Rail Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

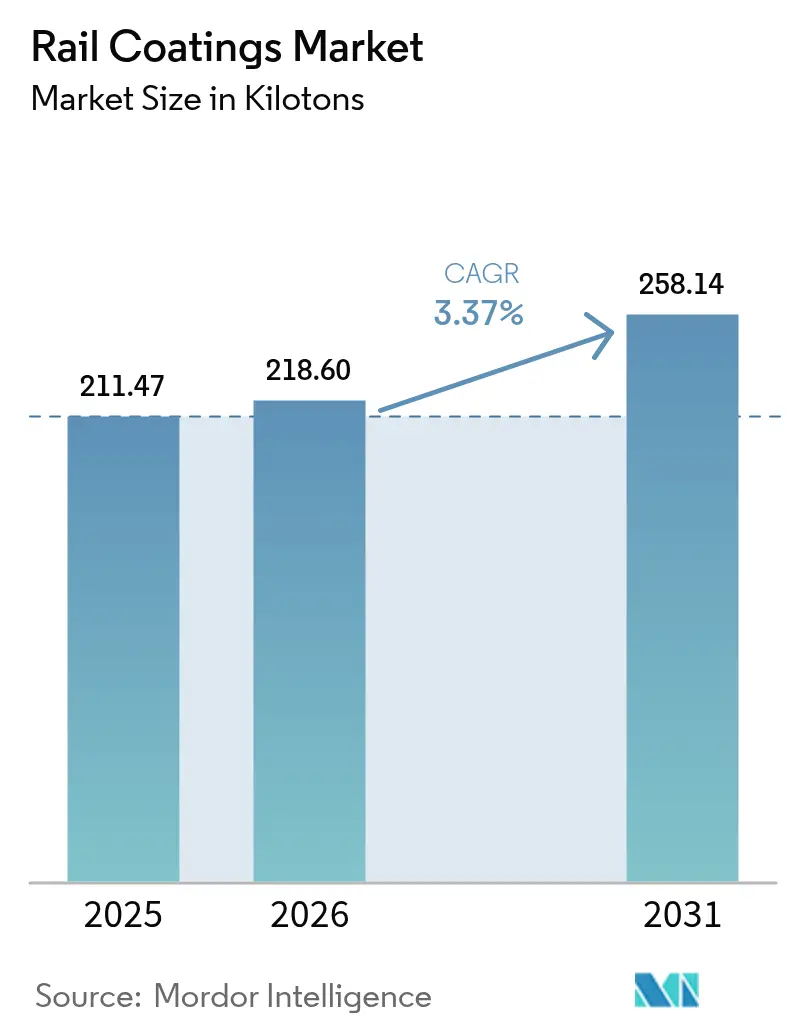

| Market Volume (2026) | 218.6 kilotons |

| Market Volume (2031) | 258.14 kilotons |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

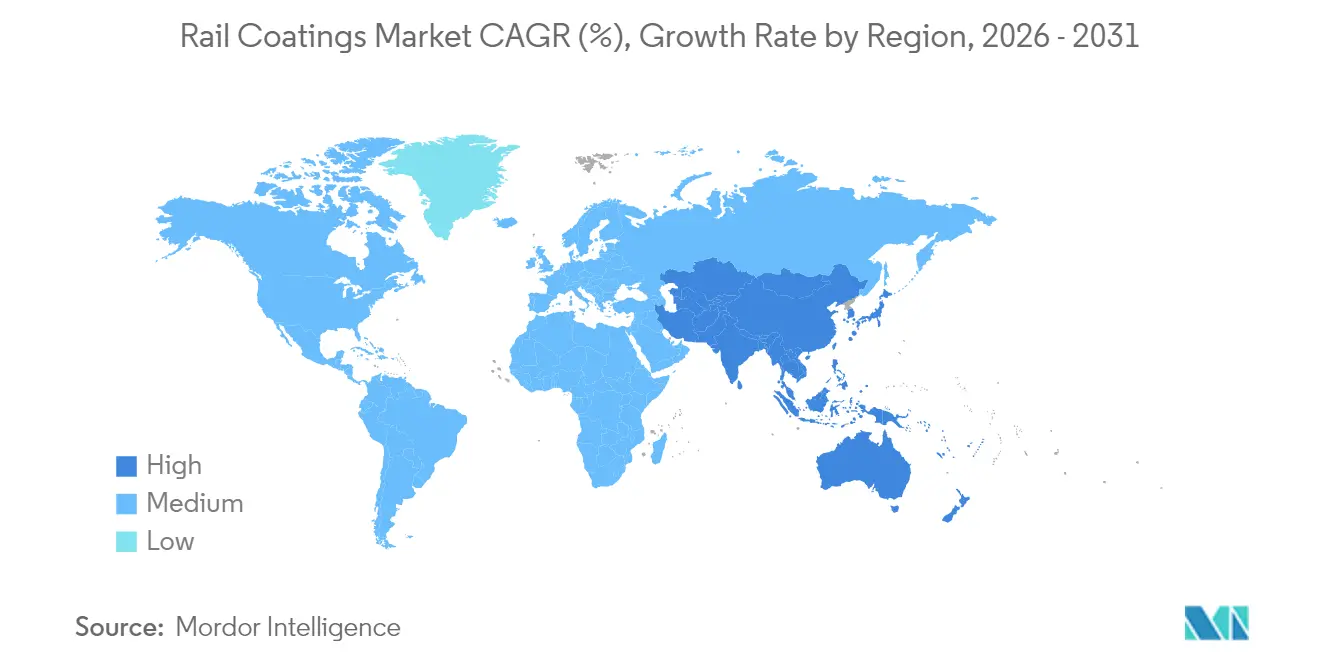

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rail Coatings Market Analysis by Mordor Intelligence

The Rail Coatings Market size is expected to grow from 211.47 kilotons in 2025 to 218.6 kilotons in 2026 and is forecast to reach 258.14 kilotons by 2031 at 3.37% CAGR over 2026-2031. This gradual expansion shows how the rail coatings market is shifting from aggressive capacity addition to careful asset preservation, as owners demand longer-lasting films that lower lifetime recoating costs. High-speed and urban-rail projects reinforce demand; however, coating consumption per kilometer is no longer increasing. Suppliers therefore compete on training, on-site support, and predictive maintenance software, rather than film build volumes. Environmental compliance, particularly low-VOC mandates, accelerates chemistry changes, while raw-material volatility forces suppliers to deepen integration or lock in long-term resin contracts. Consolidation continues, but specialist applicators still thrive by tailoring solutions to local climate, substrate, and regulatory needs.

Key Report Takeaways

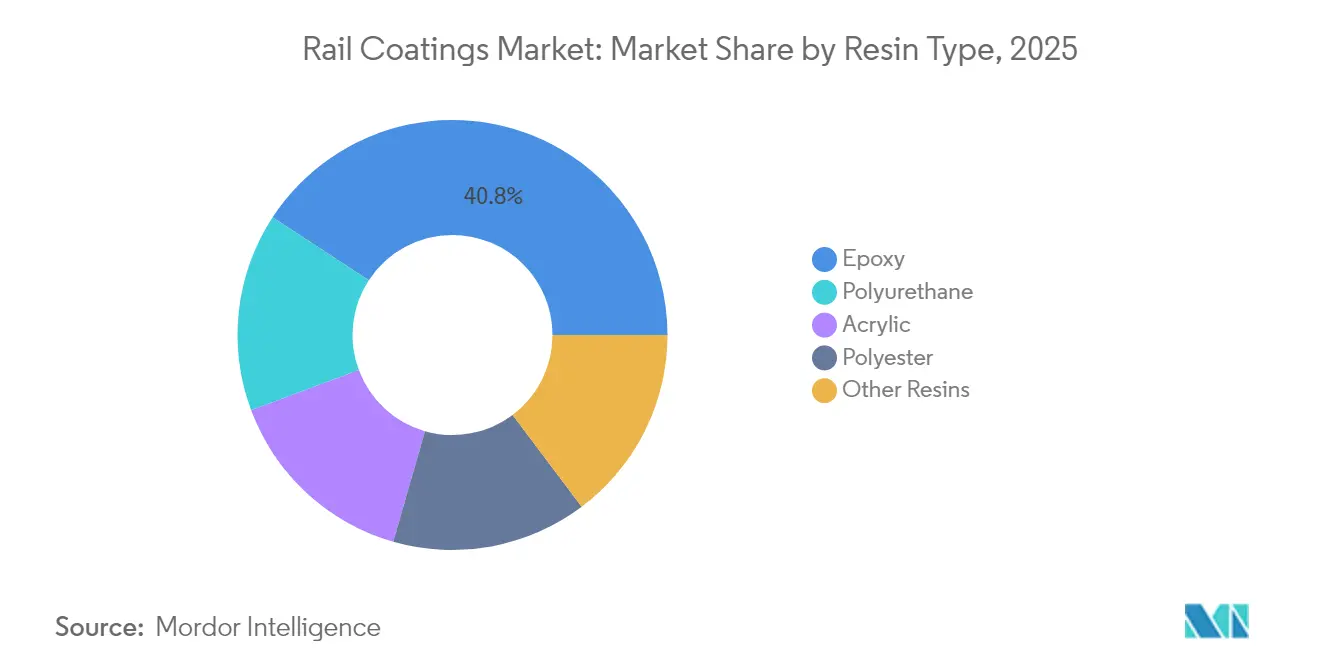

- By resin type, epoxy led the rail coatings market with a 40.78% market share in 2025; polyurethane is projected to expand at a 3.62% CAGR through 2031.

- By 2025, solvent-based systems held 48.72% of the rail coatings market share, while water-based chemistries are projected to rise fastest at a 3.71% CAGR through 2031.

- By type, refurbishment accounted for 58.61% of the rail coatings market size in 2025, while new-build programs are projected to advance at a 3.49% CAGR through 2031.

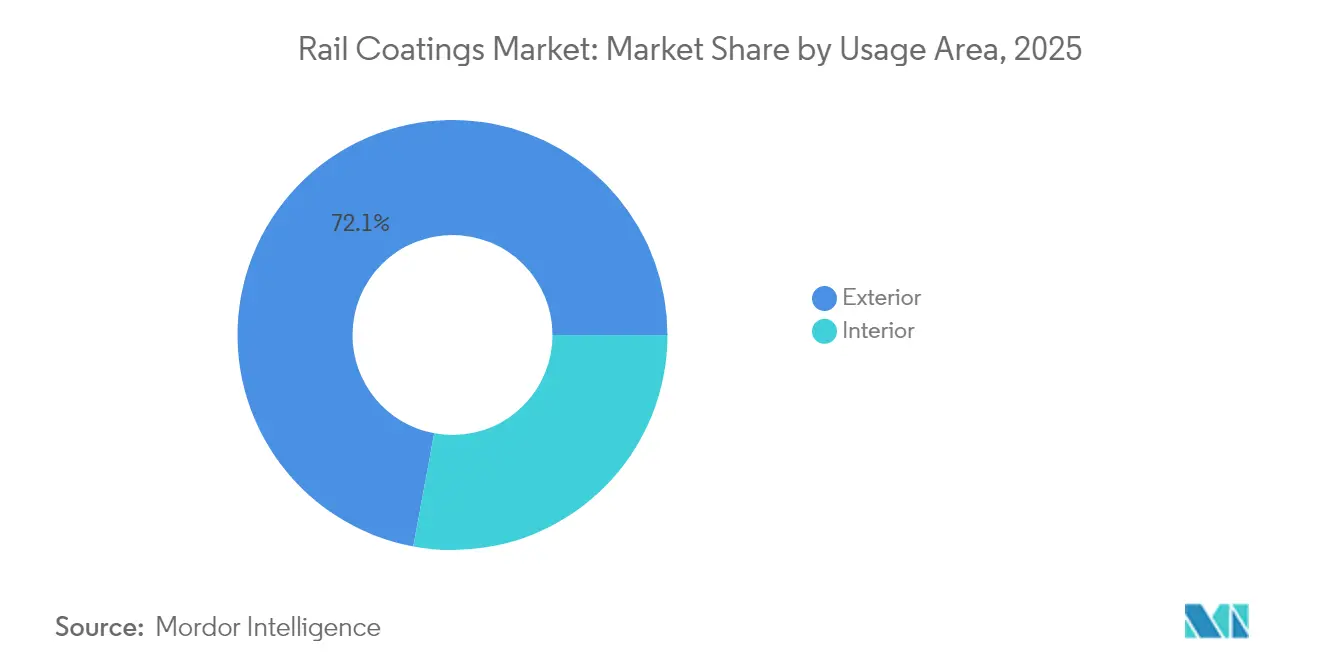

- By usage area, exterior applications accounted for a 72.08% share of the rail coatings market size in 2025 and are projected to grow at a 3.42% CAGR over the forecast period.

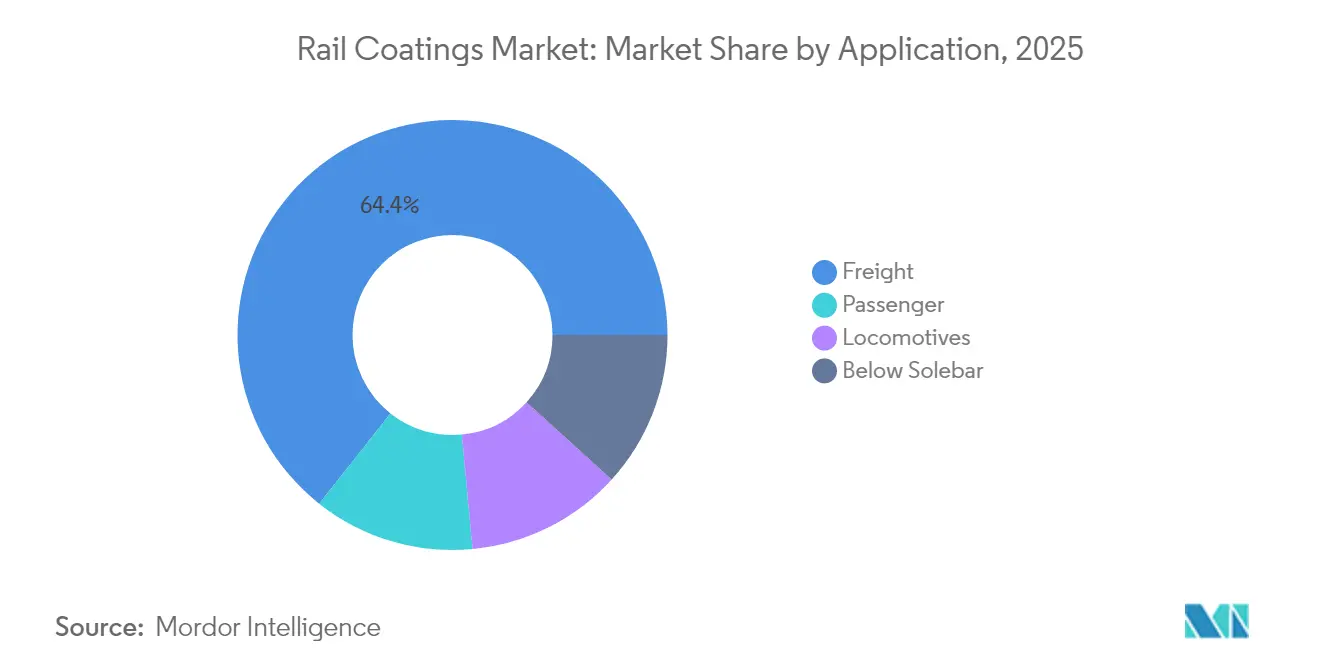

- By application, freight stock dominated the rail coatings market with a 64.35% share in 2025; passenger rolling stock is projected to have the highest CAGR of 3.59% from 2025 to 2031.

- By geography, Europe commanded a 38.72% market share in rail coatings in 2025, whereas the Asia-Pacific region is expected to grow at a 4.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rail Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of high-speed rail networks | +0.8% | Europe, Asia-Pacific, spillover to North America | Long term (≥ 4 years) |

| Surge in metro and light-rail investments | +0.6% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| Refurbishment of ageing rolling stock | +0.4% | Europe and North America | Short term (≤ 2 years) |

| Adoption of self-cleaning anti-graffiti nanocoatings | +0.3% | Global urban centers, early adoption in Europe | Medium term (2-4 years) |

| ESG-linked shift to low-VOC systems | +0.5% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of High-Speed Rail Networks

European Union funding for cross-border corridors, combined with Thailand’s first 250 km/h line, underpins long-term premium-grade demand[1]European Commission, “Connecting Europe Facility 2025,” ec.europa.eu. High-velocity operation subjects car bodies to elevated wind load, stone-chip abrasion, and heat, so specifiers mandate fluoropolymer topcoats that resist erosion. Norway’s full network electrification intensifies this requirement because electric rolling stock operates at a cooler temperature, yet carries more sensitive wiring that requires insulation from coatings. These factors raise per-car coating spend even as overall rail coatings market volume stabilizes. Vendors that certify aerodynamic, low-drag finishes secure inclusion in master specifications. The shift also micro-segments demand: tunnel sections require smoke-suppressant layers, while roof zones demand higher UV blockers, pushing the use of multi-coat systems.

Surge in Metro and Light-Rail Investments

Indian federal allocations for metros in fifteen cities translate into immediate purchase orders for intumescent primers and anti-microbial interiors. European regulators mandate smoke-toxicity tests after metro incidents, so fire-resistive films move from optional to baseline. North American transit agencies add silver-ion additives to combat surface pathogens, a post-pandemic response guided by APTA’s hygiene charter. Because carriage downtime inflates operator costs, contractors specify rapid-cure polyurethane clearcoats, replacing older alkyd maintenance paints. Lifecycle-cost tenders increasingly score solutions on day-one price and ten-year cleanability, rewarding suppliers that publish audited total-cost models. These pressures keep the rail coatings market centered on value rather than sheer liters sold.

Refurbishment of Ageing Rolling Stock

Deutsche Bahn’s fleet overhaul through 2030 exemplifies how operators defer capital expenditures on new trains while extending service life by twenty years. Refurbishment triggers systematic stripping, blasting, and full re-priming, generating predictable spurts of demand for rail coatings. Hybrid primer-topcoat bundles reduce total film buildup, thereby lessening weight and enhancing energy efficiency. Refurb contracts often bundle warranty and depot-crew training, cementing long-term supplier relationships. As refurbishment gains priority, technology migration happens faster: chemistries pioneered on new builds become standard in second-life programs.

Adoption of Self-Cleaning Anti-Graffiti Nanocoatings

Titanium dioxide photocatalytic films now slash manual cleaning cycles according to peer-reviewed trials. The London Underground embeds this specification in all new rolling stock tenders, and graffiti removal data shows a payback period of two years. Photocatalytic performance depends on UV intensity, so suppliers tailor formulations for northern climates by adding dopants that activate under visible light. Many transit agencies pair sacrificial base layers with nanostructured topcoats, ensuring quick reapplication after severe vandalism has occurred. Premium pricing is offset by labor savings and higher passenger satisfaction scores, propelling incremental revenue in the rail coatings market, even with modest tonnage. Suppliers that document quantitative cost reductions in cleaning gain a tender advantage.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC-emission regulations | −0.4% | Europe and North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Raw-material price volatility | −0.3% | Global with regional fluctuation | Medium term (2-4 years) |

| Limited maintenance windows | −0.3% | Global, acute in dense urban corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent VOC-Emission Regulations

The EU Industrial Emissions Directive caps rail-coating VOC content at 50 g/L, forcing many legacy solvent systems off spec sheets. Formulating compliant lines costs suppliers USD 5 million for each chemistry family, straining research and development budgets and widening the gap between global majors and small regionals. Transitional dual-stock strategies raise inventory charges because projects are bid two years ahead under older formulas. North America is expected to follow a similar rule set by 2027, creating phased compliance waves. Contractors must now invest in air-handling and waste-capture equipment, which pushes service prices up and slows the uptake of rail coatings in retrofit cycles.

Raw-Material Price Volatility

Titanium dioxide pigment prices swung in 2024 as energy spikes hit chloride-route producers. Epoxy and polyurethane precursors shadowed crude-oil patterns, yet contract ceilings lagged, shrinking supplier margins. Multinationals hedge by entering offtake deals directly with feedstock refiners, while small firms face cash-flow squeezes. End-users react by shortening contract tenors and accepting quarterly price triggers, introducing budgeting uncertainty. Such swings prompt buyers to specify alternative-resin options in tenders, potentially fragmenting the rail coatings market as suppliers rush to qualify multiple pigment sources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Command with Polyurethane Ascendancy

Epoxy resins accounted for 40.78% of the 2025 rail coatings market share due to their unmatched adhesion and chemical resistance, particularly in primers applied to steel bogies and aluminum car bodies. Polyurethane topcoats follow for UV and gloss retention, and their 3.62% growth rate signals accelerating switchovers on the roof and side-panel zones. Hybrid epoxy-polyurethane systems now dominate depot refurb lines because one supplier delivers matched cure profiles, slashing spray-booth turns. Fluoropolymers, though niche in volume, are seeing steady uptake on high-speed sets. Silicone-modified acrylics remain a small but growing class for non-stick ice-shedding on Nordic locomotives. Regulatory VOC limits pressure all resin classes, propelling water-dilutable epoxy dispersions into primer roles without abandoning corrosion resistance.

Continued research and development convergence of epoxy crosslinkers with low-temperature polyaspartic urethane hardeners enables single-shift overcoating even at 5 °C winter depot conditions. Suppliers that certify such chemistries against ISO 9466:2025 earn preferred-vendor status. These advances expand the rail coatings market opportunity for functional hybrids that combine chemical toughness with environmental compliance, shifting the competitive focus from resin type to lifecycle value.

By Technology: Water-Based Momentum Against Solvent Leadership

Solvent-borne platforms still held 48.72% of the 2025 rail coatings market share, primarily because they atomize reliably under variable conditions. Yet water-based growth outpaces at 3.71%, driven by exemption pressures in Europe and copycat policies in Japan and South Korea. Resin suppliers incorporate coalescent-free latexes that meet VOC caps while matching 1,000-hour salt-spray benchmarks. Powder coatings are advancing in OEM car-body shells, aided by recent breakthroughs in low-bake polyester-epoxy hybrids that cure at 150 °C, a temperature achievable for aluminum components. UV-cure oligomer systems carve out niches in interior panels where instant cure enhances production flow.

Equipment outlays still slow wholesale migration: water-borne lines require stainless spray trunks, and powder booths need reclaimed airflow loops. As leading rail operators shift to carbon-pricing tender models, however, water-borne and powder options score higher lifecycle points, nudging total rail coatings market share toward low-emission paths. Suppliers partner with equipment makers to bundle turnkey upgrades into coating contracts, easing capex hurdles for rolling-stock builders.

By Type: Refurbishment Dominates Volume Amid New-Build Innovation

Refurbishment accounted for 58.61% of the rail coatings market size in 2025, as operators extended fleet life while global supply chain glitches delayed new train deliveries. Overhaul cycles typically require full strip, prime, and topcoat routes, often exceeding the original factory film thickness to compensate for pitted substrates. Modular refurbishment now enables painters to tackle side-wall and roof modules separately, thereby improving yard throughput. New-build volumes climb at 3.49% CAGR, thanks to India, Thailand, and Indonesia placing bulk orders for metro cars and EMUs that specify premium powder-basecoat, polyurethane-clear systems.

Innovation typically debuts in new builds—such as fluoropolymer nanosilica clearcoats that cut drag—before spreading to refurb lines once costs drop. Consequently, refurbishment will continue to dominate tonnage, but new-build specifications will continue to pilot advanced chemistries, raising the performance baseline of the entire rail coatings market.

By Usage Area: Exterior Surfaces Set Performance Bar

Exterior surfaces accounted for 72.08% of the 2025 rail coatings market size, primarily due to their large surface area and harsh exposure conditions. Standard three-coat exterior stacks now integrate self-cleaning top layers that shed grime, retaining branding livery for up to four wash cycles longer. Roof zones increasingly use IR-reflective pigments that lower HVAC loads. Interior volumes grow more slowly, but spark niche demand for antimicrobial epoxies and intumescent barriers that meet EN 45545-2 flame-spread limits. While exterior remains both largest and fastest at 3.42% growth, interior re-specification for hygiene continues to widen product portfolios, compelling suppliers to harmonize color and gloss across dissimilar chemistries.

Depot paint shops pursue universal gun sets that handle both solvent- and water-based fluids, thereby reducing tool-change time. This trend aligns with whole-train painting packages, anchoring exterior segment primacy within the rail coatings market while smoothing supply-chain complexity for fleet operators.

By Application: Freight Fleet Drives Volume, Passenger Sets Push Premium

Freight wagons and locomotives delivered 64.35% of the 2025 rail coatings market share, reflecting vast wagon counts and tough corrosion environments. Paint specs focus on abrasive-blasted steel, zinc-rich primers, and economical two-coat polysiloxane tops, achieving ten-year cycles aligned with wheel overhauls. Passenger cars, although with just 3.59% growth, command higher per-car spending due to stricter fire, smoke, and toxicity norms, alongside aesthetic expectations. Locomotive hoods require high-heat silicones near exhaust stacks, while areas below the solebar use glass-flake epoxies to withstand ballast impact.

Post-COVID hygiene protocols emphasize the use of antimicrobial interior topcoats, particularly in suburban EMUs with high ridership turnover. Premium demand from the passenger segment keeps margins up, balancing the high-volume but low-margin freight segment, and together they reinforce the diversified structure of the rail coatings market.

Geography Analysis

Europe maintained a 38.72% rail coatings market share in 2025, thanks to its mature networks, strict VOC rules, and multi-billion-euro rolling-stock renewal programs by SNCF and Deutsche Bahn. The resurgence of high-speed and night trains further stokes premium coating demand, particularly for fluoropolymer top layers that promise 15-year warranties. Cross-border interoperability prompts OEMs to standardize coatings that withstand varying climate zones, fueling pan-regional approved product lists that lock in established suppliers.

Asia-Pacific leads growth at 4.02% CAGR to 2031 on the back of India’s modernization plan and China’s metro expansions into second-tier cities. Rapid urbanization drives mid-range polyurethane demand for commuter EMUs, while Southeast Asian high-speed corridors adopt imported nano-silica topcoats to meet aerodynamic and humidity challenges. ESG standards lag behind those in Europe, but Japan’s green-procurement rules are nudging its neighbors to adopt low-VOC thresholds, thereby accelerating waterborne sales.

North America’s freight-heavy operators invest in track and equipment upkeep, resulting in steady demand for protective coatings. Metro refurbishments in New York and Toronto specify intumescent layers, sustaining niche high-margin sales. South America focuses on bulk-freight corridors and cost-efficient zinc-rich primers, whereas the Middle East’s desert railways require silicones that resist sand erosion and 50°C ambient heat. Africa remains nascent; yet as financing clears for transnational corridors, it represents a long-tail opportunity for the rail coatings market.

Competitive Landscape

The rail coatings market is moderately consolidated. Regional challengers such as Kansai Helios boost their scale through acquisitions; the Weilburger deal expanded its powder portfolio for German OEM car shops. Niche specialists stay competitive by offering depot-on-site technical crews that cut turnaround hours. Digital services grow: IoT sensors embedded under clearcoats stream film thickness and temperature data to cloud dashboards, allowing operators to predict maintenance windows[2]IEEE, “IoT Coating Monitoring,” ieee.org . Suppliers that bundle coatings with data analytics and on-site training win multiyear framework agreements, signaling a strategic shift from commodity liters to lifecycle performance. Market contestants also co-develop low-cure powder booths with equipment OEMs, thereby tightening the ecosystem's lock-in.

Rail Coatings Industry Leaders

PPG Industries Inc.

Akzo Nobel N.V.

The Sherwin-Williams Company

Axalta Coating Systems LLC

Nippon Paint Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sherwin-Williams Protective and Marine launched three CarClad water-based products, claiming the rail sector’s lowest total applied cost through extended service life and faster re-coat cycles.

- May 2024: Kansai Helios acquired Weilburger Coatings and the full Industrial Coatings division of Grebe Holding, thereby strengthening its reach in railway coatings and expanding its European footprint.

Global Rail Coatings Market Report Scope

Rail coatings are specialized coatings designed to safeguard rail infrastructure, encompassing rails, wheels, and various other components, from corrosion and wear. By preserving the integrity and performance of rail systems, these coatings are vital for the safe and efficient transportation of both people and goods.

The global rail coatings market is segmented by resin, technology, and geography. By resin, the market is segmented into acrylic, epoxy, polyurethane, plastisols, polyester, fluoropolymers, and other resins. By technology, the market is segmented into water-based and solvent-based. The report also covers the market sizes and forecasts for the global rail coatings market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Acrylic |

| Epoxy |

| Polyurethane |

| Polyester |

| Other Resins (Fluoropolymers and silicone) |

| Water-based |

| Solvent-based |

| Powder Coatings |

| UV-Cured |

| New Build |

| Refurbishment |

| Interior |

| Exterior |

| Locomotives |

| Passenger |

| Freight |

| Below Solebar |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Polyester | ||

| Other Resins (Fluoropolymers and silicone) | ||

| By Technology | Water-based | |

| Solvent-based | ||

| Powder Coatings | ||

| UV-Cured | ||

| By Type | New Build | |

| Refurbishment | ||

| By Usage Area | Interior | |

| Exterior | ||

| By Application | Locomotives | |

| Passenger | ||

| Freight | ||

| Below Solebar | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for rail coatings in 2031?

The rail coatings market is projected to reach 258.14 kilotons by 2031, growing at a 3.37% CAGR.

Which region will grow fastest in rail coating demand?

The Asia-Pacific region is expected to lead growth at a 4.02% CAGR through 2031, driven by the Indian and Chinese rail programs.

Why do operators prefer refurbishment coatings over new builds?

Refurbishment extends fleet life and captures 58.61% of 2025 volume, providing predictable demand cycles.

What factors push the adoption of anti-graffiti nanocoatings?

Urban operators reduce manual cleaning and enhance passenger satisfaction, making premium photocatalytic films a financially attractive option.

Page last updated on: