Solar Cooker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

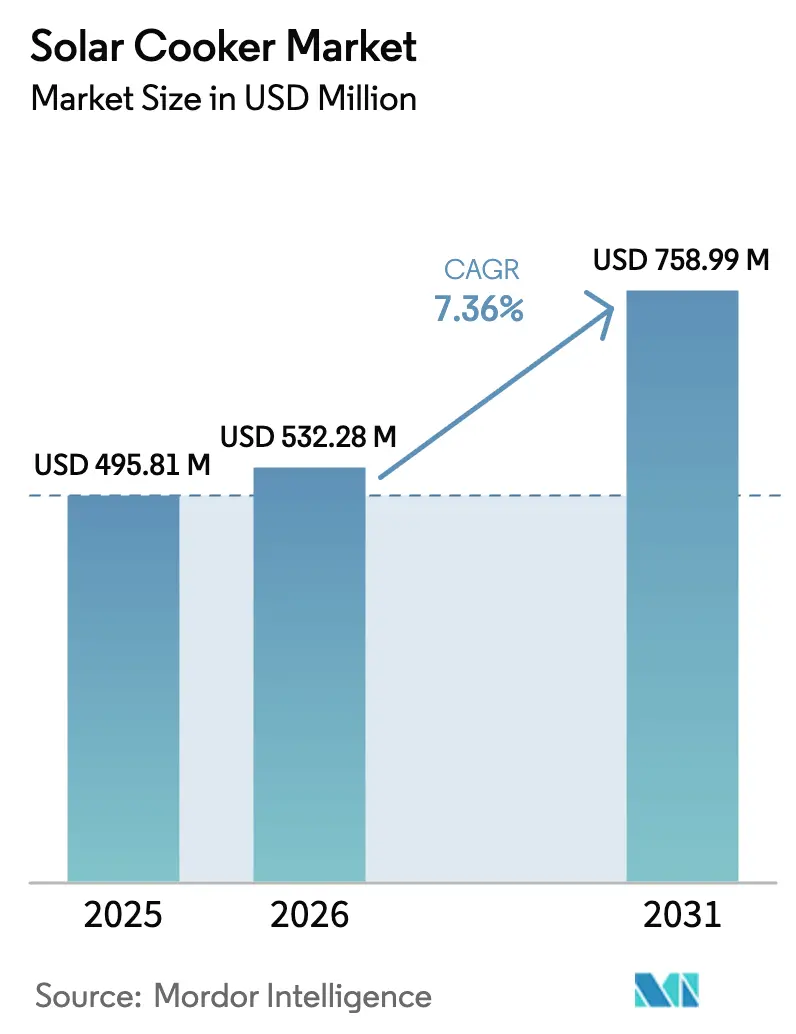

| Market Size (2026) | USD 532.28 Million |

| Market Size (2031) | USD 758.99 Million |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Cooker Market Analysis by Mordor Intelligence

The solar cookers market size was valued at USD 495.81 million in 2025 and estimated to grow from USD 532.28 million in 2026 to reach USD 758.99 million by 2031, at a CAGR of 7.36% during the forecast period (2026-2031). Rising clean-cooking mandates, supportive public policies, and sustained humanitarian procurement combine to accelerate product uptake. Continuous design upgrades—particularly in vacuum-tube and hybrid solar-electric models—elevate cooking temperatures and reduce weather dependence, enhancing user confidence. Institutional buyers increasingly compare the lifetime economics of solar cookers with the healthcare costs of indoor air pollution, strengthening the shift toward cleaner solutions. E-commerce penetration broadens reach into rural and recreational segments, while premium offerings capture consumers willing to invest in reliability and convenience. Technology differentiation, local manufacturing incentives, and evolving micro-finance products further underpin adoption.

Key Report Takeaways

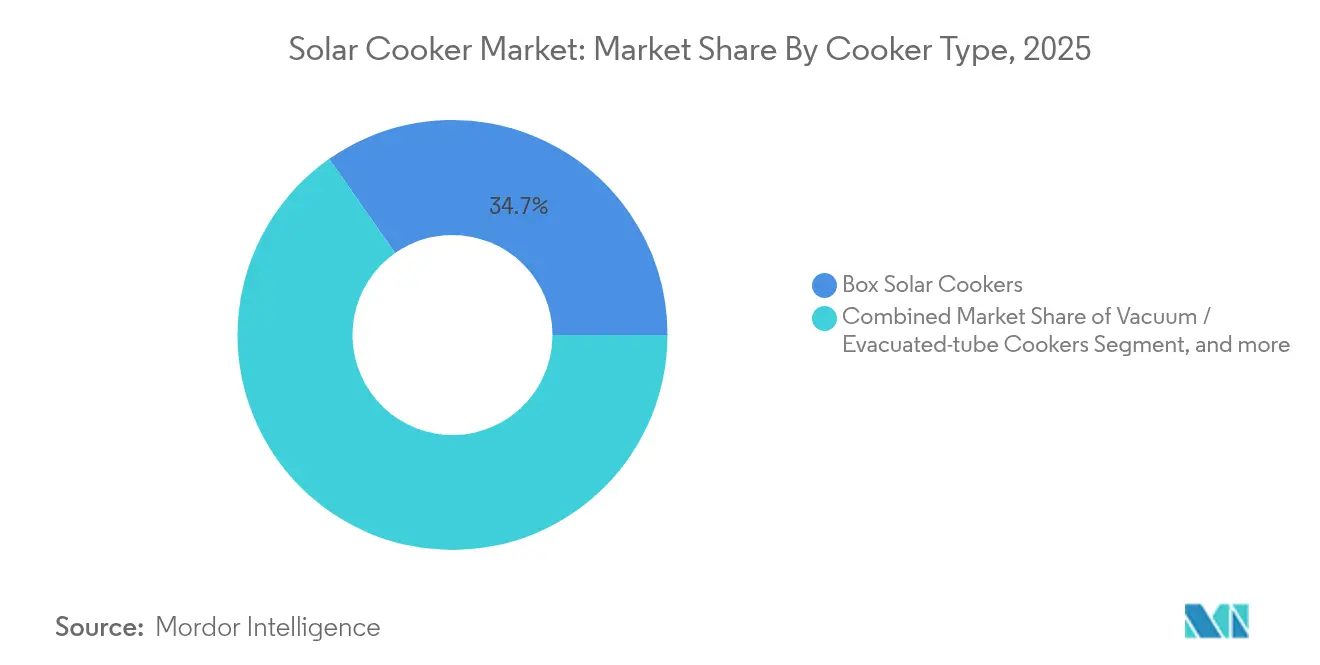

- By cooker type, box cookers led with 34.72% revenue share of the solar cooker market in 2025, whereas vacuum and evacuated-tube designs are projected to expand at a 8.81% CAGR to 2031.

- By end-user, residential consumers held 47.15% demand of the solar cooker market in 2025, while humanitarian and relief camps represent the fastest-growing segment at a 9.46% CAGR through 2031.

- By distribution channel, NGO and aid-agency procurement captured 36.05% of the solar cookers market share in 2025; direct-to-consumer webstores exhibit the highest CAGR at 10.62% to 2031.

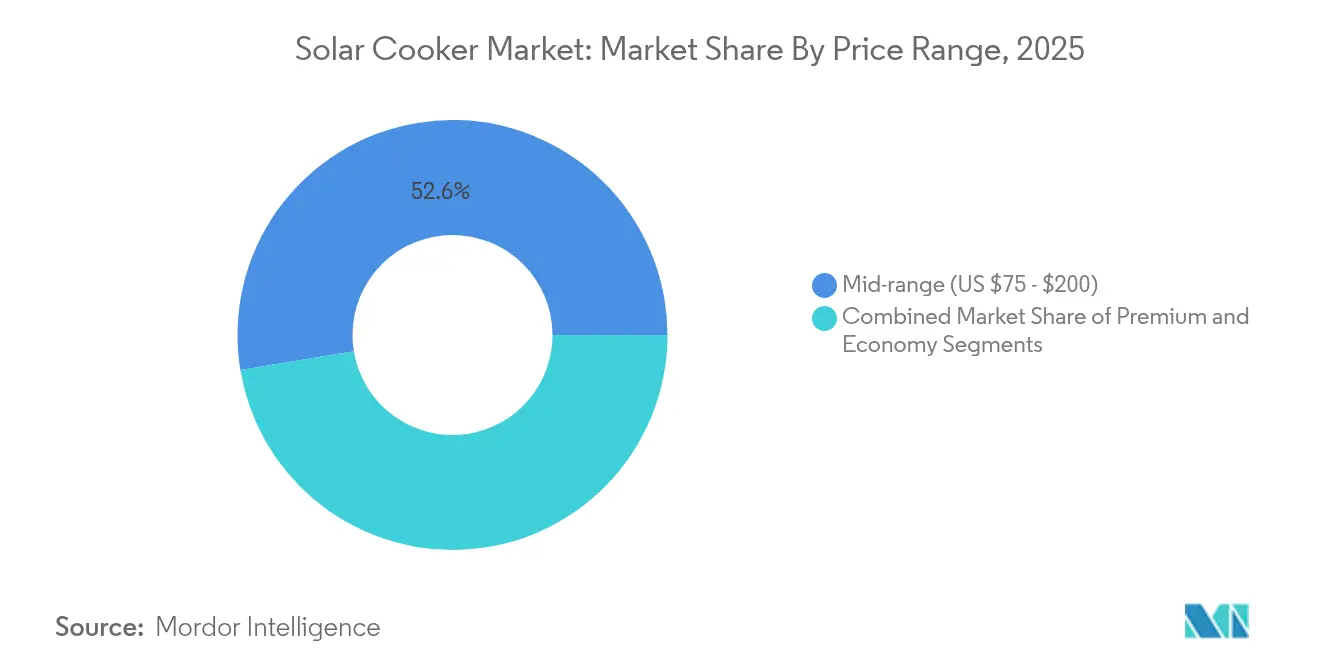

- By price range, the USD 75-200 tier accounted for 52.61% share of the solar cookers market size in 2025, but products priced above USD 200 are advancing at a 8.93% CAGR.

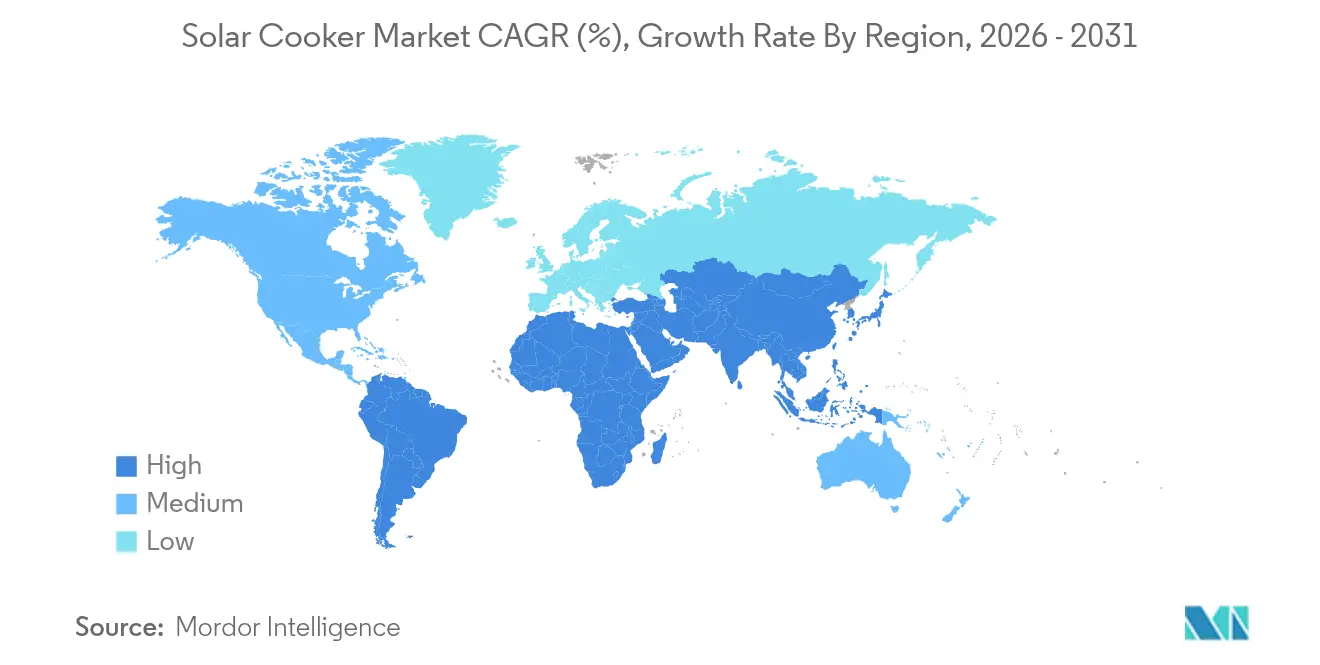

- By geography, Asia-Pacific commanded 42.92% of revenue of the solar cooker market in 2025, while North America is poised for the quickest regional growth at a 9.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Solar Cooker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for clean-cooking solutions | +2.1% | Sub-Saharan Africa & South Asia | Medium term (2-4 years) |

| Government subsidies & clean-cooking programmes | +1.8% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| High-efficiency vacuum tube & parabolic tech | +1.4% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Hybrid solar-electric cookers (PV + battery) | +1.2% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Micro-finance for off-grid e-cooking | +0.9% | Rural Sub-Saharan Africa & South Asia | Long term (≥ 4 years) |

| Community solar-kitchen deployments | +0.7% | Global institutional buyers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Clean-Cooking Solutions

Health-related cost awareness, more than climate sentiment, now drives institutional adoption. The Clean Cooking Declaration at the 2024 UNIDO Summit noted that 2.3 billion people lack modern cooking options and that household air pollution causes millions of deaths annually[1]United Nations Industrial Development Organization, “Clean Cooking Declaration 2024,” unido.org . Hospitals and schools increasingly compare treatment costs for respiratory illness with the two-year payback offered by a quality solar cooker. Multilateral programs such as the Netherlands Enterprise Agency’s Energising Development initiative funnel grants and technical support into early-stage markets. This total-cost-of-ownership lens positions the solar cookers market as an economically rational upgrade rather than an aspirational green purchase.

Government Subsidies & Clean-Cooking Programmes

Policies now integrate manufacturing incentives, financing facilities, and consumer subsidies. India’s Solar Household Scheme and the PM-KUSUM program jointly target 74 GW of distributed capacity, while production-linked incentives lower domestic component costs. Australia’s Small-Scale Renewable Energy Scheme grants tradable certificates and interest-free loans that consumers can bundle with solar cookers. Analysts at IEEFA anticipate that shifting LPG subsidies toward solar-electric cooking could improve India’s energy security [2]Institute for Energy Economics and Financial Analysis, “India’s Clean Cooking Transition,” ieefa.org . Similar policy mosaics across Southeast Asia and parts of Africa shorten the payback window and widen the solar cookers market.

High-Efficiency Vacuum Tube & Parabolic Tech

Double-walled evacuated tubes are now capable of achieving temperatures above 150 °C even in colder climates, effectively addressing the seasonal performance limitations observed in earlier models. The integration of patented light-guide lens technology significantly enhances energy concentration, ensuring consistent performance regardless of the sun's angle. These technological advancements expand the functional capabilities of solar systems, enabling applications such as baking and roasting that were previously constrained. Furthermore, these developments play a pivotal role in addressing cultural preferences for high-heat cooking methods, thereby broadening market acceptance. Collectively, these innovations represent a substantial leap forward in the efficiency and versatility of solar thermal technologies.

Hybrid Solar-Electric Cookers (PV + Small Battery)

Declining photovoltaic (PV) prices and advancements in compact lithium storage technology are driving the adoption of energy units capable of storing midday energy for evening consumption. ATEC's Internet of Things (IoT) stoves capitalize on carbon markets to generate revenue by monetizing up to 10 GWh of clean cooking energy daily, supported by USD 3.75 million secured through Series A funding. GoSun's hybrid oven, designed to reach temperatures of 550°F under sunlight, incorporates a seamless transition to grid or battery power during periods of insufficient sunlight [3]GoSun, “Solar Kitchen Product Specifications,” gosun.co . The combination of revenue from verified carbon credits and enhanced cooking flexibility positions hybrid solar cookers as a premium segment within the solar cookers market. These developments underscore the growing potential of innovative cooking solutions to address both energy efficiency and sustainability goals in the market.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost vs. legacy stoves | -1.9% | Global, sharply felt in low-income regions | Short term (≤ 2 years) |

| Cultural resistance to solar-only cooking | -1.6% | Traditional rural markets worldwide | Long term (≥ 4 years) |

| Quality variance hurting consumer trust | -1.1% | Emerging markets with weak standards | Medium term (2-4 years) |

| LPG / biogas subsidy competition | -0.8% | Asia-Pacific & Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs. Legacy Stoves

In Malawi, the adoption of solar cookers remains limited due to their high upfront costs, despite offering substantial long-term savings. The negligible purchase price of traditional biomass stoves continues to influence consumer preferences, driven by behavioral economics favoring established fuel sources. Although micro-finance initiatives aim to address affordability challenges, the underdeveloped rural banking infrastructure significantly restricts their scalability. Furthermore, in markets where government subsidies reduce the cost of LPG, the economic appeal of solar cookers diminishes, weakening their competitive positioning. To address price sensitivity among consumers, vendors have responded by introducing cost-effective economy models tailored to these segments.

Cultural Resistance to Solar-Only Cooking

In 2024, a survey in Uganda indicated that clean cooking methods had achieved a household penetration rate of only 3.8%, despite the presence of favorable policy initiatives aimed at promoting adoption. The integration of community demonstrations and hybrid systems, which combine solar energy with battery storage, has emerged as a promising approach to address this challenge. However, the transition to clean cooking technologies often requires a phased implementation, where solar solutions are introduced as a supplementary option rather than a complete replacement for traditional methods. This gradual adoption is particularly critical given that evening meal preparation frequently coincides with reduced daylight availability, limiting the effectiveness of solar energy alone. Additionally, the sustained high-heat requirements of certain cuisines, such as frying or simmering, further underscore the need for hybrid systems to meet diverse cooking demands effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooker Type: Vacuum Tubes Drive Technology Evolution

Vacuum and evacuated-tube models are projected to grow at 8.81% annually, while box cookers are expected to hold 34.72% of the solar cookers market in 2025. Evacuated tubes, with double-glazing technology, retain heat to achieve cooking temperatures of 150 °C–290 °C, surpassing box cookers. This performance enhances baking and roasting capabilities, appealing to diverse culinary needs. Panel and parabolic cookers cater to portability and high-temperature requirements but face limited adoption due to complexity and capacity constraints. These factors position vacuum and evacuated-tube models as key players in the solar cookers market.

Hybrid designs combining vacuum tubes with PV panels and batteries are gaining traction. GoSun’s Sport model, which cooks in 20 minutes under sunlight and folds for portability, exemplifies this trend. The shift toward premium, portable solutions reflects evolving consumer preferences and market innovation. As production scales, cost differences between vacuum tube models and box cookers are narrowing. This trend positions vacuum tube models to challenge box cookers’ dominance before 2031, reshaping the competitive landscape.

By End-User: Humanitarian Applications Accelerate Adoption

Residential users generated 47.15% of 2025 revenue, but humanitarian and relief camps showcase the fastest 9.46% CAGR. Coordinated procurement bypasses individual financing hurdles: UNHCR’s 2024 Pakistan project solarized 103 schools and 16 clinics, proving multi-facility viability . Such deployments cut fuel costs and indoor smoke, translating into health and budgetary savings for agencies.

The adoption of solar cookers in the hospitality industry and outdoor event management is driven by the dual objectives of enhancing sustainability credentials and reducing operational expenditures. Military organizations are actively testing lightweight parabolic solar cooker kits to minimize logistical challenges associated with fuel transportation. In residential markets, the increasing visibility of solar cooking in camps and school kitchens is fostering greater acceptance and adoption within surrounding communities. This normalization of solar cooking practices is gradually influencing consumer behavior and promoting sustainable energy solutions. The integration of solar cooking technologies across these sectors highlights a growing trend toward cost efficiency and environmental responsibility.

By Distribution Channel: E-Commerce Transforms Market Access

NGOs and aid agencies accounted for a significant 36.05% market share. However, direct-to-consumer webstores are anticipated to achieve the highest annual growth rate of 10.62%, surpassing all other distribution channels. These online platforms enable manufacturers to directly serve rural and recreational buyers, optimizing supply chain efficiency by minimizing inventory costs. The availability of demonstration videos and peer reviews addresses consumer concerns about product performance, fostering trust in premium-priced models. This shift highlights the growing importance of digital channels in driving market expansion.

Specialty outdoor retailers remain competitive by offering bundled packages that combine solar cookers with camping gear, catering to niche consumer needs. Local workshops continue to thrive by leveraging hands-on demonstrations to convert hesitant households into customers. Hybrid distribution strategies, such as Glenergy’s Kenya-based assembly line, effectively combine advanced technology like GoSun with local labor resources. This approach integrates online marketing with localized support systems, ensuring broader market penetration. Such models underscore the value of blending global innovation with community-level engagement.

By Price Range: Premium Segment Gains Momentum

In 2025, the mid-range segment, priced between USD 75 and 200, dominated the market, capturing 52.61% of the total demand. Premium products priced above USD 200 are anticipated to grow at a robust CAGR of 8.93%, driven by rising disposable incomes, increasing recreational activities, and the appeal of hybrid functionalities. The higher price point is further validated by innovative offerings like GoSun's Solar Kitchen, priced at USD 999, which integrates cooking, cooling, and device charging into a single solution. This trend highlights the growing consumer preference for multifunctional and high-performance products in the solar cookers market. The premium segment's growth underscores the willingness of consumers to invest in advanced technologies that deliver enhanced utility and convenience.

Economy models priced below USD 75 continue to serve as essential solutions for humanitarian initiatives and low-income households, despite ongoing concerns about product quality. As economies of scale drive down the cost of vacuum tube technology, manufacturers are expected to incorporate select premium features into mid-range models. This development is likely to redefine consumer expectations regarding price-performance ratios in the market. The integration of advanced features into more affordable segments could also intensify competition among manufacturers. Consequently, the solar cookers market is poised for significant transformation, with innovation and cost optimization shaping its future trajectory.

Geography Analysis

Asia-Pacific retained 42.92% of global revenue in 2025, supported by government clean-cooking initiatives and vast off-grid populations. Yet cultural cooking preferences and limited financing slow penetration despite national solar targets such as India’s 100 GW mission. China’s dominance in component manufacturing reduces system costs, while Japan and Australia show strong recreational and emergency-preparedness demand, especially for premium hybrids.

North America is forecast to expand 9.78% annually through 2031, the fastest worldwide. Growth stems from outdoor recreation, preparedness culture, and robust e-commerce infrastructure. State-level incentives and public recognition, such as California’s commendation of Solar Cookers International, spur awareness. Rising climate-driven grid concerns prompt homeowners to stock alternative cooking systems, further lifting the solar cookers market size in the region.

Europe, the Middle East, and Africa reveal mixed drivers. EU customers pair sustainability goals with camping lifestyles, whereas refugee and conflict zones in MEA rely on donor-funded installations. The Azraq camp in Jordan demonstrates solar cooking’s social benefits by reducing the need for firewood collection, improving safety, and livelihood security. South America trails but displays latent potential as economic growth and environmental awareness converge.

Competitive Landscape

The market exhibits moderate competition, with the top five brands collectively accounting for approximately half of the total market share. GoSun secures the leading position by leveraging its patented vacuum-tube heat retention technology, a direct-to-consumer sales strategy, and an expanding portfolio of hybrid products. One Earth Designs ranks as a key competitor, focusing on durable solar concentrators designed for institutional cooking applications. Mid-tier companies, including SunFlair, Haines Solar Cookers, and Solar Oven Society, target specific niche markets. These players primarily address demands for portable solutions and community-oriented cooking systems.

R&D investment centers on efficiency gains, hybrid power integration, and user-friendly form factors. Patent filings covering multi-stage thermal storage and advanced light-guide lenses signal an arms race in heat concentration technology. White spaces remain in defense logistics, cold-weather institutional kitchens, and digitally connected stoves that generate carbon credit revenue.

E-commerce erodes traditional entry barriers, allowing regional start-ups to tap overseas demand quickly. Established leaders respond with localized manufacturing—illustrated by GoSun’s partnership with Glenergy in East Africa—and extended product bundles that integrate cooling or charging functions. The solar cookers market thus balances scale economies with room for agile innovators.

Solar Cooker Industry Leaders

GoSun Inc

SunFire Solutions

Global Sun Oven

SunSpot Solar Ovens

Solar Brother (SunChef)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OnePlanet Solar Recycling secured USD 7 million seed funding for a US module recycling plant expected to process 2 million PV panels annually by 2027, enhancing the domestic supply of silicon and aluminum inputs for the solar cookers market, FinSMEs.

- April 2025: Boviet Solar committed USD 294 million to its first US module factory in North Carolina, adding 2 GW capacity that strengthens hybrid cooker component availability Boviet Solar.

- March 2025: OCI and Mission Solar began building a 2 GW cell plant in Texas, expanding the US photovoltaic supply for solar-electric cookers, Solar Power World.

- March 2025: Norway has allocated USD 5.5 million to support a pilot initiative. Under the UNDP Green Energy Recovery Programme in Ukraine, 13 solar power plants are scheduled for deployment in 2025. These installations, strategically placed across 8 hospitals and 5 schools, will deliver a total capacity of 1.1 MW, supported by energy storage systems with a cumulative capacity of 2.3 MWh.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global solar cooker market as all newly manufactured, stand-alone appliances that convert direct solar radiation into heat for food preparation through box, panel, parabolic, evacuated-tube, or hybrid solar-electric designs sold to residential, commercial, institutional, and humanitarian users.

Scope exclusion: industrial solar concentrator fields built mainly for thermal power generation or bulk steam production sit outside this analysis.

Segmentation Overview

- By Cooker Type

- Box Solar Cookers

- Panel Solar Cookers

- Parabolic / Concentrating Cookers

- Vacuum / Evacuated-tube Cookers

- Solar-Electric (PV-powered) Cookers

- By Price Range

- Economy (Less than USD 75)

- Mid-range (USD 75 – USD 200)

- Premium (More than 200)

- By End-User

- Residential

- Commercial (Hospitality, Catering, Outdoor Events)

- Institutional (Schools, Hospitals, Prisons)

- Humanitarian & Relief Camps

- Military & Defense

- By Distribution Channel

- Online Retail Marketplaces

- Specialty Outdoor Retailers

- NGO & Aid-Agency Procurement

- Direct-to-Consumer Webstores

- Local Workshops & Informal Networks

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview cooker makers, NGO procurement officers, rural micro-finance lenders, and campsite retailers across Asia-Pacific, Africa, Europe, and the Americas.

These conversations validate penetration rates, seasonal usage patterns, and ASP movement, filling gaps that desk work alone cannot.

Desk Research

We first map addressable demand using tier-1 public sources such as IRENA renewables capacity tables, Clean Cooking Alliance adoption surveys, WHO indoor-air-pollution statistics, national customs import files, and peer-reviewed journals on solar thermal efficiency.

Company filings, patent families gathered via Questel, and shipment news in Dow Jones Factiva reveal manufacturer counts, average selling prices, and trade lanes.

Next, our analysts layer country-level solar-insolation grids, LPG price indices, and off-grid population figures to size the potential pool before aligning it with supplier disclosures.

D&B Hoovers revenue splits let us benchmark channel mixes.

The list above is illustrative, and many additional open and subscription datasets inform the evidence stack.

Market-Sizing & Forecasting

We apply a top-down build that starts with households and institutions lacking clean-cooking options, adjusts them by solar-radiation hours, disposable-income brackets, and subsidy coverage, and then multiplies by verified penetration rates.

Select bottom-up checks using supplier shipment totals and sampled ASP × volume refine the output.

Key variables include global horizontal irradiance, LPG price inflation, NGO funding flows, e-commerce solar-appliance sales, and rural electrification pace.

A multivariate regression links these drivers to historic uptake, while ARIMA overlays capture short-run seasonality.

Where shipment data are sparse, proportional allocation from export manifests bridges gaps.

Data Validation & Update Cycle

Before sign-off, outputs pass three-layer variance screening, peer review, and at least one reconfirmation call.

Mordor Intelligence refreshes every twelve months and issues interim updates whenever subsidies, duties, or major product launches materially shift the baseline.

Why Mordor's Solar Cooker Baseline Earns Unmatched Trust

Published estimates often diverge because some studies mix solar water heaters, count second-hand units, or apply blanket rural adoption targets.

Our disciplined scope, annual refresh, and dual-track modeling keep numbers transparent.

Key gap drivers include inclusion of hybrid PV cooktops, use of uniform ASPs without regional weighting, and static exchange-rate assumptions in other studies, whereas Mordor updates currency and inflation quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 495.8 M (2025) | Mordor Intelligence | - |

| USD 445.0 M (2024) | Regional Consultancy A | Excludes humanitarian procurement and relies on online retail sales only |

| USD 2.05 B (2023) | Global Consultancy B | Counts solar water heaters and lacks ASP regionalization |

| USD 1.80 B (2024) | Industry Journal C | Converts shipment tonnage to value with generic price multipliers |

The comparison shows that Mordor's balanced, variable-rich model delivers a dependable baseline clients can trace back to explicit scope choices and repeatable calculations.

Key Questions Answered in the Report

What is the current global solar cookers market size?

The solar cookers market size stands at USD 532.28 million in 2026 and is on track to hit USD 758.99 million by 2031.

Which region leads the solar cookers market in revenue?

Asia-Pacific holds the largest share at 42.92% of 2025 revenue, driven by clean-cooking policies and a sizable off-grid population.

Which cooker type is growing fastest?

Vacuum and evacuated-tube cookers post the highest growth, expanding at a 8.81% CAGR through 2031 due to higher thermal efficiency.

Who are the main players in the market?

GoSun, with a commanding share, is followed closely by One Earth Designs, and together they account for nearly one-third of global sales.

Why are hybrid solar-electric cookers gaining popularity?

Falling PV prices and compact batteries allow cooking after sunset and under cloudy skies, addressing the primary limitation of solar-only models.

What restrains wider adoption of solar cookers?

High upfront costs, cultural cooking preferences, and competition from subsidized LPG can slow uptake, especially in low-income markets.

Page last updated on: