In-Silico Drug Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

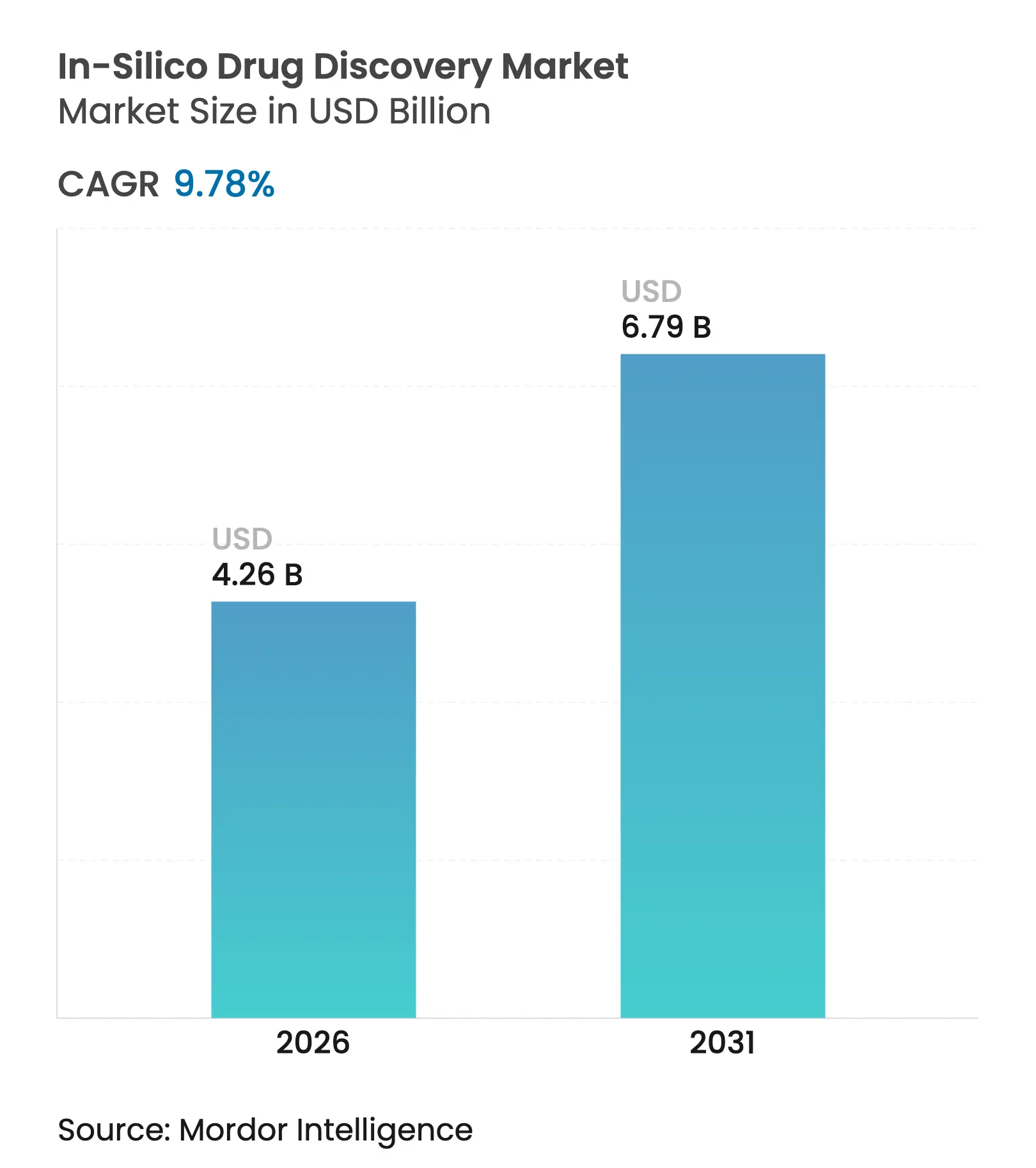

| Market Size (2026) | USD 4.26 Billion |

| Market Size (2031) | USD 6.79 Billion |

| Growth Rate (2026 - 2031) | 9.78 % CAGR |

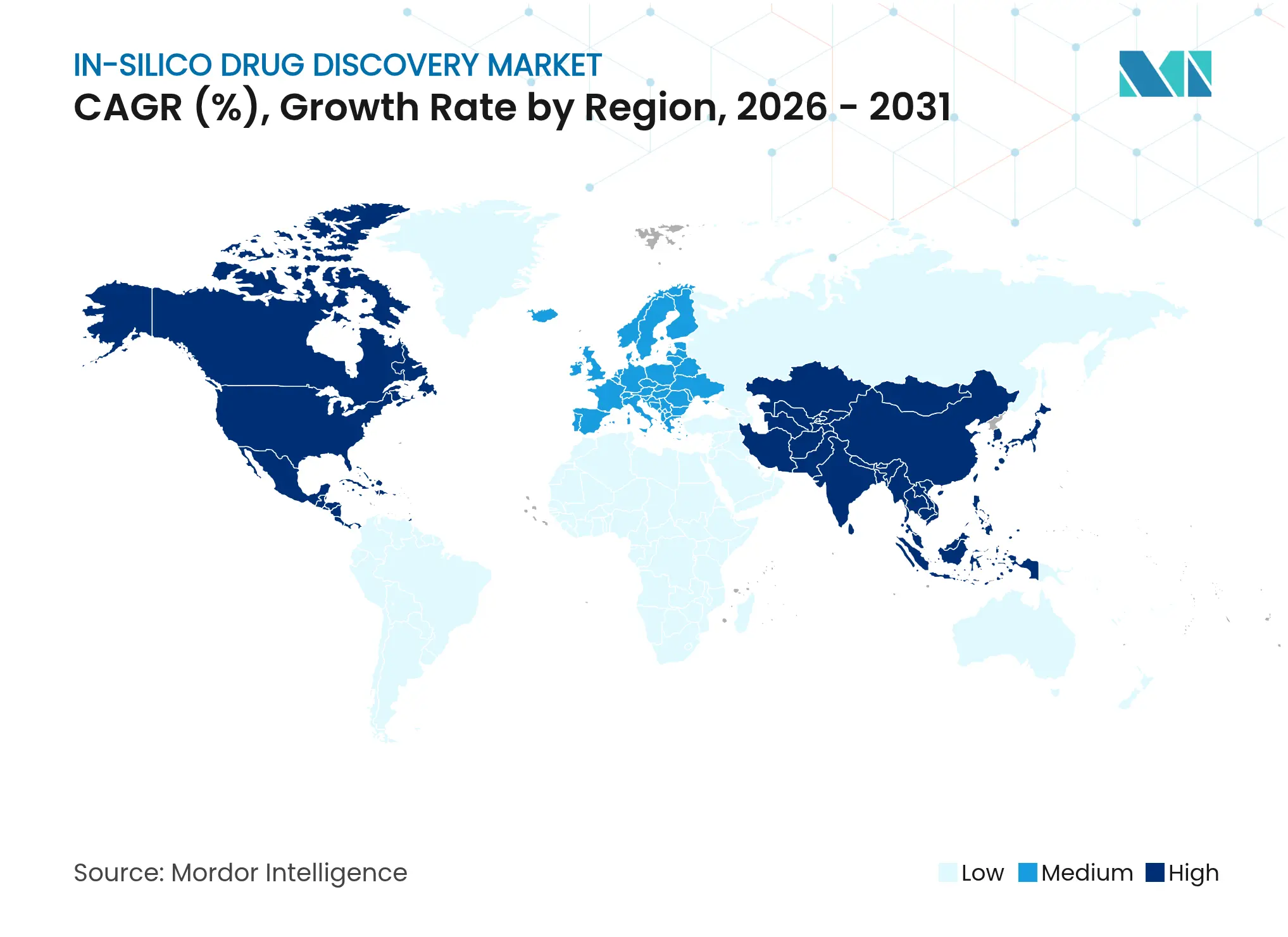

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

In-Silico Drug Discovery Market Analysis by Mordor Intelligence

In-Silico Drug Discovery market size in 2026 is estimated at USD 4.26 billion, growing from 2025 value of USD 3.88 billion with 2031 projections showing USD 6.79 billion, growing at 9.78% CAGR over 2026-2031. Growth reflects rising adoption of virtual screening, predictive modeling, and quantum-ready simulations that are compressing discovery timelines from years to months while curbing escalating R&D expenses that now exceed USD 2.6 billion per approved therapy. Pharmaceutical companies are integrating cloud-native high-performance computing (HPC) to democratize access for smaller biotechnology firms, while regulators are publishing AI guidance that clarifies credibility requirements for computational models[1]Source: Nature Communications Medicine, “Clinical-stage AI-designed Candidates,” nature.com. Consolidation is accelerating as incumbents acquire AI-native platforms to secure differentiated algorithms and automated synthesis. Investment in quantum-enhanced pipelines, which can resolve molecular dynamics beyond classical limits, signals an impending leap in simulation accuracy that will reshape candidate prioritization.

Key Report Takeaways

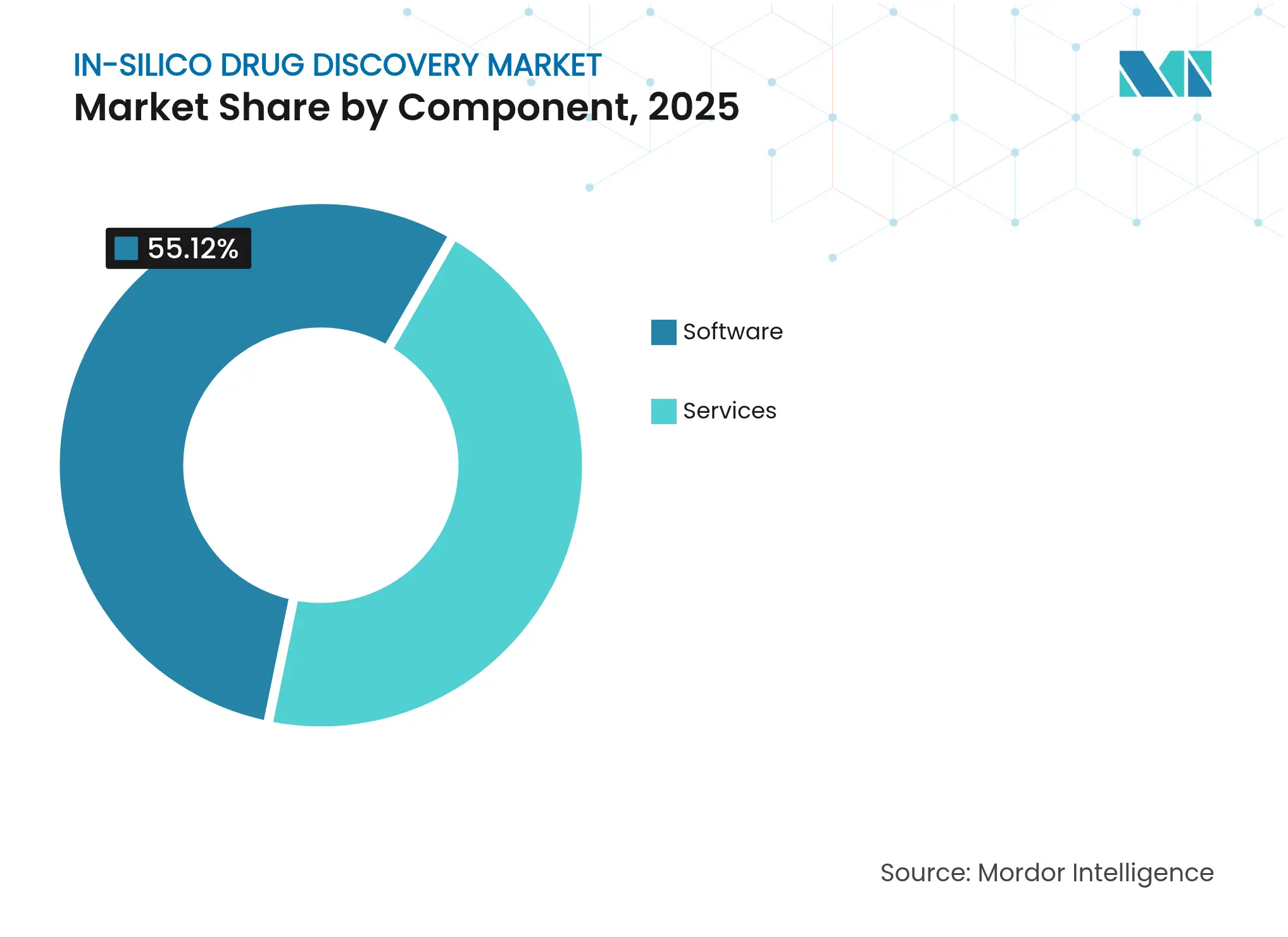

- By component, software led with 55.12% revenue share in 2025; services posted the fastest 6.93% CAGR through 2031.

- By drug discovery phase, the target identification & validation commanded 46.82% of the market share in 2025, while the hit identification is projected to advance at a 7.34% CAGR to 2031.

- By therapeutic area, oncology accounted for 36.61% of the market size in 2025; neurology is expanding at an 8.83% CAGR through 2031.

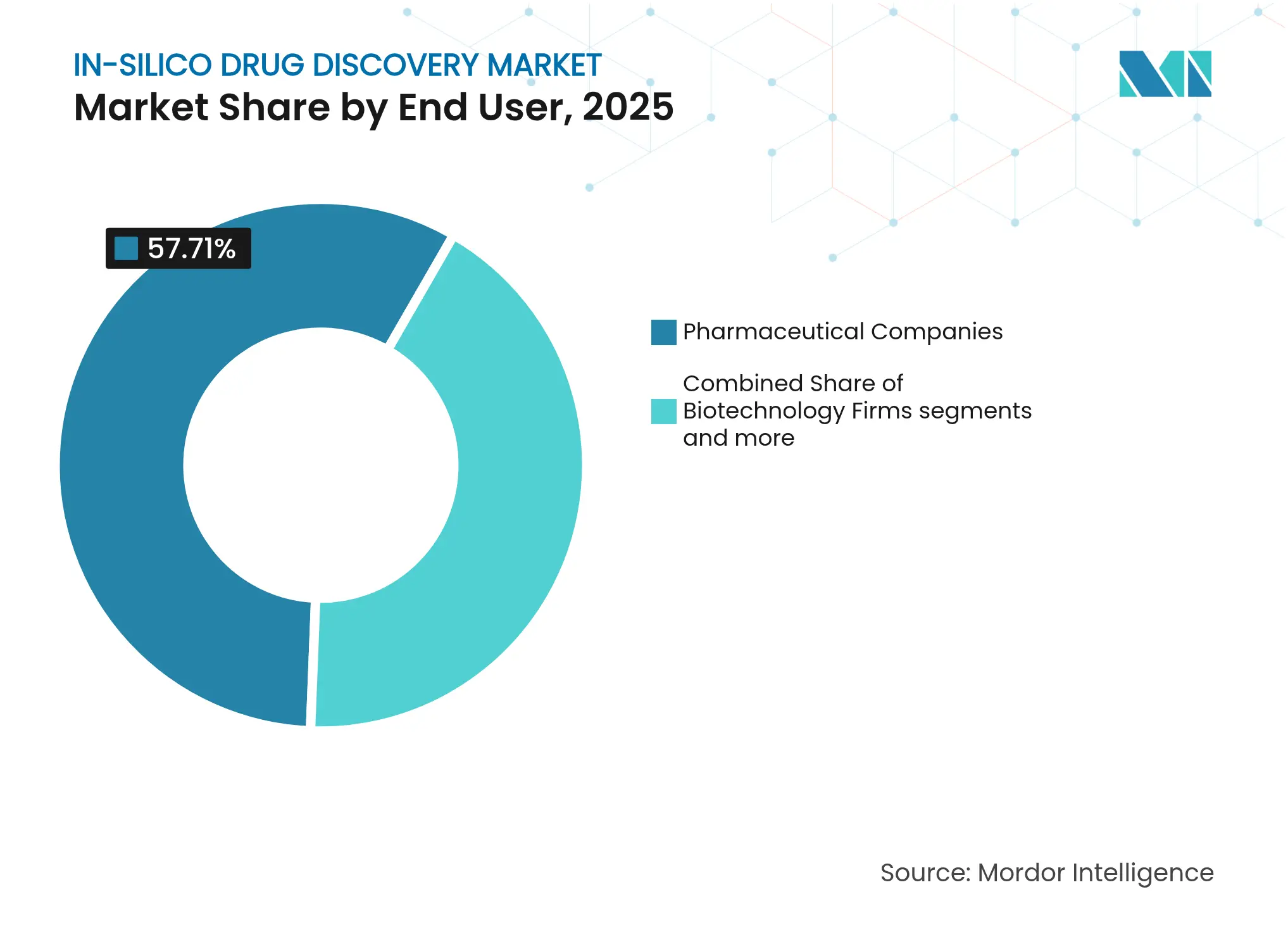

- By end user, pharmaceutical and biotechnology companies controlled a 57.71% share in 2025, whereas CROs are on track for an 8.33% CAGR through 2031.

- By deployment mode, cloud-based controlled 67.22% share in 2025, and is on track for a 7.81% CAGR through 2031.

- By geography, North America retained a 37.61% share in 2025; Asia-Pacific records the strongest 8.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In-Silico Drug Discovery Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating AI Adoption In Hit Identification

Escalating AI Adoption In Hit Identification

| +2.1% | Global, with early gains in US, EU, China | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Global, with early gains in US, EU, China

|

Impact Timeline

:

Short term (≤ 2 years)

|

Cloud-Native HPC Lowering Entry Barriers

Cloud-Native HPC Lowering Entry Barriers

| +1.8% | Global, accelerated in emerging markets | Medium term (2-4 years) | |||

Rising R&D Costs Pressuring ROI

Rising R&D Costs Pressuring ROI

| +1.5% | Global pharmaceutical hubs | Short term (≤ 2 years) | |||

Pharma Shift To Fail-Fast Virtual Screens

Pharma Shift To Fail-Fast Virtual Screens

| +1.3% | North America & EU, spill-over to APAC | Medium term (2-4 years) | |||

Regulatory Sandboxes For In-Silico Trials

Regulatory Sandboxes For In-Silico Trials

| +0.9% | US FDA, EMA regions, select APAC markets | Long term (≥ 4 years) | |||

Digital-Twin Pipelines For Precision Meds

Digital-Twin Pipelines For Precision Meds

| +0.7% | Advanced healthcare systems globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating AI Adoption in Hit Identification

Generative AI platforms now underpin more than 70 clinical-stage candidates, reflecting rapid integration of language models with molecular design workflows[2]Source: U.S. Food and Drug Administration, “Considerations for Use of AI to Support Regulatory Decision-Making,” fda.gov . INS018_055, the first fully AI-designed molecule to reach Phase 2, demonstrated a discovery cycle of 18 months rather than the historical multi-year average. Atomwise’s 318-target study confirmed that algorithmic exploration of chemical space yields structurally novel scaffolds at scale. Oncology programs benefit most, as AI can interrogate complex tumor heterogeneity to surface undruggable pathways. The next inflection will couple quantum hardware with AI to refine binding free-energy calculations, unlocking more precise affinity predictions that strengthen early-stage triaging.

Cloud-Native HPC Lowering Entry Barriers

Subscription-based HPC delivered through hyperscale clouds lets start-ups run multi-million-compound screens without capital-intensive server clusters. Exscientia launched an AWS-powered pipeline that combines generative design with robotic labs, compressing design–make–test cycles and enabling 24/7 unattended synthesis. Pharmaceutical majors increasingly integrate Google Vertex AI for federated model training, allowing internal datasets to remain behind firewalls while contributing insights to global models. In Asia-Pacific, cloud uptake bypasses infrastructure deficits, steering the region toward double-digit adoption growth. Dense security and compliance tooling from providers has dispelled earlier data-sovereignty concerns, stimulating enterprise-scale migrations.

Rising R&D Costs Pressuring ROI

The average investment to secure one new molecular entity surpassed USD 2.6 billion in 2024, amplifying demand for predictive simulations that curtail late-stage failures. Clinical attrition remains near 90%, so modelling toxicity and pharmacokinetics digitally before animal studies can conserve hundreds of millions per asset. Quantum-ready workflows already deliver thousands of viable leads against cancer proteins in silico, highlighting cost-saving potential. Economics are especially acute in rare diseases with small patient pools, where virtual approaches make niche programs commercially feasible. In response, top pharmas now earmark up to USD 25 million annually for quantum-computing pilots, betting that sub-angstrom accuracy will further de-risk pipelines.

Pharma Shift to “Fail-Fast” Virtual Screens

Drug developers increasingly stage million-molecule virtual libraries before committing chemistry resources, rejecting weak binders within days. Digital-twin patient cohorts simulate efficacy and safety, and the US FDA has broadened its definition of in-silico trials to include these complex models. Model Medicines achieved a perfect hit rate on antiviral prioritization by embedding generative AI within iterative screen–validate cycles . As structural databases expand, AI can explore chemical neighborhoods that were once computationally prohibitive, allowing discovery programs to pivot rapidly toward viable scaffolds. This mindset accelerates decision-making and aligns with investors’ preference for capital-efficient milestones

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Model Bias From Legacy Datasets

Model Bias From Legacy Datasets

| -1.2% | Global, acute in diverse population studies | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.2%

|

Geographic Relevance

:

Global, acute in diverse population studies

|

Impact Timeline

:

Medium term (2-4 years)

|

Shortage Of Computational Chemists

Shortage Of Computational Chemists

| -1.0% | Global, severe in emerging markets | Long term (≥ 4 years) | |||

IP Ambiguity For AI-Generated Molecules

IP Ambiguity For AI-Generated Molecules

| -0.8% | Global, regulatory uncertainty worldwide | Long term (≥ 4 years) | |||

Quantum-Hardware Cost Constraints

Quantum-Hardware Cost Constraints

| -0.6% | Advanced research institutions globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Model Bias from Legacy Datasets

Historical repositories under-represent diverse ethnic groups and rare disease phenotypes, risking biased AI outputs that underperform in real-world populations. Molecule libraries often skew toward well-studied scaffolds, limiting algorithmic creativity for neglected conditions. Regulators now mandate diversity audits for training data, prompting companies to invest in consortia that curate inclusive datasets. Without remediation, biased predictions could place patients at risk and expose sponsors to regulatory setbacks, damping adoption rates among cautious stakeholders.

Shortage of Computational Chemists

Industry demand for AI-literate chemists outpaces graduate output, straining project timelines and inflating talent costs. Specialized programs such as UCSF’s AI-driven drug-discovery MSc enroll limited cohorts, insufficient to satisfy global needs. Companies are countering with online certifications from Schrödinger and internal academies that upskill bench scientists in coding, yet progress is gradual. Talent gaps are pronounced in Asia-Pacific where market growth outruns local training capacity, leading firms to outsource tasks to CROs. Persistent shortages risk slowing algorithm deployment and widening performance disparities between resource-rich multinationals and smaller entrants.

Segment Analysis

By Component: Software Platforms Extend Dominance

Software held 55.12% of 2025 revenue as laboratories converged wet-bench data, cheminformatics, and bioinformatics into unified workspaces that streamline decision flow within the In-Silico Drug Discovery market. These platforms offer modular subscription tiers, easing upgrades and facilitating quantum-mechanics plug-ins that elevate docking fidelity. Services, however, are forecast to grow 6.93% annually as firms lacking internal AI teams outsource algorithm refinement and validation to specialist CROs.

Software suites from Schrödinger and Chemical Computing Group embed quantum mechanics and free-energy perturbation methods, broadening molecular-property prediction accuracy. Cloud-native deployments eliminate hardware limitations, enticing venture-backed biotechs to scale screens from 10,000 to 10 million compounds without capital outlay. Integration of multi-omics data streams with language-model generation further differentiates offerings, enabling holistic insights that cross molecular, cellular, and clinical domains and reinforcing vendor lock-in within the expanding In-Silico Drug Discovery market.

Note: Segment shares of all individual segments available upon report purchase

By Drug-Discovery Phase: Lead Optimization Gains Strategic Attention

Target identification remained the revenue leader in 2025, supported by AI's ability to mine multi-omics repositories and reveal non-obvious therapeutic nodes. Hit identification is poised for 7.34% annual growth, buoyed by generative models that enumerate novel chemotypes quickly. Lead optimization now commands strategic focus because minute tweaks in polarity, solubility, or off-target profiles can pivot an otherwise viable scaffold toward clinical viability, directly influencing In-Silico Drug Discovery market size for this phase.

Quantum-enabled free-energy calculations shrink prediction error margins, allowing researchers to prioritize the best-in-class candidates before synthesis, which conserves valuable chemistry batches. Candidate validation leverages physiologically based pharmacokinetic modelling to forecast interactions across polypharmacy regimens, a critical capability as patient populations age. Platforms that connect docking, ADMET, and synthetic-route design in one workflow shorten development cycles and heighten asset-quality metrics across the In-Silico Drug Discovery market.

By Therapeutic Area: Oncology Retains Prime Focus

Oncology represented 36.61% of the In-Silico Drug Discovery market share in 2025 as the sector’s genomic complexity aligns well with AI-driven multi-omic analytics. Neurology, forecast to expand 8.83% per year, benefits from deep-learning models that simulate neuronal signaling and protein misfolding events implicated in neurodegenerative diseases. Cardiovascular research, increasingly reliant on virtual-twin hemodynamics, has gained momentum as predictive modeling personalizes dosing.

Infectious disease programs demonstrate continued relevance post-COVID-19, leveraging AI for antigenic drift prediction and rapid vaccine target selection. Metabolic disorders such as diabetes receive renewed focus amid the obesity epidemic, where large phenotypic datasets feed machine-learning classifiers for target prioritization. Cross-disciplinary advances thus drive therapeutic diversification inside the growing In-Silico Drug Discovery market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: CROs Propel Outsourced Growth

Pharmaceutical and biotechnology companies controlled 57.71% of 2025 spending, harnessing internal platforms and tailored AI modules. CROs advanced fastest at 8.33% CAGR as sponsors sought flexible capacity and specialized algorithms without hiring scarce talent. Biotechnology start-ups rely heavily on cloud ecosystems, equalizing R&D firepower versus large pharma and broadening participation within the In-Silico Drug Discovery industry.

Academic centers continue foundational research, contributing docking benchmarks and open-source models that raise the innovation baseline but hold modest revenue share due to funding constraints. Strategic tri-party collaborations spanning pharma, CRO, and academia proliferate, pooling compound libraries, virtual screening pipelines, and disease experts to de-risk ambitious programs that target first-in-class modalities.

Note: Segment shares of all individual segments available upon report purchase

By Deployment: Cloud Migration Accelerates

Cloud architectures captured 67.22% of 2025 revenue and are scaling at 7.81% annually as elastic compute, version-controlled environments, and global collaboration trump traditional on-premise servers. The COVID-19 pandemic normalised distributed project teams, further validating remote workflows. Hybrid models persist among large pharma for sovereignty reasons, yet gradually cede ground to multi-tenant life-sciences-specific clouds that satisfy GDPR, HIPAA, and GxP mandates.

Security advances, including confidential computing and private-AI enclaves, mitigate data-exfiltration fears. Integrated marketplaces for compound libraries, property-prediction APIs, and synthetic-route planners enable end-to-end virtual drug discovery in a single subscription, amplifying customer lifetime value for leading vendors across the expanding In-Silico Drug Discovery market.

Geography Analysis

North America retained 37.61% share in 2025, underpinned by robust venture funding, progressive FDA guidance enabling AI-supported submissions, and deep quantum-computing expertise concentrated in technology corridors. A series of high-value partnerships, including Schrödinger’s USD 2.3 billion agreement with Novartis, signals investor confidence in the region’s algorithmic leadership.

Europe maintains significant scale owing to strong public-sector research and harmonized regulatory frameworks that prioritize animal-free testing alternatives. The European Medicines Agency’s ongoing guidance on model-informed drug development elevates acceptance of in-silico dossiers across major EU markets, supporting steady adoption and driving regional In-Silico Drug Discovery market growth.

Asia-Pacific is the fastest-growing geography at an 8.86% CAGR, propelled by China’s multi-fold increase in clinical trials and Japan’s national initiatives championing generative AI in life sciences. Government backing of public-private partnerships and cloud-first policies lower entry barriers, inviting new regional bio-innovators to participate in the In-Silico Drug Discovery market. Elsewhere, Latin America and the Middle East & Africa develop gradually, leveraging cloud platforms to overcome HPC infrastructure deficits and forging capacity-building alliances.

Competitive Landscape

Market Concentration

Competition is moderate, with established computational chemistry pioneers contending with AI-native entrants whose data architectures are cloud-born. Schrödinger combines 30-plus years of physics-based methods with machine-learning acceleration, attracting blockbuster partnerships and expanding predictive toxicology initiatives backed by philanthropic funding. The USD 688 million Recursion-Exscientia merger exemplifies horizontal integration aimed at uniting automated synthesis, image-based phenomics, and generative design within one stack.

Technology giants intensify rivalry: NVIDIA supplies GPU-accelerated molecular-dynamics frameworks and partners with Novo Nordisk on bespoke AI supercomputers for cardiometabolic pipelines. Google’s Isomorphic Labs secured USD 600 million funding to transform DeepMind’s modeling breakthroughs into commercial drug-discovery contracts. Quantum-computing vendors, including IonQ, pilot drug-binding simulations with AstraZeneca, laying groundwork for differentiated value propositions once hardware scales. Overall, platform interoperability, data-quality governance, and automated wet-lab integration will dictate long-term market standing across the In-Silico Drug Discovery market.

In-Silico Drug Discovery Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Isomorphic Labs announced a USD 600 million external funding round to accelerate AI-enabled discovery across multiple therapeutic areas.

- January 2025: The FDA issued draft guidance on AI use in drug development, establishing risk-based frameworks for model credibility.

- January 2025: United States Food and Drug Administration in collaboration with Dassault Systèmes introduced The in-silico clinical trials playbook. The playbook highlights the program's use of virtual human modeling and generative AI to develop in-silico clinical trials for both medical devices and pharmaceuticals.

Table of Contents for In-Silico Drug Discovery Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Escalating AI adoption in hit identification

- 4.2.2Cloud-native HPC lowering entry barriers

- 4.2.3Rising R&D costs pressuring ROI

- 4.2.4Pharma shift to fail-fast virtual screens

- 4.2.5Regulatory sandboxes for in-silico trials

- 4.2.6Digital-twin pipelines for precision meds

- 4.3Market Restraints

- 4.3.1Model bias from legacy datasets

- 4.3.2Shortage of computational chemists

- 4.3.3IP ambiguity for AI-generated molecules

- 4.3.4Quantum-hardware cost constraints

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Buyers

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, 2024-2030)

- 5.1By Component

- 5.1.1Software

- 5.1.2Services

- 5.2By Drug-Discovery Phase

- 5.2.1Target Identification & Validation

- 5.2.2Hit Identification

- 5.2.3Lead Optimization

- 5.2.4Candidate Validation

- 5.3By Therapeutic Area

- 5.3.1Oncology

- 5.3.2Neurology

- 5.3.3Cardiovascular

- 5.3.4Infectious Diseases

- 5.3.5Metabolic Disorders

- 5.4By End User

- 5.4.1Pharmaceutical Companies

- 5.4.2Biotechnology Firms

- 5.4.3Academic & Research Institutes

- 5.4.4CROs

- 5.5By Deployment

- 5.5.1On-premise

- 5.5.2Cloud-based

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2India

- 5.6.3.3Japan

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4South America

- 5.6.4.1Brazil

- 5.6.4.2Argentina

- 5.6.4.3Rest of South America

- 5.6.5Middle East and Africa

- 5.6.5.1GCC

- 5.6.5.2South Africa

- 5.6.5.3Rest of Middle East & Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Schrödinger Inc.

- 6.3.2Dassault Systèmes (SE) – BIOVIA

- 6.3.3Certara

- 6.3.4Charles River Laboratories

- 6.3.5Chemical Computing Group (CCG)

- 6.3.6Cresset

- 6.3.7Simulations Plus

- 6.3.8Genedata

- 6.3.9PerkinElmer (Revvity)

- 6.3.10Evotec

- 6.3.11Atomwise

- 6.3.12Insilico Medicine

- 6.3.13Exscientia

- 6.3.14BenevolentAI

- 6.3.15Aria Pharmaceuticals

- 6.3.16DeepCure

- 6.3.17BioAge Labs

- 6.3.18Nimbus Therapeutics

- 6.3.19Numerate

- 6.3.20Cloud Pharmaceuticals

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global In-Silico Drug Discovery Market Report Scope

As per the scope of the report, in-silico drug discovery refers to the use of computer-based techniques and simulations to identify, design, and evaluate potential drug candidates.

The in-silico drug discovery market is segmented by product, therapeutic area, and end user. In terms of products, the market is segmented as software and services. In terms of therapeutic areas, the market is segmented as oncology, infectious disease, cardiology, neurology, diabetes, and other therapeutic areas. By end user, the market is segmented as pharmaceutical and biotechnology companies, contract research, organizations, academic institutes and research centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD) for the above segments.