Conjunctivitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.71 Billion |

| Market Size (2031) | USD 5.72 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

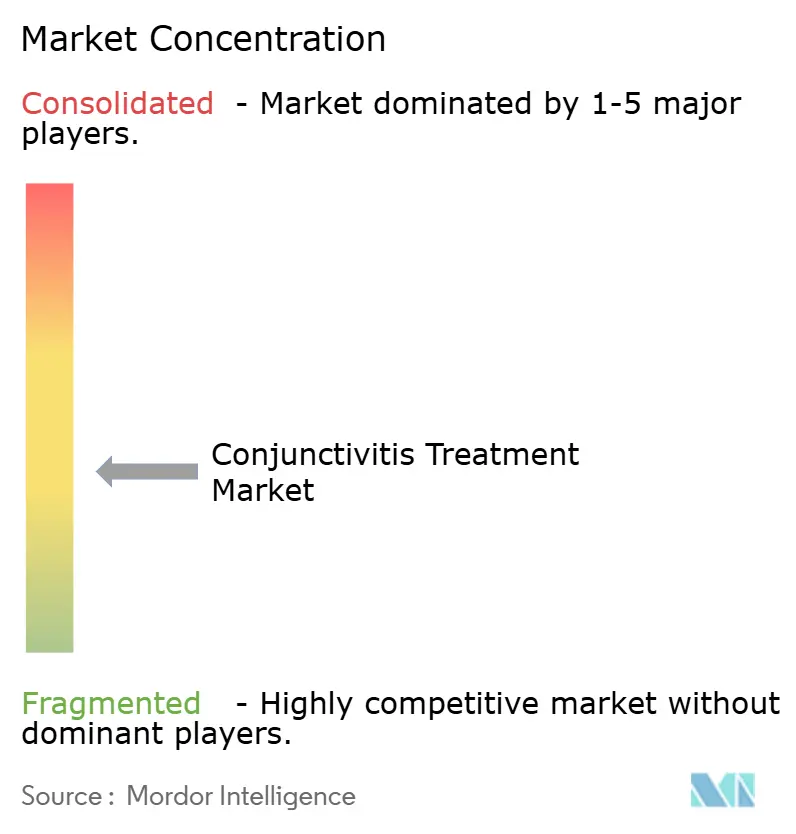

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conjunctivitis Treatment Market Analysis by Mordor Intelligence

The conjunctivitis treatment market size was valued at USD 4.53 billion in 2025 and estimated to grow from USD 4.71 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). That growth reflects stable demand for therapies that address one of the most common eye disorders worldwide. Key momentum comes from fast-tracked regulatory approvals for novel ophthalmic drugs, growing over-the-counter (OTC) availability of anti-infective drops, and lengthening allergen seasons that lift allergic case numbers. North American consumption remains the largest contributor because of widespread insurance coverage and established treatment protocols, while Asia-Pacific demand accelerates on the back of expanded rural eye-care programs and rising screen-time-related ocular strain. Competitive differentiation increasingly rests on preservative-free formulations and supply-chain resilience that mitigate active-pharmaceutical-ingredient (API) shortages.

Key Report Takeaways

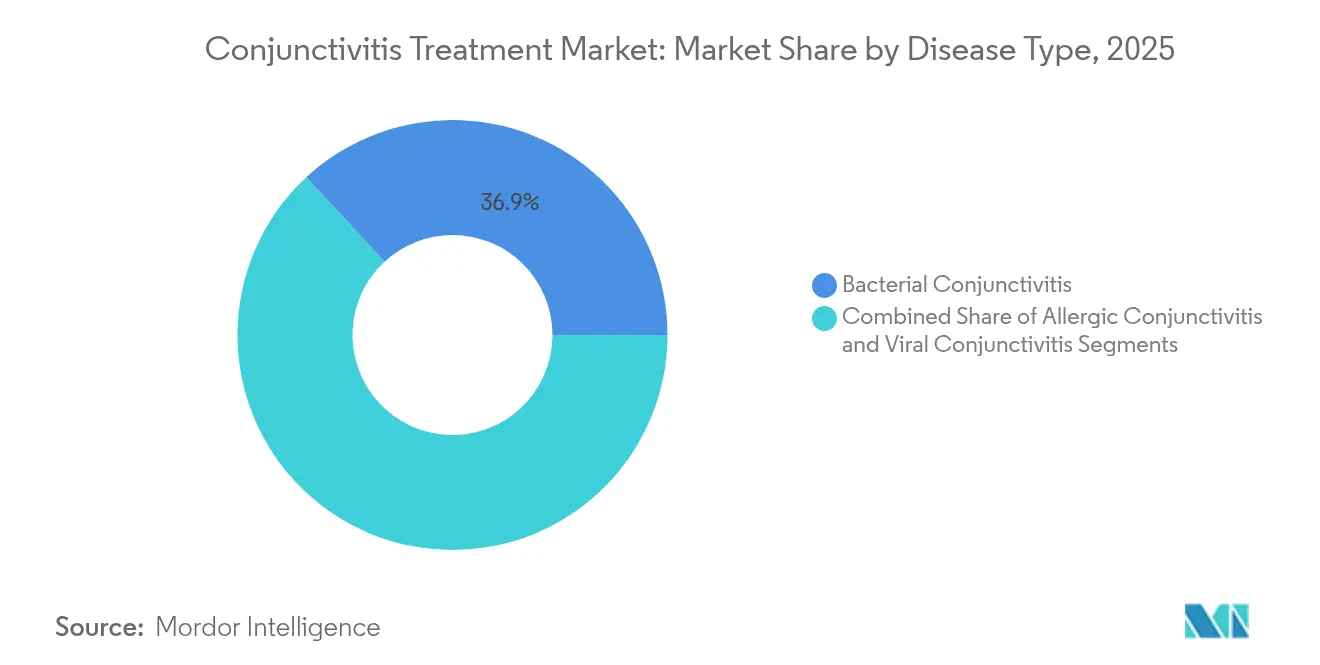

- By disease type, bacterial conjunctivitis led with 36.90% of conjunctivitis treatment market share in 2025, whereas allergic conjunctivitis is projected to post the fastest 6.90% CAGR to 2031.

- By formulation, eye drops captured 62.95% revenue in 2025; ointments are expected to expand at a 7.32% CAGR through 2031.

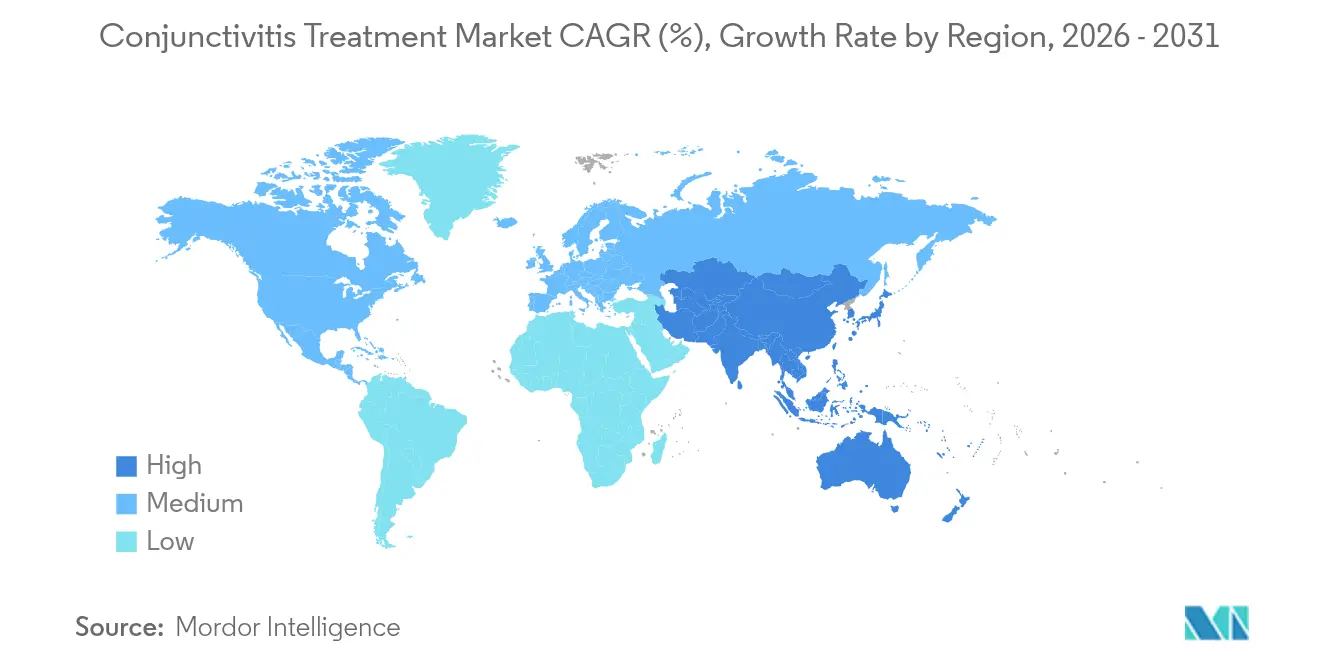

- By geography, North America commanded 32.40% of conjunctivitis treatment market share in 2025; Asia-Pacific is forecast to grow at 7.18% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Conjunctivitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Viral & Allergic Conjunctivitis | +0.8% | Global, with higher impact in APAC and MEA | Medium term (2-4 years) |

| Growing OTC Availability Of Anti-Infective Eye Drops | +0.6% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Expedited FDA Approvals For Ophthalmic Formulations | +0.5% | Global, with primary impact in North America | Short term (≤ 2 years) |

| Surge In Screen-Time–Induced Dry-Eye Triggering Secondary Infections | +0.7% | Global, with highest impact in developed markets | Medium term (2-4 years) |

| Climate-Change-Driven Allergen Seasons Lengthening | +0.4% | Global, with pronounced effects in temperate regions | Long term (≥ 4 years) |

| Tele-Ophthalmology Boosting Early Diagnosis In Rural Areas | +0.3% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Viral & Allergic Conjunctivitis

Seasonal adenoviral outbreaks and climate-linked allergen surges continue to lift overall case counts. Adenovirus strains resist standard antibiotics, pushing demand for targeted antivirals. Climate change is extending pollen seasons, and poor urban air quality magnifies allergic episodes. Pediatric digital lifestyles increase inflammation rates, reinforcing the need for combination anti-inflammatory and anti-infective products[1]Mutahir Shah, “Excessive Screen Time Exposure Leads to Dry Eyes and Inflammatory Conjunctivitis in Children,” PubMed, pubmed.ncbi.nlm.nih.gov. Health systems now frame conjunctivitis as a gateway issue that warrants comprehensive ocular-health management.

Growing OTC Availability of Anti-Infective Eye Drops

Regulators in the United States, Europe, and parts of Asia have reclassified several once-prescription antibiotics for OTC sale. Easier access speeds symptom relief, especially where ophthalmologist density is low. Manufacturers reformulate drops to remove harsh preservatives and simplify dosing. Oversight bodies counter antibiotic misuse risks with consumer education and digital decision-support tools.

Expedited FDA Approvals for Ophthalmic Formulations

The Food and Drug Administration’s priority review pathway has shortened time-to-market for therapies such as lotilaner for blepharitis and acoltremon for dry-eye-linked inflammation. These clearances encourage R&D investment in new mechanisms that address antimicrobial resistance and preservative concerns.

Surge in Screen-Time-Induced Dry-Eye Triggering Secondary Infections

Extended device usage destabilizes tear film, reducing innate ocular defense against pathogens. Clinicians report higher secondary bacterial and viral infections among heavy screen users, especially children. The linkage is prompting demand for preventive lubricants co-formulated with mild antimicrobials and for digital-health applications that track screen exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Antimicrobial Resistance In Ocular Pathogens | -0.9% | Global, with highest impact in developing markets | Medium term (2-4 years) |

| Growing Popularity Of Herbal & Home-Remedy Alternatives | -0.4% | APAC and MEA primarily, emerging in developed markets | Long term (≥ 4 years) |

| Stringent Preservatives-Related Regulatory Scrutiny | -0.3% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| API Supply-Chain Disruptions For Ophthalmic Antibiotics | -0.6% | Global, with acute impact during disruption periods | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Antimicrobial Resistance in Ocular Pathogens

Surveillance studies have documented escalating resistance among Staphylococcus and Streptococcus isolates, limiting first-line therapy effectiveness. Hospitals respond with stewardship programs and demand for next-generation agents, but prolonged development cycles weigh on market expansion.

API Supply-Chain Disruptions for Ophthalmic Antibiotics

Generic-drug supply relies on concentrated manufacturing hubs. Plant shutdowns and raw-material shortages have triggered recalls and temporary product absences, as seen with recent hypromellose shortages[2]Elyse MacDonald, “Drug Shortage Detail: Hypromellose Ophthalmic Solution,” ASHP, ashp.org. Companies now diversify sourcing and invest in dual-site production, but near-term volatility persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Bacterial Dominance Amid Allergic Acceleration

Bacterial conjunctivitis held 36.90% of conjunctivitis treatment market share in 2025. The segment commands higher per-patient spending because culture-guided antibiotic selection is still the clinical norm. Yet antimicrobial resistance trends are reducing the lifespan of established molecules, encouraging premium-priced next-generation launches. The conjunctivitis treatment market size for bacterial infections is expected to rise steadily alongside diagnostic innovations that enable targeted therapy. Allergic conjunctivitis, advancing at a 6.90% CAGR, benefits from OTC antihistamine uptake and climate-driven pollen surges. Manufacturers add mast-cell stabilizers and anti-inflammatory actives to single-dose vials that address both acute itch and chronic redness. Viral cases remain sizeable, though growth is tempered by the self-limited nature of most infections; demand centers on lubricants and symptom-control formulations.

A shift toward preservative-free multidose bottles now influences product choice across disease categories. Innovations such as cationic-oil micro-emulsions deliver prolonged corneal residence, reducing instillation frequency. Clinical guidelines increasingly advocate combination therapy for mixed-etiology presentations, further expanding average selling prices. Against this backdrop, companies that pivot to broad-spectrum or dual-mechanism formulations secure wider formularies and stronger brand loyalty within the conjunctivitis treatment market.

By Formulation Type: Eye-Drop Supremacy with Ointment Innovation

Eye drops contributed 62.95% of 2025 revenue and remain the default route because patients value quick absorption and minimal vision impairment post-instillation. The conjunctivitis treatment market size attached to drops is projected to grow in line with the overall 3.98% CAGR as dual-action lubricating antibiotics gain traction. However, ointments are set to outpace other formats, expanding at 7.32% CAGR. Advances in nano-lipid carriers have improved spreadability and reduced blurring, making nighttime dosing more acceptable. The conjunctivitis treatment market observes heightened preference among pediatric and geriatric cohorts for ointments that allow once-daily adherence.

Sustained-release in-eye inserts sit at the premium end. Though adoption is nascent, payers show willingness to reimburse when inserts replace multiple drop regimens. Oral agents remain niche, reserved for systemic infections or post-surgical prophylaxis when topical bioavailability proves inadequate. Altogether, formulation diversity underscores the industry’s movement toward convenience without compromising antimicrobial stewardship, a trend that should lift both unit volumes and value-per-unit in the conjunctivitis treatment market.

Geography Analysis

North America led the conjunctivitis treatment market in 2025 with a 32.40% share. Uptake is driven by insurance coverage that defrays branded-drug copays, sophisticated diagnostic labs that pinpoint causative pathogens, and expedited FDA approvals that fast-track novel agents into clinical practice. Generic disruptions, however, expose supply vulnerabilities and occasionally force therapeutic substitutions, stimulating calls for domestic API hubs. Canada’s universal coverage supports equitable access, while Mexico’s expanding retail pharmacy chains boost OTC category growth.

Asia-Pacific is the fastest-expanding territory, registering a 7.18% CAGR. China’s hospital reforms are streamlining ophthalmology workflows, cutting wait times and lifting prescription volumes. India’s tele-ophthalmology pilots screen rural residents and direct confirmed cases to district-level centers, increasing treated incidence. Japan’s rapidly aging population remains susceptible to dry-eye-linked infections, propelling demand for lubricating antibiotics. South Korea’s high digital-content consumption translates into elevated dry-eye episodes that convert to secondary bacterial conjunctivitis, sustaining premium drop sales.

Europe holds a mature share with stable growth. The region’s strict antimicrobial- stewardship protocols temper unnecessary antibiotic use, channeling demand toward narrow-spectrum or combination agents only when culture results justify. Individual markets such as Germany and France favor preservative-free formulations given benzalkonium chloride exposure concerns. Southern European countries are seeing climatically driven allergy seasons that lengthen treatment duration. Middle East and Africa remain under-penetrated but notable public-private eye-care partnerships in the Gulf Cooperation Council are improving access to branded formulations. South America presents restrained, though rising, demand driven by urbanization and insurance reforms that extend ophthalmic cover to broader populations.

Competitive Landscape

The conjunctivitis treatment market is moderately concentrated. AbbVie, Novartis, and Bausch + Lomb collectively occupy a leadership corridor by means of deep R&D pipelines, wide distribution, and continual product-line refreshes. Bausch + Lomb’s 2025 ARVO data release underscored its commitment to evidence-led marketing while reinforcing physician confidence in its expanding dry-eye portfolio[3]Bausch + Lomb Corporation, “Bausch + Lomb Highlights Nearly 40 Scientific Studies at ARVO 2025,” bausch.com. Novartis continues to integrate preservative-free technology across its Sandoz generics to blunt competitive pressure from startups.

Emerging players target white-space opportunities using drug-delivery innovations that extend ocular-surface contact time or leverage biodegradable inserts for eight-hour release. Digital-therapeutic ventures collaborate with ophthalmic multipliers to create screen-time adherence apps that alert users to prophylactic dosing. These value-adds foster brand stickiness in consumer segments with growing self-care preferences.

Strategic moves center on supply-chain resilience. AbbVie has diversified moxifloxacin API sourcing across three continents, while mid-tier firms enter long-term toll-manufacturing agreements to hedge against regional shutdowns. Licensing deals proliferate as innovators out-license early-stage molecules to majors, accelerating global reach. The race for preservative-free multidose technology remains intense because it removes benzalkonium chloride concerns without adding cost-heavy single-use vials, thereby protecting margins across the conjunctivitis treatment market.

Conjunctivitis Treatment Industry Leaders

NicOx S.A.

Novartis AG

Bausch + Lomb

AbbVie Inc

Alembic Pharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Okogen Inc raised USD 3.3 million to complete Phase 2b trials for acute infectious conjunctivitis.

- June 2024: The FDA cleared Xdemvy (lotilaner) drops for Demodex blepharitis, broadening therapeutic options for parasite-linked ocular inflammation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the conjunctivitis treatment market as all prescription or over-the-counter pharmaceutical products, eye drops, ointments, gels, and clinically accepted oral agents, indicated to prevent, relieve, or cure bacterial, viral, or allergic conjunctivitis in humans.

Scope Exclusions: Non-medicated artificial tears sold solely for dry-eye relief and any surgical or device-based interventions are excluded.

Segmentation Overview

- By Disease Type

- Allergic Conjunctivitis

- Bacterial Conjunctivitis

- Viral Conjunctivitis

- By Formulation Type

- Ointments

- Eye Drops

- Oral/Parenteral Drugs

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with hospital ophthalmologists, retail pharmacists, and community optometrists across North America, Europe, and five high-growth Asian nations. The conversations confirmed prevalence drift, real-world prescription mix, and what end-users actually pay, enabling us to tighten every model input.

Desk Research

We began by compiling incidence and treatment-seeking statistics from the US Centers for Disease Control and Prevention, the World Health Organization morbidity database, and regional ministries of health. Trade codes for ophthalmic preparations in UN Comtrade clarified cross-border flows, while peer-reviewed journals such as Ophthalmology and Cornea supplied dosage norms and treated versus untreated ratios.

Company 10-Ks, FDA and EMA approval logs, and news archives on Dow Jones Factiva and D&B Hoovers helped us map launch timelines and price corridors. These examples illustrate the breadth of sources consulted; many other public and paid references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

We applied a top-down epidemiology sheet, country-level conjunctivitis incidence multiplied by treatment penetration and standard therapy days, and then cross-checked totals with sampled manufacturer shipment data and channel checks. Key variables include allergy season length, pediatric contact-lens adoption, OTC switch velocity, average selling price by formulation, regulatory approval cadence, and currency movements. A multivariate regression projects each driver through 2030, and alternate scenarios test sensitivity. Data gaps where supplier volumes were opaque were bridged with region-specific ASP ranges validated in pharmacist surveys.

Data Validation & Update Cycle

Outputs pass three layers of variance screening, peer review, and senior sign-off. Divergences beyond +/-5 percent versus historic sales curves trigger immediate re-contacts. Reports refresh once a year, and if a widespread outbreak or major label change occurs, Mordor Intelligence issues an interim update so clients always have the latest baseline.

Why Our Conjunctivitis Treatment Baseline Commands Trusted Status

Published market values often diverge because firms slice scope, price assumptions, and refresh timing in different ways.

Key gap drivers include alternate models that blend generic dry-eye lubricants with conjunctivitis therapies, apply flat global ASPs, or extend straight-line CAGRs beyond regulatory inflection points. According to Mordor Intelligence, our file isolates conjunctivitis-specific drugs, converts revenues at prevailing rates, and revalidates every variable with frontline clinicians each year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.53 B (2025) | Mordor Intelligence | |

| USD 5.30 B (2024) | Global Consultancy A | Includes dry-eye lubricants and device revenues; flat ASP assumption |

| USD 4.30 B (2023) | Industry Association B | Hospital-only sales, excludes OTC channels and Asia-Pacific markets |

In sum, the disciplined scoping, live clinical inputs, and annual refresh cycle practiced by Mordor Intelligence provide decision-makers with a balanced, transparent foundation they can trace and reuse with confidence.

Key Questions Answered in the Report

What is the current conjunctivitis treatment market size?

The conjunctivitis treatment market size stands at USD 4.71 billion in 2026.

How fast will the conjunctivitis treatment market grow?

The market is forecast to expand at a 3.98% CAGR, reaching USD 5.72 billion by 2031.

Which disease segment is expanding the fastest?

Allergic conjunctivitis is the fastest-growing segment, projected at a 6.90% CAGR through 2031.

What formulation type is gaining momentum?

Ointments are set to rise at a 7.32% CAGR due to extended-release technologies that improve comfort and adherence.

Which region offers the strongest growth potential?

Asia-Pacific posts the highest regional CAGR at 7.18% thanks to widening healthcare access and tele-ophthalmology rollouts.

Page last updated on: