Quartz Crystal Oscillators Market Size and Share

Market Overview

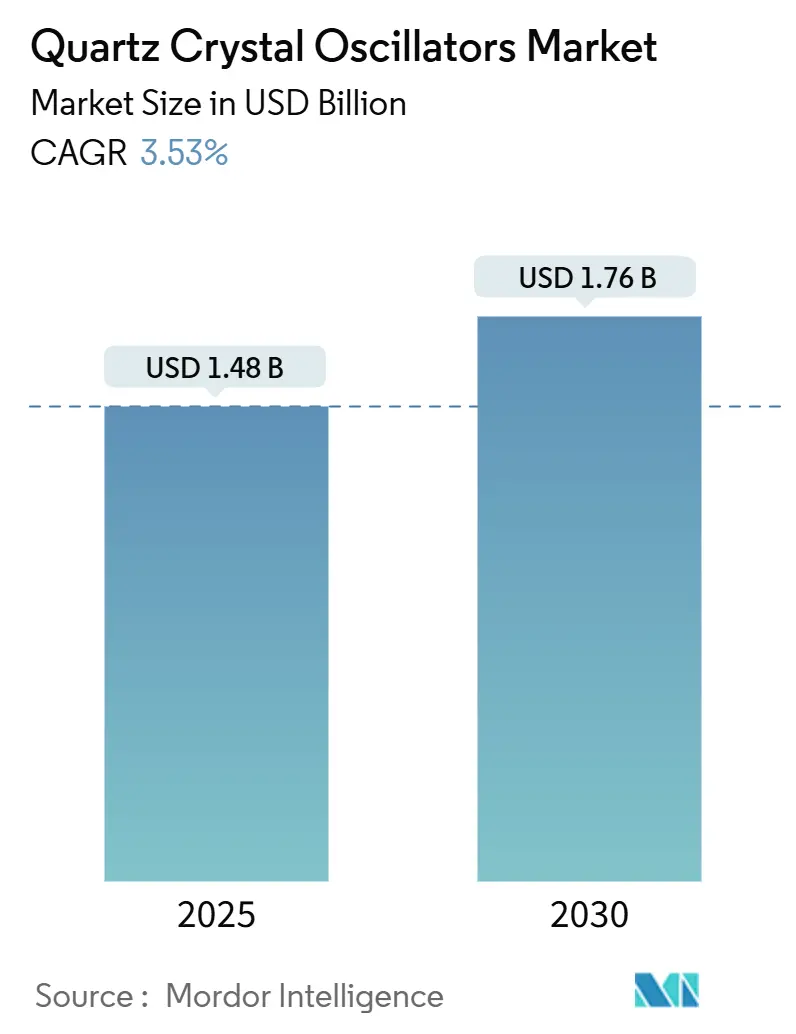

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.48 Billion |

| Market Size (2030) | USD 1.76 Billion |

| Growth Rate (2025 - 2030) | 3.53% CAGR |

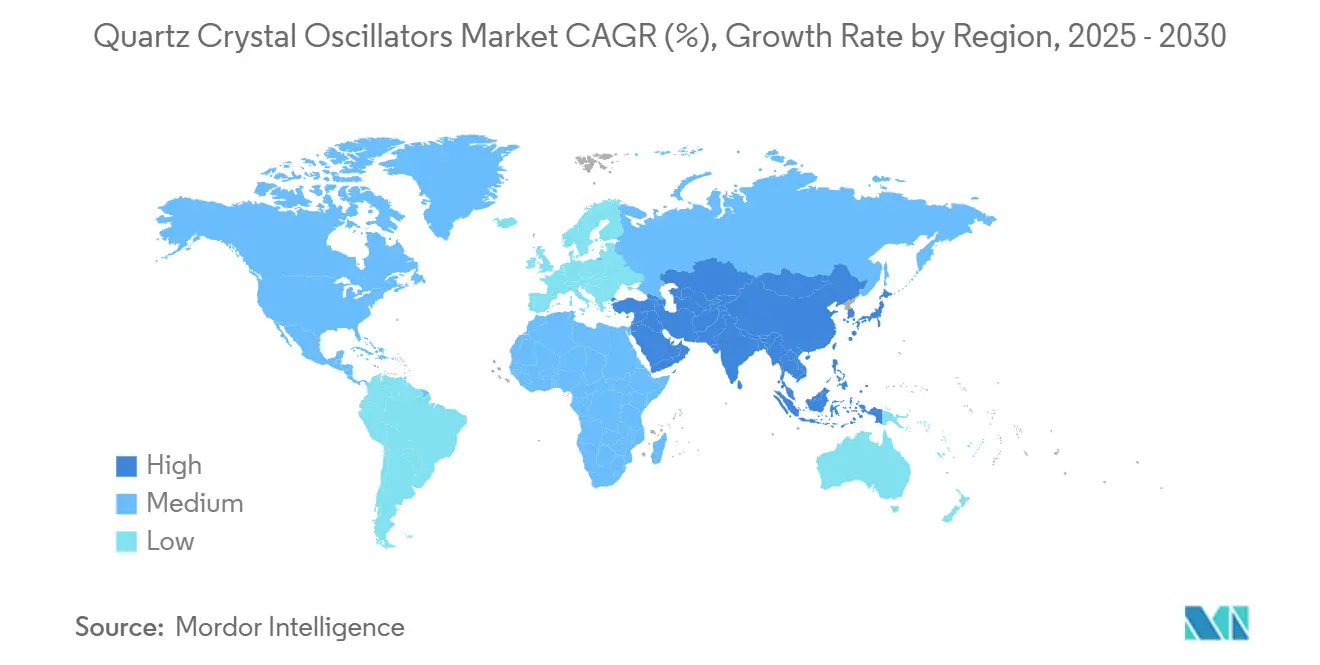

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Quartz Crystal Oscillators Market Analysis by Mordor Intelligence

Quartz crystal oscillators market revenue reached USD 1.48 billion in 2025 and is forecast to climb to USD 1.76 billion by 2030, reflecting a steady 3.53% CAGR as demand for precise timing solutions spreads from smartphones to 5G base-stations and low-earth-orbit satellites. The measured growth underscores a maturing yet resilient landscape in which quartz continues to outperform rival technologies on phase-noise, power consumption and start-up time. Expansion of semiconductor fabs in Asia-Pacific, accelerated electrification of vehicles, and migration of hyperscale data-centres to 400/800 G optical links are the principal catalysts. At the same time, supply-chain shocks in high-purity quartz and mounting competition from MEMS oscillators moderate the trajectory yet fail to displace the incumbent technology in high-precision niches.

Key Report Takeaways

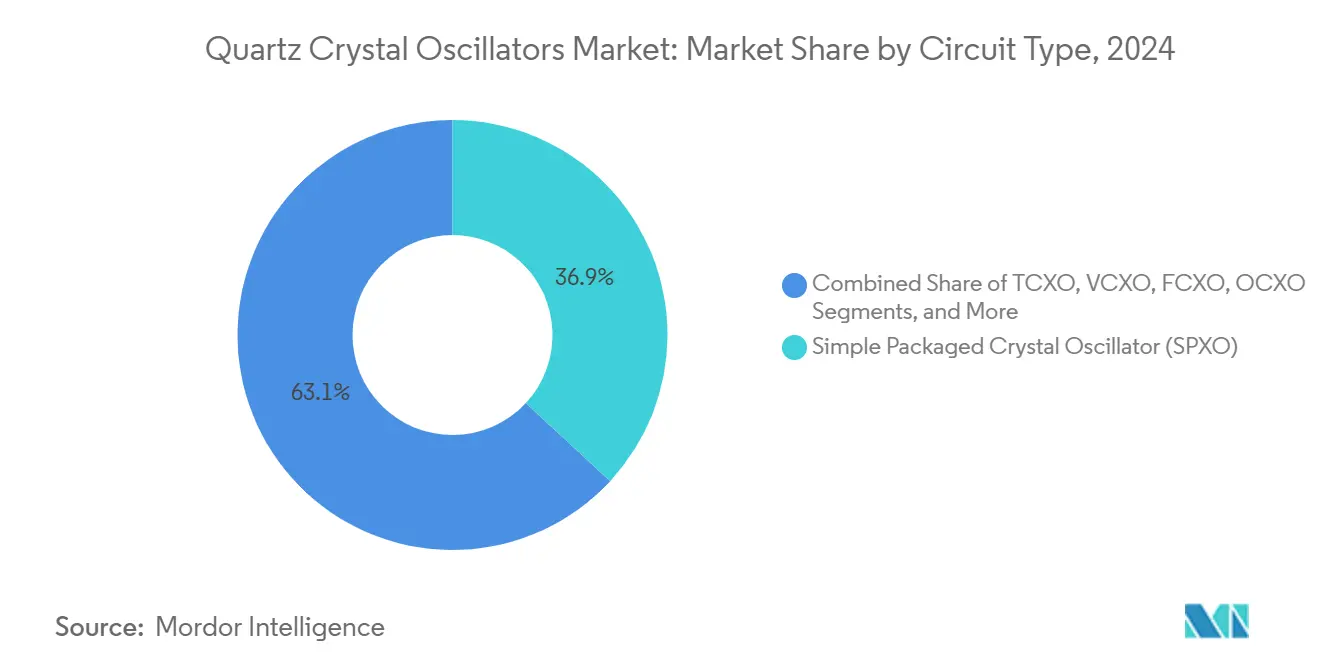

- By circuit type, Simple-Packaged Crystal Oscillators led with 36.9% of Quartz crystal oscillators market share in 2024, whereas Temperature-Compensated devices are set to expand at a 4.2% CAGR through 2030.

- By mounting type, surface-mount packages held 81.7% share of the Quartz crystal oscillators market size in 2024 and through-hole formats log the fastest projected 3.7% CAGR to 2030.

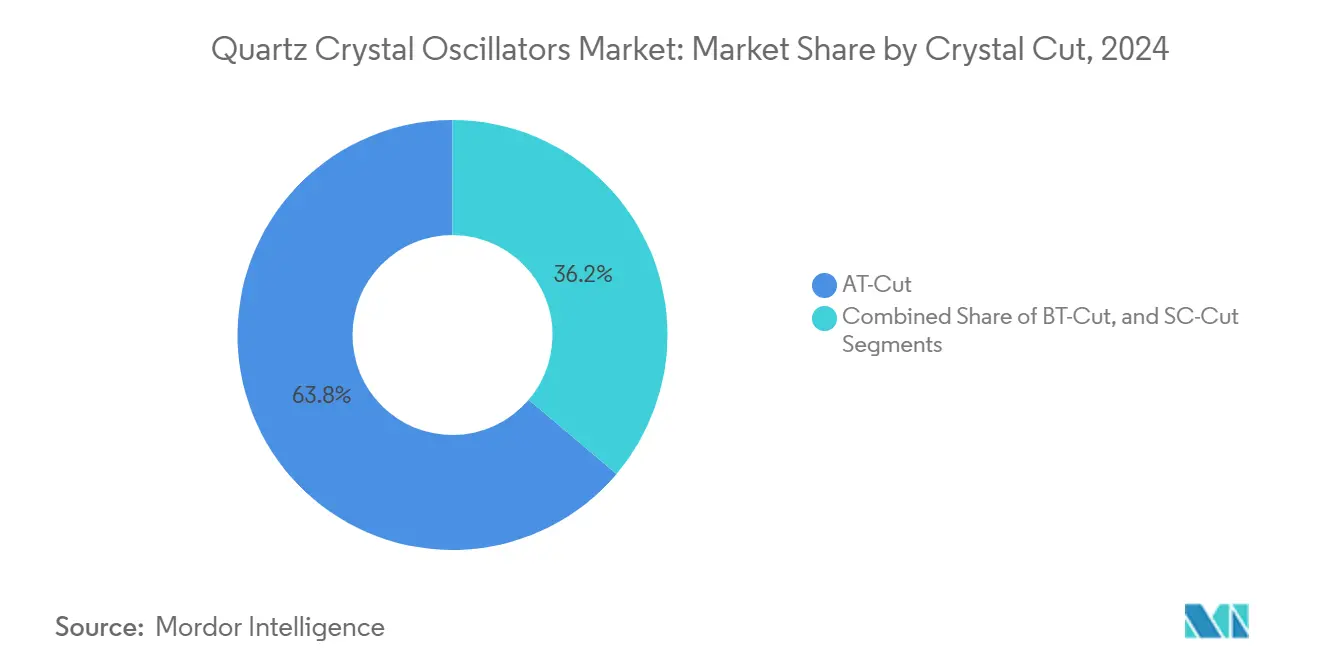

- By crystal cut, AT-cut units accounted for 63.8% share of the Quartz crystal oscillators market size in 2024; SC-cut variants lead growth at 4.6% CAGR.

- By end-user, consumer electronics retained 41.2% revenue share in 2024, while automotive demand advances at a 5.1% CAGR as electric-drive and ADAS architectures proliferate.

- By geography, Asia-Pacific commanded 45.6% revenue in 2024; the Middle East records the quickest 3.9% CAGR as 5G and smart-city programmes accelerate.

Global Quartz Crystal Oscillators Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G base-stations elevating high-stability timing demand | 0.80% | Global, led by APAC & North America | Medium term (2-4 years) |

| ADAS & autonomous driving electronics requiring low-jitter clock sources | 0.60% | North America, Europe, China | Medium term (2-4 years) |

| Miniaturisation trend in wearables fuelling µ-package XTAL adoption | 0.40% | Global consumer-electronics hubs | Short term (≤ 2 years) |

| Industry 4.0 retro-fits boosting industrial-grade TCXO uptake | 0.30% | Europe & North America corridors | Long term (≥ 4 years) |

| Satellite mega-constellations expanding OCXO deployment | 0.20% | Global, US & China lead | Long term (≥ 4 years) |

| Data-centre migration to 400/800 G driving low-phase-noise VCXO | 0.50% | North America, Europe, APAC | Medium term (2-4 years) |

Source: Mordor Intelligence

Proliferation of 5G Base-Stations Elevating High-Stability Timing Demand

The shift from 4G frequency-only synchronisation to 5G’s time-division-duplex architecture imposes UTC-traceable phase accuracy within ±1.5 µs, compelling operators to deploy ePRTC-grade OCXOs and TCXOs in radio heads and grandmasters.[1]Microchip Technology, “Synchronizing 5G Networks with Timing Design and Management,” microchip.comSpecifications such as ITU-T G.8272.1 prescribe ±30 ns limits, encouraging vendors like Rakon to miniaturise OCXOs able to holdover during GNSS loss. Each small-cell node in dense urban layouts now embeds its own precision source, multiplying unit demand as macro-only roll-outs give way to distributed antenna systems. Solutions such as Oscilloquartz OSA 5430 integrate optical atomic references to future-proof 5G timing architectures, reinforcing quartz relevance where picosecond-level jitter tolerance is mandatory. [2]Oscilloquartz, “Synchronizing 5G Networks,” oscilloquartz.com

ADAS and Autonomous Driving Electronics Requiring Low-Jitter Clock Sources

Level-3 autonomy increases sensor fusion and real-time compute loads that must align to sub-ns windows over automotive Ethernet. Skyworks and SiTime have qualified low-jitter oscillators to AEC-Q100 and ISO 26262 standards, delivering power budgets below 1 µW for always-on domains while surviving vibration peaks above 20 g.[3]Skyworks Solutions, “Automotive – ADAS and Automated Driving,” skyworksinc.com TDK forecasts 27% electric-vehicle production growth, implying a parallel expansion in timing nodes per chassis as zonal ECUs replace distributed architectures. Centralised processors linked by PCIe demand clock sources with RMS phase-noise under 100 fs, a threshold still favouring quartz in high-reliability settings.

Miniaturisation Trend in Wearables Fuelling µ-Package XTAL Adoption

Wearable form-factors compress by double-digit percentages each design cycle. Daishinku’s 1.6 × 1.2 mm DSO1612AR occupies just 58% of its predecessor’s volume yet covers 0.6-80 MHz, supporting everything from BLE beacons to GNSS receivers. Epson’s vertically integrated quartz growth enables defect-free wafers essential for die-level lithography that scales below 0.5 mm thickness. Medical wearables need timing references that survive sweat-induced corrosion and 10 °C body-temperature swings without recalibration, reinforcing demand for hermetically sealed SMD crystals.

Industry-4.0 Retro-fits in Brown-Field Plants Boosting Industrial-Grade TCXO Uptake

Deterministic Ethernet upgrades in legacy factories rely on IEEE 802.1AS profiles achieving sub-µs accuracy across daisy-chained switches. Texas Instruments’ Sitara processors integrate TSN hardware, but network latency still hinges on the local oscillator’s temperature coefficient. Industrial-grade TCXOs, rated -40 °C to +105 °C and shielded for EMI immunity, satisfy retrofit constraints where through-hole cards are replaced in-situ without climate control. Analog Devices highlights that every millisecond drift in multiaxis robotics elongates toolpath execution and raises scrap rates, linking timing precision directly to yield

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of MEMS-based silicon oscillators cannibalising entry-level SPXO | -0.90% | Global consumer segments | Short term (≤ 2 years) |

| Price volatility in high-purity synthetic quartz supply chain | -0.40% | Global high-end users | Medium term (2-4 years) |

| Natural-disaster disruptions at Spruce Pine source mine | -0.30% | North America-centric supply | Short term (≤ 2 years) |

| High power consumption restraining OCXO use in mobile devices | -0.20% | Global telecom & IoT | Medium term (2-4 years) |

Source: Mordor Intelligence

Emergence of MEMS-Based Silicon Oscillators Cannibalising Entry-Level SPXO

SiTime and a handful of rivals now ship programmable MEMS clocks that withstand 50,000 g shocks and operate up to 125 °C, benefits that resonate in smart-phones, action cameras and industrial IoT . Unit absorption escalated after SiTime posted USD 144 million revenue in 2024, up seven-fold in a decade, indicating broad acceptance in cost-sensitive designs. Yet quartz retains supremacy where 0.18 ps rms phase-noise, 3 mA supply current and sub-100 µs start-up dominate the specification sheet, sustaining the Quartz crystal oscillators market at the high-performance end.

Price Volatility in High-Purity Synthetic Quartz Supply Chain

urricane Helene exposed the fragility of a supply chain in which Spruce Pine mines deliver up to 90% of 99.9%-pure SiO₂ feedstock for semiconductor fabs. Producers of OCXOs and TCXOs that require ultra-low alkali content faced spot-price spikes exceeding 35% in late 2024. China’s April 2025 discovery of new deposits may diversify sources, but purification know-how and qualification cycles extend beyond the forecast horizon. Such volatility squeezes margins for oscillator vendors tied to long-term fixed-price contracts with telecom OEMs.

Segment Analysis

By Circuit Type: TCXO Growth Outpaces Traditional SPXO Dominance

SPXOs held 36.9% of the Quartz crystal oscillators market in 2024, reflecting their ubiquity in mass-market electronics. TCXOs, while accounting for a smaller slice today, are projected to expand 4.2% annually as 5G radios, Industry 4.0 gateways and ADAS modules place thermal-stability above BOM cost. VCXOs uphold a niche in optical interconnects where the Quartz crystal oscillators market size requirement ties directly to phase-locked loop accuracy at 56 Gbps and above.

NDK, Epson and Rakon race to shrink power draw in OCXOs so that sub-ppb stability migrates from core networks to edge nodes. Epson’s OG7050CAN, 85% smaller than legacy devices yet delivering 56% lower power, signals a pathway for OCXO penetration into rack-mounted base-band units . Meanwhile, FCXO architectures surface in quantum-computing testbeds that demand 10⁻¹⁴ short-term stability unattainable by standard cuts. The resulting mix preserves the fragmented character of the Quartz crystal oscillators market while enabling specialist suppliers to capture outsized margins.

Note: Segment shares of all individual segments available upon report purchase

By Mounting Type: Surface-Mount Dominance Reflects Miniaturisation Imperative

Surface-mount packages accounted for 81.7% revenue in 2024 as smartphones, wearables and IoT sensors pursue reflow-solderable components compatible with automated pick-and-place lines. The Quartz crystal oscillators market continues shifting toward chip-scale and µ-package footprints, with Daishinku’s 0.5 mm-high SPXOs setting industry benchmarks in volumetric efficiency.

Through-hole formats still chart a 3.7% CAGR because defense avionics and harsh-environment machinery favour socketed replacements that survive repeated thermal cycling. Large-body oscillators also host heater-regulated chambers indispensable for high-end OCXOs, sustaining a profitable if narrow segment. Supplier differentiation now hinges on plating chemistry and lead-free solderability, parameters that protect installed bases across automotive and rail signalling where design lifecycles exceed 15 years.

By Crystal Cut: AT-Cut Stability Meets SC-Cut Innovation

AT-cut blanks delivered 63.8% share of 2024 revenue owing to balanced cost, temperature drift and manufacturability. SC-cut devices, although dearer, grow 4.6% annually as telecom backhaul and satellite payloads insist on drift below 20 ppb per year. The Quartz crystal oscillators market size attached to SC-cut resonators thus rises disproportionately to their unit volume.

Process yield improvements shrink the premium once associated with SC-cut angles that deviate by mere arc-seconds. Vendors now deploy laser-alignment tooling and X-ray diffraction feedback to elevate throughput, making SC-cut variants viable for remote-radio-head deployments where operating budgets tighten. BT-cut crystals persist in real-time clocks at 32.768 kHz, ensuring the Quartz crystal oscillators market covers both extremes of frequency and stability.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Automotive Acceleration Challenges Consumer Electronics Leadership

Consumer electronics sustained 41.2% share in 2024, yet growth normalises as handset saturation peaks. Automotive applications expand 5.1% annually, reflecting surging ECU counts in battery-electric vehicles, lidar modules and vehicle-to-everything (V2X) gateways. Each platform needs multiple redundant timing channels, pushing the Quartz crystal oscillators market deeper into AEC-Q200 grade production.

Telecom networks remain pivotal, absorbing OCXOs and TCXOs that anchor ePRTC nodes and PTP grandmasters. Industrial users are retrofitting brown-field factories with TSN-enabled switches; deterministic control loops thereby enlarge addressable demand for temperature-hardened oscillators. Aerospace and defense purchasers, though volume-small, procure radiation-hardened variants priced at multi-hundred USD, bolstering the blended ASP for the Quartz crystal oscillators market.

Geography Analysis

Asia-Pacific commanded 45.6% of 2024 revenue as China, Japan and South Korea manufactured more than 70% of global chips and housed tier-one oscillator makers. SEMI projects wafer starts in the region to climb 7% in 2025, translating into incremental pull-through for timing devices across test-and-measurement benches and lithography steppers. Japan’s heritage suppliers such as NDK and Epson exploit local quartz mines and vertically integrated fabs to retain leadership in sub-pS jitter performance.

North America benefits from hyperscale data-centre build-outs and a vibrant aerospace sector. RTX recorded USD 80.7 billion sales in 2024, underlining defense programmes that specify rad-hard quartz oscillators in missile guidance and secure communication payloads. Europe advances industrial-automation and electric-vehicle ecosystems that favour TCXO deployments for deterministic networking; Germany’s Industry 4.0 initiatives and France’s manufacturing revitalisation create tailwinds despite macroeconomic slowdowns.

The Middle East, while currently holding a modest slice, registers the fastest 3.9% CAGR to 2030 as operators in the United Arab Emirates and Saudi Arabia fast-track 5G and smart-city grids. National diversification drives semiconductor assembly programmes that in turn consume discrete timing parts. Latin America and Africa lag broader adoption because 4G still predominates and electronics production remains limited, yet small-cell densification and IoT agriculture pilots hint at incremental demand that sustains global volume growth within the Quartz crystal oscillators market.

Competitive Landscape

The market remains moderately fragmented. The top five vendors combine for roughly 55% of global shipments, leaving ample room for regional specialists. NDK posted JPY 50.31 billion revenue and JPY 2.33 billion net income in FY 2024, leveraging proprietary crystal-growth furnaces and global back-end plants Finas. Epson capitalises on complete vertical integration from synthetic quartz pulling to automated dicing, yielding defect densities that underpin its leadership in µ-sized packages.

Murata reported 883.5 billion yen sales in Q2 2024, driven by smartphone RF modules that embed multi-output clock generators. Rakon, meanwhile, pursues niche leadership with MercuryX that fuses ASIC drivers and XMEMS resonators targeting AI server clock trees. SiTime’s MEMS portfolio continues to challenge quartz incumbents in harsh-motion and high-temperature domains, yet its technology coexists rather than fully displaces quartz because telecom and satellite integrators still mandate picosecond-class phase-noise unattainable via capacitive MEMS actuation.

Strategic moves in 2024 included Epson’s launch of a 56% lower-power OCXO for edge-compute blades, NDK’s capacity expansion in Malaysia to mitigate single-site risk, and SiTime’s partnership with NVIDIA to synchronise GPU lanes inside AI clusters. M&A activity stays muted as antitrust scrutiny discourages consolidation that might elevate component ASPs, sustaining the broadly competitive profile of the Quartz crystal oscillators market.

Quartz Crystal Oscillators Industry Leaders

-

Nihon Dempa Kogyo Co., Ltd. (NDK)

-

Epson Device Corporation

-

Daishinku Corp. (KDS)

-

Murata Manufacturing Co., Ltd.

-

Microchip Technology Inc. (Microsemi/Vectron)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SiTime introduced its Super-TCXO MEMS clock optimised for AI workloads, promising substantial data-centre energy savings

- January 2025: Microchip launched the SA65-LN chip-scale atomic clock combining crystal and atomic references for low-power aerospace timing

- January 2025: Texas Instruments reported Q4 2024 revenue of USD 4.01 billion, with analog clocks contributing to segment resilience

- October 2024: Epson unveiled the OG7050CAN OCXO, 85% smaller and 56% more efficient, tailored for base-stations and data-centres

Global Quartz Crystal Oscillators Market Report Scope

Quartz crystal oscillator makes use of quartz crystal as a frequency selective element for obtaining an inverse piezoelectric effect. It uses the mechanical resonance of the vibrating crystal that has piezoelectric properties to obtain an electric signal with a high-precision frequency. The study considers different types of quartz crystal oscillators and mounting types, along with the applications in the end-user industries, geographical developments, and driving factors in global and regional markets which influence the demand for quartz crystal oscillators. The study also covers the impact of COVID-19 on the market.

| By Circuit Type | Simple Packaged Crystal Oscillator (SPXO) | |||

| Temperature-Compensated Crystal Oscillator (TCXO) | ||||

| Voltage-Controlled Crystal Oscillator (VCXO) | ||||

| Frequency-Controlled Crystal Oscillator (FCXO) | ||||

| Oven-Controlled Crystal Oscillator (OCXO) | ||||

| Other Circuit Types | ||||

| By Mounting Type | Surface-Mount | |||

| Thru-Hole | ||||

| By Crystal Cut | AT-Cut | |||

| BT-Cut | ||||

| SC-Cut | ||||

| By End-User | Consumer Electronics | |||

| Telecom and Networking | ||||

| Industrial Automation and IoT | ||||

| Automotive (ADAS, Infotainment, EV Powertrain) | ||||

| Aerospace and Defense | ||||

| Medical and Healthcare Devices | ||||

| Others | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Nordics | ||||

| Rest of Europe | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South-East Asia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | ||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Simple Packaged Crystal Oscillator (SPXO) |

| Temperature-Compensated Crystal Oscillator (TCXO) |

| Voltage-Controlled Crystal Oscillator (VCXO) |

| Frequency-Controlled Crystal Oscillator (FCXO) |

| Oven-Controlled Crystal Oscillator (OCXO) |

| Other Circuit Types |

| Surface-Mount |

| Thru-Hole |

| AT-Cut |

| BT-Cut |

| SC-Cut |

| Consumer Electronics |

| Telecom and Networking |

| Industrial Automation and IoT |

| Automotive (ADAS, Infotainment, EV Powertrain) |

| Aerospace and Defense |

| Medical and Healthcare Devices |

| Others |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Quartz crystal oscillators market?

The market generated USD 1.48 billion revenue in 2025 and is projected to reach USD 1.76 billion by 2030 at a 3.53% CAGR.

Which circuit type grows the fastest?

Temperature-Compensated Crystal Oscillators (TCXO) expand at 4.2% annually through 2030, outpacing other circuit categories.

Why does Asia-Pacific hold the largest regional share?

High semiconductor fabrication density in China, Japan and South Korea underpins 45.6% of 2024 revenues, supported by continual fab capacity expansion.

How are MEMS oscillators influencing the market outlook?

MEMS devices capture cost-sensitive consumer segments and trim growth by about 0.9 percentage points, yet quartz remains favoured where picosecond-level jitter and low power draw are critical.