Radiopharmaceutical Theranostics Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

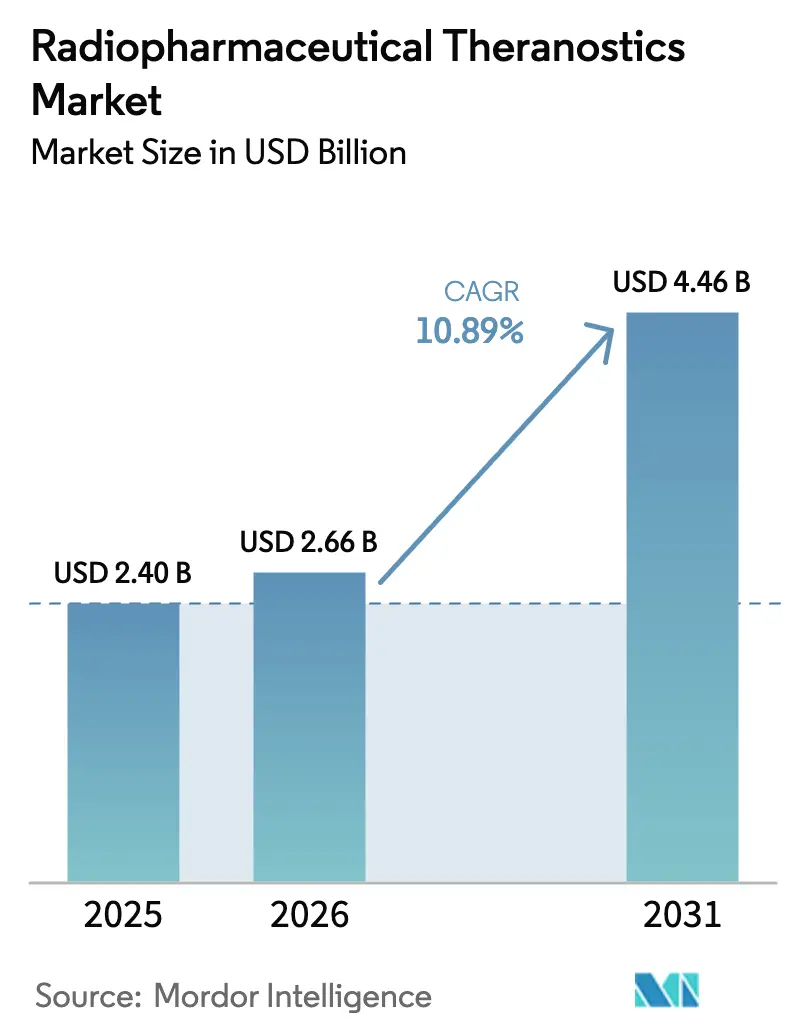

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 4.46 Billion |

| Growth Rate (2026 - 2031) | 10.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiopharmaceutical Theranostics Market Analysis by Mordor Intelligence

The radiopharmaceutical theranostics market size is expected to grow from USD 2.40 billion in 2025 to USD 2.66 billion in 2026 and is forecast to reach USD 4.46 billion by 2031 at 10.89% CAGR over 2026-2031. Clinical proof from targeted radioligand therapies, steady reimbursement expansion, and capacity investments in isotope production have shifted nuclear medicine from niche diagnostics to precision oncology mainstay. Breakthrough approvals such as the U.S. Food and Drug Administration’s March 2025 decision to move lutetium-177 PSMA-617 into earlier-line prostate cancer unlocked material upside for therapy-led revenue models. Acquisition-driven supply-chain integration by large pharmaceutical groups, together with government-backed isotope facilities, is strengthening long-term security of radioisotope feedstock. Meanwhile, talent shortages in radiopharmacy, logistics hurdles linked to short half-life isotopes, and reactor downtime expose operational vulnerabilities that encourage automation and AI-enabled workflow optimization. Collectively, these forces reinforce the double-digit trajectory of the radiopharmaceutical theranostics market as platform economics mature across imaging-therapy pairs, alpha-emitter pipelines, and integrated companion diagnostics.

Key Report Takeaways

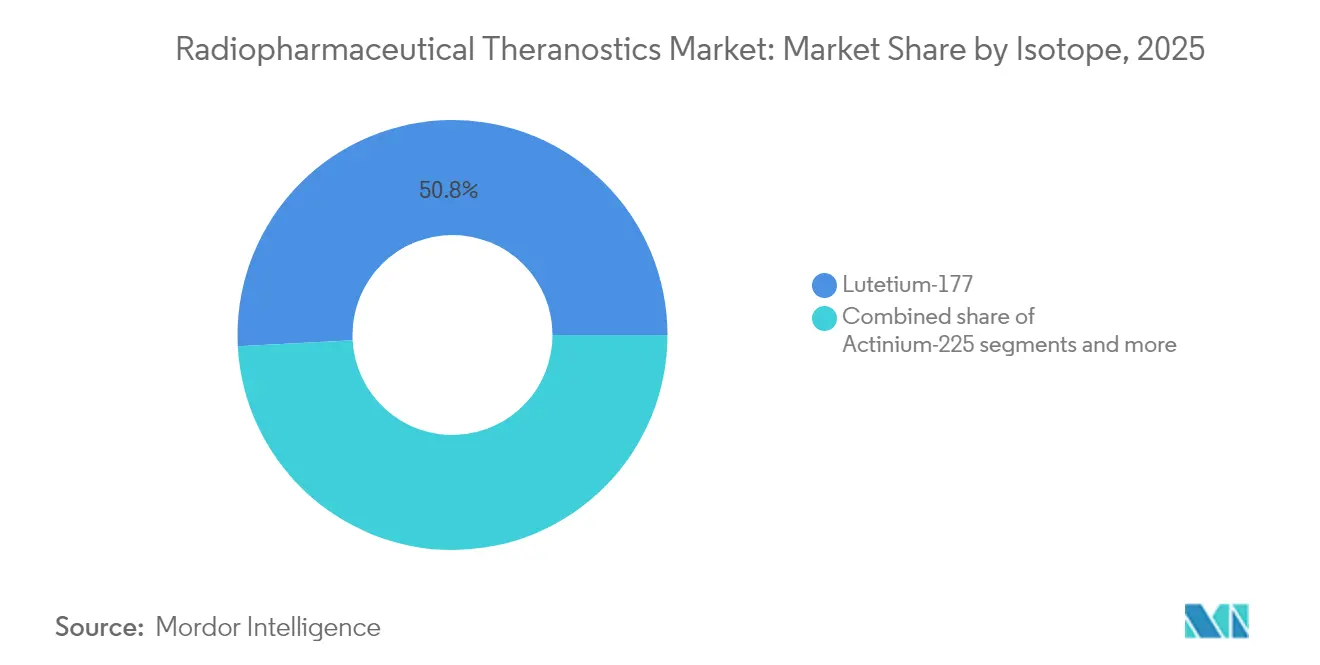

- By isotope, lutetium-177 led with 10.98% CAGR through 2031 while commanding the largest share of the radiopharmaceutical theranostics market size in 2025.

- By cancer type, prostate cancer held 72.56% of radiopharmaceutical theranostics market share in 2025; neuroendocrine tumors record the fastest 11.08% CAGR to 2031.

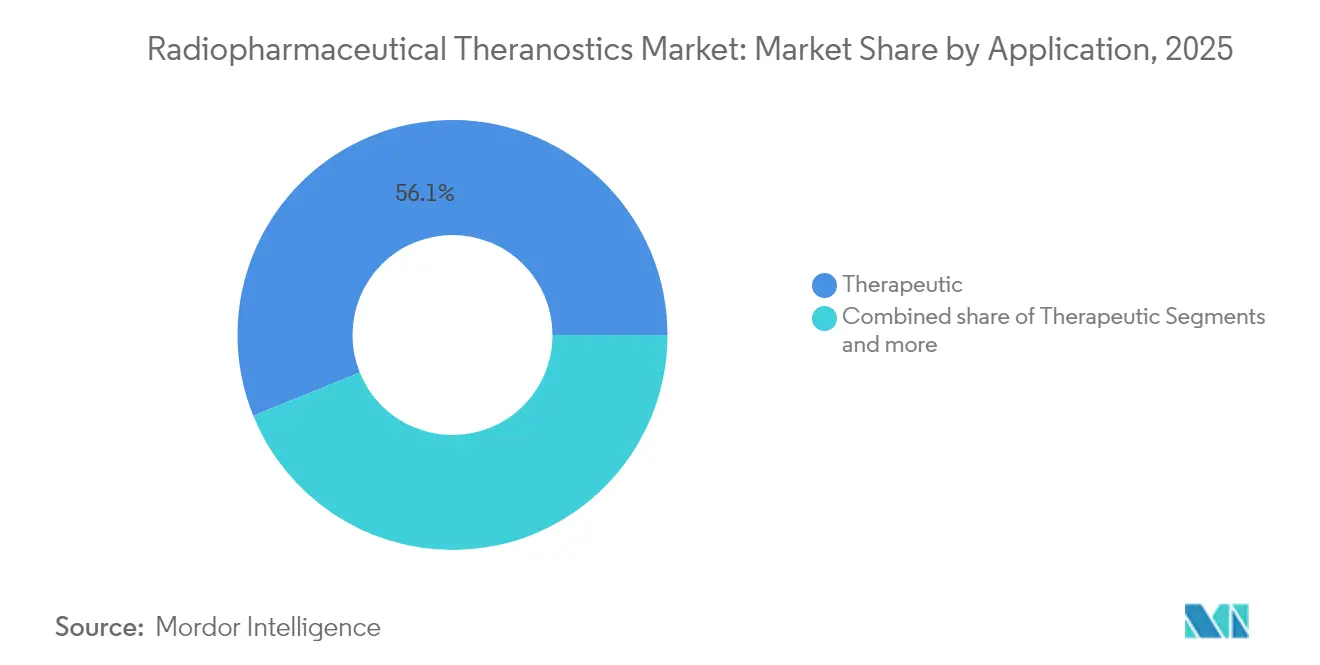

- By application, therapeutic use accounted for 56.12% of the radiopharmaceutical theranostics market size in 2025 and is projected to grow at 11.52% CAGR.

- By end user, hospitals captured 61.79% revenue share of the radiopharmaceutical theranostics market in 2025, outpacing specialized cancer centers in absolute dollar terms.

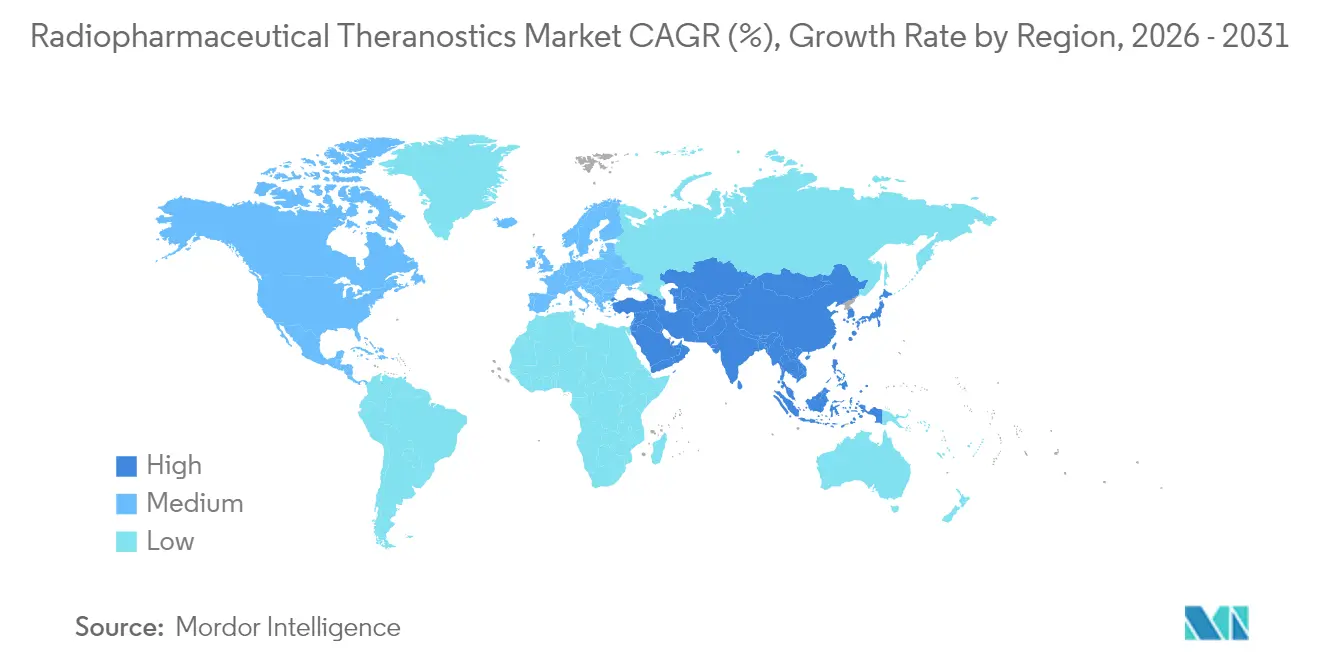

- By geography, North America commanded 49.43% radiopharmaceutical theranostics market share in 2025, whereas Asia-Pacific is poised for the highest 11.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radiopharmaceutical Theranostics Market Trends and Insights

Driver Impact Analysis*

| Increasing Lu-177 PSMA therapy approvals | +2.8% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Rising incidence of neuroendocrine tumours (NETs) | +1.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Government isotope-production investments (US, EU) | +1.5% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Alpha-emitter supply-chain breakthroughs (Ac-225, Tb-161) | +2.2% | Global, with manufacturing hubs in US, Germany, Canada | Medium term (2-4 years) |

| AI-driven personalised dosimetry adoption | +1.3% | Global, concentrated in advanced healthcare systems | Medium term (2-4 years) |

| Hospital-based GMP radiopharmacies scaling globally | +1.0% | Global, with faster adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Lu-177 PSMA Therapy Approvals

The March 2025 FDA[1]Source: “FDA approves expanded indication for Pluvicto in prostate cancer,” U.S. Food and Drug Administration, FDA.gov label expansion doubled the eligible U.S. prostate-cancer population to roughly 70,000 candidates annually, proving that earlier intervention delivers clinical benefit and commercial scale. Companion PSMA-PET diagnostics lock imaging and therapy into a single workflow, which hospitals can replicate across oncology service lines. As European centralized approvals progress, reimbursement negotiations produce uneven access, yet uptake still accelerates in Germany, France, and Italy. Active trials now extend Lu-177 PSMA targeting beyond prostate cancer into renal and brain tumors, ensuring pipeline longevity. Collectively, the milestone derisks capacity expansions at isotope suppliers and strengthens physician confidence in theranostic algorithms driving the radiopharmaceutical theranostics market.

Rising Incidence of Neuroendocrine Tumors (NETs)

Improved gallium-68 DOTATATE PET technology reveals previously occult NETs, expanding the candidate pool for lutetium-177 DOTATATE therapy. Median progression-free survival is nearly doubled versus standard chemotherapy, which persuades oncologists to adopt radionuclide regimens earlier. Health systems favor the integrated diagnose-treat-monitor cycle because it reduces downstream hospitalization and supports value-based metrics. Fractionated dosing protocols are refining tolerability, enabling community centers without high-dose isolation wards to participate. As incidence climbs in aging Western populations, NET-focused protocols reinforce sustained growth for the radiopharmaceutical theranostics market.

Government Isotope-Production Investments (US, EU)

The U.S. Department of Energy’s USD 88.8 million Oak Ridge facility de-risks domestic actinium-225 production and provides strategic redundancy to European supply chains. In the EU, Germany’s NUCLIDIUM secured EUR 84 million to advance thorium-228 generator technology, accelerating alpha-emitter initiatives. Public funding improves uptime, shortens logistics corridors, and anchors manufacturing jobs, thereby encouraging private-sector drug developers to co-locate manufacturing. These moves reduce import dependence and buffer geopolitical disruptions, delivering a steady isotope flow that underpins the radiopharmaceutical theranostics market’s expansion.

Alpha-Emitter Supply-Chain Breakthroughs (Ac-225, Tb-161)

Reactor-based actinium-225 from TerraPower and distributed cyclotron techniques from Actinium Pharmaceuticals[2]Source: Actinium Pharmaceuticals, “Actinium Pharmaceuticals announces breakthrough Ac-225 production,” ActiniumPharma.com confirm commercial viability of alpha-isotopes at scale. BWXT Medical and ITM’s transatlantic alliance shortens lead times by positioning stock on both continents. Terbium-161’s 6.9-day half-life offers a logistics advantage over actinium-225, broadening protocol flexibility. These breakthroughs unlock first-in-human trials across solid tumors and hematologic malignancies, creating a pipeline of high-value radio-conjugates that further enlarge the radiopharmaceutical theranostics market.

Restraint Impact Analysis*

| Cyclotron/reactor capacity bottlenecks | -1.8% | Global, acute in APAC emerging markets | Short term (≤ 2 years) |

| Short radio-isotope half-life logistics gaps | -1.2% | Global, pronounced in regions with limited nuclear infrastructure | Medium term (2-4 years) |

| Oncology-nuclear-medicine talent shortage | -1.5% | Global, most severe in North America & Europe | Medium term (2-4 years) |

| High therapy reimbursement uncertainty | -0.9% | Global, particularly challenging in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyclotron/Reactor Capacity Bottlenecks

Unplanned outages in European reactors cut molybdenum-99 supply by 30% in 2024 and signaled fragility across the isotope ecosystem. Cyclotrons now run near full utilization to meet fluorine-18 and gallium-68 demand, limiting headroom for theranostic isotopes. Construction lead times of three to five years and stringent licensing slow relief efforts. Emerging Asia-Pacific nations rely on imports, adding shipping days and customs variability that erode isotope potency. Until new reactors come online, capacity limits will temper near-term scaling of the radiopharmaceutical theranostics market.

Short Radio-Isotope Half-Life Logistics Gaps

Lutetium-177 decays 6.7 days post-production, requiring synchronized scheduling across production, quality control, and treatment units. Cross-border variance in radioactive-material regulation complicates flight routings and last-mile delivery. Rural centers face longer transit times, reducing dose efficacy and forcing patients to travel to urban hubs. Specialized Type-A packaging and real-time temperature monitoring inflate overhead, pressuring margins. The complexity favors centralized hubs, raising equity concerns yet reinforcing collaboration between hospital networks and radiopharmacies as the radiopharmaceutical theranostics market matures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Isotope: Lutetium-177 Dominates Clinical Applications

Lutetium-177 contributes the largest slice of radiopharmaceutical theranostics market size and is set to grow 10.98% annually to 2031. Its 6.7-day half-life matches hospital logistics windows, and its beta emission profile spares surrounding tissue. ITM’s NOVA plant and SHINE Technologies’ Cassiopeia facility doubled global capacity in 2024-25, ensuring supply continuity for tens of thousands of therapy cycles. The radiopharmaceutical theranostics market share commanded by lutetium-177 is fortified by multi-indication approvals in prostate and neuroendocrine tumors, while dosimetry software refines patient-specific activity planning. Actinium-225 accelerates from a smaller base, drawing investor interest because its high-linear-energy-transfer alpha particles yield potent tumor kill at fewer cycles.

Thor Medical’s thorium-228 generator deal with ARTBIO illustrates upstream partnerships that mitigate isotope scarcity. Yttrium-90 persists in liver-directed microsphere therapy, and radium-223 remains standard for bone metastases, yet both grow slower compared with beta-emitter incumbents. As supply-chain resiliency improves, emerging isotopes are expected to capture incremental radiopharmaceutical theranostics market share without displacing lutetium-177 in the medium term.

By Cancer Type: Prostate Cancer Leads Therapeutic Adoption

Prostate applications generated 72.56% of radiopharmaceutical theranostics market share in 2025 on the strength of PSMA-targeted regimens. Real-world studies from German and Australian centers mirror pivotal PSMAfore data, showing response rates above 50% even in late-line settings. Earlier therapy lines are forecast to drive unit demand as urologists adopt standardized PSMA-PET staging at diagnosis. Neuroendocrine tumors grow fastest, expanding 11.08% per year as gallium-68 DOTATATE scanning uncovers indolent lesions previously overlooked. Indications across thyroid, bone, and liver metastases remain valuable niches, particularly where radioiodine or yttrium-90 yields palliative benefit. Trial pipelines now include fibroblast activation protein and CXCR4 ligands, signaling entry into pancreatic, bladder, and hematology spaces. The broadening oncology footprint keeps the radiopharmaceutical theranostics market on a diversification track while guarding prostate’s dominant revenue position.

By Application: Therapeutic Segment Drives Market Growth

Therapeutic use cases accounted for 56.12% of radiopharmaceutical theranostics market size in 2025, and revenues are projected to climb 11.52% annually. Each lutetium-177 PSMA treatment course can invoice USD 40,000–60,000, dwarfing diagnostic scan revenues and lifting blended margin profiles for nuclear medicine clinics. AI-guided personalized dosimetry enhances tumor dose while reducing renal uptake, improving quality-of-life metrics in value-based models. Diagnostic procedures continue to underpin staging and follow-up, anchoring a recurring service loop that increases patient lifetime value. As therapy protocols move earlier in disease, the diagnostic-to-therapeutic conversion rate rises, enhancing systemic throughput across the radiopharmaceutical theranostics market.

By End User: Hospitals Maintain Infrastructure Advantages

Hospitals held 61.79% of 2025 radiopharmaceutical theranostics market revenue and are positioned for 11.83% CAGR growth. Academic centers integrate imaging, infusion, and monitoring under one roof, leveraging multidisciplinary boards to coordinate swift treatment decisions. Cardinal Health’s nationwide radiopharmacy network supplies unit-dosed radioligands, lowering on-site compounding risks. Specialized cancer clinics gain share where capital investment enables in-house cyclotrons or isotopic hot cells, speeding precision scheduling. Radiopharmacies solidify hub-and-spoke frameworks, distributing prepared doses to satellite hospitals, which mitigates decay loss. Workforce development partnerships with universities are alleviating technologist shortages, crucial for scaling the radiopharmaceutical theranostics market.

Geography Analysis

North America retained 49.43% radiopharmaceutical theranostics market share in 2025 as FDA accelerated pathways and Medicare payment reforms aligned financial incentives. Novartis operates its Indiana facility at full tilt for Pluvicto, while RayzeBio integration gives Bristol Myers Squibb control of an actinium-225 line. Academic hubs in Texas, Massachusetts, and California provide the talent and clinical trial throughput that keep protocol innovation local.

Asia-Pacific posts the steepest 11.16% CAGR through 2031, driven by China’s fast-track approvals and burgeoning private hospital chains. National Medical Products Administration reforms encourage simultaneous global filings, shortening launch lags. Telix Pharmaceuticals is scaling isotope production partnerships in Japan and South Korea to tap into rapidly aging populations with high oncologic incidence. Government-led infrastructure programs in India earmark new cyclotrons, alleviating import dependence.

Europe grows at a steady mid-single-digit clip. Germany anchors manufacturing with ITM’s lutetium-177 hub and NUCLIDIUM’s thorium generator research. Although the EMA’s centralized drug approval simplifies pan-EU marketing authorization, each country negotiates reimbursement separately, causing launch-price segmentation. Switzerland remains an early-adopter outlier as Swissmedic routinely greenlights therapies months ahead of broader EU roll-outs. South America and the Middle East & Africa remain nascent, but Brazil and the Gulf Cooperation Council fund nuclear-medicine suites within oncology mega-centers to reduce outbound medical tourism. In these territories, isotope import logistics and workforce gaps constrain near-term uptake yet position them as long-range contributors to the radiopharmaceutical theranostics market.

Competitive Landscape

Industry concentration is moderate, with convergence around supply-chain mastery and targeting technology. Novartis’ Lutathera and Pluvicto franchises topped USD 1.2 billion in 2024 sales, funding further capacity at its Indianapolis site. Bristol Myers Squibb’s USD 4.1 billion RayzeBio deal and Eli Lilly’s USD 1.4 billion Point Biopharma acquisition illustrate big-pharma appetite for vertically integrated alpha platforms. AstraZeneca echoed the theme via a USD 2.4 billion Fusion Pharmaceuticals purchase, securing actinium-225 access.

Telix Pharmaceuticals’ acquisition of ARTMS adds solid-target isotope production that reduces dependency on reactor schedules, strengthening its Asia-Pacific channel. Technology differentiation centers on AI-assisted dosimetry, dual-isotope constructs, and novel vectors such as antibodies, peptides, or small molecules. White-space therapeutic areas include pediatrics, rare cancers, and combination regimens pairing radiopharmaceuticals with checkpoint inhibitors. As first-generation patents approach expiration post-2030, biosimilar players prepare to enter, while incumbents pivot to next-generation ligands with better tumor-to-kidney ratios. Competitive intensity will tighten, yet supply-chain control and regulatory know-how remain formidable entry barriers, sustaining high-value positions across the radiopharmaceutical theranostics market.

Radiopharmaceutical Theranostics Industry Leaders

Bayer AG

Cardinal Health

GE HealthCare

Novartis AG

Jubilant Pharmova Limited (Jubilant Radiopharma)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ITM secures up to USD 262.5 million debt financing from Blue Owl Capital to scale ITM-11 manufacturing ahead of commercial launch.

- April 2025: Telix and Cardinal Health sign distribution pact for Gozellix, embedding ARTMS QUANTM systems in Cardinal’s network to localize gallium-68 supply.

Global Radiopharmaceutical Theranostics Market Report Scope

Radiopharmaceutical theranostics involves the development and utilization of radiopharmaceuticals for both diagnostic imaging and targeted therapeutics interventions. This innovative approach integrates both components, enabling personalized treatment strategies, particularly in oncology. Radiopharmaceutical theranostics aims to enhance precision in medicine by combining diagnostic insights with therapeutic applications tailored to individual patient needs.

The radiopharmaceutical theranostics market is segmented by type, radioisotopes, application, end user, and geography. By type, the market is segmented into companion diagnostic radiopharmaceuticals and targeted therapeutic radiopharmaceuticals. By radioisotopes, the market is segmented into technetium-99, gallium-68, iodine-131, lutetium-177, copper-67 and 64, and other radioisotopes. By source, the market is segmented into nuclear reactors and cyclotrons. By application, the market is segmented into oncology, cardiology, neurology, and other applications. By end user, the market is segmented into hospitals, diagnostic imaging centers, research institutes, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Actinium-225 |

| Radium-223 |

| Iodine-131 |

| Yttrium-90 |

| Other Isotopes |

| Prostate Cancer |

| Neuroendocrine Tumours |

| Thyroid Cancer |

| Bone Metastases |

| Liver Cancer |

| Others |

| Therapeutic |

| Diagnostic (Imaging) |

| Hospitals |

| Specialised Cancer Centres |

| Academic & Research Institutes |

| Radiopharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| Lutetium-177 | Actinium-225 | |

| Radium-223 | ||

| Iodine-131 | ||

| Yttrium-90 | ||

| Other Isotopes | ||

| By Cancer Type | Prostate Cancer | |

| Neuroendocrine Tumours | ||

| Thyroid Cancer | ||

| Bone Metastases | ||

| Liver Cancer | ||

| Others | ||

| By Application | Therapeutic | |

| Diagnostic (Imaging) | ||

| By End User | Hospitals | |

| Specialised Cancer Centres | ||

| Academic & Research Institutes | ||

| Radiopharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the radiopharmaceutical theranostics market in 2031?

The market is expected to reach USD 4.46 billion by 2031, reflecting an 10.89% CAGR over 2026-2031.

Which radioisotope currently generates the highest revenue?

Lutetium-177 leads thanks to expansive clinical use in prostate and neuroendocrine tumors and is forecast to grow 10.98% annually.

Why are hospitals the dominant end-user segment?

Hospitals possess integrated nuclear medicine suites, trained staff, and regulatory frameworks, capturing 61.79% of 2025 revenue and sustaining 11.83% CAGR.

Which region will grow fastest through 2031?

Asia-Pacific is set for the quickest advance at 11.16% CAGR due to infrastructure build-out and streamlined approvals in China, Japan, and South Korea.

How are supply-chain risks being mitigated?

Government-funded reactors, private cyclotron builds, and transatlantic isotope alliances are expanding capacity and reducing logistics bottlenecks.

Page last updated on: