s role as a hedge and from millennial household formation in metropolitan areas. Despite high headline interest rates, mortgage spreads on urban-transformation and green-rated projects remain favorable, sustaining primary sales in the Turkey residential real estate market.

Key Report Takeaways

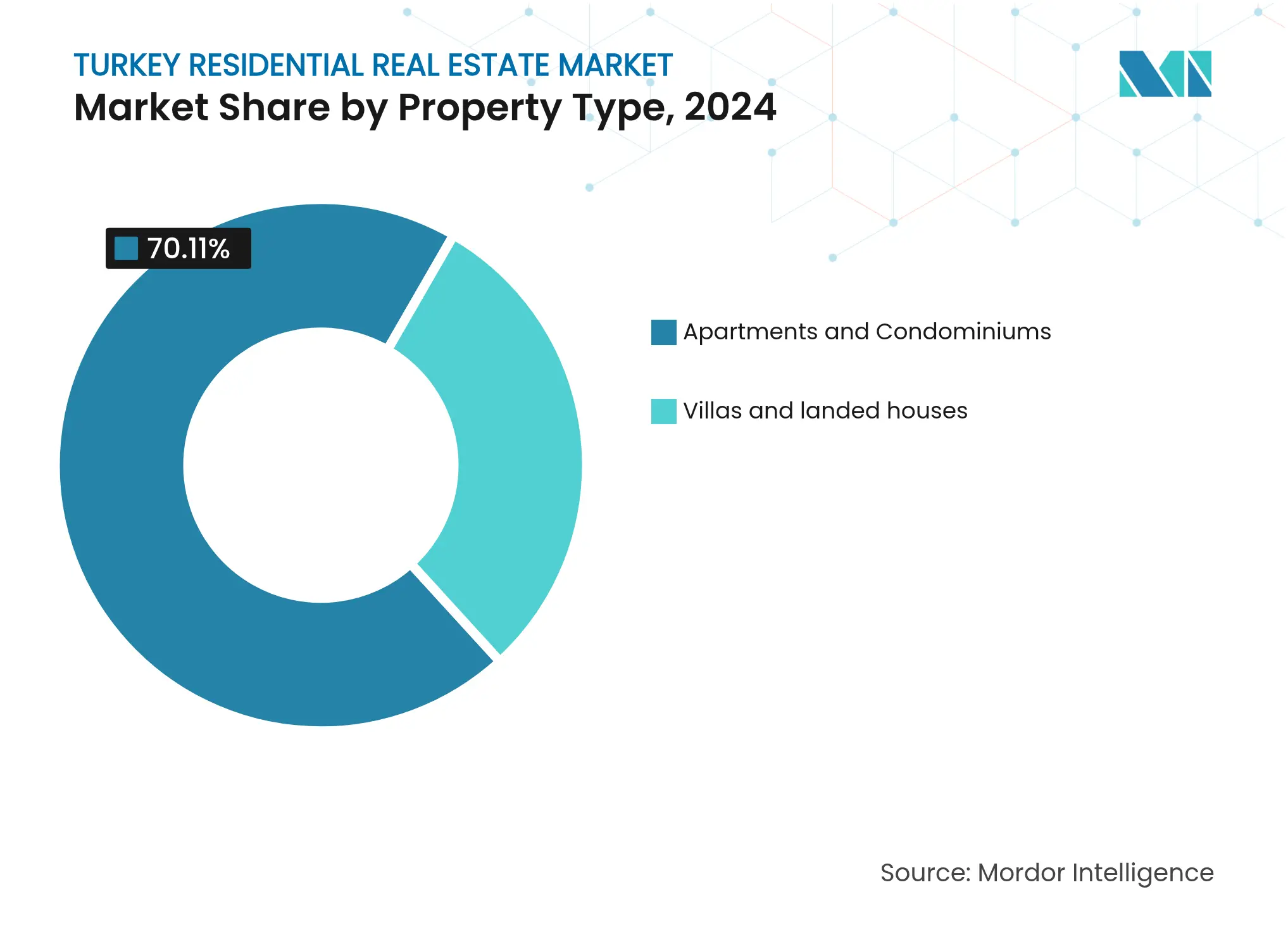

- By property type, apartments and condominiums led with 70.1% of Turkey residential real estate market share in 2024; villas and landed houses are projected to expand at a 6.88% CAGR to 2030.

- By price band, the mid-market segment accounted for 50.1% of the Turkey residential real estate market in 2024, while luxury properties are forecast to grow at a 6.96% CAGR through 2030.

- By business model, primary sales held 56.1% of the Turkey residential real estate market in 2024; secondary transactions record the highest projected CAGR at 7.35% to 2030.

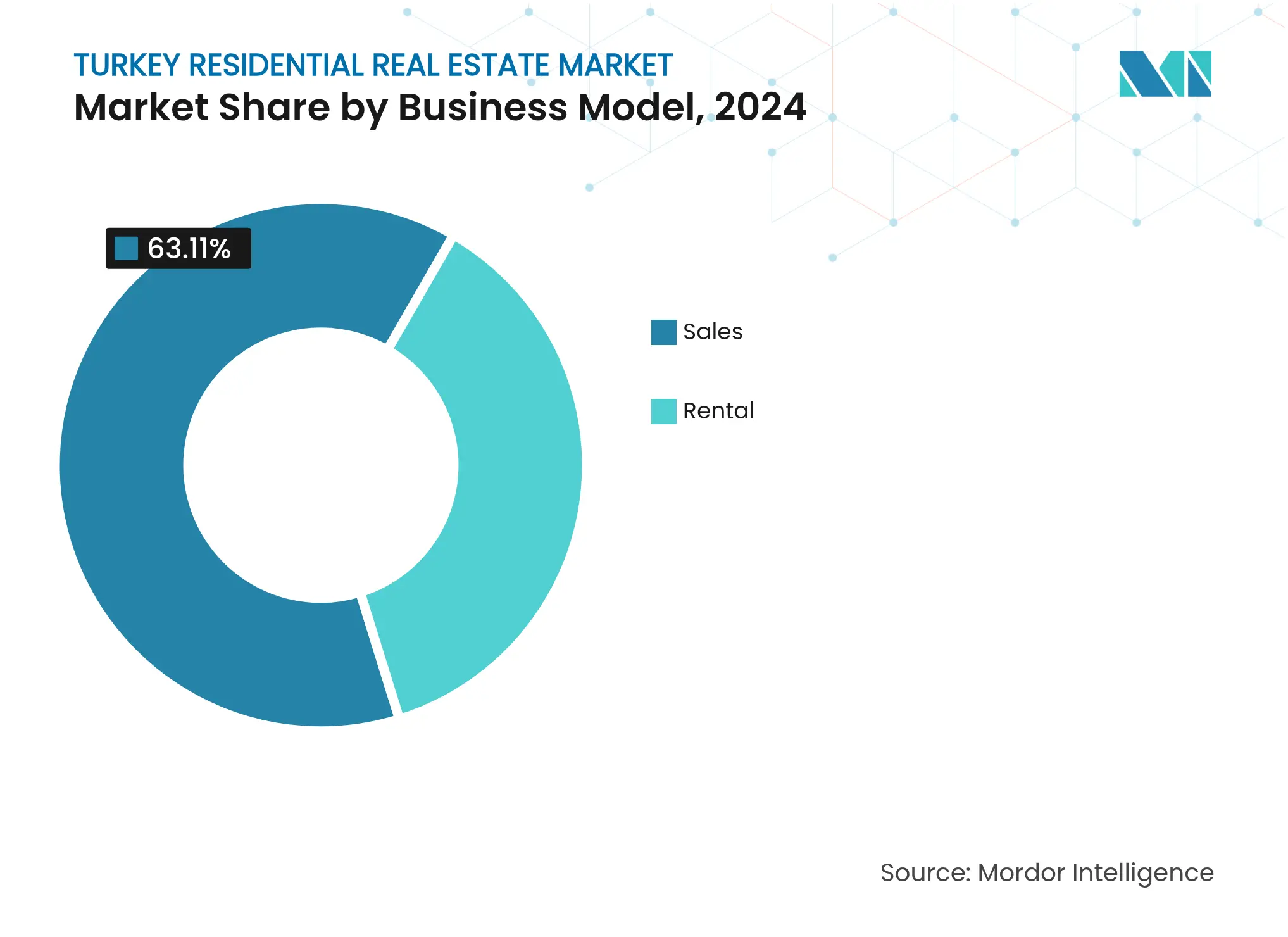

- By mode of sale, ownership transactions captured 63.1% share of the Turkey residential real estate market size in 2024; rentals are advancing at a 7.55% CAGR during the outlook period.

- By key cities, Istanbul commanded 31.5% of the Turkey residential real estate market in 2024, whereas Antalya is the fastest-growing city at a 7.68% CAGR through 2030.

Turkey Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Urban

renewal program replacing aging stock

Urban

renewal program replacing aging stock

| +1.8% | National; Istanbul-centric | Medium term (2-4 years) | ( ~ ) % Impact on CAGR Forecast:

+1.8%

|

Geographic

Relevance

:

National;

Istanbul-centric

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Competitive

mortgage regime post-2024 regulation

Competitive

mortgage regime post-2024 regulation

| +1.2% | National; major cities | Short term (≤ 2 years) | |||

Rapid

urbanisation & millennial household formation

Rapid

urbanisation & millennial household formation

| +1.1% | Istanbul, Ankara, Izmir | Long term (≥ 4 years) | |||

Citizenship-by-investment

scheme

Citizenship-by-investment

scheme

| +0.9% | Istanbul, Antalya, coastal regions | Long term (≥ 4 years) | |||

Istanbul

Canal unlocking new waterfront zones

Istanbul

Canal unlocking new waterfront zones

| +0.7% | Istanbul | Long term (≥ 4 years) | |||

Manufacturing-hub

expansion in Anatolia

Manufacturing-hub

expansion in Anatolia

| +0.6% | Central and Eastern Anatolia | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Urban renewal (“Kentsel Dönüşüm”) program accelerates stock modernisation

Turkey’s sweeping Kentsel Dönüşüm initiative targets the replacement of seismically vulnerable structures with code-compliant buildings. Momentum intensified after the 2023 earthquakes, which caused USD 60 billion in damages, of which 54.9% related to residential failures. Istanbul’s “Yarısı Bizden” scheme alone processed more than 106,000 applications and channelled USD 72 million across 213 buildings by 2024. Grants of up to USD 48,000 per unit create a multiplier effect for demolition and reconstruction, underpinning steady contractor pipelines. The systematic nature of these subsidies differentiates Turkey from peers that rely on organic supply cycles, securing multi-year demand for new homes. Consequently, the Turkey residential real estate market benefits from predictable project flow and heightened lender confidence.

Competitive mortgage environment emerges despite elevated policy rates

Regulatory tweaks adopted in 2024 allow banks to price mortgages for certified urban-transformation and green-rated units below headline lending rates. Housing loan rates eased to 39.6% even as average commercial credit costs remained near 49%. State-owned Ziraat Bank exemplifies this segmentation: mortgages form 38% of its retail book, yet non-performing loans stay at 0.1%. Preferential financing channels maintain affordability for first-time buyers and investors who comply with sustainability standards. This targeted approach mitigates interest-rate drag on absorption rates and sustains primary sales volume in the Turkey residential real estate market[1]Central Bank of the Republic of Turkey, “Weekly Monetary and Banking Statistics—April 2025,” Central Bank of the Republic of Turkey, tcmb.gov.tr.

Citizenship-by-investment program widens foreign capital access

The USD 400,000 property-purchase threshold for Turkish citizenship continues to attract investors from the Middle East, North Africa, and the Commonwealth of Independent States. Transactional data remain confidential, yet land-registry figures show sustained momentum in Istanbul and Antalya coastal districts, where foreign-buyer ratios top 40% of monthly deeds. The rule’s permanence, coupled with streamlined residency processing, provides policy certainty that underpins cross-border deal flow. Foreign capital often targets luxury waterfront assets, lifting per-square-meter values well above national averages. Ancillary service ecosystems—legal, property management, and furnishing—scale in tandem, amplifying the economic footprint of the Turkey residential real estate market.

Rapid urbanisation and millennial household formation sustain core demand

Between 2025 and 2030, Turkey’s three largest metros are projected to add more than 2 million new inhabitants, led by migration from secondary cities, according to official population registers. Millennials—now representing over one-third of urban households—prioritise proximity to mass transit, digital connectivity, and energy efficiency. Developers respond with integrated mixed-use projects that bundle co-living, retail, and office amenities within transit-oriented corridors. Household-formation momentum offsets inflation-related affordability pressure, keeping baseline absorption consistent. As a result, the Turkey residential real estate market maintains a diversified buyer mix that cushions cyclical volatility.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Currency

volatility & inflation eroding purchasing power

Currency

volatility & inflation eroding purchasing power

| -1.4% | Nationwide | Short term (≤ 2 years) | ( ~ ) % Impact on CAGR Forecast:

-1.4%

|

Geographic

Relevance

:

Nationwide

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

Earthquake-risk

compliance raising construction costs

Earthquake-risk

compliance raising construction costs

| -0.8% | Western seismic zones | Medium term (2-4 years) | |||

Rising

post-2023 insurance premiums

Rising

post-2023 insurance premiums

| -0.6% | Earthquake-prone regions | Short term (≤ 2 years) | |||

Middle-class

talent flight from secondary cities

Middle-class

talent flight from secondary cities

| -0.5% | Interior provinces | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Currency volatility constrains household affordability

Consumer-price inflation reached 42.1% in January 2025, compressing real incomes and lowering the median mortgage eligibility threshold. The lira’s swings elevate imported material costs, pushing developers to reopen tender prices weekly, which erodes pricing visibility for off-plan buyers. Although wage growth partially offsets inflation, the mismatch delays purchase decisions and lengthens sales cycles. Developers increasingly introduce extended instalment plans denominated in USD to hedge currency risk. Until macro-stability returns, exchange-rate uncertainty remains the strongest brake on the Turkey residential real estate market.

Stricter seismic compliance elevates build costs

Revised building codes introduced after the 2023 quakes mandate higher rebar density, compulsory shear-wall ratios, and certified low-carbon cement. Industry estimates place the added cost burden at 15-20% per square meter. Insurance penetration also rises, as underwriters demand robust engineering audits before issuing policies, further bolstering upfront expenses for developers. While these standards improve lifecycle resilience, they raise entry-level prices, limiting access for middle-income buyers. The cost-compliance trade-off, therefore, tempers the long-range growth potential of the Turkey residential real estate market[2]Turkish Standards Institution, “Green Cement Specification TS 15000 (2025 Revision),” Turkish Standards Institution, tse.org.tr.

Segment Analysis

By Property Type: Apartments Anchor Urban Density While Villas Gain Momentum

Apartments and condominiums held 70.11% of the Turkey residential real estate market in 2024, reflecting vertical-living norms in land-constrained metros. Multi-tower projects inside urban-transformation zones leverage shared foundations and modular façades to reduce per-unit costs, ensuring steady middle-class take-up. In Istanbul’s Arnavutköy district, TOKİ’s 24,150-unit master plan epitomises this scale-driven model, aligning residential density with planned metro extensions. The Turkey residential real estate market size for apartments is projected to expand congruently with city-centre renewal schemes, maintaining its leadership through 2030.

Villas and landed houses represent a 29.89% share but chart a 6.88% CAGR, the fastest among property types. Buyers cite demand for private gardens and home-office spaces—preferences reinforced during pandemic lockdowns. Premium detached projects in Bodrum and Fethiye trade at two-to-three-fold city-centre prices, supported by foreign-buyer appetite. Although planning-density limitations restrict mass deployment, high ticket values underpin developers’ margins. Consequently, while apartments anchor volume, villas provide a margin-diversification lever in the broader Turkey residential real estate industry.

Note: Segment shares of all individual segments available upon report purchase

By Price Band: Mid-Market Units Secure Core Volumes While Luxury Surges

Mid-market homes accounted for 50.12% of the Turkey residential real estate market in 2024, driven by salaried household demand and public-mortgage support. Developers package units between USD 120,000 and USD 220,000, balancing cost discipline with energy-efficiency features that unlock subsidised interest rates. Government vouchers covering up to 40% of retrofitting costs for A-rated buildings further encourage green upgrades. The Turkey residential real estate market size for mid-tier units, therefore, remains the stabilising backbone of annual supply pipelines.

Luxury properties, comprising 23.11% of transactions, grow at 6.96% CAGR as citizenship-motivated inflows boost coastal and waterfront demand. Prime units along the prospective Istanbul Canal secure land pre-sales at premiums approaching 25% over surrounding districts. Estate-scale resorts in Antalya integrate branded residences with hotel amenities, capturing both rental yield and capital-gain upside. Despite a narrower buyer base, robust equity financing and dollar-linked pricing shelter the luxury tier from lira depreciation, ensuring steady contribution to the Turkey residential real estate market.

By Business Model: Primary Sales Dominate but Secondary Market Matures

Primary sales represented 56.12% of the Turkey residential real estate market in 2024 as newly built units enjoy tax incentives and seismic-compliance reassurance. Bulk releases from state-sponsored developers compress per-unit land cost and enable aggressive promotional campaigns. Many off-plan purchases employ progressive-payment schedules tied to construction milestones, reducing immediate cash outlays. This financing architecture supports volume even during rate spikes, preserving the dominant role of primary sales in the Turkey residential real estate market.

Secondary transactions, though smaller at 43.88%, post a 7.35% CAGR as digitised deeds and valuation databases improve liquidity. Rail upgrades between Halkalı and Kapıkule, for instance, lifted resale prices in Thrace corridors by 5–8% in one year. Investors seeking immediate rental income gravitate toward existing stock in well-served neighbourhoods, shortening vacancy latency. Rising renovation services also add aftermarket value, promoting secondary-market acceptance within the Turkey residential real estate industry.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Sale: Ownership Prevails While Rentals Accelerate

Sales transactions captured 63.11% of the Turkey residential real estate market in 2024, underpinned by cultural preferences for asset ownership as a hedge against inflation. The requirement to hold title deeds for citizenship eligibility channels foreign funds almost exclusively into purchase deals. Domestic buyers likewise prioritise ownership, financing acquisitions through extended instalments that mirror wage-indexation clauses.

Rentals, at 36.89%, are advancing at a 7.55% CAGR, fuelled by mobile professionals and delayed first-home purchases. Institutional landlords are emerging, bundling fragmented units into professionally managed portfolios to satisfy long-stay and short-stay demand. High-yield short-term lettings in tourist zones generate annualised returns exceeding 8%, drawing capital into build-to-rent formats. The rental-income narrative provides a countercyclical plank within the Turkey residential real estate market.

Geography Analysis

Istanbul’s primacy in the Turkey residential real estate market rests on an unmatched mix of employment density, transit upgrades, and state-backed megaprojects. The “Yarısı Bizden” grant program has already channelled USD 72 million into seismic retrofits, signalling official commitment to safe densification. Simultaneously, canal-front zoning revisions expand waterfront inventory, drawing both domestic premium buyers and foreign investors seeking citizenship pathways. Consequently, the city preserves liquidity even during national credit tightening phases, anchoring overall transaction volume[3]Presidency of Strategy and Budget, “Twelfth Development Plan (2024-2028),” Presidency of Strategy and Budget, sbb.gov.tr .

Antalya’s ascendancy reflects dual demand from lifestyle migrants and tourism-driven investors. Visa liberalisation for Gulf nationals and the continuation of open-skies aviation agreements bolster seasonal visitor numbers, strengthening short-term income fundamentals. New marinas and cruise-port upgrades extend visitor stays, which in turn raise occupancy rates for branded residences. Such infrastructure boosts underscore a virtuous cycle in which leisure spending and residential absorption reinforce each other, propelling Antalya ahead of peer metros on a relative growth basis.

Interior manufacturing hubs such as Konya and Kayseri illustrate the dispersion potential of the Turkey residential real estate market. Government incentive packages for export-oriented industries generate skilled-worker inflows, spurring demand for mid-range apartments near organised industrial zones. Yet outbound migration of university-educated talent toward Istanbul and coastal regions remains a headwind. Rail corridors linking Anatolian interiors to Marmara ports aim to mitigate this divergence by cutting logistics time, thereby supporting wage growth and, ultimately, local housing demand. Regional development plans thus strive to balance metropolitan magnetism with provincial uplift, ensuring wider participation in market expansion.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Competition in the Turkey residential real estate market is characterised by a dual structure in which state-controlled developers dominate large-scale social and urban-transformation projects, while private firms pursue niche and premium opportunities. Emlak Konut GYO, backed by the Housing Development Administration (TOKİ), booked USD 1 billion in revenue during 2024 and holds a vast land bank earmarked for phased releases. Its scale advantage secures cost-efficient procurement and favourable infrastructure linkages, crowding smaller rivals out of mega-parcel bidding.

Private developers such as Sinpaş GYO and Sur Yapı focus on branded lifestyle compounds that differentiate through amenity intensity—integrated schools, health clinics, and retail boulevards. Financing strategies pivot toward pre-sales backed by dollar-indexed receivables, mitigating lira depreciation risk. Partnerships with foreign hospitality groups introduce co-branded residence-hotel hybrids, enabling price premiums and international marketing reach. These alliances illustrate how design and service innovation provide defensible niches within the Turkey residential real estate market.

Sustainability and technology adoption form the next battleground. Early movers deploy BIM-enabled construction to cut waste and embed smart-home sensors that qualify units for green-mortgage discounts. In parallel, PropTech sales platforms shorten closing cycles through digital title checks and virtual tours, reducing customer acquisition costs. Companies that hard-wire seismic monitoring into building management systems gain a reputational edge, especially in Istanbul’s transformation districts. Overall, the Turkish market rewards firms that align engineering rigour with customer-centric amenities, reinforcing a moderate concentration trend where the top five players control an estimated 45–50% of annual deliveries.

Turkey Residential Real Estate Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Emlak Konut GYO opened USD 2.8 billion in tenders for Dursunköy residential parcels adjoining the Istanbul Canal, signalling the commercial launch of canal-front housing.

- April 2025: The Central Bank reduced average mortgage rates to 39.6% while leaving benchmark lending ceilings unchanged, sustaining preferential financing for compliant projects.

- January 2025: TOKİ tendered 24,150 residential units plus commercial amenities in Arnavutköy, marking the largest single tranche of new homes linked to the canal corridor.

- October 2024: Istanbul’s “Yarısı Bizden” campaign disbursed USD 72 million in seismic-retrofit grants across 213 structures, with over 106,000 applications logged.

Table of Contents for Turkey Residential Real Estate Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Overview of the Economy and Market

- 4.2Real Estate Buying Trends – Socio-economic and Demographic Insights

- 4.3Government Initiatives and Regulatory Aspects for the Residential Real Estate Sector

- 4.4Focus on Technology Innovation, Start-ups, and PropTech in Real Estate

- 4.5Insights into Rental Yields in Real Estate Segment

- 4.6Real Estate Lending Dynamics

- 4.7Insights into Affordable-Housing Support Provided by Government and Public-private Partnerships

- 4.8Drivers

- 4.8.1Urban renewal (“Kentsel Dönüşüm”) program replacing aging stock

- 4.8.2Competitive mortgage-rate regime post-2024 regulation

- 4.8.3Citizenship-by-investment scheme attracting foreign capital

- 4.8.4Rapid urbanisation & millennial household formation in megacities

- 4.8.5Istanbul Canal mega-project unlocking new waterfront zones

- 4.8.6Manufacturing-hub expansion spurring demand in Anatolian cities

- 4.9Restraints

- 4.9.1Currency volatility & inflation eroding purchasing power

- 4.9.2Earthquake-risk compliance raising construction costs

- 4.9.3Rising post-2023 insurance premiums dampening buyer sentiment

- 4.9.4Middle-class talent flight from secondary cities

- 4.10Value / Supply-Chain Analysis

- 4.10.1Overview

- 4.10.2Real-estate Developers & Contractors – Key Quantitative and Qualitative Insights

- 4.10.3Real-estate Brokers and Agents – Key Quantitative and Qualitative Insights

- 4.10.4Property-management Companies – Key Quantitative and Qualitative Insights

- 4.10.5Insights on Valuation Advisory and Other Real-estate Services

- 4.10.6State of the Building-materials Industry & Partnerships with Key Developers

- 4.10.7Insights on Key Strategic Real-estate Investors/Buyers in the Market

- 4.11Porter’s Five Forces

- 4.11.1Bargaining Power of Suppliers

- 4.11.2Bargaining Power of Buyers

- 4.11.3Threat of New Entrants

- 4.11.4Threat of Substitutes

- 4.11.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Property Type

- 5.1.1Apartments & Condominiums

- 5.1.2Villas & Landed Houses

- 5.2By Price Band

- 5.2.1Affordable

- 5.2.2Mid-Market

- 5.2.3Luxury

- 5.3By Business Model

- 5.3.1Sales

- 5.3.2Rental

- 5.4By Mode of Sale

- 5.4.1Primary (New-Build)

- 5.4.2Secondary (Existing-home Resale)

- 5.5By Key Cities

- 5.5.1Istanbul

- 5.5.2Ankara

- 5.5.3Izmir

- 5.5.4Antalya

- 5.5.5Rest of Turkey

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves (M&A, JV, Land-bank Acquisitions, IPOs)

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1Emlak Konut GYO

- 6.4.2Toplu Konut İdaresi (TOKİ)

- 6.4.3Sinpaş GYO

- 6.4.4Sur Yapı

- 6.4.5Ağaoğlu Şirketler Grubu

- 6.4.6NEF Real Estate

- 6.4.7Kuzu Group

- 6.4.8Tahincioğlu Real Estate

- 6.4.9Tekfen Real Estate

- 6.4.10Mesa Mesken

- 6.4.11Ant Yapı

- 6.4.12Fuzul Yapı

- 6.4.13Kiler GYO

- 6.4.14GAP İnşaat

- 6.4.15Ofton Construction

- 6.4.16Seba Construction

- 6.4.17Dumankaya İnşaat

- 6.4.18Özyurtlar Holding

- 6.4.19Koray GYO

- 6.4.20Gul Proje

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment (Senior-Living, Green-Certified Homes, Co-Living)

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Turkish residential real estate market as all transactions in newly built or existing homes, including apartments, condominiums, villas, and other landed houses, concluded for owner-occupation or rental across the Republic of Turkey within a calendar year.

Scope exclusion: commercial, industrial, and purely agricultural land parcels are not covered.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- Apartments & Condominiums

- By Price Band

- Affordable

- Mid-Market

- Luxury

- Affordable

- By Business Model

- Sales

- Rental

- Sales

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing-home Resale)

- Primary (New-Build)

- By Key Cities

- Istanbul

- Ankara

- Izmir

- Antalya

- Rest of Turkey

- Istanbul

Detailed Research Methodology and Data Validation

Desk Research

We begin with macro and sector statistics from publicly available, high-credibility sources such as the Turkish Statistical Institute, the Ministry of Environment, Urbanization & Climate Change, the Central Bank's housing price index, and municipal cadaster records. These data sets anchor construction starts, issued occupancy permits, mortgage flows, and transaction volumes. Complementary insight is drawn from trade bodies such as the Association of Housing Developers and the Istanbul Chamber of Realtors, plus court-filed developer prospectuses.

To enrich context, analysts pull property tax filings, customs data on building materials, academic housing affordability studies, and press archives accessed through Dow Jones Factiva and D&B Hoovers. Numerous additional open sources were reviewed; the list above is illustrative, not exhaustive.

Primary Research

Senior brokers, project financiers, loan officers, prop-tech platform managers, and city planning officials across Istanbul, Ankara, Izmir, Antalya, and secondary towns are interviewed or surveyed. Their inputs validate selling price bands, velocity of off-plan sales, typical rental yields, and expected seismic retrofit costs, closing key information gaps surfaced during desk work.

Market-Sizing & Forecasting

A top-down model converts national housing stock, annual build completions, and resale turnover into value using city-specific average selling prices, which are then cross-checked with selective bottom-up rollups from listed developers' reported unit deliveries. Influencer variables, mortgage rate trends, urban household formation, foreign-buyer share, seismic compliance cost premiums, and citizenship-by-investment transactions feed multivariate regression to project demand through 2030. Where developer disclosures are incomplete, sample average selling prices are imputed from brokerage panels before being benchmarked against tax-record medians.

Data Validation & Update Cycle

Outputs pass three reviews: variance checks versus independent housing and banking series, senior analyst peer review, and a pre-publish refresh. The model is updated annually, with interim adjustments if policy shocks or natural disasters materially shift market drivers.

Why Mordor's Turkey Residential Real Estate Baseline Commands Reliability

Benchmark comparison

Published estimates often diverge because research firms apply distinct property scopes, conversion rates, and refresh cadences. Our analysts disclose all inclusions, vet every variable against source documents, and update figures every twelve months, which keeps our baseline tightly aligned with what the market is actually transacting.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 71.11 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 138.32 B (2024) | Global Consultancy A | Includes land development and commercial units, applies aggressive exchange-rate assumptions | ||

USD 90 B (2023) | Industry Association B | Uses contractor revenue surveys without adjusting for multi-year project overlap | ||

USD 64.32 B (2024) | Research Firm C | Relies on limited metropolitan deed data, undercounts secondary-city resale activity |