Residential Induction Cooktops Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.54 Billion |

| Market Size (2031) | USD 23.90 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Induction Cooktops Market Analysis by Mordor Intelligence

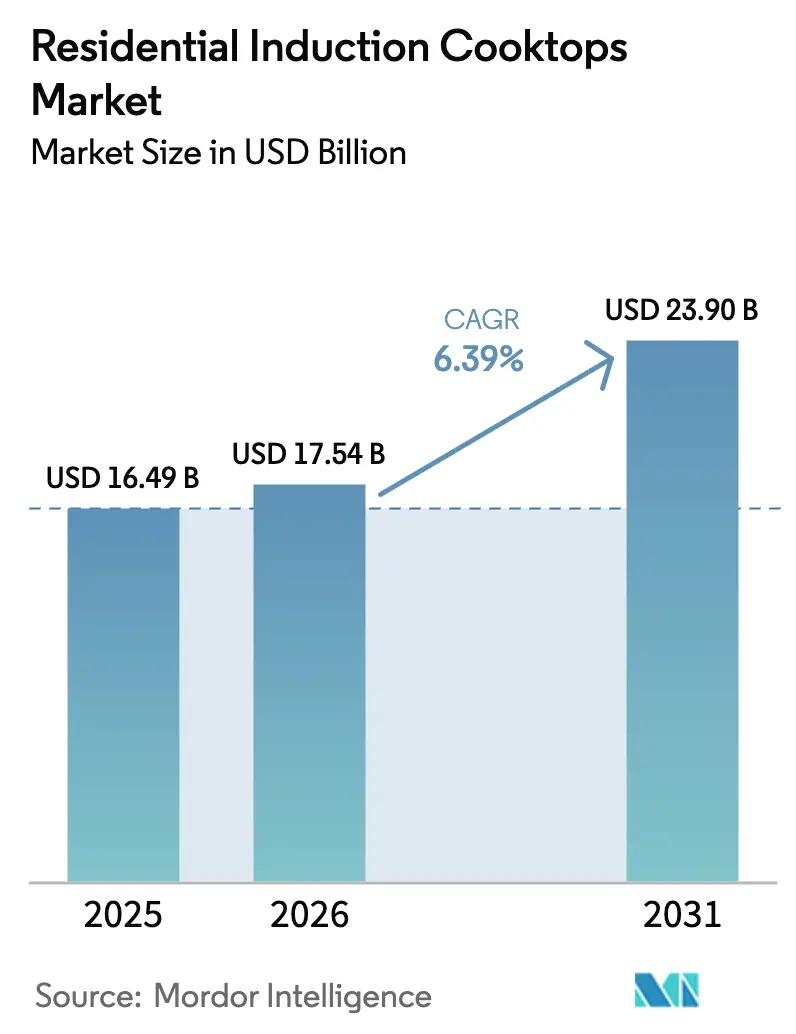

The residential induction cooktops market size is expected to increase from USD 16.49 billion in 2025 to USD 17.54 billion in 2026 and reach USD 23.90 billion by 2031, growing at a CAGR of 6.39% over 2026-2031. The pricing parity shift is accelerating adoption as Europe advances new Ecodesign requirements for domestic cooking appliances and mandates emissions reporting for gas appliances, which strengthens the relative efficiency case for induction systems with high energy transfer to cookware. Rising standards in the United States add to this structural tilt since the Department of Energy has finalized energy conservation rules that press manufacturers toward higher-efficiency topologies and aligned component choices. The efficiency profile of induction relative to gas and radiant designs still plays a central role in consumer decision-making, supported by advances in power electronics that cut losses and shrink inverter footprints. Regional policy and code changes combine with design innovations to lower retrofit barriers, expand addressable households, and widen distribution opportunities across value tiers within the residential induction cooktops market.

Key Report Takeaways

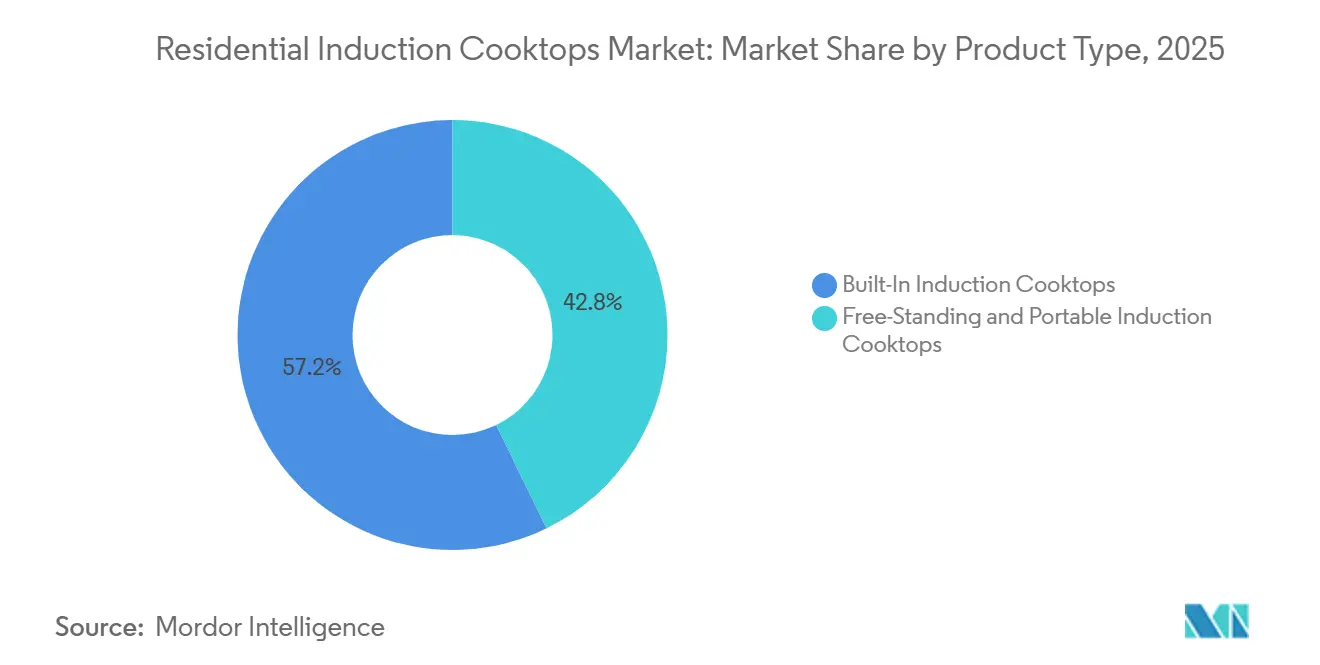

- By product type, built-in induction cooktops held 57.20% of the residential induction cooktops market size in 2025, while free-standing and portable variants are projected to advance at a 7.45% CAGR through 2031.

- By cooktop size, three-to-four-zone configurations accounted for 45.40% of the residential induction cooktops market share in 2025, while two-zone models are forecast to grow at an 8.28% CAGR through 2031.

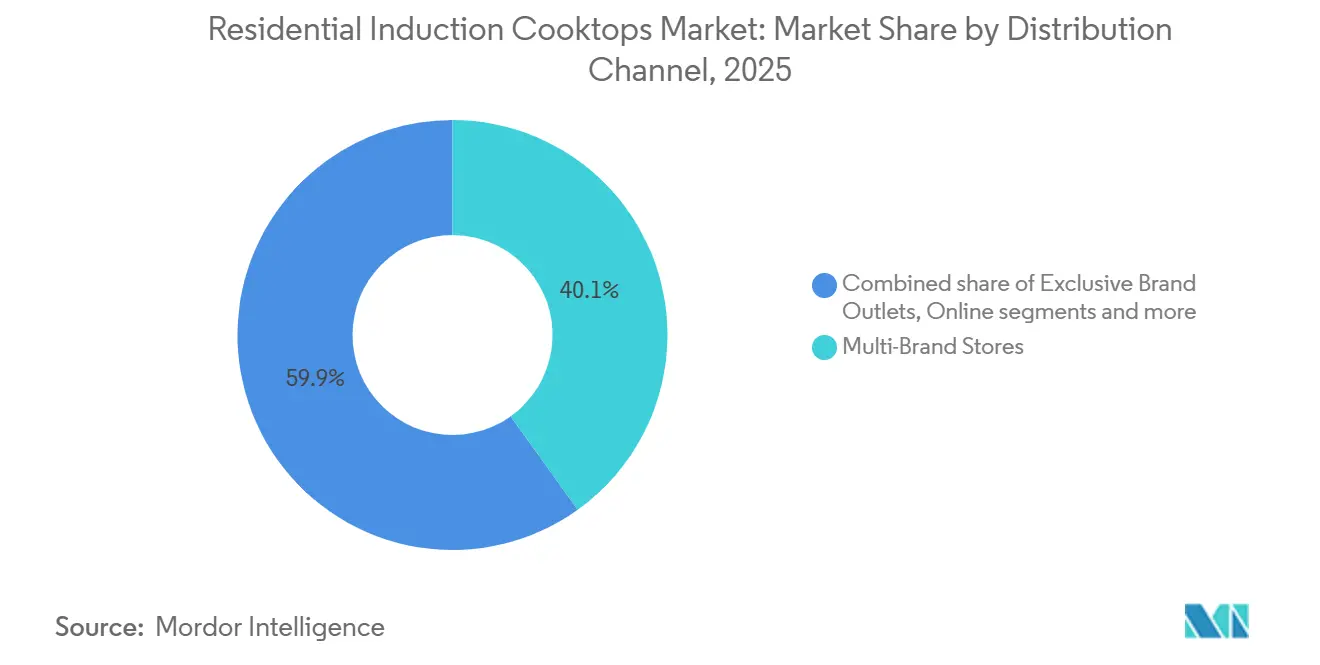

- By distribution channel, multi-brand stores held 40.05% of the residential induction cooktops market share in 2025, while online channels are projected to register a 9.16% CAGR through 2031.

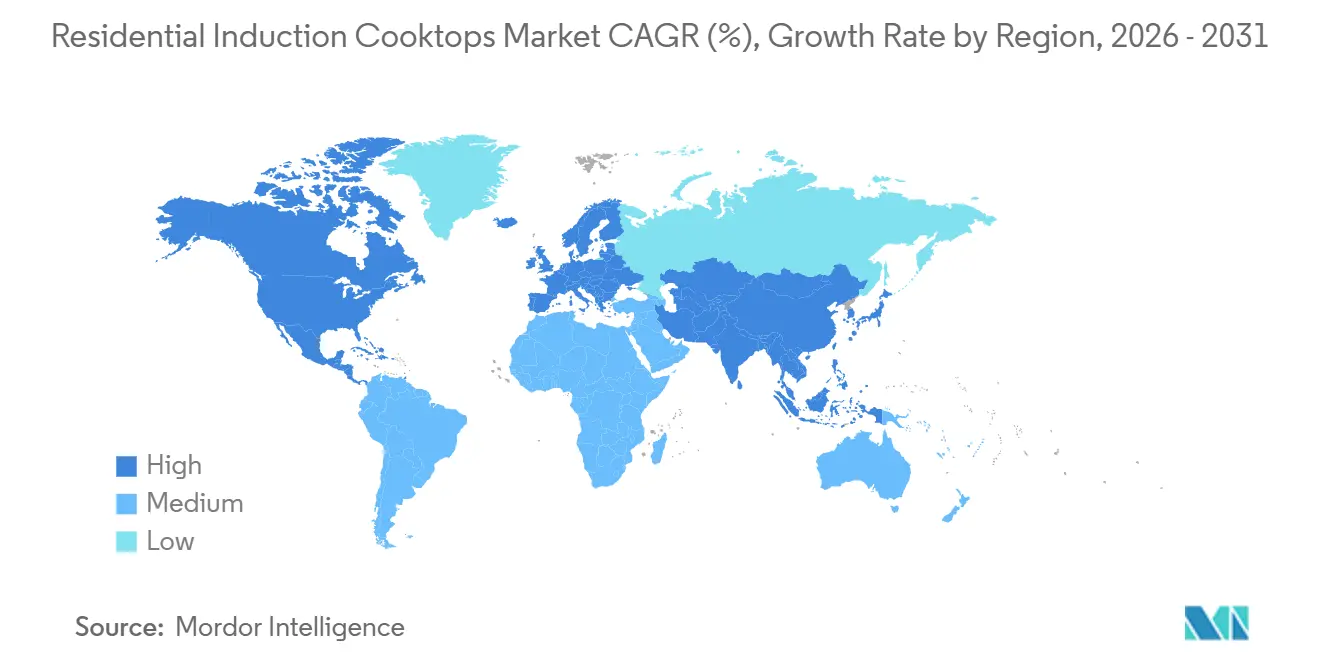

- By geography, Asia-Pacific commanded 45.40% of the residential induction cooktops market share in 2025 and is projected to grow at an 8.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Residential Induction Cooktops Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory energy-efficiency regulations | +1.8% | Global, core in EU, North America, China | Medium term (2-4 years) |

| Urban adoption of smart kitchens and remodels | +1.3% | North America and EU, expanding to Asia urban cores | Medium term (2-4 years) |

| Government-backed electrification in Asia | +2.1% | APAC core with spill-over to MEA | Long term (≥ 4 years) |

| Declining cost of wide-band-gap power electronics | +1.0% | Global, faster where fabs are local | Long term (≥ 4 years) |

| Micro-living driving portable demand | +0.6% | National, early in dense urban areas | Short term (≤ 2 years) |

| Integration of AI-powered energy management systems | +1.5% | Global, early adoption in tech-forward regions (North America, EU, APAC urban centers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Energy-Efficiency Regulations in Key Economies

Policy changes in the United States and Europe are reshaping the residential induction cooktops market. The United States Department of Energy’s Direct Final Rule limits annual energy consumption for smooth-element electric cooktops to 207 kilowatt-hours starting January 2028, promoting higher-efficiency designs[1]U.S. Department of Energy, “Energy Conservation Program: Energy Conservation Standards for Consumer Conventional Cooking Products,” Energy.gov.. In Europe, stricter Ecodesign standards enhance performance and emissions transparency, increasing compliance challenges for gas appliances while boosting induction cooktops' appeal due to their energy efficiency. Manufacturers are focusing on induction designs with advanced semiconductors to reduce switching losses. Updates to standards and testing protocols streamline design options, enabling scalable, high-efficiency platforms across brands. These regulatory developments are driving market growth by aligning product designs with compliance requirements and consumer demand for energy-efficient solutions through 2031.

Rising Urban Adoption of Smart Kitchens & Premium Remodels

Increasing adoption of connected features, interoperability, and premium remodeling preferences is driving the demand for induction cooktops in urban households. Smart home appliance usage, including ovens and connected kitchen devices, reached 12.8% in the European Union, with 14.2% using internet-connected energy management systems[2]Eurostat, “Internet connected devices in the EU,” ec.europa.eu, 2024. AI-powered recommendations, guided cooking, app connectivity, and integration with digital assistants are making induction cooktops a key digital interface in modern kitchens. Manufacturers and semiconductor partners are enhancing voice control, touch interfaces, and cross-brand communication through open standards. Premium options like downdraft cooktops address structural and ventilation needs, reducing ducting requirements in urban areas. Supplier messaging highlights health, safety, and air quality benefits, aligning with urban electrification initiatives.

Government-Backed Electrification of Cooking in Asia

Efforts across Asia are integrating efficient electric cooking into clean-cooking and electrification agendas, boosting the residential induction cooktops market. India focuses on public institution deployments, labeling improvements, and tariffs supporting electric cooking in states with favorable electricity pricing. South and Southeast Asia are incorporating induction devices into strategies to reduce fuel imports and improve indoor air quality. Hydroelectricity-rich nations use low-carbon electricity to promote modern cooking solutions, while pilots define electricity access thresholds for sustained use. In sub-Saharan Africa, 80% of households lack clean cooking access. New policies and investments, backed by a USD 2.2 billion global commitment, have driven progress in Ghana, Kenya, and Nigeria. Investments rose in 2023, covering most previously underserved populations[3]International Energy Agency, “Universal Access to Clean Cooking in Africa,” iea.org..

Declining Cost of Wide-Band-Gap Power Electronics

Silicon carbide and gallium nitride devices are improving inverter efficiency, enabling smaller and cooler induction power stages, which reduce system costs in residential induction cooktops. Enhanced switching frequencies and thermal performance allow compact designs for portable enclosures, minimizing active cooling needs and expanding form-factor options. Scaling 300-millimeter manufacturing for wide-band-gap devices improves unit economics and shortens delivery times for advanced power components. Studies show nearly 97% converter efficiency at domestic power levels, balancing performance and cost with hybrid devices. These advancements drive miniaturization and simplify thermal management for portable and built-in segments. Lower costs of wide-band-gap semiconductors also allow mid-tier brands to offer efficient, price-competitive cooktop platforms in the residential market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost vs. gas and coil | -1.5% | Global, acute in price-sensitive Asia and South America | Short term (≤ 2 years) |

| Limited cookware compatibility | -0.9% | Global, stronger in rural India and Sub-Saharan Africa | Medium term (2-4 years) |

| Intermittent electricity supply in emerging markets | -1.2% | APAC, Africa, Latin America | Short term (≤ 2 years) |

| Consumer hesitation due to unfamiliar technology | -0.8% | Global, stronger in older demographics and rural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs. Gas & Coil Cookers

High entry prices remain a challenge for budget-conscious households, despite improvements in the total cost of ownership in many regions of the residential induction cooktops market. Incentive programs in the United States reduce initial costs for income-qualified buyers, while in Europe, higher purchase prices for induction models compared to gas or coil units slow adoption, where subsidies or electricity tariffs fail to close the gap. Financing and pay-as-you-go models in emerging markets address affordability issues, but households often prioritize lower upfront costs over long-term savings. Premium brands focus on performance, connectivity, and noise reduction, while mid-tier brands emphasize value through bundled features and warranties. These factors will influence adoption rates across regions and retail channels.

Limited Cookware Compatibility (Ferromagnetic)

Ferromagnetic cookware requirements create challenges for first-time buyers in the residential induction cooktops market, often leading to additional purchases. Public programs in Asia have bundled compatible cookware to improve user experience and reduce return rates in regions with varying utensil quality. Field pilots in India revealed temperature-safety issues with low-quality utensils, prompting upgrades to tri-ply vessels for better thermal performance. High-efficiency portable induction products offer benefits like speed and control, but the need for compatible cookware increases costs for households. Perception gaps about heat strength persist among gas users, highlighting the importance of in-store demonstrations and education. Features like flex-zone cooking and pan-size detection may ease compatibility issues, though ferromagnetic bases remain essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Built-In Installations Entrench Premium Positioning as Portable Battery Variants Address Retrofit Gaps

Built-in induction cooktops held 57.20% of the 2025 market share due to their compatibility with integrated cabinetry, new construction, and premium remodels prioritizing design continuity, high-end features, and energy efficiency. These cooktops dominate the European and North American retail markets, offering features such as guided cooking, self-cleaning ovens, and smart-home connectivity. Premium models focus on improved acoustic performance, expanded flex-zone capabilities, and durable surfaces, aligning with full-kitchen remodel budgets. Partnerships with other brands and semiconductor firms enhance interoperability and advanced control interfaces, reinforcing their role as a standard in affluent neighborhoods and builder programs for spec homes.

Free-standing and portable induction cooktops are expected to grow at a 7.45% CAGR through 2031, supported by 115-volt and 120-volt designs that require minimal electrical work and by battery-integrated models that boost peak power without new circuits. Retrofit-friendly downdraft units eliminate ductwork, enabling installations in older apartments and open-plan remodels. Demonstrations in U.S. pilot programs show lower-power induction platforms meet typical household cooking needs, expanding their appeal beyond all-electric new construction. Product launches and awards highlight momentum for retrofit designs across premium and mid-tier segments, with distribution through builder networks, showrooms, and online platforms. These trends address legacy housing stock in urban areas where panel upgrades are costly or delayed.

By Cooktop Size: Three-to-Four-Zone Configurations Dominate Standard Kitchens While Compact Two-Zone Models Capture Urban Micro-Spaces

Three-to-four-zone cooktops, holding 45.40% of the 2025 market share, are the preferred choice for family kitchens. These models fit standard countertop cutouts and allow multi-pot cooking without altering surface layouts. Recent product launches introduced four-zone models with integrated downdraft extraction and improved glass-ceramic finishes, reducing visible scratches and enhancing durability. High-end 80-centimeter platforms focus on quiet operation and larger bridgeable zones, accommodating griddles or oversized cookware in open-plan kitchens. Smart features, such as app control and smart-home hub compatibility, are now available in mid-tier models, increasing value at mainstream price points. These features reinforce the popularity of three-to-four-zone cooktops, offering a balance of capacity, footprint, and installation convenience.

Two-zone cooktops are expected to grow at a CAGR of 8.28% through 2031, driven by demand in micro-apartments and secondary units where compact size and lower electrical loads are essential. Enhanced with silent coil designs and durable surfaces, these cooktops withstand heavy daily use in small spaces. Compact appliances like induction rice cookers complement two-zone models, catering to smaller households and urban lifestyles. Standard-outlet models suit temporary setups, student housing, and rentals where permanent installation is impractical. Five-zone layouts and modular configurations remain relevant for luxury kitchens but are limited to premium budgets due to higher power requirements and costs.

By Distribution Channel: Multi-Brand Stores Leverage Demonstration Advantages While Online Platforms Ride Mobile-Commerce Surge in Asia

Multi-brand stores, accounting for 40.05% of the 2025 market share, emphasize the value of in-person demonstrations. These help consumers understand cookware compatibility, heat responsiveness, and noise profiles before purchasing. Retailers simplify technical features into practical benefits through side-by-side comparisons and expert guides, addressing terms such as flex zones and bridge elements. Physical showrooms are essential for built-in models requiring custom fitting, where advisors assist with ventilation, cabinetry, and electrical considerations. Exclusive brand outlets focus on advanced features and app ecosystems in experiential spaces, enabling buyers to evaluate connected functionalities. This channel strategy ensures informed decisions and aligns assortments with local preferences in the residential induction cooktops market.

Online channels are expected to grow at a 9.16% CAGR through 2031, supported by digital demonstrations, live videos, and bundled promotions that streamline the buying process. Enhanced logistics and installation coordination for free-standing and portable units are driving e-commerce growth, even in areas with limited specialty showrooms. Builder and direct-to-consumer channels are expanding as electrified cooking gains traction through municipal and utility programs. Mid-tier brands rely on marketplace ratings and service plans to assure buyers of reliability at competitive online prices. These trends are shaping a channel mix that balances high-touch showrooms with scalable digital fulfillment in the residential induction cooktops market.

Geography Analysis

Holding 45.40% of the global market share in 2025, the Asia-Pacific region is projected to grow at a CAGR of 8.83% through 2031. This growth is fueled by policy initiatives, increasing urban demand, and a variety of price points that enhance market accessibility. Government programs and electrification roadmaps in South and Southeast Asia are integrating efficient cooking technologies into clean-cooking strategies, particularly in areas with grid access. Demonstration pilots have shown that service quality and time-of-use tariffs significantly influence sustained usage, shaping program designs and hardware specifications. Japan’s established consumer base for electromagnetic cooking, especially induction rice cookers, reflects strong brand leadership. Regional OEM activities and export programs are tailoring product assortments and pricing strategies to suit varying urbanization levels and housing stock, driving the residential induction cooktops market.

Manufacturers in North America are increasingly focusing on localized production of induction ranges and cooktops, driven by trade policies and rebate incentives. GE Appliances has committed USD 3 billion to modernize 11 manufacturing plants across multiple states, creating over 1,000 jobs and boosting domestic production of ranges, cooktops, refrigerators, and other appliances[4]GE Appliances Announces Historic USD3 Billion Investment to Expand U.S. Manufacturing, pressroom.geappliances.com.. State-level funding for lower-voltage induction stoves is improving access for low-income households, while pilot programs are shaping performance and safety standards. Urban jurisdictions embedding electrification into building codes are fostering the adoption of induction, though cultural preferences for gas remain a challenge. These developments are gradually reshaping production footprints, product assortments, and channel strategies, supporting long-term market growth.

Europe has the highest per-capita penetration of induction cooktops, driven by favorable policies, cost-of-ownership benefits, and demand for premium features such as surface durability and silent operation. Long-term cost comparisons often favor induction over gas in many EU countries. Manufacturers are increasing local production of advanced glass-ceramic surfaces to enhance premium finishes and reduce the visibility of scratches. Partnerships between appliance makers and utilities are promoting induction cooking as part of energy-transition campaigns, supported by consumer education and co-branded promotions. While adoption rates vary due to cooking traditions and contractor familiarity, product innovation and regulatory clarity continue to drive market growth.

Competitive Landscape

Regional strengths, investments in component partnerships, and premium design differentiation drive competition in the residential induction cooktops market. European manufacturers lead the built-in premium segment by utilizing locally produced advanced glass-ceramic platforms, ensuring supply chain resilience and superior finishes. North American producers are expanding domestic assembly and product development to align with incentives and reduce tariff exposure. Semiconductor partnerships enable higher-efficiency inverters, quieter operation, and advanced control interfaces, accelerating feature rollouts while maintaining compatibility across connected-home ecosystems.

Strategic initiatives combine design innovation with manufacturing upgrades to support market growth. A US brand's downdraft induction cooktop, recognized at a major industry event, highlights retrofit advantages in challenging ductwork scenarios. A European manufacturer plans to launch matte-finish glass-ceramic surfaces with improved scratch resistance, setting new showroom standards. A leading manufacturer's multi-year US investment in induction capacity reflects alignment with consumer trends and policy incentives. These efforts are supported by R&D in wide-band-gap semiconductors, enhancing efficiency and reducing system size in next-generation platforms.

Emerging ecosystems integrate battery-backed home energy systems to support essential appliances during outages, aligning with portable induction use in regions with grid instability. Compact battery systems can power refrigerators and potentially support portable cooking during disruptions. Appliance makers are strengthening supply commitments and forming channel partnerships in regions where cookware compatibility education is critical. Recognition for high-efficiency portable induction cooktops is growing in off-grid and low-power contexts, emphasizing quick boil times and responsive controls. As suppliers converge on common semiconductor platforms, competition is shifting toward finish quality, acoustic performance, and connected features.

Residential Induction Cooktops Industry Leaders

LG Electronics, Inc.

Whirlpool Corporation

Panasonic Corporation

Robert Bosch GmbH

Electrolux Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Gorenje unveiled its OmniFlex induction cooktops, manufactured in Europe. These cooktops offer matte, scratch-resistant surfaces, integrated downdraft options, exceptional energy efficiency, and rapid InstaDetect pot recognition, ensuring enhanced functionality and durability.

- September 2025: The Miele M Sense intelligent cookware system, showcased at IFA 2025 in Berlin, features pots with touch controls and three temperature sensors. Designed to pair with KM 8000 induction cooktops, it ensures automatic cooking power regulation, preventing boil-overs and eliminating manual heat adjustments.

- August 2025: GE Appliances planned to invest over USD 3 billion in U.S. manufacturing over the next five years. This investment focuses on modernizing and expanding facilities across various states, increasing production, and creating over 1,000 jobs. The initiative aims to strengthen domestic appliance innovation and operations.

Global Residential Induction Cooktops Market Report Scope

The residential induction cooktops market refers to the global industry for electromagnetic cooking appliances designed for household use, offering efficient, safe, and modern alternatives to traditional gas and coil cookers. The market is driven by energy-efficiency regulations, urban adoption of smart kitchens, and government-backed electrification programs, particularly in Asia, alongside declining costs of wide-band-gap power electronics and the rise of micro-living trends that favor portable cooktops. These factors, combined with consumer demand for premium remodels and sustainability-focused appliances, are shaping product innovation and distribution strategies worldwide.

The market is segmented by product type, cooktop size, distribution channel, and geography. By product type, it includes built-in induction cooktops and free-standing or portable induction cooktops, reflecting differences in installation preferences and mobility. By cooktop size, the market is divided into ≤2 zones, 3–4 zones, and ≥5 zones, catering to varied household sizes and cooking requirements. By distribution channel, the market covers multi-brand stores, exclusive brand outlets, online platforms, and other distribution channels, highlighting the balance between traditional retail and digital-first sales. By geography, the market spans North America (United States, Canada, Mexico), South America (Brazil, Peru, Chile, Argentina, and others), Asia-Pacific (India, China, Japan, Australia, South Korea, Southeast Asia, and the rest of Asia-Pacific), Europe (United Kingdom, Germany, France, Spain, Italy, BENELUX, Nordics, and the rest of Europe), and the Middle East & Africa (UAE, Saudi Arabia, South Africa, Nigeria, and others), each region reflecting unique adoption drivers such as electrification policies, premium demand, or affordability constraints. The report offers Market size and forecasts for the Residential Induction Cooktops Market in value (USD Billion) for all the above segments.

| Built-In Induction Cooktops |

| Free-Standing & Portable Induction Cooktops |

| ≤2 Zones |

| 3–4 Zones |

| ≥5 Zones |

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Built-In Induction Cooktops | |

| Free-Standing & Portable Induction Cooktops | ||

| By Cooktop Size | ≤2 Zones | |

| 3–4 Zones | ||

| ≥5 Zones | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and projected growth of the residential induction cooktops market?

The residential induction cooktops market size is estimated USD 17.54 billion in 2026 and is projected to reach USD 23.90 billion by 2031 at a 6.39% CAGR.

Which product type leads and which will grow the fastest through 2031?

Built-in units lead with 57.20% of the 2025 market share, while free-standing and portable formats are forecast to grow at a 7.45% CAGR through 2031.

Which cooktop size segment commands the largest share and which grows fastest?

Three-to-four-zone formats hold 45.40% of the 2025 market share and remain the standard, while two-zone formats are projected as the fastest at an 8.28% CAGR.

Which channel is most important today and which is growing fastest?

Multi-brand stores hold 40.05% of the 2025 market share due to in-person demos, while online channels are projected to grow at a 9.16% CAGR through 2031.

Which region leads the category and what is its growth outlook?

Asia-Pacific leads with 45.40% of 2025 global share and is projected to grow at an 8.83% CAGR through 2031.

What features and innovations are influencing buyer decisions in 2026?

AI-guided cooking, smart-home interoperability, quieter coils, matte-finish glass-ceramic surfaces, and downdraft designs are shaping purchasing choices across budgets.

Page last updated on: