Market Overview

| Study Period | 2020 - 2031 |

|---|---|

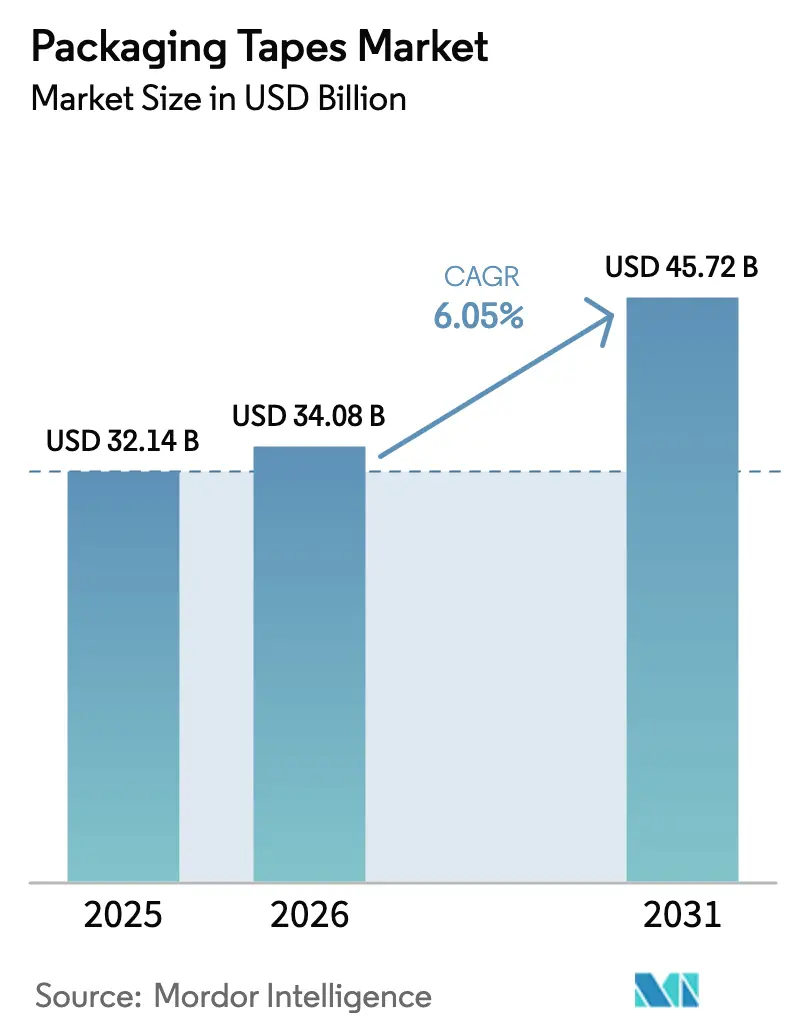

| Market Size (2026) | USD 34.08 Billion |

| Market Size (2031) | USD 45.72 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Tapes Market Analysis by Mordor Intelligence

Packaging Tapes Market size in 2026 is estimated at USD 34.08 billion, growing from 2025 value of USD 32.14 billion with 2031 projections showing USD 45.72 billion, growing at 6.05% CAGR over 2026-2031. This trajectory mirrors rapid e-commerce parcel growth, steady cold-chain expansion, and automation investments that streamline case-sealing operations. Brand owners are installing right-sized carton lines that trim 10 to 50 cents of material per parcel while lifting throughput, which keeps the packaging tapes market on a predictable growth path. Plastic-based tapes still dominate daily fulfillment tasks, yet paper tapes are gaining traction as OECD plastic-tax regimes reshape cost models and corporations target recycled-content thresholds. Asia Pacific remains the epicenter for capacity additions, aided by India’s push to scale its USD 200 billion packaging sector and China’s electronics boom that relies on pressure-sensitive seals for static-sensitive parts.

Key Report Takeaways

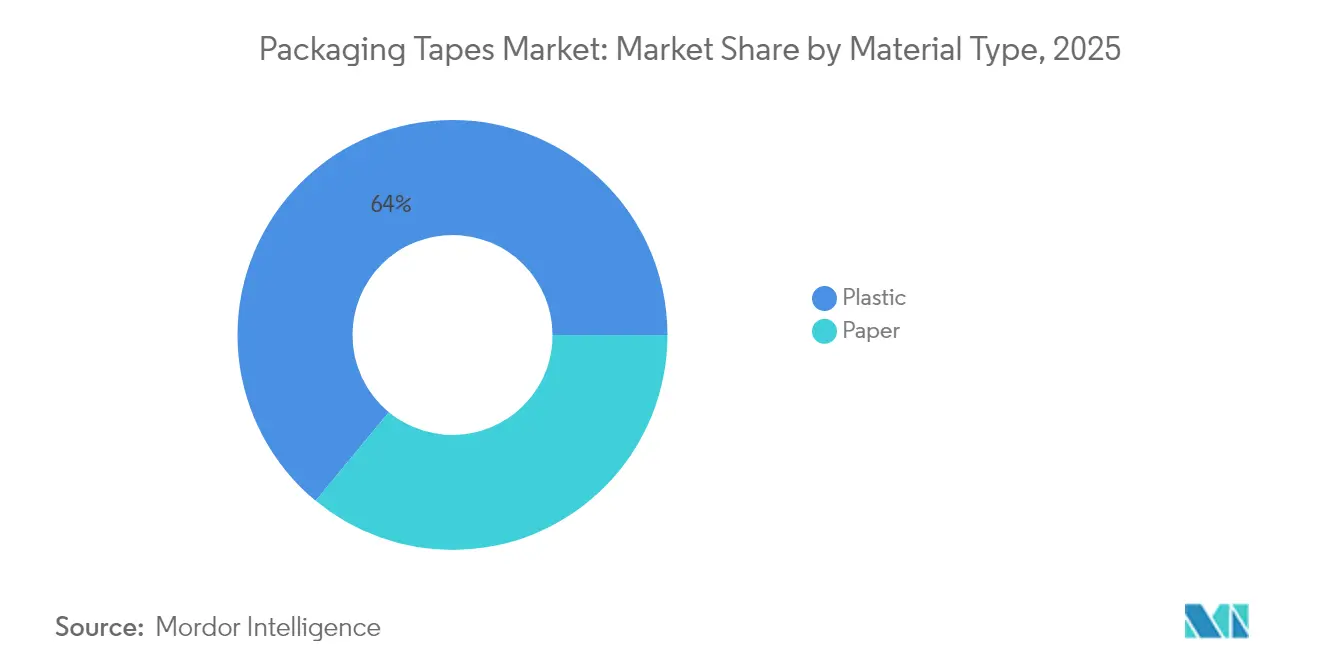

- By material type, plastic substrates led with 64.02% of the packaging tapes market share in 2025, while paper tapes are poised to grow at a 6.79% CAGR through 2031.

- By adhesive type, acrylic systems commanded 44.12% share of the packaging tapes market size in 2025; rubber-based chemistries record the fastest 6.58% CAGR.

- By product form, strapping and bundling lines captured 58.63% revenue share in 2025; carton-sealing tapes are projected to expand at 6.83% CAGR.

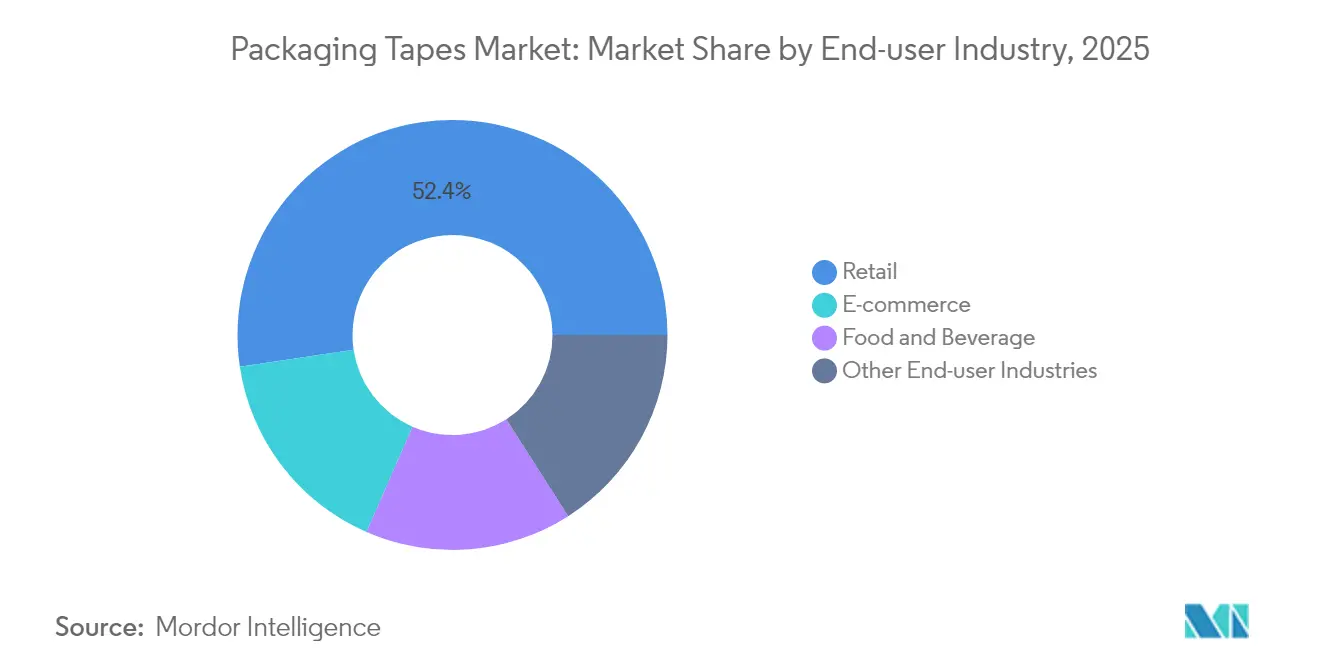

- By end-user industry, retail accounted for 52.35% of the packaging tapes market size in 2025, whereas e-commerce is advancing at a 6.88% CAGR.

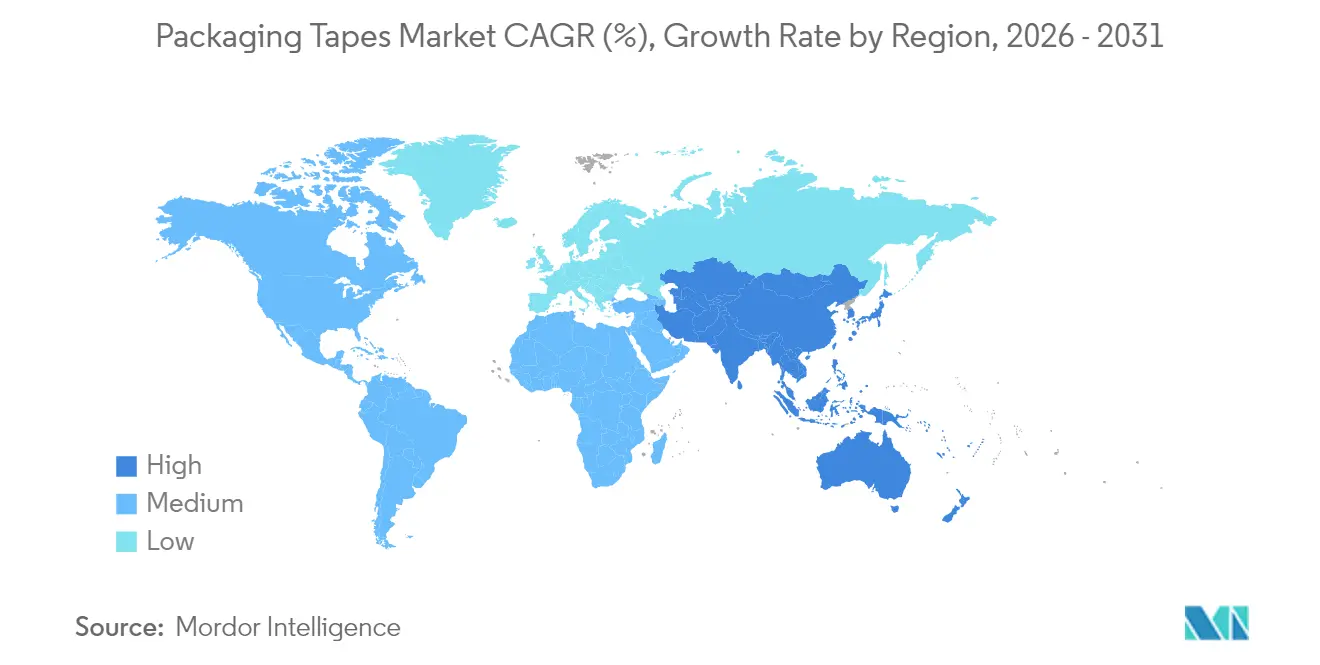

- By geography, Asia Pacific held a 39.10% share in 2025 and is expected to grow at a 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaging Tapes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce carton-volume boom in Tier-2 and Tier-3 cities | +1.8% | Asia Pacific, Latin America | Medium term (2-4 years) |

| Demand spikes from temperature-controlled grocery fulfillment centers | +1.2% | Global; early gains in North America, Europe | Short term (≤ 2 years) |

| Shift from manual to automated case-sealing lines | +1.5% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Retailers’ private-label expansion in emerging markets | +0.9% | Asia Pacific, Latin America, MEA | Long term (≥ 4 years) |

| OEM specification of quiet-release tapes for worker safety | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Carton-Volume Boom Drives Tier-2 and Tier-3 Penetration

Secondary-city logistics hubs in India, Brazil, and Indonesia are becoming critical nodes in e-commerce networks. India’s e-commerce packaging spending is projected to climb from USD 451.4 million in 2019 to USD 975.4 million in 2025, raising localized demand for pressure-sensitive seals[1]Indian Brand Equity Foundation, “Indian E-commerce Logistics Outlook,” ibef.org. Fulfillment centers are pairing machine-learning box-sizing algorithms with paper-reel dispensers that cut corrugate usage by 35% in North America and Europe. These installations reduce void fill, shorten pick times, and sustain double-digit parcel throughput, spurring procurement managers to lock in long-term tape contracts. Asian suppliers such as tesa have opened Mumbai and Bengaluru service hubs to stay within 24-hour reach of electronics OEMs now shifting to tier-2 industrial corridors.

Demand Spike from Temperature-Controlled Grocery Fulfillment Centers

Supermarket chains are rolling out micro-fulfillment assets that must keep perishables between -25 °C and +8 °C across last-mile routes. UPS added four Temperature True lines in 2024, tailoring Med 100 cartons for ambient medicines and Med 400 for frozen biologics. These box styles need acrylic or rubber adhesives that retain tack below -20 °C, prompting a shift away from hot-melt grades that crack at sub-zero loading docks. The trend penetrates Latin America and Southeast Asia where urban grocery startups sign subscription deals for tapes pre-qualified under ISTA 7D cold-chain protocols.

Shift From Manual to Automated Case-Sealing Lines

Western converters are replacing handheld dispensers with high-speed extruders that cut trim losses by 25% and allow continuous uptime. 3M’s VHB Extrudable Tape, launched in 2024, bonds instantly, dispenses on demand, and rewinds scrap for recycling. Case-sealer OEMs bundle predictive analytics that flag glue-line anomalies, which reduces downtime and adhesive waste. With the U.S. packaging machinery market tracking 8% annual growth through 2027, integrators forecast an 18-month payback on fully automated tape heads.

Retailers’ Private-Label Expansion in Emerging Markets

Regional grocers are adding private-label SKUs in packaged foods, beauty, and home care. These programs raise short-run volumes that require flexible carton sizes and branding tapes printed in smaller lots. Asian converters respond with digital printing and water-based inks certified to more than 5 wt% VOC, boosting regional sales for recyclable paper seals.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OECD-level plastic-packaging taxes | -1.4% | Europe, North America; spillover to APAC | Medium term (2-4 years) |

| VOC-emission caps on solvent-based acrylics | -0.8% | Global, stringent in developed markets | Short term (≤ 2 years) |

| Supply crunch of natural rubber due to disease outbreaks | -0.6% | Global, acute impact in Southeast Asia | Short term (≤ 2 years) |

| Carton-free shipping pilots by leading marketplaces | -1.1% | North America, Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carton-Free Shipping Initiatives Challenge Traditional Packaging Models

Amazon’s policy to eradicate 95% of plastic air pillows in North America and broaden Ships in Own Container protocols cuts tape consumption on certain SKUs. Its frustration-free program has eliminated 181,000 tons of excess material and avoided 307 million boxes since launch. Marketplace rivals now pilot on-demand paper-bagging machines that seal without adhesive, presenting a long-term volume drag for the packaging tapes market.

OECD-Level Plastic Packaging Taxes Reshape Material Selection

The UK’s Plastic Packaging Tax levies GBP 210.82 per tonne on containers with < 30% recycled content, generating GBP 276 million in its first fiscal year and pushing converters toward fiber-based tapes. Spain’s EUR 0.45/kg fee exerts parallel pressure specright.com. Germany plans a national tax framework by 2026, compounding EU plastic-levy obligations and accelerating trials of water-resistant kraft substrates. While paper tapes meet curbside recycling norms, suppliers still absorb higher pulp costs, compressing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Dominance Challenged by Sustainable Alternatives

Plastic substrates captured 64.02% of the packaging tapes market share in 2025 because BOPP films deliver high tensile strength, optical clarity, and low cost. BOPP seals overtake PVC in North American parcel centers, while rigid PVC persists in European pharma distribution due to chemical resistance. The packaging tapes market size for plastic grades is projected to reach USD 29.12 billion in 2031, though its share will erode as taxes bite.

Paper-based alternatives are growing 6.79% CAGR. Recyclability, curbside acceptance, and rising Kraft supply in Southeast Asia encourage adoption despite moisture concerns. Producers now add biodegradable barrier coatings that withstand 24-hour 90%-RH testing.

By Adhesive Type: Acrylic Leadership Amid Rubber-Based Innovation

Acrylic chemistries accounted for 44.12% of the packaging tapes market size in 2025, thanks to UV stability and compliance with more than 5 wt% solvent rules under EU BAT directives. Water-based acrylics also bond well to recycled corrugate, a rising substrate in Europe.

Rubber-based systems post the fastest 6.58% CAGR by leveraging styrenic block copolymers that maintain tack down to -25 °C. KRATON’s SIBS platform cuts organosolvent use 30%, meeting California’s Air Resources Board limits. Tex Year’s bio-based compostable rubber adhesive reaches 85% bio-content with 90% degradation in 180 days, suiting circular-economy packaging

By Product Form: Industrial Applications Drive Strapping Dominance

Industrial shippers favor glass-filament or mono-oriented PET strapping tapes that seized 58.63% of the packaging tapes market share in 2025, protecting palletized white goods and steel coils in transit. Average pull strength surpasses 400 N, limiting load shift and damage claims.

Carton-sealing tapes will grow 6.83% CAGR as e-commerce SKUs proliferate. Automated inside-the-box labelers now apply narrow 38-mm rolls, 10 mm less than manual grades, saving as much as USD 200,000 annually in a 60-parcel-per-minute facility. 3M’s extrudable platform reinforces this trend by allowing precise bead placement and reclaiming trim waste

By End-User Industry: Retail Leadership Amid E-Commerce Acceleration

Store-level shelf prep, price-tagging, and back-room boxing kept retail ahead at 52.35% of the packaging tapes market size in 2025. Big-box chains added eco-logoed paper filler-seal tapes that double as tamper evidence, enhancing brand perception.

E-commerce now expands 6.88% CAGR, hitting 25.40% share by 2031 as same-day grocery orders soar. Amazon alone has removed over 2 million tons of packaging since 2015 by adopting machine-learning carton layouts, yet total parcel counts keep overall tape volumes rising. Pharmaceutical 3-pl logistics increase demand for cryogenic-certified tapes that survive dry-ice freight.

Geography Analysis

Asia Pacific held 39.10% of the packaging tapes market share in 2025, fueled by mobile-first retail and a sizable contract-manufacturing pipeline. Chinese converters supply antistatic BOPP tapes to smartphone plants in the Greater Bay Area, where 2024 output exceeded 250 million handsets.

North America focuses on case-sealer automation to offset labor scarcity. The region introduces noise-reduced tapes that meet OSHA 75 dB limits, supporting ergonomic mandates. Amazon’s 95% plastic-air-pillow removal shifts uptake toward paper-based rolls sourced from U.S. kraft mills, stimulating domestic tape coating lines.

Europe’s stringent plastic taxes intensify trials of recycled-content films and solvent-free adhesives. Spain, France, and Italy replicate the UK levy, incentivizing fiber substrates and bumping up kraft-line utilization.

Competitive Landscape

The packaging tapes market is highly fragmented and centers on a dozen global groups, yet regional specialists thrive on custom runs. 3M deepened its moat with the extrusion-ready VHB line that slashes waste by 25%, a decisive edge as brand owners target Scope 3 emissions. tesa teamed up with Snowflake to crunch production data across 14 plants, rolling out AI algorithms that cut unscheduled downtime by14%.

Packaging Tapes Industry Leaders

3M

tesa SE

Intertape Polymer Group Inc.

Nitto Denko Corporation

Berry Global Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: tesa established new offices in Mumbai and Bengaluru to strengthen its presence in India's manufacturing sector and advance its growth strategy in the Asia-Pacific region.

- August 2024: tesa SE announced plans to integrate green hydrogen into production, with the first hydrogen-enabled adhesive tapes slated for Hamburg-Hausbruch in 2027.

Global Packaging Tapes Market Report Scope

Packaging tape is a form of adhesive tape that is widely used in the preparation of items for handling, storage, or shipping purposes. Packaging tapes are used in the temporary sealing, wrapping, enclosing, and bundling of items like boxes, bottles, and other types of isolating storage units. This helps to maintain a tolerance that keeps cargo within the restraint of its receptacle. The packaging tape market is segmented by material type, adhesive type, end-user industry, and geography. By material type, the market is segmented into plastic and paper. By adhesive type, the market is segmented into acrylic, hot melt, rubber-based, and other adhesive types. By end-user industry, the market is segmented into e-commerce, food & beverage, retail, and other end-user Industries. By geography, the market is segmented into Asia-Pacific, North America, Europe, South America, and Middle East and Africa. The report also covers the market size and forecasts for the packaging tapes market in 15 countries across major regions. For each market segment, the market sizing and forecasts have been provided on the basis of value (USD million).

By Material Type

| Plastic |

| Paper |

By Adhesive Type

| Acrylic |

| Hot-Melt |

| Rubber-Based |

| Other Adhesive Types |

By Product Form

| Carton-Sealing Tapes |

| Masking and Painter's Tapes |

| Strapping and Bundling Tapes |

By End-user Industry

| E-commerce |

| Food and Beverage |

| Retail |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Plastic | |

| Paper | ||

| By Adhesive Type | Acrylic | |

| Hot-Melt | ||

| Rubber-Based | ||

| Other Adhesive Types | ||

| By Product Form | Carton-Sealing Tapes | |

| Masking and Painter's Tapes | ||

| Strapping and Bundling Tapes | ||

| By End-user Industry | E-commerce | |

| Food and Beverage | ||

| Retail | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the packaging tapes market?

The packaging tapes market is valued at USD 34.08 billion in 2026 and is projected to reach USD 45.72 billion by 2031.

Which material segment leads the packaging tapes market?

Plastic substrates lead with 64.02% share in 2025, though paper tapes are the fastest-growing alternative at a 6.79% CAGR.

Why are acrylic adhesives dominant in packaging tapes?

Acrylic systems combine UV resistance, broad temperature tolerance, and compliance with global VOC caps, which secured 44.12% market share in 2025.

How will plastic packaging taxes affect tape selection?

OECD-level levies raise the cost of virgin-plastic tapes, accelerating adoption of recycled-content films and recyclable paper tapes that avoid the surcharge.

Which region offers the highest growth opportunity?

Asia Pacific commands 39.10% share and leads growth at a 7.05% CAGR, propelled by e-commerce expansion and manufacturing relocations into India and Southeast Asia.

Page last updated on: