Release Liners Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.21 Billion |

| Market Size (2031) | USD 24.76 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Release Liners Market Analysis by Mordor Intelligence

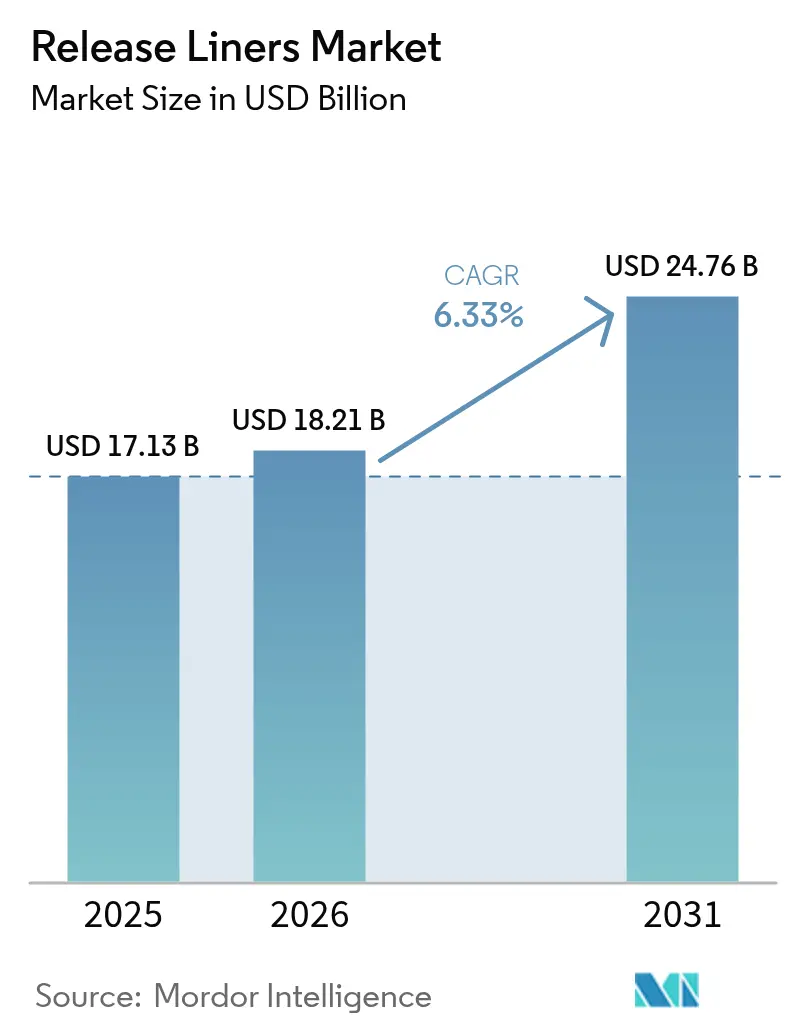

The Release Liners Market size was valued at USD 17.13 billion in 2025 and estimated to grow from USD 18.21 billion in 2026 to reach USD 24.76 billion by 2031, at a CAGR of 6.33% during the forecast period (2026-2031). Steady demand stems from e-commerce logistics, premium food packaging, and advanced industrial tapes, all of which require consistent release performance and tight dimensional tolerances. Labels remain the anchor application, yet medical devices, prepreg composites, and battery cell tapes are expanding faster and reshaping the product mix toward higher-margin, technology-intensive constructions. Asia-Pacific’s dual leadership in volume and growth reinforces production scale advantages while exposing Western brand owners to supply-chain concentration risks. Material innovation is accelerating: glassine paper still dominates, but filmic and poly-coated alternatives are growing quickly as converters seek moisture, heat, and chemical resistance without sacrificing recyclability.

Key Report Takeaways

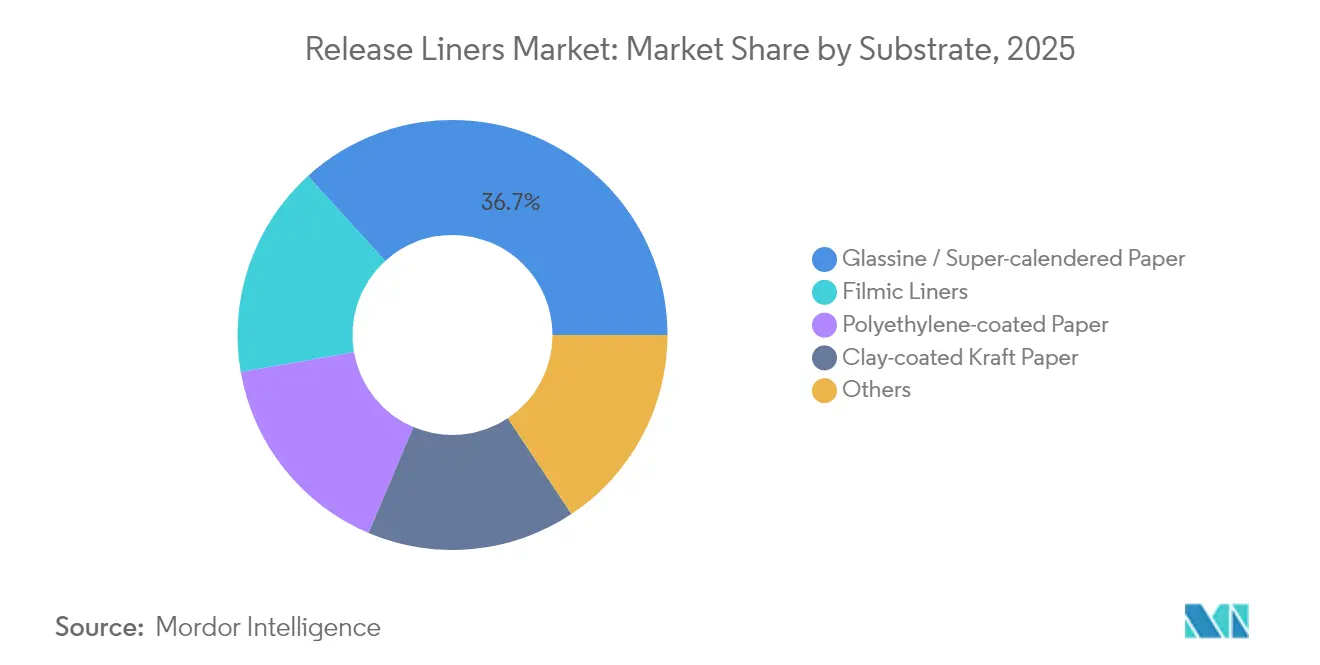

- By substrate, glassine/super-calendered paper led with 36.74% of release liner market share in 2025; filmic liners are forecast to expand at a 7.62% CAGR through 2031.

- By release agent, silicone chemistry retained 80.65% revenue share in 2025, while fluoropolymer systems are projected to grow at a 7.42% CAGR to 2031.

- By application, labels commanded 60.20% of the release liner market size in 2025; medical applications are set to grow fastest at a 7.65% CAGR to 2031.

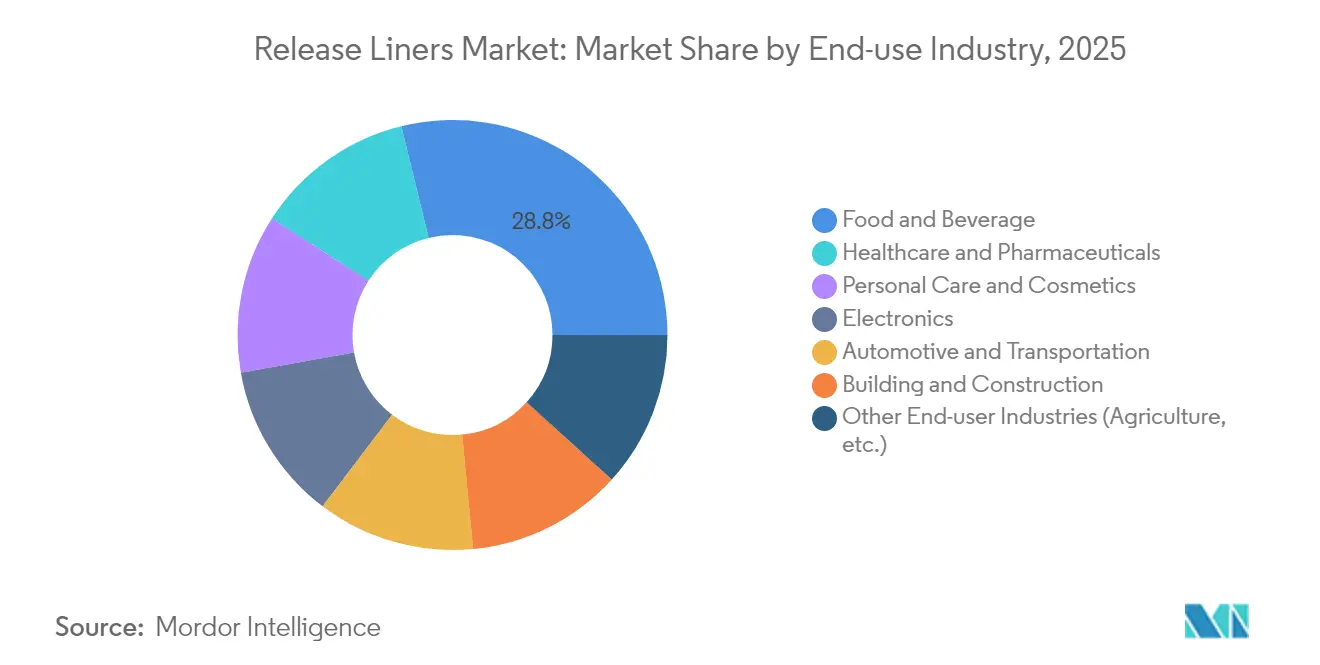

- By end-use industry, food and beverage held 28.83% of the 2025 release liner market size, whereas healthcare and pharmaceuticals are advancing at an 7.78% CAGR through 2031.

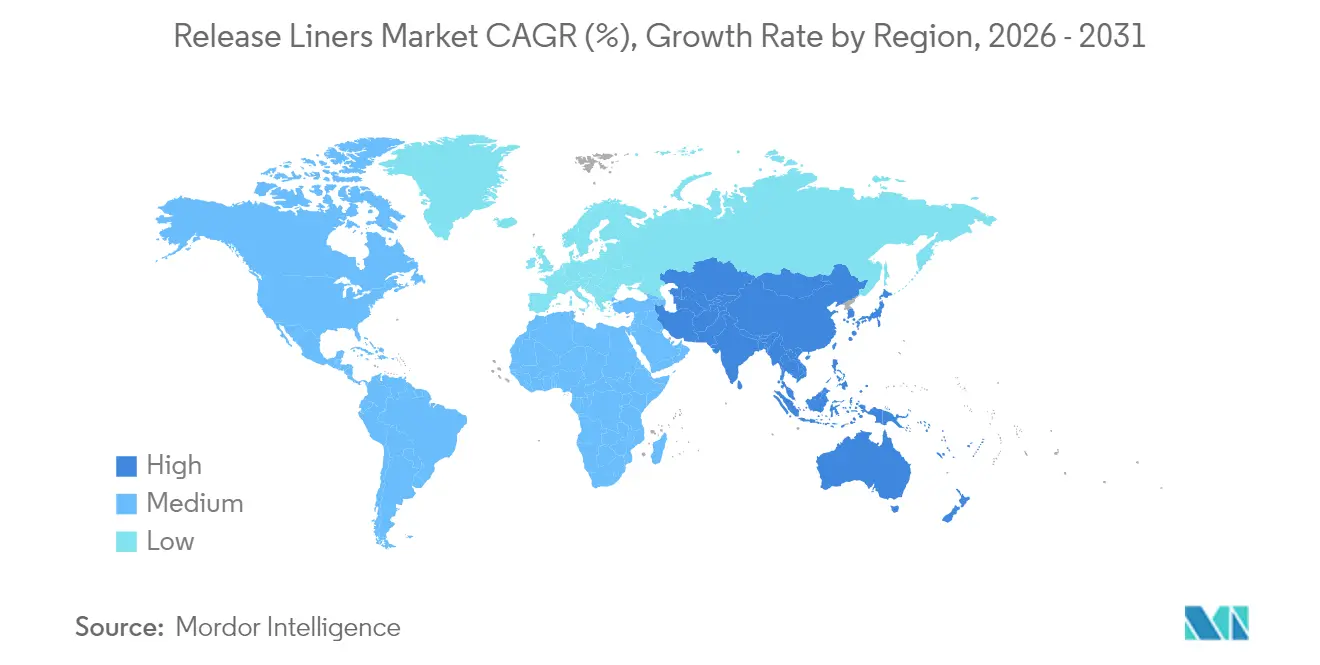

- By geography, Asia-Pacific captured 42.40% revenue share in 2025 and is forecast to expand at a 7.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Release Liners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Clean-Label Packaging in Food and Beverage | +1.8% | North America, EU, global roll-out | Medium term (2-4 years) |

| E-commerce Boom Accelerating Label Demand | +2.1% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Uptake of Premium Hygiene and Medical Tapes | +1.4% | Developed markets worldwide | Medium term (2-4 years) |

| Aerospace and Wind Prepregs Needing Specialty Liners | +0.9% | North America, EU, expanding Asia-Pacific | Long term (≥ 4 years) |

| Electric Vehicles Battery Cell Electrode Tapes Adoption | +1.2% | Asia-Pacific core, global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Clean-Label Packaging in Food and Beverage

Food and beverage brand owners are replacing bleached substrates and solvent-based coatings with unbleached glassine, water-borne silicones, and compostable chemistries that meet direct-food-contact rules. LINTEC’s natural-tone glassine illustrates the pivot toward minimally processed papers that enable gravure print fidelity while eliminating optical brighteners [1]LINTEC, “Natural Glassine Papers for Food Applications,” lintec.com. Functional performance now extends to barrier protection against grease and moisture, permitting clear ingredient transparency without adhesive migration. Converters able to document traceability capture price premiums as retailers tighten sustainability scorecards. Demand for PFAS-free systems is spreading from the EU to North America, pushing suppliers to scale fluorine-free alternatives that still release cleanly at high application speeds. With food and beverage holding 29.26% share in 2024, iterative material upgrades ripple quickly across global volumes and reinforce supplier qualification hurdles.

E-commerce Boom Accelerating Label Demand

Parcel volumes continue rising with click-and-collect, subscription, and same-day delivery models. Release liners must perform across automated print-apply lines that exceed 150 m/min, handle variable-data barcoding, and endure cold-chain swings from −20 °C to 40 °C. Consistent release force and web flatness minimize downtime and misapplies, directly influencing fulfillment cost per package. Premium unboxing trends now extend to omnichannel grocery and personal-care shipments, boosting demand for multi-layer labels with tactile varnishes and metallic accents. These constructions rely on precision-coated liners to protect ink integrity until point-of-use. The release liner market, therefore, sees volume gains plus a value shift toward high-spec paper and film backings optimized for robotics and vision inspection equipment.

Uptake of Premium Hygiene and Medical Tapes

Chronic-care products, transdermal drug patches, and wearable sensors require hypoallergenic adhesives paired with liners with low extractables and occlusive barriers. Recent patents covering corticosteroid-loaded adhesive matrices show how release layers must preserve active stability yet peel cleanly for dose accuracy. Hospitals are adopting breathable tapes with micro-perforated liners that support moisture vapor transmission while maintaining sheath integrity until application. Global aging demographics and home-care reimbursement fuel volume, while strict ISO 10993 biocompatibility testing narrows the qualified supplier base. These factors underpin the 7.91% CAGR projected for medical uses, delivering outsized margin upside for converters mastering clean-room coating and in-line vision inspection.

Aerospace and Wind Prepregs Needing Specialty Liners

Composite airframes, space structures, and multi-megawatt wind blades cure at up to 180 °C and demand liners that neither shrink nor embrittle. Hexcel’s HexPly systems rely on high-stability PET and polyimide liners that maintain planarity throughout autoclave cycles. In wind energy, larger blade molds require uninterrupted release sheets exceeding 60 m, underscoring the importance of low-defect roll stock. The transition to bio-epoxy and natural-fiber prepregs adds chemical variability, putting pressure on liner suppliers to validate release performance across new resin chemistries. Such qualification programmes lock in multi-year supply positions, creating durable revenue streams despite the composite sector’s cyclical order patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Release-liner Waste Disposal | −0.8% | EU leading, global uptake | Medium term (2-4 years) |

| Volatile Pulp & Silicone Prices | −1.1% | Worldwide, cost-sensitive users | Short term (≤ 2 years) |

| Shift to Linerless Labelling | −0.6% | North America, EU first movers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Release-Liner Waste Disposal Challenges

Used liner is largely landfilled because silicone residues impede standard recycling. FINAT’s CELAB-Europe consortium aims for 75% recycling by 2025, but progress hinges on collection logistics and end-market demand for recovered fibers. Western Michigan University’s water-soluble barrier layer enables silicone removal during pulping, yet commercial adoption remains limited by process retrofits and bale transport costs. Sustana Group’s Wisconsin plant shows technical feasibility, but its geographic reach is narrow. As Extended Producer Responsibility schemes spread, converters face escalating fees that erode price competitiveness versus linerless or reusable formats.

Volatile Pulp and Silicone Raw-Material Prices

Softwood pulp prices fluctuate with housing starts and currency shifts, stressing margins for glassine and clay-coated kraft producers. Statistics Canada recorded a 4.9% year-over-year rise in industrial chemical indices in February 2025, amplifying silicone elastomer costs [2]Statistics Canada, “Industrial Product Price Index, February 2025,” statcan.gc.ca. Automotive electrification and solar encapsulant demand tighten supply of base siloxanes, forcing smaller coaters to ration volumes or accept spot premiums. Although bio-based waxes and 5-HMF-derived resins show promise, qualification cycles are lengthy and unit costs remain above incumbent inputs. Volatility therefore prompts forward-buying and index-linked contracts that complicate long-term pricing to end users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Glassine Paper Dominance Faces Innovation Pressure

Glassine retained 36.74% share of release liner market size in 2025 and continues to anchor high-volume label and tape programs thanks to cost efficiency, surface smoothness, and FDA food-contact clearances. Yet growth moderates as brand owners specify lower-grammage liners to cut freight emissions, eroding tonnage even where square-meter demand rises. Polyethylene-coated kraft papers are gaining in chilled-food and outdoor labeling where moisture resistance outperforms uncoated grades. Filmic liners made from BO-PET and BOPP are expanding quickly in electronics, aerospace, and automotive laminates that cure at temperatures beyond the glass-transition point of cellulosic papers.

Alternative substrates inside the “Others” category are setting the pace: bi-axially oriented polyamide, PTFE-coated glass cloth, and micro-fibrillated cellulose composites deliver multi-functional properties such as anti-static release, thermal stability above 260 °C, and repulpability. Adoption remains niche yet lifts average selling price because converters implement multi-pass coating lines and inline plasma treatments to anchor release agents. Glassine suppliers are responding with barrier-enhanced variations—unbleached, metallized, or calcium-carbonate-filled—aimed at clean-label packaging. These iterative shifts ensure glassine stays relevant while ceding the fastest growth slices to engineered films.

By Release Agent: Silicone Leadership Challenged by Fluoropolymer Innovation

Silicone systems controlled 80.65% of the 2025 release liner market, supported by versatile cure chemistries, low surface energy, and abundant supply of base siloxanes. Platinum-catalyzed UV silicones shorten cure windows, enabling high-speed 1,000 m/min coating that sustains price competitiveness. The release liner market size for fluoropolymer-based agents is smaller yet advancing at 7.42% CAGR because perfluorinated chains deliver chemical inertness and ultra-low release force vital in high-temperature composite molds and aggressive adhesive tapes.

Regulatory pressure on PFAS chemicals is fostering a split: legacy fluoro-silicones for aerospace retain demand, while packaging and hygiene sectors shift toward acrylic or polyolefin release varnishes. Suppliers such as Hightower Products now market PFAS-free formulations customized by viscosity and anchorage resins, balancing clean release with recyclability. Silicone producers answer with controlled-migration grades that minimize siloxane transfer onto optical films and semiconductor wafers. Competitive advantage hinges on analytical capability to verify sub-ppm migration and accelerate customer qualification.

By Application: Labels Dominance Supported by E-commerce Growth

Labels contributed 60.20% of 2025 revenue and continue to underpin baseline volumes for every major coater. Automated fulfillment centers require liners with uniform thickness and tight caliper profiles so that high-speed applicators maintain 0.2 mm registration accuracy. Specialty converters are layering tactile soft-touch lacquers and foil accents that demand ultra-flat liners to avoid air entrapment, elevating value per square meter. The labels segment alone accounted for 60.20% of release liner market share in 2025, illustrating its centrality to growth.

Medical uses, although only mid-single-digit share today, are outpacing overall growth at 7.65% CAGR. Transdermal patches, hydrocolloid dressings, and microfluidic test strips all require low-surface-energy liners formulated for gamma or ethylene-oxide sterilization without fogging. Graphics applications draw benefit from latex and UV-inkjet printers that favor removable decals, yet face substitution risk from direct-print technologies in retail décor. The tapes sector, ranging from construction flashing to consumer electronics assembly, remains fragmented; yet EV battery and 5G smartphone designs demand flame-retardant liners exhibiting zero ionic contamination.

By End-use Industry: Healthcare Acceleration Challenges Food and Beverage Leadership

Food and beverage held 28.83% share of the 2025 release liner market size, generated by pressure-sensitive labels, lidding films, and bakery release sheets that require FDA and EU Regulation 1935/2004 compliance. Clean-label and allergen-free claims are prompting shorter ingredient lists on decorative labels, spurring high-resolution variable printing that benefits from premium liners. Meanwhile, healthcare and pharmaceuticals, forecast at an 7.78% CAGR, are driving qualification projects for breathable polyurethane and silicone gel dressings.

Personal care and cosmetics leverage premium packaging aesthetics—metallic foils, embossing, holographic films—that demand optically flawless liners. Automotive and transportation applications are entering a material transition: battery module bonding tapes, EMI shielding fabrics, and lightweight composite body panels all specify release liners with elevated thermal resistance. Electronics manufacturers use anti-static film liners in flexible circuit production to prevent dust adhesion and electrostatic discharge. Building and construction remains cyclical, yet membrane roofing and acrylic structural glazing tapes provide niche expansion paths when residential starts recover.

Geography Analysis

Asia-Pacific dominated with 42.40% market share in 2025 and is projected to grow at a 7.31% CAGR through 2031, underpinned by the region’s vertically integrated pulp-to-coating supply chain and expanding middle-class consumption. China accounts for the bulk of incremental tonnage as packaging converters ramp capacity near e-commerce fulfilment hubs, while Japan and South Korea specialize in high-precision liners for semiconductor fabs and battery cell assembly. Government incentives for renewable energy also lift demand for prepreg liners in wind-blade production.

North America preserves a sizeable installed base in aerospace, medical device, and quick-service restaurant packaging. The United States is the hub for FDA-cleared medical tape development, benefiting from clusters around Minnesota, Massachusetts, and California. Canada leverages abundant forest resources to promote FSC-certified glassine and clay-coated kraft, aligning with retailer sustainability mandates. Mexico’s near-shoring boom encourages multinationals to co-locate RFID, label, and filmic coating facilities close to automotive and consumer-electronics plants; Avery Dennison’s USD 100 million investment testifies to this momentum.

Europe remains the regulatory vanguard, driving circularity targets that reward suppliers able to certify post-consumer liner recycling rates. Germany spearheads industrial tape innovation linked to automotive lightweighting, whereas Italy and France capitalize on luxury packaging where small-batch, high-finish labels command premium liners. Nordic countries influence global material standards by mandating PFAS phase-outs and promoting bio-based alternatives. Eastern Europe serves as a cost-effective production corridor supplying the EU single market, though geopolitical tensions occasionally disrupt feedstock logistics.

Competitive Landscape

The Release Liners Market is moderately consolidated, with the five largest players controlling most worldwide revenue. 3M, Avery Dennison Corporation, LINTEC Corporation, UPM, and Loparex are the major players in the market. Strategic focus areas include sustainability and automation readiness. 3M’s public pledge to exit PFAS manufacturing by 2025 catalyzes supplier realignment toward fluorine-free release agents. Emerging disruptors include companies developing linerless alternatives and circular economy solutions, with Avery Dennison Corporation's micro-perforation technology achieving 30% CO2 reduction and 40% water usage decrease. Partnership models are rising between substrate makers and recycling innovators to co-develop closed-loop take-back schemes.

Release Liners Industry Leaders

Loparex

3M

Avery Dennison Corporation

LINTEC Corporation

UPM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Techlan unveiled its latest product: a 100% recycled release liner. The 60gsm Honey glassine, crafted entirely from recycled materials, boasts a 67% smaller CO2 footprint than its traditional counterparts.

- February 2024: Mondi enhanced the circularity of material flows at its release liner production sites in Germany and the Netherlands. Through strategic partnerships, the company now channels 95% of its production waste as secondary raw material for various industries.

Global Release Liners Market Report Scope

Release liners are coated films that are mainly used to protect a sticky surface from releasing early. These are extensively used in several applications owing to their cleanliness and ease of removal. They mainly support laminated films, ceramics, cast foams, and coated adhesives. It has different substrates, such as film-based, paper-based, poly-coated-based, etc.

The market is segmented based on application and geography. By application, the market is segmented into labels, graphics, tapes, medical, industrial, and other applications. The report offers market size and forecasts for 15 countries across major regions.

For each segment, market sizing and forecasts have been done on the basis of revenue (USD) for all the above segments.

| Glassine / Super-calendered Paper |

| Polyethylene-coated Paper |

| Filmic Liners |

| Clay-coated Kraft Paper |

| Others (Poly-coated Biaxially Oriented Polyethylene Terephthalate (BO-PET) film, etc.) |

| Silicone |

| Fluoropolymer |

| Non-silicone (Acrylic, Others) |

| Labels |

| Graphics |

| Tapes |

| Medical |

| Industrial |

| Other Applications (Hydiene Products, etc.) |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Automotive and Transportation |

| Electronics |

| Building and Construction |

| Other End-user Industries (Agriculture, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Substrate | Glassine / Super-calendered Paper | |

| Polyethylene-coated Paper | ||

| Filmic Liners | ||

| Clay-coated Kraft Paper | ||

| Others (Poly-coated Biaxially Oriented Polyethylene Terephthalate (BO-PET) film, etc.) | ||

| By Release Agent | Silicone | |

| Fluoropolymer | ||

| Non-silicone (Acrylic, Others) | ||

| By Application | Labels | |

| Graphics | ||

| Tapes | ||

| Medical | ||

| Industrial | ||

| Other Applications (Hydiene Products, etc.) | ||

| By End-use Industry | Food and Beverage | |

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Automotive and Transportation | ||

| Electronics | ||

| Building and Construction | ||

| Other End-user Industries (Agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the release liner market?

The Release Liners Market size is expected to reach USD 18.21 Billion in 2026 and grow at a CAGR of 6.33% to reach USD 24.76 Billion by 2031.

Which substrate segment holds the largest share?

Glassine/other super-calendered papers held 36.74% of global revenue in 2025, remaining the dominant substrate despite share pressure from filmic alternatives.

Why are medical applications growing faster than other segments?

Regulatory demand for biocompatible materials, the rise of wearable drug-delivery patches, and aging populations are driving a 7.65% CAGR for medical uses through 2031.

How significant is Asia-Pacific in the release liner market?

Asia-Pacific commanded 42.40% revenue share in 2025 and is the fastest-growing region at a projected 7.31% CAGR, benefiting from integrated supply chains and expanding consumer markets.

What are the main sustainability challenges for release liners?

Waste management tops the list because silicone-coated liners are hard to recycle; Extended Producer Responsibility schemes in the EU are pushing suppliers toward recyclable, compostable, or linerless solutions.

Page last updated on: