Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

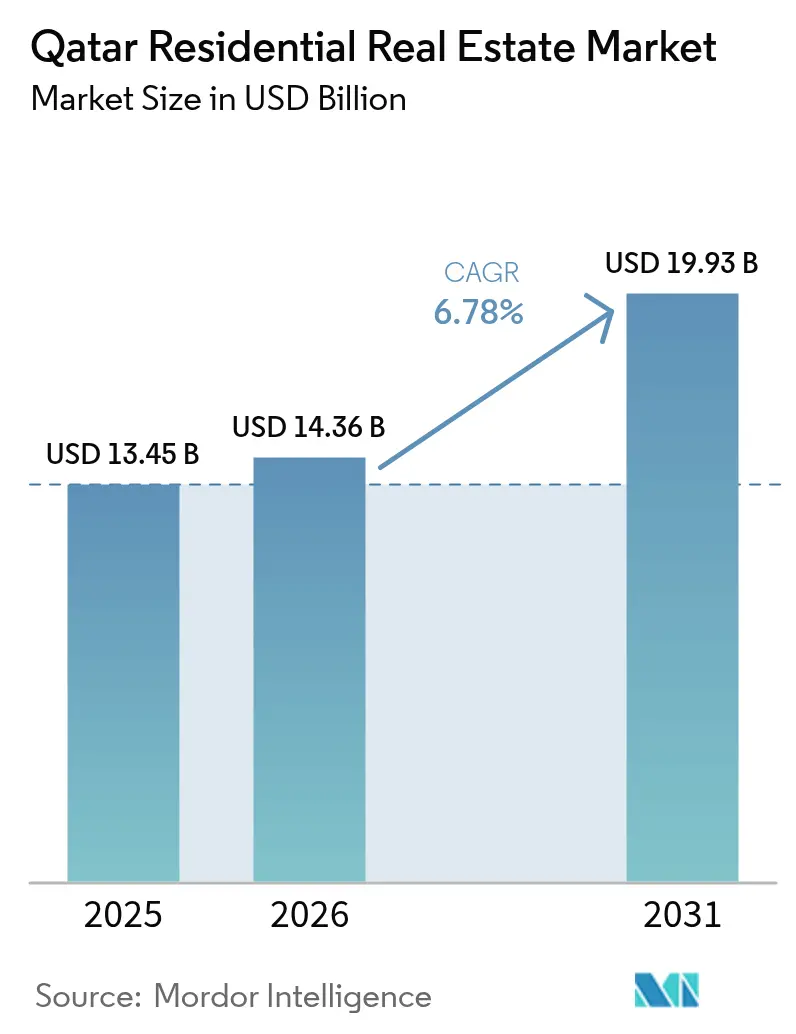

| Base Year Market Size (2025) | USD 13.45 Billion |

| Market Size (2026) | USD 14.36 Billion |

| Market Size (2031) | USD 19.93 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

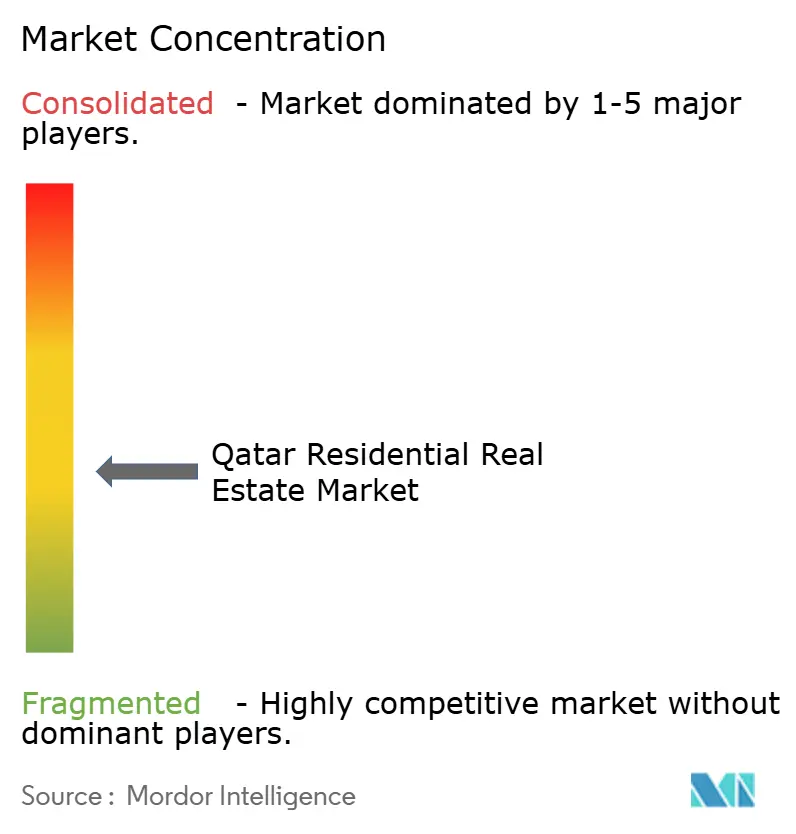

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Residential Real Estate Market Analysis by Mordor Intelligence

Qatar residential real estate market size in 2026 is estimated at USD 14.36 billion, growing from 2025 value of USD 13.45 billion with 2031 projections showing USD 19.93 billion, growing at 6.78% CAGR over 2026-2031. Demand is anchored by post-World Cup infrastructure, liberalized foreign-ownership rules and a permanent-residency‐for-investment program that links property purchases above QAR 730,000 to long-term visas[1]Nasser Al-Khater, “QAR 730,000 Residency Threshold Guidelines,” Real Estate Regulatory Authority, aqarat.gov.qa. Rising tourism, government-backed mortgages for nationals and the forthcoming 2030 Asian Games further reinforce owner-occupier and rental demand. At the same time, oversupply in mid-tier apartments and higher building-material costs continue to pressure yields and margins. Developers therefore pivot toward premium villas, mixed-use megaprojects and technology-driven sales channels to sustain growth in the Qatar residential real estate market.

Key Report Takeaways

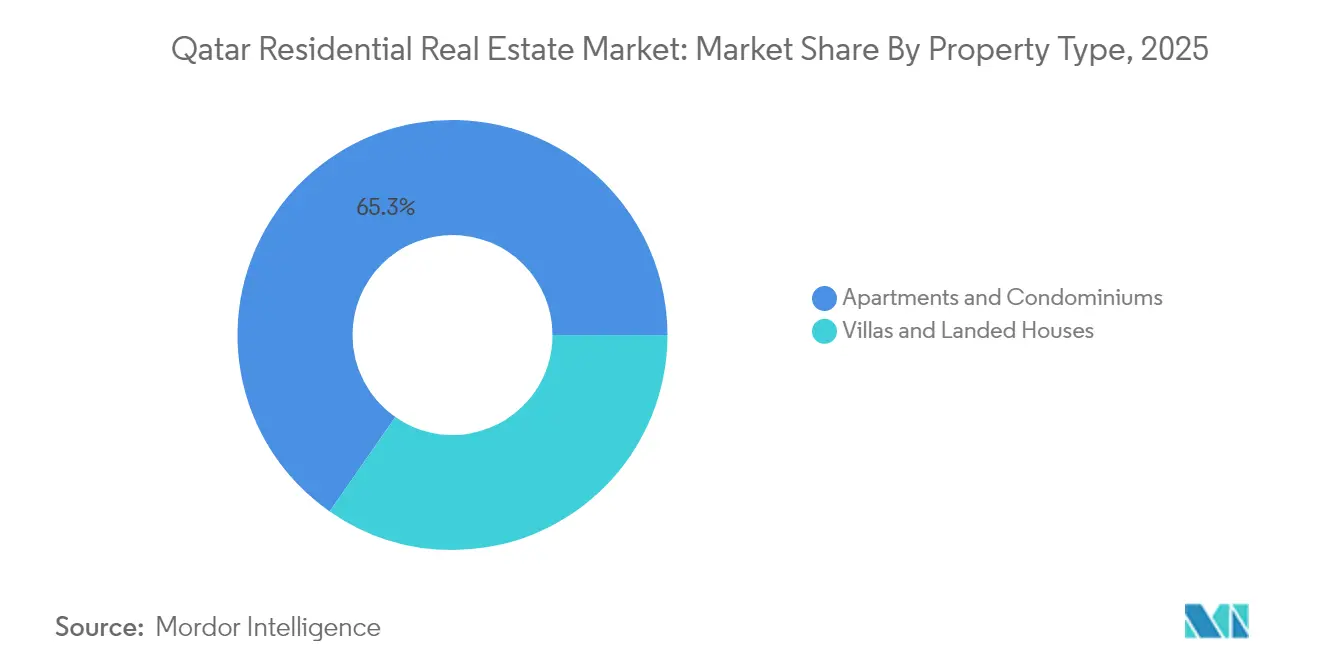

• By property type, apartments held 66% of the Qatar residential real estate market share in 2024, whereas villas and landed houses are forecast to grow at a 7.36% CAGR through 2030.

• By price band, the mid-market segment commanded 51% of the Qatar residential real estate market size in 2024; the luxury segment is advancing at a 7.45% CAGR to 2030.

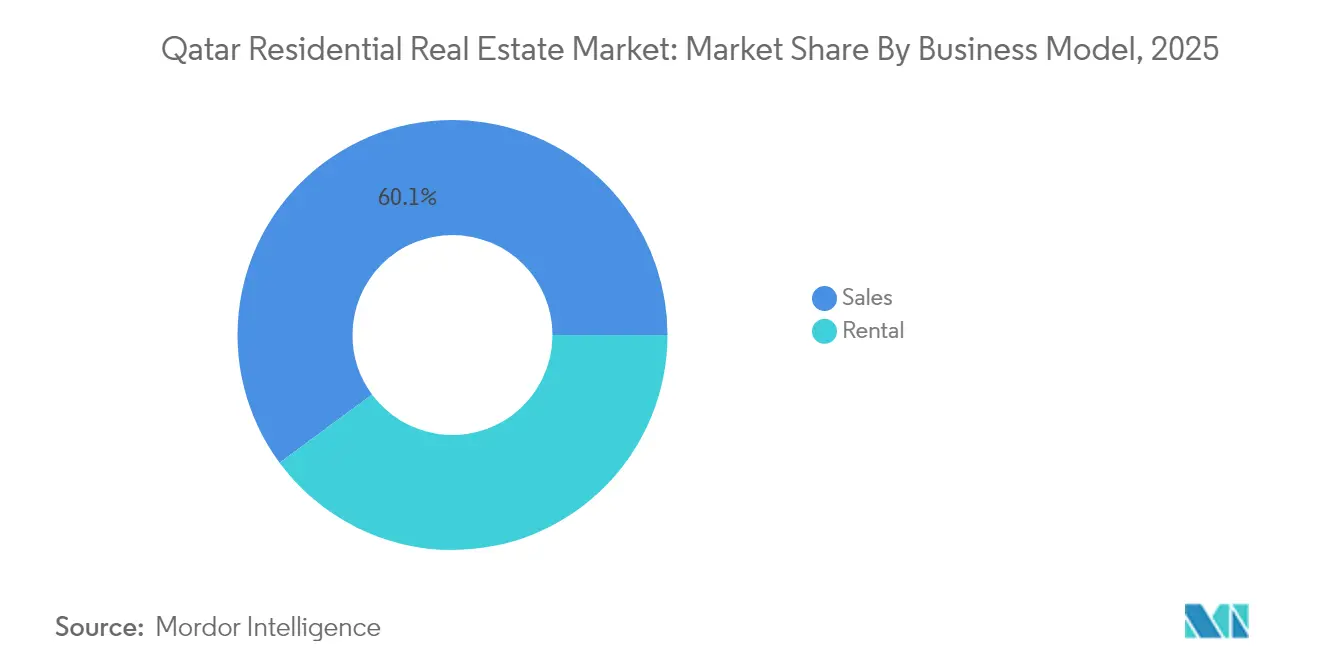

• By business model, primary (new-build) sales captured 59% revenue of the Qatar residential real estate in 2024, while rentals record the fastest projected CAGR at 8.08% through 2030.

• By mode of sale, sales transactions accounted for 61% of the Qatar residential real estate in 2024; the rental mode is rising at an 8.08% CAGR on the same horizon.

• By municipality, Doha controlled 70% market share of the Qatar residential real estate in 2024; Al Daayen and Lusail are set to expand at an 8.22% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign Ownership Law (Law 16 of 2018) Broadening Expat Titles | +1.8% | Freehold zones: West Bay, The Pearl, Lusail, Al Khor Resort | Long term (≥ 4 years) |

| Expansion of Lusail & Pearl Freehold Zones Attracting Foreign Buyers | +1.5% | Lusail City, The Pearl-Qatar, West Bay freehold areas | Long term (≥ 4 years) |

| FIFA World Cup 2022 Legacy Infrastructure Catalyzing Residential Demand | +1.2% | National, with concentrated benefits in Doha, Lusail, Al Rayyan | Medium term (2-4 years) |

| Upcoming 2030 Asian Games & Tourism Vision Elevating Rental Demand | +1.1% | Doha core, spillover to Al Rayyan, emerging in Lusail | Medium term (2-4 years) |

| Government-backed Mortgage Scheme for Nationals Boosting Home Purchases | +0.9% | National, with higher uptake in Doha metropolitan area | Short term (≤ 2 years) |

| Rapid Growth in PropTech Platforms Improving Market Transparency | +0.7% | National, with higher adoption in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Foreign Ownership Law (Law 16 of 2018) broadening expat titles

The statute opened 10 freehold and 16 usufruct zones to non-Qataris, effectively converting the sector into a global investment destination. Residency is granted automatically to buyers exceeding QAR 730,000, stimulating cross-border demand. Partnerships such as Al Rayan Bank’s UK campaign offer Sharia-compliant finance up to 60% of purchase value, lowering entry barriers for foreign investors. Transaction volumes reached QAR 8.16 billion in 1H 2024, up markedly from the prior year. The Office for Non-Qatari Real Estate Ownership centralizes approvals, shortening deal cycles and adding transparency. These measures heighten liquidity and broaden the buyer pool for the Qatar residential real estate market over the long term.

FIFA World Cup 2022 legacy infrastructure catalyzing residential demand

Mass-transit lines, airport expansion and expressways funded for the World Cup have improved access to once-peripheral zones, encouraging developers to release new inventory in Lusail, Al Rayyan and along the Doha Metro corridor. The tournament attracted 1 million visitors and boosted GDP 1% in tourism receipts, validating the long-term capacity of this infrastructure to handle population surges. Demand is now migrating toward transit-oriented projects such as Lusail Towers, where 1.1 million m² of mixed-use floor space is under development. Hotel-to-residence conversions around Hamad International Airport further bridge hospitality and housing. Collectively, these linkages underpin steady absorption in the Qatar residential real estate market during the medium term.

Upcoming 2030 Asian Games & tourism vision elevating rental demand

Qatar targets 6 million annual visitors by 2030, intending to double tourism’s GDP contribution to 12%. Preparations for the Asian Games mirror the World Cup’s infrastructure blueprint, triggering additional hotel-residence hybrids and extended-stay units. Expatriates—already 60% of residents—anchor the rental base, and population growth of 3.1% in July 2024 underscores momentum. Institutional landlords are bundling leases with concierge services to appeal to high-spending, event-led tenants. As a result, rental yields in premium sub-markets are widening, offsetting compression in oversupplied mid-tier apartments and strengthening the Qatar residential real estate market.

Government-backed mortgage scheme for nationals boosting home purchases

Real-estate loans represented 21% of total private-sector credit in July 2024, growing 6.3% year-over-year[2]Yaqoub Al-Baker, “Real Estate Lending Trends July 2024,” Qatar Central Bank, qcb.gov.qa. Budgetary allocations of QAR 3.3 billion fund subsidized mortgages, while the new Real Estate Regulatory Authority (Aqarat) provides standard contracts and dispute-resolution channels. Although construction material cost inflation reached 15-20% since 2024, mortgage support cushions affordability for nationals, stabilizing the Qatar residential real estate market. Enhanced disclosure rules also lift buyer confidence, pushing forward the short-term sales cycle, especially for first-time homeowners.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oversupply in Mid-tier Apartment Segment Depressing Rental Yields | -1.4% | Doha core, Al Rayyan, emerging oversupply in Lusail | Short term (≤ 2 years) |

| Rising Construction-Input Costs Squeezing Developer Margins | -1.1% | National, with acute impact in Doha and major developments | Short term (≤ 2 years) |

| Volatility in Hydrocarbon Revenues Influencing Employment & Housing Demand | -0.8% | National, with higher sensitivity in industrial zones | Medium term (2-4 years) |

| Restrictive Expat Residency Tenure Limiting Long-term Ownership Appetite | -0.6% | Freehold zones, particularly affecting non-GCC expatriates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oversupply in mid-tier apartment segment depressing rental yields

Residential stock stood at 394,000 units by Q2 2024 with another 9,200 units scheduled for delivery the same year. Median apartment rents slid 6% year-over-year to QAR 6,000, while concessions such as one-month-free leases became common. The mismatch is greatest in the mid-market, which forms 51% of inventory but faces thinning demand as occupants either trade up to luxury or downsize for cost savings. The Real Estate Regulatory Authority counters by launching an open-data platform to aid market clearing, yet near-term oversupply will continue to pressure returns in the Qatar residential real estate market.

Volatility in hydrocarbon revenues influencing employment and housing demand

Hydrocarbon receipts declined 18% in 2024, narrowing the fiscal surplus and tempering public hiring. Bank exposure to post-World-Cup real-estate loans led to tighter credit standards. Although non-hydrocarbon GDP expanded 3.7% in 2024, expatriate employment remains sensitive to oil-price swings. The government’s multiyear LNG expansion and NDS3 diversification initiatives partially buffer volatility[3]Saad Al-Kaabi, “North Field LNG Expansion Update 2024,” QatarEnergy, qatarenergy.qa. Nonetheless, cyclical layoffs in energy and related services can dent absorption, posing a medium-term drag on the Qatar residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: apartments dominate, villas accelerate

Apartments and condominiums dominated with 65.32% share of the Qatar residential real estate market in 2025, largely reflecting urban density and expatriate leasing preferences. Villas, however, post the fastest 7.05% CAGR to 2031 on demand from nationals and high-net-worth expatriates seeking larger plots. Projects such as Al Dana Garden II deliver 142 villas worth QAR 119 million, signaling robust premium appetite. Hybrid waterfront schemes like The Grove combine apartment convenience with villa-style amenities, blurring category lines and reinforcing upscale supply. Consequently, developers rebalance portfolios toward low-density formats to absorb purchasing-power migration within the Qatar residential real estate market.

Villa momentum also benefits from the residency-by-investment option because typical ticket sizes exceed the QAR 730,000 threshold. Mortgage programs reserve favorable terms for single-family housing, amplifying take-up. Meanwhile, apartment landlords refresh mid-tier stock via refurbishments to defend occupancy. Over time, a two-speed pattern emerges: compact city-core units for transient renters and suburban villas for ownership seekers, jointly sustaining depth and liquidity in the Qatar residential real estate market.

By Price Band: Mid-market steadies while luxury leads growth

The mid-range properties retained 50.42% of the 2025 volume, yet oversupply eroded rents and moderated pricing power. Construction-cost inflation passes through more acutely to affordable brackets, tightening developer margins. Contrastingly, the luxury band records a 7.12% CAGR to 2031, lifted by trophy projects such as the Trump International Golf Club villas and Lusail waterfront penthouses. Wealth inflow from foreign buyers seeking long-term visas underpins resilience. This bifurcation means premium units increasingly anchor headline value in the Qatar residential real estate market size, whereas mid-market stock delivers liquidity but lower returns.

Government housing allowances and supply-chain subsidies steady affordable demand but cannot fully offset rising steel and cement costs. Developers therefore bundle energy-efficient fittings and rent-to-own offers to widen mid-segment appeal. Yet, capital appreciation stays strongest at the top end where scarcity and lifestyle amenities differentiate. These dynamics collectively guide pricing strategy across the Qatar residential real estate industry.

By Business Model: Primary sales prevail, rentals outpace growth

Primary (new-build) deals captured 60.12% of 2025 transactions as megaproject pipelines remained active after the World Cup. Some USD 85 billion in public-private construction is scheduled to 2030, fueling continuous handovers. Conversely, the rental channel posts the quickest 7.74% CAGR, mirroring the expatriate majority and tourism-led occupancy surges. Extended-stay formats and branded residences widen the product mix, boosting rental yields in premium districts despite general oversupply.

Secondary-market liquidity increases following Law No. 5 of 2024 on digital title registration, shortening transfer times to less than a week. Blockchain tokenization under the Qatar Financial Centre framework also seeds fractional ownership schemes. These innovations elevate transparency and investor participation, fostering a more balanced ecosystem for the Qatar residential real estate market.

By Mode of Sale: Sales hold volume led, rentals show velocity

Sales accounted for 60.12% of 2025 market activity, supported by foreign-ownership reforms that generated QAR 8.16 billion in 1H 2024 trading. Rental demand, however, expands faster at an 7.74% CAGR as population growth and mega-event staff inflows lift occupancy. Corporate leasing packages inclusive of schooling and health insurance gain traction, especially for project-based expatriates.

Meanwhile, sale prices in oversupplied segments remain flat, nudging investors toward buy-to-let strategies. Institutional landlords leverage scale to negotiate maintenance contracts, protecting margins. Dual-income households among young Qataris also favor lease-to-own models, smoothing the transition from renting to owning within the Qatar residential real estate market.

By Key Municipalities: Doha’s scale vs Lusail’s surge

Doha maintained a dominant 69.35% share in 2025 driven by government hubs and cultural landmarks. Yet land scarcity and apartment oversupply constrain upside. Regeneration schemes like Msheireb Downtown inject smart-city amenities and raise asset quality. Meanwhile, Al Daayen and Lusail clock an 7.9% CAGR on the back of master-planned districts paired with state-of-the-art transit links. Lusail Towers alone spans 1.1 million m², signaling its role as a new CBD.

Al Rayyan benefits from affordable plots and proximity to Education City, drawing young families. Coastal Al Khor leverages freehold eligibility to court foreign buyers seeking second homes. Together, satellite municipalities ease congestion, diversify supply and extend investment optionality across the Qatar residential real estate market.

Geography Analysis

Doha’s 69.35% slice of the Qatar residential real estate market anchors national performance. Its metro network, airport hub and cultural districts sustain demand, yet 394,000 existing units plus 9,200 incoming deliveries weigh on occupancy. Lower median rents, incentives like one-month-free leases and retrofits of older blocks characterize the near-term landscape. Nonetheless, flagship redevelopments at Msheireb Downtown Doha elevate the city’s premium stock and long-term appeal.

Al Daayen and Lusail represent the fastest-rising municipalities, each projecting 7.9% CAGR through 2031. Expansive land banks support low-density villa clusters, while the Doha Metro Red Line and Lusail LRT connect residents to the capital in under 30 minutes. Cultural anchors such as the Herzog & de Meuron-designed Lusail Museum augment lifestyle vibrancy. These dynamics are pulling both domestic upgraders and foreign capital toward the northern growth corridor, diversifying the Qatar residential real estate market.

Secondary nodes including Al Rayyan, Al Khor and coastal Simaisma add breadth. Al Rayyan captures spill-over demand from Doha at lower entry prices and larger lot sizes. Al Khor’s freehold designation and proximity to Ras Laffan industrial hub draw expatriates seeking longer leases. Simaisma’s Trump International Golf Club positions the coastline as a luxury enclave, extending premium supply beyond The Pearl. Together, these geographies underscore a multipolar future for the Qatar residential real estate market.

Regulatory Landscape

Qatar’s residential real estate regulation is being consolidated under the General Authority for Real Estate Regulation (Aqarat), which is strengthening a single-window model for licensing and oversight. In February 2026, the Cabinet approved transferring the Real Estate Brokerage Department from the Ministry of Justice to Aqarat, centralizing brokerage supervision alongside the authority’s wider mandate for market governance.

The framework also advanced investor protection and foreign participation. In January 2026, the Ministry of Justice issued a decision regulating off-plan sales procedures through a Preliminary Real Estate Registry with electronic registration, supporting transparency around pre-completion unit sales. In June 2026, Cabinet Resolution No. 21 of 2026 updated the designated non-Qatari ownership and usufruct areas and added the Simaisma Resort and Beach Project, aligning tourism-led master plans with property ownership eligibility. Parallel municipal updates, including Ministerial Decision No. 108 of 2026 on villa and mansion design standards, directly affect residential permitting and product design for landed housing.

Value Chain Analysis

Qatar’s residential real estate value chain starts with land allocation and master planning, then moves through development, construction, marketing and brokerage, financing, handover, and ongoing property and community management. Developers and contractors execute the delivery pipeline, while broker networks drive transactions in both freehold and usufruct zones. Financing links subsidized mortgages for nationals and Sharia-compliant products for eligible buyers, and settlement, valuation advisory, and conveyancing are increasingly tied to digital registration workflows under reforms connected to Law No. 5 of 2024 and its 2025 executive regulations.

Regulatory digitization is reshaping process friction points across the chain, particularly for off-plan launches and secondary transfers. Aqarat’s market reforms and the shift toward electronic registration strengthen documentation, shorten transaction cycles, and improve data-driven price discovery, which becomes more relevant under mid-tier apartment oversupply. On the delivery side, updated residential villa and mansion specifications issued by the Ministry of Municipality in 2026 affect design decisions, bill of quantities, and permitting, while escrow-style mechanisms and compliance requirements for registered developers formalize buyer protection and reduce counterparty risk in pre-handover sales.

Competitive Landscape

The sector features moderate concentration: the top five developers deliver roughly 45% of annual completions, while hundreds of local firms manage smaller plots. Ezdan Holding Group continues to scale rental communities, leveraging its 30,000-unit portfolio for economies of scale. Barwa Real Estate advances mixed-use schemes such as Madinatna, integrating smart-home technologies to lift tenant retention. United Development Company redirected USD 216.6 million from its Qatar Cool stake sale into The Pearl and Gewan Islands, signalling a focus on high-margin waterfront assets.

New entrants collaborate with global brands to differentiate. Qatari Diar and Dar Global’s Simaisma project imports the Trump hospitality label, attracting international buyers. Technology is another battleground: the Qatar Financial Centre’s Digital Asset Framework enables tokenized property stakes, and early adopters like Aspire Zone explore blockchain leasing smart contracts[5]Hessa Al-Mannai, “Law No. 5 of 2024 on Digital Property Registration,” Ministry of Justice, gov.qa. Sustainability also shapes competition, with LEED-certified builds gaining mortgage rate discounts from banks pivoting toward green portfolios.

Financing hurdles persist as lenders recalibrate exposure after post-World-Cup loan losses. Developers with robust balance sheets tap sukuk markets, while smaller players seek joint ventures to share risk. Opportunities remain in senior-living, co-living and energy-efficient retrofits—segments currently under-supplied in the Qatar residential real estate market.

Qatar Residential Real Estate Industry Leaders

Al Mana Real Estate

United Development Company

Qatari Diar Real Estate Company

Ezdan Holding Group

Barwa Real Estate

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product rebalancing toward landed housing and larger-format units is supported by policy changes that expand design flexibility. Ministerial Decision No. 108 of 2026 updated villa and mansion standards (including higher permitted villa height and allowance for mezzanine floors), giving developers room to increase usable area within existing plots and better match demand that has been shifting away from oversupplied mid-tier apartments. The June 2026 update to non-Qatari ownership areas, adding the Simaisma Resort and Beach Project as a designated area, also creates a channel for foreign-buyer demand linked to integrated resort and lifestyle positioning.

A second opportunity set is in transaction efficiency and construction delivery enabled by government-backed digital tools. The Ministry of Municipality’s AI-powered building permit system (launched October 2025) compresses permitting timelines by integrating GIS and utility databases, supporting faster project mobilization and reducing pre-construction uncertainty. On execution, Ashghal’s BIM and GIS work around a National Digital Twin, showcased in June 2026, points to deeper standardization of digital planning and asset management, while high-profile automation examples (such as UCC Holding’s 3D-printed school work for Ashghal) indicate near-term momentum for industrialized methods that can help developers and contractors manage labor and schedule constraints under elevated input-cost conditions.

Recent Industry Developments

- June 2026: United Development Company confirmed progress on the Perlita Gardens redevelopment at The Pearl Island after completing initial demolition and enabling works. The update signaled continued capital deployment into repositioning mature waterfront assets to refresh the residential offering and protect pricing in premium sub-markets.

- November 2025: United Development Companys Extraordinary General Assembly approved the purchase of the Perlita Villas project for QR 625 million and amended the companys articles to expand real estate activities. The move strengthened UDCs control over a key residential asset base at The Pearl and created a clearer platform for redevelopment-led value creation.

- December 2024: Qatar introduced Law No. 5 of 2024 enabling digital title registration, supporting faster transfers and more transparent recordkeeping in residential transactions. This reform reduced administrative friction in the secondary market and underpinned broader adoption of electronic workflows across brokers, banks, and registries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the total value of residential homes in Qatar that are bought or leased for long-term living, measured in USD, and covering the full country.

Scope exclusions: This sizing does not include worker camps, student dormitories, timeshare units, or serviced apartments that are treated as hospitality.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing-home Resale)

- By Key Municipalities

- Doha

- Al Rayyan

- Al Khor

- Rest of Qatar

Data Sources, Market Sizing, and Validation

Desk Research

We started by building a clear fact base around Qatar housing demand, supply, and pricing, so later model inputs could be anchored in public data. Common sources used include national statistics and planning releases, central bank and banking sector publications (including mortgage and credit trends), municipal and land registration disclosures where available, and energy or macro dashboards from international institutions such as the IMF or World Bank.

To cross-check the direction of the market, we also reviewed sources such as developer and broker publications, listed-company filings and investor presentations, and press coverage of project launches and handovers. We also tracked policy updates related to residency and ownership rules. In a few places, subscription tools for company financials and business intelligence were used to sanity-check revenue exposure and project pipelines, and then assumptions were kept conservative unless confirmed elsewhere. These desk research sources are illustrative only, and we used other public references to collect data, validate figures, and clarify open questions.

Primary Interviews and Surveys

We then tested the desk findings through expert interviews and structured surveys with people active in Qatar residential sales and rental markets, including developers, brokers, property managers, lenders, and advisers. Input was gathered across the main municipalities, so pricing behavior, absorption pace, and long-lease rental patterns were not inferred from one micro-market. What we heard was used to fill gaps, correct unrealistic assumptions, and triangulate the final market totals before forecast sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 33% | |

| Smaller Players: 16% | Managers: 55% |

Market-Sizing & Forecasting

The core sizing was built using a top-down and bottom-up blend, where national housing activity was reconstructed from demand and transaction signals and then corroborated using selective roll-ups. On the top-down side, we linked the demand pool to indicators such as population and household formation, residential transaction and mortgage activity, typical price movements by unit type, and rental rate direction for long leases.

Once the high-level value was formed, it was checked using bottom-up approximations like sampled unit counts in active communities, typical ticket sizes for apartments versus villas, and channel checks on the split between primary (new-build) and secondary (resale) sales. Where data was not consistently available by municipality or price band, gaps were handled using proportional splits validated by interviews, followed by sensitivity checks so a single assumption did not move the full market.

For forecasting, scenario analysis was used because the market can move based on policy changes, new supply delivery timing, and credit conditions. Forecast drivers were kept simple and explainable, and then adjusted only after expert consensus confirmed the likely direction for prices, absorption, and long-lease rental yields over the forecast window.

Data Validation & Update Cycle

We validated the outputs through multiple checks so the final number stayed tied to real market signals. Results were compared against independent indicators such as housing loan growth, transaction momentum, and observed movement of rents and sale prices in key areas, and then outliers were reviewed before internal sign-off.

If a variance was large or a key assumption changed, respondents were re-contacted and the model inputs were updated, followed by another review pass. Reports are refreshed annually, with interim updates when material events occur that can shift supply, demand, or pricing. Before delivery, a fresh analyst review is completed so clients receive the latest updated view.

Mordor Intelligence's Qatar Residential Real Estate Market Size Compared With Other Published Estimates

Different published market sizes for Qatar residential real estate can look far apart, even when they cover the same country and broad property types. In practice, the gap usually comes from what value is counted, which year is treated as the base, and how sales values versus rental receipts are combined into one total.

Serviced apartments that are classified as hospitality sit outside Mordor Intelligence's scope, and that single exclusion can shift totals when other estimates fold them into residential value. A second driver is whether models treat the market as only sales transactions or also include long-lease rentals, and then how price levels are converted to USD and updated when the market turns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.36 B (2026) | |

| Industry Research Publisher A | USD 9.04 B (2026) | Often presented as a narrower sales-led value pool, with less explicit treatment of long-lease rental receipts and limited disclosure on municipal weighting and price-band splits. |

| Press-led Estimate B | USD 7.83 B (2024) | Usually anchored to an older base year and headline indicators, with less clarity on whether the figure represents transactions only or the combined sales plus long-lease rental value. |

The spread in the table is mostly explained by what is counted as residential, whether rentals are included alongside sales, and the choice of base year for pricing and currency timing. By keeping the scope tied to long-term habitation units and cross-checking totals against credit, pricing, and absorption signals, the market value stays traceable to a repeatable set of inputs.

Key Questions Answered in the Report

What is the current size of the Qatar residential real estate market?

The market is valued at USD 14.36 billion in 2026 and is expected to reach USD 19.93 billion by 2031 at a 6.78% CAGR.

Which property type is growing fastest in Qatar’s housing sector?

Villas and landed houses lead growth with a 7.05% CAGR through 2031, driven by high-net-worth expatriates and nationals.

How does Law 16 of 2018 affect foreign buyers?

It allows non-Qataris to purchase freehold property in 10 zones and obtain residency for investments above QAR 730,000.

Why are rental yields fluctuating in Doha?

Mid-tier apartment oversupply has pushed median rents down 6% year-over-year, although premium rentals remain resilient.

Page last updated on: