Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

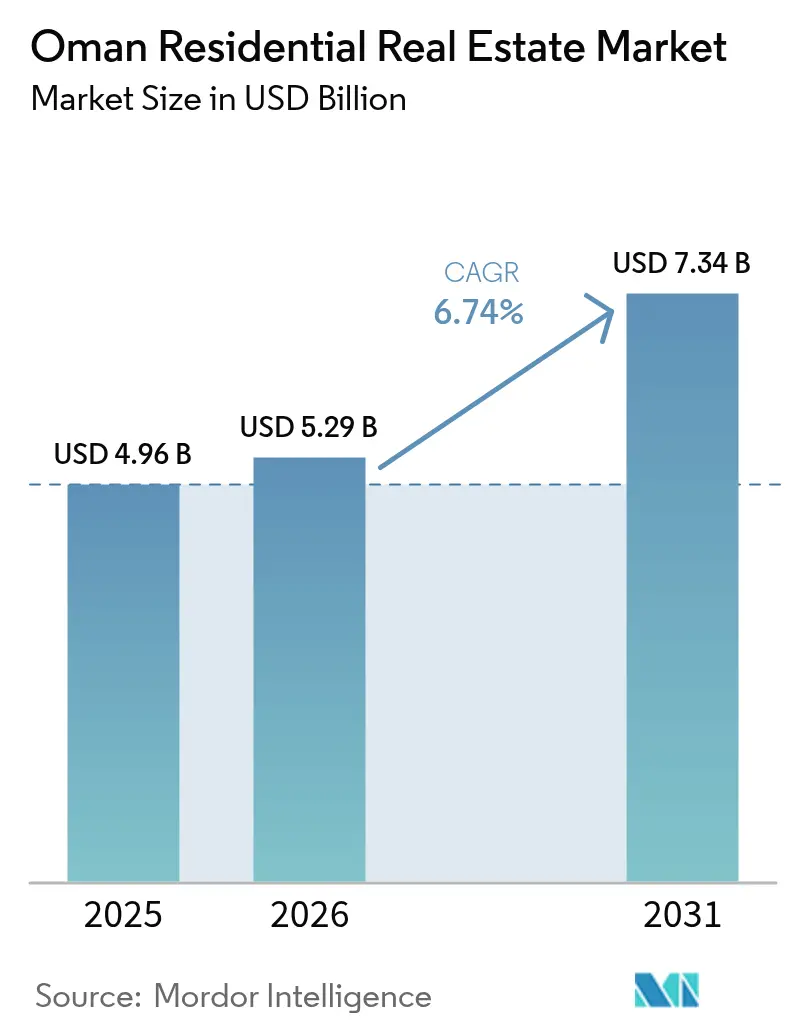

| Base Year Market Size (2025) | USD 4.96 Billion |

| Market Size (2026) | USD 5.29 Billion |

| Market Size (2031) | USD 7.34 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

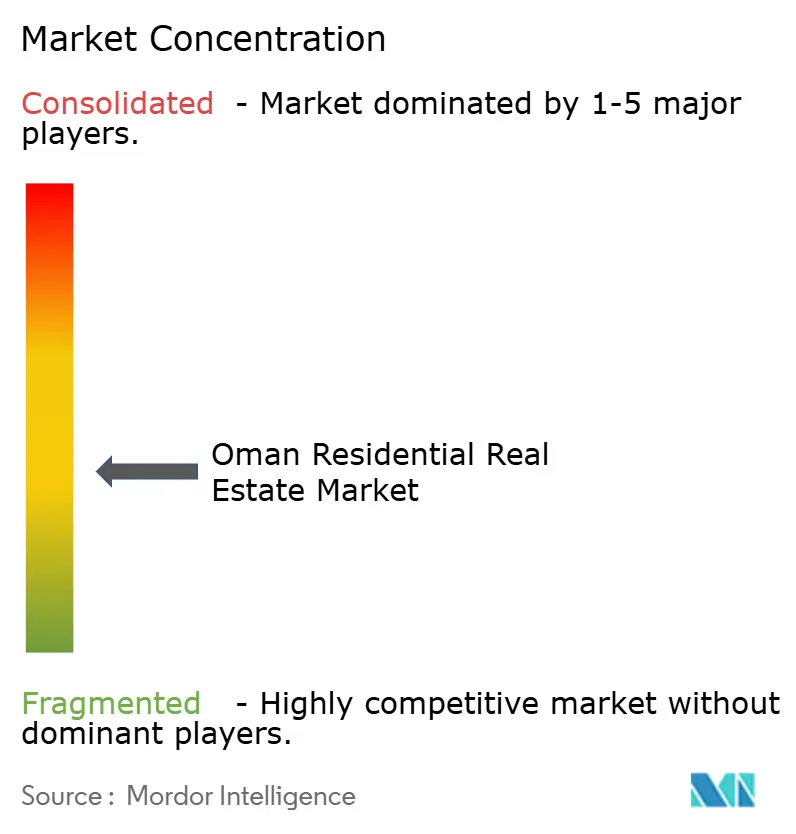

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Residential Real Estate Market Analysis by Mordor Intelligence

The Oman residential real estate market size in 2026 is estimated at USD 5.29 billion, growing from 2025 value of USD 4.96 billion with 2031 projections showing USD 7.34 billion, growing at 6.74% CAGR over 2026-2031. The expansion is underpinned by Vision 2040 infrastructure spending, a steady population increase, and fresh freehold rules that widen the eligible buyer base. Large-scale master plans such as Sultan Haitham City and New City Salalah are accelerating land absorption, while lower transaction fees encourage first-time purchasers. Developers are also pushing smart-home features and green building standards to capture demand from younger households, a move that differentiates offerings and supports price resilience. Sustained mortgage growth—supported by the banking sector’s rising appetite for longer tenors—keeps the sales pipeline predictable, even as rental yields between 5.6% and 8.3% remain attractive relative to regional peers.

Key Report Takeaways

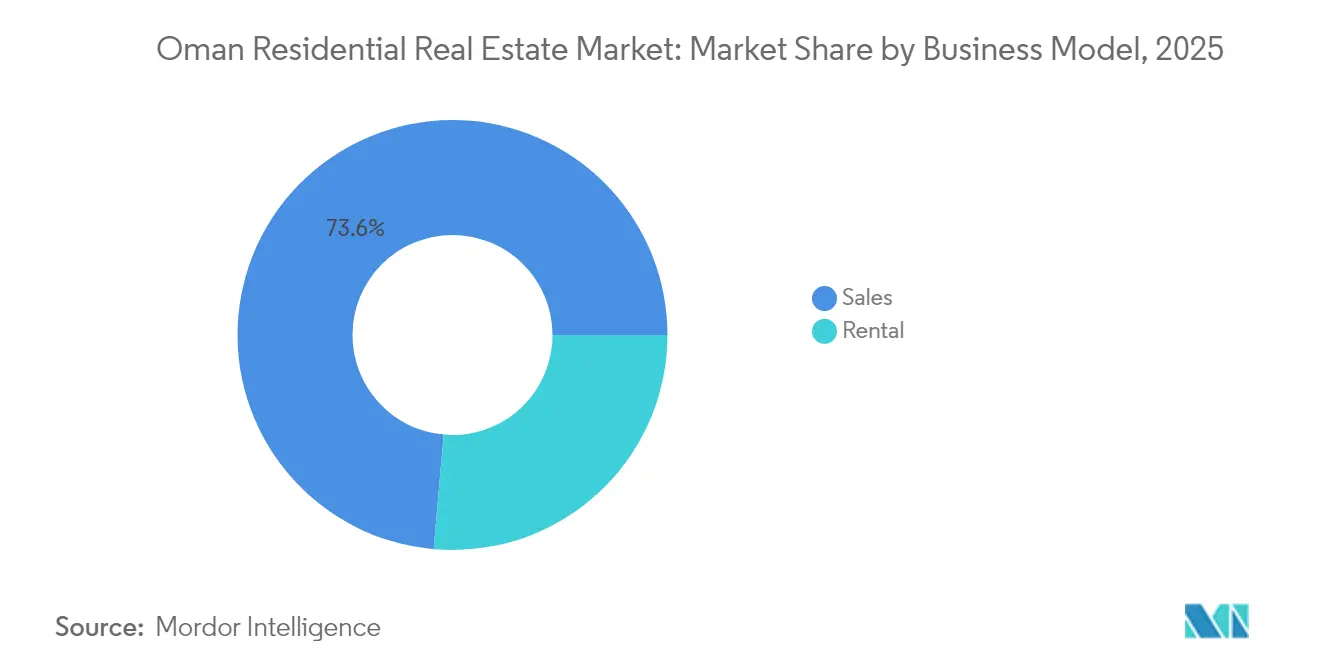

- By business model, the sales segment led with 73.60% of the Oman residential real estate market share in 2025, while rentals are projected to post the fastest 7.28% CAGR through 2031.

- By property type, villas held 66.85% of the Oman residential real estate market share in 2025; apartments are on track for the highest 7.36% CAGR to 2031.

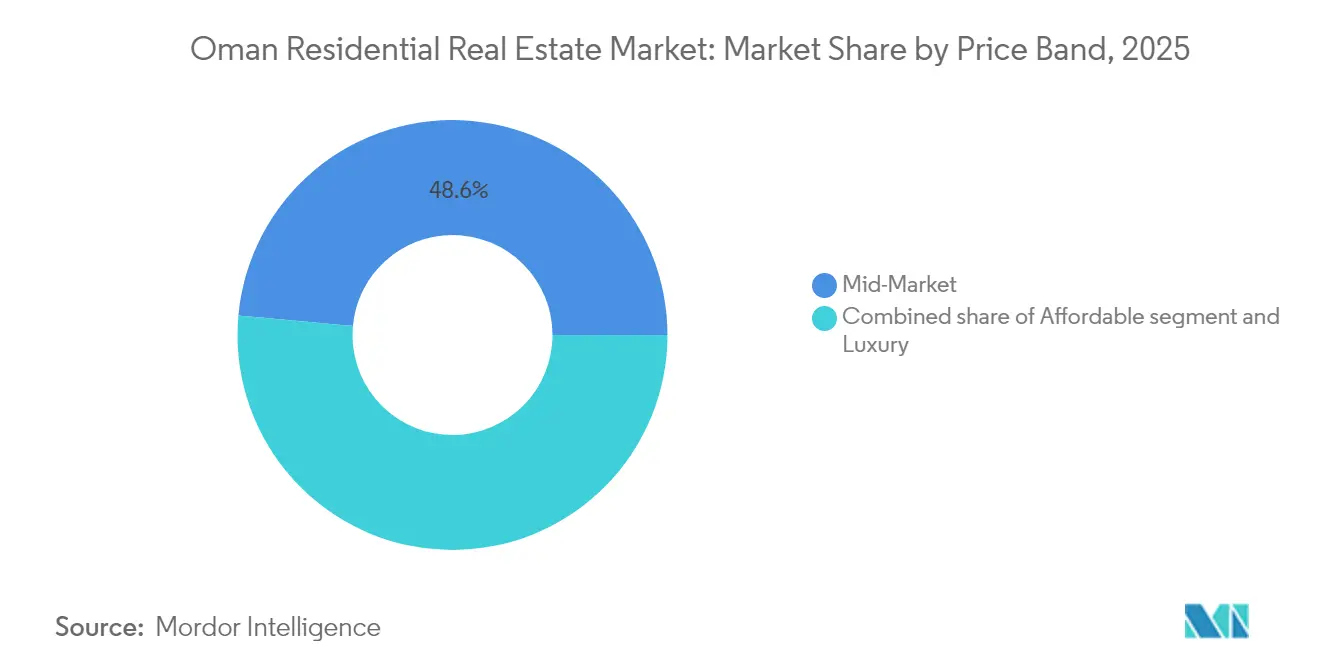

- By price band, mid-market homes captured 48.55% share of the Oman residential real estate market size in 2025, whereas luxury units are forecast to expand at a 7.56% CAGR between 2026-2031.

- By mode of sale, primary transactions accounted for 54.10% of the Oman residential real estate market size in 2025 and are advancing at a 7.32% CAGR over the outlook period.

- By city, Muscat commanded 47.35% revenue share in 2025; Dhofar is set to record the quickest 7.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Young, expanding population fuels household formation | +1.8% | Muscat and key secondary cities | Medium term (2-4 years) |

| Urban master plans create new residential hubs | +1.5% | Muscat, Salalah, Dhofar | Long term (≥ 4 years) |

| Housing programs and subsidies widen ownership access | +1.2% | Nationwide integrated neighborhoods | Long term (≥ 4 years) |

| Expatriate demand rises in freehold and ITC zones | +0.9% | Muscat, Al Mouj, SEZs | Medium term (2-4 years) |

| Lifestyle shift toward modern apartments and gated communities | +0.7% | Urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Housing Demand Supported by a Young, Expanding Population

A median age below 32 and a 15% population jump over five years are steadily enlarging the pool of first-time buyers. Ministry data show 500,000 active housing requests and 125,000 families lacking suitable dwellings, underscoring an urgent supply gap. The government has reacted with 22 integrated residential-neighborhood projects that fold in schools, clinics, and green areas to match rising lifestyle expectations. Simultaneously, an 8% rebound in expatriate numbers during 2024 revived rental absorption in Muscat’s core districts. Modest but targeted job programs—300-400 positions annually—add incremental purchasing power to the Oman residential real estate market[1]Husam Al-Mukhaini, “Annual Housing Requests and Allocations Report 2024,” Ministry of Housing and Urban Planning, mohup.gov.om.

Government Housing Programs and Subsidies Improving Affordability

In 2024, the Social Housing Program supported 1,382 families, while the “Choose Your Land” scheme allocated 25,000 serviced plots. Registration fees fell from 2% to 1% for citizens, and Islamic-finance charges were trimmed, jointly lowering entry costs. A USD 1.3 billion public-private partnership envelope mobilizes private capital for low- and mid-income communities, securing faster build-out without fiscal overstretch. Preferential land grants to marriage-fund beneficiaries further streamline the ownership path for young couples. Together, these levers expand the addressable Oman residential real estate market[2]Fatma Al-Zadjali, “Budget Execution Update 2024,” Ministry of Finance, mof.gov.om.

Urban Development Plans Creating New Residential Hubs

The Greater Muscat Structural Plan maps land use across 1,360 km² to 2040, earmarking transit-oriented corridors and mixed-use clusters. Al Khuwair Downtown, a USD 2.6 billion waterfront project, integrates offices, retail, and 4,000 homes, showcasing greener design and shorter commute times. In Dhofar, New City Salalah spans 7.3 km² with 12,000 housing units and climate-resilient drainage, indicating how secondary cities are absorbing spillover demand. Vision 2040’s USD 85 billion project pipeline also lists five future cities, signaling a long runway for the Oman residential real estate market[3]Ahmed Al-Habsi, “Greater Muscat Structural Plan 2040 Summary,” Muscat Municipality, muscatmun.gov.om.

Rising Interest from Expatriates via Freehold Zones and ITCs

April 2025 regulations allow full ownership for non-Omani individuals in Special Economic Zones, building on earlier Integrated Tourism Complex provisions. Foreign purchase transactions climbed 19.4% year-on-year in 2024, and the First-Class Residency Card ties a five-year visa to a USD 1.3 million property outlay. New touristic districts beyond Al Mouj enlarge the inventory that foreigners can legally buy, while SEZAD’s asset base of USD 54.6 billion validates investor confidence. These incentives widen the Oman residential real estate market’s global catchment.

Restraints Impact Analysis*

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction costs and skilled-labor shortages | -1.1% | Nationwide, large projects | Short term (≤ 2 years) |

| Oil-revenue dependence causing demand fluctuations | -0.8% | Nationwide | Medium term (2-4 years) |

| Regulatory and procedural delays | -0.6% | Nationwide, mixed-use schemes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Construction Costs and Limited Skilled Labor

Input prices climbed in 2024 as steel and cement import costs tracked global commodity swings, squeezing contractor margins on fixed-price contracts. Omanization quotas complicate hiring pipelines, and visa clearances for specialists often extend beyond eight weeks. The construction sector added USD 9 billion to GDP in 2023, but must now stretch to deliver a USD 85 billion project backlog. Early adopters of 3D printing note 30% material savings, hinting at a partial offset to escalating costs. Overall, execution risk mildly tempers the Oman residential real estate market growth.

Economic Dependence on Oil Revenues

Oil still funds close to 65% of fiscal receipts, so budgeted housing programs track Brent-price swings. While non-hydrocarbon GDP advanced 3.7% in 2024, any extended crude-price slump could trim infrastructure outlays and cool buyer sentiment. IMF stress tests flag banks’ 17.1% real-estate lending exposure as a watch point should prices soften. A rising sovereign net-asset position provides a short-term buffer, yet deeper diversification will determine long-term stability for the Oman residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales Dominance with Rental Acceleration

Sales held 73.60% of the Oman residential real estate market share in 2025 on the back of subsidized mortgages and lower transaction fees. Mortgage values jumped 44.8% year-on-year to USD 5.5 billion, even as contract counts dipped, implying larger ticket sizes. Buy-to-let investors from neighboring GCC economies remain active, lured by tax-free rental income and 5%–8% gross yields. The rental segment’s 7.28% CAGR outlook reflects rebounding expatriate inflows and the build-out of Integrated Tourism Complexes that bundle hospitality and residential assets.

Developers are experimenting with rent-to-own contracts that convert monthly leases into down-payments, a mechanism that broadens affordability without over-leveraging households. Digital tenancy platforms enhance transparency on lease terms and enable real-time inventory tracking, shortening vacancy periods. Corporate leasing demand also shows promise as multinational firms reopen regional offices, adding a new stripe of long-term tenants. Altogether, these dynamics point to a more balanced Oman residential real estate market over time.

By Property Type: Villas Lead While Apartments Gain Momentum

Villas retained a 66.85% Oman residential real estate market share in 2025, underlining cultural preferences for larger footprints and privacy. Projects such as the Al Ahlam District in Sultan Haitham City offer 47 energy-efficient villas equipped with solar rooftops and gray-water recycling, bringing sustainability into the luxury segment. Yet apartments post the stronger 7.36% CAGR, buoyed by urban land scarcity and demand for lock-and-leave lifestyles. Pipeline launches, including the six-tower Yenaier Residences, promise more than 1,200 units by 2027, swelling the apartment slice of the Oman residential real estate market size.

Smart-apartment deployments use IoT sensors to cut energy usage by 25%, an attractive feature for tenants amid rising utility tariffs. Meanwhile, mixed-use icons such as AIDA in Yiti will knit 3,500 residences with hotels, retail, and an 18-hole golf course, blurring traditional property boundaries. In the medium term, villas are expected to maintain value defensiveness, whereas apartments will underpin volume acceleration.

By Price Band: Mid-Market Stability with Luxury Premium Growth

Mid-market listings sat at 48.55% of the Oman residential real estate market size in 2025, serving a broad base of salaried nationals and expatriate professionals. Average ticket prices between USD 250,000 and USD 400,000 remained within reach thanks to subsidies on registration and easing down-payment norms. The luxury tier, priced above USD 650,000, is forecast to grow at a 7.56% CAGR, energized by high-net-worth GCC investors seeking coastal second homes cheaper than Dubai. Freehold villa plots in Muscat’s Al Mouj sell for up to USD 1.3 million yet still undercut regional benchmarks by 20%–30%.

Eco-luxury trends, including net-zero energy design and organic landscaping, are reshaping the upper end and broadening appeal to ESG-minded foreign buyers. At the opposite end, the Sustainable City-Yiti targets middle-income households with a promise of 100% renewable power and zero waste. These bifurcated strategies keep both value-driven and aspirational buyers engaged in the Oman residential real estate market.

By Mode of Sale: Primary Sales Drive Growth with Secondary Maturation

Primary deals made up 54.10% of the Oman residential real estate market share in 2025, thanks to fresh master-plan launches and quicker land-title approvals—SEZAD now processes usufruct applications in 5 days, down from 30. Flagship projects, including Sultan Haitham City’s USD 2.6 billion first phase, feed a robust off-plan funnel. Secondary trading is maturing as early investors monetize gains; real-estate digital registry “Amlak” logged 133,000 transfers in 2024, cutting paperwork times by half.

Price dispersion became more visible: Muscat apartment values slipped 12.9% year-on-year, whereas villa prices rose 2.5%, reflecting divergent demand pools. Regional arbitrage also surfaced, with land in North Al Batinah appreciating 18.8% as industrial expansion spilled into housing. This two-track performance creates new risk-adjusted opportunities across the Oman residential real estate market.

Geography Analysis

Muscat commanded 47.35% of the 2025 transaction value, cementing its role as the administrative and financial hub of the Oman residential real estate market. The Greater Muscat Plan meshes public transit with density nodes to keep commute times under 30 minutes, a quality-of-life metric that sustains buyer interest. Digital city services—from e-approvals to unified maintenance portals—improve municipal responsiveness and underpin property values. Ongoing migration from Ruwi and Muttrah toward newly minted districts such as Al Khuwair reflects preferences for modern infrastructure and walkable mixed-use clusters.

Dhofar is the fastest-growing pocket, set to post a 7.82% CAGR through 2031. New City Salalah will roll out 5,827 residential units in its first tranche, targeting a permanent population of 60,000. A 6-kilometer public beach, extensive mangrove restoration, and flood-resilient drainage fortify the development against climate risks. Seasonal tourism peaks align with the Khareef monsoon, lengthening occupancy cycles for investors seeking steady cash flow within the Oman residential real estate market.

Musandam and the rest of Oman are also on the government’s decentralization radar. Each governorate now receives USD 52 million annually for community upgrades, double the prior allocation. The Palm Hills project in Khasab reserves 25% of its 650 units for foreign buyers, introducing a novel demand segment. Royal Decree 36/2022 empowers local authorities to fast-track permits, accelerating the pace at which smaller cities can absorb migration from Muscat. Collectively, these regional efforts diversify the geographical base of the Oman residential real estate market.

Regulatory Landscape

Oman is modernizing residential real estate governance under the Ministry of Housing and Urban Planning (MoHUP), with Royal Decree 79/2025 (Law Regulating Real Estate) establishing a consolidated framework across ownership structuring, development, brokerage practices, and related controls. This consolidation supports the market shift toward larger master-planned and off-plan schemes, while keeping a single oversight point for the sector through MoHUP.

A further step followed with Royal Decree 56/2026 (Real Estate Registry Law), effective May 18, 2026, which replaced the 1998 Real Estate Register System and anchored electronic registration for property transactions. The law grants electronic documents (including title documentation) legal validity, requires registration of rights in rem to be enforceable, and explicitly defines the registry role for off-plan units and real estate development projects, improving transaction certainty across primary sales and institutional-grade assets.

Value Chain Analysis

The Oman residential real estate value chain is anchored by public planning and regulation, with MoHUP central to land allocation, project supervision, and the licensing environment under the unified legal framework introduced by Royal Decree 79/2025. Upstream supply includes land release and master planning (for example, Sultan Haitham City), along with enabling infrastructure delivered through public-private models that interface with utilities and connectivity providers such as Nama Water Services, Nama Electricity Distribution, and Oman Broadband Company, influencing the pace and quality of integrated neighborhood delivery.

Midstream execution is led by developers, contractors, and specialist consultants (design, engineering, and project management), followed by marketing and distribution through brokers and direct developer sales, and then downstream property and community management. Digitization is also moving into delivery and transfer workflows, reinforced by national steps toward electronic registration. Operational bottlenecks remain concentrated in construction execution (input-cost swings, skilled labor availability, and on-the-ground logistics such as congestion affecting materials movement), which can extend handover timelines and lift delivered unit costs.

Competitive Landscape

Roughly 90 licensed developers compete across the Oman residential real estate industry, making the field moderately fragmented. OMRAN Group’s joint venture with Saudi-based Dar Al Arkan on the USD 1.5 billion AIDA resort underscores a trend toward cross-border capital pools that share design expertise and risk. Public-private partnership templates now standardize land-lease terms, tenure rights, and utility responsibilities, lowering barriers for new entrants while maintaining governance clarity.

Digital tools are sharpening competitive edges. Early adopters of building information modeling report 20% faster design iterations, while 3D-printed elements shorten villa shell timelines by 30 days. The Oman Endowment Foundation’s profit-sharing structures introduce a social-impact layer, blending commercial returns with community development. Smart-home packages bundled into mortgages increase customer stickiness and enable developers to command slight price premiums within the Oman residential real estate market.

Regulatory tightening raises the bar on quality. Mandatory green-building codes phase in from 2026, compelling material efficiency and thermal standards. Developers investing in compliance ahead of schedule will likely win institutional buyers seeking ESG-aligned assets. Meanwhile, secondary-city specialists enjoy lower land costs and loosened zoning caps, allowing them to underprice Muscat peers without sacrificing margins. The competitive narrative, therefore, revolves around capital depth, technology adoption, and geographic focus rather than price alone.

Oman Residential Real Estate Industry Leaders

Al Mouj Muscat

Al Raid Group

Wujha Real Estate

Al-Taher Group

Maysan Properties SAOC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale, government-enabled execution is creating clearer whitespace in integrated communities and mid-market supply, backed by national programs and named master plans. The Ministry of Housing and Urban Planning reported that total investments in Sultan Haitham City exceeded RO 2.4 billion with more than 1,700 units sold (April 2026). The same period also included additional development agreements for Sultan Haitham City neighborhoods and Sorouh initiative agreements across multiple governorates for over 2,100 units, expanding the investable and developable inventory beyond core Muscat.

Regulatory and process modernization is also opening room in primary transactions, off-plan structuring, and digitized conveyancing. Royal Decree 56/2026 (Real Estate Registry Law), effective May 18, 2026, formalizes electronic registration and clarifies registry treatment for development projects and off-plan units, while Royal Decree 79/2025 provides a consolidated sector framework under MoHUP. In parallel with visible demand levers, including freehold expansion in eligible zones (April 2025) and ongoing buyer focus on amenity-rich master plans such as Al Khuwair Downtown and New City Salalah, the opportunity favors developers and platforms that can package compliant off-plan products, align buyer protections with escrow-ready processes, and support faster title transfer experiences.

Recent Industry Developments

- May 2026: Musstir unveiled the RO 300 million Musstir Heights residential destination at Al Jabal Al Akhdar as part of the Al Jabal Al Aali masterplan. The launch expands investable residential supply into a higher-altitude, lifestyle-led location, reinforcing the role of destination projects in attracting both second-home and investment demand.

- February 2026: Al Mouj Muscat launched the final release of Azura Beach Residences III and IV with 100% freehold ownership. The release adds premium coastal inventory and shows how freehold-enabled master plans are being used to deepen foreign and expatriate participation in Oman residential assets.

- February 2025: The Ministry of Housing and Urban Planning signed multiple partnership agreements to expand the delivery of integrated neighborhoods. The deals reinforce PPP-style delivery and broaden the project pipeline feeding primary sales activity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers the value of residential real estate activity in Oman, where homes are bought, sold, developed, or leased for living purposes across key cities and the rest of the country.

Scope exclusions: We exclude commercial, industrial, and hospitality real estate activity, along with pure land banking that is not linked to residential housing delivery or occupancy.

Segmentation Overview

- By Business Model

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public indicators that explain how the housing market is behaving in Oman, and then the assumptions were narrowed down for demand, supply, and pricing. We relied on sources such as Oman government housing and planning releases, the National Centre for Statistics and Information for macro and population trends, the Central Bank for credit and mortgage direction, and international sources such as World Bank and IMF macro series for income and inflation context.

To connect activity to market value, we also reviewed public transaction and mortgage commentary where available, plus developer announcements, project pipeline notes, and reputable press coverage on new launches and handovers. In parallel, a paid subscription that aggregates company financials and another that tracks news and financial disclosures were used to cross-check revenue ranges and investment signals when public statements were limited. These desk research sources are illustrative, and many additional public documents and datasets were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually selling and renting, and what price moves are realistic across apartment and villa stock in Oman. We spoke with a mix of developers, brokerage and property management firms, lenders and valuation professionals, and informed buyers or landlord-side respondents across the main demand centers, which helped close gaps left by public data and align assumptions on absorption, discounting, and resale activity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 46% | Functional/Unit leaders: 33% | |

| Smaller Players: 20% | Managers: 48% |

Market-Sizing & Forecasting

Sizing used top-down and bottom-up logic together, where a demand pool was first reconstructed using Oman housing demand signals and then tested against observed supply delivery. The top-down build links household formation, expat inflow, mortgage appetite, and project handover volumes to a value outcome through price and rent benchmarks, before being adjusted for realistic take-up and vacancy behavior.

To keep the model grounded, a few market fingerprints were tracked closely, including residential transaction momentum (where disclosed), mortgage growth direction and lending terms, new unit deliveries in large master plans, split of apartments versus villas in buyer preference, and the rental-to-sale switching seen when rates or job conditions change. Forecasting was run using scenario analysis supported by simple time-series smoothing on key drivers, and the scenarios were stress-tested in interviews so the base case reflects the most likely pricing and absorption path. Where bottom-up inputs were incomplete for certain cities or secondary resale flow, we filled gaps using conservative peer benchmarks and then checked the totals back to demand indicators so the final number stayed consistent.

Data Validation & Update Cycle

Outputs were validated through multiple passes, starting with internal checks on price, volume, and growth rates so that no single assumption overpowered the results. We compared the final value trend against independent signals such as mortgage direction, announced handovers, and reported transaction value narratives, and then revisited any large variances with follow-up calls.

Before sign-off, another analyst reviews the logic and the key inputs, and any outliers are traced back to the exact driver that caused them. Reports are refreshed annually, and interim updates are made when there is a material event such as policy changes affecting ownership, major launch delays, or a visible shift in financing conditions. Right before delivery, a final refresh pass is done so the client receives the latest view available at that time.

Mordor Intelligence's Oman Residential Real Estate Market Sizing Compared With Other Published Estimates

Published market sizes for Oman residential real estate often do not match, even when the topic sounds identical, because each study counts value in its own way. Differences usually come from whether the estimate focuses on primary sales only or also includes rentals, whether secondary resale is treated as market value, and how price and volume assumptions are updated.

Here, the key gap drivers were checked one by one, including the city coverage split versus a Muscat-heavy view, treatment of apartments versus villas, and how price bands are rolled up when luxury projects shift the average price. Currency timing also matters, since FX windows and inflation periods can change the USD value for the same local trend, and refresh cadence can lag fast changes in mortgage conditions and discounting. The spread is largely explained by counting rentals and secondary transactions differently across cities and price bands, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.29 B (2026) | |

| Trade Journal A | USD 4.38 B (2024) | Uses an earlier base year and a shorter outlook, and it typically reflects a sales-led view that can undercount rental value and later-cycle handovers in large master plans. |

| Industry Publisher B | USD 3.67 B (2022) | Anchors the estimate to an older market phase and simpler property-type buckets, which can miss post-2022 pricing resets, financing shifts, and the city mix changes that lift the value base. |

Taken together, the table shows that year choice and value definition drive most of the difference, more than any single assumption. By tying the total to clear demand indicators and then checking it against delivery and financing signals, the estimate stays traceable and repeatable while still reflecting how the market is actually transacting.

Key Questions Answered in the Report

What is the current value of the Oman residential real estate market?

The Oman residential real estate market size is USD 5.29 billion in 2026.

How fast is the market expected to grow?

It is projected to expand at a 6.74% CAGR, reaching USD 7.34 billion by 2031 over 2026-2031.

Which region is growing the quickest?

Dhofar is forecast to post the fastest 7.82% CAGR, powered by New City Salalah, through 2031.

Are foreigners allowed to buy homes in Oman?

Yes, April 2025 regulations grant freehold rights to non-Omanis in Special Economic Zones and Integrated Tourism Complexes.

What rental yields can investors expect?

Gross yields typically range between 5.6% and 8.3%, depending on property type and location.

Page last updated on: